FIN20014 Financial Analysis: Investment Appraisal for ALLCURE

VerifiedAdded on 2023/04/23

|22

|6231

|249

Report

AI Summary

This report assesses the financial viability of two product lines proposed by ALLCURE Inc. using investment appraisal techniques, including Net Present Value (NPV), Discounted Payback Period, and Internal Rate of Return (IRR). A qualitative analysis is also conducted to evaluate the social impact of the projects, considering ALLCURE Inc.'s involvement in pharmaceuticals. The analysis suggests that investing in the T-REC project is more beneficial due to its higher NPV at a 24% discount rate, acceptable IRR and discounted payback period. The qualitative analysis supports T-REC due to the potential health hazards associated with P-REC. The report recommends immediate investment in T-REC, with a reassessment of P-REC after further research and development.

Running head: FINANCIAL ANALYSIS

Financial Analysis

Name of the Student:

Name of the University:

Authors Note:

Financial Analysis

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

1

Executive Summary:

The assessment aims in evaluating the two-product line that is aimed by ALLCURE Inc. to

produce in future, for increasing its revenue generation capability. The analysis is based on

Investment appraisal techniques, which is used for detecting the financial viability of the

proposed projects. In addition, adequate evaluation of the qualitative analysis has been

conducted in the assessment for identifying social viability in approving the project.

ALLCURE Inc. deals with medicines, which can have negative and positive impact on the

health of the consumer that directly raises the social concerns of the CFO, while making any

kind of investment decisions. However, after evaluating all the relevant information

regarding the qualitative and quantitative analysis, it can be detected that investment T-REC

is highly beneficial for the organization. Therefore, ALLCURE Inc. can start the project with

T-REC and after getting the report from R&D about P-REC, the next project can be started.

1

Executive Summary:

The assessment aims in evaluating the two-product line that is aimed by ALLCURE Inc. to

produce in future, for increasing its revenue generation capability. The analysis is based on

Investment appraisal techniques, which is used for detecting the financial viability of the

proposed projects. In addition, adequate evaluation of the qualitative analysis has been

conducted in the assessment for identifying social viability in approving the project.

ALLCURE Inc. deals with medicines, which can have negative and positive impact on the

health of the consumer that directly raises the social concerns of the CFO, while making any

kind of investment decisions. However, after evaluating all the relevant information

regarding the qualitative and quantitative analysis, it can be detected that investment T-REC

is highly beneficial for the organization. Therefore, ALLCURE Inc. can start the project with

T-REC and after getting the report from R&D about P-REC, the next project can be started.

FINANCIAL ANALYSIS

2

Table of Contents

1. Introduction:...........................................................................................................................3

2. Findings:.................................................................................................................................3

2.1 Quantitative Analysis:..........................................................................................................3

2.2 Qualitative Analysis:............................................................................................................5

3. Recommendation and Justifications:......................................................................................6

4. Detailed comparison and Further Recommendations:...........................................................6

5. Conclusion:............................................................................................................................7

Reference and Bibliography:......................................................................................................9

Appendix:.................................................................................................................................11

2

Table of Contents

1. Introduction:...........................................................................................................................3

2. Findings:.................................................................................................................................3

2.1 Quantitative Analysis:..........................................................................................................3

2.2 Qualitative Analysis:............................................................................................................5

3. Recommendation and Justifications:......................................................................................6

4. Detailed comparison and Further Recommendations:...........................................................6

5. Conclusion:............................................................................................................................7

Reference and Bibliography:......................................................................................................9

Appendix:.................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS

3

1. Introduction:

The assessment aims in evaluating the two-product line that is aimed by ALLCURE

Inc. to produce in future, for increasing its revenue generation capability. The analysis is

based on Investment appraisal techniques, which is used for detecting the financial viability

of the proposed projects. In addition, adequate evaluation of the qualitative analysis has been

conducted in the assessment for identifying social viability in approving the project.

ALLCURE Inc. deals with medicines, which can have negative and positive impact on the

health of the consumer that directly raises the social concerns of the CFO, while making any

kind of investment decisions. The recommendations an adequate justification for the

recommendation is demanded by the CFO who intends to start one of the proposed projects

for ALLCURE Inc. Detailed comparison and justification for the proposed project has been

conducted for allowing the CFO to make adequate investment decisions based on both

quantitative and qualitative analysis.

2. Findings:

2.1 Quantitative Analysis:

The quantitative analysis evaluates the net present value, discounted payback period,

and internal rate of return of the two proposed project. From the evaluation, it could be

identified that T-REC project is acceptable, as it complies with the requirements of the firm.

According to the case study, the organization needs the minimum 5-year discounted payback

for the project to be accepted, as an adequate investment options. Moreover, the payback

period of P-REC is at 6.1 years, whereas T-REC payback period is 4.9 years. Therefore, in

accordance with the payback period criteria the T-REC project needs to be selected by the

organization. The investment appraisal techniques such as present value and internal rate of

3

1. Introduction:

The assessment aims in evaluating the two-product line that is aimed by ALLCURE

Inc. to produce in future, for increasing its revenue generation capability. The analysis is

based on Investment appraisal techniques, which is used for detecting the financial viability

of the proposed projects. In addition, adequate evaluation of the qualitative analysis has been

conducted in the assessment for identifying social viability in approving the project.

ALLCURE Inc. deals with medicines, which can have negative and positive impact on the

health of the consumer that directly raises the social concerns of the CFO, while making any

kind of investment decisions. The recommendations an adequate justification for the

recommendation is demanded by the CFO who intends to start one of the proposed projects

for ALLCURE Inc. Detailed comparison and justification for the proposed project has been

conducted for allowing the CFO to make adequate investment decisions based on both

quantitative and qualitative analysis.

2. Findings:

2.1 Quantitative Analysis:

The quantitative analysis evaluates the net present value, discounted payback period,

and internal rate of return of the two proposed project. From the evaluation, it could be

identified that T-REC project is acceptable, as it complies with the requirements of the firm.

According to the case study, the organization needs the minimum 5-year discounted payback

for the project to be accepted, as an adequate investment options. Moreover, the payback

period of P-REC is at 6.1 years, whereas T-REC payback period is 4.9 years. Therefore, in

accordance with the payback period criteria the T-REC project needs to be selected by the

organization. The investment appraisal techniques such as present value and internal rate of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

4

return are also evaluated in the calculation, which indicates alternative results. The internal

rate of return directly highlight that T-REC project is viable for the organization as it has a

value of 25.61% in comparison to 24.35% for P-REC. However, the net present value

evaluation of the project provides an alternative recommendation, as P-REC value is higher

than T-REC. As per the investment appraisal rules, the project with higher net present value

needs to be selected by the organization, as it evaluates the future cash flow by using time

value of money. The analysis of the project based on 18% discount rate, where project P-RE

C needs to be selected by the organization. Baum and Crosby (2014) stated that projects are

evaluated on the basis of NPV, as it allows the organization to detect the investment options,

which can increase firm value in the long run.

The analysis of the investment appraisal technique has been conducted with the

discount rate of 24% to identify the financial viability of the projects. After revaluating the

investment appraisal techniques such as net present value and discounted payback period

with a discount rate of 24%, the financial viability of the project the is detected. The cashew

conditions of the project will not be altered, as only the discounting rate has been changed

from 18 % to 24%. From the overall calculation, it is detected that Net present value of P-

REC has declined exponential, which has increased the financial viability of T-REC project.

In addition, the payback period calculated about the projects directly highlight that T-REC

project is much more viable for investment P-REC project. However, raising the discounting

rate will not allow the project comply with the discounted payback period terms of the

organization. Harris (2017) argued that without adequate research the investment appraisal

techniques could provide wrong information and data to the company.

The third quantitative measure that is conducted in the calculation in accommodating

research and development cost for P-REC. This mainly helps in detecting whether the

investment will provide adequate returns to the organization. After implementing research

4

return are also evaluated in the calculation, which indicates alternative results. The internal

rate of return directly highlight that T-REC project is viable for the organization as it has a

value of 25.61% in comparison to 24.35% for P-REC. However, the net present value

evaluation of the project provides an alternative recommendation, as P-REC value is higher

than T-REC. As per the investment appraisal rules, the project with higher net present value

needs to be selected by the organization, as it evaluates the future cash flow by using time

value of money. The analysis of the project based on 18% discount rate, where project P-RE

C needs to be selected by the organization. Baum and Crosby (2014) stated that projects are

evaluated on the basis of NPV, as it allows the organization to detect the investment options,

which can increase firm value in the long run.

The analysis of the investment appraisal technique has been conducted with the

discount rate of 24% to identify the financial viability of the projects. After revaluating the

investment appraisal techniques such as net present value and discounted payback period

with a discount rate of 24%, the financial viability of the project the is detected. The cashew

conditions of the project will not be altered, as only the discounting rate has been changed

from 18 % to 24%. From the overall calculation, it is detected that Net present value of P-

REC has declined exponential, which has increased the financial viability of T-REC project.

In addition, the payback period calculated about the projects directly highlight that T-REC

project is much more viable for investment P-REC project. However, raising the discounting

rate will not allow the project comply with the discounted payback period terms of the

organization. Harris (2017) argued that without adequate research the investment appraisal

techniques could provide wrong information and data to the company.

The third quantitative measure that is conducted in the calculation in accommodating

research and development cost for P-REC. This mainly helps in detecting whether the

investment will provide adequate returns to the organization. After implementing research

FINANCIAL ANALYSIS

5

and development cost, the net present value of the project P-REC is higher than T-REC.

Hence, under the circumstances, it could be understood that the financial capability of project

P-REC is considered viable in comparison to project T-REC. Therefore, from the valuation it

can be understood that the investment appraisal techniques highlight P-REC, as the most

viable investment options if NPV is considered. On the other and, T-REC projects in only

consider if the company emphases more on discounted payback period and internal rate of

return calculations. Throsby (2016) mentioned that investment appraisal techniques allow the

organization to evaluate the project under present value, which clears the investment

prospects for the organization.

2.2 Qualitative Analysis:

Qualitative analysis helps the CFO of ALLCURE Inc. to identify the socially

acceptable investment option, which does not have negative impact on the image of the

organization. The analysis is based on the image and social commitment ALLCURE Inc. for

using adequate investment option that does not affect the consumer’s health. The qualitative

analysis of P-REC indicates that the project is not adequate for commencement, as there is

huge controversy regarding the long-term health hazard that can have negative impact on

health of the consumers. Moreover, the P-REC drug is introduced as a revolutionary pre-

version of the actual medicine, where it has alternative flaws, which can negatively affect the

health conditions of the consumer. On the other hand, the analysis of T-REC drug indicates

that there is no harmful effect on the consumers as projector in the report. In addition, the T-

REC drug is considered to be less effective with the traditional treatment plan. This would

directly reduce the demand among potential customers, as its impacts are relatively low

(Vesty and Oliver 2014).

Hence, the qualitative analysis mentions about the ethical viability, while making

adequate investment decisions. Therefore, from evaluation it could be understood that

5

and development cost, the net present value of the project P-REC is higher than T-REC.

Hence, under the circumstances, it could be understood that the financial capability of project

P-REC is considered viable in comparison to project T-REC. Therefore, from the valuation it

can be understood that the investment appraisal techniques highlight P-REC, as the most

viable investment options if NPV is considered. On the other and, T-REC projects in only

consider if the company emphases more on discounted payback period and internal rate of

return calculations. Throsby (2016) mentioned that investment appraisal techniques allow the

organization to evaluate the project under present value, which clears the investment

prospects for the organization.

2.2 Qualitative Analysis:

Qualitative analysis helps the CFO of ALLCURE Inc. to identify the socially

acceptable investment option, which does not have negative impact on the image of the

organization. The analysis is based on the image and social commitment ALLCURE Inc. for

using adequate investment option that does not affect the consumer’s health. The qualitative

analysis of P-REC indicates that the project is not adequate for commencement, as there is

huge controversy regarding the long-term health hazard that can have negative impact on

health of the consumers. Moreover, the P-REC drug is introduced as a revolutionary pre-

version of the actual medicine, where it has alternative flaws, which can negatively affect the

health conditions of the consumer. On the other hand, the analysis of T-REC drug indicates

that there is no harmful effect on the consumers as projector in the report. In addition, the T-

REC drug is considered to be less effective with the traditional treatment plan. This would

directly reduce the demand among potential customers, as its impacts are relatively low

(Vesty and Oliver 2014).

Hence, the qualitative analysis mentions about the ethical viability, while making

adequate investment decisions. Therefore, from evaluation it could be understood that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS

6

Investments T-REC is considered to be viable, as it does not have negative impact on the

health of the customers. However, after collecting the report of P-REC after 8 years, the

company can adequately start the project on the basis of the publisher report. Research and

development information will allow the organization to improve the current performance of

P-REC drug and reduce its negative impact on the customer’s health (Hoesli and MacGregor

2014).

3. Recommendation and Justifications:

After evaluating the quantitative and qualitative analysis for both the projects, it could

be identified that investment in T-REC is much more profitable for the organization can

investing in P-REC. According to the quantitative method, the net present value of T-REC is

higher when the discounting rate increases to 24%. In addition, the analysis based on internal

rate of return and discounted payback Period of the organization directly highlights project T-

REC, as the most viable investment option. Moreover, the qualitative Analysis also highlight

that investment in T-REC is more socially acceptable, as it does not have any kind of side

effects to the consumer of the medicine. On the other hand, the P-REC medicine that has

proposed by the organization is still in research and development stage, where it has certain

harmful effects on consumer, which cannot be rectified or detected until now.

4. Detailed comparison and Further Recommendations:

Comparison between T-REC and P-REC

T-REC P-REC

Socially Acceptable as considered safe Socially Not Acceptable considered harmful

NPV is higher only under 24% discounting rate NPV is higher only under 18% discounting rate

6

Investments T-REC is considered to be viable, as it does not have negative impact on the

health of the customers. However, after collecting the report of P-REC after 8 years, the

company can adequately start the project on the basis of the publisher report. Research and

development information will allow the organization to improve the current performance of

P-REC drug and reduce its negative impact on the customer’s health (Hoesli and MacGregor

2014).

3. Recommendation and Justifications:

After evaluating the quantitative and qualitative analysis for both the projects, it could

be identified that investment in T-REC is much more profitable for the organization can

investing in P-REC. According to the quantitative method, the net present value of T-REC is

higher when the discounting rate increases to 24%. In addition, the analysis based on internal

rate of return and discounted payback Period of the organization directly highlights project T-

REC, as the most viable investment option. Moreover, the qualitative Analysis also highlight

that investment in T-REC is more socially acceptable, as it does not have any kind of side

effects to the consumer of the medicine. On the other hand, the P-REC medicine that has

proposed by the organization is still in research and development stage, where it has certain

harmful effects on consumer, which cannot be rectified or detected until now.

4. Detailed comparison and Further Recommendations:

Comparison between T-REC and P-REC

T-REC P-REC

Socially Acceptable as considered safe Socially Not Acceptable considered harmful

NPV is higher only under 24% discounting rate NPV is higher only under 18% discounting rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

7

Discounting payback period and Internal rate of

return is acceptable

Discounting payback period and Internal rate of

return is not acceptable

Research has been completed with adequate data Research has not been completed, where the results

will be declared after 8 years

The above detailed analysis or comparison of the project mainly states the Financial

and ethical viability of T-REC project on comparison to P-REC project. The further

evaluation of both projects directly highlight that investment can be conducted in T-REC as

well as P-REC. however, the Investment on both the project is to be conducted in different

timelines, as P-REC report will be generated after 8 years until that T-REC project will be

completed. Therefore, both the projects can be accommodated, which will generate adequate

income in the long run that can eventually help is improving the substantial growth condition

of the organization. Hence, it is recommended for the organization that Investments T-REC

can be conducted immediately, while P-REC project can be accommodated after the

completion of the R&D report.

5. Conclusion:

After evaluating both the investment options, it could be identified that Investments

T-REC is both financially and socially viable for the organization. Moreover, after validating

the calculations to can be detected that the increment in discounting rate from 18 % to 24%

directly indicate financial viability of T-REC project in comparison to P-REC project. The

adequate comparison between T-REC project and P-REC project has been conducted, which

highlights the financial viability of T-REC investment option. The net present value of P-

REC is only hire when the discounting rate is 18%, which reduces the financial viability of T-

REC. However, after evaluating all the relevant information regarding the qualitative and

7

Discounting payback period and Internal rate of

return is acceptable

Discounting payback period and Internal rate of

return is not acceptable

Research has been completed with adequate data Research has not been completed, where the results

will be declared after 8 years

The above detailed analysis or comparison of the project mainly states the Financial

and ethical viability of T-REC project on comparison to P-REC project. The further

evaluation of both projects directly highlight that investment can be conducted in T-REC as

well as P-REC. however, the Investment on both the project is to be conducted in different

timelines, as P-REC report will be generated after 8 years until that T-REC project will be

completed. Therefore, both the projects can be accommodated, which will generate adequate

income in the long run that can eventually help is improving the substantial growth condition

of the organization. Hence, it is recommended for the organization that Investments T-REC

can be conducted immediately, while P-REC project can be accommodated after the

completion of the R&D report.

5. Conclusion:

After evaluating both the investment options, it could be identified that Investments

T-REC is both financially and socially viable for the organization. Moreover, after validating

the calculations to can be detected that the increment in discounting rate from 18 % to 24%

directly indicate financial viability of T-REC project in comparison to P-REC project. The

adequate comparison between T-REC project and P-REC project has been conducted, which

highlights the financial viability of T-REC investment option. The net present value of P-

REC is only hire when the discounting rate is 18%, which reduces the financial viability of T-

REC. However, after evaluating all the relevant information regarding the qualitative and

FINANCIAL ANALYSIS

8

quantitative analysis, it can be detected that investment T-REC is highly beneficial for the

organization. Therefore, ALLCURE Inc. can start the project with T-REC and after getting

the report from R&D about P-REC, the next project can be started.

8

quantitative analysis, it can be detected that investment T-REC is highly beneficial for the

organization. Therefore, ALLCURE Inc. can start the project with T-REC and after getting

the report from R&D about P-REC, the next project can be started.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ANALYSIS

9

Reference and Bibliography:

Alkaraan, F., 2016. Strategic investment decision-making–Scanning and screening

investment opportunities: The expansion of Guinness in West Africa. Meditari Accountancy

Research, 24(4), pp.505-526.

Baddeley, M., 2017. Investment: Theories and Analyses. Macmillan International Higher

Education.

Baum, A.E. and Crosby, N., 2014. Property investment appraisal. John Wiley & Sons.

Chaysin, P., Daengdej, J. and Tangjitprom, N., 2016. Survey on Available Methods to

Evaluate IT Investment. Electronic Journal Information Systems Evaluation Volume, 19(1).

Elmassri, M.M., Harris, E.P. and Carter, D.B., 2016. Accounting for strategic investment

decision-making under extreme uncertainty. The British Accounting Review, 48(2), pp.151-

168.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Hoesli, M. and MacGregor, B.D., 2014. Property investment: principles and practice of

portfolio management. Routledge.

Jorge-Calderón, D., 2016. Aviation investment: Economic appraisal for airports, air traffic

management, airlines and aeronautics. Routledge.

Kafuku, J.M., Saman, M.Z.M., Sharif, S. and Zakuan, N., 2015. Investment decision issues

from remanufacturing system perspective: literature review and further research. Procedia

CIRP, 26, pp.589-594.

9

Reference and Bibliography:

Alkaraan, F., 2016. Strategic investment decision-making–Scanning and screening

investment opportunities: The expansion of Guinness in West Africa. Meditari Accountancy

Research, 24(4), pp.505-526.

Baddeley, M., 2017. Investment: Theories and Analyses. Macmillan International Higher

Education.

Baum, A.E. and Crosby, N., 2014. Property investment appraisal. John Wiley & Sons.

Chaysin, P., Daengdej, J. and Tangjitprom, N., 2016. Survey on Available Methods to

Evaluate IT Investment. Electronic Journal Information Systems Evaluation Volume, 19(1).

Elmassri, M.M., Harris, E.P. and Carter, D.B., 2016. Accounting for strategic investment

decision-making under extreme uncertainty. The British Accounting Review, 48(2), pp.151-

168.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Hoesli, M. and MacGregor, B.D., 2014. Property investment: principles and practice of

portfolio management. Routledge.

Jorge-Calderón, D., 2016. Aviation investment: Economic appraisal for airports, air traffic

management, airlines and aeronautics. Routledge.

Kafuku, J.M., Saman, M.Z.M., Sharif, S. and Zakuan, N., 2015. Investment decision issues

from remanufacturing system perspective: literature review and further research. Procedia

CIRP, 26, pp.589-594.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ANALYSIS

10

Locatelli, G., Invernizzi, D.C. and Mancini, M., 2016. Investment and risk appraisal in

energy storage systems: A real options approach. Energy, 104, pp.114-131.

Throsby, D., 2016. Investment in urban heritage conservation in developing countries:

Concepts, methods and data. City, Culture and Society, 7(2), pp.81-86.

Vesty, G. and Oliver, J., 2014. Corporate strategy and accounting for sustainability in

investment appraisal. Corporate Ownership and Control, 11(2D), pp.377-388.

10

Locatelli, G., Invernizzi, D.C. and Mancini, M., 2016. Investment and risk appraisal in

energy storage systems: A real options approach. Energy, 104, pp.114-131.

Throsby, D., 2016. Investment in urban heritage conservation in developing countries:

Concepts, methods and data. City, Culture and Society, 7(2), pp.81-86.

Vesty, G. and Oliver, J., 2014. Corporate strategy and accounting for sustainability in

investment appraisal. Corporate Ownership and Control, 11(2D), pp.377-388.

FINANCIAL ANALYSIS

11

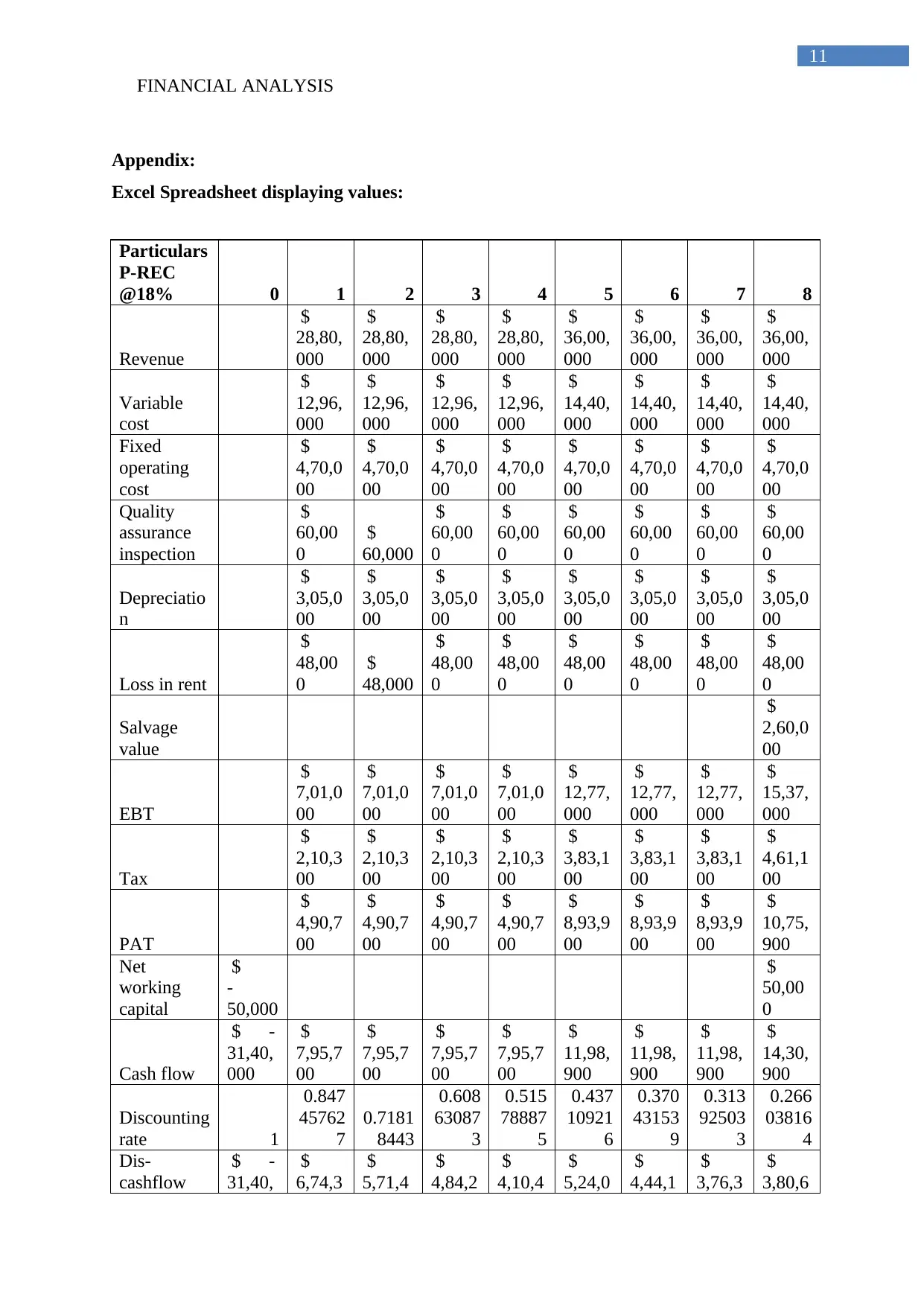

Appendix:

Excel Spreadsheet displaying values:

Particulars

P-REC

@18% 0 1 2 3 4 5 6 7 8

Revenue

$

28,80,

000

$

28,80,

000

$

28,80,

000

$

28,80,

000

$

36,00,

000

$

36,00,

000

$

36,00,

000

$

36,00,

000

Variable

cost

$

12,96,

000

$

12,96,

000

$

12,96,

000

$

12,96,

000

$

14,40,

000

$

14,40,

000

$

14,40,

000

$

14,40,

000

Fixed

operating

cost

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

Quality

assurance

inspection

$

60,00

0

$

60,000

$

60,00

0

$

60,00

0

$

60,00

0

$

60,00

0

$

60,00

0

$

60,00

0

Depreciatio

n

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

Loss in rent

$

48,00

0

$

48,000

$

48,00

0

$

48,00

0

$

48,00

0

$

48,00

0

$

48,00

0

$

48,00

0

Salvage

value

$

2,60,0

00

EBT

$

7,01,0

00

$

7,01,0

00

$

7,01,0

00

$

7,01,0

00

$

12,77,

000

$

12,77,

000

$

12,77,

000

$

15,37,

000

Tax

$

2,10,3

00

$

2,10,3

00

$

2,10,3

00

$

2,10,3

00

$

3,83,1

00

$

3,83,1

00

$

3,83,1

00

$

4,61,1

00

PAT

$

4,90,7

00

$

4,90,7

00

$

4,90,7

00

$

4,90,7

00

$

8,93,9

00

$

8,93,9

00

$

8,93,9

00

$

10,75,

900

Net

working

capital

$

-

50,000

$

50,00

0

Cash flow

$ -

31,40,

000

$

7,95,7

00

$

7,95,7

00

$

7,95,7

00

$

7,95,7

00

$

11,98,

900

$

11,98,

900

$

11,98,

900

$

14,30,

900

Discounting

rate 1

0.847

45762

7

0.7181

8443

0.608

63087

3

0.515

78887

5

0.437

10921

6

0.370

43153

9

0.313

92503

3

0.266

03816

4

Dis-

cashflow

$ -

31,40,

$

6,74,3

$

5,71,4

$

4,84,2

$

4,10,4

$

5,24,0

$

4,44,1

$

3,76,3

$

3,80,6

11

Appendix:

Excel Spreadsheet displaying values:

Particulars

P-REC

@18% 0 1 2 3 4 5 6 7 8

Revenue

$

28,80,

000

$

28,80,

000

$

28,80,

000

$

28,80,

000

$

36,00,

000

$

36,00,

000

$

36,00,

000

$

36,00,

000

Variable

cost

$

12,96,

000

$

12,96,

000

$

12,96,

000

$

12,96,

000

$

14,40,

000

$

14,40,

000

$

14,40,

000

$

14,40,

000

Fixed

operating

cost

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

$

4,70,0

00

Quality

assurance

inspection

$

60,00

0

$

60,000

$

60,00

0

$

60,00

0

$

60,00

0

$

60,00

0

$

60,00

0

$

60,00

0

Depreciatio

n

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

$

3,05,0

00

Loss in rent

$

48,00

0

$

48,000

$

48,00

0

$

48,00

0

$

48,00

0

$

48,00

0

$

48,00

0

$

48,00

0

Salvage

value

$

2,60,0

00

EBT

$

7,01,0

00

$

7,01,0

00

$

7,01,0

00

$

7,01,0

00

$

12,77,

000

$

12,77,

000

$

12,77,

000

$

15,37,

000

Tax

$

2,10,3

00

$

2,10,3

00

$

2,10,3

00

$

2,10,3

00

$

3,83,1

00

$

3,83,1

00

$

3,83,1

00

$

4,61,1

00

PAT

$

4,90,7

00

$

4,90,7

00

$

4,90,7

00

$

4,90,7

00

$

8,93,9

00

$

8,93,9

00

$

8,93,9

00

$

10,75,

900

Net

working

capital

$

-

50,000

$

50,00

0

Cash flow

$ -

31,40,

000

$

7,95,7

00

$

7,95,7

00

$

7,95,7

00

$

7,95,7

00

$

11,98,

900

$

11,98,

900

$

11,98,

900

$

14,30,

900

Discounting

rate 1

0.847

45762

7

0.7181

8443

0.608

63087

3

0.515

78887

5

0.437

10921

6

0.370

43153

9

0.313

92503

3

0.266

03816

4

Dis-

cashflow

$ -

31,40,

$

6,74,3

$

5,71,4

$

4,84,2

$

4,10,4

$

5,24,0

$

4,44,1

$

3,76,3

$

3,80,6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.