FIN20014 - Financial Management: ALLCURE Inc. Project Report

VerifiedAdded on 2023/06/03

|16

|2933

|429

Report

AI Summary

This report presents a financial feasibility analysis of a drug product under consideration by ALLCURE Inc. It employs capital budgeting techniques, including Net Present Value (NPV) and payback period, to assess the project's viability. The analysis considers both qualitative and quantitative factors, such as management expertise and market conditions. The findings indicate that the production of P-REC is beneficial at an 18% discount rate, yielding a positive NPV and a payback period of 5.51 years. However, if the discount rate increases to 24%, the alternative product T-REC becomes more attractive. The report recommends that the management consider the risks and uncertainties associated with capital budgeting decisions before making a final choice, emphasizing the importance of accurate cash flow forecasting and sensitivity analysis to changes in the discount rate.

Accounting and Financial Analysis Report

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report presented here deals with the financial feasibility analysis of a drug product

being considered for development by ALLCURE Inc. The results of the analysis depicts that the

production of P-REC would be beneficial for the company if the discount rate happens to be

18%. The NPV of the product at this rate is $972,011.71 with the payback period of 5.51 years.

However, if the discount rate increases to 24%, then it would be more beneficial for the company

to go for alternative product T-REC in place of P-REC. T-REC would produce an NPV of

$410,070.19 with the payback period of 5.34 years which is better than P-REC. Further, there are

many risks and uncertainties associated with the capital budgeting decisions which should be

taken into account by the management of the company before making the final choice.

2

The report presented here deals with the financial feasibility analysis of a drug product

being considered for development by ALLCURE Inc. The results of the analysis depicts that the

production of P-REC would be beneficial for the company if the discount rate happens to be

18%. The NPV of the product at this rate is $972,011.71 with the payback period of 5.51 years.

However, if the discount rate increases to 24%, then it would be more beneficial for the company

to go for alternative product T-REC in place of P-REC. T-REC would produce an NPV of

$410,070.19 with the payback period of 5.34 years which is better than P-REC. Further, there are

many risks and uncertainties associated with the capital budgeting decisions which should be

taken into account by the management of the company before making the final choice.

2

Contents

Introduction.................................................................................................................................................4

Findings.......................................................................................................................................................4

Qualitative...............................................................................................................................................4

Quantitative.............................................................................................................................................4

Recommendations and Justifications..........................................................................................................6

Detailed Comparison and Recommendations.............................................................................................7

Conclusion...................................................................................................................................................8

References...................................................................................................................................................9

Appendix...................................................................................................................................................10

3

Introduction.................................................................................................................................................4

Findings.......................................................................................................................................................4

Qualitative...............................................................................................................................................4

Quantitative.............................................................................................................................................4

Recommendations and Justifications..........................................................................................................6

Detailed Comparison and Recommendations.............................................................................................7

Conclusion...................................................................................................................................................8

References...................................................................................................................................................9

Appendix...................................................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The role of financial feasibility is crucial in deciding as to whether a project should be

accepted and implemented or not. Financial feasibility means assessing the project from finance

view point. The capital budgeting technique is applied to assess the financial feasibility of a

project which involves computation of net present value, payback period, or IRR (Andor,

Mohanty, and Toth, 2015). In this context, a report has been presented here that provide analysis

of financial feasibility of a project being considered by ALLCURE Inc. ALLCURE Inc is

considering bringing a pre-version of a drug named P-REC.

Findings

Qualitative

It is not only the quantitative analysis which is to be focused by an analyst in analyzing a

project’s financial feasibility. The qualitative analysis also equally plays significant role in such

analysis and decisions. The qualitative analysis covers factors which are not quantifiable such as

management expertise of a firm, industry cycle, research and development, labor relations etc

(Ragin, 2014). In the current case of ALLCURE Inc, the company is considering an option of

establishing production line for P-REC. There are various qualitative factors which require

consideration in this decision. For instance, the management will have to sacrifice the use of

facilities and factory site being made for the current purposes. The company stands at the danger

of losing clients of the existing product or services. On the other hand, the company may also

enjoy added advantages due to implementation of the new project. The new project might help

the company to increase sales of the existing products. P-REC which is a pre-version of a drug

could help the company in enhancing the sale of its existing drugs. So, it would be advantageous

for the company to accept and go along with the project (Ragin, 2014).

Quantitative

The second method which is applied in assessing the financial feasibility of a project is

quantitative analysis. Quantitative analysis involves mathematical base being used in the analysis

(Hopkinson, 2017). There are various capital budgeting techniques which are applied in

conducting the quantitative analysis. In the current case the question in front of the management

of ALLCURE Inc is that whether they should accept the investment in establishing production

4

The role of financial feasibility is crucial in deciding as to whether a project should be

accepted and implemented or not. Financial feasibility means assessing the project from finance

view point. The capital budgeting technique is applied to assess the financial feasibility of a

project which involves computation of net present value, payback period, or IRR (Andor,

Mohanty, and Toth, 2015). In this context, a report has been presented here that provide analysis

of financial feasibility of a project being considered by ALLCURE Inc. ALLCURE Inc is

considering bringing a pre-version of a drug named P-REC.

Findings

Qualitative

It is not only the quantitative analysis which is to be focused by an analyst in analyzing a

project’s financial feasibility. The qualitative analysis also equally plays significant role in such

analysis and decisions. The qualitative analysis covers factors which are not quantifiable such as

management expertise of a firm, industry cycle, research and development, labor relations etc

(Ragin, 2014). In the current case of ALLCURE Inc, the company is considering an option of

establishing production line for P-REC. There are various qualitative factors which require

consideration in this decision. For instance, the management will have to sacrifice the use of

facilities and factory site being made for the current purposes. The company stands at the danger

of losing clients of the existing product or services. On the other hand, the company may also

enjoy added advantages due to implementation of the new project. The new project might help

the company to increase sales of the existing products. P-REC which is a pre-version of a drug

could help the company in enhancing the sale of its existing drugs. So, it would be advantageous

for the company to accept and go along with the project (Ragin, 2014).

Quantitative

The second method which is applied in assessing the financial feasibility of a project is

quantitative analysis. Quantitative analysis involves mathematical base being used in the analysis

(Hopkinson, 2017). There are various capital budgeting techniques which are applied in

conducting the quantitative analysis. In the current case the question in front of the management

of ALLCURE Inc is that whether they should accept the investment in establishing production

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

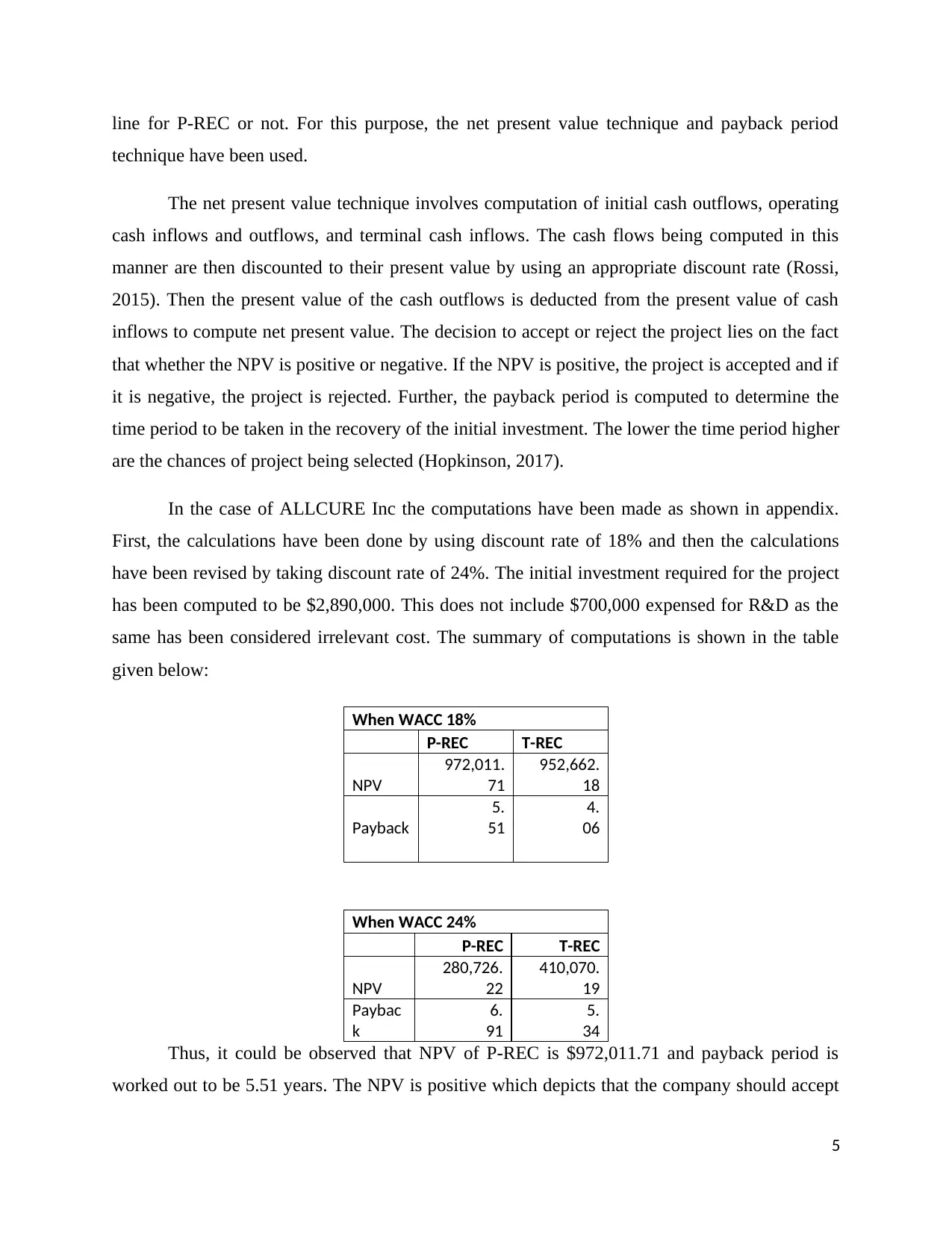

line for P-REC or not. For this purpose, the net present value technique and payback period

technique have been used.

The net present value technique involves computation of initial cash outflows, operating

cash inflows and outflows, and terminal cash inflows. The cash flows being computed in this

manner are then discounted to their present value by using an appropriate discount rate (Rossi,

2015). Then the present value of the cash outflows is deducted from the present value of cash

inflows to compute net present value. The decision to accept or reject the project lies on the fact

that whether the NPV is positive or negative. If the NPV is positive, the project is accepted and if

it is negative, the project is rejected. Further, the payback period is computed to determine the

time period to be taken in the recovery of the initial investment. The lower the time period higher

are the chances of project being selected (Hopkinson, 2017).

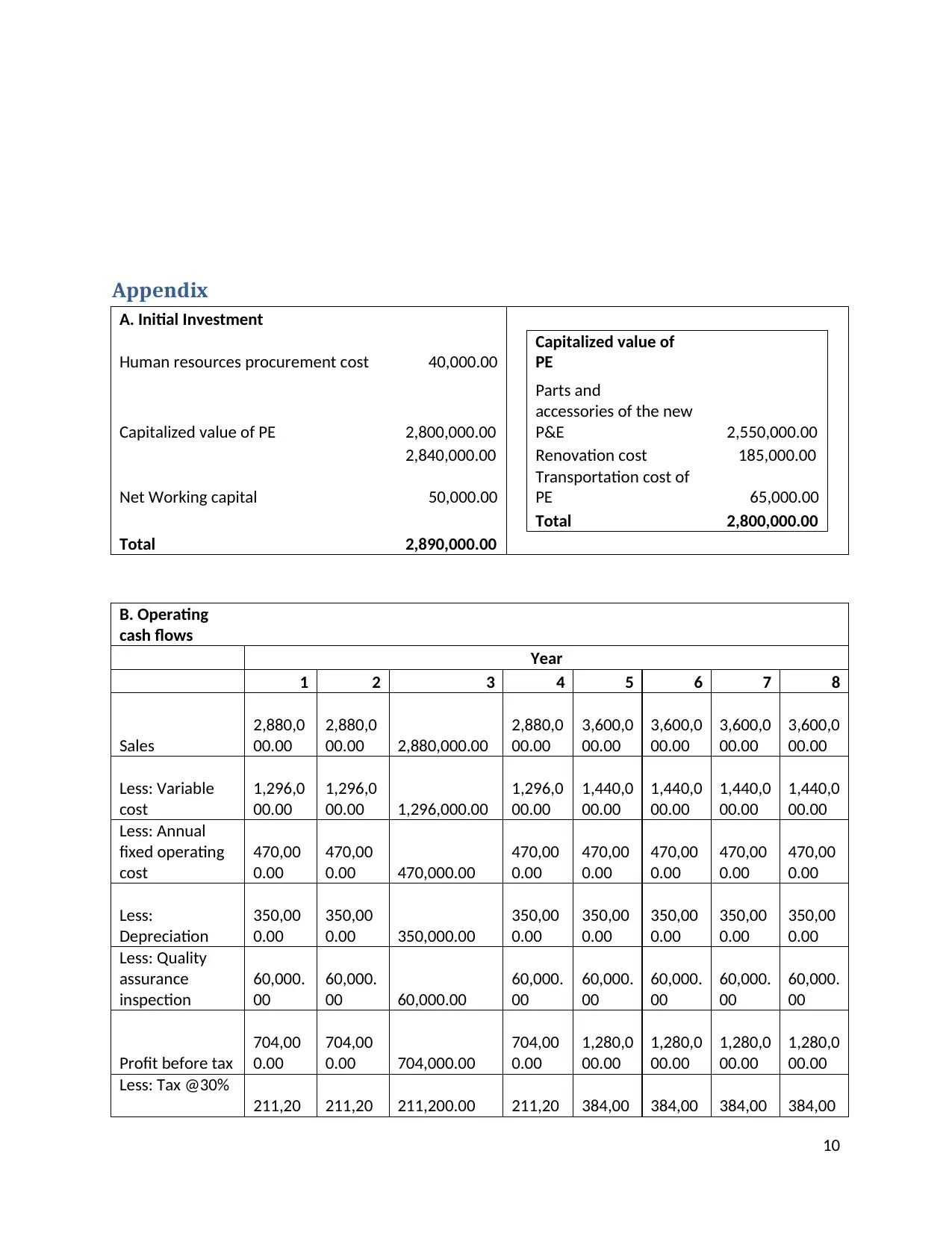

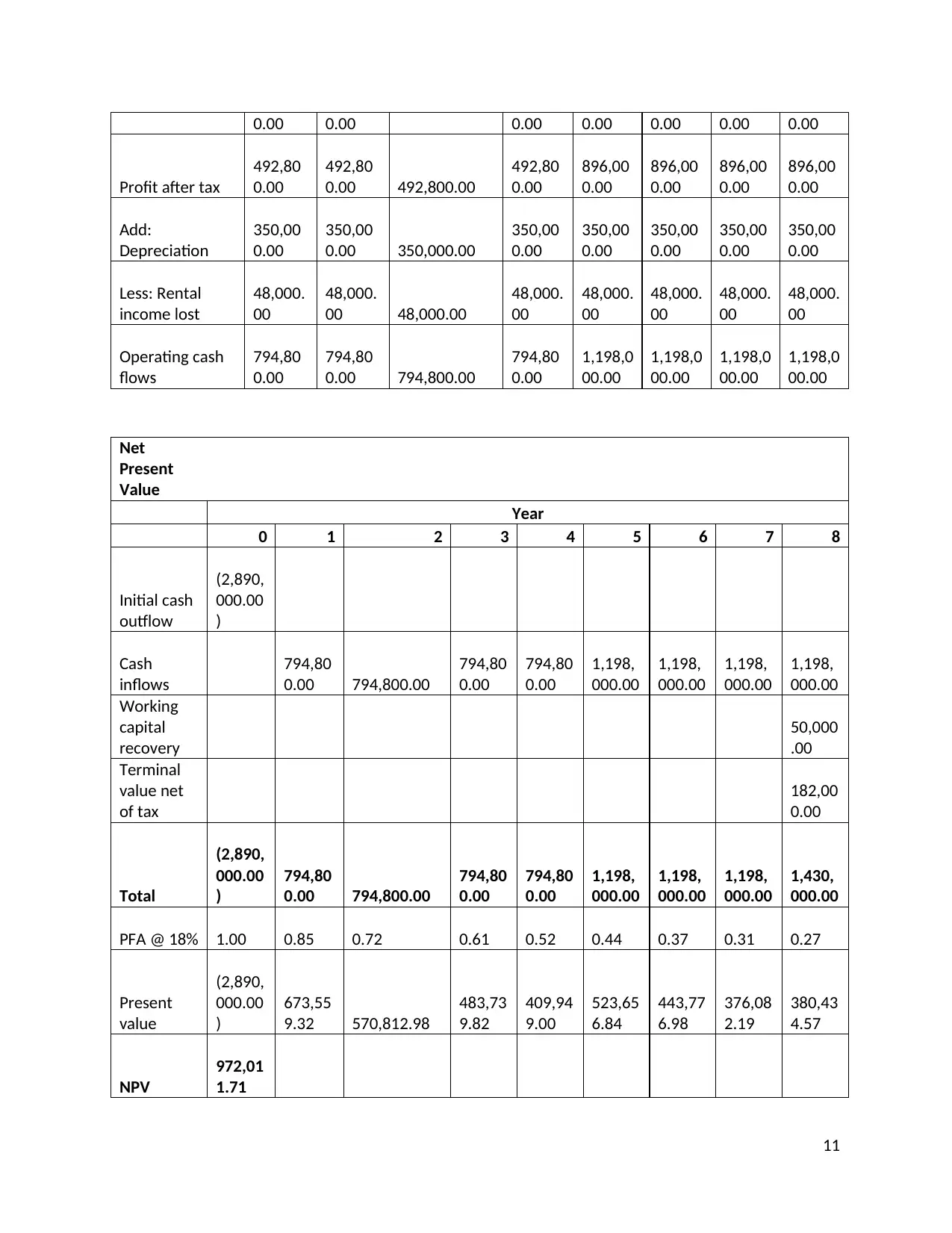

In the case of ALLCURE Inc the computations have been made as shown in appendix.

First, the calculations have been done by using discount rate of 18% and then the calculations

have been revised by taking discount rate of 24%. The initial investment required for the project

has been computed to be $2,890,000. This does not include $700,000 expensed for R&D as the

same has been considered irrelevant cost. The summary of computations is shown in the table

given below:

When WACC 18%

P-REC T-REC

NPV

972,011.

71

952,662.

18

Payback

5.

51

4.

06

When WACC 24%

P-REC T-REC

NPV

280,726.

22

410,070.

19

Paybac

k

6.

91

5.

34

Thus, it could be observed that NPV of P-REC is $972,011.71 and payback period is

worked out to be 5.51 years. The NPV is positive which depicts that the company should accept

5

technique have been used.

The net present value technique involves computation of initial cash outflows, operating

cash inflows and outflows, and terminal cash inflows. The cash flows being computed in this

manner are then discounted to their present value by using an appropriate discount rate (Rossi,

2015). Then the present value of the cash outflows is deducted from the present value of cash

inflows to compute net present value. The decision to accept or reject the project lies on the fact

that whether the NPV is positive or negative. If the NPV is positive, the project is accepted and if

it is negative, the project is rejected. Further, the payback period is computed to determine the

time period to be taken in the recovery of the initial investment. The lower the time period higher

are the chances of project being selected (Hopkinson, 2017).

In the case of ALLCURE Inc the computations have been made as shown in appendix.

First, the calculations have been done by using discount rate of 18% and then the calculations

have been revised by taking discount rate of 24%. The initial investment required for the project

has been computed to be $2,890,000. This does not include $700,000 expensed for R&D as the

same has been considered irrelevant cost. The summary of computations is shown in the table

given below:

When WACC 18%

P-REC T-REC

NPV

972,011.

71

952,662.

18

Payback

5.

51

4.

06

When WACC 24%

P-REC T-REC

NPV

280,726.

22

410,070.

19

Paybac

k

6.

91

5.

34

Thus, it could be observed that NPV of P-REC is $972,011.71 and payback period is

worked out to be 5.51 years. The NPV is positive which depicts that the company should accept

5

the project. Further, the management apprehends that the payback period of the project should be

5 years or less. The payback of P-REC is 5.51 years which is higher than what the management

apprehends. Thus, if the decision is purely based on payback period, the management would

reject the project, however, if the decision is based on NPV, the management would accept the

project.

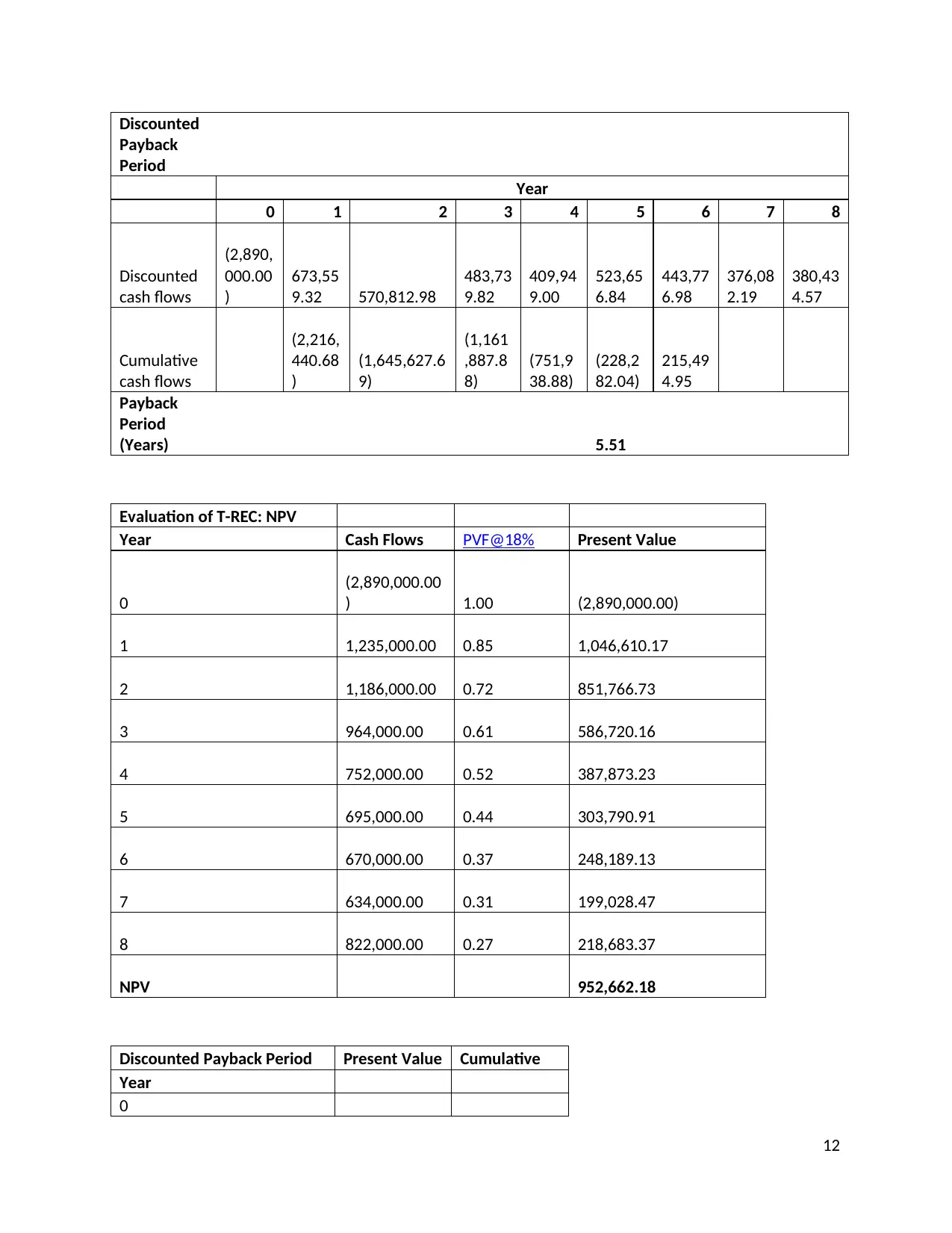

The NPV of alternative product T-REC is worked out to be $952,662.18 and its payback

period is 4.06 years. The NPV is lower as compared to P-REC and the payback period is also

lower. The lower NPV put the alternative less desirable but lower payback period makes it

preferable for the management. If the decision is based on payback period, the management

would prefer T-REC over P-REC.

The scenario changes when the discount rate is changed from 18% to 24%. It could be

observed that the NPV of P-REC declines drastically and payback period increases to 6.91 years

from 5.51 years. The same effect is perceived on T-REC but with less intensity. The NPV of T-

REC still stands at $410,070.19 which is higher than that of P-REC. Further, the payback period

is also 5.34 years which is better as compared to P-REC. Therefore, T-REC completely

outperforms P-REC at discount rate of 24%.

The capital budgeting decisions are surrounded by risk and uncertainties. There are many

risks and uncertainties associated with the current project. The biggest uncertainty is associated

with the discount rate. Further, the operating cash flows have also been worked out based on

different assumptions. There is a possibility of assumptions being going wrong. If it happens, the

operating cash flows would change and it might turn negatively for the company (Chadha, 2018).

Recommendations and Justifications

The management has two primary parameters of deciding the project. The first is payback

period and the second is profitability. The management sets the target for payback period as 5

years or less and profitability should be enough to cover R&D expenses of $24,000 per year. If

the project meets these two criteria, the project becomes acceptable. In the case of ALLCURE

Inc, the management first analyzed P-REC which is a pre-version of a drug. The analysis was

made at two different discount rates i.e. 18% and 24%.

6

5 years or less. The payback of P-REC is 5.51 years which is higher than what the management

apprehends. Thus, if the decision is purely based on payback period, the management would

reject the project, however, if the decision is based on NPV, the management would accept the

project.

The NPV of alternative product T-REC is worked out to be $952,662.18 and its payback

period is 4.06 years. The NPV is lower as compared to P-REC and the payback period is also

lower. The lower NPV put the alternative less desirable but lower payback period makes it

preferable for the management. If the decision is based on payback period, the management

would prefer T-REC over P-REC.

The scenario changes when the discount rate is changed from 18% to 24%. It could be

observed that the NPV of P-REC declines drastically and payback period increases to 6.91 years

from 5.51 years. The same effect is perceived on T-REC but with less intensity. The NPV of T-

REC still stands at $410,070.19 which is higher than that of P-REC. Further, the payback period

is also 5.34 years which is better as compared to P-REC. Therefore, T-REC completely

outperforms P-REC at discount rate of 24%.

The capital budgeting decisions are surrounded by risk and uncertainties. There are many

risks and uncertainties associated with the current project. The biggest uncertainty is associated

with the discount rate. Further, the operating cash flows have also been worked out based on

different assumptions. There is a possibility of assumptions being going wrong. If it happens, the

operating cash flows would change and it might turn negatively for the company (Chadha, 2018).

Recommendations and Justifications

The management has two primary parameters of deciding the project. The first is payback

period and the second is profitability. The management sets the target for payback period as 5

years or less and profitability should be enough to cover R&D expenses of $24,000 per year. If

the project meets these two criteria, the project becomes acceptable. In the case of ALLCURE

Inc, the management first analyzed P-REC which is a pre-version of a drug. The analysis was

made at two different discount rates i.e. 18% and 24%.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

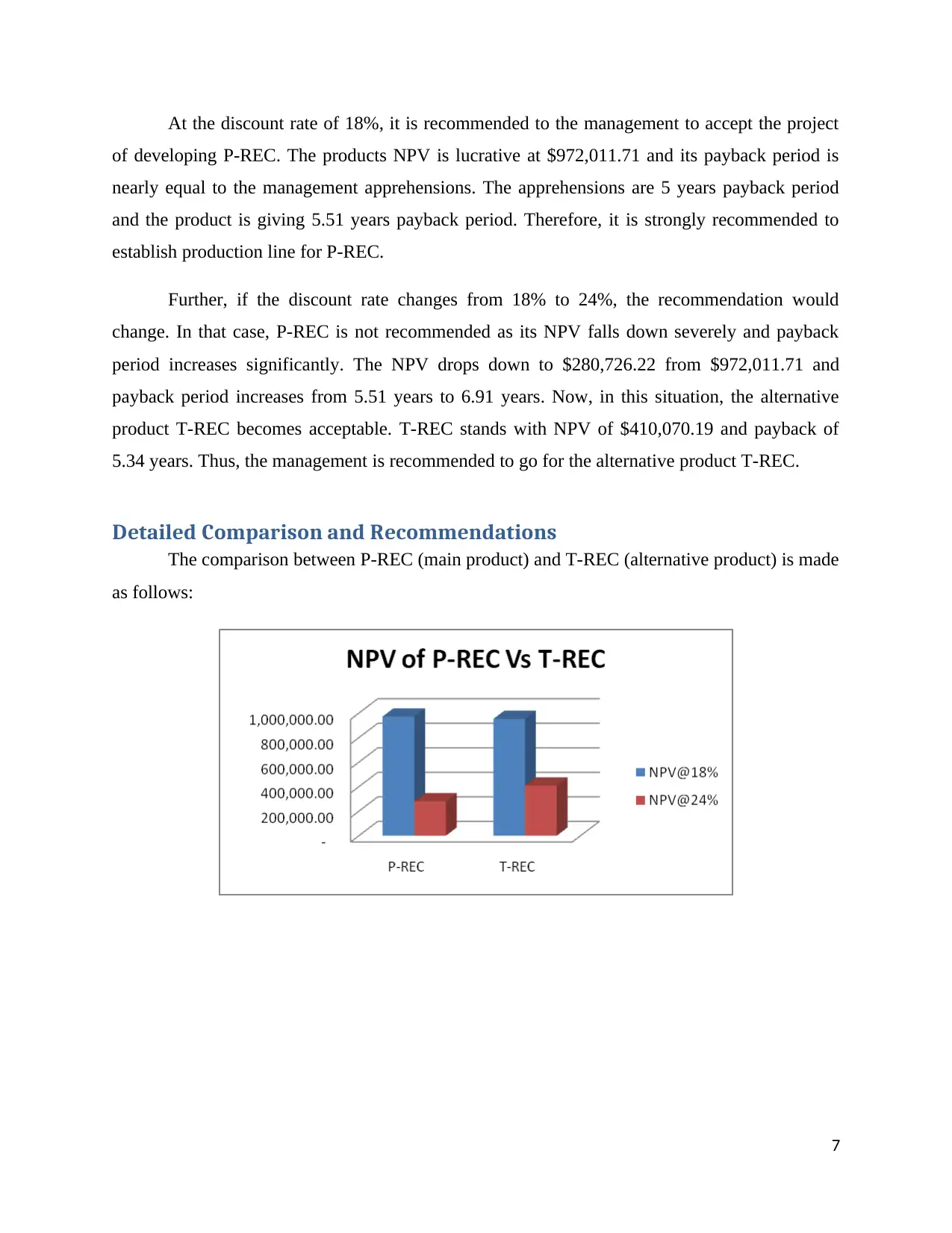

At the discount rate of 18%, it is recommended to the management to accept the project

of developing P-REC. The products NPV is lucrative at $972,011.71 and its payback period is

nearly equal to the management apprehensions. The apprehensions are 5 years payback period

and the product is giving 5.51 years payback period. Therefore, it is strongly recommended to

establish production line for P-REC.

Further, if the discount rate changes from 18% to 24%, the recommendation would

change. In that case, P-REC is not recommended as its NPV falls down severely and payback

period increases significantly. The NPV drops down to $280,726.22 from $972,011.71 and

payback period increases from 5.51 years to 6.91 years. Now, in this situation, the alternative

product T-REC becomes acceptable. T-REC stands with NPV of $410,070.19 and payback of

5.34 years. Thus, the management is recommended to go for the alternative product T-REC.

Detailed Comparison and Recommendations

The comparison between P-REC (main product) and T-REC (alternative product) is made

as follows:

7

of developing P-REC. The products NPV is lucrative at $972,011.71 and its payback period is

nearly equal to the management apprehensions. The apprehensions are 5 years payback period

and the product is giving 5.51 years payback period. Therefore, it is strongly recommended to

establish production line for P-REC.

Further, if the discount rate changes from 18% to 24%, the recommendation would

change. In that case, P-REC is not recommended as its NPV falls down severely and payback

period increases significantly. The NPV drops down to $280,726.22 from $972,011.71 and

payback period increases from 5.51 years to 6.91 years. Now, in this situation, the alternative

product T-REC becomes acceptable. T-REC stands with NPV of $410,070.19 and payback of

5.34 years. Thus, the management is recommended to go for the alternative product T-REC.

Detailed Comparison and Recommendations

The comparison between P-REC (main product) and T-REC (alternative product) is made

as follows:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

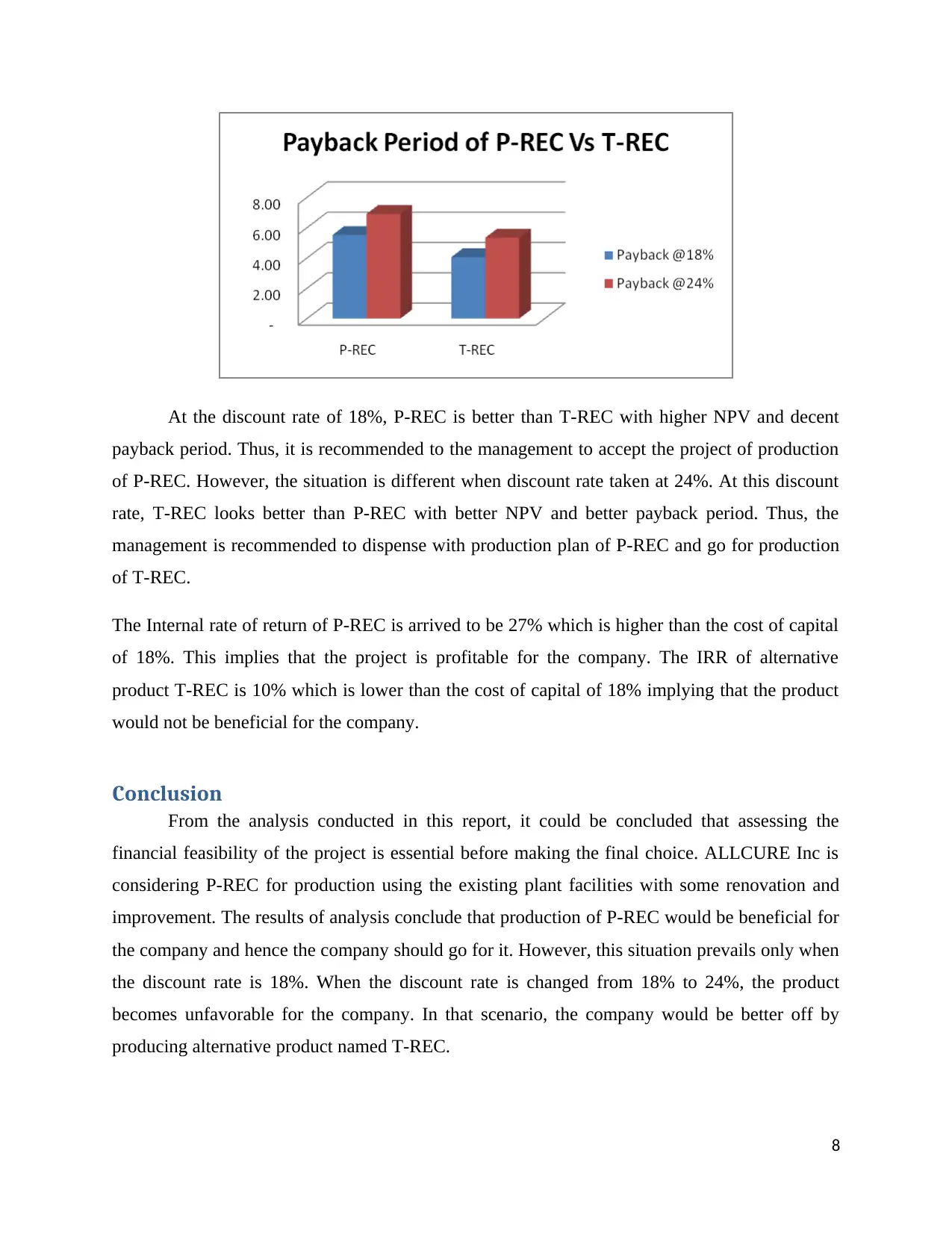

At the discount rate of 18%, P-REC is better than T-REC with higher NPV and decent

payback period. Thus, it is recommended to the management to accept the project of production

of P-REC. However, the situation is different when discount rate taken at 24%. At this discount

rate, T-REC looks better than P-REC with better NPV and better payback period. Thus, the

management is recommended to dispense with production plan of P-REC and go for production

of T-REC.

The Internal rate of return of P-REC is arrived to be 27% which is higher than the cost of capital

of 18%. This implies that the project is profitable for the company. The IRR of alternative

product T-REC is 10% which is lower than the cost of capital of 18% implying that the product

would not be beneficial for the company.

Conclusion

From the analysis conducted in this report, it could be concluded that assessing the

financial feasibility of the project is essential before making the final choice. ALLCURE Inc is

considering P-REC for production using the existing plant facilities with some renovation and

improvement. The results of analysis conclude that production of P-REC would be beneficial for

the company and hence the company should go for it. However, this situation prevails only when

the discount rate is 18%. When the discount rate is changed from 18% to 24%, the product

becomes unfavorable for the company. In that scenario, the company would be better off by

producing alternative product named T-REC.

8

payback period. Thus, it is recommended to the management to accept the project of production

of P-REC. However, the situation is different when discount rate taken at 24%. At this discount

rate, T-REC looks better than P-REC with better NPV and better payback period. Thus, the

management is recommended to dispense with production plan of P-REC and go for production

of T-REC.

The Internal rate of return of P-REC is arrived to be 27% which is higher than the cost of capital

of 18%. This implies that the project is profitable for the company. The IRR of alternative

product T-REC is 10% which is lower than the cost of capital of 18% implying that the product

would not be beneficial for the company.

Conclusion

From the analysis conducted in this report, it could be concluded that assessing the

financial feasibility of the project is essential before making the final choice. ALLCURE Inc is

considering P-REC for production using the existing plant facilities with some renovation and

improvement. The results of analysis conclude that production of P-REC would be beneficial for

the company and hence the company should go for it. However, this situation prevails only when

the discount rate is 18%. When the discount rate is changed from 18% to 24%, the product

becomes unfavorable for the company. In that scenario, the company would be better off by

producing alternative product named T-REC.

8

References

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Chadha, S., 2018, March. CAPITAL BUDGETING TECHNIQUES: EVIDENCE FROM

INDIAN MANUFACTURING SECTOR. In Proceedings of NIDA International Business

Conference 2018–Dealing with Disruption (p. 356).

Hopkinson, M., 2017. Net Present value and risk modelling for projects. Routledge.

Ragin, C.C., 2014. The comparative method: Moving beyond qualitative and quantitative

strategies. Univ of California Press.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

9

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of Central

and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Chadha, S., 2018, March. CAPITAL BUDGETING TECHNIQUES: EVIDENCE FROM

INDIAN MANUFACTURING SECTOR. In Proceedings of NIDA International Business

Conference 2018–Dealing with Disruption (p. 356).

Hopkinson, M., 2017. Net Present value and risk modelling for projects. Routledge.

Ragin, C.C., 2014. The comparative method: Moving beyond qualitative and quantitative

strategies. Univ of California Press.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International

Journal of Management Practice, 8(1), pp.43-56.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendix

A. Initial Investment

Human resources procurement cost 40,000.00

Capitalized value of

PE

Capitalized value of PE 2,800,000.00

Parts and

accessories of the new

P&E 2,550,000.00

2,840,000.00 Renovation cost 185,000.00

Net Working capital 50,000.00

Transportation cost of

PE 65,000.00

Total 2,800,000.00

Total 2,890,000.00

B. Operating

cash flows

Year

1 2 3 4 5 6 7 8

Sales

2,880,0

00.00

2,880,0

00.00 2,880,000.00

2,880,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

Less: Variable

cost

1,296,0

00.00

1,296,0

00.00 1,296,000.00

1,296,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

Less: Annual

fixed operating

cost

470,00

0.00

470,00

0.00 470,000.00

470,00

0.00

470,00

0.00

470,00

0.00

470,00

0.00

470,00

0.00

Less:

Depreciation

350,00

0.00

350,00

0.00 350,000.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

Less: Quality

assurance

inspection

60,000.

00

60,000.

00 60,000.00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

Profit before tax

704,00

0.00

704,00

0.00 704,000.00

704,00

0.00

1,280,0

00.00

1,280,0

00.00

1,280,0

00.00

1,280,0

00.00

Less: Tax @30%

211,20 211,20 211,200.00 211,20 384,00 384,00 384,00 384,00

10

A. Initial Investment

Human resources procurement cost 40,000.00

Capitalized value of

PE

Capitalized value of PE 2,800,000.00

Parts and

accessories of the new

P&E 2,550,000.00

2,840,000.00 Renovation cost 185,000.00

Net Working capital 50,000.00

Transportation cost of

PE 65,000.00

Total 2,800,000.00

Total 2,890,000.00

B. Operating

cash flows

Year

1 2 3 4 5 6 7 8

Sales

2,880,0

00.00

2,880,0

00.00 2,880,000.00

2,880,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

3,600,0

00.00

Less: Variable

cost

1,296,0

00.00

1,296,0

00.00 1,296,000.00

1,296,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

1,440,0

00.00

Less: Annual

fixed operating

cost

470,00

0.00

470,00

0.00 470,000.00

470,00

0.00

470,00

0.00

470,00

0.00

470,00

0.00

470,00

0.00

Less:

Depreciation

350,00

0.00

350,00

0.00 350,000.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

Less: Quality

assurance

inspection

60,000.

00

60,000.

00 60,000.00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

60,000.

00

Profit before tax

704,00

0.00

704,00

0.00 704,000.00

704,00

0.00

1,280,0

00.00

1,280,0

00.00

1,280,0

00.00

1,280,0

00.00

Less: Tax @30%

211,20 211,20 211,200.00 211,20 384,00 384,00 384,00 384,00

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.00 0.00 0.00 0.00 0.00 0.00 0.00

Profit after tax

492,80

0.00

492,80

0.00 492,800.00

492,80

0.00

896,00

0.00

896,00

0.00

896,00

0.00

896,00

0.00

Add:

Depreciation

350,00

0.00

350,00

0.00 350,000.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

Less: Rental

income lost

48,000.

00

48,000.

00 48,000.00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

Operating cash

flows

794,80

0.00

794,80

0.00 794,800.00

794,80

0.00

1,198,0

00.00

1,198,0

00.00

1,198,0

00.00

1,198,0

00.00

Net

Present

Value

Year

0 1 2 3 4 5 6 7 8

Initial cash

outflow

(2,890,

000.00

)

Cash

inflows

794,80

0.00 794,800.00

794,80

0.00

794,80

0.00

1,198,

000.00

1,198,

000.00

1,198,

000.00

1,198,

000.00

Working

capital

recovery

50,000

.00

Terminal

value net

of tax

182,00

0.00

Total

(2,890,

000.00

)

794,80

0.00 794,800.00

794,80

0.00

794,80

0.00

1,198,

000.00

1,198,

000.00

1,198,

000.00

1,430,

000.00

PFA @ 18% 1.00 0.85 0.72 0.61 0.52 0.44 0.37 0.31 0.27

Present

value

(2,890,

000.00

)

673,55

9.32 570,812.98

483,73

9.82

409,94

9.00

523,65

6.84

443,77

6.98

376,08

2.19

380,43

4.57

NPV

972,01

1.71

11

Profit after tax

492,80

0.00

492,80

0.00 492,800.00

492,80

0.00

896,00

0.00

896,00

0.00

896,00

0.00

896,00

0.00

Add:

Depreciation

350,00

0.00

350,00

0.00 350,000.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

350,00

0.00

Less: Rental

income lost

48,000.

00

48,000.

00 48,000.00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

48,000.

00

Operating cash

flows

794,80

0.00

794,80

0.00 794,800.00

794,80

0.00

1,198,0

00.00

1,198,0

00.00

1,198,0

00.00

1,198,0

00.00

Net

Present

Value

Year

0 1 2 3 4 5 6 7 8

Initial cash

outflow

(2,890,

000.00

)

Cash

inflows

794,80

0.00 794,800.00

794,80

0.00

794,80

0.00

1,198,

000.00

1,198,

000.00

1,198,

000.00

1,198,

000.00

Working

capital

recovery

50,000

.00

Terminal

value net

of tax

182,00

0.00

Total

(2,890,

000.00

)

794,80

0.00 794,800.00

794,80

0.00

794,80

0.00

1,198,

000.00

1,198,

000.00

1,198,

000.00

1,430,

000.00

PFA @ 18% 1.00 0.85 0.72 0.61 0.52 0.44 0.37 0.31 0.27

Present

value

(2,890,

000.00

)

673,55

9.32 570,812.98

483,73

9.82

409,94

9.00

523,65

6.84

443,77

6.98

376,08

2.19

380,43

4.57

NPV

972,01

1.71

11

Discounted

Payback

Period

Year

0 1 2 3 4 5 6 7 8

Discounted

cash flows

(2,890,

000.00

)

673,55

9.32 570,812.98

483,73

9.82

409,94

9.00

523,65

6.84

443,77

6.98

376,08

2.19

380,43

4.57

Cumulative

cash flows

(2,216,

440.68

)

(1,645,627.6

9)

(1,161

,887.8

8)

(751,9

38.88)

(228,2

82.04)

215,49

4.95

Payback

Period

(Years) 5.51

Evaluation of T-REC: NPV

Year Cash Flows PVF@18% Present Value

0

(2,890,000.00

) 1.00 (2,890,000.00)

1 1,235,000.00 0.85 1,046,610.17

2 1,186,000.00 0.72 851,766.73

3 964,000.00 0.61 586,720.16

4 752,000.00 0.52 387,873.23

5 695,000.00 0.44 303,790.91

6 670,000.00 0.37 248,189.13

7 634,000.00 0.31 199,028.47

8 822,000.00 0.27 218,683.37

NPV 952,662.18

Discounted Payback Period Present Value Cumulative

Year

0

12

Payback

Period

Year

0 1 2 3 4 5 6 7 8

Discounted

cash flows

(2,890,

000.00

)

673,55

9.32 570,812.98

483,73

9.82

409,94

9.00

523,65

6.84

443,77

6.98

376,08

2.19

380,43

4.57

Cumulative

cash flows

(2,216,

440.68

)

(1,645,627.6

9)

(1,161

,887.8

8)

(751,9

38.88)

(228,2

82.04)

215,49

4.95

Payback

Period

(Years) 5.51

Evaluation of T-REC: NPV

Year Cash Flows PVF@18% Present Value

0

(2,890,000.00

) 1.00 (2,890,000.00)

1 1,235,000.00 0.85 1,046,610.17

2 1,186,000.00 0.72 851,766.73

3 964,000.00 0.61 586,720.16

4 752,000.00 0.52 387,873.23

5 695,000.00 0.44 303,790.91

6 670,000.00 0.37 248,189.13

7 634,000.00 0.31 199,028.47

8 822,000.00 0.27 218,683.37

NPV 952,662.18

Discounted Payback Period Present Value Cumulative

Year

0

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.