Hatfield Manufacturing System Plc: Turkey Expansion Feasibility Report

VerifiedAdded on 2022/09/12

|5

|2292

|10

Report

AI Summary

This report presents a comprehensive financial feasibility analysis of Hatfield Manufacturing System Plc's (HMS Plc) proposed business expansion into Turkey. The analysis employs capital budgeting techniques, primarily focusing on Net Present Value (NPV), to evaluate the project's financial viability under various financing scenarios: all-debt, all-equity, and a mix of debt and equity. The report details the assumptions made, including cost of machinery, depreciation, revenue growth, variable and fixed costs, tax rates, and the cost of capital. The findings reveal that the project is financially feasible under all three scenarios, with the all-debt financing structure yielding the highest NPV. The analysis also considers the perspective of financing (home country perspective) and highlights the impact of foreign exchange volatility on the project's value. The report concludes by emphasizing the value addition of the project to the company and the importance of hedging against foreign exchange risks.

Assignment on Analysis of Feasibility of Proposed Investment Plan

Introduction

Hatfield Manufacturing System Plc, UK is a British company propose to expand its business

operations in Turkey. The company is an engineering firm which has specialisation in the

field of design, development and manufacture of additive layer manufacturing systems. The

company proposed to set up a new plant for the purpose of manufacturing the aforesaid

products in Turkey. The major business customer of the above products encompass aerospace

and motor vehicle industries. Since Turkey has a very competitive automotive industry,

setting up the unit in Turkey shall greatly help the company. The company wishes to

understand the following for the proposed Turkey Exapansion:

(a) Financial Viability of the project;

(b) Should they adopt foreign country or home country perspective;

(c) Does the project have any value addition to the company;

(d) Impact of foreign exchange volatility on value created by HMS;

(e) Method of financing the project

Analysis

Financial Viability of the project;

For analysing the feasibility of the project, capital budgeting has been considered as the most

appropriate tool with Net Present Value being the parameter tested. Net Present Value is

generally used to analyse the feasibility of the project by discounting the project inflows with

the weighted average cost of capital of the company. If the discounted inflow is greater than

discounted outflow, project is feasible. Further, the higher the Net Present Value, the better

the project shall be.

For computing the Net present Value of the project, the following facts have been taken into

consideration:

(a) Cost of Machinery purchased has been considered as upfront outflow of TL110 Mio;

(b) Depreciation of asset has been charged over 10 years based on straight line method;

(c) Revenue has been proposed to increase by 12% over year;

(d) Cost of production has been segregated in two categories Labour and other variable

cost where in labour cost increase by 2% year on year while other variable cost

increases by 1.5% on year on year basis;

(e) Fixed cost shall increase by 1%;

(f) Tax has been considered @19% on account of benefits of Double Taxation Avoidance

Agreement;

(g) Risk Premium has been assumed @ 5%;

(h) Cost of Debt has been considered @6%;

(i) Funding shall be procured in UK and shall be infused in equity;

Based on above facts, the feasibility analysis of the project has been conducted to determine

the net present value of the project under three proposed scenarios:

(a) When the project is financed by using debt in UK@ 6%;

(b) When project is financed by all equity by procuring funds through issue of equity;

Introduction

Hatfield Manufacturing System Plc, UK is a British company propose to expand its business

operations in Turkey. The company is an engineering firm which has specialisation in the

field of design, development and manufacture of additive layer manufacturing systems. The

company proposed to set up a new plant for the purpose of manufacturing the aforesaid

products in Turkey. The major business customer of the above products encompass aerospace

and motor vehicle industries. Since Turkey has a very competitive automotive industry,

setting up the unit in Turkey shall greatly help the company. The company wishes to

understand the following for the proposed Turkey Exapansion:

(a) Financial Viability of the project;

(b) Should they adopt foreign country or home country perspective;

(c) Does the project have any value addition to the company;

(d) Impact of foreign exchange volatility on value created by HMS;

(e) Method of financing the project

Analysis

Financial Viability of the project;

For analysing the feasibility of the project, capital budgeting has been considered as the most

appropriate tool with Net Present Value being the parameter tested. Net Present Value is

generally used to analyse the feasibility of the project by discounting the project inflows with

the weighted average cost of capital of the company. If the discounted inflow is greater than

discounted outflow, project is feasible. Further, the higher the Net Present Value, the better

the project shall be.

For computing the Net present Value of the project, the following facts have been taken into

consideration:

(a) Cost of Machinery purchased has been considered as upfront outflow of TL110 Mio;

(b) Depreciation of asset has been charged over 10 years based on straight line method;

(c) Revenue has been proposed to increase by 12% over year;

(d) Cost of production has been segregated in two categories Labour and other variable

cost where in labour cost increase by 2% year on year while other variable cost

increases by 1.5% on year on year basis;

(e) Fixed cost shall increase by 1%;

(f) Tax has been considered @19% on account of benefits of Double Taxation Avoidance

Agreement;

(g) Risk Premium has been assumed @ 5%;

(h) Cost of Debt has been considered @6%;

(i) Funding shall be procured in UK and shall be infused in equity;

Based on above facts, the feasibility analysis of the project has been conducted to determine

the net present value of the project under three proposed scenarios:

(a) When the project is financed by using debt in UK@ 6%;

(b) When project is financed by all equity by procuring funds through issue of equity;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(c) When project is financed through mix of debt and equity;

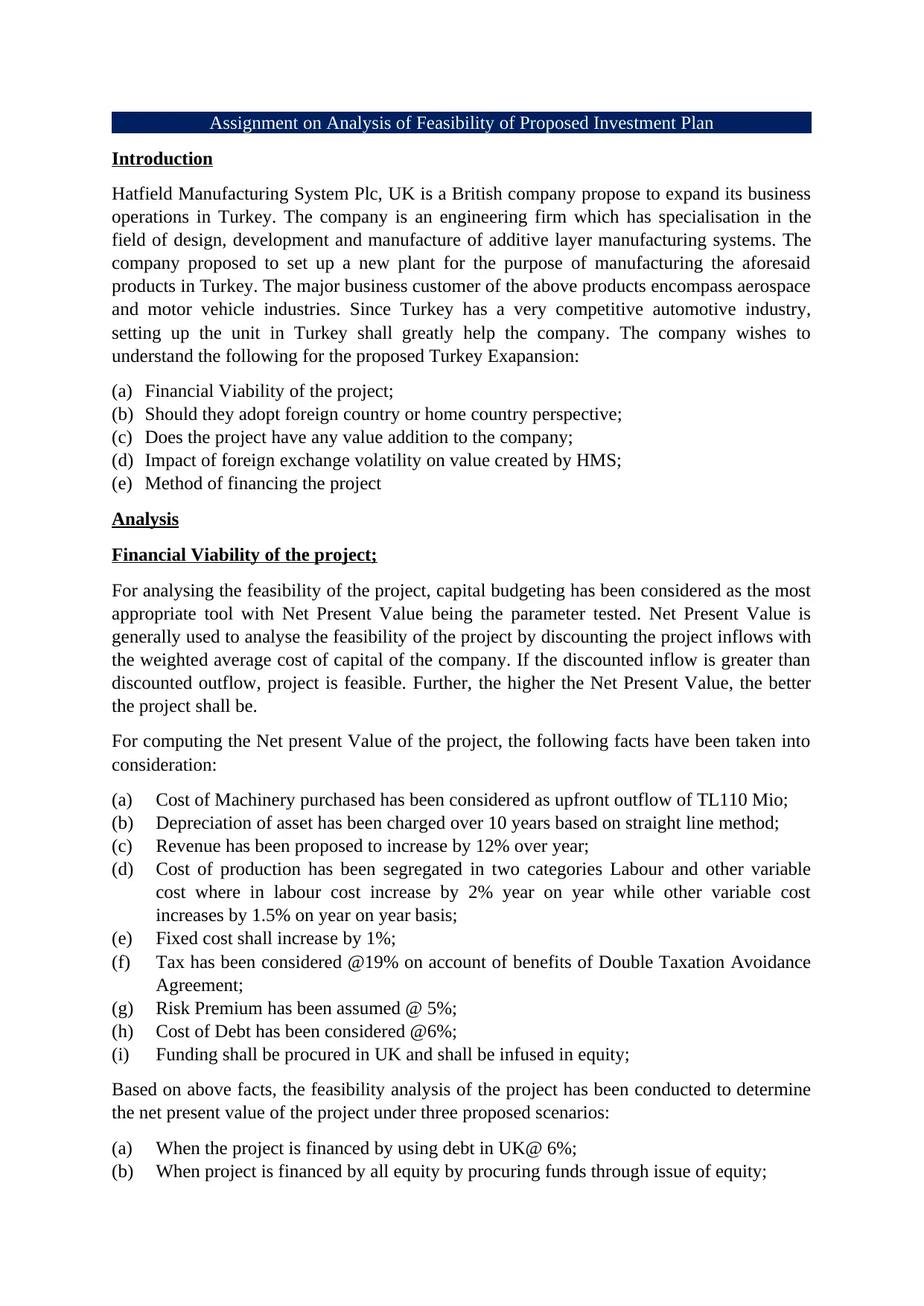

When the project is financed by using debt in UK@ 6%

If the project is financed using debt overall, the company present level of debt of Sterling

5000K shall increase by Sterling 12.46 Million, The said decision shall increase the debt level

of the company significantly. The feasibility of the plan under proposed financing shall be

very high as the cost of debt shall be low as compared to equity. Further, funding shall be

procured in the domestic market as compared to foreign market as the rate of interest is low

in the domestic market. However, one needs to consider the impact of foreign exchange

fluctuation while taking the concerned decision. Based on the concerned facts, the net present

value for an all debt capital structure has been computed here-in-below:

Year

Sl

No Particulars 0 1 2 3 4 5 6 7 8 9 10

1 Cost of machinery

-

110000000

2 Depreciation

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

3 Revenue 15518000 17380160 19465779 21801673 24417873 27348018 30629780 34305354 38421997 43032636

4 Variable Cost of Production

Labour -513450 -523719 -534193.4 -544877.2 -555774.8 -566890.3 -578228.1 -589792.7 -601588.5 -613620.3

Other Variable Cost -953550 -967853.3 -982371 -997106.6 -1012063 -1027244 -1042653 -1058293 -1074167 -1090280

5 Fixed Cost -1144 -1155.44 -1166.994 -1178.664 -1190.451 -1202.355 -1214.379 -1226.523 -1238.788 -1251.176

6 Profit Before Tax 3049856

4887432.

3

6948047.

8

9258510.

2 11848845 14752681 18007685 21656042 25745002 30327485

7

Tax @19% (Being higher for

UK) -579472.6 -928612.1 -1320129 -1759117 -2251281 -2803009 -3421460 -4114648 -4891550 -5762222

8 Profit after tax

-

110000000

2470383.

4

3958820.

2

5627918.

7

7499393.

2

9597564.

4 11949672 14586225 17541394 20853452 24565263

9 Depreciation 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000

10 Cash flow

-

110000000 13470383 14958820 16627919 18499393 20597564 22949672 25586225 28541394 31853452 35565263

11 Discounting Factor @6% 1

0.943396

2

0.889996

4

0.839619

3

0.792093

7

0.747258

2

0.704960

5

0.665057

1

0.627412

4

0.591898

5

0.558394

8

12 PV

-

110000000 12707909 13313297 13961121 14653252 15391698 16178613 17016301 17907224 18854009 19859457

13 NPV

49842881.

4

Based on above simulation, the net present value of the above project has been computed at

49 Million approx. after considering the cost of capital. The resultant extra capital with the

company shall add value to financials and net profit of the company.

When the project is financed by using Equity

If the project is financed using equity overall, the company present level of equity of Sterling

83930K shall increase by Sterling 12.46 Million, The said decision shall increase the equity

level of the company significantly. The feasibility of the plan under proposed financing shall

be low as the cost of equity shall be high as compared to debt. Further, funding shall be

procured in the domestic market as compared to foreign market as the risk free rate of interest

is low in the domestic market. However, one needs to consider the impact of foreign

exchange fluctuation while taking the concerned decision. Based on the concerned facts, the

net present value for an all equity capital structure has been computed here-in-below:

Year

When the project is financed by using debt in UK@ 6%

If the project is financed using debt overall, the company present level of debt of Sterling

5000K shall increase by Sterling 12.46 Million, The said decision shall increase the debt level

of the company significantly. The feasibility of the plan under proposed financing shall be

very high as the cost of debt shall be low as compared to equity. Further, funding shall be

procured in the domestic market as compared to foreign market as the rate of interest is low

in the domestic market. However, one needs to consider the impact of foreign exchange

fluctuation while taking the concerned decision. Based on the concerned facts, the net present

value for an all debt capital structure has been computed here-in-below:

Year

Sl

No Particulars 0 1 2 3 4 5 6 7 8 9 10

1 Cost of machinery

-

110000000

2 Depreciation

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

3 Revenue 15518000 17380160 19465779 21801673 24417873 27348018 30629780 34305354 38421997 43032636

4 Variable Cost of Production

Labour -513450 -523719 -534193.4 -544877.2 -555774.8 -566890.3 -578228.1 -589792.7 -601588.5 -613620.3

Other Variable Cost -953550 -967853.3 -982371 -997106.6 -1012063 -1027244 -1042653 -1058293 -1074167 -1090280

5 Fixed Cost -1144 -1155.44 -1166.994 -1178.664 -1190.451 -1202.355 -1214.379 -1226.523 -1238.788 -1251.176

6 Profit Before Tax 3049856

4887432.

3

6948047.

8

9258510.

2 11848845 14752681 18007685 21656042 25745002 30327485

7

Tax @19% (Being higher for

UK) -579472.6 -928612.1 -1320129 -1759117 -2251281 -2803009 -3421460 -4114648 -4891550 -5762222

8 Profit after tax

-

110000000

2470383.

4

3958820.

2

5627918.

7

7499393.

2

9597564.

4 11949672 14586225 17541394 20853452 24565263

9 Depreciation 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000

10 Cash flow

-

110000000 13470383 14958820 16627919 18499393 20597564 22949672 25586225 28541394 31853452 35565263

11 Discounting Factor @6% 1

0.943396

2

0.889996

4

0.839619

3

0.792093

7

0.747258

2

0.704960

5

0.665057

1

0.627412

4

0.591898

5

0.558394

8

12 PV

-

110000000 12707909 13313297 13961121 14653252 15391698 16178613 17016301 17907224 18854009 19859457

13 NPV

49842881.

4

Based on above simulation, the net present value of the above project has been computed at

49 Million approx. after considering the cost of capital. The resultant extra capital with the

company shall add value to financials and net profit of the company.

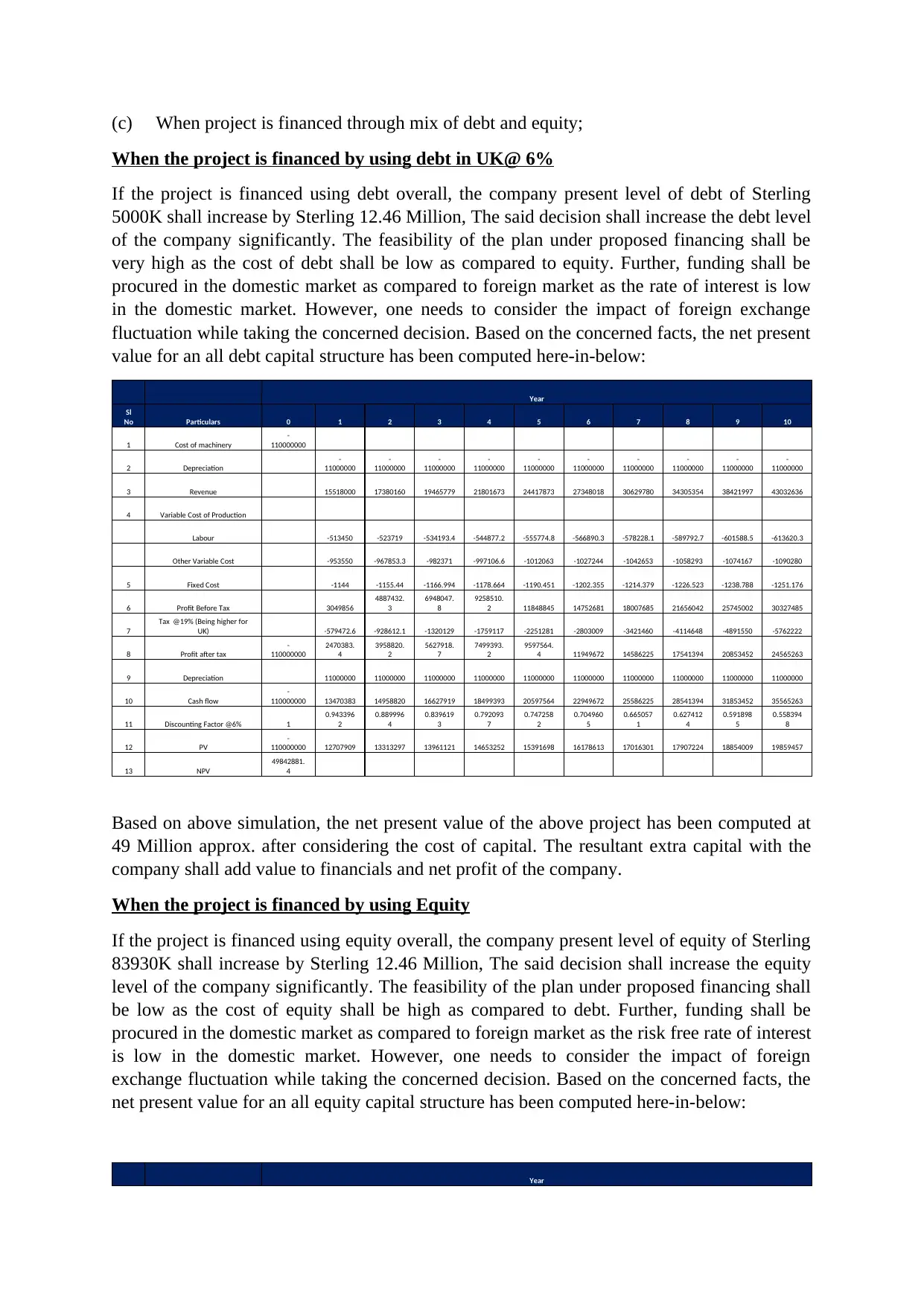

When the project is financed by using Equity

If the project is financed using equity overall, the company present level of equity of Sterling

83930K shall increase by Sterling 12.46 Million, The said decision shall increase the equity

level of the company significantly. The feasibility of the plan under proposed financing shall

be low as the cost of equity shall be high as compared to debt. Further, funding shall be

procured in the domestic market as compared to foreign market as the risk free rate of interest

is low in the domestic market. However, one needs to consider the impact of foreign

exchange fluctuation while taking the concerned decision. Based on the concerned facts, the

net present value for an all equity capital structure has been computed here-in-below:

Year

Sl

No Particulars 0 1 2 3 4 5 6 7 8 9 10

1 Cost of machinery

-

110000000

2 Depreciation

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

3 Revenue 15518000 17380160 19465779 21801673 24417873 27348018 30629780 34305354 38421997 43032636

4 Variable Cost of Production

Labour -513450 -523719 -534193.4 -544877.2 -555774.8 -566890.3 -578228.1 -589792.7 -601588.5 -613620.3

Other Variable Cost -953550 -967853.3 -982371 -997106.6 -1012063 -1027244 -1042653 -1058293 -1074167 -1090280

5 Fixed Cost -1144 -1155.44 -1166.994 -1178.664 -1190.451 -1202.355 -1214.379 -1226.523 -1238.788 -1251.176

6 Profit Before Tax 3049856

4887432.

3

6948047.

8

9258510.

2 11848845 14752681 18007685 21656042 25745002 30327485

7

Tax @19% (Being higher for

UK) -579472.6 -928612.1 -1320129 -1759117 -2251281 -2803009 -3421460 -4114648 -4891550 -5762222

8 Profit after tax

-

110000000

2470383.

4

3958820.

2

5627918.

7

7499393.

2

9597564.

4 11949672 14586225 17541394 20853452 24565263

9 Depreciation 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000

10 Cash flow

-

110000000 13470383 14958820 16627919 18499393 20597564 22949672 25586225 28541394 31853452 35565263

11 Discounting Factor @9% 1

0.917431

2 0.84168

0.772183

5

0.708425

2

0.649931

4

0.596267

3

0.547034

2

0.501866

3

0.460427

8

0.422410

8

12 PV

-

110000000 12358150 12590540 12839804 13105437 13387004 13684140 13996541 14323963 14666214 15023151

13 NPV

25974943.

5

Based on above simulation, the net present value of the above project has been computed at

26 Million approx. after considering the cost of capital. The resultant extra capital with the

company shall add value to financials and net profit of the company. The resultant NPV has

decreased to half as compared to an overall debt capital structure.

When the project is financed by using Equity and Debt in proportion of 50% each

If the project is financed using debt & equity 50% each, the company present level of equity

of Sterling 83930K shall increase by Sterling 6.23 Million and correspondingly debt shall

increase from 5000K to 11.23 Million, The said decision shall increase the equity & debt

level of the company significantly thereby maintaining debt equity level of the company. The

feasibility of the plan under proposed financing shall be medium as the cost of equity shall be

high as compared to debt. Further, funding shall be procured in the domestic market as

compared to foreign market as the risk free rate of interest and debt rate is low in the

domestic market. However, one needs to consider the impact of foreign exchange fluctuation

while taking the concerned decision. Based on the concerned facts, the net present value for

an mixed capital structure has been computed here-in-below:

Year

Sl

No Particulars 0 1 2 3 4 5 6 7 8 9 10

1 Cost of machinery

-

110000000

2 Depreciation

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

3 Revenue 15518000 17380160 19465779 21801673 24417873 27348018 30629780 34305354 38421997 43032636

4 Variable Cost of Production

Labour -513450 -523719 -534193.4 -544877.2 -555774.8 -566890.3 -578228.1 -589792.7 -601588.5 -613620.3

Other Variable Cost -953550 -967853.3 -982371 -997106.6 -1012063 -1027244 -1042653 -1058293 -1074167 -1090280

5 Fixed Cost -1144 -1155.44 -1166.994 -1178.664 -1190.451 -1202.355 -1214.379 -1226.523 -1238.788 -1251.176

6 Profit Before Tax 3049856

4887432.

3

6948047.

8

9258510.

2 11848845 14752681 18007685 21656042 25745002 30327485

7

Tax @19% (Being higher for

UK) -579472.6 -928612.1 -1320129 -1759117 -2251281 -2803009 -3421460 -4114648 -4891550 -5762222

8 Profit after tax

-

110000000

2470383.

4

3958820.

2

5627918.

7

7499393.

2

9597564.

4 11949672 14586225 17541394 20853452 24565263

No Particulars 0 1 2 3 4 5 6 7 8 9 10

1 Cost of machinery

-

110000000

2 Depreciation

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

3 Revenue 15518000 17380160 19465779 21801673 24417873 27348018 30629780 34305354 38421997 43032636

4 Variable Cost of Production

Labour -513450 -523719 -534193.4 -544877.2 -555774.8 -566890.3 -578228.1 -589792.7 -601588.5 -613620.3

Other Variable Cost -953550 -967853.3 -982371 -997106.6 -1012063 -1027244 -1042653 -1058293 -1074167 -1090280

5 Fixed Cost -1144 -1155.44 -1166.994 -1178.664 -1190.451 -1202.355 -1214.379 -1226.523 -1238.788 -1251.176

6 Profit Before Tax 3049856

4887432.

3

6948047.

8

9258510.

2 11848845 14752681 18007685 21656042 25745002 30327485

7

Tax @19% (Being higher for

UK) -579472.6 -928612.1 -1320129 -1759117 -2251281 -2803009 -3421460 -4114648 -4891550 -5762222

8 Profit after tax

-

110000000

2470383.

4

3958820.

2

5627918.

7

7499393.

2

9597564.

4 11949672 14586225 17541394 20853452 24565263

9 Depreciation 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000

10 Cash flow

-

110000000 13470383 14958820 16627919 18499393 20597564 22949672 25586225 28541394 31853452 35565263

11 Discounting Factor @9% 1

0.917431

2 0.84168

0.772183

5

0.708425

2

0.649931

4

0.596267

3

0.547034

2

0.501866

3

0.460427

8

0.422410

8

12 PV

-

110000000 12358150 12590540 12839804 13105437 13387004 13684140 13996541 14323963 14666214 15023151

13 NPV

25974943.

5

Based on above simulation, the net present value of the above project has been computed at

26 Million approx. after considering the cost of capital. The resultant extra capital with the

company shall add value to financials and net profit of the company. The resultant NPV has

decreased to half as compared to an overall debt capital structure.

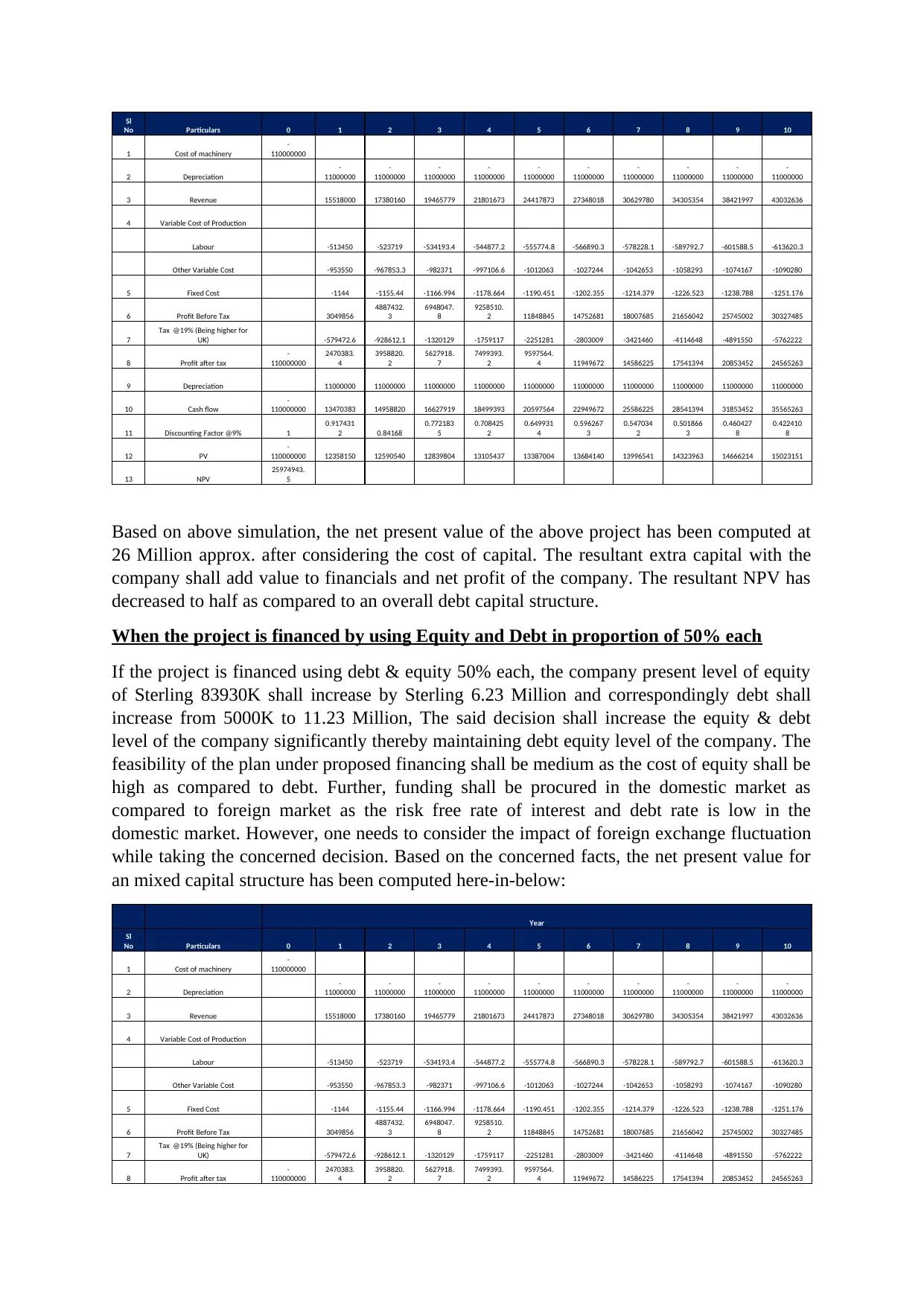

When the project is financed by using Equity and Debt in proportion of 50% each

If the project is financed using debt & equity 50% each, the company present level of equity

of Sterling 83930K shall increase by Sterling 6.23 Million and correspondingly debt shall

increase from 5000K to 11.23 Million, The said decision shall increase the equity & debt

level of the company significantly thereby maintaining debt equity level of the company. The

feasibility of the plan under proposed financing shall be medium as the cost of equity shall be

high as compared to debt. Further, funding shall be procured in the domestic market as

compared to foreign market as the risk free rate of interest and debt rate is low in the

domestic market. However, one needs to consider the impact of foreign exchange fluctuation

while taking the concerned decision. Based on the concerned facts, the net present value for

an mixed capital structure has been computed here-in-below:

Year

Sl

No Particulars 0 1 2 3 4 5 6 7 8 9 10

1 Cost of machinery

-

110000000

2 Depreciation

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

-

11000000

3 Revenue 15518000 17380160 19465779 21801673 24417873 27348018 30629780 34305354 38421997 43032636

4 Variable Cost of Production

Labour -513450 -523719 -534193.4 -544877.2 -555774.8 -566890.3 -578228.1 -589792.7 -601588.5 -613620.3

Other Variable Cost -953550 -967853.3 -982371 -997106.6 -1012063 -1027244 -1042653 -1058293 -1074167 -1090280

5 Fixed Cost -1144 -1155.44 -1166.994 -1178.664 -1190.451 -1202.355 -1214.379 -1226.523 -1238.788 -1251.176

6 Profit Before Tax 3049856

4887432.

3

6948047.

8

9258510.

2 11848845 14752681 18007685 21656042 25745002 30327485

7

Tax @19% (Being higher for

UK) -579472.6 -928612.1 -1320129 -1759117 -2251281 -2803009 -3421460 -4114648 -4891550 -5762222

8 Profit after tax

-

110000000

2470383.

4

3958820.

2

5627918.

7

7499393.

2

9597564.

4 11949672 14586225 17541394 20853452 24565263

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year

Sl

No Particulars 0 1 2 3 4 5 6 7 8 9 10

9 Depreciation 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000

10 Cash flow

-

110000000 13470383 14958820 16627919 18499393 20597564 22949672 25586225 28541394 31853452 35565263

11 Discounting Factor @7.5% 1

0.930232

6

0.865332

6

0.804960

6

0.748800

5

0.696558

6

0.647961

5

0.602754

9

0.560702

2

0.521583

5

0.485193

9

12 PV

-

110000000 12530589 12944355 13384819 13852355 14347411 14870504 15422222 16003224 16614234 17256050

13 NPV

37225763.

8

Based on above simulation, the net present value of the above project has been computed at

37 Million approx. after considering the cost of capital. The resultant extra capital with the

company shall add value to financials and net profit of the company. The resultant NPV has

decreased to half as compared to an overall debt capital structure.

Based on above three simulation, it may be deciphered that proposed plan is feasible under

the three concerned scenarios and may be put into practice.

Should they adopt foreign country or home country perspective

The perspective that shall be adopted under the current scenario shall be home country

perspective as the planning of the company is to bring any additional cash flow in UK.

Further, the required capital for the proposed plan shall be very high, it shall be cheaper for

the company to procure such funds in a developed market compared to developing market.

Also, the company does not have such huge market image that any foreign lending institution

shall lend such high amount of capital. Based on above rationale, home country perspective is

an ideal option. However, one need to consider the impact of debt to equity capital structure

in the proposed plan.

Does the project have any value addition to the company

Yes, the project is adding value to the company as the Net Present Value for all the three

scenarios presented above are high. Thus, it may be safely concluded that the project shall

add significant value to the financials of the company over the period. The value that shall be

added under an overall debt structure shall be 49 Million TL, while the value added under an

overall equity structure shall be 26 Million TL and under mixed capital structure of debt and

equity in equal proportion shall be 37 Million TL.

Impact of foreign exchange volatility on value created by HMS

There shall be significant impact on value created by HMS as the risk free interest rate of

both the countries are significantly different. Also, by looking at past trend of volatility of

foreign exchange one can easily contend that sterling shall be stronger currency compared to

TL in the near future. Accordingly, one needs to consider the impact of foreign exchange

fluctuation on the feasibility of the project. In the proposed plan structure, since the

fluctuation in foreign currency is significantly high the proposed plan of bringing back the

capital shall be highly contested. Also, the fluctuation in foreign exchange will render the

feasibility of project to be ineffective. Accordingly, the company should not bring the capital

back. Alternatively, the company may borrow in the foreign market @ 20.5% + premium

which may render the project ineffective. Thus, company should appropriate hedge the risk of

Sl

No Particulars 0 1 2 3 4 5 6 7 8 9 10

9 Depreciation 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000 11000000

10 Cash flow

-

110000000 13470383 14958820 16627919 18499393 20597564 22949672 25586225 28541394 31853452 35565263

11 Discounting Factor @7.5% 1

0.930232

6

0.865332

6

0.804960

6

0.748800

5

0.696558

6

0.647961

5

0.602754

9

0.560702

2

0.521583

5

0.485193

9

12 PV

-

110000000 12530589 12944355 13384819 13852355 14347411 14870504 15422222 16003224 16614234 17256050

13 NPV

37225763.

8

Based on above simulation, the net present value of the above project has been computed at

37 Million approx. after considering the cost of capital. The resultant extra capital with the

company shall add value to financials and net profit of the company. The resultant NPV has

decreased to half as compared to an overall debt capital structure.

Based on above three simulation, it may be deciphered that proposed plan is feasible under

the three concerned scenarios and may be put into practice.

Should they adopt foreign country or home country perspective

The perspective that shall be adopted under the current scenario shall be home country

perspective as the planning of the company is to bring any additional cash flow in UK.

Further, the required capital for the proposed plan shall be very high, it shall be cheaper for

the company to procure such funds in a developed market compared to developing market.

Also, the company does not have such huge market image that any foreign lending institution

shall lend such high amount of capital. Based on above rationale, home country perspective is

an ideal option. However, one need to consider the impact of debt to equity capital structure

in the proposed plan.

Does the project have any value addition to the company

Yes, the project is adding value to the company as the Net Present Value for all the three

scenarios presented above are high. Thus, it may be safely concluded that the project shall

add significant value to the financials of the company over the period. The value that shall be

added under an overall debt structure shall be 49 Million TL, while the value added under an

overall equity structure shall be 26 Million TL and under mixed capital structure of debt and

equity in equal proportion shall be 37 Million TL.

Impact of foreign exchange volatility on value created by HMS

There shall be significant impact on value created by HMS as the risk free interest rate of

both the countries are significantly different. Also, by looking at past trend of volatility of

foreign exchange one can easily contend that sterling shall be stronger currency compared to

TL in the near future. Accordingly, one needs to consider the impact of foreign exchange

fluctuation on the feasibility of the project. In the proposed plan structure, since the

fluctuation in foreign currency is significantly high the proposed plan of bringing back the

capital shall be highly contested. Also, the fluctuation in foreign exchange will render the

feasibility of project to be ineffective. Accordingly, the company should not bring the capital

back. Alternatively, the company may borrow in the foreign market @ 20.5% + premium

which may render the project ineffective. Thus, company should appropriate hedge the risk of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

foreign exchange fluctuation. Also, company may take appropriate loan in the market

wherein sales from Turkey is made to reduce the loss on account of exchange.

Method of financing the project

An ideal method of financing the project shall be a mix of debt and equity in equal proportion

as the said funding shall strengthen the financials of the company and also shall add value to

the tune of 37 Million TL in the books of the company over the period of 10 years. However,

considering the level of fluctuation in the currency in the foreign an all equity structure may

also be promulgated and thought upon.

Conclusion

The project is feasible if the loan is procured in the domestic market of the company as there

is a huge variation in the interest rate at two countries. Further, the impact of foreign

exchange fluctuation may seriously challenge the viability of the project in the long run.

wherein sales from Turkey is made to reduce the loss on account of exchange.

Method of financing the project

An ideal method of financing the project shall be a mix of debt and equity in equal proportion

as the said funding shall strengthen the financials of the company and also shall add value to

the tune of 37 Million TL in the books of the company over the period of 10 years. However,

considering the level of fluctuation in the currency in the foreign an all equity structure may

also be promulgated and thought upon.

Conclusion

The project is feasible if the loan is procured in the domestic market of the company as there

is a huge variation in the interest rate at two countries. Further, the impact of foreign

exchange fluctuation may seriously challenge the viability of the project in the long run.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.