7SSMM100: Research Methods Assignment on FDI and Exports

VerifiedAdded on 2023/03/21

|14

|2496

|31

Report

AI Summary

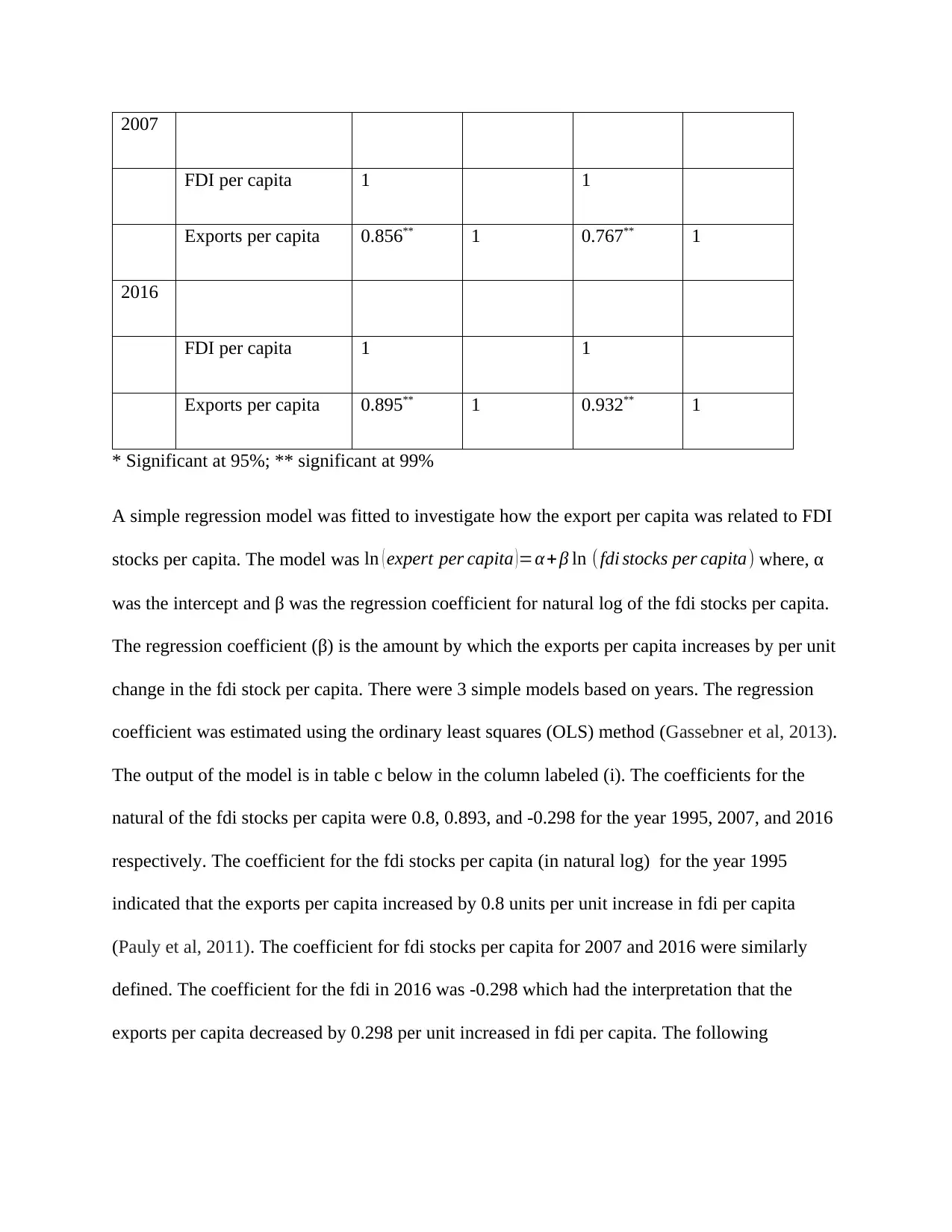

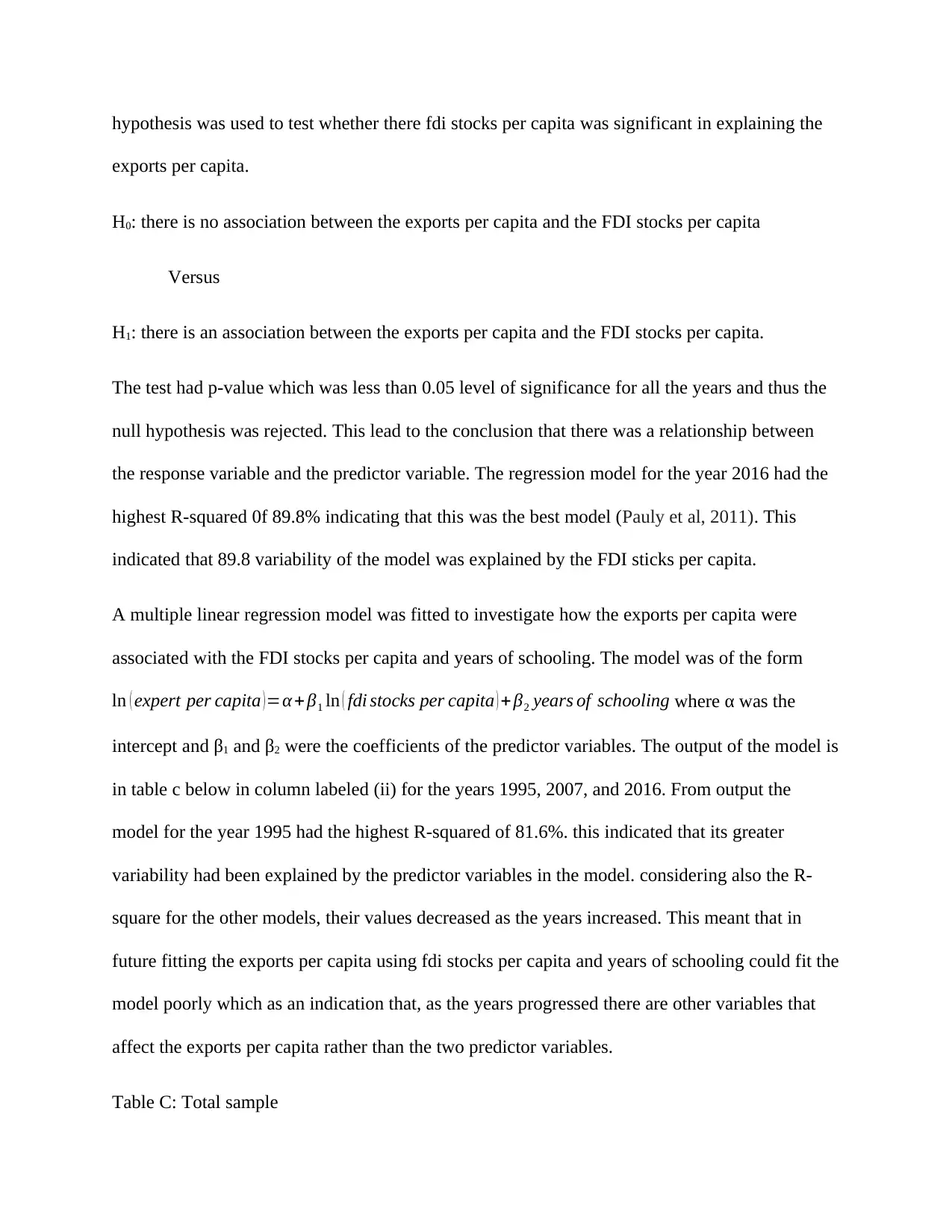

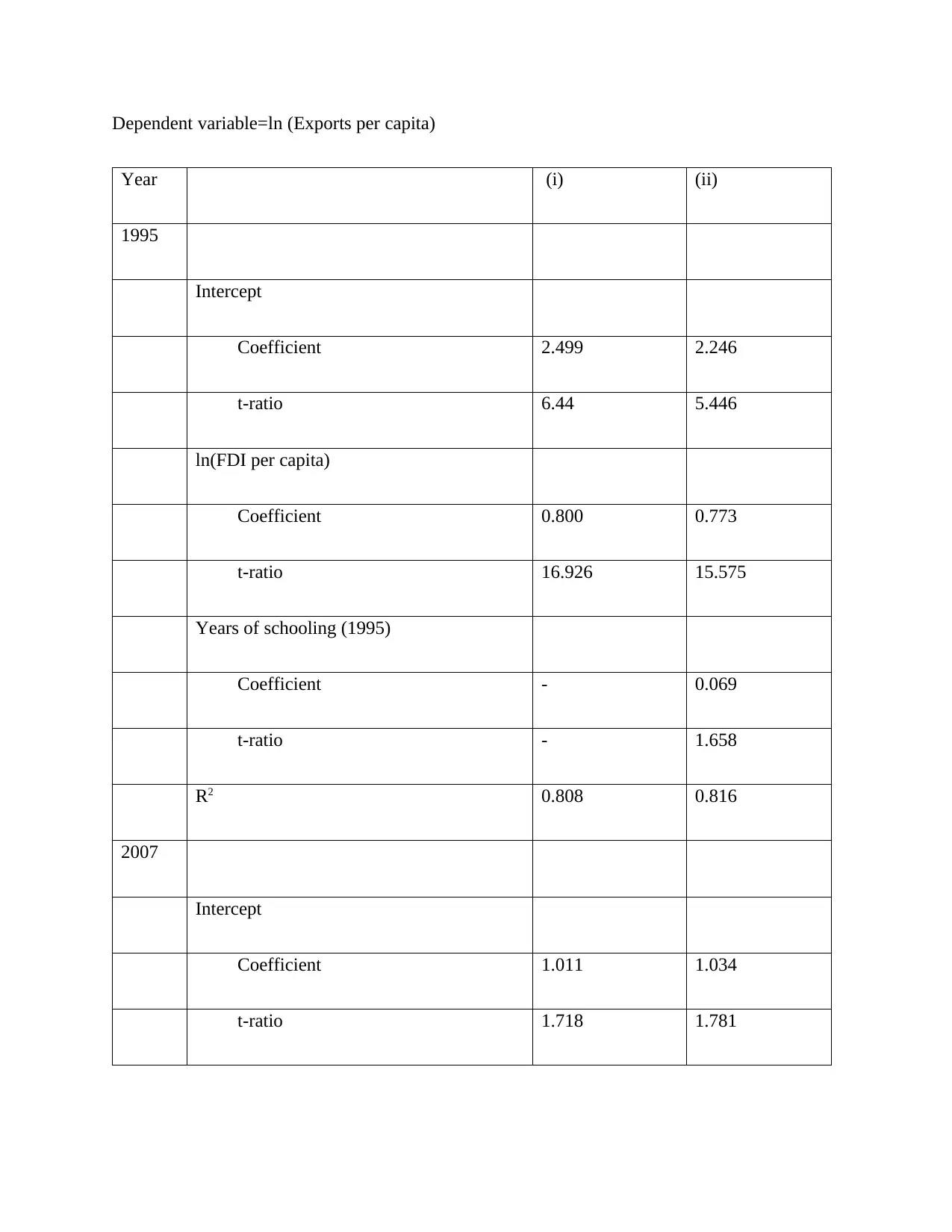

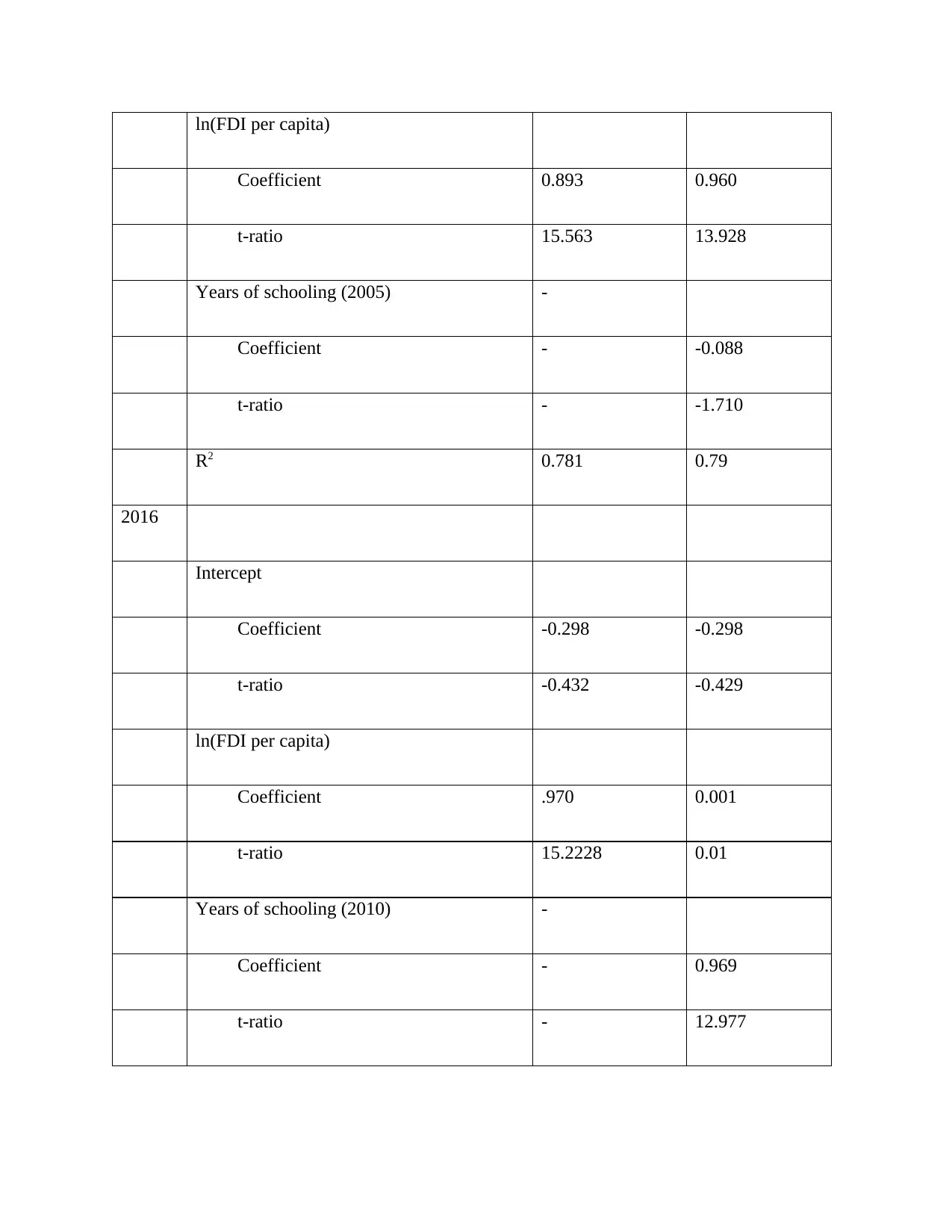

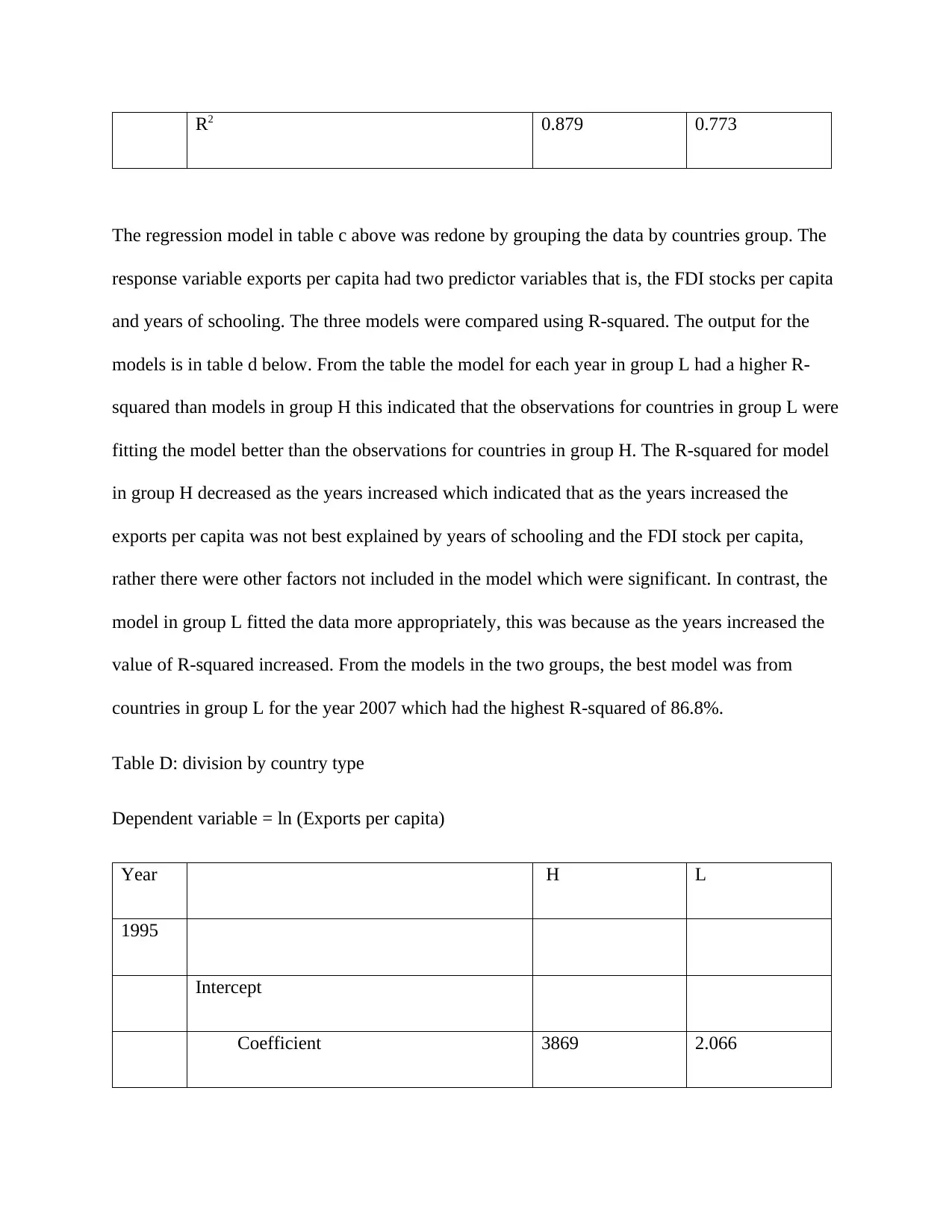

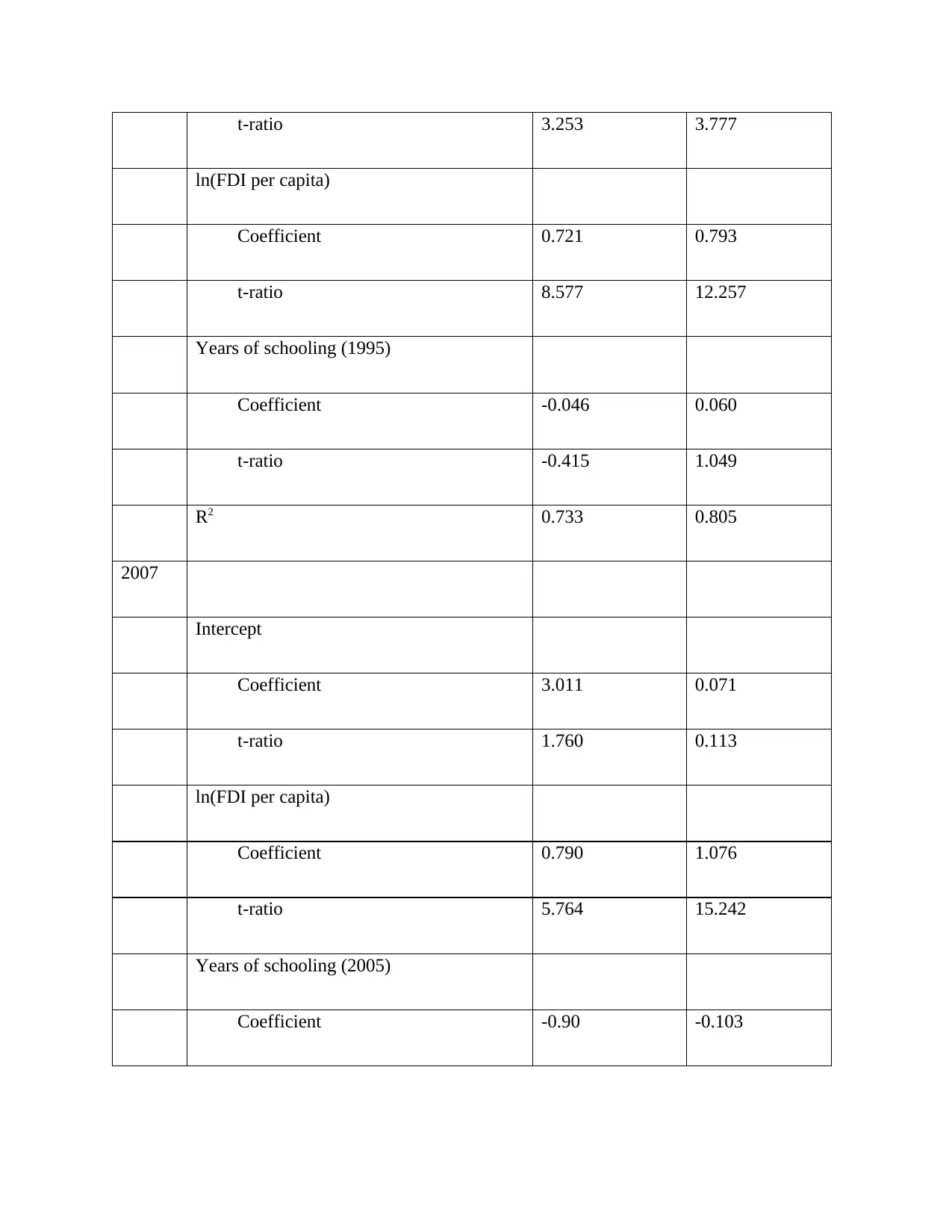

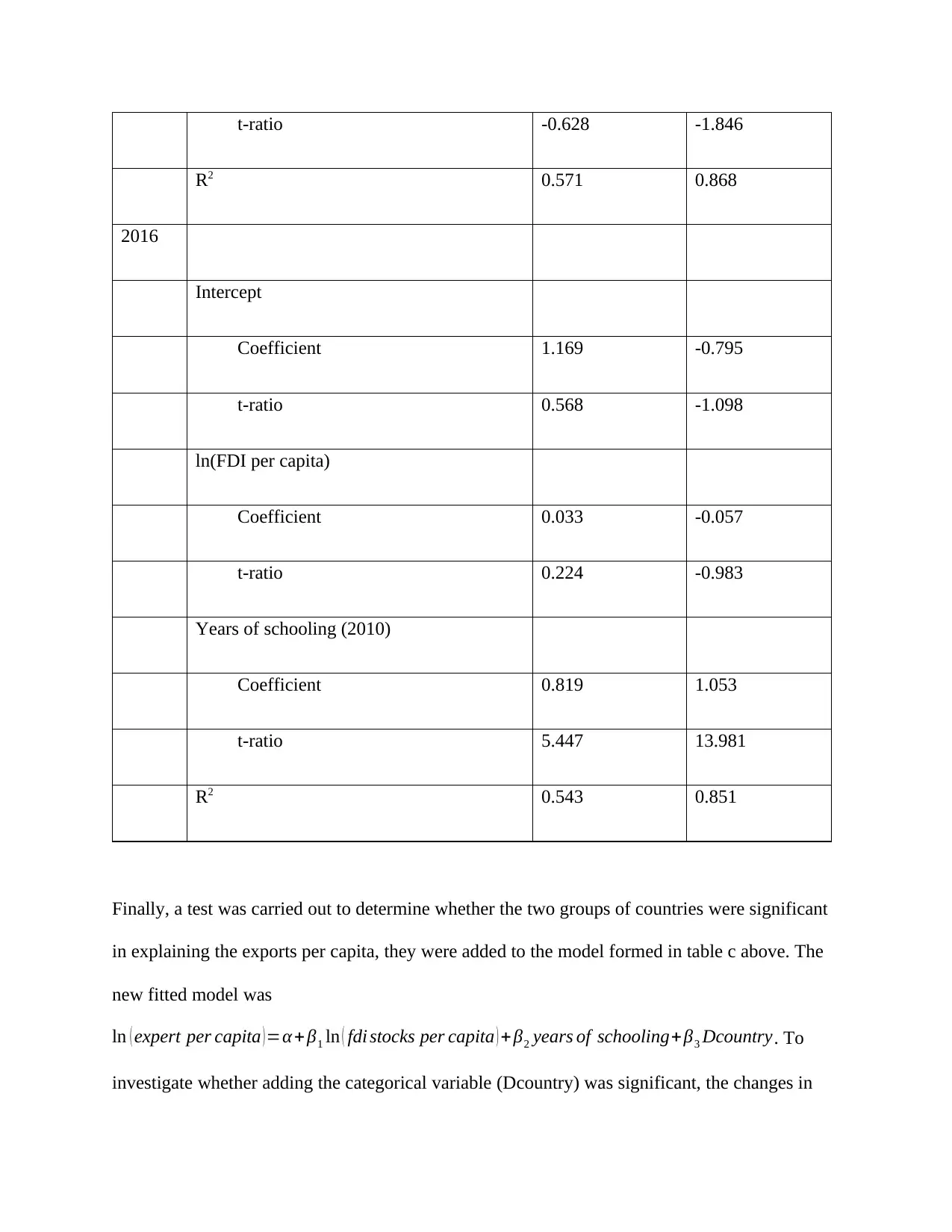

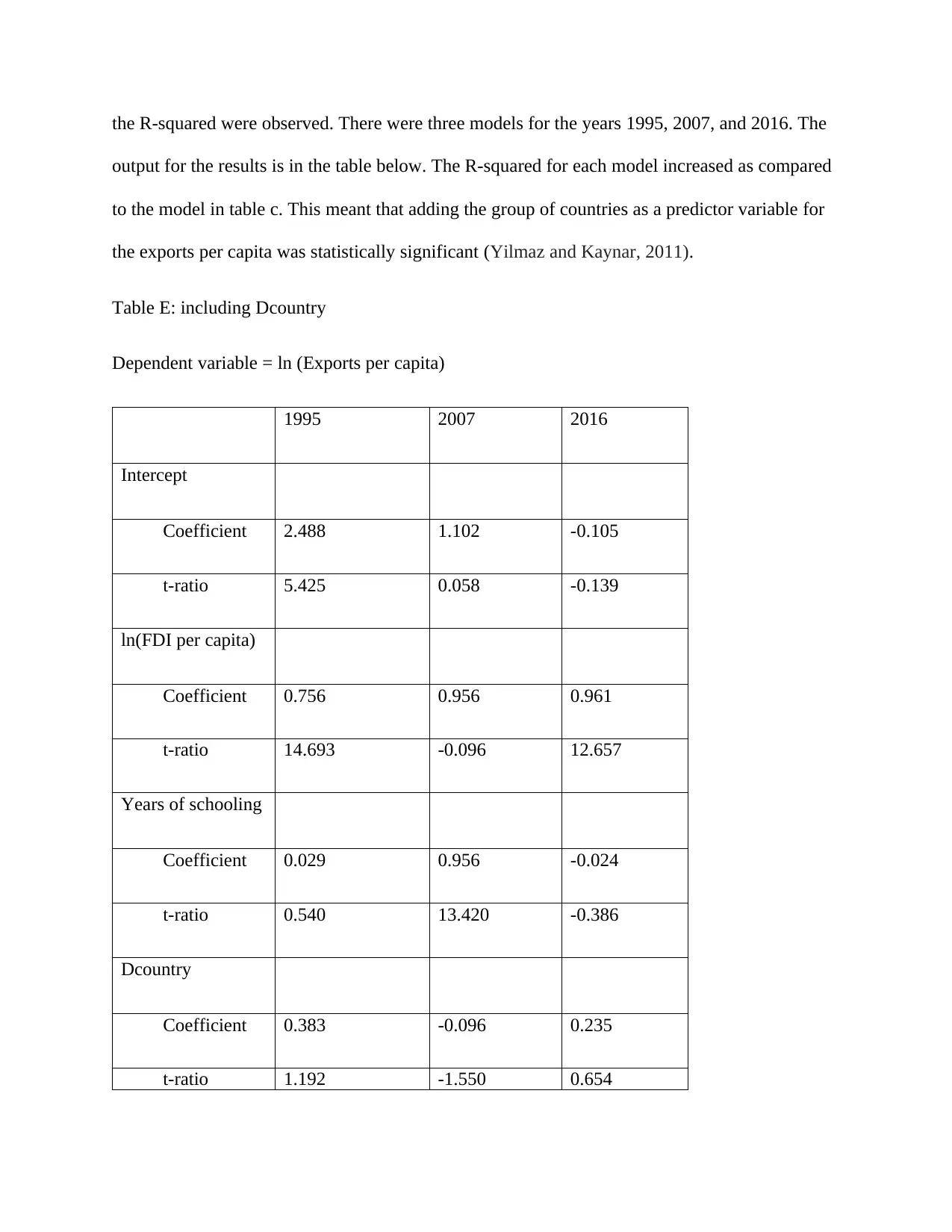

This report presents an analysis of the relationship between Foreign Direct Investment (FDI) and exports per capita. The analysis is based on statistical tests, including t-tests and correlation analysis, to determine if there are significant differences between countries in group H and group L regarding FDI stocks and exports per capita across three different years (1995, 2007, and 2016). The report also examines the correlation between FDI and exports per capita, both for the whole sample and divided into the country groups, revealing a strong positive linear relationship. Furthermore, the study employs regression models to assess the impact of FDI stocks per capita and years of schooling on exports per capita, both individually and combined. The findings indicate a significant relationship between FDI and exports, with varying degrees of influence across the years and country groups. The report concludes by evaluating the significance of country groups as a predictor variable in the regression models, demonstrating their impact on explaining exports per capita.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.