ECON6000: Comparative Analysis of FHOG and FHP in Australia

VerifiedAdded on 2022/08/16

|14

|3662

|10

Report

AI Summary

This report provides a comprehensive analysis of the First Home Owners Grant (FHOG) and First Home Plus (FHP) schemes in Australia, comparing and contrasting their eligibility requirements, similarities, and differences. It evaluates the impact of FHOG on demand and supply patterns across Australia's states and territories, discussing its influence on the price elasticity of demand in the housing market. The report also examines the market structure under which FHOG operates and provides a critical discussion of related economic policies, such as stamp duties. The analysis aims to determine which scheme is more beneficial and suitable for the Australian property market, providing valuable insights into government policies and their effects on the housing sector. The report uses diagrams and academic references to support its findings, offering a detailed examination of the microeconomic principles at play.

Running head: FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

First Home Owners Grant and First Home Plus in Australia

Name of the Student

Name of the University

Student ID

First Home Owners Grant and First Home Plus in Australia

Name of the Student

Name of the University

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

Executive Summary

The report discussed about the schemes of the government of Australia that are meant for

providing monetary benefit to the first home buyers. The schemes that are discussed in this

report are First Home Owners Grant and First House Plus. Making a comparative study of the

two schemes, the report showed that FHOG is more beneficial in case of direct monetary benefit.

Conversely, FHP is more inclusive and provides concessional benefit to all. Introduction of

FHOG increased the demand in the housing market and since price elasticity of demand of

homes are greater than 1 increase demand was higher than the fall in price. The market structure

of housing market is more like monopoly. It is further found from the statement of Ken Henry

that stamp duty is more like hurdle for the youth and an annual house tax would be more

beneficial for youth first home buyers and housing market as well.

Executive Summary

The report discussed about the schemes of the government of Australia that are meant for

providing monetary benefit to the first home buyers. The schemes that are discussed in this

report are First Home Owners Grant and First House Plus. Making a comparative study of the

two schemes, the report showed that FHOG is more beneficial in case of direct monetary benefit.

Conversely, FHP is more inclusive and provides concessional benefit to all. Introduction of

FHOG increased the demand in the housing market and since price elasticity of demand of

homes are greater than 1 increase demand was higher than the fall in price. The market structure

of housing market is more like monopoly. It is further found from the statement of Ken Henry

that stamp duty is more like hurdle for the youth and an annual house tax would be more

beneficial for youth first home buyers and housing market as well.

2FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

Table of Contents

Introduction......................................................................................................................................3

Contrast between FHOG and FHP..................................................................................................3

First Home Owners Grant............................................................................................................3

First Home Plus...........................................................................................................................5

Comparison between FHOG and FHP........................................................................................5

Impact of FHOG..............................................................................................................................6

Market structure of the industry in which FHOG falls....................................................................8

Unfair property pricing....................................................................................................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

Contrast between FHOG and FHP..................................................................................................3

First Home Owners Grant............................................................................................................3

First Home Plus...........................................................................................................................5

Comparison between FHOG and FHP........................................................................................5

Impact of FHOG..............................................................................................................................6

Market structure of the industry in which FHOG falls....................................................................8

Unfair property pricing....................................................................................................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

Introduction

First Home Owners Grant (FHOG) and First Home Plus (FHP) are the schemes that

provide grant and concessions to first home buyers in Australia. Mentioned two schemes are

however different from each other. Under FHOG the grant is given to the first home buyers only

if the home bought is a newly established property (First Home Owner Grant, 2020). A first

home buyer is not eligible for the grant if the property bought is not new. However, for FHP

there is no such eligibility requirement of new property purchase (First home plus, 2020). This

report discusses and compares the two mentioned schemes for first home buyers. The

comparison that is to be done in the report is based on eligibility requirements and structural

similarities and differences between the two schemes. In addition to that, the report discusses the

impact on the supply and the demand patterns of homes in the six states and the Northern

Territory in the country. By analysis of price elasticity of demand of the home property market in

Australia, the report focuses on the influence of FHOG scheme on the concerned market.

Discussing all the above areas related to FHOG and the market structure of property market will

be explained in the report. Finally, the report provides a critical discussion on the statement

related to stamp duties on property purchases made by Ken Henry. The report thus aims to

discuss the policies of FHOG and FHP and try to find out which one is more suitable and should

be followed in order to have a balanced property market.

Contrast between FHOG and FHP

First Home Owners Grant

FHOG is a scheme that provides first home buyers a grant of up to $10, 000 in order to

encourage and the buyers to build or buy new residential property (La Cava, Leal, & Zurawski,

2017). It should be noted that a transaction made for purchase of a new residential property is

Introduction

First Home Owners Grant (FHOG) and First Home Plus (FHP) are the schemes that

provide grant and concessions to first home buyers in Australia. Mentioned two schemes are

however different from each other. Under FHOG the grant is given to the first home buyers only

if the home bought is a newly established property (First Home Owner Grant, 2020). A first

home buyer is not eligible for the grant if the property bought is not new. However, for FHP

there is no such eligibility requirement of new property purchase (First home plus, 2020). This

report discusses and compares the two mentioned schemes for first home buyers. The

comparison that is to be done in the report is based on eligibility requirements and structural

similarities and differences between the two schemes. In addition to that, the report discusses the

impact on the supply and the demand patterns of homes in the six states and the Northern

Territory in the country. By analysis of price elasticity of demand of the home property market in

Australia, the report focuses on the influence of FHOG scheme on the concerned market.

Discussing all the above areas related to FHOG and the market structure of property market will

be explained in the report. Finally, the report provides a critical discussion on the statement

related to stamp duties on property purchases made by Ken Henry. The report thus aims to

discuss the policies of FHOG and FHP and try to find out which one is more suitable and should

be followed in order to have a balanced property market.

Contrast between FHOG and FHP

First Home Owners Grant

FHOG is a scheme that provides first home buyers a grant of up to $10, 000 in order to

encourage and the buyers to build or buy new residential property (La Cava, Leal, & Zurawski,

2017). It should be noted that a transaction made for purchase of a new residential property is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

eligible for one grant only irrespective of the number of purchasers. It means that if three persons

together buy their first home then they will receive a single grant as the number of purchase of

new residential property is one. Purchase of an already established property even if it is the first

home for the buyer is not eligible for the grant. The eligibility requirements of FHOG are:

The applicant must be above 18 years during the time of application submission.

However, exemption is of this requirement is made on submission of application with

valid reasons.

Only a citizen or permanent residence of Australia is eligible for the grant.

The purchased home should be the primary residence and the buyer must stay there for at

least six months within a year from the date of purchase or completion of building of

home.

A person has to apply for the grant within 1 year of completion of transaction or building

of home.

Other eligibility conditions

FHOG provides the boost payment facilities for the buyers that made purchase contract

between 1st January and 30th June 2017. However, there are various terms and conditions, which

a buyer should meet in order to get the facility (First home owner grant, 2020). Any contract,

starting of building a home and purchase of home should be conducted on or after 1st July 2000

in order to be an eligible transaction for FHOG. The value of transactions are important for the

grant as there is cap on the value. Transactions within the capped value are eligible for the grant.

Value of properties south of the 26th parallel including land of are capped to $750, 000 and

properties north of the 26th parallel are capped at $1, 000, 000. Therefore, to avail the First Home

Owners Grant a buyer need to fulfil all of the above discussed eligibility criteria.

eligible for one grant only irrespective of the number of purchasers. It means that if three persons

together buy their first home then they will receive a single grant as the number of purchase of

new residential property is one. Purchase of an already established property even if it is the first

home for the buyer is not eligible for the grant. The eligibility requirements of FHOG are:

The applicant must be above 18 years during the time of application submission.

However, exemption is of this requirement is made on submission of application with

valid reasons.

Only a citizen or permanent residence of Australia is eligible for the grant.

The purchased home should be the primary residence and the buyer must stay there for at

least six months within a year from the date of purchase or completion of building of

home.

A person has to apply for the grant within 1 year of completion of transaction or building

of home.

Other eligibility conditions

FHOG provides the boost payment facilities for the buyers that made purchase contract

between 1st January and 30th June 2017. However, there are various terms and conditions, which

a buyer should meet in order to get the facility (First home owner grant, 2020). Any contract,

starting of building a home and purchase of home should be conducted on or after 1st July 2000

in order to be an eligible transaction for FHOG. The value of transactions are important for the

grant as there is cap on the value. Transactions within the capped value are eligible for the grant.

Value of properties south of the 26th parallel including land of are capped to $750, 000 and

properties north of the 26th parallel are capped at $1, 000, 000. Therefore, to avail the First Home

Owners Grant a buyer need to fulfil all of the above discussed eligibility criteria.

5FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

First Home Plus

First Home Plus scheme was launched after many years of introduction of First Home

Owners Grant. Under this scheme, concession is given on the transfer duty. First home buyers

are eligible for the concession irrespective of category of property that is new and established.

The eligibility criteria for availing FHP scheme are as follows.

The buyer have to be over 18 years of age.

Purchase of the property must be done by an individual.

A whole property should be purchased in order to avail the scheme.

Buyer of property should be a citizen of Australia or a permanent resident of the country.

Other eligibility conditions

First home buyers who purchased a property after 21st October 2009 are eligible for FHP.

There are exceptions for the buyers who are member of Australian Defence Force. A buyer who

wish to purchase a new home and is willing to avail FHP then he or she should not be co-owner

of a home in the country and must not have received the benefit of FHP earlier. The buyer must

shift into the new home within 1 year from the date of purchase or completion building of home.

The amount paid for the purchase or building of home determines the amount of transfer duty

that is to be paid by the buyer.

Comparison between FHOG and FHP

FHOG and FHP are both government schemes that aims to assist first home buyers to

buy their first home. Two schemes are similar to each other in various areas and are different in

many other areas too (Coates & Nolan, 2019). The basic criteria of both the schemes are similar

that is the age and citizenship criteria. In case of FHP whole property needed to be purchased

First Home Plus

First Home Plus scheme was launched after many years of introduction of First Home

Owners Grant. Under this scheme, concession is given on the transfer duty. First home buyers

are eligible for the concession irrespective of category of property that is new and established.

The eligibility criteria for availing FHP scheme are as follows.

The buyer have to be over 18 years of age.

Purchase of the property must be done by an individual.

A whole property should be purchased in order to avail the scheme.

Buyer of property should be a citizen of Australia or a permanent resident of the country.

Other eligibility conditions

First home buyers who purchased a property after 21st October 2009 are eligible for FHP.

There are exceptions for the buyers who are member of Australian Defence Force. A buyer who

wish to purchase a new home and is willing to avail FHP then he or she should not be co-owner

of a home in the country and must not have received the benefit of FHP earlier. The buyer must

shift into the new home within 1 year from the date of purchase or completion building of home.

The amount paid for the purchase or building of home determines the amount of transfer duty

that is to be paid by the buyer.

Comparison between FHOG and FHP

FHOG and FHP are both government schemes that aims to assist first home buyers to

buy their first home. Two schemes are similar to each other in various areas and are different in

many other areas too (Coates & Nolan, 2019). The basic criteria of both the schemes are similar

that is the age and citizenship criteria. In case of FHP whole property needed to be purchased

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

which is not the case with FHOG. The major difference between the two schemes is the kind of

monetary benefit given to the first home buyers. In FHOG, the first home buyers are provided

with the lump sum monetary benefit of up to $ 10, 000 depending on the value of property

purchased. Alternatively, in the case of FHP the benefit is given by providing concession on

transfer duty only. The buyers have an advantage in availing FHP as the benefit under the

scheme is applicable for purchase of new homes and existing homes. Therefore, in the case of

FHP all the first home buyers get the benefit. However, from the business perspective of the

property market FHP is not very effective since there is no special incentive for the new home

buyers and thus it does not encourages building of new homes. FHOG is effective for the growth

of property market as it encourages purchase of new homes and thereby causes to increase

investment in the property market (Mangioni, 2017). Therefore, FHOG is more suitable policy

than FHP and the government of Australia should follow the policy.

Impact of FHOG

First Home Owners Grant is a scheme under which the first home buyers are provided

monetary for their purchase. It is done with the objective of encouraging buyers to purchase new

homes such that the housing market in the country improves (Murray, 2019). After the launch of

FHOG, there was sudden increase in the demand for the new homes in the country. The rise in

demand for the new homes increased and that was the reason due to which the price of new

homes increased in Australian states (Wong et al., 2018). Even though the FHOG is aimed to

provide the first home buyers benefits, the buyers residing in different states had so far enjoyed

the benefits but the amount has been different since the amount of grant provided under FHOG

was different for different states. The demand for new homes depends on the grant provided by

the respective states. The effective price is highly dependent on the grant as the buyers need to

which is not the case with FHOG. The major difference between the two schemes is the kind of

monetary benefit given to the first home buyers. In FHOG, the first home buyers are provided

with the lump sum monetary benefit of up to $ 10, 000 depending on the value of property

purchased. Alternatively, in the case of FHP the benefit is given by providing concession on

transfer duty only. The buyers have an advantage in availing FHP as the benefit under the

scheme is applicable for purchase of new homes and existing homes. Therefore, in the case of

FHP all the first home buyers get the benefit. However, from the business perspective of the

property market FHP is not very effective since there is no special incentive for the new home

buyers and thus it does not encourages building of new homes. FHOG is effective for the growth

of property market as it encourages purchase of new homes and thereby causes to increase

investment in the property market (Mangioni, 2017). Therefore, FHOG is more suitable policy

than FHP and the government of Australia should follow the policy.

Impact of FHOG

First Home Owners Grant is a scheme under which the first home buyers are provided

monetary for their purchase. It is done with the objective of encouraging buyers to purchase new

homes such that the housing market in the country improves (Murray, 2019). After the launch of

FHOG, there was sudden increase in the demand for the new homes in the country. The rise in

demand for the new homes increased and that was the reason due to which the price of new

homes increased in Australian states (Wong et al., 2018). Even though the FHOG is aimed to

provide the first home buyers benefits, the buyers residing in different states had so far enjoyed

the benefits but the amount has been different since the amount of grant provided under FHOG

was different for different states. The demand for new homes depends on the grant provided by

the respective states. The effective price is highly dependent on the grant as the buyers need to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

pay the amount for homes given by the difference between the actual price of new homes and

grant provided. According to microeconomic theory of demand and supply, it is known that these

two factors are dependent on price (Shi, Rahman & Wang, 2019). FHOG in different states is

different and thus effective price of new homes is different too. In NSW, the grant provided to

the first home buyers can go up to $ 15, 000. In case of Queensland the amount of much higher

which is up to $ 20, 000. In South Australia, the amount of grant is same as NSW which is $ 15,

000 (Gurran & Phibbs, 2017). However, unlike NSW, South Australia do not have the grant

amount option of $ 10, 000. It has only one grant amount. For all the other states that are

Northern Territory, Victoria and Western Australia the grant given to the first home buyers is $

10, 000, only the Australian Capital Territory has the lowest grant (Valadkhani & Smyth, 2017).

The grant provided by Australian Capital Territory is $ 7, 000. Therefore, it is evident that the

demand for new homes will be highest in the states where the effective price is the lowest.

Corresponding to the increased demand for new homes the supply of homes will increase too in

the concerned states of the country.

Home is luxury product because they are highly expensive. The change in price thus

affect the demand for homes significantly. For luxury goods, the price elasticity of demand is

greater than 1, indicating that the demand is relatively elastic (Popova, 2017). Price elasticity of

demand measures the amount of change in quantity demanded in response to the change in price

of the product. For relatively price elastic products, demand decreases by more than

proportionate change in price. It means that due to 1% increase in price the demand for goods

will decrease by more than 1% (Becker, 2017). Similarly, with fall in 1% price the demand will

increase by more than 1%. Therefore, it can be said that the effective price of homes has

decreased in Australia after launch of FHOG and thus due to effect of price elasticity the demand

pay the amount for homes given by the difference between the actual price of new homes and

grant provided. According to microeconomic theory of demand and supply, it is known that these

two factors are dependent on price (Shi, Rahman & Wang, 2019). FHOG in different states is

different and thus effective price of new homes is different too. In NSW, the grant provided to

the first home buyers can go up to $ 15, 000. In case of Queensland the amount of much higher

which is up to $ 20, 000. In South Australia, the amount of grant is same as NSW which is $ 15,

000 (Gurran & Phibbs, 2017). However, unlike NSW, South Australia do not have the grant

amount option of $ 10, 000. It has only one grant amount. For all the other states that are

Northern Territory, Victoria and Western Australia the grant given to the first home buyers is $

10, 000, only the Australian Capital Territory has the lowest grant (Valadkhani & Smyth, 2017).

The grant provided by Australian Capital Territory is $ 7, 000. Therefore, it is evident that the

demand for new homes will be highest in the states where the effective price is the lowest.

Corresponding to the increased demand for new homes the supply of homes will increase too in

the concerned states of the country.

Home is luxury product because they are highly expensive. The change in price thus

affect the demand for homes significantly. For luxury goods, the price elasticity of demand is

greater than 1, indicating that the demand is relatively elastic (Popova, 2017). Price elasticity of

demand measures the amount of change in quantity demanded in response to the change in price

of the product. For relatively price elastic products, demand decreases by more than

proportionate change in price. It means that due to 1% increase in price the demand for goods

will decrease by more than 1% (Becker, 2017). Similarly, with fall in 1% price the demand will

increase by more than 1%. Therefore, it can be said that the effective price of homes has

decreased in Australia after launch of FHOG and thus due to effect of price elasticity the demand

8FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

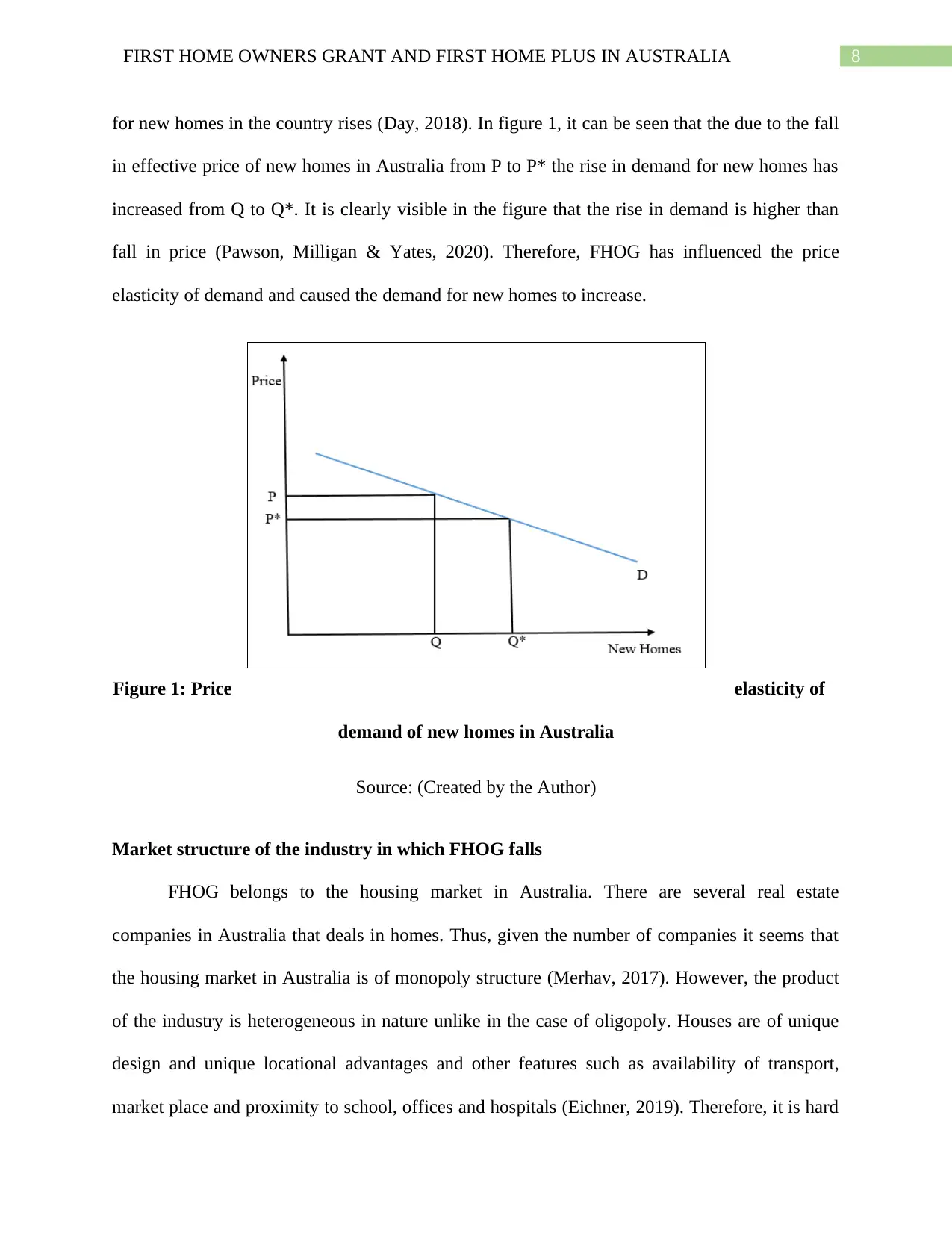

for new homes in the country rises (Day, 2018). In figure 1, it can be seen that the due to the fall

in effective price of new homes in Australia from P to P* the rise in demand for new homes has

increased from Q to Q*. It is clearly visible in the figure that the rise in demand is higher than

fall in price (Pawson, Milligan & Yates, 2020). Therefore, FHOG has influenced the price

elasticity of demand and caused the demand for new homes to increase.

Figure 1: Price elasticity of

demand of new homes in Australia

Source: (Created by the Author)

Market structure of the industry in which FHOG falls

FHOG belongs to the housing market in Australia. There are several real estate

companies in Australia that deals in homes. Thus, given the number of companies it seems that

the housing market in Australia is of monopoly structure (Merhav, 2017). However, the product

of the industry is heterogeneous in nature unlike in the case of oligopoly. Houses are of unique

design and unique locational advantages and other features such as availability of transport,

market place and proximity to school, offices and hospitals (Eichner, 2019). Therefore, it is hard

for new homes in the country rises (Day, 2018). In figure 1, it can be seen that the due to the fall

in effective price of new homes in Australia from P to P* the rise in demand for new homes has

increased from Q to Q*. It is clearly visible in the figure that the rise in demand is higher than

fall in price (Pawson, Milligan & Yates, 2020). Therefore, FHOG has influenced the price

elasticity of demand and caused the demand for new homes to increase.

Figure 1: Price elasticity of

demand of new homes in Australia

Source: (Created by the Author)

Market structure of the industry in which FHOG falls

FHOG belongs to the housing market in Australia. There are several real estate

companies in Australia that deals in homes. Thus, given the number of companies it seems that

the housing market in Australia is of monopoly structure (Merhav, 2017). However, the product

of the industry is heterogeneous in nature unlike in the case of oligopoly. Houses are of unique

design and unique locational advantages and other features such as availability of transport,

market place and proximity to school, offices and hospitals (Eichner, 2019). Therefore, it is hard

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

to find substitute of a particular house depending on the factors mentioned above. Each house is

unique in characteristics and is sold by a single company or seller. This is the reason companies

could charge price as per their wish and a buyer with similar demand preferences and tastes have

to take the price. Thus, it can be said that housing market in a particular area is dominated by a

single company giving rise to monopoly structure in the market. The fixed cost associated with

the housing market is very high (Laszek, Olszewski & Waszczuk, 2016). The major factor of

production of houses is land which is exclusive and unique and cannot be used by more than one

company for development of houses. Therefore, a company enjoys monopoly power for its own

product and charges high price. There is complete restrictions to entry and exit and the

companies operating in the industry earn supernormal profit (Geltner, Kumar & Van de Minne,

2019). It should be noted that all the companies that enjoy monopoly in their region completely

free of any future threat from new companies because of the land factor. There is no substitute of

land. It is the main reason due to which the FHOG benefit provided to the first home buyers is

different in different states in Australia. It can be inferred that with several number of companies

operating in the housing market in Australia, the companies are in monopoly market structure

due to the characteristics of the product.

Unfair property pricing

The statement made by Ken Henry gives the notion that stamp duties creates a hurdle for

the youths willing to buy new homes. It is difficult for youths to pay such duties upfront because

savings for the payment for new home and then again for the stamp duty increases the burden

(Liang, 2018). Stamp duty along with burden increases the effective price of property and that

discourages the buyers from buying new home. It has negative impact on the housing market as

well since buyers judge the price of buying a new home including the stamp duty since the both

to find substitute of a particular house depending on the factors mentioned above. Each house is

unique in characteristics and is sold by a single company or seller. This is the reason companies

could charge price as per their wish and a buyer with similar demand preferences and tastes have

to take the price. Thus, it can be said that housing market in a particular area is dominated by a

single company giving rise to monopoly structure in the market. The fixed cost associated with

the housing market is very high (Laszek, Olszewski & Waszczuk, 2016). The major factor of

production of houses is land which is exclusive and unique and cannot be used by more than one

company for development of houses. Therefore, a company enjoys monopoly power for its own

product and charges high price. There is complete restrictions to entry and exit and the

companies operating in the industry earn supernormal profit (Geltner, Kumar & Van de Minne,

2019). It should be noted that all the companies that enjoy monopoly in their region completely

free of any future threat from new companies because of the land factor. There is no substitute of

land. It is the main reason due to which the FHOG benefit provided to the first home buyers is

different in different states in Australia. It can be inferred that with several number of companies

operating in the housing market in Australia, the companies are in monopoly market structure

due to the characteristics of the product.

Unfair property pricing

The statement made by Ken Henry gives the notion that stamp duties creates a hurdle for

the youths willing to buy new homes. It is difficult for youths to pay such duties upfront because

savings for the payment for new home and then again for the stamp duty increases the burden

(Liang, 2018). Stamp duty along with burden increases the effective price of property and that

discourages the buyers from buying new home. It has negative impact on the housing market as

well since buyers judge the price of buying a new home including the stamp duty since the both

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

the payments needed to be paid up front. Therefore, demand for new homes might fall due this

imposition of stamp duty. The government can use an alternative way of collecting revenue from

sale if new homes. Imposition of annual tax for a certain period for example 10 years or 15 years

whatever is suitable to collect the money equivalent to the money the government would have

collected from stamp duty in real terms. Annual house tax will lower the monetary burden on the

youth and they will be able to purchase new home with ease (Cho, Li & Uren, 2019). It should

be noted that the aggregate amount of annual house tax will be higher than the onetime payment

of stamp duty. It is because of the annual house tax is to be inflated to make the tax amount equal

to the stamp duty in real terms otherwise the government would loss revenue. Thus, it can be

said that stamp duty is really a hurdle for the youths willing to buy new home.

Conclusion

The above discussion on the FHOG and FHP leads to the conclusion that in direct benefit

part FHOG is better than FHP since it does not depend on the rate of transfer duty. Conversely,

FHP is better in inclusiveness as it provides concessional benefit to all the first home buyers

irrespective of the type of purchase that is new home or renovated home. Impact of FHOG on the

housing market is beneficial as it increased the demand for new homes. With rise in demand, the

price of new homes increased and thereby supply increased. Increased demand expanded the

housing sector. Homes are luxury products and thus the demand is relatively price elastic and

with rise in price the demand falls more than the proportionate rise in price and vice versa. It is

evident from the discussion about the market that the structure is close to monopoly as the

companies operating enjoy monopoly power in their respective region of operation. Finally, from

the statement of Ken Henry it can be understood that the stamp duty imposes burden on the

the payments needed to be paid up front. Therefore, demand for new homes might fall due this

imposition of stamp duty. The government can use an alternative way of collecting revenue from

sale if new homes. Imposition of annual tax for a certain period for example 10 years or 15 years

whatever is suitable to collect the money equivalent to the money the government would have

collected from stamp duty in real terms. Annual house tax will lower the monetary burden on the

youth and they will be able to purchase new home with ease (Cho, Li & Uren, 2019). It should

be noted that the aggregate amount of annual house tax will be higher than the onetime payment

of stamp duty. It is because of the annual house tax is to be inflated to make the tax amount equal

to the stamp duty in real terms otherwise the government would loss revenue. Thus, it can be

said that stamp duty is really a hurdle for the youths willing to buy new home.

Conclusion

The above discussion on the FHOG and FHP leads to the conclusion that in direct benefit

part FHOG is better than FHP since it does not depend on the rate of transfer duty. Conversely,

FHP is better in inclusiveness as it provides concessional benefit to all the first home buyers

irrespective of the type of purchase that is new home or renovated home. Impact of FHOG on the

housing market is beneficial as it increased the demand for new homes. With rise in demand, the

price of new homes increased and thereby supply increased. Increased demand expanded the

housing sector. Homes are luxury products and thus the demand is relatively price elastic and

with rise in price the demand falls more than the proportionate rise in price and vice versa. It is

evident from the discussion about the market that the structure is close to monopoly as the

companies operating enjoy monopoly power in their respective region of operation. Finally, from

the statement of Ken Henry it can be understood that the stamp duty imposes burden on the

11FIRST HOME OWNERS GRANT AND FIRST HOME PLUS IN AUSTRALIA

youth buyers and affects the housing market adversely. It is better to have annual house tax

instead of stamp duty.

Reference

Cho, Y., Li, S. M., & Uren, L. (2019). Investment Housing Tax Concessions and Welfare:

Evidence from Australia.

Coates, B., & Nolan, J. (2019). Submission to Inquiry into the National Housing Finance and

Investment Corporation Amendment Bill 2019.

Day, C. (2018). Australia's growth in households and house prices. Australian Economic

Review, 51(4), 502-511.

Eichner, A. S. (2019). The Emergence of Oligopoly: Sugar refining as a case study. JHU Press.

First Home Owner Grant. (2020). Firsthome.gov.au. Retrieved 6 March 2020, from

http://www.firsthome.gov.au/

First home owner grant. (2020). Revenue NSW. Retrieved from

https://www.revenue.nsw.gov.au/grants-schemes/previous-schemes/first-home-owner-

grant

First home plus. (2020). Revenue NSW. Retrieved from https://www.revenue.nsw.gov.au/grants-

schemes/previous-schemes/first-home-plus

Geltner, D., Kumar, A., & Van de Minne, A. (2019). Super-Normal Profit in Real Estate

Development. Available at SSRN 3444309.

youth buyers and affects the housing market adversely. It is better to have annual house tax

instead of stamp duty.

Reference

Cho, Y., Li, S. M., & Uren, L. (2019). Investment Housing Tax Concessions and Welfare:

Evidence from Australia.

Coates, B., & Nolan, J. (2019). Submission to Inquiry into the National Housing Finance and

Investment Corporation Amendment Bill 2019.

Day, C. (2018). Australia's growth in households and house prices. Australian Economic

Review, 51(4), 502-511.

Eichner, A. S. (2019). The Emergence of Oligopoly: Sugar refining as a case study. JHU Press.

First Home Owner Grant. (2020). Firsthome.gov.au. Retrieved 6 March 2020, from

http://www.firsthome.gov.au/

First home owner grant. (2020). Revenue NSW. Retrieved from

https://www.revenue.nsw.gov.au/grants-schemes/previous-schemes/first-home-owner-

grant

First home plus. (2020). Revenue NSW. Retrieved from https://www.revenue.nsw.gov.au/grants-

schemes/previous-schemes/first-home-plus

Geltner, D., Kumar, A., & Van de Minne, A. (2019). Super-Normal Profit in Real Estate

Development. Available at SSRN 3444309.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.