Project: FIN 3020 Winter 2020 - Rosy Evans 2019 Tax Return Analysis

VerifiedAdded on 2022/07/29

|54

|29338

|19

Homework Assignment

AI Summary

This document presents a comprehensive analysis of Rosy Evans' 2019 Canadian Income Tax and Benefit Return. The assignment involves completing the tax return based on the provided client information, including personal details, employment income, and rental property income. Rosy Evans, a single chef, owns a rental property with six units, and the analysis includes calculating rental income, expenses (hydro, water, gas, mortgage, property taxes, maintenance, insurance, and management fees), and net rental income. Additionally, the assignment considers other income sources such as taxable scholarships and addresses the relevant deductions. The solution demonstrates the steps to determine the total income, net income, and taxable income, leading to the final tax liability or refund calculation. The document provides a detailed breakdown of each line item, ensuring accurate tax preparation and compliance with Canadian tax regulations.

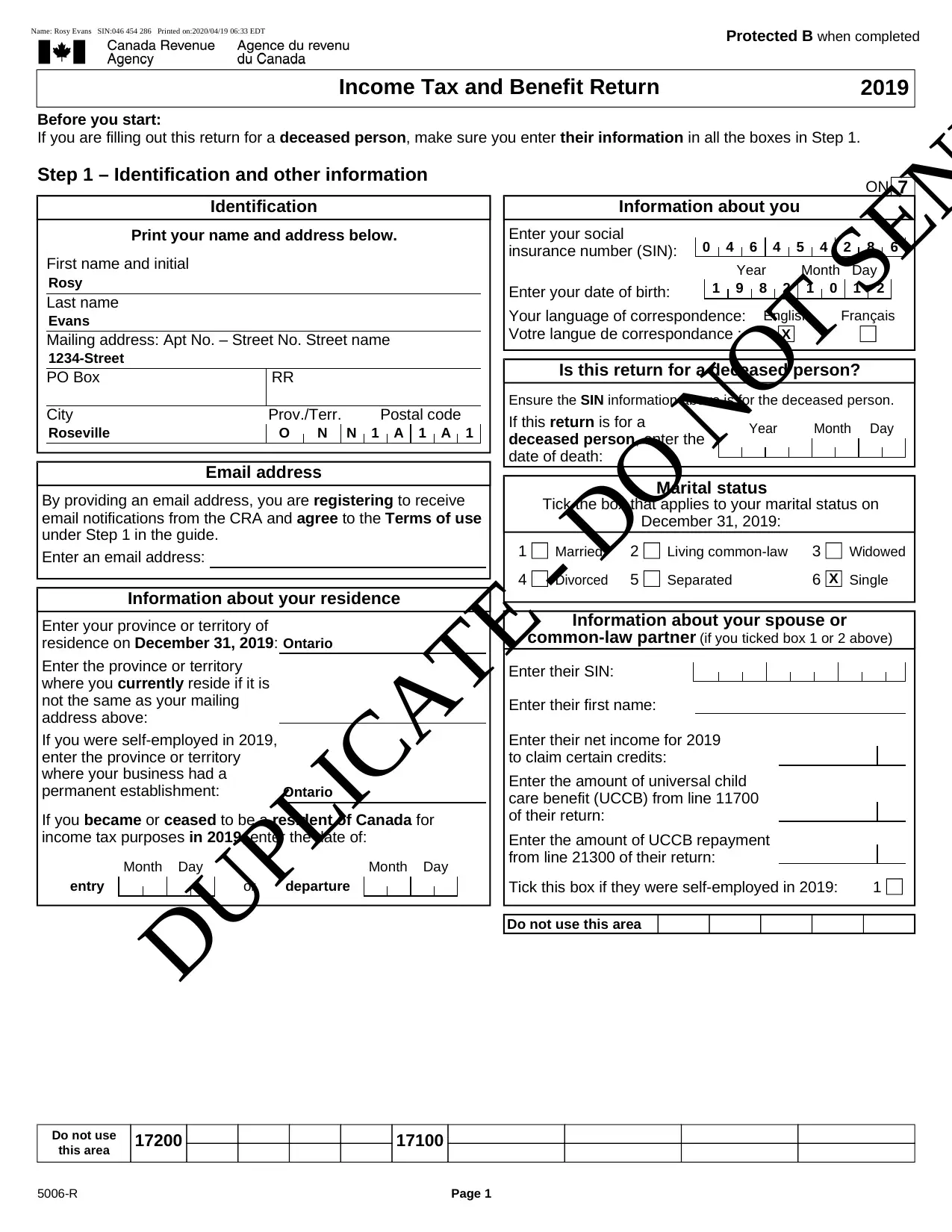

Protected B when completed

2019Income Tax and Benefit Return

ON 7

Before you start:

If you are filling out this return for a deceased person, make sure you enter their information in all the boxes in Step 1.

Step 1 – Identification and other information

Identification

Print your name and address below.

First name and initial

Last name

Mailing address: Apt No. – Street No. Street name

PO Box RR

City Prov./Terr. Postal code

Email address

By providing an email address, you are registering to receive

email notifications from the CRA and agree to the Terms of use

under Step 1 in the guide.

Enter an email address:

Information about your residence

Enter your province or territory of

residence on December 31, 2019:

Enter the province or territory

where you currently reside if it is

not the same as your mailing

address above:

If you were self-employed in 2019,

enter the province or territory

where your business had a

permanent establishment:

If you became or ceased to be a resident of Canada for

income tax purposes in 2019, enter the date of:

entry

Month Day

or departure

Month Day

Information about you

Enter your social

insurance number (SIN):

Enter your date of birth:

Year Month Day

Your language of correspondence:

Votre langue de correspondance :

English Français

Is this return for a deceased person?

Ensure the SIN information above is for the deceased person.

If this return is for a

deceased person, enter the

date of death:

Year Month Day

Marital status

Tick the box that applies to your marital status on

December 31, 2019:

1 Married 2 Living common-law 3 Widowed

4 Divorced 5 Separated 6 Single

Information about your spouse or

common-law partner (if you ticked box 1 or 2 above)

Enter their SIN:

Enter their first name:

Enter their net income for 2019

to claim certain credits:

Enter the amount of universal child

care benefit (UCCB) from line 11700

of their return:

Enter the amount of UCCB repayment

from line 21300 of their return:

Tick this box if they were self-employed in 2019: 1

Do not use this area

Do not use

this area 17200 17100

5006-R Page 1

0 4 6 4 5 4 2 8 6

Rosy 1 9 8 2 1 0 1 2

Evans X

1234-Street

Roseville O N N 1 A 1 A 1

X

Ontario

Ontario

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

2019Income Tax and Benefit Return

ON 7

Before you start:

If you are filling out this return for a deceased person, make sure you enter their information in all the boxes in Step 1.

Step 1 – Identification and other information

Identification

Print your name and address below.

First name and initial

Last name

Mailing address: Apt No. – Street No. Street name

PO Box RR

City Prov./Terr. Postal code

Email address

By providing an email address, you are registering to receive

email notifications from the CRA and agree to the Terms of use

under Step 1 in the guide.

Enter an email address:

Information about your residence

Enter your province or territory of

residence on December 31, 2019:

Enter the province or territory

where you currently reside if it is

not the same as your mailing

address above:

If you were self-employed in 2019,

enter the province or territory

where your business had a

permanent establishment:

If you became or ceased to be a resident of Canada for

income tax purposes in 2019, enter the date of:

entry

Month Day

or departure

Month Day

Information about you

Enter your social

insurance number (SIN):

Enter your date of birth:

Year Month Day

Your language of correspondence:

Votre langue de correspondance :

English Français

Is this return for a deceased person?

Ensure the SIN information above is for the deceased person.

If this return is for a

deceased person, enter the

date of death:

Year Month Day

Marital status

Tick the box that applies to your marital status on

December 31, 2019:

1 Married 2 Living common-law 3 Widowed

4 Divorced 5 Separated 6 Single

Information about your spouse or

common-law partner (if you ticked box 1 or 2 above)

Enter their SIN:

Enter their first name:

Enter their net income for 2019

to claim certain credits:

Enter the amount of universal child

care benefit (UCCB) from line 11700

of their return:

Enter the amount of UCCB repayment

from line 21300 of their return:

Tick this box if they were self-employed in 2019: 1

Do not use this area

Do not use

this area 17200 17100

5006-R Page 1

0 4 6 4 5 4 2 8 6

Rosy 1 9 8 2 1 0 1 2

Evans X

1234-Street

Roseville O N N 1 A 1 A 1

X

Ontario

Ontario

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Protected B when completed

Step 1 – Identification and other information (continued)

Please answer the following questions.

Elections Canada (For more information, see "Elections Canada" under Step 1, in the guide.)

A) Do you have Canadian citizenship? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1Yes 2No

If yes, go to question B. If no, skip question B.

B) As a Canadian citizen, do you authorize the Canada Revenue Agency to give your name, address,

date of birth, and citizenship to Elections Canada to update the National Register of Electors or , if

you are aged 14 to 17, to update the Register of Future Electors? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Yes 2No

Your authorization is valid until you file your next tax return. Your information will only be used for purposes permitted under

the Canada Elections Act, which include sharing lists of electors produced from the National Register of Electors with

provincial and territorial electoral agencies, members of Parliament, registered and eligible political parties, and candidates

at election time.

Your information in the Register of Future Electors will be included in the National Register of Electors once you turn 18.

Information from the Register of Future Electors can be shared only with provincial and territorial electoral agencies that are

allowed to collect future elector information. In addition, Elections Canada can use information in the Register of Future

Electors to provide youth with educational information about the electoral process.

Indian Act – Exempt income

Tick this box if you have any income that is exempt under the Indian Act.

For more information on this type of income, go to canada.ca/taxes-aboriginal-peoples. 1

If you tick the box, get and complete Form T90, Income Exempt under the Indian Act. Complete this form so that the CRA

can calculate your Canada training credit limit for the 2020 tax year. The information you provide may also be used to

calculate your Canada workers benefit for the 2019 tax year, if applicable.

Foreign property

26600

Did you own or hold specified foreign property where the total cost amount of all such

property, at any time in 2019, was more than CAN$100,000? .. . . . . . . . . . . . . . . . . . . . . . 1Yes 2No

If yes, get and complete Form T1135, Foreign Income Verification Statement. There are substantial penalties for not

completing and filing Form T1135 by the due date. For more information, see Form T1135.

5006-R Page 2

X

X

X

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Step 1 – Identification and other information (continued)

Please answer the following questions.

Elections Canada (For more information, see "Elections Canada" under Step 1, in the guide.)

A) Do you have Canadian citizenship? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1Yes 2No

If yes, go to question B. If no, skip question B.

B) As a Canadian citizen, do you authorize the Canada Revenue Agency to give your name, address,

date of birth, and citizenship to Elections Canada to update the National Register of Electors or , if

you are aged 14 to 17, to update the Register of Future Electors? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Yes 2No

Your authorization is valid until you file your next tax return. Your information will only be used for purposes permitted under

the Canada Elections Act, which include sharing lists of electors produced from the National Register of Electors with

provincial and territorial electoral agencies, members of Parliament, registered and eligible political parties, and candidates

at election time.

Your information in the Register of Future Electors will be included in the National Register of Electors once you turn 18.

Information from the Register of Future Electors can be shared only with provincial and territorial electoral agencies that are

allowed to collect future elector information. In addition, Elections Canada can use information in the Register of Future

Electors to provide youth with educational information about the electoral process.

Indian Act – Exempt income

Tick this box if you have any income that is exempt under the Indian Act.

For more information on this type of income, go to canada.ca/taxes-aboriginal-peoples. 1

If you tick the box, get and complete Form T90, Income Exempt under the Indian Act. Complete this form so that the CRA

can calculate your Canada training credit limit for the 2020 tax year. The information you provide may also be used to

calculate your Canada workers benefit for the 2019 tax year, if applicable.

Foreign property

26600

Did you own or hold specified foreign property where the total cost amount of all such

property, at any time in 2019, was more than CAN$100,000? .. . . . . . . . . . . . . . . . . . . . . . 1Yes 2No

If yes, get and complete Form T1135, Foreign Income Verification Statement. There are substantial penalties for not

completing and filing Form T1135 by the due date. For more information, see Form T1135.

5006-R Page 2

X

X

X

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Protected B when completed

Attach only the documents (schedules, information slips, forms, or receipts) requested to support

any claim or deduction. Keep all other supporting documents.

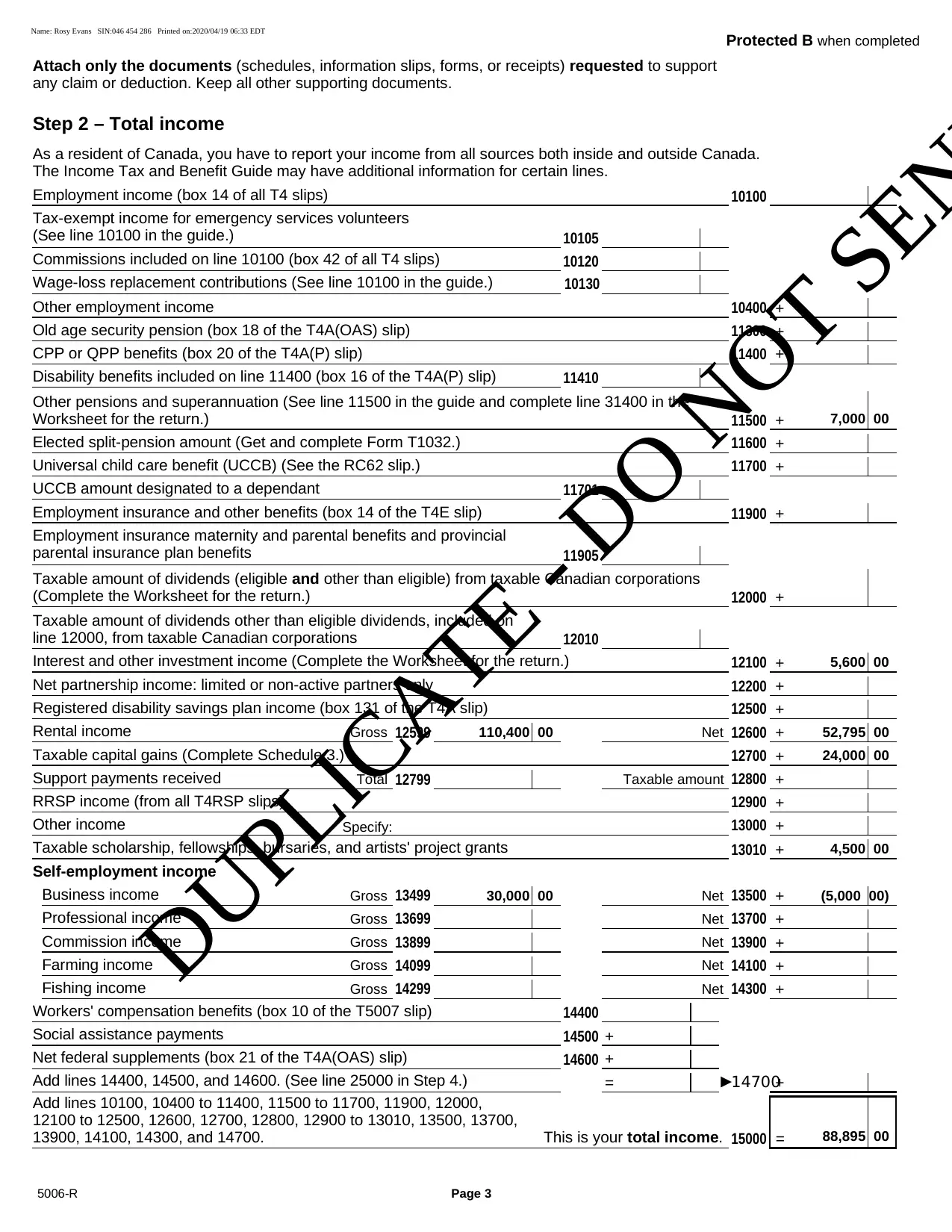

Step 2 – Total income

As a resident of Canada, you have to report your income from all sources both inside and outside Canada.

The Income Tax and Benefit Guide may have additional information for certain lines.

10100Employment income (box 14 of all T4 slips)

10105

Tax-exempt income for emergency services volunteers

(See line 10100 in the guide.)

10120Commissions included on line 10100 (box 42 of all T4 slips)

10130Wage-loss replacement contributions (See line 10100 in the guide.)

10400Other employment income +

11300Old age security pension (box 18 of the T4A(OAS) slip) +

11400CPP or QPP benefits (box 20 of the T4A(P) slip) +

11410Disability benefits included on line 11400 (box 16 of the T4A(P) slip)

11500

Other pensions and superannuation (See line 11500 in the guide and complete line 31400 in the

Worksheet for the return.) +

11600Elected split-pension amount (Get and complete Form T1032.) +

11700Universal child care benefit (UCCB) (See the RC62 slip.) +

11701UCCB amount designated to a dependant

11900Employment insurance and other benefits (box 14 of the T4E slip) +

11905

Employment insurance maternity and parental benefits and provincial

parental insurance plan benefits

12000

Taxable amount of dividends (eligible and other than eligible) from taxable Canadian corporations

(Complete the Worksheet for the return.) +

12010

Taxable amount of dividends other than eligible dividends, included on

line 12000, from taxable Canadian corporations

12100Interest and other investment income (Complete the Worksheet for the return.) +

12200Net partnership income: limited or non-active partners only +

12500Registered disability savings plan income (box 131 of the T4A slip) +

Rental income 12599Gross 12600Net +

12700Taxable capital gains (Complete Schedule 3.) +

Support payments received 12799Total 12800Taxable amount +

12900RRSP income (from all T4RSP slips) +

13000Other income Specify: +

13010Taxable scholarship, fellowships, bursaries, and artists' project grants +

Self-employment income

Business income 13499Gross 13500Net +

Professional income 13699Gross 13700Net +

Commission income 13899Gross 13900Net +

Farming income 14099Gross 14100Net +

Fishing income 14299Gross 14300Net +

14400Workers' compensation benefits (box 10 of the T5007 slip)

14500Social assistance payments +

14600Net federal supplements (box 21 of the T4A(OAS) slip) +

14700Add lines 14400, 14500, and 14600. (See line 25000 in Step 4.) =

◄ +

15000This is your total income.

Add lines 10100, 10400 to 11400, 11500 to 11700, 11900, 12000,

12100 to 12500, 12600, 12700, 12800, 12900 to 13010, 13500, 13700,

13900, 14100, 14300, and 14700. =

5006-R Page 3

7,000 00

5,600 00

110,400 00 52,795 00

24,000 00

4,500 00

30,000 00 (5,000 00)

88,895 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Attach only the documents (schedules, information slips, forms, or receipts) requested to support

any claim or deduction. Keep all other supporting documents.

Step 2 – Total income

As a resident of Canada, you have to report your income from all sources both inside and outside Canada.

The Income Tax and Benefit Guide may have additional information for certain lines.

10100Employment income (box 14 of all T4 slips)

10105

Tax-exempt income for emergency services volunteers

(See line 10100 in the guide.)

10120Commissions included on line 10100 (box 42 of all T4 slips)

10130Wage-loss replacement contributions (See line 10100 in the guide.)

10400Other employment income +

11300Old age security pension (box 18 of the T4A(OAS) slip) +

11400CPP or QPP benefits (box 20 of the T4A(P) slip) +

11410Disability benefits included on line 11400 (box 16 of the T4A(P) slip)

11500

Other pensions and superannuation (See line 11500 in the guide and complete line 31400 in the

Worksheet for the return.) +

11600Elected split-pension amount (Get and complete Form T1032.) +

11700Universal child care benefit (UCCB) (See the RC62 slip.) +

11701UCCB amount designated to a dependant

11900Employment insurance and other benefits (box 14 of the T4E slip) +

11905

Employment insurance maternity and parental benefits and provincial

parental insurance plan benefits

12000

Taxable amount of dividends (eligible and other than eligible) from taxable Canadian corporations

(Complete the Worksheet for the return.) +

12010

Taxable amount of dividends other than eligible dividends, included on

line 12000, from taxable Canadian corporations

12100Interest and other investment income (Complete the Worksheet for the return.) +

12200Net partnership income: limited or non-active partners only +

12500Registered disability savings plan income (box 131 of the T4A slip) +

Rental income 12599Gross 12600Net +

12700Taxable capital gains (Complete Schedule 3.) +

Support payments received 12799Total 12800Taxable amount +

12900RRSP income (from all T4RSP slips) +

13000Other income Specify: +

13010Taxable scholarship, fellowships, bursaries, and artists' project grants +

Self-employment income

Business income 13499Gross 13500Net +

Professional income 13699Gross 13700Net +

Commission income 13899Gross 13900Net +

Farming income 14099Gross 14100Net +

Fishing income 14299Gross 14300Net +

14400Workers' compensation benefits (box 10 of the T5007 slip)

14500Social assistance payments +

14600Net federal supplements (box 21 of the T4A(OAS) slip) +

14700Add lines 14400, 14500, and 14600. (See line 25000 in Step 4.) =

◄ +

15000This is your total income.

Add lines 10100, 10400 to 11400, 11500 to 11700, 11900, 12000,

12100 to 12500, 12600, 12700, 12800, 12900 to 13010, 13500, 13700,

13900, 14100, 14300, and 14700. =

5006-R Page 3

7,000 00

5,600 00

110,400 00 52,795 00

24,000 00

4,500 00

30,000 00 (5,000 00)

88,895 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Protected B when completed

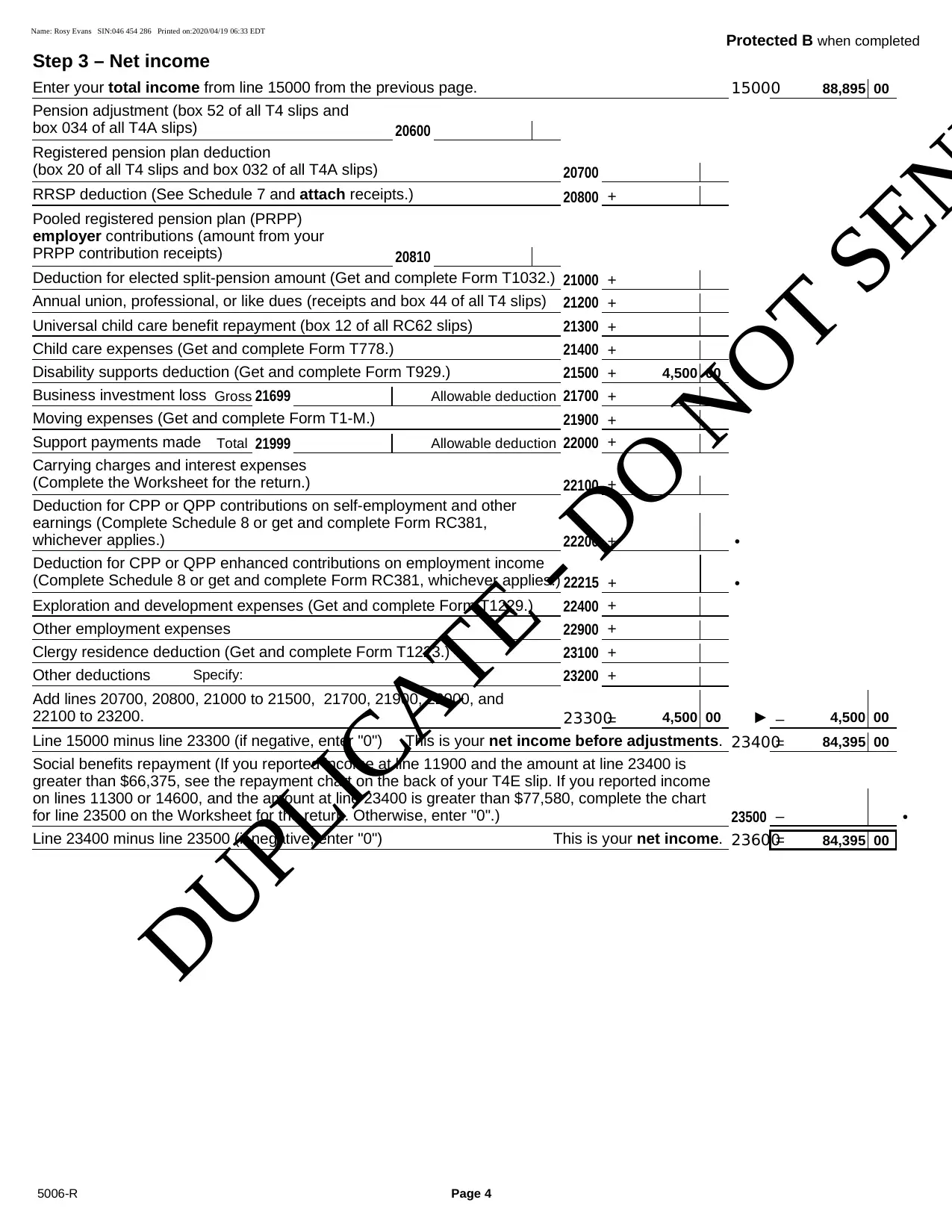

Step 3 – Net income

15000Enter your total income from line 15000 from the previous page.

20600

Pension adjustment (box 52 of all T4 slips and

box 034 of all T4A slips)

20700

Registered pension plan deduction

(box 20 of all T4 slips and box 032 of all T4A slips)

20800RRSP deduction (See Schedule 7 and attach receipts.) +

20810

Pooled registered pension plan (PRPP)

employer contributions (amount from your

PRPP contribution receipts)

21000Deduction for elected split-pension amount (Get and complete Form T1032.) +

21200Annual union, professional, or like dues (receipts and box 44 of all T4 slips) +

21300Universal child care benefit repayment (box 12 of all RC62 slips) +

21400Child care expenses (Get and complete Form T778.) +

21500Disability supports deduction (Get and complete Form T929.) +

Business investment loss 21699Gross 21700Allowable deduction +

21900Moving expenses (Get and complete Form T1-M.) +

Support payments made 21999Total 22000Allowable deduction +

22100

Carrying charges and interest expenses

(Complete the Worksheet for the return.) +

22200

Deduction for CPP or QPP contributions on self-employment and other

earnings (Complete Schedule 8 or get and complete Form RC381,

whichever applies.) + •

22215

Deduction for CPP or QPP enhanced contributions on employment income

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) + •

22400Exploration and development expenses (Get and complete Form T1229.) +

22900Other employment expenses +

23100Clergy residence deduction (Get and complete Form T1223.) +

23200Other deductions Specify: +

23300

Add lines 20700, 20800, 21000 to 21500, 21700, 21900, 22000, and

22100 to 23200. =

◄ –

23400This is your net income before adjustments.Line 15000 minus line 23300 (if negative, enter "0") =

23500

Social benefits repayment (If you reported income at line 11900 and the amount at line 23400 is

greater than $66,375, see the repayment chart on the back of your T4E slip. If you reported income

on lines 11300 or 14600, and the amount at line 23400 is greater than $77,580, complete the chart

for line 23500 on the Worksheet for the return. Otherwise, enter "0".) – •

23600This is your net income.Line 23400 minus line 23500 (if negative, enter "0") =

5006-R Page 4

88,895 00

4,500 00

4,500 00 4,500 00

84,395 00

84,395 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Step 3 – Net income

15000Enter your total income from line 15000 from the previous page.

20600

Pension adjustment (box 52 of all T4 slips and

box 034 of all T4A slips)

20700

Registered pension plan deduction

(box 20 of all T4 slips and box 032 of all T4A slips)

20800RRSP deduction (See Schedule 7 and attach receipts.) +

20810

Pooled registered pension plan (PRPP)

employer contributions (amount from your

PRPP contribution receipts)

21000Deduction for elected split-pension amount (Get and complete Form T1032.) +

21200Annual union, professional, or like dues (receipts and box 44 of all T4 slips) +

21300Universal child care benefit repayment (box 12 of all RC62 slips) +

21400Child care expenses (Get and complete Form T778.) +

21500Disability supports deduction (Get and complete Form T929.) +

Business investment loss 21699Gross 21700Allowable deduction +

21900Moving expenses (Get and complete Form T1-M.) +

Support payments made 21999Total 22000Allowable deduction +

22100

Carrying charges and interest expenses

(Complete the Worksheet for the return.) +

22200

Deduction for CPP or QPP contributions on self-employment and other

earnings (Complete Schedule 8 or get and complete Form RC381,

whichever applies.) + •

22215

Deduction for CPP or QPP enhanced contributions on employment income

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) + •

22400Exploration and development expenses (Get and complete Form T1229.) +

22900Other employment expenses +

23100Clergy residence deduction (Get and complete Form T1223.) +

23200Other deductions Specify: +

23300

Add lines 20700, 20800, 21000 to 21500, 21700, 21900, 22000, and

22100 to 23200. =

◄ –

23400This is your net income before adjustments.Line 15000 minus line 23300 (if negative, enter "0") =

23500

Social benefits repayment (If you reported income at line 11900 and the amount at line 23400 is

greater than $66,375, see the repayment chart on the back of your T4E slip. If you reported income

on lines 11300 or 14600, and the amount at line 23400 is greater than $77,580, complete the chart

for line 23500 on the Worksheet for the return. Otherwise, enter "0".) – •

23600This is your net income.Line 23400 minus line 23500 (if negative, enter "0") =

5006-R Page 4

88,895 00

4,500 00

4,500 00 4,500 00

84,395 00

84,395 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Protected B when completed

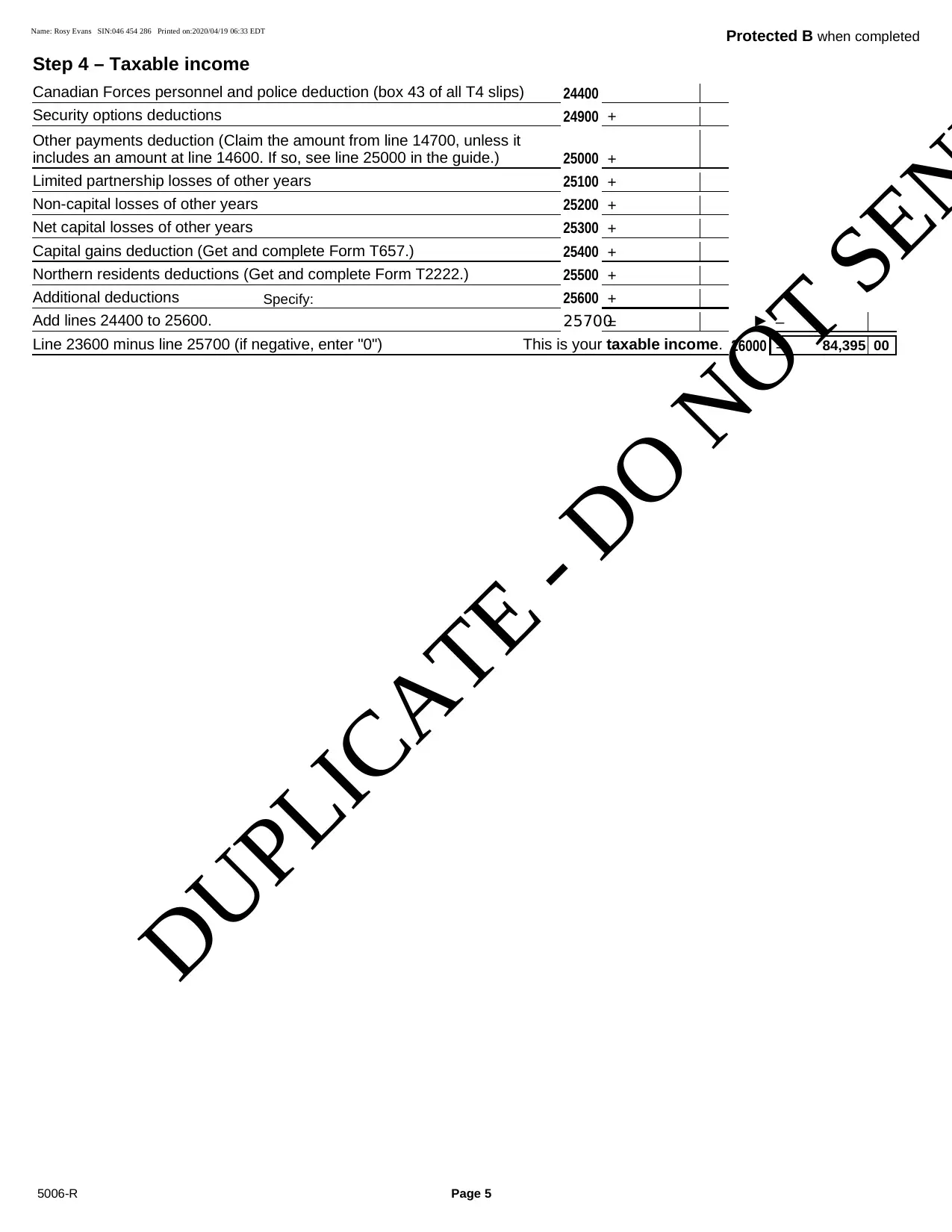

Step 4 – Taxable income

24400Canadian Forces personnel and police deduction (box 43 of all T4 slips)

24900Security options deductions +

25000

Other payments deduction (Claim the amount from line 14700, unless it

includes an amount at line 14600. If so, see line 25000 in the guide.) +

25100Limited partnership losses of other years +

25200Non-capital losses of other years +

25300Net capital losses of other years +

25400Capital gains deduction (Get and complete Form T657.) +

25500Northern residents deductions (Get and complete Form T2222.) +

25600Additional deductions Specify: +

25700Add lines 24400 to 25600. =

◄ –

26000This is your taxable income.Line 23600 minus line 25700 (if negative, enter "0") =

5006-R Page 5

84,395 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Step 4 – Taxable income

24400Canadian Forces personnel and police deduction (box 43 of all T4 slips)

24900Security options deductions +

25000

Other payments deduction (Claim the amount from line 14700, unless it

includes an amount at line 14600. If so, see line 25000 in the guide.) +

25100Limited partnership losses of other years +

25200Non-capital losses of other years +

25300Net capital losses of other years +

25400Capital gains deduction (Get and complete Form T657.) +

25500Northern residents deductions (Get and complete Form T2222.) +

25600Additional deductions Specify: +

25700Add lines 24400 to 25600. =

◄ –

26000This is your taxable income.Line 23600 minus line 25700 (if negative, enter "0") =

5006-R Page 5

84,395 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Protected B when completed

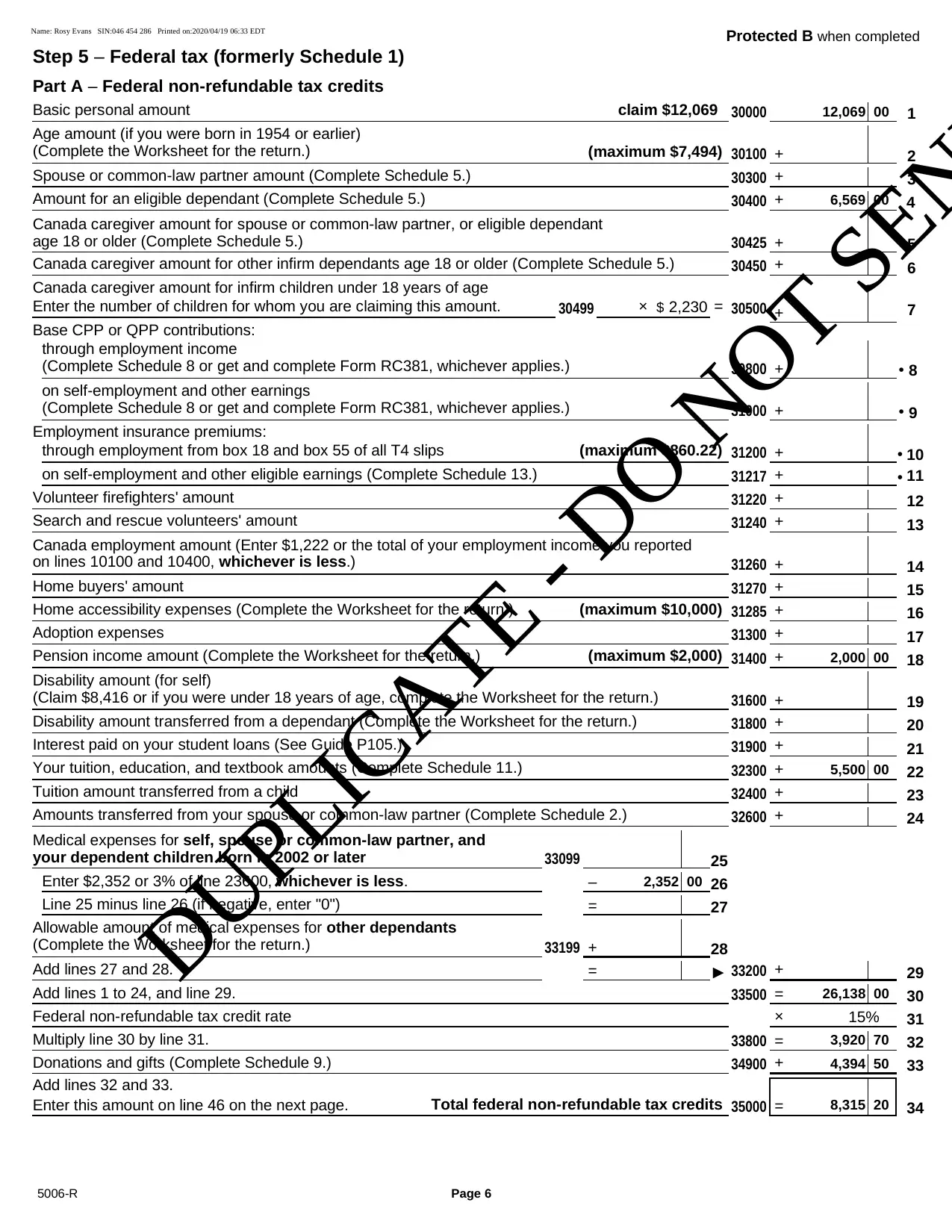

Step 5 – Federal tax (formerly Schedule 1)

Part A – Federal non-refundable tax credits

30000 1Basic personal amount claim $12,069

30100 2

Age amount (if you were born in 1954 or earlier)

(Complete the Worksheet for the return.) (maximum $7,494) +

30300 3Spouse or common-law partner amount (Complete Schedule 5.) +

30400 4Amount for an eligible dependant (Complete Schedule 5.) +

30425 5

Canada caregiver amount for spouse or common-law partner, or eligible dependant

age 18 or older (Complete Schedule 5.) +

30450 6Canada caregiver amount for other infirm dependants age 18 or older (Complete Schedule 5.) +

Canada caregiver amount for infirm children under 18 years of age

30499Enter the number of children for whom you are claiming this amount. × $ 2,230 = 30500 7+

Base CPP or QPP contributions:

30800 8

through employment income

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) + •

31000 9

on self-employment and other earnings

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) + •

Employment insurance premiums:

31200 10through employment from box 18 and box 55 of all T4 slips (maximum $860.22) + •

31217 11on self-employment and other eligible earnings (Complete Schedule 13.) + •

31220 12Volunteer firefighters' amount +

31240 13Search and rescue volunteers' amount +

31260 14

Canada employment amount (Enter $1,222 or the total of your employment income you reported

on lines 10100 and 10400, whichever is less.) +

31270 15Home buyers' amount +

31285 16Home accessibility expenses (Complete the Worksheet for the return.) (maximum $10,000) +

31300 17Adoption expenses +

31400 18Pension income amount (Complete the Worksheet for the return.) (maximum $2,000) +

31600 19

Disability amount (for self)

(Claim $8,416 or if you were under 18 years of age, complete the Worksheet for the return.) +

31800 20Disability amount transferred from a dependant (Complete the Worksheet for the return.) +

31900 21Interest paid on your student loans (See Guide P105.) +

32300 22Your tuition, education, and textbook amounts (Complete Schedule 11.) +

32400 23Tuition amount transferred from a child +

32600 24Amounts transferred from your spouse or common-law partner (Complete Schedule 2.) +

33099 25

Medical expenses for self, spouse or common-law partner, and

your dependent children born in 2002 or later

26Enter $2,352 or 3% of line 23600, whichever is less. –

27Line 25 minus line 26 (if negative, enter "0") =

33199 28

Allowable amount of medical expenses for other dependants

(Complete the Worksheet for the return.) +

33200 29Add lines 27 and 28. =

◄ +

33500 30Add lines 1 to 24, and line 29. =

31Federal non-refundable tax credit rate × 15%

33800 32Multiply line 30 by line 31. =

34900 33Donations and gifts (Complete Schedule 9.) +

35000 34Total federal non-refundable tax credits

Add lines 32 and 33.

Enter this amount on line 46 on the next page. =

5006-R Page 6

12,069 00

6,569 00

2,000 00

5,500 00

2,352 00

26,138 00

3,920 70

4,394 50

8,315 20

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Step 5 – Federal tax (formerly Schedule 1)

Part A – Federal non-refundable tax credits

30000 1Basic personal amount claim $12,069

30100 2

Age amount (if you were born in 1954 or earlier)

(Complete the Worksheet for the return.) (maximum $7,494) +

30300 3Spouse or common-law partner amount (Complete Schedule 5.) +

30400 4Amount for an eligible dependant (Complete Schedule 5.) +

30425 5

Canada caregiver amount for spouse or common-law partner, or eligible dependant

age 18 or older (Complete Schedule 5.) +

30450 6Canada caregiver amount for other infirm dependants age 18 or older (Complete Schedule 5.) +

Canada caregiver amount for infirm children under 18 years of age

30499Enter the number of children for whom you are claiming this amount. × $ 2,230 = 30500 7+

Base CPP or QPP contributions:

30800 8

through employment income

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) + •

31000 9

on self-employment and other earnings

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) + •

Employment insurance premiums:

31200 10through employment from box 18 and box 55 of all T4 slips (maximum $860.22) + •

31217 11on self-employment and other eligible earnings (Complete Schedule 13.) + •

31220 12Volunteer firefighters' amount +

31240 13Search and rescue volunteers' amount +

31260 14

Canada employment amount (Enter $1,222 or the total of your employment income you reported

on lines 10100 and 10400, whichever is less.) +

31270 15Home buyers' amount +

31285 16Home accessibility expenses (Complete the Worksheet for the return.) (maximum $10,000) +

31300 17Adoption expenses +

31400 18Pension income amount (Complete the Worksheet for the return.) (maximum $2,000) +

31600 19

Disability amount (for self)

(Claim $8,416 or if you were under 18 years of age, complete the Worksheet for the return.) +

31800 20Disability amount transferred from a dependant (Complete the Worksheet for the return.) +

31900 21Interest paid on your student loans (See Guide P105.) +

32300 22Your tuition, education, and textbook amounts (Complete Schedule 11.) +

32400 23Tuition amount transferred from a child +

32600 24Amounts transferred from your spouse or common-law partner (Complete Schedule 2.) +

33099 25

Medical expenses for self, spouse or common-law partner, and

your dependent children born in 2002 or later

26Enter $2,352 or 3% of line 23600, whichever is less. –

27Line 25 minus line 26 (if negative, enter "0") =

33199 28

Allowable amount of medical expenses for other dependants

(Complete the Worksheet for the return.) +

33200 29Add lines 27 and 28. =

◄ +

33500 30Add lines 1 to 24, and line 29. =

31Federal non-refundable tax credit rate × 15%

33800 32Multiply line 30 by line 31. =

34900 33Donations and gifts (Complete Schedule 9.) +

35000 34Total federal non-refundable tax credits

Add lines 32 and 33.

Enter this amount on line 46 on the next page. =

5006-R Page 6

12,069 00

6,569 00

2,000 00

5,500 00

2,352 00

26,138 00

3,920 70

4,394 50

8,315 20

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Protected B when completed

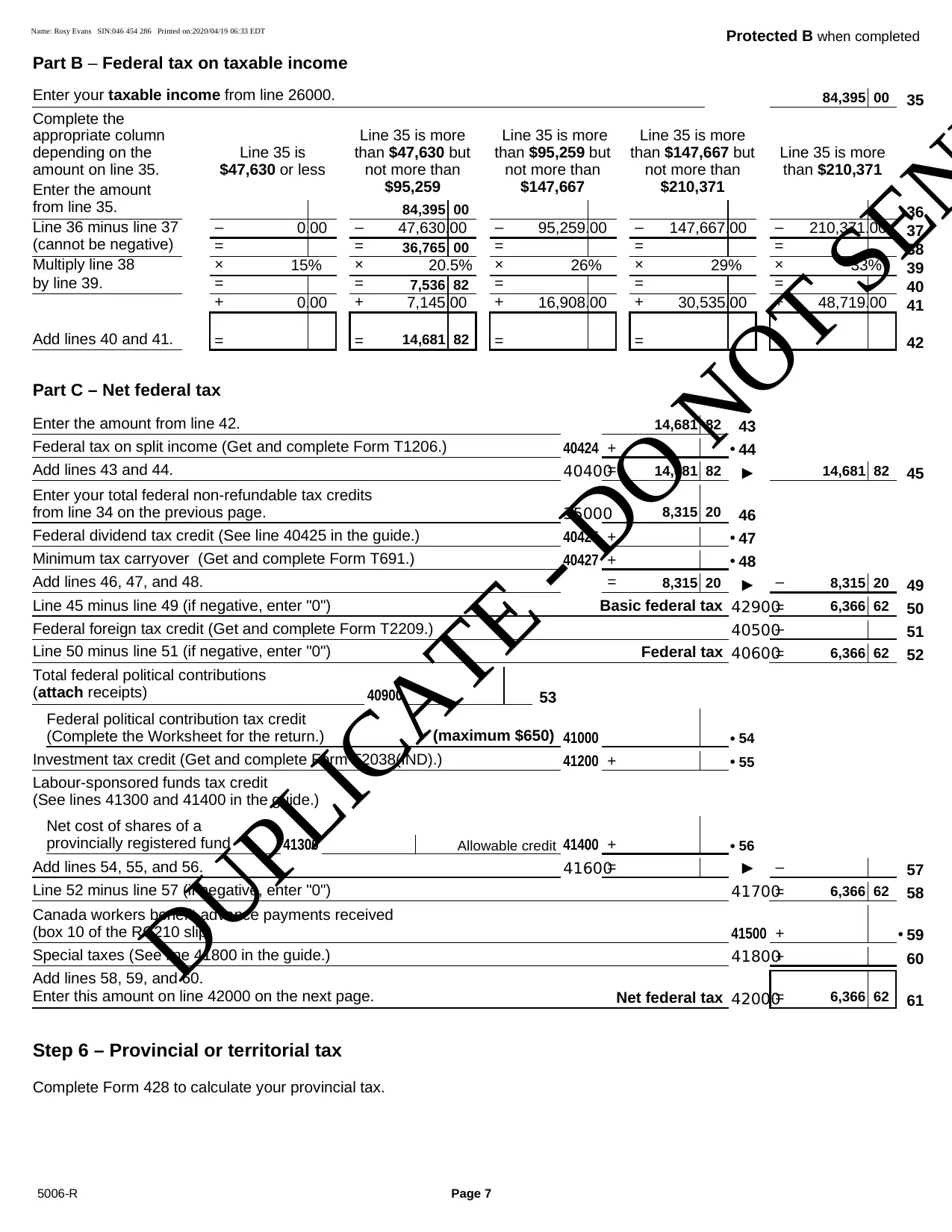

Part B – Federal tax on taxable income

35Enter your taxable income from line 26000.

Complete the

appropriate column

depending on the

amount on line 35.

Line 35 is

$47,630 or less

Enter the amount

from line 35.

– 0.00Line 36 minus line 37

(cannot be negative) =

× 15%Multiply line 38

by line 39. =

+ 0.00

Add lines 40 and 41. =

Line 35 is more

than $47,630 but

not more than

$95,259

– 47,630.00

=

× 20.5%

=

+ 7,145.00

=

Line 35 is more

than $95,259 but

not more than

$147,667

– 95,259.00

=

× 26%

=

+ 16,908.00

=

Line 35 is more

than $147,667 but

not more than

$210,371

– 147,667.00

=

× 29%

=

+ 30,535.00

=

Line 35 is more

than $210,371

– 210,371.00

=

× 33%

=

+ 48,719.00

=

36

37

38

39

40

41

42

Part C – Net federal tax

43Enter the amount from line 42.

40424 44Federal tax on split income (Get and complete Form T1206.) + •

40400 45Add lines 43 and 44. =◄

35000 46

Enter your total federal non-refundable tax credits

from line 34 on the previous page.

40425 47Federal dividend tax credit (See line 40425 in the guide.) + •

40427 48Minimum tax carryover (Get and complete Form T691.) + •

49Add lines 46, 47, and 48. =◄ –

42900 50Basic federal taxLine 45 minus line 49 (if negative, enter "0") =

40500 51Federal foreign tax credit (Get and complete Form T2209.) –

40600 52Federal taxLine 50 minus line 51 (if negative, enter "0") =

40900 53

Total federal political contributions

(attach receipts)

41000 54

Federal political contribution tax credit

(Complete the Worksheet for the return.) (maximum $650) •

41200 55Investment tax credit (Get and complete Form T2038(IND).) + •

Labour-sponsored funds tax credit

(See lines 41300 and 41400 in the guide.)

41300

Net cost of shares of a

provincially registered fund 41400 56Allowable credit + •

41600 57Add lines 54, 55, and 56. =

◄ –

41700 58Line 52 minus line 57 (if negative, enter "0") =

41500 59

Canada workers benefit advance payments received

(box 10 of the RC210 slip) + •

41800 60Special taxes (See line 41800 in the guide.) +

42000 61Net federal tax

Add lines 58, 59, and 60.

Enter this amount on line 42000 on the next page. =

Step 6 – Provincial or territorial tax

Complete Form 428 to calculate your provincial tax.

5006-R Page 7

84,395 00

84,395 00

36,765 00

7,536 82

14,681 82

14,681 82

14,681 82 14,681 82

8,315 20

8,315 20 8,315 20

6,366 62

6,366 62

6,366 62

6,366 62

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Part B – Federal tax on taxable income

35Enter your taxable income from line 26000.

Complete the

appropriate column

depending on the

amount on line 35.

Line 35 is

$47,630 or less

Enter the amount

from line 35.

– 0.00Line 36 minus line 37

(cannot be negative) =

× 15%Multiply line 38

by line 39. =

+ 0.00

Add lines 40 and 41. =

Line 35 is more

than $47,630 but

not more than

$95,259

– 47,630.00

=

× 20.5%

=

+ 7,145.00

=

Line 35 is more

than $95,259 but

not more than

$147,667

– 95,259.00

=

× 26%

=

+ 16,908.00

=

Line 35 is more

than $147,667 but

not more than

$210,371

– 147,667.00

=

× 29%

=

+ 30,535.00

=

Line 35 is more

than $210,371

– 210,371.00

=

× 33%

=

+ 48,719.00

=

36

37

38

39

40

41

42

Part C – Net federal tax

43Enter the amount from line 42.

40424 44Federal tax on split income (Get and complete Form T1206.) + •

40400 45Add lines 43 and 44. =◄

35000 46

Enter your total federal non-refundable tax credits

from line 34 on the previous page.

40425 47Federal dividend tax credit (See line 40425 in the guide.) + •

40427 48Minimum tax carryover (Get and complete Form T691.) + •

49Add lines 46, 47, and 48. =◄ –

42900 50Basic federal taxLine 45 minus line 49 (if negative, enter "0") =

40500 51Federal foreign tax credit (Get and complete Form T2209.) –

40600 52Federal taxLine 50 minus line 51 (if negative, enter "0") =

40900 53

Total federal political contributions

(attach receipts)

41000 54

Federal political contribution tax credit

(Complete the Worksheet for the return.) (maximum $650) •

41200 55Investment tax credit (Get and complete Form T2038(IND).) + •

Labour-sponsored funds tax credit

(See lines 41300 and 41400 in the guide.)

41300

Net cost of shares of a

provincially registered fund 41400 56Allowable credit + •

41600 57Add lines 54, 55, and 56. =

◄ –

41700 58Line 52 minus line 57 (if negative, enter "0") =

41500 59

Canada workers benefit advance payments received

(box 10 of the RC210 slip) + •

41800 60Special taxes (See line 41800 in the guide.) +

42000 61Net federal tax

Add lines 58, 59, and 60.

Enter this amount on line 42000 on the next page. =

Step 6 – Provincial or territorial tax

Complete Form 428 to calculate your provincial tax.

5006-R Page 7

84,395 00

84,395 00

36,765 00

7,536 82

14,681 82

14,681 82

14,681 82 14,681 82

8,315 20

8,315 20 8,315 20

6,366 62

6,366 62

6,366 62

6,366 62

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Protected B when completed

42000

Step 7 – Refund or balance owing

Net federal tax: enter the amount from line 61 from the previous page.

42100

CPP contributions payable on self-employment and other earnings

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) +

42120

Employment insurance premiums payable on self-employment and other eligible earnings

(Complete Schedule 13.) +

42200Social benefits repayment (amount from line 23500) +

42800Provincial or territorial tax (Attach Form 428, even if the result is "0".) +

43500This is your total payable.Add lines 42000, 42100, 42120, 42200, and 42800. = •

43700Total income tax deducted (amounts from all Canadian slips) •

44000Refundable Quebec abatement (See line 44000 in the guide.) + •

44800CPP overpayment (See line 30800 in the guide.) + •

45000Employment insurance overpayment (See line 45000 in the guide.) + •

45110Climate Action Incentive (Complete Schedule 14.) + •

45200

Refundable medical expense supplement

(Complete the Worksheet for the return.) + •

45300Canada workers benefit (CWB) (Complete Schedule 6.) + •

45400Refund of investment tax credit (Get and complete Form T2038(IND).) + •

45600Part XII.2 trust tax credit (box 38 of all T3 slips and box 209 of all T5013 slips) + •

45700Employee and partner GST/HST rebate (Get and complete Form GST370.) + •

Eligible educator school supply tax credit

46800Supplies expenses (maximum $1,000) × 15% = 46900 + •

47600Tax paid by instalments + •

47900Provincial or territorial credits (Complete Form 479, if it applies.) + •

48200These are your total credits.

Add lines 43700 to 45700, and

46900 to 47900. =

◄ –

This is your refund or balance owing.Line 43500 minus line 48200 =

If the result is negative, you have a refund. If the result is positive, you have a balance owing.

Enter the amount below on whichever line applies.

Generally, we do not charge or refund a difference of $2 or less.

◄

◄

48400Refund • 48500Balance owing •

◄

For more information on how to receive your refund by

direct deposit, see line 48400 in the guide or go to

canada.ca/cra-direct-deposit.

For more information on how to make your payment, see

line 48500 in the guide or go to canada.ca/payments.

Your payment is due no later than April 30, 2020.

Ontario opportunities fund

You can help reduce Ontario's debt by completing this area to

donate some or all of your 2019 refund to the Ontario opportunities

fund. Please see the provincial pages for details.

1Amount from line 48400 above

46500 2

Your donation to the

Ontario opportunities fund – •

46600 3Net refund (line 1 minus line 2) = •

◄

I certify that the information given on this return and in any

documents attached is correct and complete and fully discloses

all my income.

Sign here

It is a serious offence to make a false return.

Telephone number:

Date

If this return was completed by a tax professional, tick the

applicable box and provide the following information:

49000 Was a fee charged? 1Yes 2No

48900 EFILE number (if applicable):

Name of tax professional:

Telephone number:

Personal information (including the SIN) is collected for the purposes of the administration or enforcement of the Income Tax Act and related programs and

activities including administering tax, benefits, audit, compliance, and collection. The information collected may be used or disclosed for purposes of other

federal acts that provide for the imposition and collection of a tax or duty. It may also be disclosed to other federal, provincial, territorial or foreign government

institutions to the extent authorized by law. Failure to provide this information may result in interest payable, penalties or other actions. Under the Privacy Act,

individuals have the right to access their personal information, request correction, or file a complaint to the Privacy Commissioner of Canada regarding the

handling of the individual’s personal information. Refer to Personal Information Bank CRA PPU 005 on Info Source at canada.ca/cra-info-source.

Do not use

this area 48700 48800 • 48600 •

5006-R Page 8 Canada Revenue Agency Approval # : RC-19-107

6,366 62

4,152 45

10,519 07

224 00

12,000 00

12,224 00 12,224 00

(1,704 93)

1,704 93

1,704 93

1,704 93

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

42000

Step 7 – Refund or balance owing

Net federal tax: enter the amount from line 61 from the previous page.

42100

CPP contributions payable on self-employment and other earnings

(Complete Schedule 8 or get and complete Form RC381, whichever applies.) +

42120

Employment insurance premiums payable on self-employment and other eligible earnings

(Complete Schedule 13.) +

42200Social benefits repayment (amount from line 23500) +

42800Provincial or territorial tax (Attach Form 428, even if the result is "0".) +

43500This is your total payable.Add lines 42000, 42100, 42120, 42200, and 42800. = •

43700Total income tax deducted (amounts from all Canadian slips) •

44000Refundable Quebec abatement (See line 44000 in the guide.) + •

44800CPP overpayment (See line 30800 in the guide.) + •

45000Employment insurance overpayment (See line 45000 in the guide.) + •

45110Climate Action Incentive (Complete Schedule 14.) + •

45200

Refundable medical expense supplement

(Complete the Worksheet for the return.) + •

45300Canada workers benefit (CWB) (Complete Schedule 6.) + •

45400Refund of investment tax credit (Get and complete Form T2038(IND).) + •

45600Part XII.2 trust tax credit (box 38 of all T3 slips and box 209 of all T5013 slips) + •

45700Employee and partner GST/HST rebate (Get and complete Form GST370.) + •

Eligible educator school supply tax credit

46800Supplies expenses (maximum $1,000) × 15% = 46900 + •

47600Tax paid by instalments + •

47900Provincial or territorial credits (Complete Form 479, if it applies.) + •

48200These are your total credits.

Add lines 43700 to 45700, and

46900 to 47900. =

◄ –

This is your refund or balance owing.Line 43500 minus line 48200 =

If the result is negative, you have a refund. If the result is positive, you have a balance owing.

Enter the amount below on whichever line applies.

Generally, we do not charge or refund a difference of $2 or less.

◄

◄

48400Refund • 48500Balance owing •

◄

For more information on how to receive your refund by

direct deposit, see line 48400 in the guide or go to

canada.ca/cra-direct-deposit.

For more information on how to make your payment, see

line 48500 in the guide or go to canada.ca/payments.

Your payment is due no later than April 30, 2020.

Ontario opportunities fund

You can help reduce Ontario's debt by completing this area to

donate some or all of your 2019 refund to the Ontario opportunities

fund. Please see the provincial pages for details.

1Amount from line 48400 above

46500 2

Your donation to the

Ontario opportunities fund – •

46600 3Net refund (line 1 minus line 2) = •

◄

I certify that the information given on this return and in any

documents attached is correct and complete and fully discloses

all my income.

Sign here

It is a serious offence to make a false return.

Telephone number:

Date

If this return was completed by a tax professional, tick the

applicable box and provide the following information:

49000 Was a fee charged? 1Yes 2No

48900 EFILE number (if applicable):

Name of tax professional:

Telephone number:

Personal information (including the SIN) is collected for the purposes of the administration or enforcement of the Income Tax Act and related programs and

activities including administering tax, benefits, audit, compliance, and collection. The information collected may be used or disclosed for purposes of other

federal acts that provide for the imposition and collection of a tax or duty. It may also be disclosed to other federal, provincial, territorial or foreign government

institutions to the extent authorized by law. Failure to provide this information may result in interest payable, penalties or other actions. Under the Privacy Act,

individuals have the right to access their personal information, request correction, or file a complaint to the Privacy Commissioner of Canada regarding the

handling of the individual’s personal information. Refer to Personal Information Bank CRA PPU 005 on Info Source at canada.ca/cra-info-source.

Do not use

this area 48700 48800 • 48600 •

5006-R Page 8 Canada Revenue Agency Approval # : RC-19-107

6,366 62

4,152 45

10,519 07

224 00

12,000 00

12,224 00 12,224 00

(1,704 93)

1,704 93

1,704 93

1,704 93

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

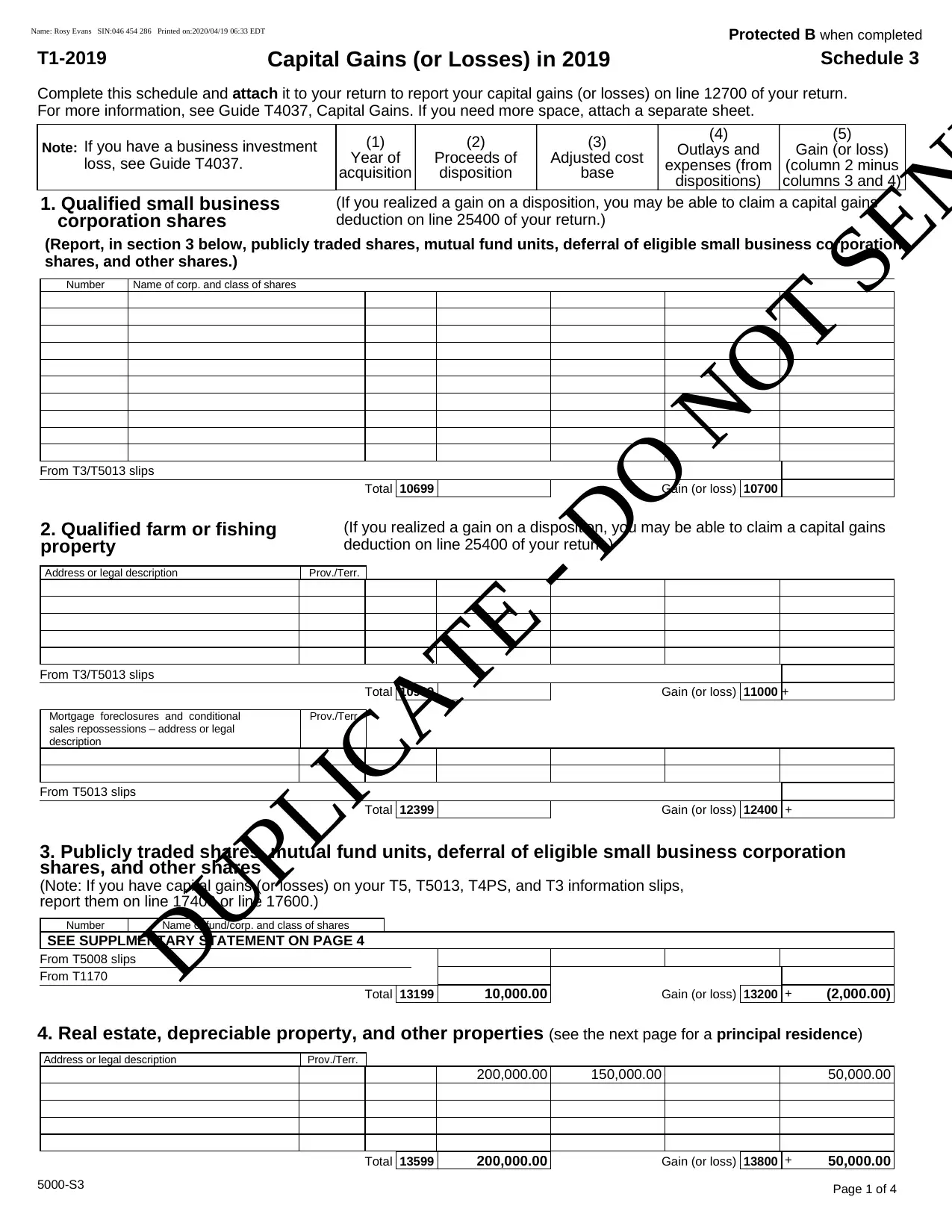

Number Name of corp. and class of shares

10699 10700Total Gain (or loss)

Address or legal description Prov./Terr.

10999 11000 +

Mortgage foreclosures and conditional

sales repossessions – address or legal

description

Prov./Terr.

12399 12400 +Total Gain (or loss)

Number Name of fund/corp. and class of shares

SEE SUPPLMENTARY STATEMENT ON PAGE 4

13199 13200

From T5008 slips

From T1170

Total Gain (or loss)

Address or legal description Prov./Terr.

13599 13800Total Gain (or loss)

Page 1 of 4

From T3/T5013 slips

From T3/T5013 slips

Total Gain (or loss)

From T5013 slips

+

+

5000-S3

Protected B when completed

T1-2019 Schedule 3Capital Gains (or Losses) in 2019

Complete this schedule and attach it to your return to report your capital gains (or losses) on line 12700 of your return.

For more information, see Guide T4037, Capital Gains. If you need more space, attach a separate sheet.

Note: If you have a business investment

loss, see Guide T4037.

(1)

Year of

acquisition

(2)

Proceeds of

disposition

(3)

Adjusted cost

base

(4)

Outlays and

expenses (from

dispositions)

(5)

Gain (or loss)

(column 2 minus

columns 3 and 4)

1. Qualified small business

corporation shares

(If you realized a gain on a disposition, you may be able to claim a capital gains

deduction on line 25400 of your return.)

(Report, in section 3 below, publicly traded shares, mutual fund units, deferral of eligible small business corporation

shares, and other shares.)

2. Qualified farm or fishing

property

(If you realized a gain on a disposition, you may be able to claim a capital gains

deduction on line 25400 of your return.)

3. Publicly traded shares, mutual fund units, deferral of eligible small business corporation

shares, and other shares

(Note: If you have capital gains (or losses) on your T5, T5013, T4PS, and T3 information slips,

report them on line 17400 or line 17600.)

4. Real estate, depreciable property, and other properties (see the next page for a principal residence)

10,000.00 (2,000.00)

200,000.00 150,000.00 50,000.00

200,000.00 50,000.00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

10699 10700Total Gain (or loss)

Address or legal description Prov./Terr.

10999 11000 +

Mortgage foreclosures and conditional

sales repossessions – address or legal

description

Prov./Terr.

12399 12400 +Total Gain (or loss)

Number Name of fund/corp. and class of shares

SEE SUPPLMENTARY STATEMENT ON PAGE 4

13199 13200

From T5008 slips

From T1170

Total Gain (or loss)

Address or legal description Prov./Terr.

13599 13800Total Gain (or loss)

Page 1 of 4

From T3/T5013 slips

From T3/T5013 slips

Total Gain (or loss)

From T5013 slips

+

+

5000-S3

Protected B when completed

T1-2019 Schedule 3Capital Gains (or Losses) in 2019

Complete this schedule and attach it to your return to report your capital gains (or losses) on line 12700 of your return.

For more information, see Guide T4037, Capital Gains. If you need more space, attach a separate sheet.

Note: If you have a business investment

loss, see Guide T4037.

(1)

Year of

acquisition

(2)

Proceeds of

disposition

(3)

Adjusted cost

base

(4)

Outlays and

expenses (from

dispositions)

(5)

Gain (or loss)

(column 2 minus

columns 3 and 4)

1. Qualified small business

corporation shares

(If you realized a gain on a disposition, you may be able to claim a capital gains

deduction on line 25400 of your return.)

(Report, in section 3 below, publicly traded shares, mutual fund units, deferral of eligible small business corporation

shares, and other shares.)

2. Qualified farm or fishing

property

(If you realized a gain on a disposition, you may be able to claim a capital gains

deduction on line 25400 of your return.)

3. Publicly traded shares, mutual fund units, deferral of eligible small business corporation

shares, and other shares

(Note: If you have capital gains (or losses) on your T5, T5013, T4PS, and T3 information slips,

report them on line 17400 or line 17600.)

4. Real estate, depreciable property, and other properties (see the next page for a principal residence)

10,000.00 (2,000.00)

200,000.00 150,000.00 50,000.00

200,000.00 50,000.00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

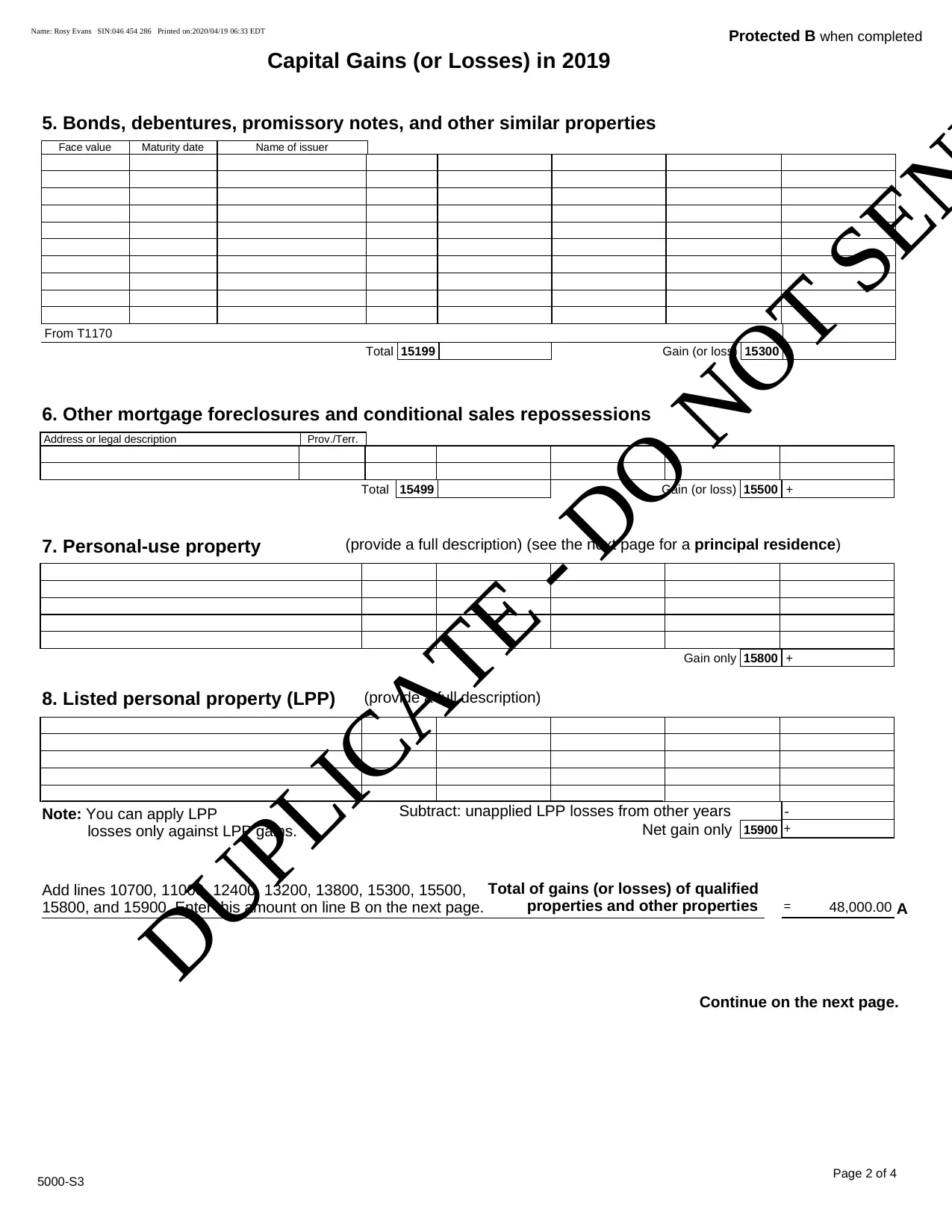

Address or legal description Prov./Terr.

15499 15500Total Gain (or loss)

15800

-

15900

Gain only

Face value Maturity date Name of issuer

15199 15300

From T1170

Total Gain (or loss)

Page 2 of 4

+

+

7. Personal-use property (provide a full description) (see the next page for a principal residence)

8. Listed personal property (LPP) (provide a full description)

Note: You can apply LPP

losses only against LPP gains.

Subtract: unapplied LPP losses from other years

Net gain only

+

+

A

Total of gains (or losses) of qualified

properties and other properties

Add lines 10700, 11000, 12400, 13200, 13800, 15300, 15500,

15800, and 15900. Enter this amount on line B on the next page.

Continue on the next page.

5000-S3

=

6. Other mortgage foreclosures and conditional sales repossessions

5. Bonds, debentures, promissory notes, and other similar properties

Protected B when completed

Capital Gains (or Losses) in 2019

48,000.00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

15499 15500Total Gain (or loss)

15800

-

15900

Gain only

Face value Maturity date Name of issuer

15199 15300

From T1170

Total Gain (or loss)

Page 2 of 4

+

+

7. Personal-use property (provide a full description) (see the next page for a principal residence)

8. Listed personal property (LPP) (provide a full description)

Note: You can apply LPP

losses only against LPP gains.

Subtract: unapplied LPP losses from other years

Net gain only

+

+

A

Total of gains (or losses) of qualified

properties and other properties

Add lines 10700, 11000, 12400, 13200, 13800, 15300, 15500,

15800, and 15900. Enter this amount on line B on the next page.

Continue on the next page.

5000-S3

=

6. Other mortgage foreclosures and conditional sales repossessions

5. Bonds, debentures, promissory notes, and other similar properties

Protected B when completed

Capital Gains (or Losses) in 2019

48,000.00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Protected B when completed

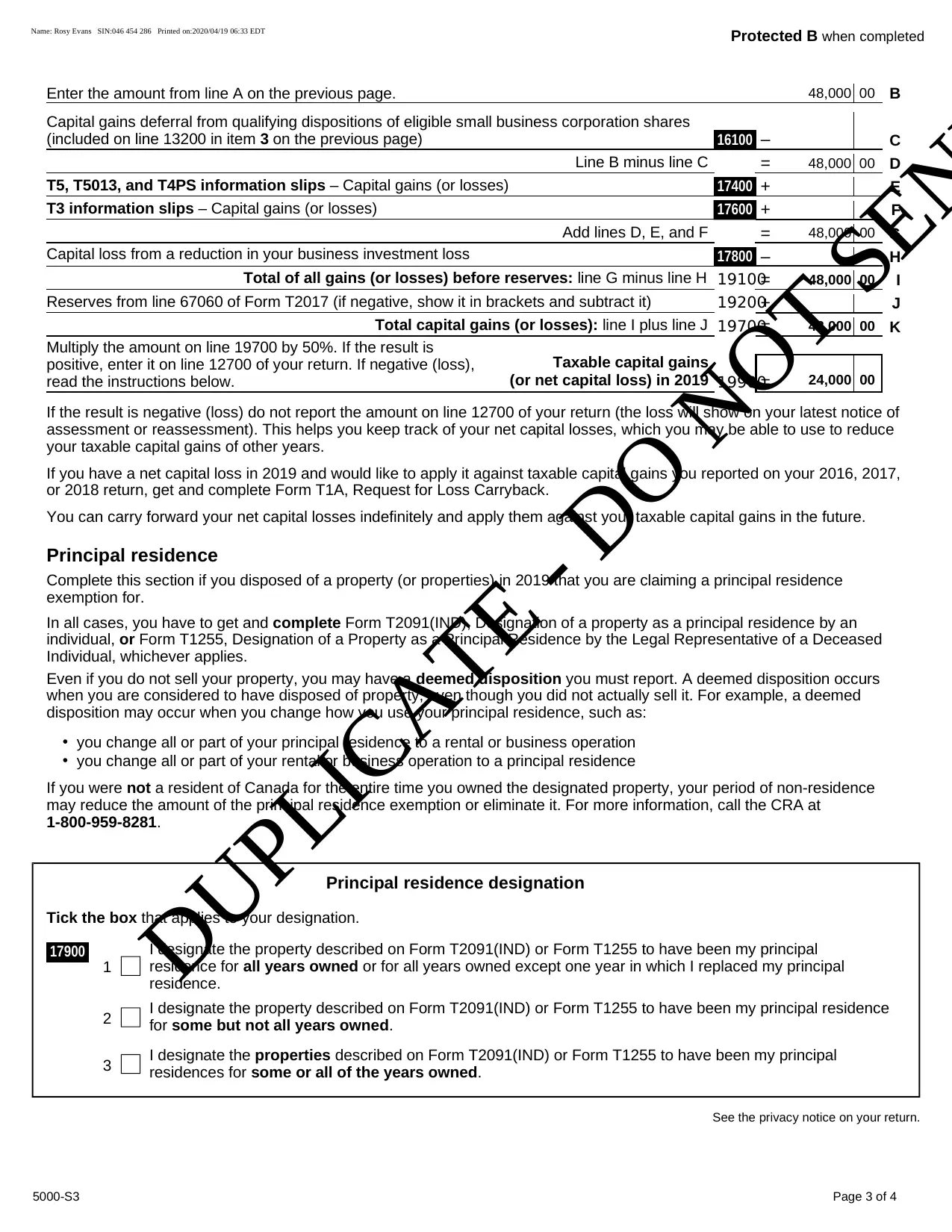

BEnter the amount from line A on the previous page.

16100 C

Capital gains deferral from qualifying dispositions of eligible small business corporation shares

(included on line 13200 in item 3 on the previous page) –

DLine B minus line C =

17400 ET5, T5013, and T4PS information slips – Capital gains (or losses) +

17600 FT3 information slips – Capital gains (or losses) +

GAdd lines D, E, and F =

17800 HCapital loss from a reduction in your business investment loss –

19100 ITotal of all gains (or losses) before reserves: line G minus line H =

19200 JReserves from line 67060 of Form T2017 (if negative, show it in brackets and subtract it) +

19700 KTotal capital gains (or losses): line I plus line J =

19900

Taxable capital gains

(or net capital loss) in 2019

Multiply the amount on line 19700 by 50%. If the result is

positive, enter it on line 12700 of your return. If negative (loss),

read the instructions below. =

If the result is negative (loss) do not report the amount on line 12700 of your return (the loss will show on your latest notice of

assessment or reassessment). This helps you keep track of your net capital losses, which you may be able to use to reduce

your taxable capital gains of other years.

If you have a net capital loss in 2019 and would like to apply it against taxable capital gains you reported on your 2016, 2017,

or 2018 return, get and complete Form T1A, Request for Loss Carryback.

You can carry forward your net capital losses indefinitely and apply them against your taxable capital gains in the future.

Principal residence

Complete this section if you disposed of a property (or properties) in 2019 that you are claiming a principal residence

exemption for.

In all cases, you have to get and complete Form T2091(IND), Designation of a property as a principal residence by an

individual, or Form T1255, Designation of a Property as a Principal Residence by the Legal Representative of a Deceased

Individual, whichever applies.

Even if you do not sell your property, you may have a deemed disposition you must report. A deemed disposition occurs

when you are considered to have disposed of property, even though you did not actually sell it. For example, a deemed

disposition may occur when you change how you use your principal residence, such as:

• you change all or part of your principal residence to a rental or business operation

• you change all or part of your rental or business operation to a principal residence

If you were not a resident of Canada for the entire time you owned the designated property, your period of non-residence

may reduce the amount of the principal residence exemption or eliminate it. For more information, call the CRA at

1-800-959-8281.

Principal residence designation

Tick the box that applies to your designation.

17900

1

I designate the property described on Form T2091(IND) or Form T1255 to have been my principal

residence for all years owned or for all years owned except one year in which I replaced my principal

residence.

2 I designate the property described on Form T2091(IND) or Form T1255 to have been my principal residence

for some but not all years owned.

3 I designate the properties described on Form T2091(IND) or Form T1255 to have been my principal

residences for some or all of the years owned.

See the privacy notice on your return.

5000-S3 Page 3 of 4

48,000 00

48,000 00

48,000 00

48,000 00

48,000 00

24,000 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

BEnter the amount from line A on the previous page.

16100 C

Capital gains deferral from qualifying dispositions of eligible small business corporation shares

(included on line 13200 in item 3 on the previous page) –

DLine B minus line C =

17400 ET5, T5013, and T4PS information slips – Capital gains (or losses) +

17600 FT3 information slips – Capital gains (or losses) +

GAdd lines D, E, and F =

17800 HCapital loss from a reduction in your business investment loss –

19100 ITotal of all gains (or losses) before reserves: line G minus line H =

19200 JReserves from line 67060 of Form T2017 (if negative, show it in brackets and subtract it) +

19700 KTotal capital gains (or losses): line I plus line J =

19900

Taxable capital gains

(or net capital loss) in 2019

Multiply the amount on line 19700 by 50%. If the result is

positive, enter it on line 12700 of your return. If negative (loss),

read the instructions below. =

If the result is negative (loss) do not report the amount on line 12700 of your return (the loss will show on your latest notice of

assessment or reassessment). This helps you keep track of your net capital losses, which you may be able to use to reduce

your taxable capital gains of other years.

If you have a net capital loss in 2019 and would like to apply it against taxable capital gains you reported on your 2016, 2017,

or 2018 return, get and complete Form T1A, Request for Loss Carryback.

You can carry forward your net capital losses indefinitely and apply them against your taxable capital gains in the future.

Principal residence

Complete this section if you disposed of a property (or properties) in 2019 that you are claiming a principal residence

exemption for.

In all cases, you have to get and complete Form T2091(IND), Designation of a property as a principal residence by an

individual, or Form T1255, Designation of a Property as a Principal Residence by the Legal Representative of a Deceased

Individual, whichever applies.

Even if you do not sell your property, you may have a deemed disposition you must report. A deemed disposition occurs

when you are considered to have disposed of property, even though you did not actually sell it. For example, a deemed

disposition may occur when you change how you use your principal residence, such as:

• you change all or part of your principal residence to a rental or business operation

• you change all or part of your rental or business operation to a principal residence

If you were not a resident of Canada for the entire time you owned the designated property, your period of non-residence

may reduce the amount of the principal residence exemption or eliminate it. For more information, call the CRA at

1-800-959-8281.

Principal residence designation

Tick the box that applies to your designation.

17900

1

I designate the property described on Form T2091(IND) or Form T1255 to have been my principal

residence for all years owned or for all years owned except one year in which I replaced my principal

residence.

2 I designate the property described on Form T2091(IND) or Form T1255 to have been my principal residence

for some but not all years owned.

3 I designate the properties described on Form T2091(IND) or Form T1255 to have been my principal

residences for some or all of the years owned.

See the privacy notice on your return.

5000-S3 Page 3 of 4

48,000 00

48,000 00

48,000 00

48,000 00

48,000 00

24,000 00

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

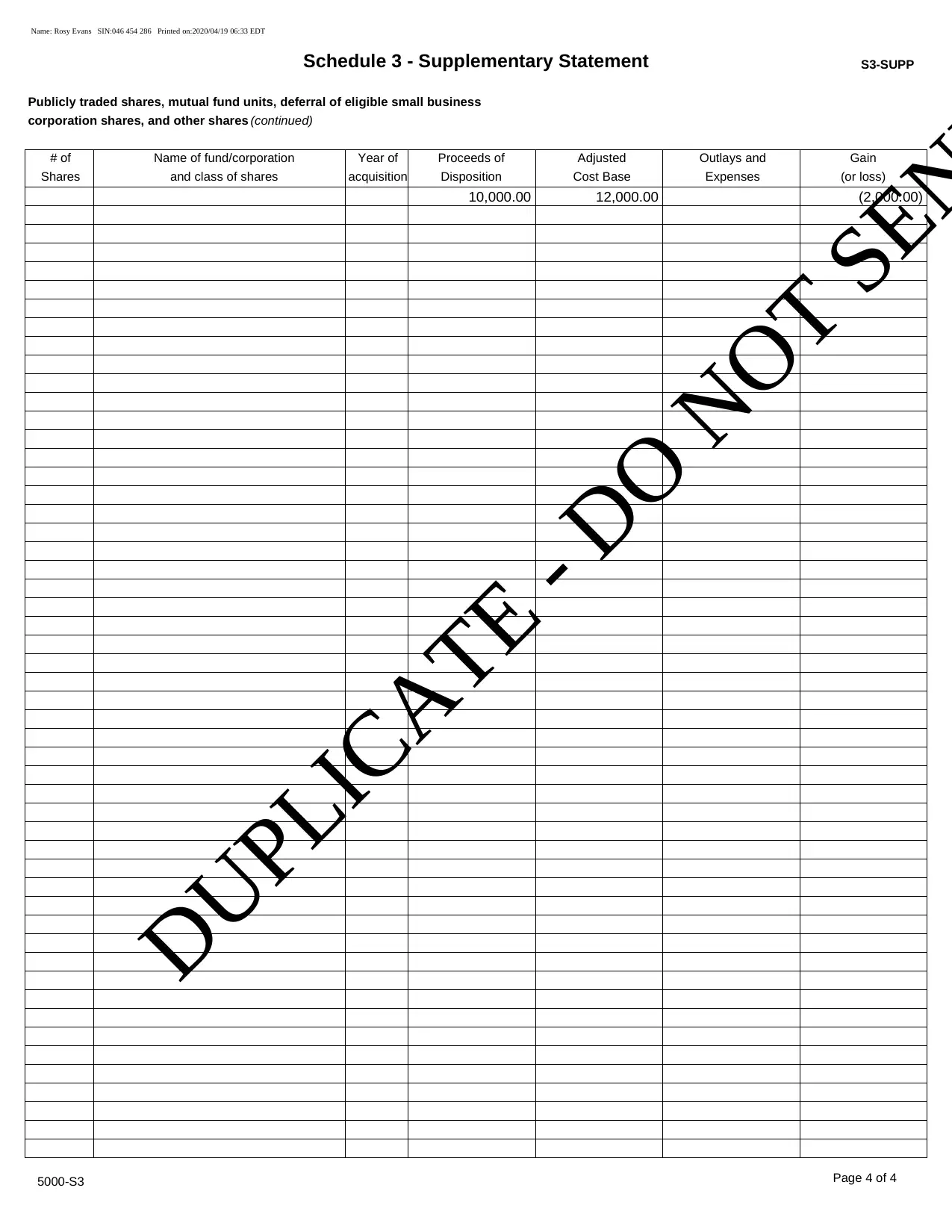

Schedule 3 - Supplementary Statement S3-SUPP

Publicly traded shares, mutual fund units, deferral of eligible small business

corporation shares, and other shares (continued)

# of Name of fund/corporation Year of Proceeds of Adjusted Outlays and Gain

Shares and class of shares acquisition Disposition Cost Base Expenses (or loss)

Page 4 of 45000-S3

10,000.00 12,000.00 (2,000.00)

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

Publicly traded shares, mutual fund units, deferral of eligible small business

corporation shares, and other shares (continued)

# of Name of fund/corporation Year of Proceeds of Adjusted Outlays and Gain

Shares and class of shares acquisition Disposition Cost Base Expenses (or loss)

Page 4 of 45000-S3

10,000.00 12,000.00 (2,000.00)

DUPLICATE - DO NOT SEN

Name: Rosy Evans SIN:046 454 286 Printed on:2020/04/19 06:33 EDT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 54

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.