Brunel University: Savings and Investment Analysis in Iran (EC5615)

VerifiedAdded on 2023/01/03

|11

|2920

|83

Report

AI Summary

This report presents an empirical analysis of the relationship between savings and investment in Iran's economy, focusing on the Feldstein-Horioka puzzle. The study utilizes time-series data from 1959 to 2008 and employs the Autoregressive Distributed Lag (ARDL) approach to examine both short-run and long-run dynamics. The methodology includes unit root tests and cointegration analysis to ensure the robustness of the results. The findings suggest a long-run equilibrium relationship between savings and investment, with savings having a significant impact on investment. The results also indicate that it takes over two years to settle the shock to investment. The study concludes that the hypothesis of complete capital immobility in Iran cannot be rejected, and suggests that providing facilities for foreign investment could be an effective policy recommendation.

ASSESSMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................4

Literature Review............................................................................................................................5

Data and Methodology....................................................................................................................6

Results and Analysis........................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Introduction......................................................................................................................................4

Literature Review............................................................................................................................5

Data and Methodology....................................................................................................................6

Results and Analysis........................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This paper centers around the connection among reserve funds and interest in Iran's economy. In

light of the consequences of this investigation, there is a since quite a while ago run balance

connection among reserve funds and gross homegrown venture, and direct critical impact of

reserve funds on interest over the long haul is more grounded than that in the short run.

Accordingly, thinking about Feldstein's and Horioka's hypothesis, a theory of complete capital

fixed status in Iran isn't dismissed. The assessed coefficient of mistake remedy term shows that

over two years is needed to settle the stun to speculation. Giving important offices to unfamiliar

speculation has been proposed as an arrangement suggestion in the examination.

Venture is viewed as motor of financial development in the financial matters writing. The

gathering of actual capital is required to prompts making the creation limit from one viewpoint,

and then again, in-wrinkling total interest. Consequently, expanded speculation makes new

position openings, notwithstanding expanded creation and financial development – the open

doors which increment interest for work as well. Be that as it may, other than the security,

innovation, lawful foundation, etc, financing is the one the main parts of the venture. At the end

of the day, reserve funds can assume a significant function in the gracefully of assets and assets

which can be contributed. It makes sense why the hole among reserve funds and speculation,

named as "reserve funds hole" in the "one-hole financial development models", is considered as

a significant impediment in accomplishing monetary development. The connection between

homegrown venture and public investment funds is critical to be analyzed in clarifying the

conduct of installment balance, more than being considered in the examination of the

homegrown economy.

In dissecting the conduct of reserve funds and venture, Feldstein and Horioka (1980) have

acquainted the path with relate between the two as a pointer to gauge the level of capital

versatility between nations. In the event that there is no boundary in capital portability between

nations, they accepted, public investment funds in every nation can choose the most helpful

undertakings on the planet, and can stream toward it (Caporale 2008).

This paper centers around the connection among reserve funds and interest in Iran's economy. In

light of the consequences of this investigation, there is a since quite a while ago run balance

connection among reserve funds and gross homegrown venture, and direct critical impact of

reserve funds on interest over the long haul is more grounded than that in the short run.

Accordingly, thinking about Feldstein's and Horioka's hypothesis, a theory of complete capital

fixed status in Iran isn't dismissed. The assessed coefficient of mistake remedy term shows that

over two years is needed to settle the stun to speculation. Giving important offices to unfamiliar

speculation has been proposed as an arrangement suggestion in the examination.

Venture is viewed as motor of financial development in the financial matters writing. The

gathering of actual capital is required to prompts making the creation limit from one viewpoint,

and then again, in-wrinkling total interest. Consequently, expanded speculation makes new

position openings, notwithstanding expanded creation and financial development – the open

doors which increment interest for work as well. Be that as it may, other than the security,

innovation, lawful foundation, etc, financing is the one the main parts of the venture. At the end

of the day, reserve funds can assume a significant function in the gracefully of assets and assets

which can be contributed. It makes sense why the hole among reserve funds and speculation,

named as "reserve funds hole" in the "one-hole financial development models", is considered as

a significant impediment in accomplishing monetary development. The connection between

homegrown venture and public investment funds is critical to be analyzed in clarifying the

conduct of installment balance, more than being considered in the examination of the

homegrown economy.

In dissecting the conduct of reserve funds and venture, Feldstein and Horioka (1980) have

acquainted the path with relate between the two as a pointer to gauge the level of capital

versatility between nations. In the event that there is no boundary in capital portability between

nations, they accepted, public investment funds in every nation can choose the most helpful

undertakings on the planet, and can stream toward it (Caporale 2008).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Literature Review

Obstfeld (1986) demonstrated that the connection among reserve funds and venture has more

illustrative capacity to dissect dynamic of installment adjust and see how economies respond

against hindrances in the unfamiliar economy. Utilizing Engle's and Granger's econometric

technique and yearly information from 1948 to 1987, Miller (1988) inspected the connection

among venture and investment funds in the economy of Latin America. His examination

uncovered that in the pre-World War II and in the states of fixed conversion standard framework,

there was a critical positive causal connection among venture and sparing. In light of the

discoveries of this exploration, increment in capital portability fundamentally influences the hole

among reserve funds and venture. In his investigation, Kim (1999) tried Feldstein's and Horioka's

hypothesis for 62 nations (counting 42 created nations and 14 OECD part nations) utilizing the

board information during 1958 to 1992. The aftereffects of this investigation shows that the

connection coefficient among speculation and reserve funds in the OECD part nations is more

than in created nations, while capital portability is less in OECD part nations. As such,

Feldstein's and Horioka's hypothesis has been factually affirmed in this examination. In

Panopoulou and Caporele (1999) research, the connection among venture and investment funds

has been analyzed for five chosen Latin America nations during 1950 and 1994. For this reason,

Johansen-Juselius cointegration strategy has been utilized. This examination demonstrated that

not at all like the hypothesis of Feldstein and Horioka, there is a critical positive connection

among speculation and investment funds in the considered nations over the long haul. Jansen

(2000) inspected the connection among speculation and investment funds for created nations.

Utilizing board information identified with 1962 and 1994, he assessed the connection

coefficient between the two factors, in view of whose discoveries, blemished capital portability

is streamed in this gathering of nations. In Tan Hui (2000) research, the connection among

speculation and reserve funds has been inspected for five "ASEAN" nations by utilizing Engle-

Granger strategy based on a vector auto adjustment model, in light of information of 1967 to

1997. The aftereffects of this investigation demonstrate solid, since quite a while ago run

relationship among's speculation and reserve funds in the above nations.

Obstfeld (1986) demonstrated that the connection among reserve funds and venture has more

illustrative capacity to dissect dynamic of installment adjust and see how economies respond

against hindrances in the unfamiliar economy. Utilizing Engle's and Granger's econometric

technique and yearly information from 1948 to 1987, Miller (1988) inspected the connection

among venture and investment funds in the economy of Latin America. His examination

uncovered that in the pre-World War II and in the states of fixed conversion standard framework,

there was a critical positive causal connection among venture and sparing. In light of the

discoveries of this exploration, increment in capital portability fundamentally influences the hole

among reserve funds and venture. In his investigation, Kim (1999) tried Feldstein's and Horioka's

hypothesis for 62 nations (counting 42 created nations and 14 OECD part nations) utilizing the

board information during 1958 to 1992. The aftereffects of this investigation shows that the

connection coefficient among speculation and reserve funds in the OECD part nations is more

than in created nations, while capital portability is less in OECD part nations. As such,

Feldstein's and Horioka's hypothesis has been factually affirmed in this examination. In

Panopoulou and Caporele (1999) research, the connection among venture and investment funds

has been analyzed for five chosen Latin America nations during 1950 and 1994. For this reason,

Johansen-Juselius cointegration strategy has been utilized. This examination demonstrated that

not at all like the hypothesis of Feldstein and Horioka, there is a critical positive connection

among speculation and investment funds in the considered nations over the long haul. Jansen

(2000) inspected the connection among speculation and investment funds for created nations.

Utilizing board information identified with 1962 and 1994, he assessed the connection

coefficient between the two factors, in view of whose discoveries, blemished capital portability

is streamed in this gathering of nations. In Tan Hui (2000) research, the connection among

speculation and reserve funds has been inspected for five "ASEAN" nations by utilizing Engle-

Granger strategy based on a vector auto adjustment model, in light of information of 1967 to

1997. The aftereffects of this investigation demonstrate solid, since quite a while ago run

relationship among's speculation and reserve funds in the above nations.

Fabiana (2000) analyzed the relationship among's reserve funds and venture just as its impact on

capital versatility in created nations during 1960 to 1996. For this reason, he has utilized the

board information. The outcomes show that there is a huge positive relationship be-tween

venture and sparing. Anyway thinking about the experimental proof, capital portability has

expanded in these nations after 1975. These outcomes, truth be told, are incongruent with the

hypothesis of Feldstein and Horioka. Vita and Abbott (2002) inspected the connection among

venture and reserve funds, with auto backward dispersed slack (ARDL) model and utilizing

yearly information (from 1946 to 1998) identifying with Latin American nations. As indicated by

research in these nations, connection coefficient among speculation and investment funds has

declined from 1971 onwards, due to the capital versatility. In Bassam's (2004) research, the

causal connection among venture and investment funds in the four MENA nations (Egypt,

Morocco, Jordan and Tanzania) is tentatively tried utilizing information from 1961 to 2002, with

Granger's causality strategy. His investigation uncovered that there is a single direction causal

relationship (from speculation to reserve funds) in Jordan, single direction causal relationship

(from investment funds to interest) in Morocco and Egypt, and two-way causal relationship in

Tanzania. Noman et al. (2008) analyzed the connection among reserve funds and interest in

South Asia by utilizing the fixed impact and arbitrary impact techniques for the board

information identifying with the long periods of 1973 to 2002. The outcomes show positive,

however frail relationship among's speculation and investment funds in Bangladesh, Nepal, Sri

Lanka, Pakistan and India. The analysts indicated that the powerless relationship between's the

above factors is come about because of the size of government in the economy of these nations,

rather than capital portability.

Data and Methodology

Untouched arrangement information of sparing and interest in Iran (1959 to 2008) have been

utilized in this examination to test the Feldstein-Horioka's hypothesis. Utilization of the

customary strategies in econometrics for experimental investigations has been founded on the

presumption of the factors' fixed. Notwithstanding, the examinations on this territory show that

in many time arrangement, the supposition above is inaccurate and that a large number of these

factors are questionable. It might cause misleading relapse, because of which certainty to the

assessed coefficients will be lost. Hence, as indicated by the hypothesis of cointegration in

capital versatility in created nations during 1960 to 1996. For this reason, he has utilized the

board information. The outcomes show that there is a huge positive relationship be-tween

venture and sparing. Anyway thinking about the experimental proof, capital portability has

expanded in these nations after 1975. These outcomes, truth be told, are incongruent with the

hypothesis of Feldstein and Horioka. Vita and Abbott (2002) inspected the connection among

venture and reserve funds, with auto backward dispersed slack (ARDL) model and utilizing

yearly information (from 1946 to 1998) identifying with Latin American nations. As indicated by

research in these nations, connection coefficient among speculation and investment funds has

declined from 1971 onwards, due to the capital versatility. In Bassam's (2004) research, the

causal connection among venture and investment funds in the four MENA nations (Egypt,

Morocco, Jordan and Tanzania) is tentatively tried utilizing information from 1961 to 2002, with

Granger's causality strategy. His investigation uncovered that there is a single direction causal

relationship (from speculation to reserve funds) in Jordan, single direction causal relationship

(from investment funds to interest) in Morocco and Egypt, and two-way causal relationship in

Tanzania. Noman et al. (2008) analyzed the connection among reserve funds and interest in

South Asia by utilizing the fixed impact and arbitrary impact techniques for the board

information identifying with the long periods of 1973 to 2002. The outcomes show positive,

however frail relationship among's speculation and investment funds in Bangladesh, Nepal, Sri

Lanka, Pakistan and India. The analysts indicated that the powerless relationship between's the

above factors is come about because of the size of government in the economy of these nations,

rather than capital portability.

Data and Methodology

Untouched arrangement information of sparing and interest in Iran (1959 to 2008) have been

utilized in this examination to test the Feldstein-Horioka's hypothesis. Utilization of the

customary strategies in econometrics for experimental investigations has been founded on the

presumption of the factors' fixed. Notwithstanding, the examinations on this territory show that

in many time arrangement, the supposition above is inaccurate and that a large number of these

factors are questionable. It might cause misleading relapse, because of which certainty to the

assessed coefficients will be lost. Hence, as indicated by the hypothesis of cointegration in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

present day econometrics, it is basic that those strategies mulling over fixed and co combination

to be utilized for assessing capacities, when utilizing the time arrangement. The stationer factors

may not be of a similar degree, which for this situation, Johhansen-Juselius cointegration

technique can not be valuable. Autoregressive dispersed slack methodology is among the

strategies where dissimilar to the technique Johhansen-Juselius (in which all factors must be of

degree one), the level of factors' fixed should be fundamentally in a similar extent, and the fitting

model can be picked by deciding legitimate slacks for factors. Hence, given these

contemplations, the auto backward disseminated slack (ARDL) approach is utilized in this

examination. The above strategy all the while appraises long-and short-run designs in the model,

and takes care of the issues identifying with the end of factors and autocorrelation. Along these

lines, the strategy's assessments are impartial and proficient, because of absence of such issues as

autocorrelation and endogenity.

Number of ideal slacks for every factor can be resolved with the assistance of Akaike, Schwarz-

Bayesian and Hannan-Quinn Criteria. In auto backward conveyed slack technique, short-run

relationship is assessed in two phases. Presence of a since quite a while ago run connection

between factors of the model is tried in the main stage. In the event that the absolute coefficients

assessed for variable-subordinate slacks are more modest than one in connection (1), the

dynamic model will watch out for the since quite a while ago run balance. Subsequently, for the

cointegration test, it is important to do the accompanying theory test.

By looking at the processed measurement t and the basic amount proposed by Banerjee, Dolado

and Mestera at the expected certainty level, one can understand whether there is a since quite a

while ago run relationship. In the event that a since quite a while ago run connection between

model factors is end up being available, the since quite a while ago run coefficients will be

to be utilized for assessing capacities, when utilizing the time arrangement. The stationer factors

may not be of a similar degree, which for this situation, Johhansen-Juselius cointegration

technique can not be valuable. Autoregressive dispersed slack methodology is among the

strategies where dissimilar to the technique Johhansen-Juselius (in which all factors must be of

degree one), the level of factors' fixed should be fundamentally in a similar extent, and the fitting

model can be picked by deciding legitimate slacks for factors. Hence, given these

contemplations, the auto backward disseminated slack (ARDL) approach is utilized in this

examination. The above strategy all the while appraises long-and short-run designs in the model,

and takes care of the issues identifying with the end of factors and autocorrelation. Along these

lines, the strategy's assessments are impartial and proficient, because of absence of such issues as

autocorrelation and endogenity.

Number of ideal slacks for every factor can be resolved with the assistance of Akaike, Schwarz-

Bayesian and Hannan-Quinn Criteria. In auto backward conveyed slack technique, short-run

relationship is assessed in two phases. Presence of a since quite a while ago run connection

between factors of the model is tried in the main stage. In the event that the absolute coefficients

assessed for variable-subordinate slacks are more modest than one in connection (1), the

dynamic model will watch out for the since quite a while ago run balance. Subsequently, for the

cointegration test, it is important to do the accompanying theory test.

By looking at the processed measurement t and the basic amount proposed by Banerjee, Dolado

and Mestera at the expected certainty level, one can understand whether there is a since quite a

while ago run relationship. In the event that a since quite a while ago run connection between

model factors is end up being available, the since quite a while ago run coefficients will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investigated in the subsequent stage, and its worth will be deduced. Presence of Cointegration

between a bunch of financial factors gives a premise to utilizing blunder rectification models

which relate short-run vacillations to since quite a while ago run esteems. In Microfit

programming, there is the likelihood that blunder adjustment model related with it will be

introduced when the since quite a while ago run harmony design identified with the auto

backward conveyed slack was removed. A crucial issue in building up a model which can clarify

the connection among venture and reserve funds is that the reserve funds and speculation relapse

condition can not be declared as a conduct or potentially social condition dependent on

diminished structure from illuminating a framework. Regardless of these issues, to build up an

effective model and accomplish an expected without predisposition, it is important to follow

present day macroeconomic hypotheses. Present day macroeconomic hypotheses respect the

dynamic conduct of the reserve funds and speculation as an impermanent marvel, and accept that

the reserve funds rate and venture rate over the long haul will be adjusted and uniform because

of between period spending requirements.

Blunder amendment models can typically examine the connection among reserve funds and

interest in the most ideal manner. This is basically in accordance with conversations on which

exploration works have centered as of late, to communicate the cointegration connection among

reserve funds and venture. What's more, the blunder amendment model, as a unique condition

with a harmony arrangement, can offer an appropriate response to inquiries concerning the topic.

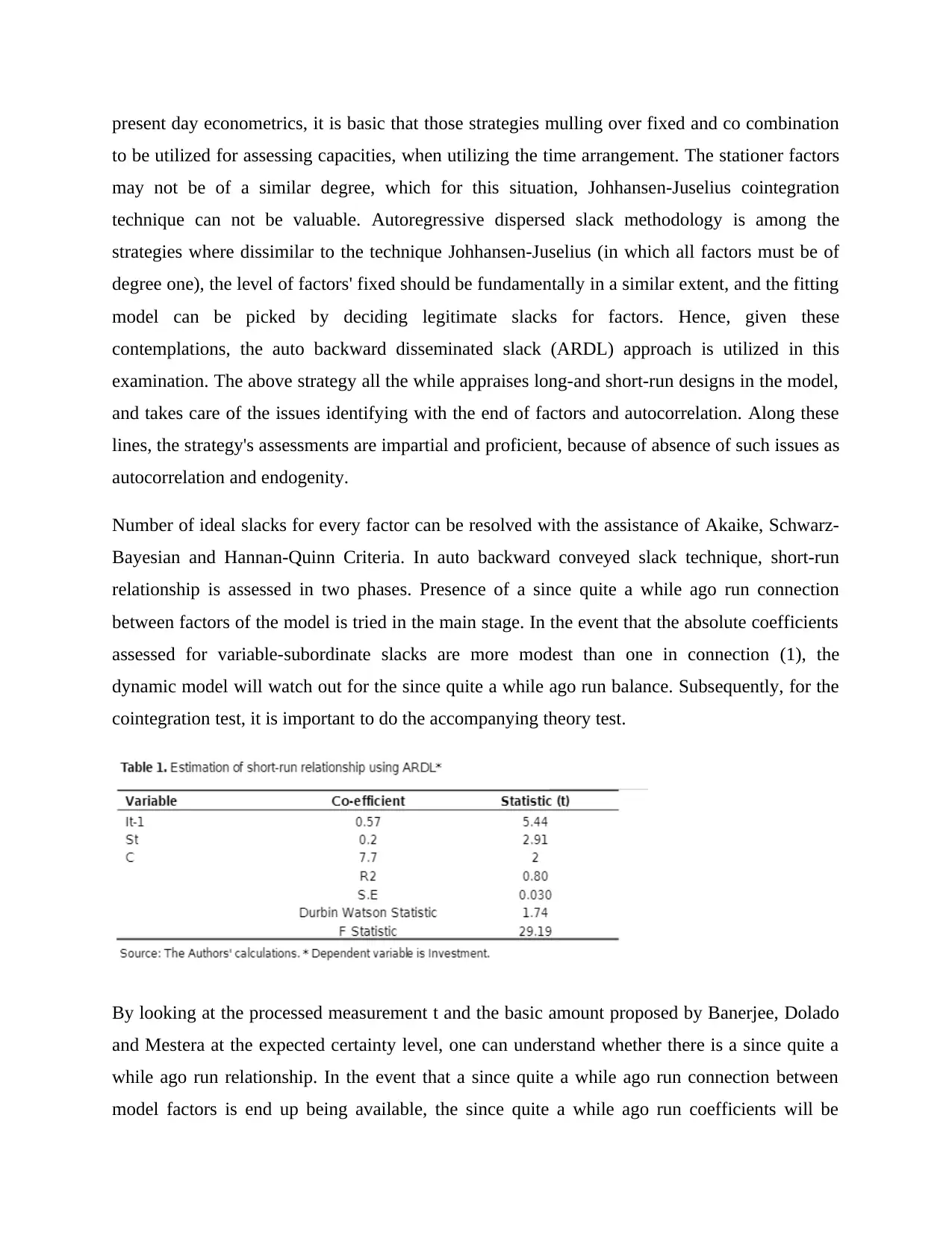

Results and Analysis

In Table 1, data about the aftereffects of assessing the short-run connection among sparing and

interest in Iran has been given autoregressive conveyed slack methodology utilizing Microfit

programming circulation. Since the Schwarz-Bayesian basis will spare in utilizing the quantity of

slacks, it has been utilized to decide the quantity of ideal slacks. The ideal slack of utilizing the

Dickey-Fuller test has been resolved for the factors (Caporale, 2008; Hiro and Chinn, 2008;

Sinha and Sinha, 2009). As per the data of Table 1, the estimation of F measurement is

equivalent to 29.19, inferring absence of inclination to determine the relapse, with mistake

likelihood under 5%. The coefficients of free factors have high t measurement esteems, whose

criticalness is affirmed with the blunder likelihood under 5 percent. It makes sense why the

between a bunch of financial factors gives a premise to utilizing blunder rectification models

which relate short-run vacillations to since quite a while ago run esteems. In Microfit

programming, there is the likelihood that blunder adjustment model related with it will be

introduced when the since quite a while ago run harmony design identified with the auto

backward conveyed slack was removed. A crucial issue in building up a model which can clarify

the connection among venture and reserve funds is that the reserve funds and speculation relapse

condition can not be declared as a conduct or potentially social condition dependent on

diminished structure from illuminating a framework. Regardless of these issues, to build up an

effective model and accomplish an expected without predisposition, it is important to follow

present day macroeconomic hypotheses. Present day macroeconomic hypotheses respect the

dynamic conduct of the reserve funds and speculation as an impermanent marvel, and accept that

the reserve funds rate and venture rate over the long haul will be adjusted and uniform because

of between period spending requirements.

Blunder amendment models can typically examine the connection among reserve funds and

interest in the most ideal manner. This is basically in accordance with conversations on which

exploration works have centered as of late, to communicate the cointegration connection among

reserve funds and venture. What's more, the blunder amendment model, as a unique condition

with a harmony arrangement, can offer an appropriate response to inquiries concerning the topic.

Results and Analysis

In Table 1, data about the aftereffects of assessing the short-run connection among sparing and

interest in Iran has been given autoregressive conveyed slack methodology utilizing Microfit

programming circulation. Since the Schwarz-Bayesian basis will spare in utilizing the quantity of

slacks, it has been utilized to decide the quantity of ideal slacks. The ideal slack of utilizing the

Dickey-Fuller test has been resolved for the factors (Caporale, 2008; Hiro and Chinn, 2008;

Sinha and Sinha, 2009). As per the data of Table 1, the estimation of F measurement is

equivalent to 29.19, inferring absence of inclination to determine the relapse, with mistake

likelihood under 5%. The coefficients of free factors have high t measurement esteems, whose

criticalness is affirmed with the blunder likelihood under 5 percent. It makes sense why the

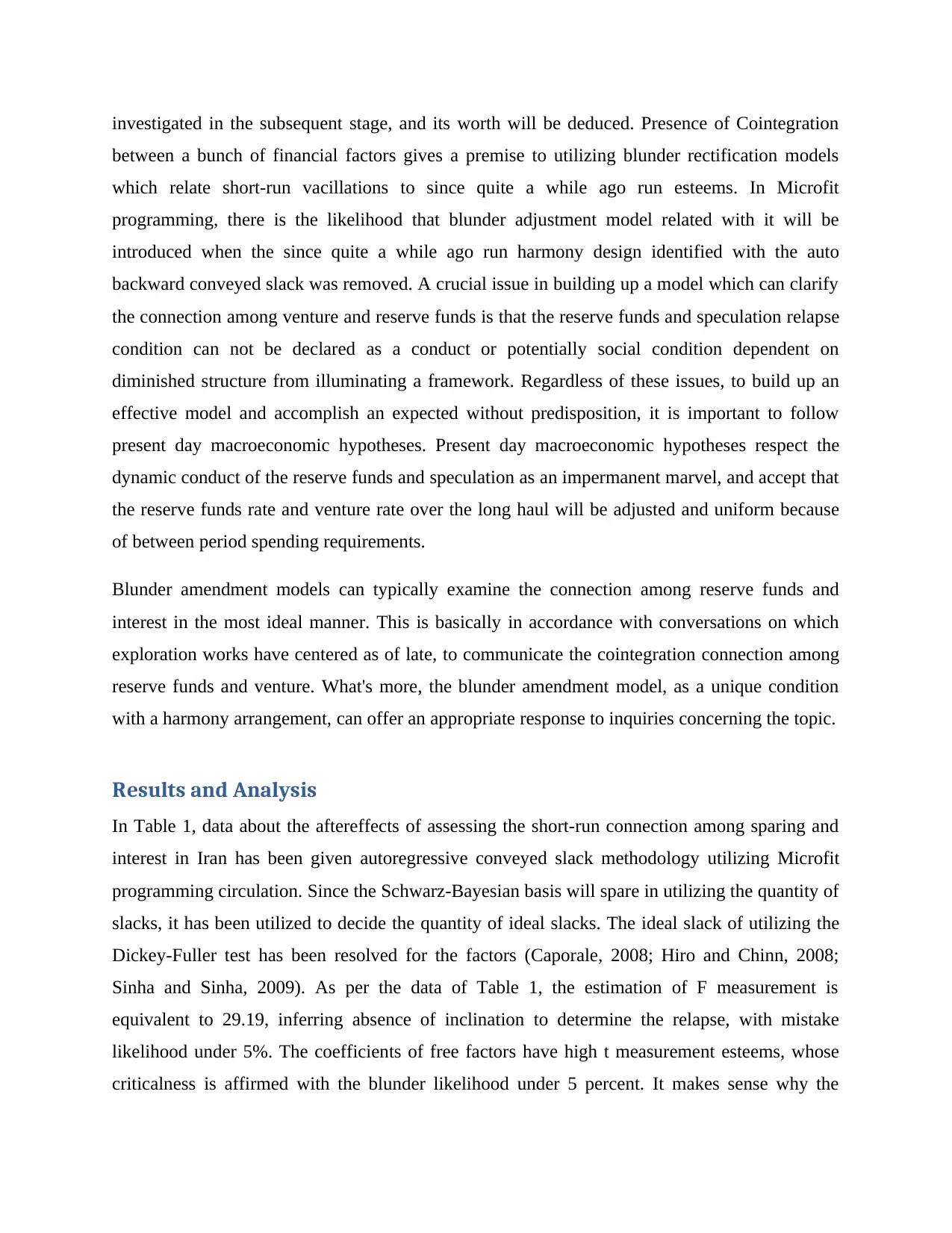

model above is presented as assessment on the short-run connection among venture and sparing

in Iran's economy. Net public sparing and speculation with one-period slack, as can be found in

Table 1, have positive effect on the venture.

After assessment of the dynamic model, presence of a since quite a while ago run connection

between the factors can be tried. Considering the connection 2, the above test measurement is

equivalent to 11.42. Correlation between the processed t measurement (11.42) and the basic

amount proposed by Banerjee, Dolado and Mestera at the certainty level of 95 percent affirms

the theory of since quite a while ago run connection transport (presence of the cointegration)

between model factors. In this way, there will be a since quite a while ago run harmony

connection between the model factors. The consequences of assessing since quite a while ago

run connection between the factors of the proposed model are given in Table 2. As can be seen

from data of the table above, there is a positive connection among's sparing and venture.

Examination of the short-run and since quite a while ago run coefficients shows that relationship

of the two factors over the long haul is higher than that in the short run. The since quite a while

ago run relationship be-tween sparing and interest in Iran's economy gives a premise to the

utilization of blunder amendment model, in which short-run changes are identified with harmony

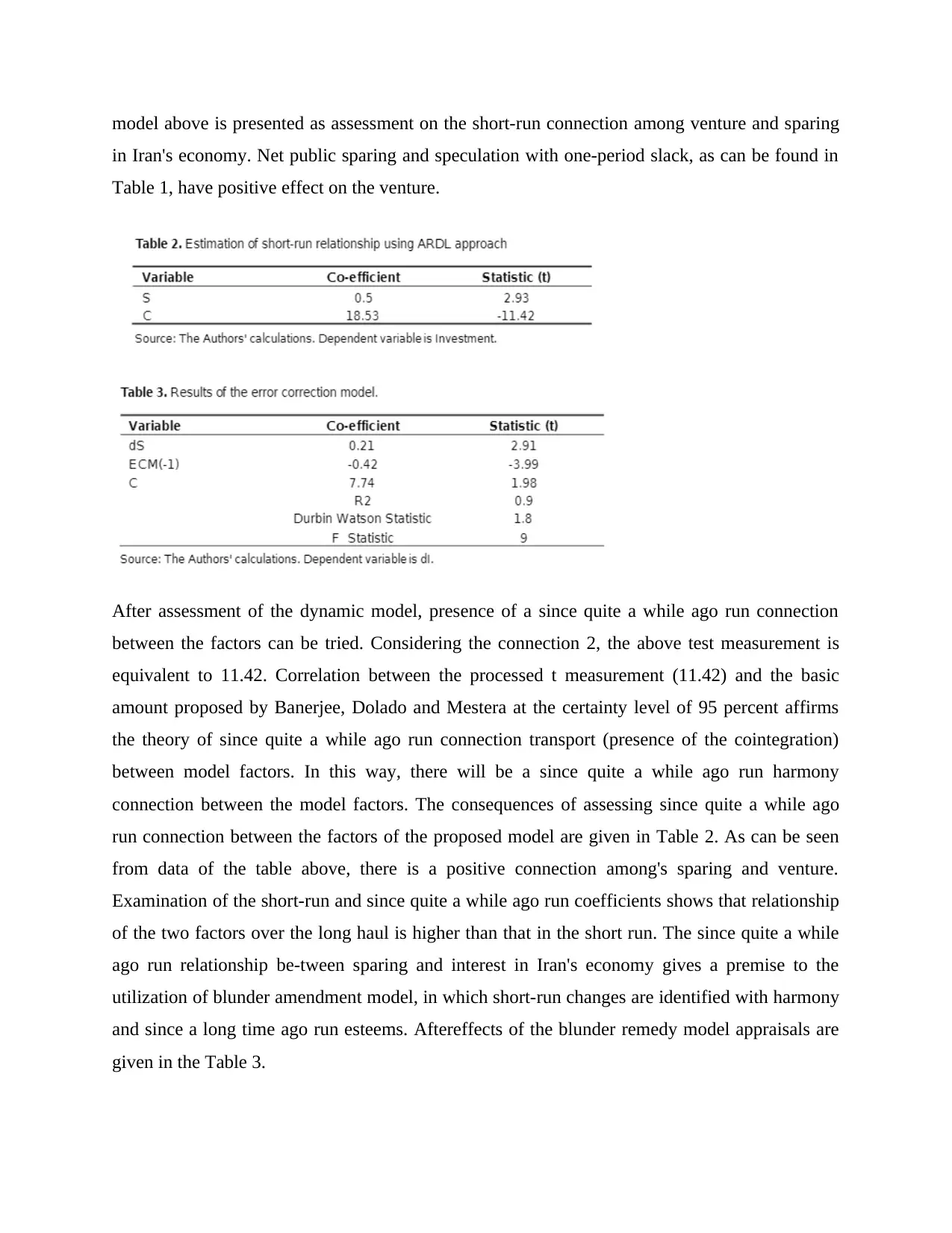

and since a long time ago run esteems. Aftereffects of the blunder remedy model appraisals are

given in the Table 3.

in Iran's economy. Net public sparing and speculation with one-period slack, as can be found in

Table 1, have positive effect on the venture.

After assessment of the dynamic model, presence of a since quite a while ago run connection

between the factors can be tried. Considering the connection 2, the above test measurement is

equivalent to 11.42. Correlation between the processed t measurement (11.42) and the basic

amount proposed by Banerjee, Dolado and Mestera at the certainty level of 95 percent affirms

the theory of since quite a while ago run connection transport (presence of the cointegration)

between model factors. In this way, there will be a since quite a while ago run harmony

connection between the model factors. The consequences of assessing since quite a while ago

run connection between the factors of the proposed model are given in Table 2. As can be seen

from data of the table above, there is a positive connection among's sparing and venture.

Examination of the short-run and since quite a while ago run coefficients shows that relationship

of the two factors over the long haul is higher than that in the short run. The since quite a while

ago run relationship be-tween sparing and interest in Iran's economy gives a premise to the

utilization of blunder amendment model, in which short-run changes are identified with harmony

and since a long time ago run esteems. Aftereffects of the blunder remedy model appraisals are

given in the Table 3.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

All factors, as can be found in Table 3, are factually huge at the certainty level over 95%

Referring to the data of the above table and coefficient ECM, it very well may be seen that in

every period, 42% of uneven characters from short-run stuns are being cleared every year. All in

all, over two years is needed to clear the stun to speculation toward the since quite a while ago

run balance esteems.

Conclusion

In 1960, Feldstein and Horioka fused "capital portability" into the investigation of the connection

among reserve funds and speculation. They demonstrated that equal changes among venture and

sparing really speak to the capital stability. This paper was centered around the connection

among reserve funds and interest in Iran with the autoregressive circulated slack methodology.

This investigation demonstrated that there is a since quite a while ago run balance connection

between the factors above. Sparing has a critical direct impact on gross homegrown venture,

whose since quite a while ago run impact on speculation is more grounded than short-run impact.

Consequently, as reserve funds and venture are adjusted, the speculation of complete capital

fixed status can't be dismissed. Also, coefficient mistake rectification is assessed to be equivalent

- 0.42, showing that 42% of the uneven characters of every period will be gotten comfortable the

following period. Iran's economy has encountered significant variances in financial development

and gross homegrown speculation, particularly during the past 50 years. Along these lines,

clearly improving the above pointers is considered as the main targets of financial policymakers

and organizers. For this reason, it appears to be that more utilization of unfamiliar financing

assets, particularly in activities requiring unfamiliar trade assets and innovation imports, can be

relied upon to prompt steadiness of different variables, greater ability for flexibly of merchandise

and expansion underway.

Referring to the data of the above table and coefficient ECM, it very well may be seen that in

every period, 42% of uneven characters from short-run stuns are being cleared every year. All in

all, over two years is needed to clear the stun to speculation toward the since quite a while ago

run balance esteems.

Conclusion

In 1960, Feldstein and Horioka fused "capital portability" into the investigation of the connection

among reserve funds and speculation. They demonstrated that equal changes among venture and

sparing really speak to the capital stability. This paper was centered around the connection

among reserve funds and interest in Iran with the autoregressive circulated slack methodology.

This investigation demonstrated that there is a since quite a while ago run balance connection

between the factors above. Sparing has a critical direct impact on gross homegrown venture,

whose since quite a while ago run impact on speculation is more grounded than short-run impact.

Consequently, as reserve funds and venture are adjusted, the speculation of complete capital

fixed status can't be dismissed. Also, coefficient mistake rectification is assessed to be equivalent

- 0.42, showing that 42% of the uneven characters of every period will be gotten comfortable the

following period. Iran's economy has encountered significant variances in financial development

and gross homegrown speculation, particularly during the past 50 years. Along these lines,

clearly improving the above pointers is considered as the main targets of financial policymakers

and organizers. For this reason, it appears to be that more utilization of unfamiliar financing

assets, particularly in activities requiring unfamiliar trade assets and innovation imports, can be

relied upon to prompt steadiness of different variables, greater ability for flexibly of merchandise

and expansion underway.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Bassam AF (2004). The Relationship between Savings and Investment in MENA Countries.

American University of Sharjah.

Caporale GM (2008). The Feldstein-Horioka Puzzle Revisited: A Monte Carlo Study. Nikitas

Pittis University of Piraeus.

Fabiana R (2000). Capital Mobility in Developing Countries: evidence from Panel Data.

Universidad de São Paulo Department of Economics.

Feldstein M, Horioka C (1980). Domestic saving and international capital flows. Econ. J.,

90: 314–329.

Hiro I, Chinn M (2008). East Asia and Global Imbalances: Saving, Investment, and

Financial Development. University of Wisconsin and NBER February 29.

Jansen W (2000). International Capital Mobility: Evidence from Panel Data. Monetary and

Economic Policy Department, De Nederlandsche Bank, P.O. Box 98, 1000 AB Amsterdam,

Netherlands. Kim SH (1999). The Saving-Investment Correlation Puzzle is Still a Puzzle.

Brandeis University. Miller SM (1988). Are saving and investment co-integrated? Econ. Lett. 27:

31–34.

Bassam AF (2004). The Relationship between Savings and Investment in MENA Countries.

American University of Sharjah.

Caporale GM (2008). The Feldstein-Horioka Puzzle Revisited: A Monte Carlo Study. Nikitas

Pittis University of Piraeus.

Fabiana R (2000). Capital Mobility in Developing Countries: evidence from Panel Data.

Universidad de São Paulo Department of Economics.

Feldstein M, Horioka C (1980). Domestic saving and international capital flows. Econ. J.,

90: 314–329.

Hiro I, Chinn M (2008). East Asia and Global Imbalances: Saving, Investment, and

Financial Development. University of Wisconsin and NBER February 29.

Jansen W (2000). International Capital Mobility: Evidence from Panel Data. Monetary and

Economic Policy Department, De Nederlandsche Bank, P.O. Box 98, 1000 AB Amsterdam,

Netherlands. Kim SH (1999). The Saving-Investment Correlation Puzzle is Still a Puzzle.

Brandeis University. Miller SM (1988). Are saving and investment co-integrated? Econ. Lett. 27:

31–34.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.