Fin 340: Investment Portfolio Analysis for Partners Healthcare, Fin

VerifiedAdded on 2022/09/14

|9

|1959

|33

Homework Assignment

AI Summary

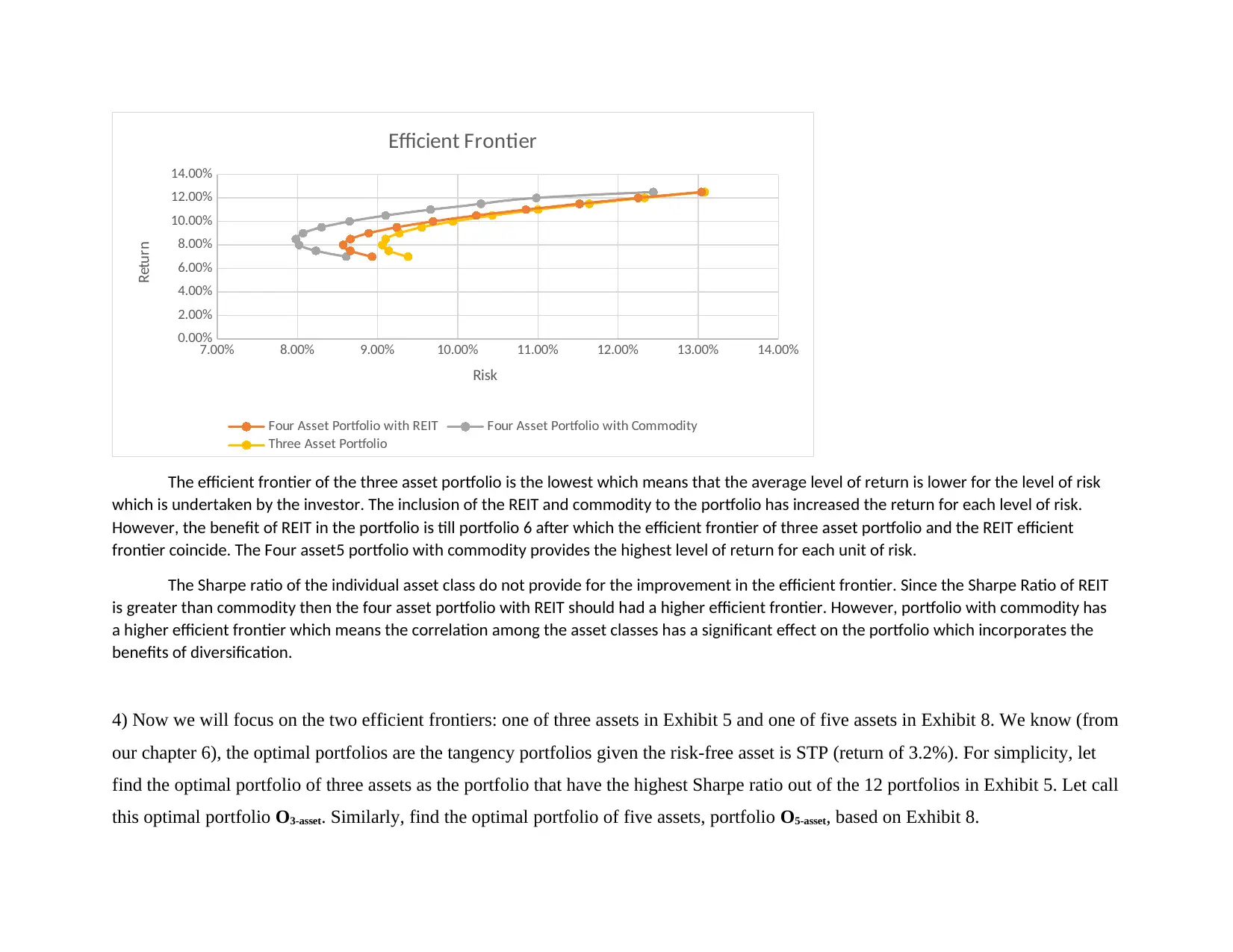

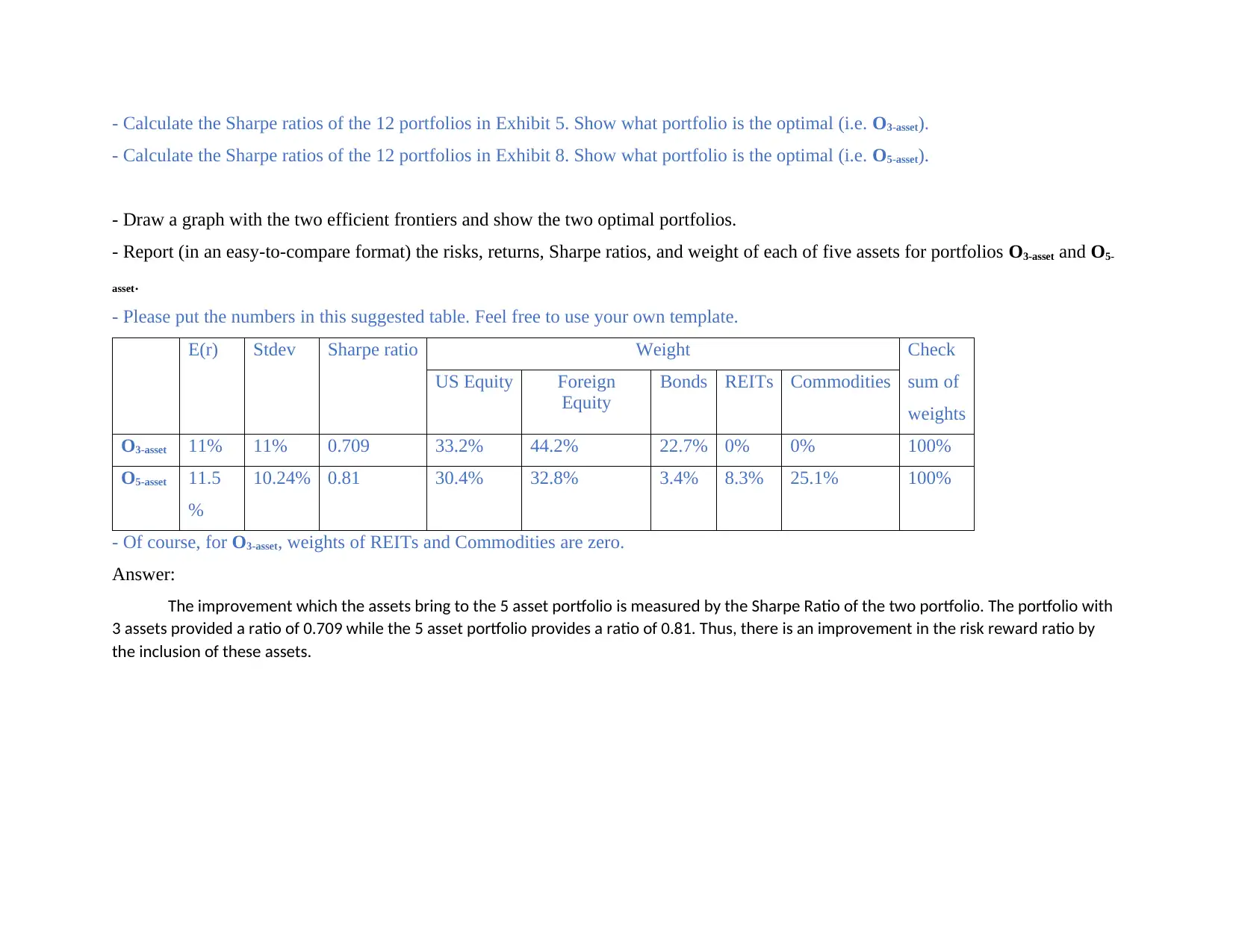

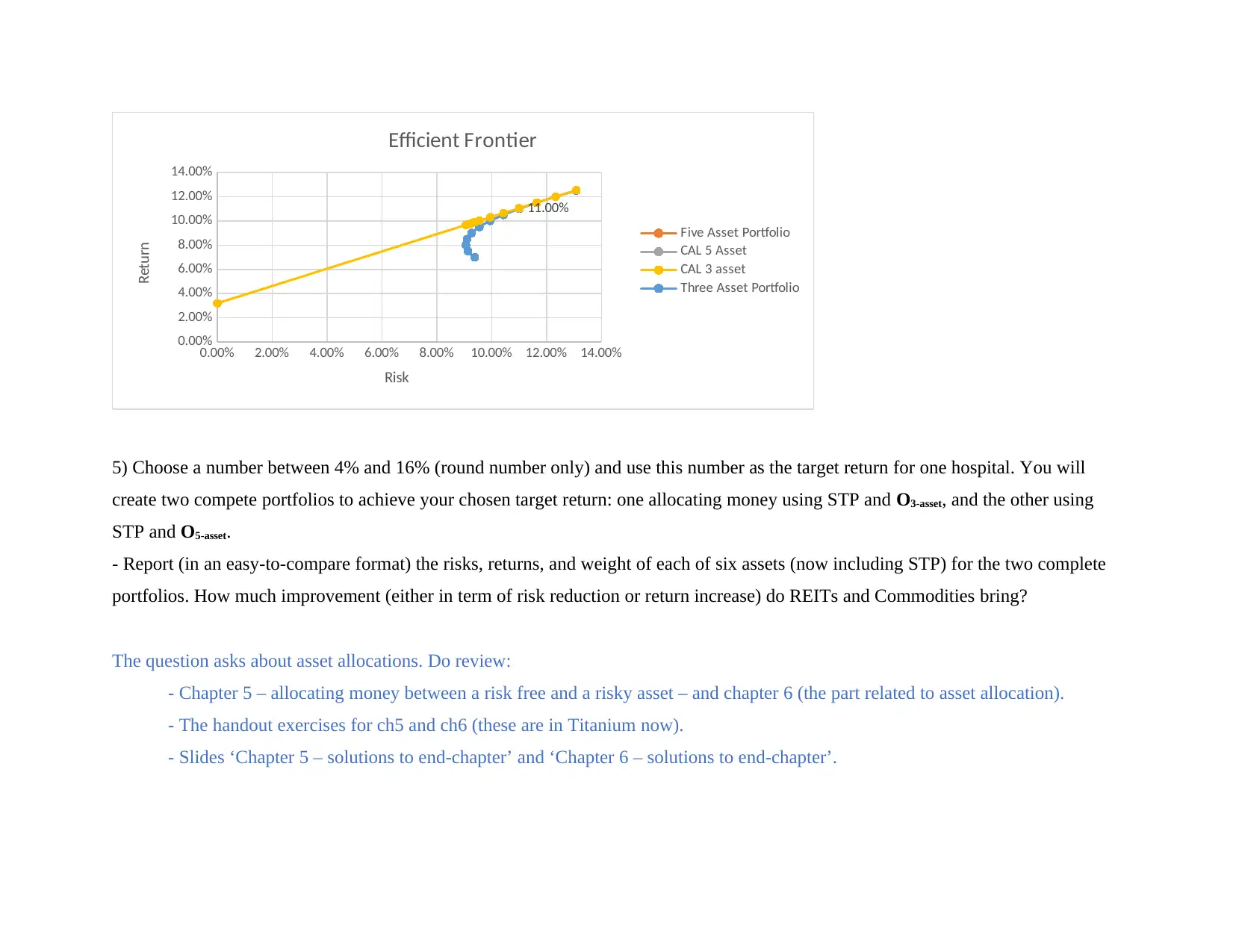

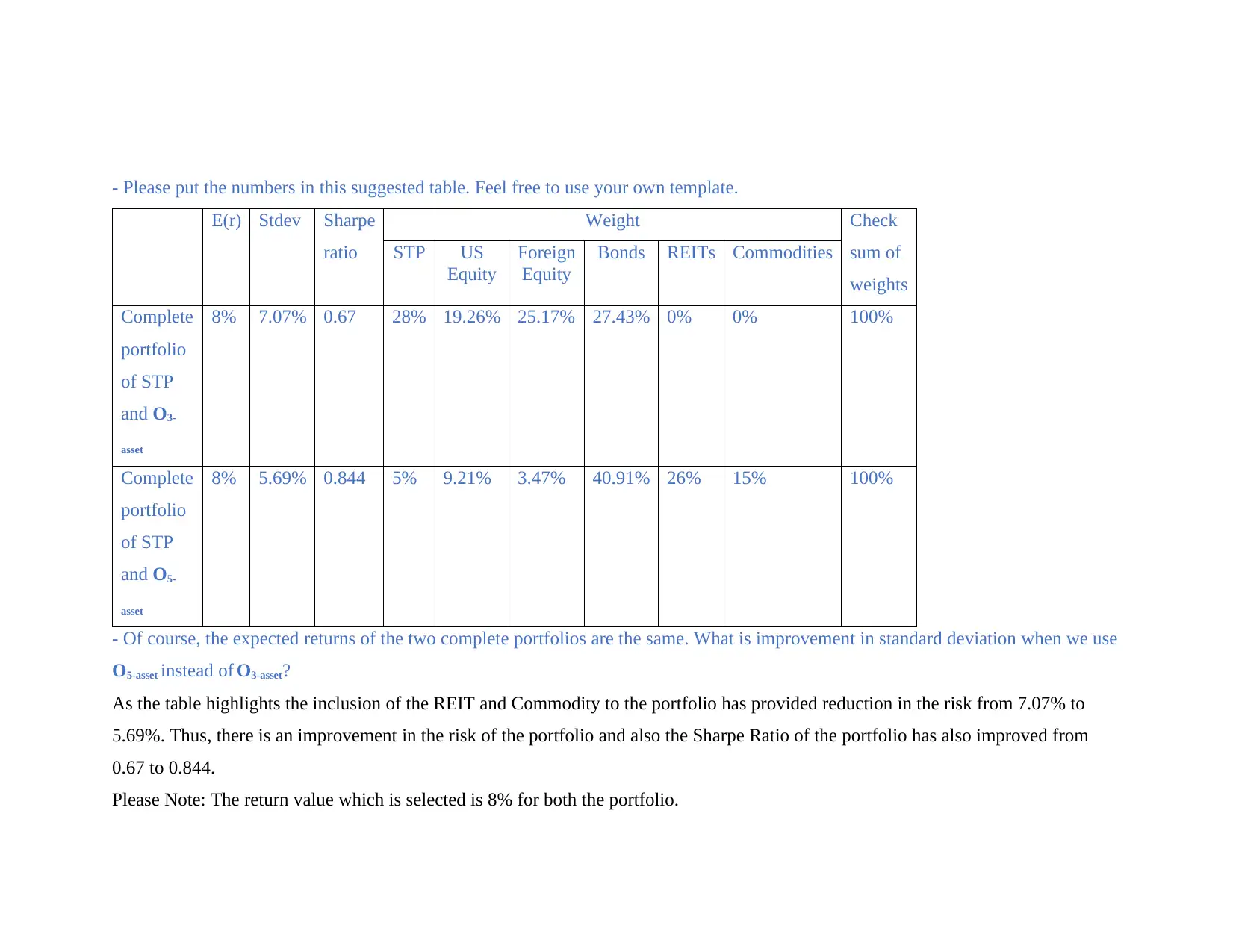

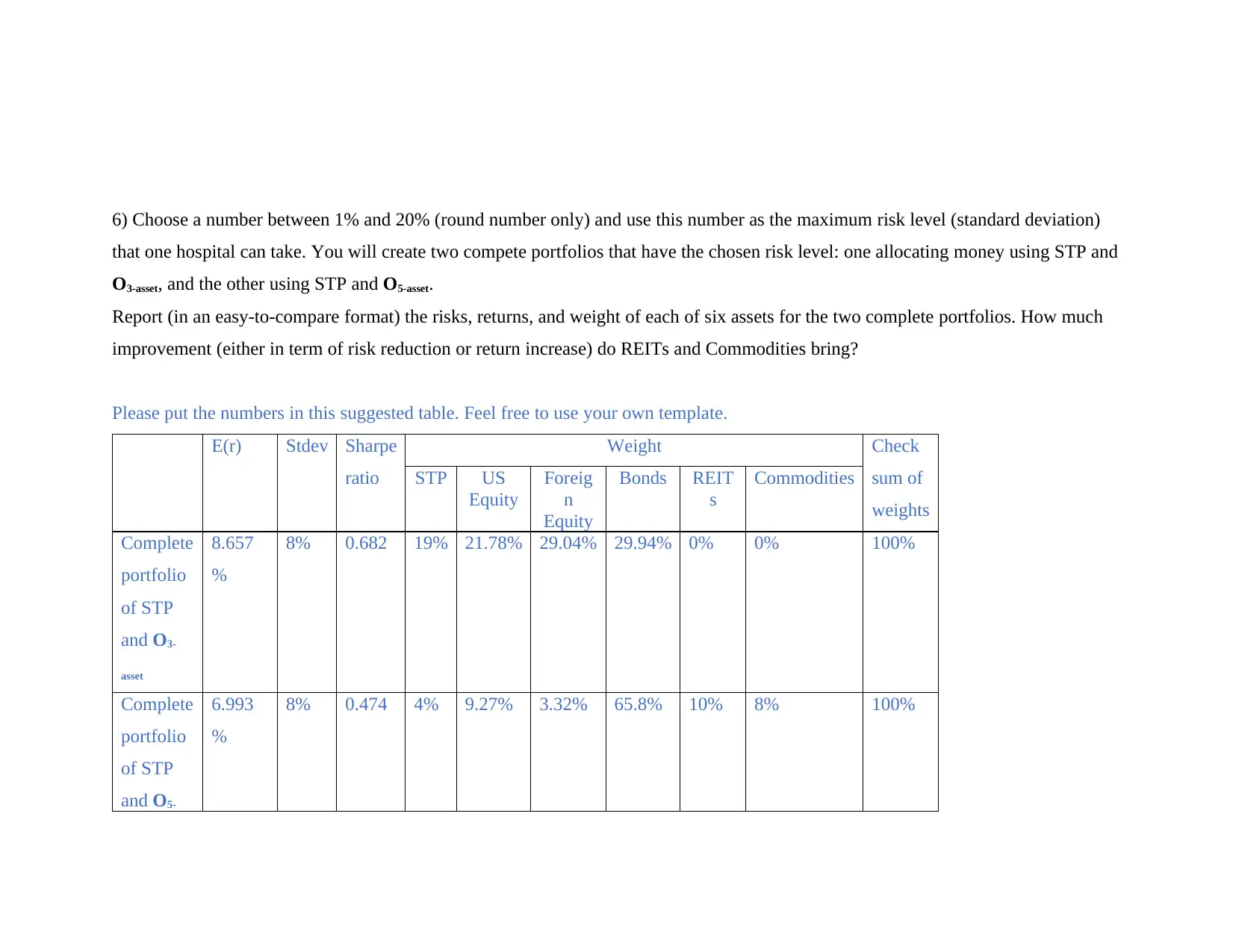

This assignment analyzes investment strategies for Partners Healthcare, focusing on portfolio optimization and risk management. The analysis includes comparing REITs and commodities using Sharpe ratios, recreating efficient frontiers for different asset combinations, and determining optimal portfolio allocations based on target returns and risk levels. The student calculates Sharpe ratios, constructs efficient frontiers, and evaluates the impact of including real estate and commodities on portfolio performance. The assignment also explores asset allocation strategies and presents the results in a comparative format, highlighting the improvements in risk-return profiles with the inclusion of different asset classes. The analysis uses provided exhibits and data to determine the most effective strategies for managing the Partners Healthcare portfolio, considering both return maximization and risk minimization.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.