FIN200 - Security Market Line, Capital Market Line & CAPM Analysis

VerifiedAdded on 2023/06/04

|11

|2573

|269

Report

AI Summary

This report provides a comparative analysis of the Security Market Line (SML) and Capital Market Line (CML), highlighting their differences using graphs and discussing the importance of minimum variance portfolios for investors. It examines how the beta coefficient and standard deviation are used to measure risk in SML and CML, respectively, and contrasts their approaches to portfolio efficiency. The report also explores the relevance of the Capital Asset Pricing Model (CAPM) equation in evaluating securities, emphasizing its ability to compute expected returns based on market rates, security betas, and risk-free rates. Furthermore, it contrasts CAPM with the Weighted Average Cost of Capital (WACC) method, arguing that CAPM provides more accurate discount rates for investment evaluation by considering systematic risk. The report concludes that while no model is perfect, CAPM offers a more practical and testable approach for investment decisions, especially when combined with other analytical tools.

FIN200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Security Market Line vs. Capital Market Line...........................................................................1

Importance of Minimum Variance Portfolios.............................................................................3

Relevance of CAPM equation.......................................................................................................5

References.......................................................................................................................................8

Security Market Line vs. Capital Market Line...........................................................................1

Importance of Minimum Variance Portfolios.............................................................................3

Relevance of CAPM equation.......................................................................................................5

References.......................................................................................................................................8

Table of Figures

Figure 1: Security Market Line........................................................................................................1

Figure 2: Capital Market Line.........................................................................................................2

Figure 3: Minimum Variance Portfolio...........................................................................................3

Figure 4: CAPM vs. WACC............................................................................................................6

Figure 1: Security Market Line........................................................................................................1

Figure 2: Capital Market Line.........................................................................................................2

Figure 3: Minimum Variance Portfolio...........................................................................................3

Figure 4: CAPM vs. WACC............................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The present report aims to conduct comparative analysis of security market line and capital

market line to identify differences among these two approaches by using appropriate graphs.

Further, this considers the meaning, importance and relevance of the minimum variance portfolio

for investors. Last part of the study describes the relevance of capital asset pricing model for

evaluation of securities.

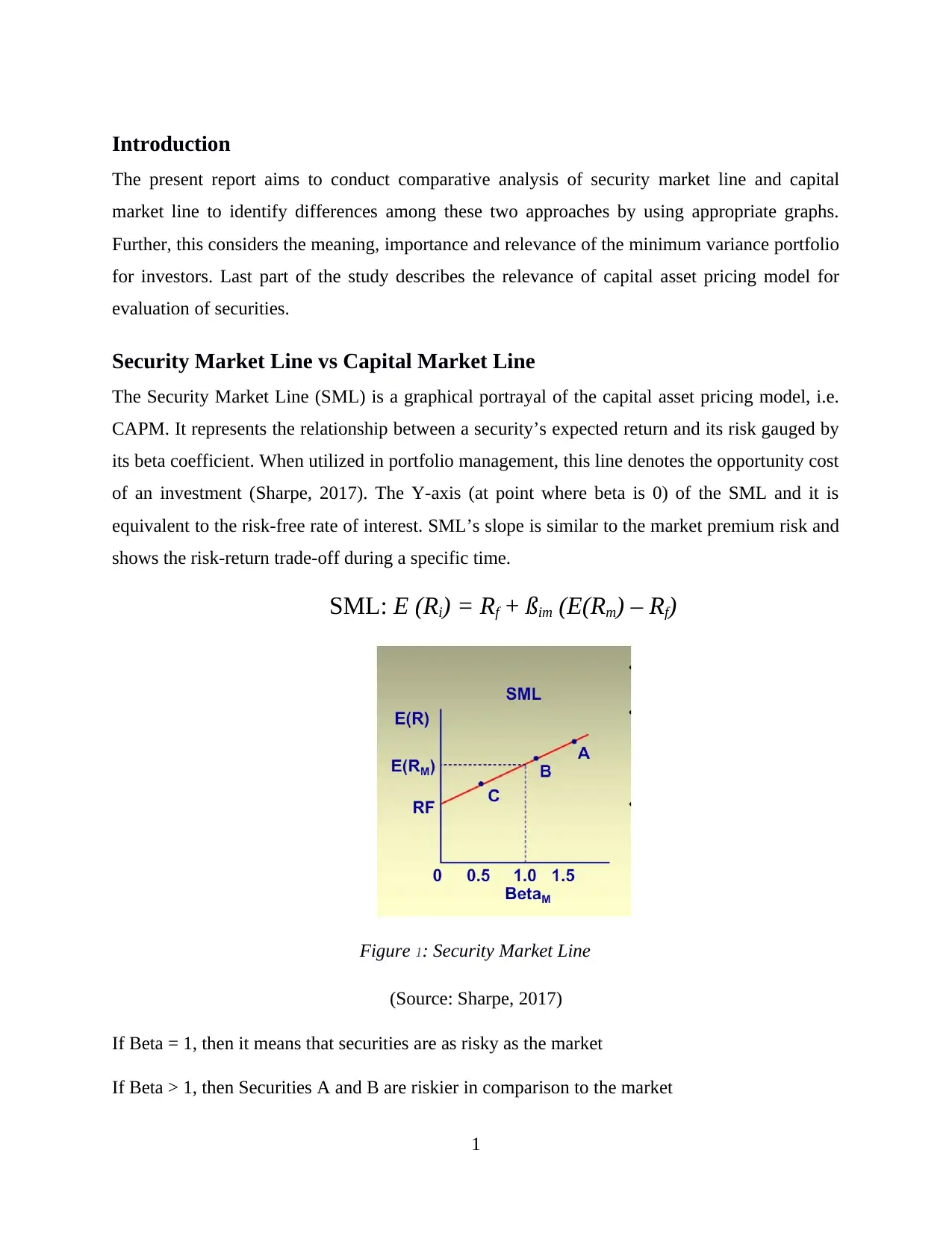

Security Market Line vs Capital Market Line

The Security Market Line (SML) is a graphical portrayal of the capital asset pricing model, i.e.

CAPM. It represents the relationship between a security’s expected return and its risk gauged by

its beta coefficient. When utilized in portfolio management, this line denotes the opportunity cost

of an investment (Sharpe, 2017). The Y-axis (at point where beta is 0) of the SML and it is

equivalent to the risk-free rate of interest. SML’s slope is similar to the market premium risk and

shows the risk-return trade-off during a specific time.

SML: E (Ri) = Rf + ßim (E(Rm) – Rf)

Figure 1: Security Market Line

(Source: Sharpe, 2017)

If Beta = 1, then it means that securities are as risky as the market

If Beta > 1, then Securities A and B are riskier in comparison to the market

1

The present report aims to conduct comparative analysis of security market line and capital

market line to identify differences among these two approaches by using appropriate graphs.

Further, this considers the meaning, importance and relevance of the minimum variance portfolio

for investors. Last part of the study describes the relevance of capital asset pricing model for

evaluation of securities.

Security Market Line vs Capital Market Line

The Security Market Line (SML) is a graphical portrayal of the capital asset pricing model, i.e.

CAPM. It represents the relationship between a security’s expected return and its risk gauged by

its beta coefficient. When utilized in portfolio management, this line denotes the opportunity cost

of an investment (Sharpe, 2017). The Y-axis (at point where beta is 0) of the SML and it is

equivalent to the risk-free rate of interest. SML’s slope is similar to the market premium risk and

shows the risk-return trade-off during a specific time.

SML: E (Ri) = Rf + ßim (E(Rm) – Rf)

Figure 1: Security Market Line

(Source: Sharpe, 2017)

If Beta = 1, then it means that securities are as risky as the market

If Beta > 1, then Securities A and B are riskier in comparison to the market

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If Beta < 1, then Security C is less risky in comparison to the market

Capital Market Line (CML) is a graph reflecting the anticipated return of a portfolio comprising

every plausible percentage between a market portfolio and risk-free asset. The diversified market

portfolio has an only systematic risk and its anticipated return is equivalent to the likely market

return in general. Every point along the CML has a high risk-return profile to any portfolio on

the efficient border. The CML is regarded to be greater than the efficient frontline as it is

supported by the inclusion of a risk-free asset in the portfolio (Sornette, 2017).

CML: E(rc) = rF + σc E(rM) – rF / σM

Figure 1: Capital Market Line

(Source: Sornette, 2017)

Line from RF to L is capital market line.

x = risk premium

= E(RM) – RF

y = risk = σM

Slope = x/y

= [E(RM) – RF]/ σM

2

Capital Market Line (CML) is a graph reflecting the anticipated return of a portfolio comprising

every plausible percentage between a market portfolio and risk-free asset. The diversified market

portfolio has an only systematic risk and its anticipated return is equivalent to the likely market

return in general. Every point along the CML has a high risk-return profile to any portfolio on

the efficient border. The CML is regarded to be greater than the efficient frontline as it is

supported by the inclusion of a risk-free asset in the portfolio (Sornette, 2017).

CML: E(rc) = rF + σc E(rM) – rF / σM

Figure 1: Capital Market Line

(Source: Sornette, 2017)

Line from RF to L is capital market line.

x = risk premium

= E(RM) – RF

y = risk = σM

Slope = x/y

= [E(RM) – RF]/ σM

2

y-intercept = RF (Sornette, 2017)

One of the key differences between SML and CML is the manner in which risk elements are

measured. Beta coefficient is the measure of risk elements in the SML. In contrast, standard

deviation determines the risk factors for CML. The SML assesses risk via beta which assists in

identifying of risk contribution by the individual security to the whole portfolio. On the other

hand, assessment of risk in CML is done by means of standard deviation or via a total risk factor

(Hong and Sraer, 2016).

While the SML defines both non-efficiency as well as efficiency of portfolios, while the CML

only shows efficient portfolios. When computing of return, the likely return of the portfolio for

CML is demonstrated alongside the Y-axis. In contrast, the return on securities for SML, is

demonstrated alongside Y axis. For CML, a portfolio’s standard deviation is demonstrated along

the Y-axis. On the other hand, for SML, the Beta of security is demonstrated along the X-axis

(Pilbeam, 2018).

Where the CML determines the risk-free assets and market portfolio, all security elements are

identified by the SML. Unlike the CML, the SML portrays the likely returns of individual assets.

The CML identifies the return or risk for efficient portfolios, and the SML shows the return or

risk for individual shares (Sharpe, 2017). The bottom line is that the CML is regarded to be

better when assessing risk elements.

Importance of Minimum Variance Portfolios

A minimum variance portfolio is a pool of investments with the least volatility, i.e. those

investments which they have less possibility of price variation because they carry the minimum

sensitivity risk. The spread of investments combined together has a lower consequent risk level

relative to the individual risk of every stock. Investors who are not willing to assume big risks

must contemplate taking a minimum variance portfolio (Yang, Couillet and McKay, 2015).

3

One of the key differences between SML and CML is the manner in which risk elements are

measured. Beta coefficient is the measure of risk elements in the SML. In contrast, standard

deviation determines the risk factors for CML. The SML assesses risk via beta which assists in

identifying of risk contribution by the individual security to the whole portfolio. On the other

hand, assessment of risk in CML is done by means of standard deviation or via a total risk factor

(Hong and Sraer, 2016).

While the SML defines both non-efficiency as well as efficiency of portfolios, while the CML

only shows efficient portfolios. When computing of return, the likely return of the portfolio for

CML is demonstrated alongside the Y-axis. In contrast, the return on securities for SML, is

demonstrated alongside Y axis. For CML, a portfolio’s standard deviation is demonstrated along

the Y-axis. On the other hand, for SML, the Beta of security is demonstrated along the X-axis

(Pilbeam, 2018).

Where the CML determines the risk-free assets and market portfolio, all security elements are

identified by the SML. Unlike the CML, the SML portrays the likely returns of individual assets.

The CML identifies the return or risk for efficient portfolios, and the SML shows the return or

risk for individual shares (Sharpe, 2017). The bottom line is that the CML is regarded to be

better when assessing risk elements.

Importance of Minimum Variance Portfolios

A minimum variance portfolio is a pool of investments with the least volatility, i.e. those

investments which they have less possibility of price variation because they carry the minimum

sensitivity risk. The spread of investments combined together has a lower consequent risk level

relative to the individual risk of every stock. Investors who are not willing to assume big risks

must contemplate taking a minimum variance portfolio (Yang, Couillet and McKay, 2015).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

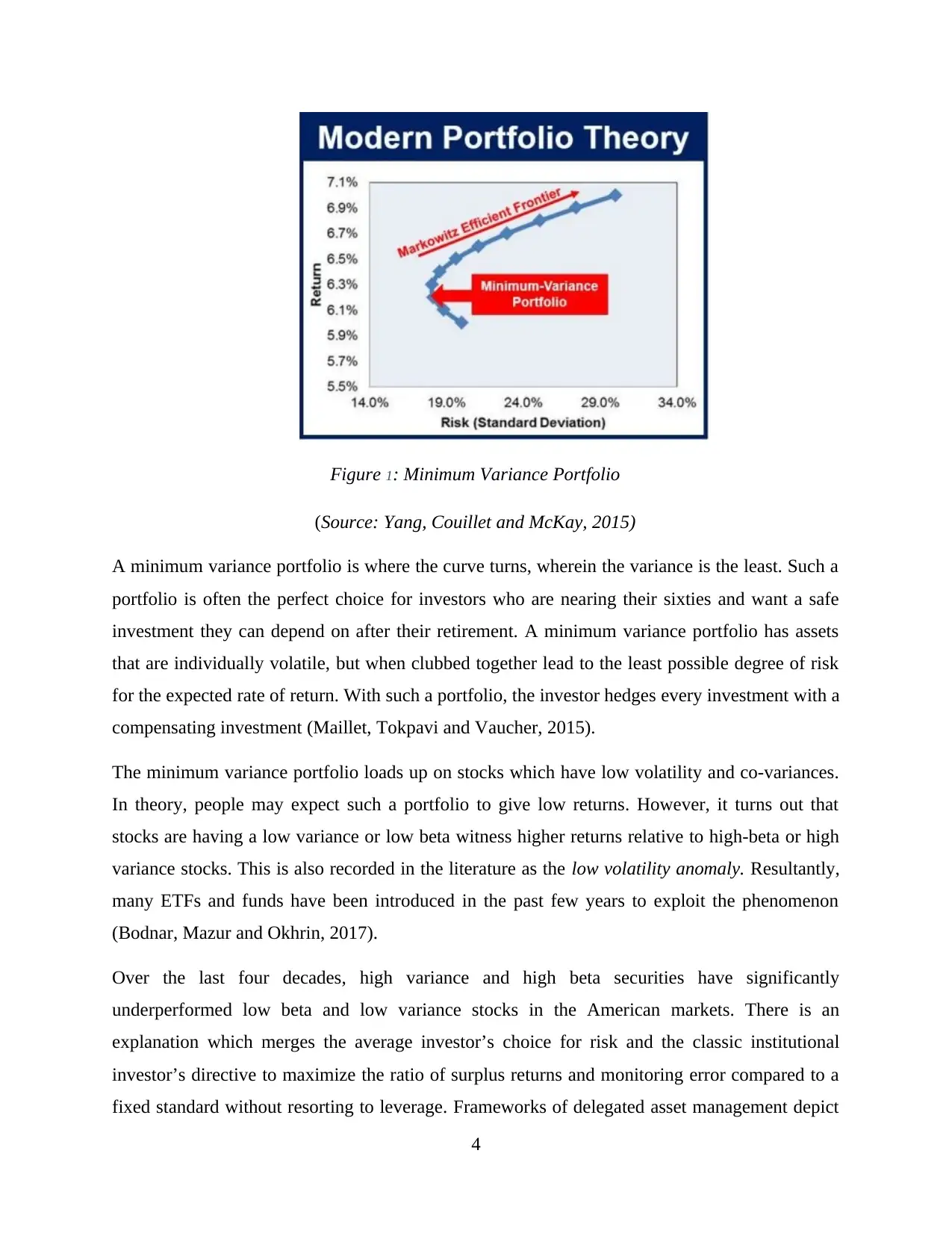

Figure 1: Minimum Variance Portfolio

(Source: Yang, Couillet and McKay, 2015)

A minimum variance portfolio is where the curve turns, wherein the variance is the least. Such a

portfolio is often the perfect choice for investors who are nearing their sixties and want a safe

investment they can depend on after their retirement. A minimum variance portfolio has assets

that are individually volatile, but when clubbed together lead to the least possible degree of risk

for the expected rate of return. With such a portfolio, the investor hedges every investment with a

compensating investment (Maillet, Tokpavi and Vaucher, 2015).

The minimum variance portfolio loads up on stocks which have low volatility and co-variances.

In theory, people may expect such a portfolio to give low returns. However, it turns out that

stocks are having a low variance or low beta witness higher returns relative to high-beta or high

variance stocks. This is also recorded in the literature as the low volatility anomaly. Resultantly,

many ETFs and funds have been introduced in the past few years to exploit the phenomenon

(Bodnar, Mazur and Okhrin, 2017).

Over the last four decades, high variance and high beta securities have significantly

underperformed low beta and low variance stocks in the American markets. There is an

explanation which merges the average investor’s choice for risk and the classic institutional

investor’s directive to maximize the ratio of surplus returns and monitoring error compared to a

fixed standard without resorting to leverage. Frameworks of delegated asset management depict

4

(Source: Yang, Couillet and McKay, 2015)

A minimum variance portfolio is where the curve turns, wherein the variance is the least. Such a

portfolio is often the perfect choice for investors who are nearing their sixties and want a safe

investment they can depend on after their retirement. A minimum variance portfolio has assets

that are individually volatile, but when clubbed together lead to the least possible degree of risk

for the expected rate of return. With such a portfolio, the investor hedges every investment with a

compensating investment (Maillet, Tokpavi and Vaucher, 2015).

The minimum variance portfolio loads up on stocks which have low volatility and co-variances.

In theory, people may expect such a portfolio to give low returns. However, it turns out that

stocks are having a low variance or low beta witness higher returns relative to high-beta or high

variance stocks. This is also recorded in the literature as the low volatility anomaly. Resultantly,

many ETFs and funds have been introduced in the past few years to exploit the phenomenon

(Bodnar, Mazur and Okhrin, 2017).

Over the last four decades, high variance and high beta securities have significantly

underperformed low beta and low variance stocks in the American markets. There is an

explanation which merges the average investor’s choice for risk and the classic institutional

investor’s directive to maximize the ratio of surplus returns and monitoring error compared to a

fixed standard without resorting to leverage. Frameworks of delegated asset management depict

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that these directives dissuade arbitrage in both low beta - high alpha, and high beta - low alpha

securities (Kempf and Memmel, 2006). This reasoning is in alignment with many facets of the

low variance anomaly entailing why it has fostered in the past few years even as the dominance

of institutional investors has increased.

Minimum market portfolios are more flexible in market downturns. As the business cycle finally

recoups, a minimum variance portfolio tends to ensure compounding performance in comparison

to return provided by market. One of the biggest advantages of the minimum variance portfolio

is that it really eliminates expected returns from the optimization which are tough to handle. As

the minimum variance portfolios have the sole goal of decreasing risk, instead of striving to

optimize the reward-risk ratio. Further, minimum variance portfolio optimization results in

noticeable attention on low variance securities in against of the cost of exploiting correlation

properties (Clarke, De Silva and Thorley, 2011). While MVP is not ideal portfolios, but they

might be appropriate for investors who intend to load up on low-risk stocks. As estimation risk

natural to projected returns is a known aspect, the fact that the MVP depends just on risk criteria

is an attractive attribute.

The relevance of the CAPM equation

The Capital Asset Pricing Model (CAPM) is a framework which computes the expected return

on the basis of the projected rate of return on the market, the beta coefficient of the security and

risk-free rate. The equation for CAPM to calculate the rate of return is

E(R) = Rf + ß (Rmarket – Rf)

The CAPM is a key domain of financial management. Indeed, it has even been proposed that

financial management only turned into an academic discipline after William Sharpe released his

derivation of the CAPM in the year 1964 (Kerzner and Saladis, 2017).

The Weighted Average Cost of Capital (WACC) method can be employed as the discount rate in

investment evaluation, given some restrictive presumptions are satisfied. These presumptions are

basically claiming that WACC can be utilized as the discount rate given that the investment

project does not alter either the financial or the business risk of the investing party. If the

business risk of the investment mosaic is not the same as that of the investing entity, the CAPM

5

securities (Kempf and Memmel, 2006). This reasoning is in alignment with many facets of the

low variance anomaly entailing why it has fostered in the past few years even as the dominance

of institutional investors has increased.

Minimum market portfolios are more flexible in market downturns. As the business cycle finally

recoups, a minimum variance portfolio tends to ensure compounding performance in comparison

to return provided by market. One of the biggest advantages of the minimum variance portfolio

is that it really eliminates expected returns from the optimization which are tough to handle. As

the minimum variance portfolios have the sole goal of decreasing risk, instead of striving to

optimize the reward-risk ratio. Further, minimum variance portfolio optimization results in

noticeable attention on low variance securities in against of the cost of exploiting correlation

properties (Clarke, De Silva and Thorley, 2011). While MVP is not ideal portfolios, but they

might be appropriate for investors who intend to load up on low-risk stocks. As estimation risk

natural to projected returns is a known aspect, the fact that the MVP depends just on risk criteria

is an attractive attribute.

The relevance of the CAPM equation

The Capital Asset Pricing Model (CAPM) is a framework which computes the expected return

on the basis of the projected rate of return on the market, the beta coefficient of the security and

risk-free rate. The equation for CAPM to calculate the rate of return is

E(R) = Rf + ß (Rmarket – Rf)

The CAPM is a key domain of financial management. Indeed, it has even been proposed that

financial management only turned into an academic discipline after William Sharpe released his

derivation of the CAPM in the year 1964 (Kerzner and Saladis, 2017).

The Weighted Average Cost of Capital (WACC) method can be employed as the discount rate in

investment evaluation, given some restrictive presumptions are satisfied. These presumptions are

basically claiming that WACC can be utilized as the discount rate given that the investment

project does not alter either the financial or the business risk of the investing party. If the

business risk of the investment mosaic is not the same as that of the investing entity, the CAPM

5

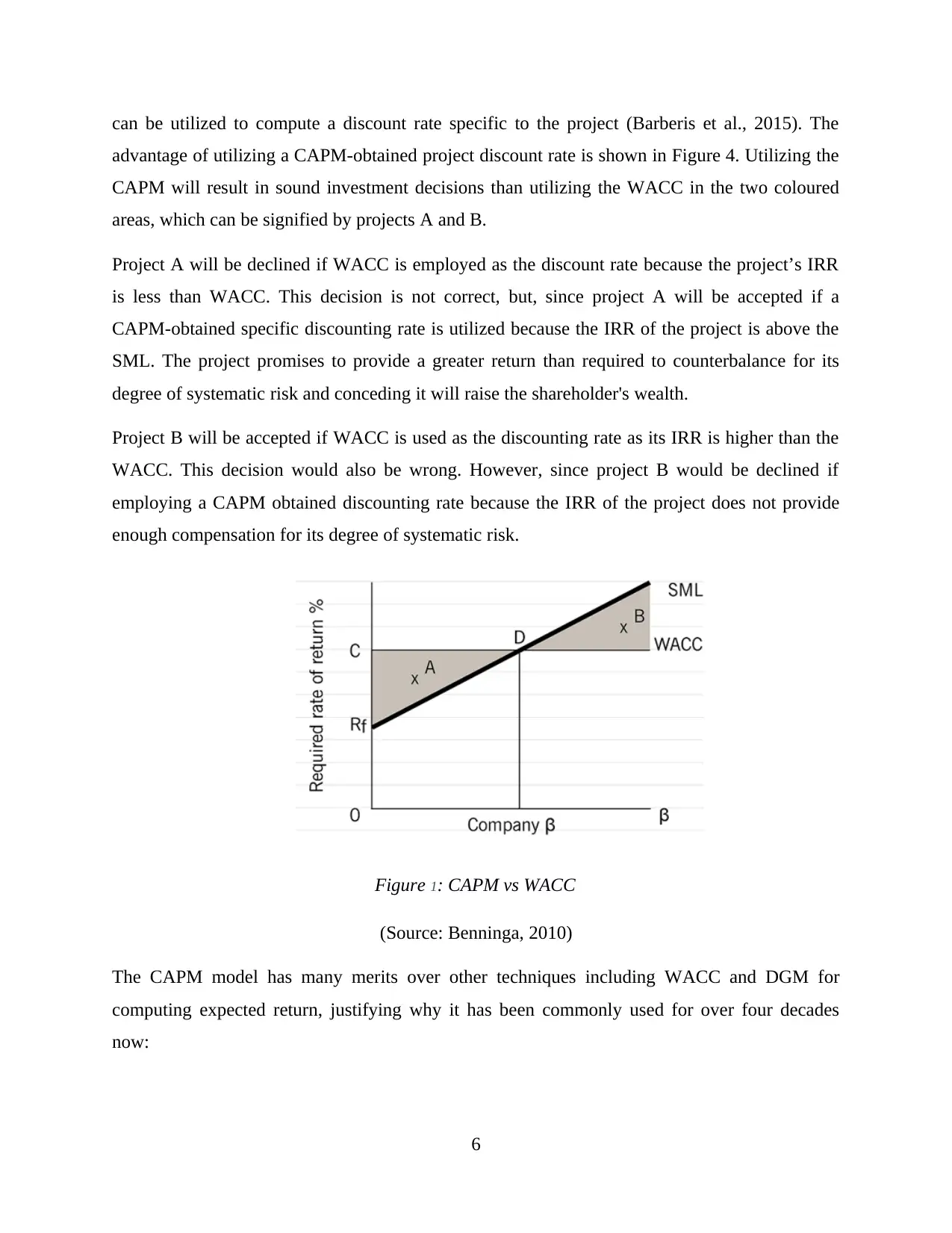

can be utilized to compute a discount rate specific to the project (Barberis et al., 2015). The

advantage of utilizing a CAPM-obtained project discount rate is shown in Figure 4. Utilizing the

CAPM will result in sound investment decisions than utilizing the WACC in the two coloured

areas, which can be signified by projects A and B.

Project A will be declined if WACC is employed as the discount rate because the project’s IRR

is less than WACC. This decision is not correct, but, since project A will be accepted if a

CAPM-obtained specific discounting rate is utilized because the IRR of the project is above the

SML. The project promises to provide a greater return than required to counterbalance for its

degree of systematic risk and conceding it will raise the shareholder's wealth.

Project B will be accepted if WACC is used as the discounting rate as its IRR is higher than the

WACC. This decision would also be wrong. However, since project B would be declined if

employing a CAPM obtained discounting rate because the IRR of the project does not provide

enough compensation for its degree of systematic risk.

Figure 1: CAPM vs WACC

(Source: Benninga, 2010)

The CAPM model has many merits over other techniques including WACC and DGM for

computing expected return, justifying why it has been commonly used for over four decades

now:

6

advantage of utilizing a CAPM-obtained project discount rate is shown in Figure 4. Utilizing the

CAPM will result in sound investment decisions than utilizing the WACC in the two coloured

areas, which can be signified by projects A and B.

Project A will be declined if WACC is employed as the discount rate because the project’s IRR

is less than WACC. This decision is not correct, but, since project A will be accepted if a

CAPM-obtained specific discounting rate is utilized because the IRR of the project is above the

SML. The project promises to provide a greater return than required to counterbalance for its

degree of systematic risk and conceding it will raise the shareholder's wealth.

Project B will be accepted if WACC is used as the discounting rate as its IRR is higher than the

WACC. This decision would also be wrong. However, since project B would be declined if

employing a CAPM obtained discounting rate because the IRR of the project does not provide

enough compensation for its degree of systematic risk.

Figure 1: CAPM vs WACC

(Source: Benninga, 2010)

The CAPM model has many merits over other techniques including WACC and DGM for

computing expected return, justifying why it has been commonly used for over four decades

now:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It only considers systematic risk, showing a real scenario in which majority investors

have a diverse portfolio supported by elimination of unsystematic risk in an essential

manner.

It is a theoretically obtained relationship among expected return and systematic risk. This

approach is prone to regular empirical testing and research (Kerzner and Saladis, 2017).

It is often viewed as a much advanced and better technique to calculate the cost of equity

in comparison to the Dividend Growth Model (DGM) in that it clearly considers a firm’s

degree of systematic risk compared to the share market as a whole.

It is evidently better than WACC in offering discount rates for utilization in investment

evaluation.

When businesses examine prospects, if the business combination and financing vary from

the existing business, then other expected return computations like WACC are rendered

useless. However, CAPM can be used in this situation (Bekaert and Hodrick, 2017).

The bottom line is that no model is ideal. However, each must have some attributes

which render it helpful and suitable. CAPM, though criticized for some of its unrealistic

presumptions, offers a more usable result than either WACC or DDM in many scenarios. It is

stress-tested and easily computed, and when employed together with other elements of an

investment mosaic, it can offer unmatched yield data which can remove or support a likely

investment (Petty et al., 2015).

Conclusion

By considering the present study conclusion can be drawn that SML and CML both assist in

evaluating efficiency on portfolios but on the basis of different backgrounds. By the application

of the minimum variance portfolio, an investor can attain expected returns from the optimization

which are tough to handle. Further, CAPM is viable in comparison to other equations as it covers

overall aspects concerned with the market for analysis of securities.

7

have a diverse portfolio supported by elimination of unsystematic risk in an essential

manner.

It is a theoretically obtained relationship among expected return and systematic risk. This

approach is prone to regular empirical testing and research (Kerzner and Saladis, 2017).

It is often viewed as a much advanced and better technique to calculate the cost of equity

in comparison to the Dividend Growth Model (DGM) in that it clearly considers a firm’s

degree of systematic risk compared to the share market as a whole.

It is evidently better than WACC in offering discount rates for utilization in investment

evaluation.

When businesses examine prospects, if the business combination and financing vary from

the existing business, then other expected return computations like WACC are rendered

useless. However, CAPM can be used in this situation (Bekaert and Hodrick, 2017).

The bottom line is that no model is ideal. However, each must have some attributes

which render it helpful and suitable. CAPM, though criticized for some of its unrealistic

presumptions, offers a more usable result than either WACC or DDM in many scenarios. It is

stress-tested and easily computed, and when employed together with other elements of an

investment mosaic, it can offer unmatched yield data which can remove or support a likely

investment (Petty et al., 2015).

Conclusion

By considering the present study conclusion can be drawn that SML and CML both assist in

evaluating efficiency on portfolios but on the basis of different backgrounds. By the application

of the minimum variance portfolio, an investor can attain expected returns from the optimization

which are tough to handle. Further, CAPM is viable in comparison to other equations as it covers

overall aspects concerned with the market for analysis of securities.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative capital

asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge University

Press.

Benninga, S., 2010. Principles of finance with excel. OUP Catalogue.

Bodnar, T., Mazur, S. and Okhrin, Y., 2017. Bayesian estimation of the global minimum

variance portfolio. European Journal of Operational Research, 256(1), pp.292-307.

Clarke, R., De Silva, H. and Thorley, S., 2011. Minimum-variance portfolio

composition. Journal of Portfolio Management, 37(2), p.31.

Hong, H. and Sraer, D.A., 2016. Speculative betas. The Journal of Finance, 71(5), pp.2095-

2144.

Kempf, A. and Memmel, C., 2006. Estimating the global minimum variance

portfolio. Schmalenbach Business Review, 58(4), pp.332-348.

Kerzner, H. and Saladis, F.P., 2017. Project management workbook and PMP/CAPM exam

study guide. John Wiley & Sons.

Maillet, B., Tokpavi, S. and Vaucher, B., 2015. Global minimum variance portfolio optimisation

under some model risk: A robust regression-based approach. European Journal of Operational

Research, 244(1), pp.289-299.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M., 2015. Financial

management: Principles and applications. Pearson Higher Education AU.

Pilbeam, K., 2018. Finance & financial markets. Macmillan International Higher Education.

Sharpe, W., 2017. Capital Market Theory, Efficiency, and Imperfections. Quantitative Financial

Analytics: The Path to Investment Profits, p.445.

Sornette, D., 2017. Why stock markets crash: critical events in complex financial systems.

Princeton University Press.

Yang, L., Couillet, R. and McKay, M.R., 2015. A robust statistics approach to minimum

variance portfolio optimization. IEEE Transactions on Signal Processing, 63(24), pp.6684-6697.

8

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative capital

asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge University

Press.

Benninga, S., 2010. Principles of finance with excel. OUP Catalogue.

Bodnar, T., Mazur, S. and Okhrin, Y., 2017. Bayesian estimation of the global minimum

variance portfolio. European Journal of Operational Research, 256(1), pp.292-307.

Clarke, R., De Silva, H. and Thorley, S., 2011. Minimum-variance portfolio

composition. Journal of Portfolio Management, 37(2), p.31.

Hong, H. and Sraer, D.A., 2016. Speculative betas. The Journal of Finance, 71(5), pp.2095-

2144.

Kempf, A. and Memmel, C., 2006. Estimating the global minimum variance

portfolio. Schmalenbach Business Review, 58(4), pp.332-348.

Kerzner, H. and Saladis, F.P., 2017. Project management workbook and PMP/CAPM exam

study guide. John Wiley & Sons.

Maillet, B., Tokpavi, S. and Vaucher, B., 2015. Global minimum variance portfolio optimisation

under some model risk: A robust regression-based approach. European Journal of Operational

Research, 244(1), pp.289-299.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M., 2015. Financial

management: Principles and applications. Pearson Higher Education AU.

Pilbeam, K., 2018. Finance & financial markets. Macmillan International Higher Education.

Sharpe, W., 2017. Capital Market Theory, Efficiency, and Imperfections. Quantitative Financial

Analytics: The Path to Investment Profits, p.445.

Sornette, D., 2017. Why stock markets crash: critical events in complex financial systems.

Princeton University Press.

Yang, L., Couillet, R. and McKay, M.R., 2015. A robust statistics approach to minimum

variance portfolio optimization. IEEE Transactions on Signal Processing, 63(24), pp.6684-6697.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.