FIN200 Trimester 2 Assignment: Analyzing CML, SML, and CAPM Model

VerifiedAdded on 2023/06/07

|12

|2832

|378

Report

AI Summary

This report provides a detailed analysis of Capital Market Line (CML) and Security Market Line (SML), highlighting their differences in risk evaluation and application in investment decisions. It discusses the significance of minimum variance portfolios in supporting conservative investment strategies and diversifying financial instruments to reduce risk. Furthermore, the report explores the Capital Asset Pricing Model (CAPM), emphasizing its relevance in calculating expected returns and its simplicity compared to alternative models, while also acknowledging its limitations. The assessment concludes that understanding these financial theories is crucial for investors in managing risk and optimizing portfolio returns. Desklib offers a range of solved assignments and study resources to aid students in mastering these concepts.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

1

Table of Contents

Introduction:...............................................................................................................................2

Capital Market Line and Security Market Line difference:.......................................................2

Minimum variance portfolio Significance:................................................................................5

CAPM calculation description and analysis:.............................................................................7

Conclusion:................................................................................................................................9

References:...............................................................................................................................10

1

Table of Contents

Introduction:...............................................................................................................................2

Capital Market Line and Security Market Line difference:.......................................................2

Minimum variance portfolio Significance:................................................................................5

CAPM calculation description and analysis:.............................................................................7

Conclusion:................................................................................................................................9

References:...............................................................................................................................10

CORPORATE FINANCE

2

Introduction:

There is significant level of risk exposures that is faced by investors, while making

investment decisions. This increment in risk exposures of the investors is relatively controlled

with the help of different level of theories and calculations. The exploration of the theories

such as Capital Market Line and Security Market Line can help in detecting the different

level of risk exposures, which the investors needs to take into consideration before

conducting the relevant investment decisions. Therefore, with the use of SML and CML

might help in detecting the different level of risk exposures of the company such as

systematic and unsystematic risk. The minimum variance portfolio has relevant significance,

which directly helps in supporting the level of conservative investment nature of the investor.

Lastly, the Capital asset pricing model has been considered to be one the rising factors, which

has allowed the investors to detect the level of expected returns of the stock. The above

identified theories and calculations has mainly allowed the investor for detecting the level of

risk exposure, which needs to be taken into consideration before conducting investments.

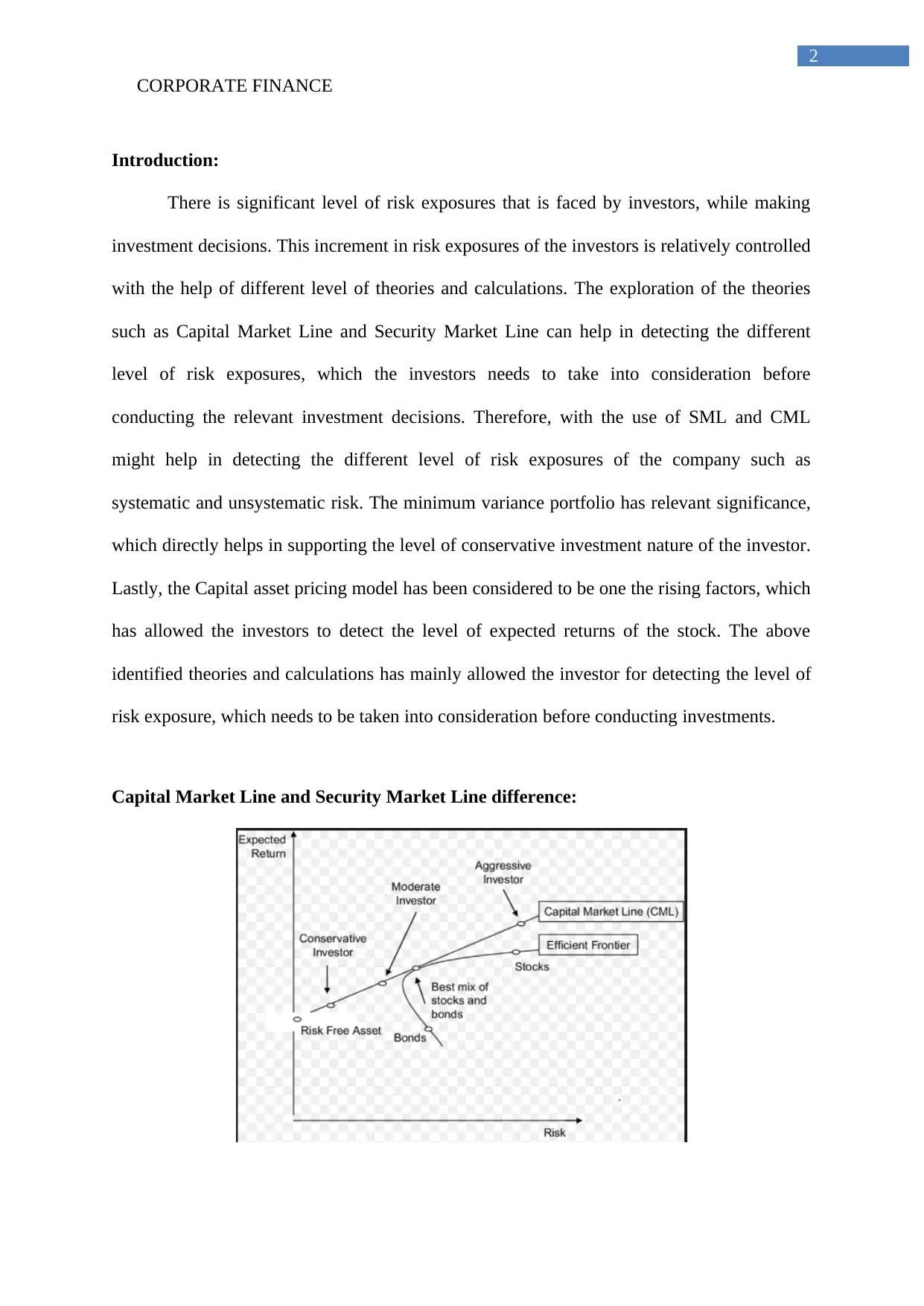

Capital Market Line and Security Market Line difference:

2

Introduction:

There is significant level of risk exposures that is faced by investors, while making

investment decisions. This increment in risk exposures of the investors is relatively controlled

with the help of different level of theories and calculations. The exploration of the theories

such as Capital Market Line and Security Market Line can help in detecting the different

level of risk exposures, which the investors needs to take into consideration before

conducting the relevant investment decisions. Therefore, with the use of SML and CML

might help in detecting the different level of risk exposures of the company such as

systematic and unsystematic risk. The minimum variance portfolio has relevant significance,

which directly helps in supporting the level of conservative investment nature of the investor.

Lastly, the Capital asset pricing model has been considered to be one the rising factors, which

has allowed the investors to detect the level of expected returns of the stock. The above

identified theories and calculations has mainly allowed the investor for detecting the level of

risk exposure, which needs to be taken into consideration before conducting investments.

Capital Market Line and Security Market Line difference:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

3

Figure 1: Graph of Capital Market Line

(Source: Milosevic 2018)

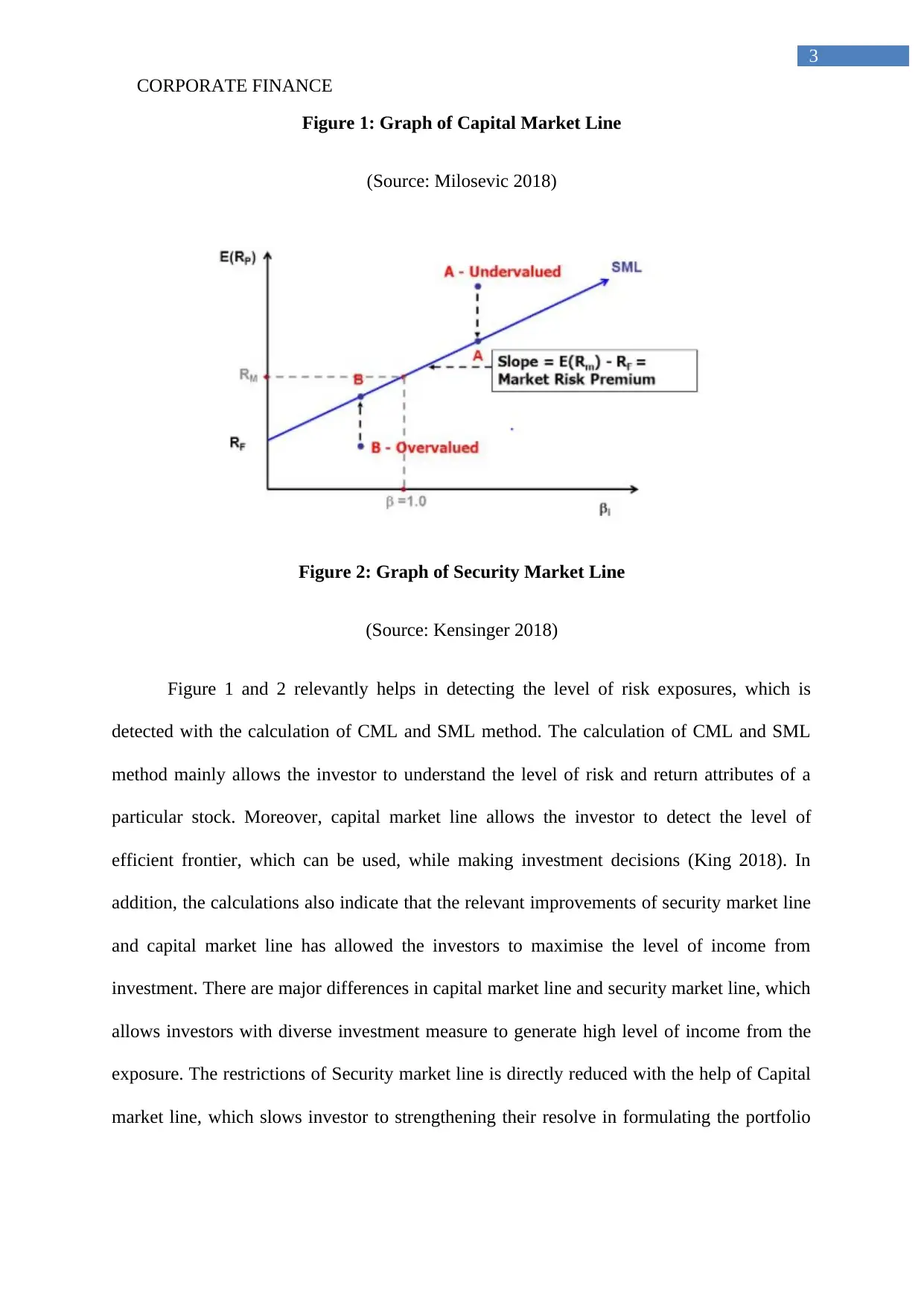

Figure 2: Graph of Security Market Line

(Source: Kensinger 2018)

Figure 1 and 2 relevantly helps in detecting the level of risk exposures, which is

detected with the calculation of CML and SML method. The calculation of CML and SML

method mainly allows the investor to understand the level of risk and return attributes of a

particular stock. Moreover, capital market line allows the investor to detect the level of

efficient frontier, which can be used, while making investment decisions (King 2018). In

addition, the calculations also indicate that the relevant improvements of security market line

and capital market line has allowed the investors to maximise the level of income from

investment. There are major differences in capital market line and security market line, which

allows investors with diverse investment measure to generate high level of income from the

exposure. The restrictions of Security market line is directly reduced with the help of Capital

market line, which slows investor to strengthening their resolve in formulating the portfolio

3

Figure 1: Graph of Capital Market Line

(Source: Milosevic 2018)

Figure 2: Graph of Security Market Line

(Source: Kensinger 2018)

Figure 1 and 2 relevantly helps in detecting the level of risk exposures, which is

detected with the calculation of CML and SML method. The calculation of CML and SML

method mainly allows the investor to understand the level of risk and return attributes of a

particular stock. Moreover, capital market line allows the investor to detect the level of

efficient frontier, which can be used, while making investment decisions (King 2018). In

addition, the calculations also indicate that the relevant improvements of security market line

and capital market line has allowed the investors to maximise the level of income from

investment. There are major differences in capital market line and security market line, which

allows investors with diverse investment measure to generate high level of income from the

exposure. The restrictions of Security market line is directly reduced with the help of Capital

market line, which slows investor to strengthening their resolve in formulating the portfolio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

4

(Tejada-Arango et al. 2018). The major differences between capital market line and security

market line are depicted as follows.

The risk evaluating attribute of both CML and SML is different, which can directly have

an impact on the investment decisions of the investor. The calculation conducted in

security market line directly uses different level risk exposures, which can be used for

investment purpose. The SML line directly uses beta for deriving the level of risk and

return capability of the stock, which helps in supporting the level of risk exposure after

conducting investments (Bothfeld and Rosenthal 2018). On the other hand, the CML

method directly utilises the standard deviation for calculating the overall risk of the stocks

listed in the portfolio. In addition, the measure directly utilises different level of risk

exposure to understand the current risk condition of the portfolio.

There is other difference between the CML and SML methods, which directly initiates

different level of risk exposures to understand the current performance of the investment

scope. The security market line directly utilises only one stock and depicts its valuation,

whether they are undervalued or overvalued. This might directly help in detecting the

level of risk exposure for generating high level of income from investment (Sweeney

2018). The calculation that has been conducted in CML line directly allows the investor

to analyse the overall portfolio, which helps in detecting the total risk involved in

investment. However, with the SML method the investors are only able to analyse one

stock and compete its with the market returns. This SML line eventually allowed the

investor to understand the specific risk of the stock, which needs to be borne during the

investment phase. Therefore, investors can utilise both CML and SML method for

creating the adequate portfolio with low risk and high returns (Korinek 2018).

The output data for Capital Market Line and Security Market Line is relevantly different,

which are used by investors to analyse different level of returns that can be generated

4

(Tejada-Arango et al. 2018). The major differences between capital market line and security

market line are depicted as follows.

The risk evaluating attribute of both CML and SML is different, which can directly have

an impact on the investment decisions of the investor. The calculation conducted in

security market line directly uses different level risk exposures, which can be used for

investment purpose. The SML line directly uses beta for deriving the level of risk and

return capability of the stock, which helps in supporting the level of risk exposure after

conducting investments (Bothfeld and Rosenthal 2018). On the other hand, the CML

method directly utilises the standard deviation for calculating the overall risk of the stocks

listed in the portfolio. In addition, the measure directly utilises different level of risk

exposure to understand the current risk condition of the portfolio.

There is other difference between the CML and SML methods, which directly initiates

different level of risk exposures to understand the current performance of the investment

scope. The security market line directly utilises only one stock and depicts its valuation,

whether they are undervalued or overvalued. This might directly help in detecting the

level of risk exposure for generating high level of income from investment (Sweeney

2018). The calculation that has been conducted in CML line directly allows the investor

to analyse the overall portfolio, which helps in detecting the total risk involved in

investment. However, with the SML method the investors are only able to analyse one

stock and compete its with the market returns. This SML line eventually allowed the

investor to understand the specific risk of the stock, which needs to be borne during the

investment phase. Therefore, investors can utilise both CML and SML method for

creating the adequate portfolio with low risk and high returns (Korinek 2018).

The output data for Capital Market Line and Security Market Line is relevantly different,

which are used by investors to analyse different level of returns that can be generated

CORPORATE FINANCE

5

from investment. The capital market line directly provides relevant calculations, which

help in detecting the overall efficient frontier that comprises of different level of risk and

return measures. The calculations have also allowed the investor to detect different level

of risk and return attributes of a combined portfolio. Moreover, the CML depicts the

systematic and unsystematic risk involved in investment. On the other hand, the SML

method only portrays the systematic risk involved in investment, which does not allow

the investor to determine its profitability. On the contrary, Walter and Kessler (2018)

argued that both CML and SML method does not factor different components of risk,

which increases the level of risk involved in investment.

Minimum variance portfolio Significance:

Figure 3: Minimum variance portfolio graph

(Source: Bodnar, Parolya and Schmid 2018)

5

from investment. The capital market line directly provides relevant calculations, which

help in detecting the overall efficient frontier that comprises of different level of risk and

return measures. The calculations have also allowed the investor to detect different level

of risk and return attributes of a combined portfolio. Moreover, the CML depicts the

systematic and unsystematic risk involved in investment. On the other hand, the SML

method only portrays the systematic risk involved in investment, which does not allow

the investor to determine its profitability. On the contrary, Walter and Kessler (2018)

argued that both CML and SML method does not factor different components of risk,

which increases the level of risk involved in investment.

Minimum variance portfolio Significance:

Figure 3: Minimum variance portfolio graph

(Source: Bodnar, Parolya and Schmid 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

6

The above graph directly indicates the level of minimum variance portfolio, which

can be used by investors in reducing the risk from investment. The minimum variance

portfolio can be used by investors to detect different level of risk exposure, which can be

used for investors for maximising the level of income from investment. The minimum

variance portfolio is mainly identified in the above figure, where the total risk involved in

investment is the lowest. The above graph relevantly represents the efficient curve, which

comprises of different portfolios that have risk and return measures. The minimum variance

portfolio has relevant significance for investors, which is depicted as follows.

The major significance of minimum variance portfolio is its capability to support the

conservative investors with their risk aversion needs. The minimum variance portfolio

directly helps investors to formulate an adequate portfolio, which helps in detecting the

level of risk and return condition of the company. The calculations directly allow the

investor for understanding the current condition of the stocks and how they can react to

volatile capital market fluctuations. Hence, investors using the minimum variance

portfolio are able to understand the level of risk involved in investment, which can be

reduced substantially for maintaining constant returns. On the other hand, Kim and Shin

(2018) criticises that minimum variance portfolio limit capability of the investor to

generate high returns, as it aims in formulating a portfolio, which has low risk.

The second significance of minimum variance portfolio is the overall accommodation of

different level of financial instruments, which can be used for creating an adequate

portfolio that can generate adequate returns with low risk. Therefore, investors with the

help of minimum variance portfolio are able to detect the risk level of different stocks,

which is used for formulating the portfolio. Hence, with the help of Minimum Variance

Portfolio investors are able to use different kinds of financial instruments such as risk free

rate, bonds and equity shares to create an adequate portfolio with the lowest risk. This

6

The above graph directly indicates the level of minimum variance portfolio, which

can be used by investors in reducing the risk from investment. The minimum variance

portfolio can be used by investors to detect different level of risk exposure, which can be

used for investors for maximising the level of income from investment. The minimum

variance portfolio is mainly identified in the above figure, where the total risk involved in

investment is the lowest. The above graph relevantly represents the efficient curve, which

comprises of different portfolios that have risk and return measures. The minimum variance

portfolio has relevant significance for investors, which is depicted as follows.

The major significance of minimum variance portfolio is its capability to support the

conservative investors with their risk aversion needs. The minimum variance portfolio

directly helps investors to formulate an adequate portfolio, which helps in detecting the

level of risk and return condition of the company. The calculations directly allow the

investor for understanding the current condition of the stocks and how they can react to

volatile capital market fluctuations. Hence, investors using the minimum variance

portfolio are able to understand the level of risk involved in investment, which can be

reduced substantially for maintaining constant returns. On the other hand, Kim and Shin

(2018) criticises that minimum variance portfolio limit capability of the investor to

generate high returns, as it aims in formulating a portfolio, which has low risk.

The second significance of minimum variance portfolio is the overall accommodation of

different level of financial instruments, which can be used for creating an adequate

portfolio that can generate adequate returns with low risk. Therefore, investors with the

help of minimum variance portfolio are able to detect the risk level of different stocks,

which is used for formulating the portfolio. Hence, with the help of Minimum Variance

Portfolio investors are able to use different kinds of financial instruments such as risk free

rate, bonds and equity shares to create an adequate portfolio with the lowest risk. This

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

7

type of measure eventually allows the investor to extend its current investments scope and

diversified portfolio to reduce the level of risk and maximize the return from investment.

Bednarek and Patel (2018) argued that investors using the minimum variance portfolio is

not able to increase their current return conditions, are a myth uses stocks in a form where

the least risk involved in investment can be exaggerated. This mainly limits the overall

condition of the investors to maximize the returns from investment.

The third significance of minimum variance portfolio is its capability to handle situations

of the capital market, which eventually protects the investor’s capital and reduces the

concern for abnormal losses. Minimum variance portfolio directly uses diverse stocks for

creating the portfolio, which relatively reduces the impact of share price change that is

influenced from the volatile capital market. Therefore investors can use the minimum

variance portfolio technique to create an efficient Frontier, which can help in detecting

the relevant curve of different portfolio combinations. This combination of different

stocks relevantly allow the investors to select an adequate portfolio which can support is

there investment criteria (Qu et al. 2018).

Therefore it would be understood that with the help of minimum variance portfolio

investors are able to analyze different stocks and conduct investments according to their

return requirements.

CAPM calculation description and analysis:

7

type of measure eventually allows the investor to extend its current investments scope and

diversified portfolio to reduce the level of risk and maximize the return from investment.

Bednarek and Patel (2018) argued that investors using the minimum variance portfolio is

not able to increase their current return conditions, are a myth uses stocks in a form where

the least risk involved in investment can be exaggerated. This mainly limits the overall

condition of the investors to maximize the returns from investment.

The third significance of minimum variance portfolio is its capability to handle situations

of the capital market, which eventually protects the investor’s capital and reduces the

concern for abnormal losses. Minimum variance portfolio directly uses diverse stocks for

creating the portfolio, which relatively reduces the impact of share price change that is

influenced from the volatile capital market. Therefore investors can use the minimum

variance portfolio technique to create an efficient Frontier, which can help in detecting

the relevant curve of different portfolio combinations. This combination of different

stocks relevantly allow the investors to select an adequate portfolio which can support is

there investment criteria (Qu et al. 2018).

Therefore it would be understood that with the help of minimum variance portfolio

investors are able to analyze different stocks and conduct investments according to their

return requirements.

CAPM calculation description and analysis:

CORPORATE FINANCE

8

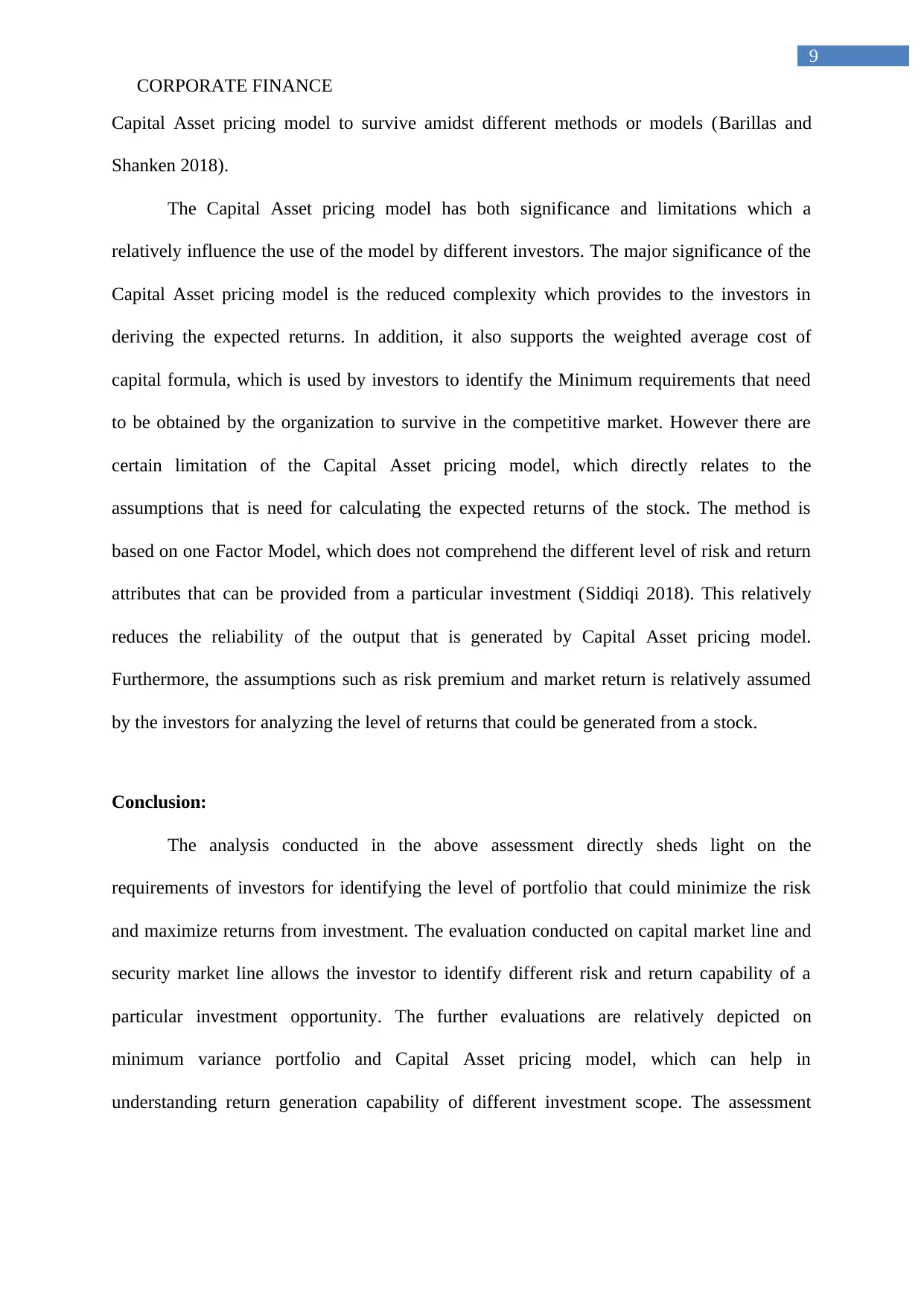

Figure 4: Capital Asset Pricing Model

(Source: Bellalah and Zhang 2018)

The figure relatively indicates the formula for Capital Asset pricing model, which

eventually allows investor to identify the level of expected returns of a particular stock. The

formula directly indicates that we need to have a relevant risk free rate, beta, and market

premium to analyses the level of return that needs to be presented by the particular stock. The

calculation also indicates that Capital Asset pricing model eventually allows investor to

understand the capability of the stock and its investment opportunity. The detection of Beta is

relatively conducted from a reliable internet sources, which is extensively used for

identifying the level of risk attributes of an investment. The calculation is fairly simple and

can be used by maximum the investors with a little assumptions and requirement (Jarrow

2018).

There have been many instances where the different level of methods has been

proposed, as an alternative to the Capital Asset pricing model. However, the proposed

method is not extensively utilized by all the investors, due to its complexity and high-end

calculations needed for deriving the results. The alternative methods that has been proposed

for Capital Asset pricing model are market price based models, arbitrage pricing model,

accounting information based models, and market price base model. The above mentioned

methods are relatively helpful for the investors to identify the exact expected return of a

particular stock or investment. However, the measures directly require additional calculations

and extensive use of statistical methods to derive the relevant expected return of the

investment scope. This relatively reduces the level of usage that can be conducted among

different in western. The above-mentioned models can only be used by large hedge fund

managers and big investors, while the normal investors cannot use the method due to its

complexity. This can be considered as one of the major components, which has allowed the

8

Figure 4: Capital Asset Pricing Model

(Source: Bellalah and Zhang 2018)

The figure relatively indicates the formula for Capital Asset pricing model, which

eventually allows investor to identify the level of expected returns of a particular stock. The

formula directly indicates that we need to have a relevant risk free rate, beta, and market

premium to analyses the level of return that needs to be presented by the particular stock. The

calculation also indicates that Capital Asset pricing model eventually allows investor to

understand the capability of the stock and its investment opportunity. The detection of Beta is

relatively conducted from a reliable internet sources, which is extensively used for

identifying the level of risk attributes of an investment. The calculation is fairly simple and

can be used by maximum the investors with a little assumptions and requirement (Jarrow

2018).

There have been many instances where the different level of methods has been

proposed, as an alternative to the Capital Asset pricing model. However, the proposed

method is not extensively utilized by all the investors, due to its complexity and high-end

calculations needed for deriving the results. The alternative methods that has been proposed

for Capital Asset pricing model are market price based models, arbitrage pricing model,

accounting information based models, and market price base model. The above mentioned

methods are relatively helpful for the investors to identify the exact expected return of a

particular stock or investment. However, the measures directly require additional calculations

and extensive use of statistical methods to derive the relevant expected return of the

investment scope. This relatively reduces the level of usage that can be conducted among

different in western. The above-mentioned models can only be used by large hedge fund

managers and big investors, while the normal investors cannot use the method due to its

complexity. This can be considered as one of the major components, which has allowed the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

9

Capital Asset pricing model to survive amidst different methods or models (Barillas and

Shanken 2018).

The Capital Asset pricing model has both significance and limitations which a

relatively influence the use of the model by different investors. The major significance of the

Capital Asset pricing model is the reduced complexity which provides to the investors in

deriving the expected returns. In addition, it also supports the weighted average cost of

capital formula, which is used by investors to identify the Minimum requirements that need

to be obtained by the organization to survive in the competitive market. However there are

certain limitation of the Capital Asset pricing model, which directly relates to the

assumptions that is need for calculating the expected returns of the stock. The method is

based on one Factor Model, which does not comprehend the different level of risk and return

attributes that can be provided from a particular investment (Siddiqi 2018). This relatively

reduces the reliability of the output that is generated by Capital Asset pricing model.

Furthermore, the assumptions such as risk premium and market return is relatively assumed

by the investors for analyzing the level of returns that could be generated from a stock.

Conclusion:

The analysis conducted in the above assessment directly sheds light on the

requirements of investors for identifying the level of portfolio that could minimize the risk

and maximize returns from investment. The evaluation conducted on capital market line and

security market line allows the investor to identify different risk and return capability of a

particular investment opportunity. The further evaluations are relatively depicted on

minimum variance portfolio and Capital Asset pricing model, which can help in

understanding return generation capability of different investment scope. The assessment

9

Capital Asset pricing model to survive amidst different methods or models (Barillas and

Shanken 2018).

The Capital Asset pricing model has both significance and limitations which a

relatively influence the use of the model by different investors. The major significance of the

Capital Asset pricing model is the reduced complexity which provides to the investors in

deriving the expected returns. In addition, it also supports the weighted average cost of

capital formula, which is used by investors to identify the Minimum requirements that need

to be obtained by the organization to survive in the competitive market. However there are

certain limitation of the Capital Asset pricing model, which directly relates to the

assumptions that is need for calculating the expected returns of the stock. The method is

based on one Factor Model, which does not comprehend the different level of risk and return

attributes that can be provided from a particular investment (Siddiqi 2018). This relatively

reduces the reliability of the output that is generated by Capital Asset pricing model.

Furthermore, the assumptions such as risk premium and market return is relatively assumed

by the investors for analyzing the level of returns that could be generated from a stock.

Conclusion:

The analysis conducted in the above assessment directly sheds light on the

requirements of investors for identifying the level of portfolio that could minimize the risk

and maximize returns from investment. The evaluation conducted on capital market line and

security market line allows the investor to identify different risk and return capability of a

particular investment opportunity. The further evaluations are relatively depicted on

minimum variance portfolio and Capital Asset pricing model, which can help in

understanding return generation capability of different investment scope. The assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

10

further evaluates different level of the relevant significance of minimum variance portfolio

investors to maximize the return and minimize the risk involved in investment.

References:

Barillas, F. and Shanken, J., 2018. Comparing asset pricing models. The Journal of

Finance, 73(2), pp.715-754.

Bednarek, Z. and Patel, P., 2018. Understanding the outperformance of the minimum

variance portfolio. Finance Research Letters, 24, pp.175-178.

Bellalah, M. and Zhang, D., 2018. An intertemporal capital asset pricing model under

incomplete information and short sales. Annals of Operations Research, pp.1-17.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Bothfeld, S. and Rosenthal, P., 2018. The End of Social Security as we know it–The Erosion

of Status Protection in German Labour Market Policy. Journal of Social Policy, 47(2),

pp.275-294.

Jarrow, R., 2018. An equilibrium capital asset pricing model in markets with price jumps and

price bubbles. Quarterly Journal of Finance, 8(02), p.1850005.

Kensinger, J.W. ed., 2018. Global Tensions in Financial Markets. Emerald Publishing

Limited.

10

further evaluates different level of the relevant significance of minimum variance portfolio

investors to maximize the return and minimize the risk involved in investment.

References:

Barillas, F. and Shanken, J., 2018. Comparing asset pricing models. The Journal of

Finance, 73(2), pp.715-754.

Bednarek, Z. and Patel, P., 2018. Understanding the outperformance of the minimum

variance portfolio. Finance Research Letters, 24, pp.175-178.

Bellalah, M. and Zhang, D., 2018. An intertemporal capital asset pricing model under

incomplete information and short sales. Annals of Operations Research, pp.1-17.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Bothfeld, S. and Rosenthal, P., 2018. The End of Social Security as we know it–The Erosion

of Status Protection in German Labour Market Policy. Journal of Social Policy, 47(2),

pp.275-294.

Jarrow, R., 2018. An equilibrium capital asset pricing model in markets with price jumps and

price bubbles. Quarterly Journal of Finance, 8(02), p.1850005.

Kensinger, J.W. ed., 2018. Global Tensions in Financial Markets. Emerald Publishing

Limited.

CORPORATE FINANCE

11

Kim, H.S. and Shin, D.W., 2018. Forecast of realized covariance matrix based on asymptotic

distribution of the LU decomposition with an application for balancing minimum variance

portfolio. Applied Economics Letters, pp.1-8.

King, M., 2018. Due diligence in capital markets. Journal of Capital Markets Studies, 2(1),

pp.6-8.

Korinek, A., 2018. Regulating capital flows to emerging markets: An externality

view. Journal of International Economics, 111, pp.61-80.

Milosevic, M., 2018. Skills or networks? Success and fundraising determinants in a low

performing venture capital market. Research Policy, 47(1), pp.49-60.

Qu, H., Wang, T., Zhang, Y. and Sun, P., 2018. Dynamic hedging using the realized

minimum-variance hedge ratio approach–Examination of the CSI 300 index futures. Pacific-

Basin Finance Journal.

Siddiqi, H., 2018. Anchoring-Adjusted Capital Asset Pricing Model. Journal of Behavioral

Finance, 19(3), pp.249-270.

Sweeney, R.J., 2018. The Information Costs of Capital Controls. In Capital Controls in

Emerging Economies (pp. 45-61). Routledge.

Tejada-Arango, D.A., Sánchez-Martın, P. and Ramos, A., 2018. Security constrained unit

commitment using line outage distribution factors. IEEE Transactions on Power

Systems, 33(1), pp.329-337.

Walter, T. and Kessler, O., 2018. The Public and Its Problems: How the EU's Capital Market

Union Defines the Bounds of Legitimate Knowledge and Redraws the Boundaries of (Public)

Authority. Indiana Journal of Global Legal Studies, 25(1), pp.157-185.

11

Kim, H.S. and Shin, D.W., 2018. Forecast of realized covariance matrix based on asymptotic

distribution of the LU decomposition with an application for balancing minimum variance

portfolio. Applied Economics Letters, pp.1-8.

King, M., 2018. Due diligence in capital markets. Journal of Capital Markets Studies, 2(1),

pp.6-8.

Korinek, A., 2018. Regulating capital flows to emerging markets: An externality

view. Journal of International Economics, 111, pp.61-80.

Milosevic, M., 2018. Skills or networks? Success and fundraising determinants in a low

performing venture capital market. Research Policy, 47(1), pp.49-60.

Qu, H., Wang, T., Zhang, Y. and Sun, P., 2018. Dynamic hedging using the realized

minimum-variance hedge ratio approach–Examination of the CSI 300 index futures. Pacific-

Basin Finance Journal.

Siddiqi, H., 2018. Anchoring-Adjusted Capital Asset Pricing Model. Journal of Behavioral

Finance, 19(3), pp.249-270.

Sweeney, R.J., 2018. The Information Costs of Capital Controls. In Capital Controls in

Emerging Economies (pp. 45-61). Routledge.

Tejada-Arango, D.A., Sánchez-Martın, P. and Ramos, A., 2018. Security constrained unit

commitment using line outage distribution factors. IEEE Transactions on Power

Systems, 33(1), pp.329-337.

Walter, T. and Kessler, O., 2018. The Public and Its Problems: How the EU's Capital Market

Union Defines the Bounds of Legitimate Knowledge and Redraws the Boundaries of (Public)

Authority. Indiana Journal of Global Legal Studies, 25(1), pp.157-185.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.