Financial Accounting Homework: Solutions and Ethics Overview

VerifiedAdded on 2021/04/19

|4

|922

|57

Homework Assignment

AI Summary

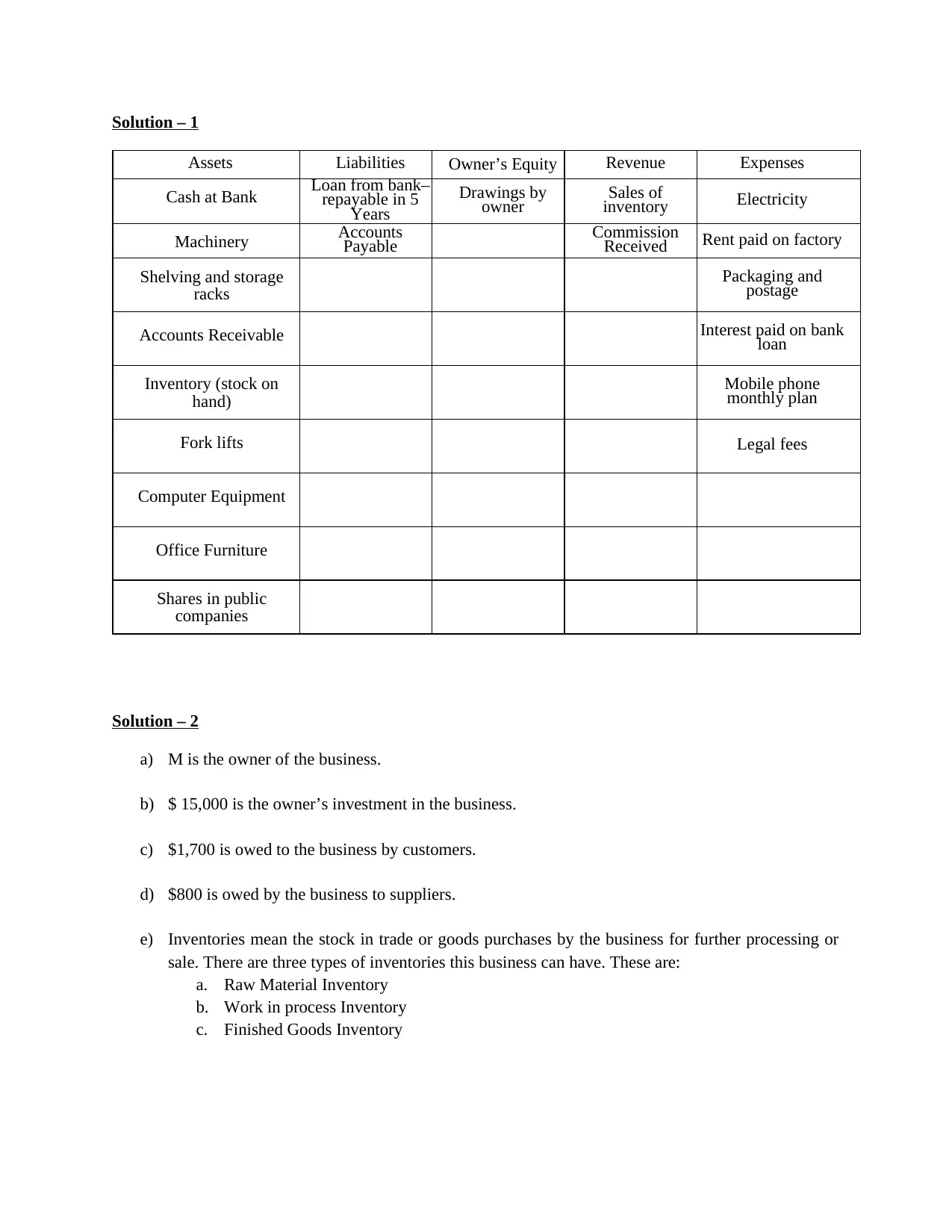

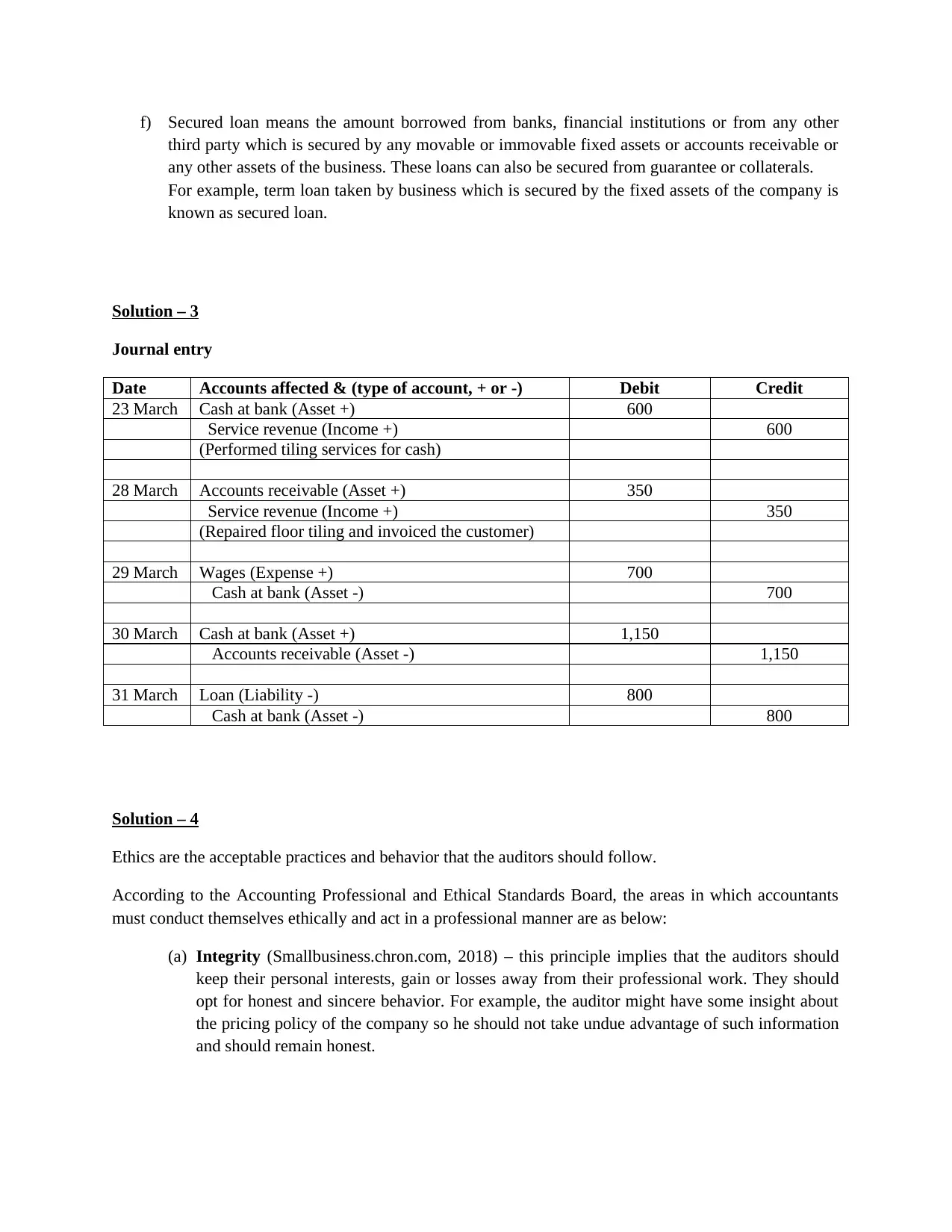

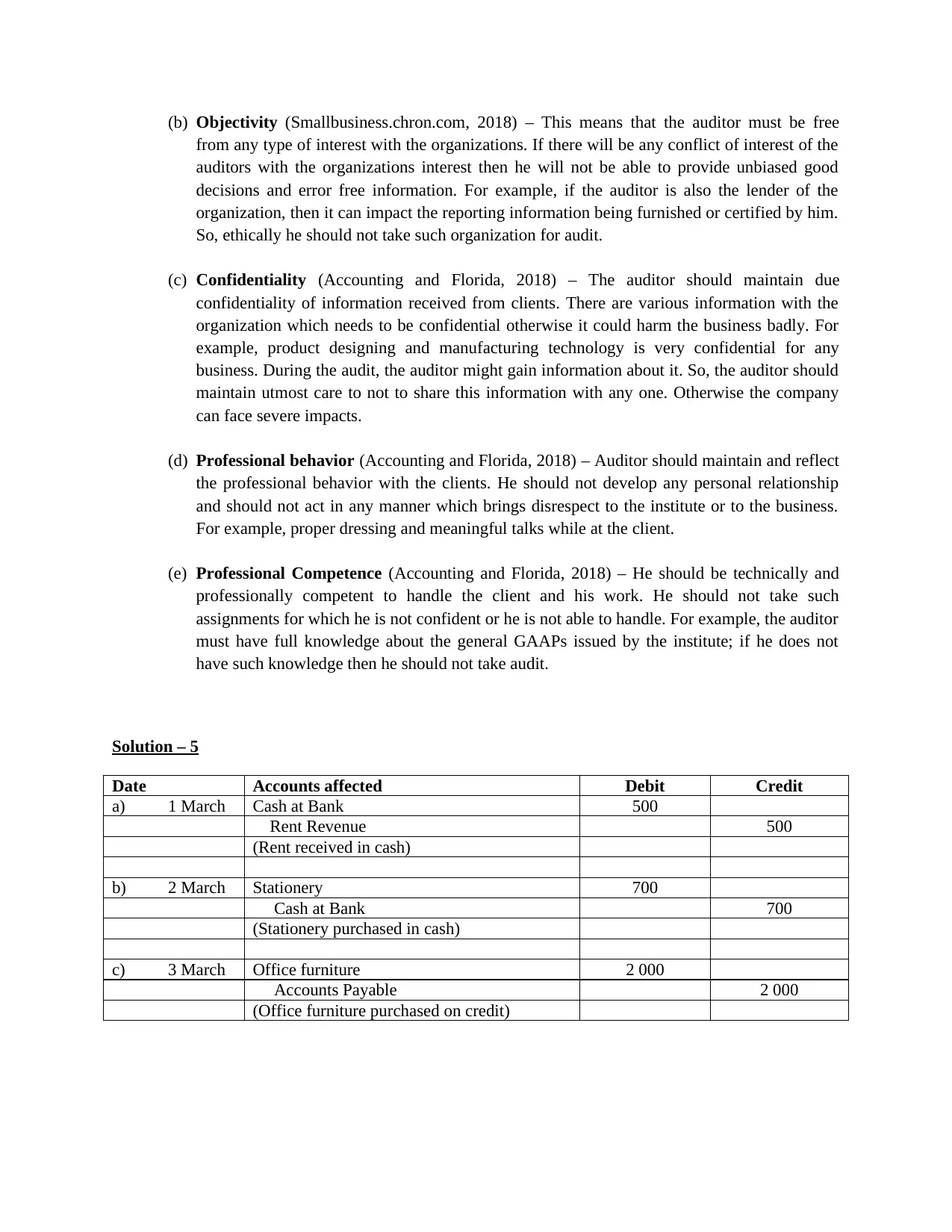

This document provides solutions to a financial accounting assignment. It begins with a breakdown of financial statement elements, including assets, liabilities, owner's equity, revenue, and expenses, along with examples of each. The assignment then presents a scenario involving a business owner's investment, accounts receivable, and payable, and inventory types. The solution includes journal entries for various transactions, such as service revenue, wage payments, and loan adjustments. The document also addresses accounting ethics, outlining key principles like integrity, objectivity, confidentiality, professional behavior, and competence. Finally, it provides journal entries for transactions involving rent revenue, stationery purchases, and office furniture acquired on credit. This resource from Desklib offers students comprehensive accounting solutions.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.