FIN30016 Management of Investment Portfolios Assignment 2, 2019

VerifiedAdded on 2022/10/03

|10

|1730

|355

Report

AI Summary

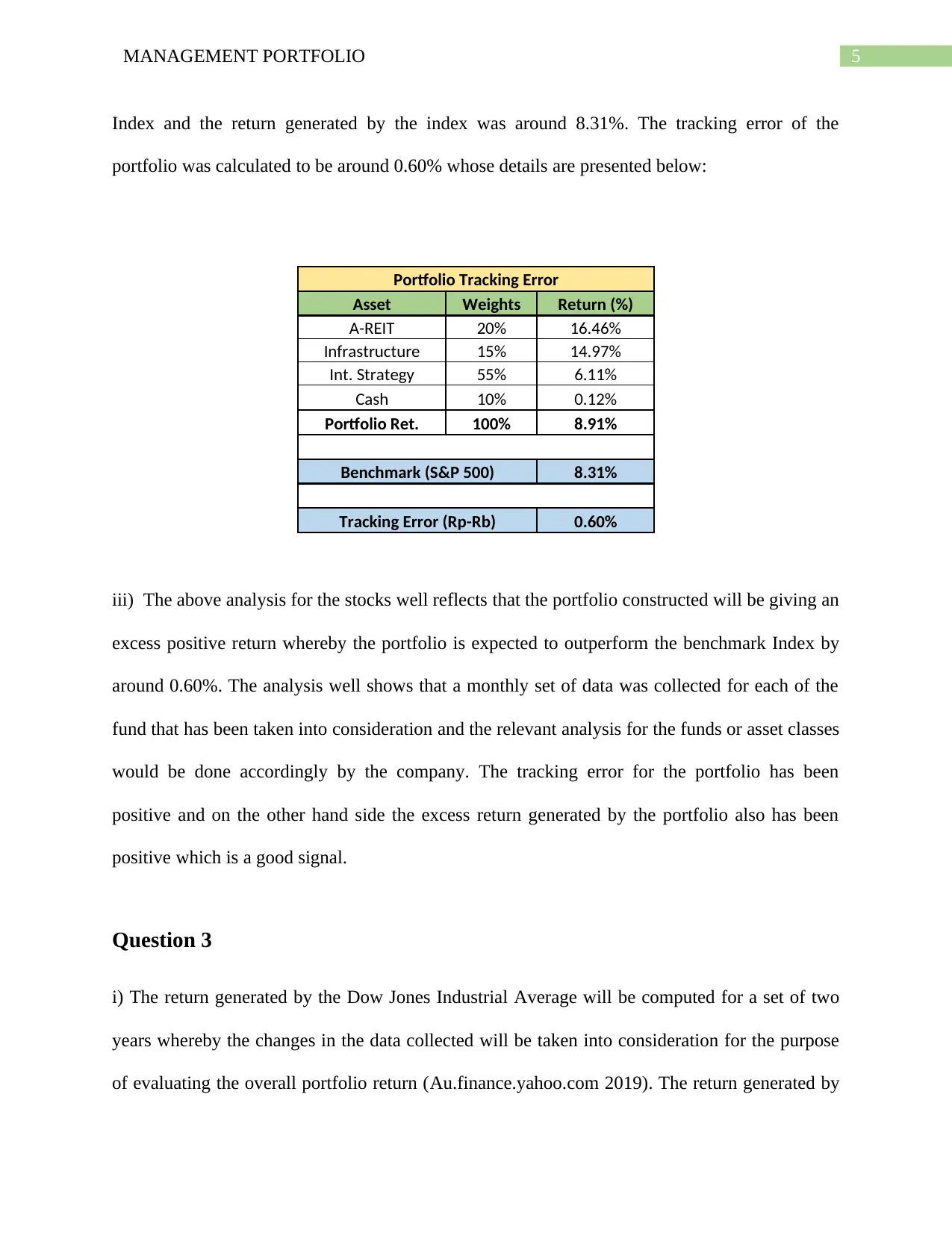

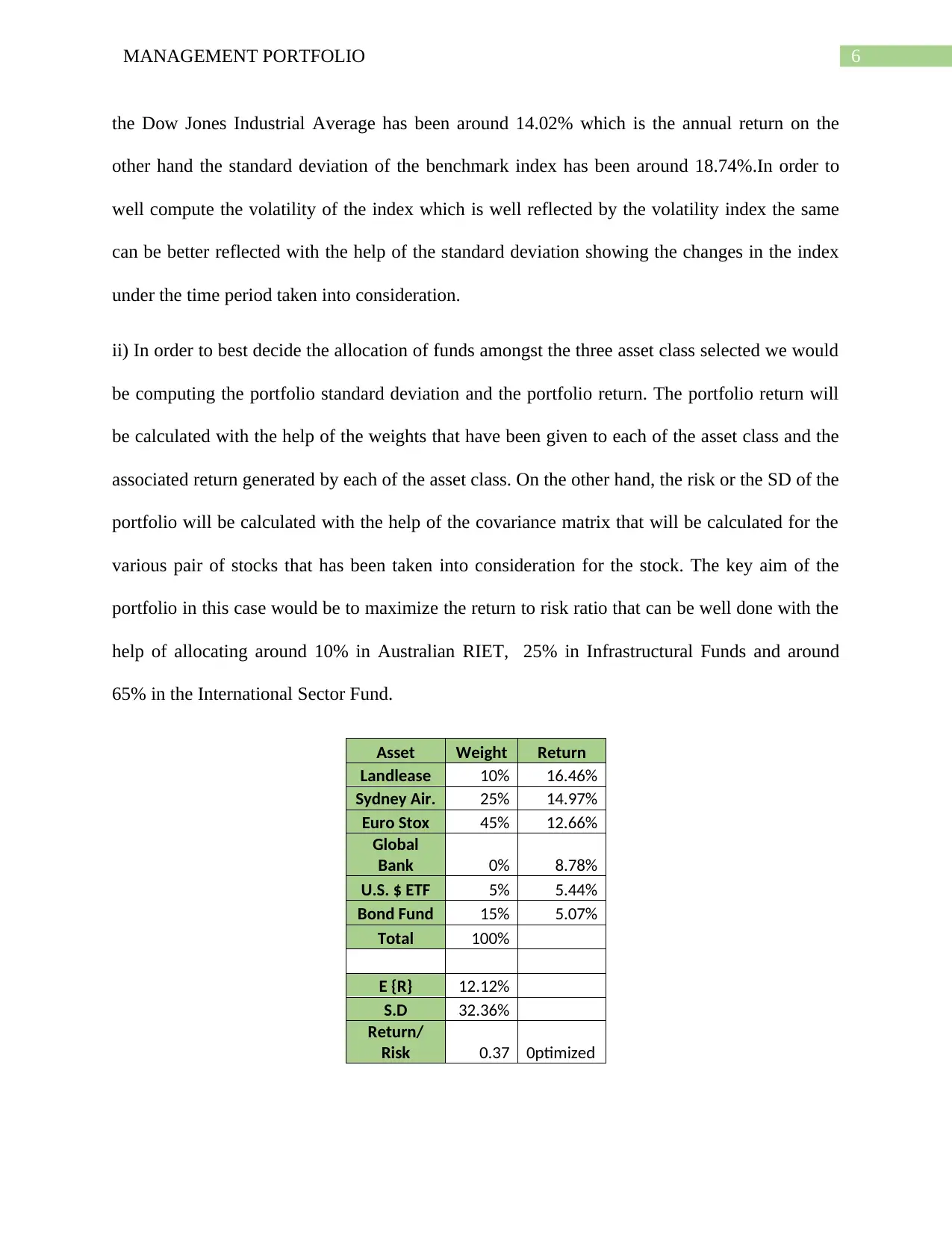

This assignment solution focuses on the management of investment portfolios, specifically addressing the selection and analysis of Exchange Traded Funds (ETFs) from the Australian Securities Exchange (ASX). It includes an analysis of Sydney Airport as an Infrastructure Fund, highlighting its revenue contributions from Aeronautical Services and Retail Business. The solution also covers the selection of International ETFs, including ETFS EURO STOXX 50 ETF, Beta Shares Global Bank ETF, Beta shares U.S. Dollar ETF, and SPDR S&P/ASX Australian Bond Fund, discussing factors influencing their performance. Furthermore, the assignment calculates excess return and tracking error for a given portfolio, comparing it against the S&P 200 Index. Finally, it computes the return and standard deviation of the Dow Jones Industrial Average and determines optimal asset allocation across different asset classes to maximize the return-to-risk ratio. The document concludes with a reference list.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.