Comprehensive Financial Plan: Investment Options - FIN 1011 Report

VerifiedAdded on 2023/06/12

|9

|2425

|165

Report

AI Summary

This report presents a comprehensive financial plan, focusing on investment options and alternatives for John and Juli Brown. It begins by assessing their current financial situation, including net worth and budget. The report outlines their financial goals, such as purchasing a house and securing their retirement. It then evaluates various investment options, including lending investments like government bonds and GICs, and ownership investments like stocks and mutual funds. The plan details how the Browns can allocate their savings towards a down payment on a house, retirement investments, and insurance, balancing their present needs with future security. The report also includes a cash flow analysis related to a loan application for purchasing a home in North York and investing in securities such as common stock, Canadian government bonds, and mutual funds, to meet both short-term and long-term financial objectives.

FIN 1011

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Current situation.........................................................................................................................3

Net worth................................................................................................................................3

Budget....................................................................................................................................3

Goals and objectives..................................................................................................................3

Alternatives and evaluation of alternatives................................................................................4

Investment Options................................................................................................................4

Preparation of financial plan......................................................................................................7

References..................................................................................................................................9

Current situation.........................................................................................................................3

Net worth................................................................................................................................3

Budget....................................................................................................................................3

Goals and objectives..................................................................................................................3

Alternatives and evaluation of alternatives................................................................................4

Investment Options................................................................................................................4

Preparation of financial plan......................................................................................................7

References..................................................................................................................................9

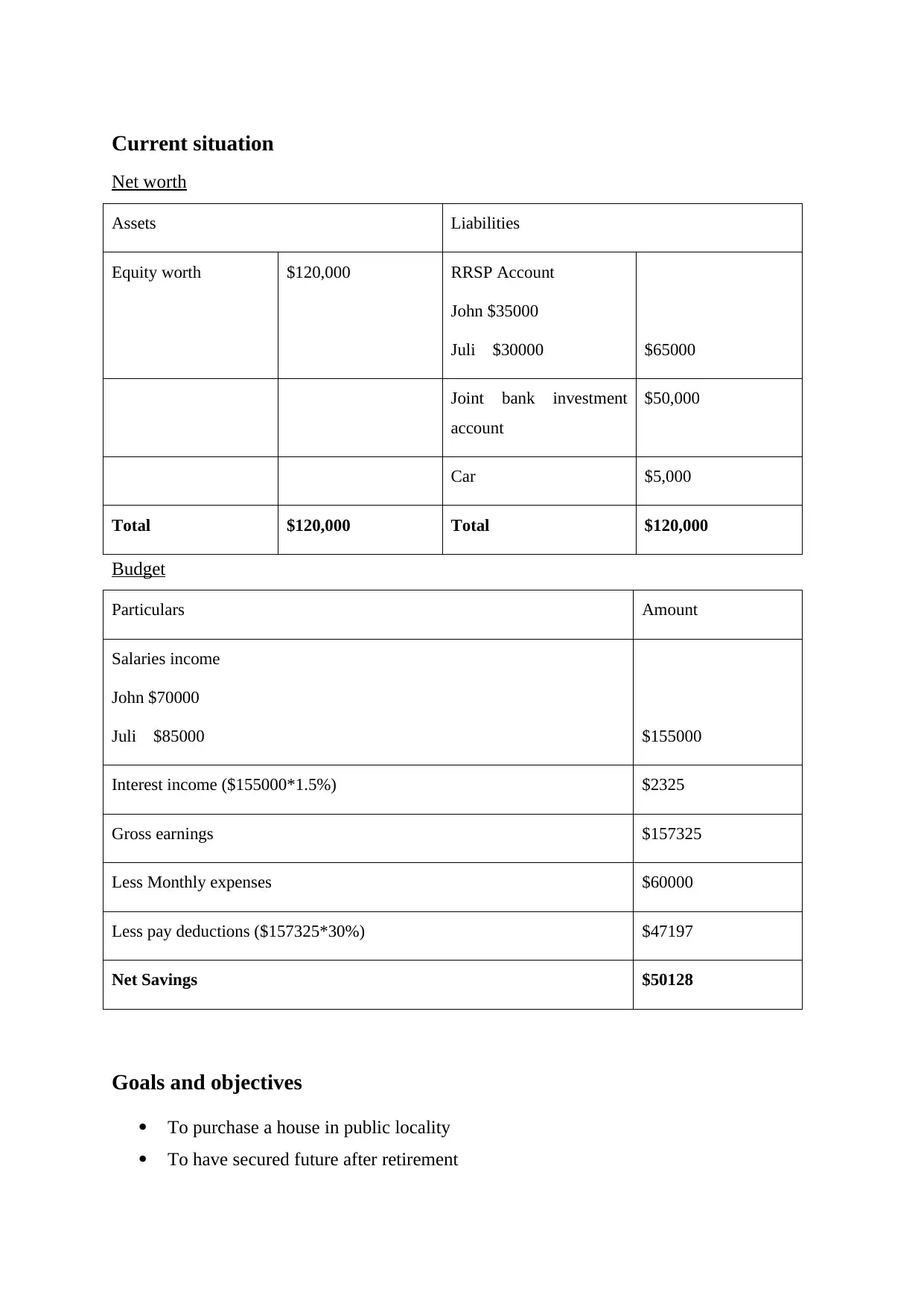

Current situation

Net worth

Assets Liabilities

Equity worth $120,000 RRSP Account

John $35000

Juli $30000 $65000

Joint bank investment

account

$50,000

Car $5,000

Total $120,000 Total $120,000

Budget

Particulars Amount

Salaries income

John $70000

Juli $85000 $155000

Interest income ($155000*1.5%) $2325

Gross earnings $157325

Less Monthly expenses $60000

Less pay deductions ($157325*30%) $47197

Net Savings $50128

Goals and objectives

To purchase a house in public locality

To have secured future after retirement

Net worth

Assets Liabilities

Equity worth $120,000 RRSP Account

John $35000

Juli $30000 $65000

Joint bank investment

account

$50,000

Car $5,000

Total $120,000 Total $120,000

Budget

Particulars Amount

Salaries income

John $70000

Juli $85000 $155000

Interest income ($155000*1.5%) $2325

Gross earnings $157325

Less Monthly expenses $60000

Less pay deductions ($157325*30%) $47197

Net Savings $50128

Goals and objectives

To purchase a house in public locality

To have secured future after retirement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To have secured investments for long term commitments

Alternatives and evaluation of alternatives

Investment Options

There are two main types of investments i.e. ownership and lending. When the

lending investment option is chosen, the party loans its money to an organization, an

individual or a company. In its return, the party gets interest payments. At the conclusion of

the consented loan period, the party will also receive its original investment amount. Lending

investments entail everything from corporate bonds to a savings account, Guaranteed

Investment Certificates and Canada Savings Bonds. On the other hand, an ownership

investment option implies that the party becomes the real owner – or part-owner – of its

investment. Ownership investments are also known as equity investments and entail stocks,

real estate, and ploughing money into a small business (Konstantelos and Strbac, 2015). If the

core property or business rises in value then the value of the share will also increase.

Hence, lender investors lend their money to other party in return of interest payments.

This loan can take the shape of Treasury bill, bond or GIC. In contrast, owner investors

become the real or part owners of the firms in which they make an investment. Therefore,

they get paid a segment of the company’s earnings. Such investors normally buy equity such

as real estate or stocks (Frank and Shen, 2016).

Lending Investments:

Government of Canada Bonds – Federal Bonds are touted to be the safest investment

options. The only risk factor is a nation may default, however it is very improbable

that Canada, which is among the most economically strongest nations will go

bankrupt. For e.g. the same is not true for Greece. As it is highly safe, the interest

received by investors for holding this bond is lower as compared to other bonds. It is

specifically small today due to the immensely low rates of interest. As of October

2011, a five-year Federal Bond gives around 1.61%. Still, if you are apprehensive of

stocks, this is a great means of saving money (Ryan and Young, 2018).

Guaranteed Income Certificates (GICs) – These are similar to bonds, only that the

banks issue them. An investor loans the bank money by purchasing a GIC and on the

maturity of this investment, you receive your money with interest. Banks normally

utilize the dough to finance other investments. The Canada Deposit Insurance

Alternatives and evaluation of alternatives

Investment Options

There are two main types of investments i.e. ownership and lending. When the

lending investment option is chosen, the party loans its money to an organization, an

individual or a company. In its return, the party gets interest payments. At the conclusion of

the consented loan period, the party will also receive its original investment amount. Lending

investments entail everything from corporate bonds to a savings account, Guaranteed

Investment Certificates and Canada Savings Bonds. On the other hand, an ownership

investment option implies that the party becomes the real owner – or part-owner – of its

investment. Ownership investments are also known as equity investments and entail stocks,

real estate, and ploughing money into a small business (Konstantelos and Strbac, 2015). If the

core property or business rises in value then the value of the share will also increase.

Hence, lender investors lend their money to other party in return of interest payments.

This loan can take the shape of Treasury bill, bond or GIC. In contrast, owner investors

become the real or part owners of the firms in which they make an investment. Therefore,

they get paid a segment of the company’s earnings. Such investors normally buy equity such

as real estate or stocks (Frank and Shen, 2016).

Lending Investments:

Government of Canada Bonds – Federal Bonds are touted to be the safest investment

options. The only risk factor is a nation may default, however it is very improbable

that Canada, which is among the most economically strongest nations will go

bankrupt. For e.g. the same is not true for Greece. As it is highly safe, the interest

received by investors for holding this bond is lower as compared to other bonds. It is

specifically small today due to the immensely low rates of interest. As of October

2011, a five-year Federal Bond gives around 1.61%. Still, if you are apprehensive of

stocks, this is a great means of saving money (Ryan and Young, 2018).

Guaranteed Income Certificates (GICs) – These are similar to bonds, only that the

banks issue them. An investor loans the bank money by purchasing a GIC and on the

maturity of this investment, you receive your money with interest. Banks normally

utilize the dough to finance other investments. The Canada Deposit Insurance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporation protects the GICs. Hence, if any bank defaults, the investor will receive

his/her money up to $100,000. The interest earned is dependent on the duration of the

GIC. An investor can buy bonds which have a maturity of just one month or between

1-5 years. The longer the period, the higher the interest rate. However, in time of low

rates of interest, the investor is not seeking great returns; for e.g. Ally’s 5-year GIC

pays 2.75%, the highest of the lot (Gotze, Northcott and Schuster, 2016). The investor

cannot sell GICs, hence majority people utilize them to park some money for a short

time period. If a person know that he/she will have to purchase a car next year, then

they may invest in GIC. On its maturity, the person will make a little more money

than what he would get from a standard bank account.

High-yield savings account – If an investor wants to deposit some cash in the bank, he

may consider a high-yield saving account. This account gives higher rate of interest as

compared to regular savings account, although some need a minimum balance to get

the high rate (Subramani, 2011).

Corporate bonds – Corporate bonds could be risky, however, they can provide the

portfolio with much-required income infusion. Basically, the investor is loaning a

business money and is getting interest in return. A company has more chances of

becoming bankrupt than a nation, hence investors receive higher rate of interest on

corporate bonds than on federal bonds. These bonds are still safer option than stocks

but ensure sticking to highly-rated bonds only (Gupta, 2017).

Owner Investments:

Stocks – Stocks are issued by companies wherein the investor is made the part-owner

of the company by purchasing its shares. There are two main types of stocks:

preferred and common. Trading of stocks is done on stock exchanges or over-the-

counter. Returns and prices of shares fluctuate immensely and there is no surety of

income (Daily, Kieff and Wilmarth, 2014).

o Common stock - With common shares/stock, investors enjoy voting rights.

These shares are normally bought for likely capital appreciation. If the firm

makes money, its investors have share in the profits. But, if the firm has a

weak year and is suffering losses or the market declines, then the share value

falls and dividends are scarce. Blue chip stocks are normally stocks of big,

his/her money up to $100,000. The interest earned is dependent on the duration of the

GIC. An investor can buy bonds which have a maturity of just one month or between

1-5 years. The longer the period, the higher the interest rate. However, in time of low

rates of interest, the investor is not seeking great returns; for e.g. Ally’s 5-year GIC

pays 2.75%, the highest of the lot (Gotze, Northcott and Schuster, 2016). The investor

cannot sell GICs, hence majority people utilize them to park some money for a short

time period. If a person know that he/she will have to purchase a car next year, then

they may invest in GIC. On its maturity, the person will make a little more money

than what he would get from a standard bank account.

High-yield savings account – If an investor wants to deposit some cash in the bank, he

may consider a high-yield saving account. This account gives higher rate of interest as

compared to regular savings account, although some need a minimum balance to get

the high rate (Subramani, 2011).

Corporate bonds – Corporate bonds could be risky, however, they can provide the

portfolio with much-required income infusion. Basically, the investor is loaning a

business money and is getting interest in return. A company has more chances of

becoming bankrupt than a nation, hence investors receive higher rate of interest on

corporate bonds than on federal bonds. These bonds are still safer option than stocks

but ensure sticking to highly-rated bonds only (Gupta, 2017).

Owner Investments:

Stocks – Stocks are issued by companies wherein the investor is made the part-owner

of the company by purchasing its shares. There are two main types of stocks:

preferred and common. Trading of stocks is done on stock exchanges or over-the-

counter. Returns and prices of shares fluctuate immensely and there is no surety of

income (Daily, Kieff and Wilmarth, 2014).

o Common stock - With common shares/stock, investors enjoy voting rights.

These shares are normally bought for likely capital appreciation. If the firm

makes money, its investors have share in the profits. But, if the firm has a

weak year and is suffering losses or the market declines, then the share value

falls and dividends are scarce. Blue chip stocks are normally stocks of big,

stable and actively traded corporations with a history of regular payment of

dividends. Penny stocks refer to low-cost common shares which are valued

under $1. These are bought for speculative intentions and issued by unproven

companies or start-ups seeking money for expansion (Anderson and Haslem,

2015). Small, mid and large-cap shares are the outcomes of companies of all

sizes issuing common stock to raise funds. Usually, the smaller the company,

the greater the risk.

o Preferred shares - These are considered as bond-like investments. Preferred

stocks are usually bought by investors who require a consistent stream of

dividends instead of capital appreciation. Dividend paid on these shares is

higher yielding as compared to common shares. The share price and value are

influenced more by trends in interest rate than company earning. The

shareholders do not have voting rights normally. They are preferred as the

investors receive preferential claim to the assets and profits before common

stockholders (Ju, Leland and Senbet, 2014).

Precious Metals – These include gold, silver, platinum and other precious metals.

Precious metals are held in form of certificates of ownership or bullion i.e. the real

metal.

Commodities – These include bulk goods like oil, grains, foods and metals and are

traded on commodities exchange (Jordan, 2014).

Derivatives – These are securities whose value is dependent on the market value of

some other thing like commodity or stock. They are intricate investments utilized by

sophisticated investors for the purpose of speculation or to aid in risk management for

e.g. as a hedge against altering market conditions. Futures and Options are examples

of derivatives. A “Futures” contract bounds the investor to purchase or sell a

particular amount of asset at a decided price on a set date. An “Options” gives the

investor the freedom to purchase or sell a particular security at a decided price before

the set date (Hull and Basu, 2016).

Mutual Funds – This is an investment product composed of many investors’

contributions, wherein a professional money manager invests in a range of securities.

dividends. Penny stocks refer to low-cost common shares which are valued

under $1. These are bought for speculative intentions and issued by unproven

companies or start-ups seeking money for expansion (Anderson and Haslem,

2015). Small, mid and large-cap shares are the outcomes of companies of all

sizes issuing common stock to raise funds. Usually, the smaller the company,

the greater the risk.

o Preferred shares - These are considered as bond-like investments. Preferred

stocks are usually bought by investors who require a consistent stream of

dividends instead of capital appreciation. Dividend paid on these shares is

higher yielding as compared to common shares. The share price and value are

influenced more by trends in interest rate than company earning. The

shareholders do not have voting rights normally. They are preferred as the

investors receive preferential claim to the assets and profits before common

stockholders (Ju, Leland and Senbet, 2014).

Precious Metals – These include gold, silver, platinum and other precious metals.

Precious metals are held in form of certificates of ownership or bullion i.e. the real

metal.

Commodities – These include bulk goods like oil, grains, foods and metals and are

traded on commodities exchange (Jordan, 2014).

Derivatives – These are securities whose value is dependent on the market value of

some other thing like commodity or stock. They are intricate investments utilized by

sophisticated investors for the purpose of speculation or to aid in risk management for

e.g. as a hedge against altering market conditions. Futures and Options are examples

of derivatives. A “Futures” contract bounds the investor to purchase or sell a

particular amount of asset at a decided price on a set date. An “Options” gives the

investor the freedom to purchase or sell a particular security at a decided price before

the set date (Hull and Basu, 2016).

Mutual Funds – This is an investment product composed of many investors’

contributions, wherein a professional money manager invests in a range of securities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This wealth pool may be invested in a particular market of geographical region, in

small company stocks or in blue-chip firms. The manager oversees the investments on

a continual basis. These funds are attractive as they provide access to a broad variety

of investments, are extensively available and are simple to purchase (Frankel and

Laby, 2015). All mutual funds levy Management Expense Ratio which is the cost of

operating and managing a fund. There are other fees as well like initial fee,

acquisition fee, and selling fee.

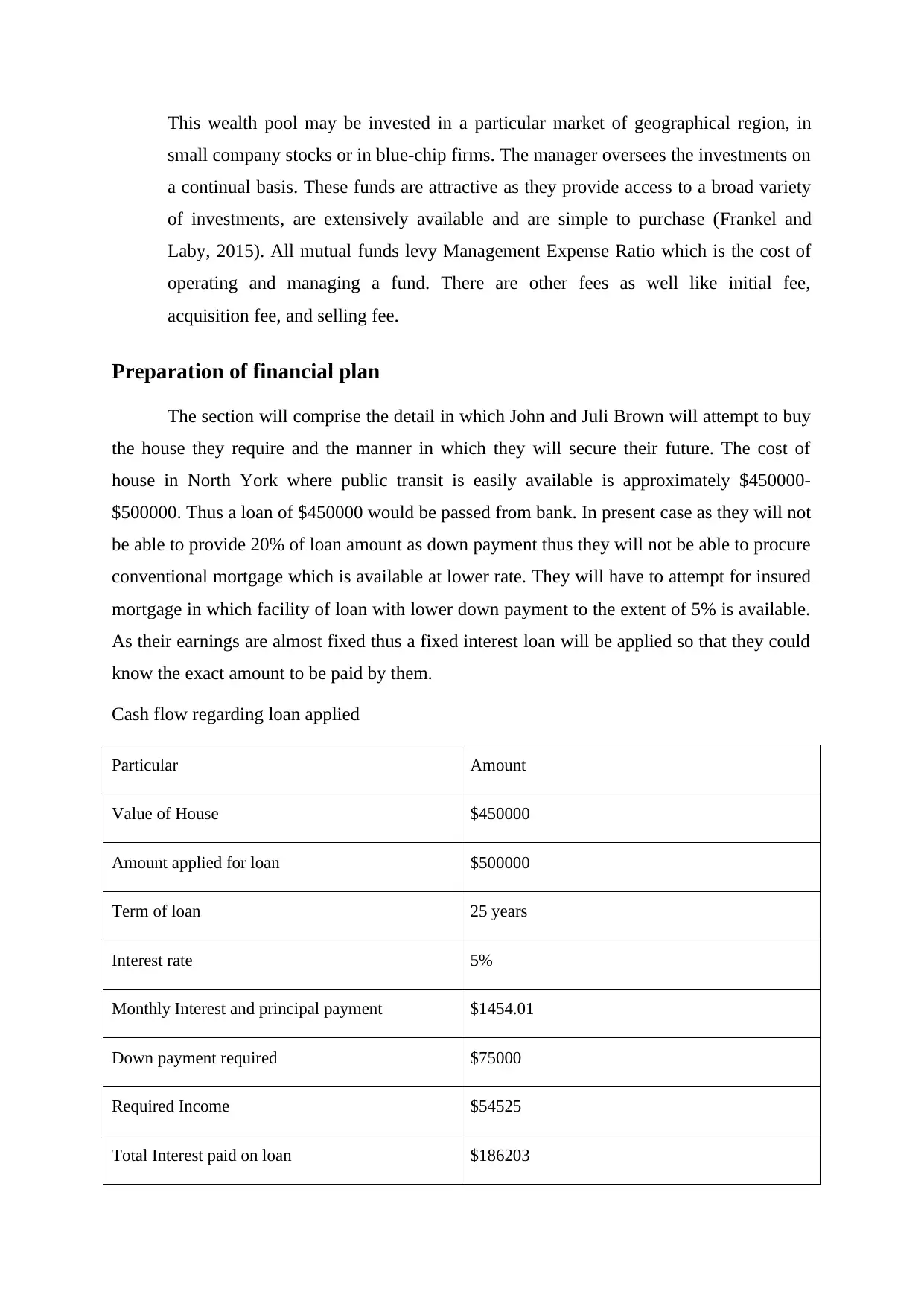

Preparation of financial plan

The section will comprise the detail in which John and Juli Brown will attempt to buy

the house they require and the manner in which they will secure their future. The cost of

house in North York where public transit is easily available is approximately $450000-

$500000. Thus a loan of $450000 would be passed from bank. In present case as they will not

be able to provide 20% of loan amount as down payment thus they will not be able to procure

conventional mortgage which is available at lower rate. They will have to attempt for insured

mortgage in which facility of loan with lower down payment to the extent of 5% is available.

As their earnings are almost fixed thus a fixed interest loan will be applied so that they could

know the exact amount to be paid by them.

Cash flow regarding loan applied

Particular Amount

Value of House $450000

Amount applied for loan $500000

Term of loan 25 years

Interest rate 5%

Monthly Interest and principal payment $1454.01

Down payment required $75000

Required Income $54525

Total Interest paid on loan $186203

small company stocks or in blue-chip firms. The manager oversees the investments on

a continual basis. These funds are attractive as they provide access to a broad variety

of investments, are extensively available and are simple to purchase (Frankel and

Laby, 2015). All mutual funds levy Management Expense Ratio which is the cost of

operating and managing a fund. There are other fees as well like initial fee,

acquisition fee, and selling fee.

Preparation of financial plan

The section will comprise the detail in which John and Juli Brown will attempt to buy

the house they require and the manner in which they will secure their future. The cost of

house in North York where public transit is easily available is approximately $450000-

$500000. Thus a loan of $450000 would be passed from bank. In present case as they will not

be able to provide 20% of loan amount as down payment thus they will not be able to procure

conventional mortgage which is available at lower rate. They will have to attempt for insured

mortgage in which facility of loan with lower down payment to the extent of 5% is available.

As their earnings are almost fixed thus a fixed interest loan will be applied so that they could

know the exact amount to be paid by them.

Cash flow regarding loan applied

Particular Amount

Value of House $450000

Amount applied for loan $500000

Term of loan 25 years

Interest rate 5%

Monthly Interest and principal payment $1454.01

Down payment required $75000

Required Income $54525

Total Interest paid on loan $186203

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total monthly payments $436197

Amount available for investment and other expenses after payment of principal and interest

amount of loan:

Net saving of John and Juli after expending their all required expenditure is $50128

Amount to be paid for loan every year (1454.01*12) $17450

Net amount retained for other expenses and savings $32678

Note: In present case as the amount to be paid for down payment is higher than

amount available as net saving to both the assessee. Thus, a higher amount of loan has been

applied so that the difference can be arranged and in case any modifications are required in

house than amount for same can be also made available.

The amount which is available after payment of loan expenses (interest and payment)

$32678, $25000 will be applied for investment purpose in retirement and other investment in

above specified securities and remain amount will be retained in case there is any emergency.

It is necessary to invest in retirement plan as they same lead to balance the

requirement of present as well as the need of tomorrow. Income tax on same will be paid at

the time when money is withdrawn and the same will done through government pension

scheme in order to remain more secured. A part of saving will also be invested in insurance in

order to secure future of their child in case they face any accident or other issue. The amount

will be invested in following manner in specified securities:

Type of Investment Proportionate of amount which will be invested

Common stock 20%

Canadian government Bonds 20%

Mutual Fund 40%

Insurance 20%

Amount available for investment and other expenses after payment of principal and interest

amount of loan:

Net saving of John and Juli after expending their all required expenditure is $50128

Amount to be paid for loan every year (1454.01*12) $17450

Net amount retained for other expenses and savings $32678

Note: In present case as the amount to be paid for down payment is higher than

amount available as net saving to both the assessee. Thus, a higher amount of loan has been

applied so that the difference can be arranged and in case any modifications are required in

house than amount for same can be also made available.

The amount which is available after payment of loan expenses (interest and payment)

$32678, $25000 will be applied for investment purpose in retirement and other investment in

above specified securities and remain amount will be retained in case there is any emergency.

It is necessary to invest in retirement plan as they same lead to balance the

requirement of present as well as the need of tomorrow. Income tax on same will be paid at

the time when money is withdrawn and the same will done through government pension

scheme in order to remain more secured. A part of saving will also be invested in insurance in

order to secure future of their child in case they face any accident or other issue. The amount

will be invested in following manner in specified securities:

Type of Investment Proportionate of amount which will be invested

Common stock 20%

Canadian government Bonds 20%

Mutual Fund 40%

Insurance 20%

References

Anderson, R. N., & Haslem, J. A. (2015). Common Stock Valuation Models: Estimation of

the Discount Rate Using the Geometric-Mean Criterion.

DAILY, J. E., KIEFF, F. S., & WILMARTH JR, A. E. (2014). Introduction. In Perspectives

on Financing Innovation (pp. 13-16). Routledge.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of

capital. Journal of Financial Economics, 119(2), 300-315.

Frankel, T., & Laby, A. B. (2015). The Regulation of Money Managers: Mutual Funds and

Advisers (Vol. 3). Wolters Kluwer Law & Business.

Gotze, U., Northcott, D., & Schuster, P. (2016). INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

Gupta, M. (2017). KEYWORDS Investor Attitudes, Investment Alternatives, Sampling

Method, Questionnaire Method. A STUDY FOR ATTITUDE OF INVESTORS

TOWARDS VARIOUS INVESTMENT ALTERNATIVES., (183).

Hull, J. C., & Basu, S. (2016). Options, futures, and other derivatives. Pearson Education

India.

Jordan, B. (2014). Fundamentals of investments. McGraw-Hill Higher Education.

Ju, N., Leland, H., & Senbet, L. W. (2014). Options, option repricing in managerial

compensation: Their effects on corporate investment risk. Journal of Corporate

Finance, 29, 628-643.

Konstantelos, I., & Strbac, G. (2015). Valuation of flexible transmission investment options

under uncertainty. IEEE Transactions on Power systems, 30(2), 1047-1055.

Ryan, S., & Young, M. (2018). Social impact bonds: the next horizon of

privatization. Studies in Political Economy, 99(1), 42-58.

Subramani, R.V. (2011). Accounting for Investments, Equities, Futures and Options. John

Wiley & Sons.

Anderson, R. N., & Haslem, J. A. (2015). Common Stock Valuation Models: Estimation of

the Discount Rate Using the Geometric-Mean Criterion.

DAILY, J. E., KIEFF, F. S., & WILMARTH JR, A. E. (2014). Introduction. In Perspectives

on Financing Innovation (pp. 13-16). Routledge.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of

capital. Journal of Financial Economics, 119(2), 300-315.

Frankel, T., & Laby, A. B. (2015). The Regulation of Money Managers: Mutual Funds and

Advisers (Vol. 3). Wolters Kluwer Law & Business.

Gotze, U., Northcott, D., & Schuster, P. (2016). INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

Gupta, M. (2017). KEYWORDS Investor Attitudes, Investment Alternatives, Sampling

Method, Questionnaire Method. A STUDY FOR ATTITUDE OF INVESTORS

TOWARDS VARIOUS INVESTMENT ALTERNATIVES., (183).

Hull, J. C., & Basu, S. (2016). Options, futures, and other derivatives. Pearson Education

India.

Jordan, B. (2014). Fundamentals of investments. McGraw-Hill Higher Education.

Ju, N., Leland, H., & Senbet, L. W. (2014). Options, option repricing in managerial

compensation: Their effects on corporate investment risk. Journal of Corporate

Finance, 29, 628-643.

Konstantelos, I., & Strbac, G. (2015). Valuation of flexible transmission investment options

under uncertainty. IEEE Transactions on Power systems, 30(2), 1047-1055.

Ryan, S., & Young, M. (2018). Social impact bonds: the next horizon of

privatization. Studies in Political Economy, 99(1), 42-58.

Subramani, R.V. (2011). Accounting for Investments, Equities, Futures and Options. John

Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.