TAXATION: Analysis of Fringe Benefit Tax for Charlie and Shine Homes

VerifiedAdded on 2020/03/23

|9

|1661

|41

Report

AI Summary

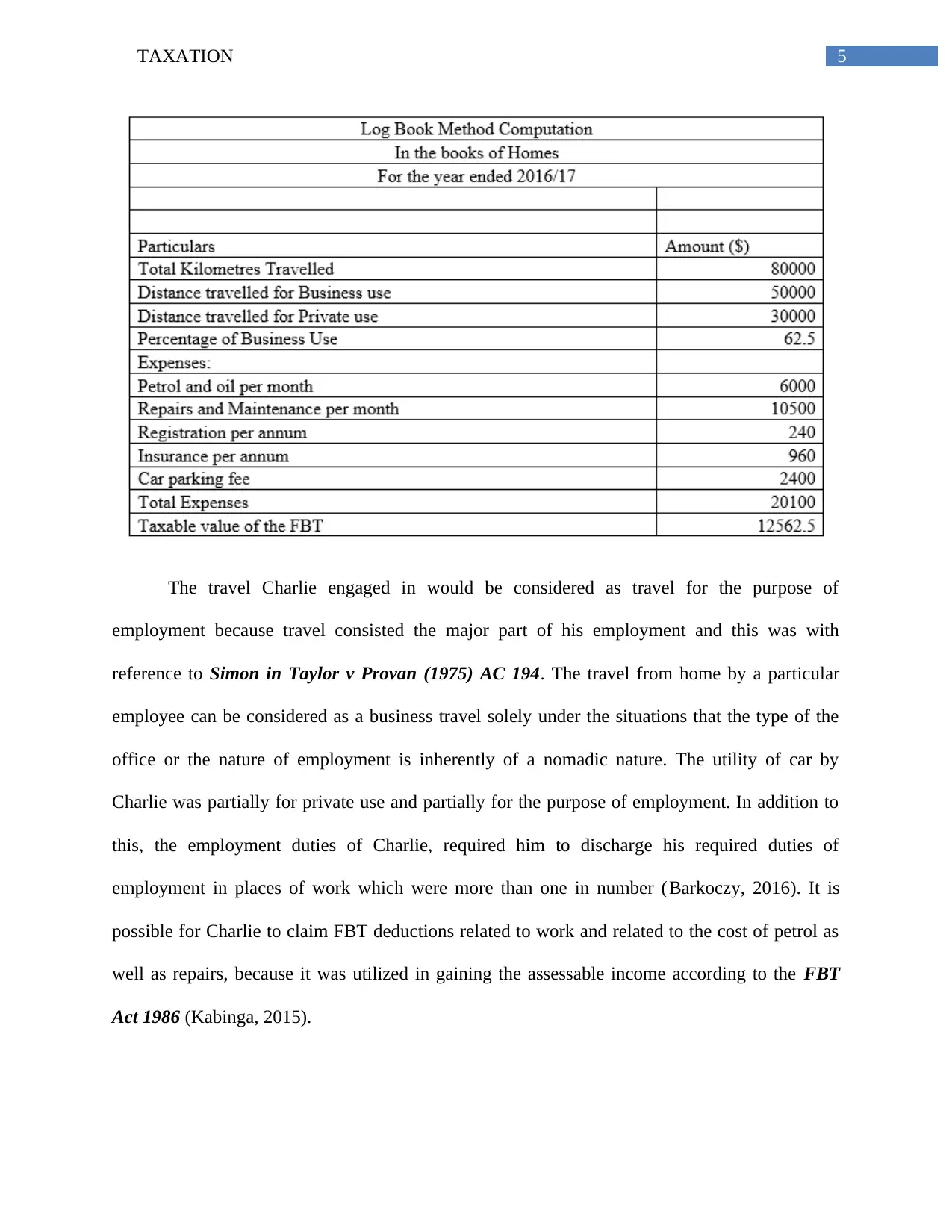

This report analyzes a taxation case study involving Charlie, an agent for Shine Homes Private Limited, and explores the fringe benefit tax (FBT) implications. The core issue revolves around the FBT consequences of a company-provided sedan, along with parking and accommodation benefits. The report references key legislation, including Section 6 of the Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act 1986, and relevant case law such as Lunney and Hayley v FCT and Newsom v Robertson. The analysis determines the business versus private use of the car, car parking benefits, and other benefits like accommodation, determining whether the car usage is considered for business purpose. The report delves into allowable deductions under the Income Tax Assessment Act 1997, and concludes that the fringe benefit expenditures are considered for tax purposes under the FBT Act 1986. It also addresses the deductibility of various expenses for both Charlie and Shine Homes, highlighting the tax liabilities and deductions available.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.