FIN320 Tax and Estate Planning: Analyzing Herbert & Dorothy's Finances

VerifiedAdded on 2023/06/07

|16

|4438

|114

Report

AI Summary

This report analyzes the financial situation of Herbert and Dorothy Evans, focusing on tax and estate planning strategies. The initial section details the current individual tax scenario for Australian residents, including tax rates, Medicare Levy Surcharge, and available tax offsets like LITO and LMITO. The report then proposes a shift from sole trader businesses to a partnership, highlighting the advantages and disadvantages, and presenting a comparative analysis of tax liabilities. Finally, it suggests future investment plans, particularly the establishment of a Self-Managed Superannuation Fund (SMSF) to manage estate planning, rental property investments, stocks, insurance, and debt reduction, outlining the benefits and flexibility of SMSFs, including tax advantages and wealth transfer.

Page1

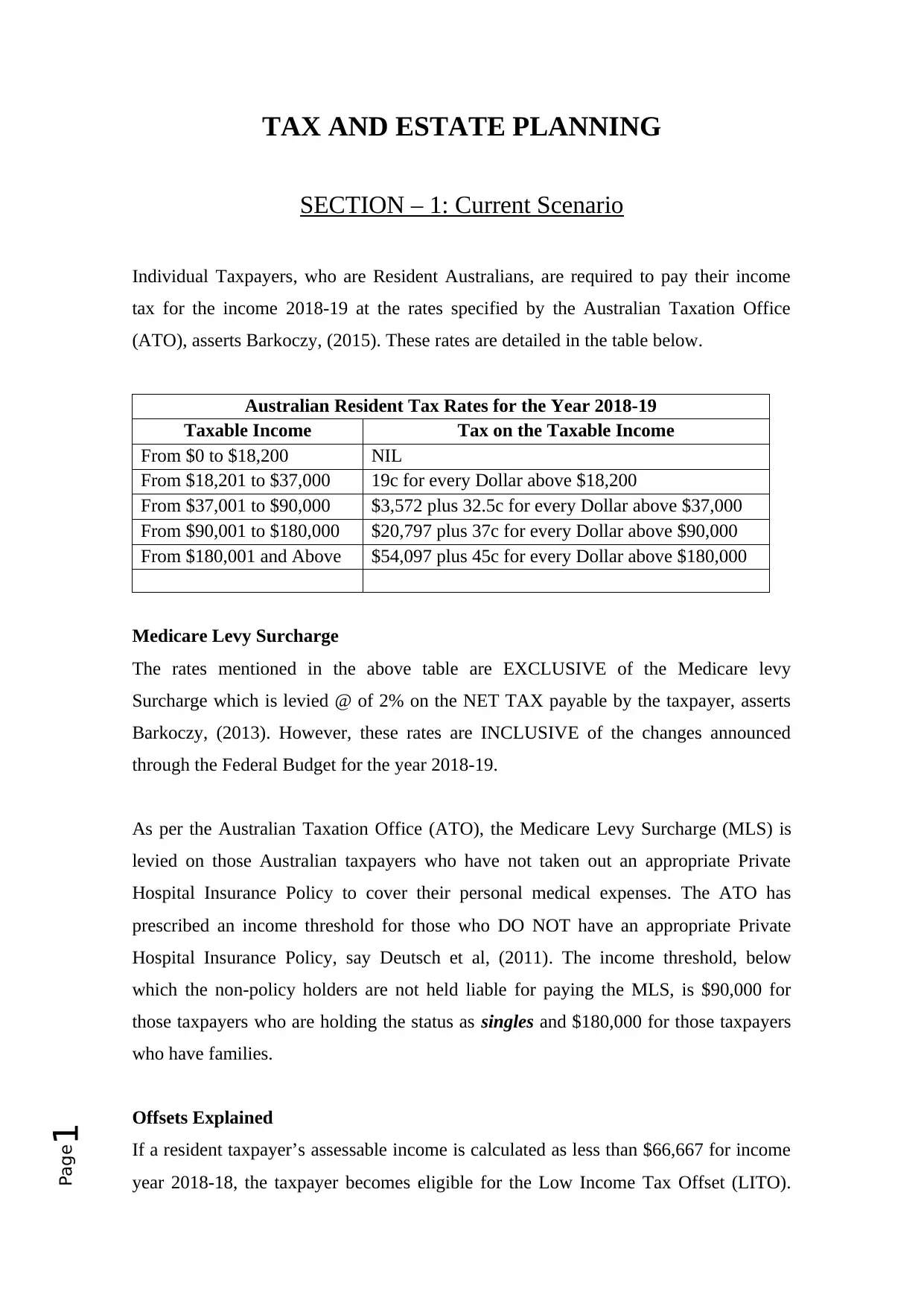

TAX AND ESTATE PLANNING

SECTION – 1: Current Scenario

Individual Taxpayers, who are Resident Australians, are required to pay their income

tax for the income 2018-19 at the rates specified by the Australian Taxation Office

(ATO), asserts Barkoczy, (2015). These rates are detailed in the table below.

Australian Resident Tax Rates for the Year 2018-19

Taxable Income Tax on the Taxable Income

From $0 to $18,200 NIL

From $18,201 to $37,000 19c for every Dollar above $18,200

From $37,001 to $90,000 $3,572 plus 32.5c for every Dollar above $37,000

From $90,001 to $180,000 $20,797 plus 37c for every Dollar above $90,000

From $180,001 and Above $54,097 plus 45c for every Dollar above $180,000

Medicare Levy Surcharge

The rates mentioned in the above table are EXCLUSIVE of the Medicare levy

Surcharge which is levied @ of 2% on the NET TAX payable by the taxpayer, asserts

Barkoczy, (2013). However, these rates are INCLUSIVE of the changes announced

through the Federal Budget for the year 2018-19.

As per the Australian Taxation Office (ATO), the Medicare Levy Surcharge (MLS) is

levied on those Australian taxpayers who have not taken out an appropriate Private

Hospital Insurance Policy to cover their personal medical expenses. The ATO has

prescribed an income threshold for those who DO NOT have an appropriate Private

Hospital Insurance Policy, say Deutsch et al, (2011). The income threshold, below

which the non-policy holders are not held liable for paying the MLS, is $90,000 for

those taxpayers who are holding the status as singles and $180,000 for those taxpayers

who have families.

Offsets Explained

If a resident taxpayer’s assessable income is calculated as less than $66,667 for income

year 2018-18, the taxpayer becomes eligible for the Low Income Tax Offset (LITO).

TAX AND ESTATE PLANNING

SECTION – 1: Current Scenario

Individual Taxpayers, who are Resident Australians, are required to pay their income

tax for the income 2018-19 at the rates specified by the Australian Taxation Office

(ATO), asserts Barkoczy, (2015). These rates are detailed in the table below.

Australian Resident Tax Rates for the Year 2018-19

Taxable Income Tax on the Taxable Income

From $0 to $18,200 NIL

From $18,201 to $37,000 19c for every Dollar above $18,200

From $37,001 to $90,000 $3,572 plus 32.5c for every Dollar above $37,000

From $90,001 to $180,000 $20,797 plus 37c for every Dollar above $90,000

From $180,001 and Above $54,097 plus 45c for every Dollar above $180,000

Medicare Levy Surcharge

The rates mentioned in the above table are EXCLUSIVE of the Medicare levy

Surcharge which is levied @ of 2% on the NET TAX payable by the taxpayer, asserts

Barkoczy, (2013). However, these rates are INCLUSIVE of the changes announced

through the Federal Budget for the year 2018-19.

As per the Australian Taxation Office (ATO), the Medicare Levy Surcharge (MLS) is

levied on those Australian taxpayers who have not taken out an appropriate Private

Hospital Insurance Policy to cover their personal medical expenses. The ATO has

prescribed an income threshold for those who DO NOT have an appropriate Private

Hospital Insurance Policy, say Deutsch et al, (2011). The income threshold, below

which the non-policy holders are not held liable for paying the MLS, is $90,000 for

those taxpayers who are holding the status as singles and $180,000 for those taxpayers

who have families.

Offsets Explained

If a resident taxpayer’s assessable income is calculated as less than $66,667 for income

year 2018-18, the taxpayer becomes eligible for the Low Income Tax Offset (LITO).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page2

However, the maximum tax offset which the resident taxpayer can avail is restricted to

$445, and is applicable to taxpayer’s whose taxable income is below $37,000. Another

provision of the ATO restricts the limitation by reducing the threshold by 1.5 cents for

each dollar over taxable income of $37,000, as per CCH, (2015).

Prior to the income year 2018-19, the Low Income Tax Offset (LITO) was the

only tax rebate available for the Australian resident individual taxpayers who were

having low income. In the Federal budget presented by the government for the year

2018-19, a proposal has been forwarded that in addition to the basic tax-free threshold

of $18,200, the applicable amount of LMITO (Low and Middle Income Tax Offset),

which was fixed at $445, will be made applicable to all Australian resident individuals

whose taxable income reaches $125,333.

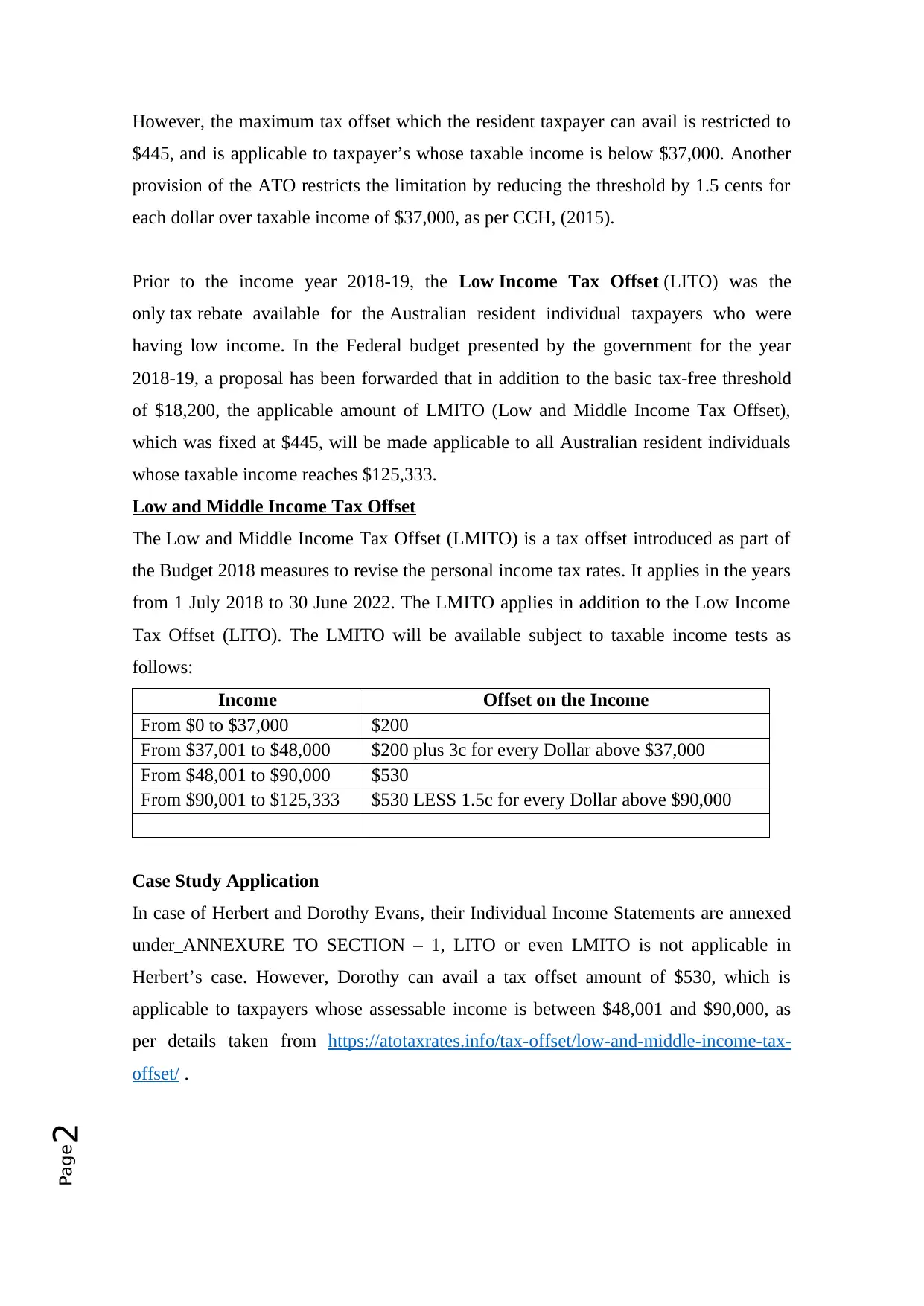

Low and Middle Income Tax Offset

The Low and Middle Income Tax Offset (LMITO) is a tax offset introduced as part of

the Budget 2018 measures to revise the personal income tax rates. It applies in the years

from 1 July 2018 to 30 June 2022. The LMITO applies in addition to the Low Income

Tax Offset (LITO). The LMITO will be available subject to taxable income tests as

follows:

Income Offset on the Income

From $0 to $37,000 $200

From $37,001 to $48,000 $200 plus 3c for every Dollar above $37,000

From $48,001 to $90,000 $530

From $90,001 to $125,333 $530 LESS 1.5c for every Dollar above $90,000

Case Study Application

In case of Herbert and Dorothy Evans, their Individual Income Statements are annexed

under ANNEXURE TO SECTION – 1, LITO or even LMITO is not applicable in

Herbert’s case. However, Dorothy can avail a tax offset amount of $530, which is

applicable to taxpayers whose assessable income is between $48,001 and $90,000, as

per details taken from https://atotaxrates.info/tax-offset/low-and-middle-income-tax-

offset/ .

However, the maximum tax offset which the resident taxpayer can avail is restricted to

$445, and is applicable to taxpayer’s whose taxable income is below $37,000. Another

provision of the ATO restricts the limitation by reducing the threshold by 1.5 cents for

each dollar over taxable income of $37,000, as per CCH, (2015).

Prior to the income year 2018-19, the Low Income Tax Offset (LITO) was the

only tax rebate available for the Australian resident individual taxpayers who were

having low income. In the Federal budget presented by the government for the year

2018-19, a proposal has been forwarded that in addition to the basic tax-free threshold

of $18,200, the applicable amount of LMITO (Low and Middle Income Tax Offset),

which was fixed at $445, will be made applicable to all Australian resident individuals

whose taxable income reaches $125,333.

Low and Middle Income Tax Offset

The Low and Middle Income Tax Offset (LMITO) is a tax offset introduced as part of

the Budget 2018 measures to revise the personal income tax rates. It applies in the years

from 1 July 2018 to 30 June 2022. The LMITO applies in addition to the Low Income

Tax Offset (LITO). The LMITO will be available subject to taxable income tests as

follows:

Income Offset on the Income

From $0 to $37,000 $200

From $37,001 to $48,000 $200 plus 3c for every Dollar above $37,000

From $48,001 to $90,000 $530

From $90,001 to $125,333 $530 LESS 1.5c for every Dollar above $90,000

Case Study Application

In case of Herbert and Dorothy Evans, their Individual Income Statements are annexed

under ANNEXURE TO SECTION – 1, LITO or even LMITO is not applicable in

Herbert’s case. However, Dorothy can avail a tax offset amount of $530, which is

applicable to taxpayers whose assessable income is between $48,001 and $90,000, as

per details taken from https://atotaxrates.info/tax-offset/low-and-middle-income-tax-

offset/ .

Page3

SECTION – 2: Proposal for Partnership

If Herbert and Dorothy were to convert their existing businesses from sole trader to a

partnership, they will first have to apply for a Business Name, Australian Business

Number (ABN) and then for tax registrations. A partnership is different from a sole

trader, in a partnership the couple will be business partners and will be personally

liable for debts of the partnership business, although they will share, in equal

proportions, the control and management of the partnership business, as per Nethercott,

Devos & Richardson, (2010). The couple will distribute the income or losses from the

partnership business among themselves in equal proportions. In comparison to other

type of entities, a partnership is inexpensive in setting up and operating. Although

partners unknown to each other may go for a written partnership agreement, in case of

Herbert and Dorothy this is not essential, as a verbal understanding is equally binding,

says Renton, (2012).

As partners, Herbert and Dorothy will have to manage their superannuation

arrangements as individuals. However, as partners, they can withdraw the contribution

for their super contribution, although the partnership firm will have to pay

superannuation, at the required terms, to its employees. As partners, assert Smith &

Koken, (2011), the Fixed Monthly Drawings which the couple will draw from the

partnership business cannot be claimed as deductible expenses for taxation purposes as

the amounts which the partners withdraw from the partnership are not considered as

wages for taxation purposes. For Taxation purposes, Herbert and Dorothy will not be

considered as employees, but they can employ workers, as per Ault, Arnold & Gest,

(2010).

Key features

Below are cited the important features of a partnership business to be followed by

Herbert and Dorothy in case they decide to merge their individual Sole Trader

businesses into a Partnership Firm –

Partnership firm must apply for an ABN which is to be used for all business

deals.

Partnership is required to register for GST in case the annual GST turnover of

the partnership business is above $75,000.

SECTION – 2: Proposal for Partnership

If Herbert and Dorothy were to convert their existing businesses from sole trader to a

partnership, they will first have to apply for a Business Name, Australian Business

Number (ABN) and then for tax registrations. A partnership is different from a sole

trader, in a partnership the couple will be business partners and will be personally

liable for debts of the partnership business, although they will share, in equal

proportions, the control and management of the partnership business, as per Nethercott,

Devos & Richardson, (2010). The couple will distribute the income or losses from the

partnership business among themselves in equal proportions. In comparison to other

type of entities, a partnership is inexpensive in setting up and operating. Although

partners unknown to each other may go for a written partnership agreement, in case of

Herbert and Dorothy this is not essential, as a verbal understanding is equally binding,

says Renton, (2012).

As partners, Herbert and Dorothy will have to manage their superannuation

arrangements as individuals. However, as partners, they can withdraw the contribution

for their super contribution, although the partnership firm will have to pay

superannuation, at the required terms, to its employees. As partners, assert Smith &

Koken, (2011), the Fixed Monthly Drawings which the couple will draw from the

partnership business cannot be claimed as deductible expenses for taxation purposes as

the amounts which the partners withdraw from the partnership are not considered as

wages for taxation purposes. For Taxation purposes, Herbert and Dorothy will not be

considered as employees, but they can employ workers, as per Ault, Arnold & Gest,

(2010).

Key features

Below are cited the important features of a partnership business to be followed by

Herbert and Dorothy in case they decide to merge their individual Sole Trader

businesses into a Partnership Firm –

Partnership firm must apply for an ABN which is to be used for all business

deals.

Partnership is required to register for GST in case the annual GST turnover of

the partnership business is above $75,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page4

All income, losses including control of the business will be shared in the agreed

proportions among the couple.

The partnership firm will have its own TFN and will be required to file its

separate partnership return annually, which will include all the income and

deductions of the partnership firm.

The partnership firm is not to pay income tax on its profits. The partners are

required to report the share earned from the partnership firm as income in their

individual tax returns.

Each partner is liable for paying tax on their earned share from the partnership

firm at tax rates applicable for individuals and if applicable, can also avail the

small business tax offset.

The only disadvantage of a partnership firm is that the partners have unlimited liability

for the debts of their partnership business and each partner is 'jointly and severally'

liable for these debts, as detailed by Nethercott, Devos & Richardson, (2010).

Case Study Application

On the basis of the above mentioned details, Herbert and Dorothy can take best

advantage of the taxation laws if they plan to merge their businesses into a single entity

based on the features of Partnership. This will give them a broader and flexible platform

for managing their tax liabilities. This can be seen from the comparative analysis given

below –

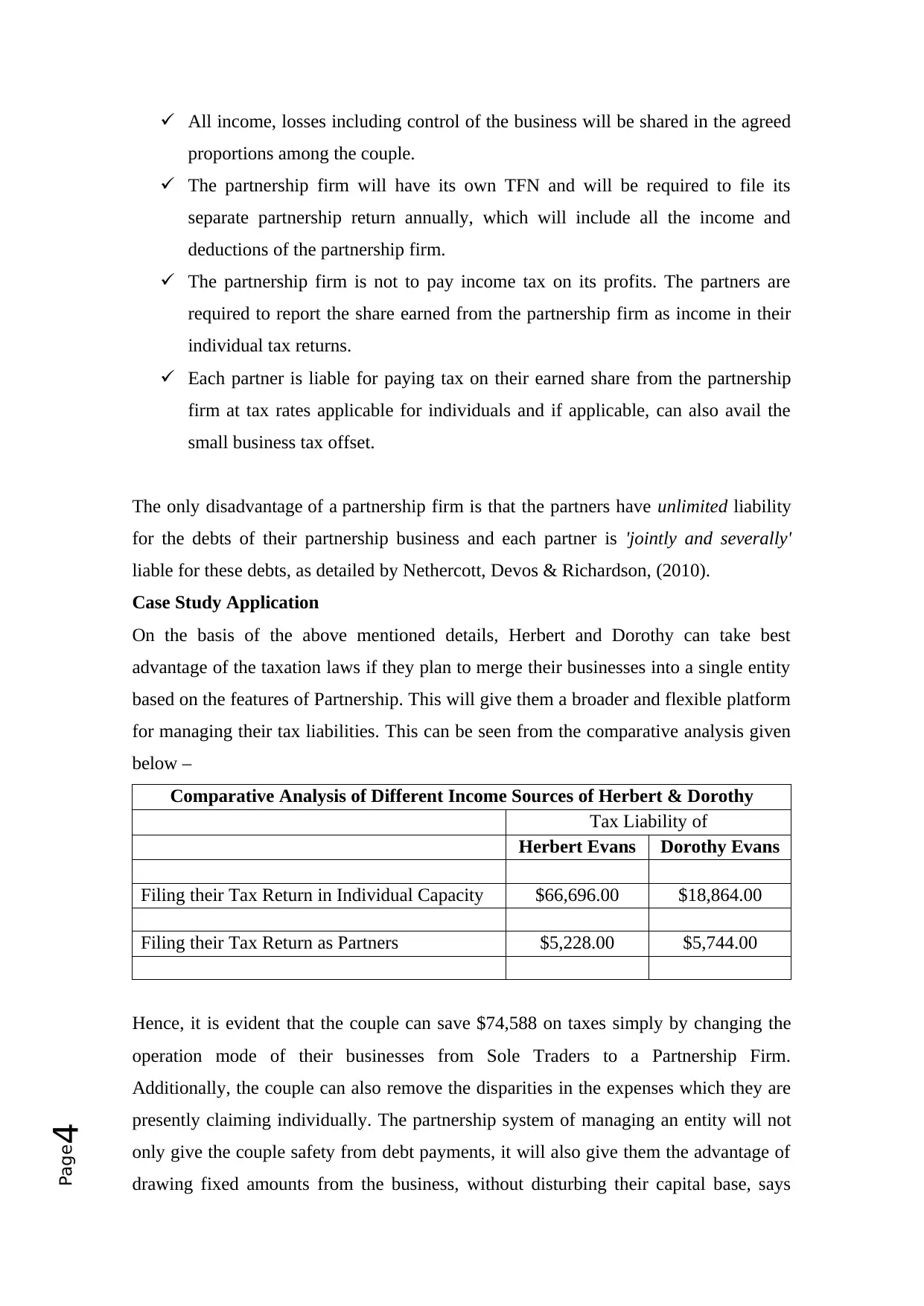

Comparative Analysis of Different Income Sources of Herbert & Dorothy

Tax Liability of

Herbert Evans Dorothy Evans

Filing their Tax Return in Individual Capacity $66,696.00 $18,864.00

Filing their Tax Return as Partners $5,228.00 $5,744.00

Hence, it is evident that the couple can save $74,588 on taxes simply by changing the

operation mode of their businesses from Sole Traders to a Partnership Firm.

Additionally, the couple can also remove the disparities in the expenses which they are

presently claiming individually. The partnership system of managing an entity will not

only give the couple safety from debt payments, it will also give them the advantage of

drawing fixed amounts from the business, without disturbing their capital base, says

All income, losses including control of the business will be shared in the agreed

proportions among the couple.

The partnership firm will have its own TFN and will be required to file its

separate partnership return annually, which will include all the income and

deductions of the partnership firm.

The partnership firm is not to pay income tax on its profits. The partners are

required to report the share earned from the partnership firm as income in their

individual tax returns.

Each partner is liable for paying tax on their earned share from the partnership

firm at tax rates applicable for individuals and if applicable, can also avail the

small business tax offset.

The only disadvantage of a partnership firm is that the partners have unlimited liability

for the debts of their partnership business and each partner is 'jointly and severally'

liable for these debts, as detailed by Nethercott, Devos & Richardson, (2010).

Case Study Application

On the basis of the above mentioned details, Herbert and Dorothy can take best

advantage of the taxation laws if they plan to merge their businesses into a single entity

based on the features of Partnership. This will give them a broader and flexible platform

for managing their tax liabilities. This can be seen from the comparative analysis given

below –

Comparative Analysis of Different Income Sources of Herbert & Dorothy

Tax Liability of

Herbert Evans Dorothy Evans

Filing their Tax Return in Individual Capacity $66,696.00 $18,864.00

Filing their Tax Return as Partners $5,228.00 $5,744.00

Hence, it is evident that the couple can save $74,588 on taxes simply by changing the

operation mode of their businesses from Sole Traders to a Partnership Firm.

Additionally, the couple can also remove the disparities in the expenses which they are

presently claiming individually. The partnership system of managing an entity will not

only give the couple safety from debt payments, it will also give them the advantage of

drawing fixed amounts from the business, without disturbing their capital base, says

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page5

CCH, (2015). An analysis of comparing their tax liabilities as individuals to their tax

liability if they form a partnership entity is annexed under ANNEXURE TO SECTION

– 2.

SECTION – 3: Future Plans

To facilitate smooth and efficient operations of their profitable business ventures, the

following avenues of channelizing their investments are proposed for Herbert and

Dorothy Evans. Some of the sectors, as per Deutsch et al, (2011), in which the couple

needs advise are –

1) Estate Planning

2) Investments in Rental Properties and Stocks

3) Insurance Planning and Debt Reduction

In the opinion of this paper, all these sectors can be taken care by Herbert and Dorothy

through the establishment of a Self-Managed Superannuation Fund (SMSF). This is the

foremost avenue to be adopted by Herbert and Dorothy for their surplus cash as well as

surplus profit from business activities. This will also give the couple an added

advantage of secure holding of their assets, be it the rental properties or stocks, assert

Ault, Arnold & Gest, (2010). The process, working and benefits of a SMSF have been

detailed below for the preview of the couple.

(A) Establishing a SMSF

Establishing a SMSF is done with the sole purpose to provide financial benefits to

members, especially after they retire and after their death to their dependents, as per

Deutsch et al, (2011). A SMSF is required to have its own Tax File Number (TFN), an

Australian Business Number (ABN) and a bank account for carrying out business

transactions. Since a SMSF functions as a trust and since minimum two trustees are

required, Herbert and Dorothy can easily start a SMSF, according to Barkoczy, (2013).

(B) Investment Choice

A SMSF will offer the couple the perfect opportunity for planning their investments

through a wide range of fixed assets, including investments in Real Estate, Stocks,

Other Immovable Assets and even Collectibles. Moreover, as per Nethercott, Devos &

Richardson, (2010), a SMSF can be used by Herbert and Dorothy for making

investments in most other investment products, including other SMSFs and assets,

whether these are located inside Australia or are located overseas, whether they held by

CCH, (2015). An analysis of comparing their tax liabilities as individuals to their tax

liability if they form a partnership entity is annexed under ANNEXURE TO SECTION

– 2.

SECTION – 3: Future Plans

To facilitate smooth and efficient operations of their profitable business ventures, the

following avenues of channelizing their investments are proposed for Herbert and

Dorothy Evans. Some of the sectors, as per Deutsch et al, (2011), in which the couple

needs advise are –

1) Estate Planning

2) Investments in Rental Properties and Stocks

3) Insurance Planning and Debt Reduction

In the opinion of this paper, all these sectors can be taken care by Herbert and Dorothy

through the establishment of a Self-Managed Superannuation Fund (SMSF). This is the

foremost avenue to be adopted by Herbert and Dorothy for their surplus cash as well as

surplus profit from business activities. This will also give the couple an added

advantage of secure holding of their assets, be it the rental properties or stocks, assert

Ault, Arnold & Gest, (2010). The process, working and benefits of a SMSF have been

detailed below for the preview of the couple.

(A) Establishing a SMSF

Establishing a SMSF is done with the sole purpose to provide financial benefits to

members, especially after they retire and after their death to their dependents, as per

Deutsch et al, (2011). A SMSF is required to have its own Tax File Number (TFN), an

Australian Business Number (ABN) and a bank account for carrying out business

transactions. Since a SMSF functions as a trust and since minimum two trustees are

required, Herbert and Dorothy can easily start a SMSF, according to Barkoczy, (2013).

(B) Investment Choice

A SMSF will offer the couple the perfect opportunity for planning their investments

through a wide range of fixed assets, including investments in Real Estate, Stocks,

Other Immovable Assets and even Collectibles. Moreover, as per Nethercott, Devos &

Richardson, (2010), a SMSF can be used by Herbert and Dorothy for making

investments in most other investment products, including other SMSFs and assets,

whether these are located inside Australia or are located overseas, whether they held by

Page6

listed or unlisted property trusts, including their derivative products such as Dividend

Warrants and Options, as detailed by Marsden, (2010).

(C) Tax Benefits

Herbert and Dorothy will be able to take advantage of the following benefits which are

provided exclusively to the SMSFs by the Australian Taxation Office (ATO). In the

Accumulation Phase of the SMSF, Herbert and Dorothy will be able to–

gain tax benefits for their Concessional Contributions which are taxed at a flat

rate of 15% in a SMSF;

get benefit of Government Co-contribution for all their qualifying contributions;

get investment earning which are taxed at maximum rate of 15% in SMSF;

pay Capital Gains Tax @10% on assets held for above 12 months; and

implement their strategies of managing individual members’ tax positions;

have all their earned income and capital gains exempt from withdrawal tax when

they transit to the Pension Phase, as detailed by Renton, (2012).

(D) Flexibility

The governing rules of SMSF, as per Smith & Koken, (2011), provide their members

with flexibility which is not available to other superannuation funds. This flexibility

offers tax benefits and a SMSF can acquire business real assets either from another

member or from other related parties of the fund, assert Ault, Arnold & Gest, (2010).

(E) Other Benefits

(a) Life Insurance

As members of a SMSF, Herbert and Dorothy will be able to get both life and income

protection insurance covers. The advantage for the couple from this approach will be

that the premium of such insurance policies will be paid by the SMSF and the premium

amount is considered as a tax-deductible expense for the SMSF, say Deutsch et al,

(2011). Since the ATO has now abolished the Reasonable Benefit Limits, the barrier for

members requiring higher life insurance through their SMSF has been removed. A

Reasonable Benefit Limit is the maximum amount of the retirement benefit an

individual can receive over the individual’s lifetime at a concessional tax rate, says

Barkoczy, (2015).

(b) Effective Transfer of Wealth

SMSF’s inherent flexibility will allow Herbert and Dorothy to make arrangements for

facilitating an effective wealth transfer after their death, asserts Renton, (2012). Since

listed or unlisted property trusts, including their derivative products such as Dividend

Warrants and Options, as detailed by Marsden, (2010).

(C) Tax Benefits

Herbert and Dorothy will be able to take advantage of the following benefits which are

provided exclusively to the SMSFs by the Australian Taxation Office (ATO). In the

Accumulation Phase of the SMSF, Herbert and Dorothy will be able to–

gain tax benefits for their Concessional Contributions which are taxed at a flat

rate of 15% in a SMSF;

get benefit of Government Co-contribution for all their qualifying contributions;

get investment earning which are taxed at maximum rate of 15% in SMSF;

pay Capital Gains Tax @10% on assets held for above 12 months; and

implement their strategies of managing individual members’ tax positions;

have all their earned income and capital gains exempt from withdrawal tax when

they transit to the Pension Phase, as detailed by Renton, (2012).

(D) Flexibility

The governing rules of SMSF, as per Smith & Koken, (2011), provide their members

with flexibility which is not available to other superannuation funds. This flexibility

offers tax benefits and a SMSF can acquire business real assets either from another

member or from other related parties of the fund, assert Ault, Arnold & Gest, (2010).

(E) Other Benefits

(a) Life Insurance

As members of a SMSF, Herbert and Dorothy will be able to get both life and income

protection insurance covers. The advantage for the couple from this approach will be

that the premium of such insurance policies will be paid by the SMSF and the premium

amount is considered as a tax-deductible expense for the SMSF, say Deutsch et al,

(2011). Since the ATO has now abolished the Reasonable Benefit Limits, the barrier for

members requiring higher life insurance through their SMSF has been removed. A

Reasonable Benefit Limit is the maximum amount of the retirement benefit an

individual can receive over the individual’s lifetime at a concessional tax rate, says

Barkoczy, (2015).

(b) Effective Transfer of Wealth

SMSF’s inherent flexibility will allow Herbert and Dorothy to make arrangements for

facilitating an effective wealth transfer after their death, asserts Renton, (2012). Since

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page7

the superannuation savings are the largest asset or, in some cases, the second largest

asset, after the individual’s family home, it becomes prudent for the authorities to

ensure that the superannuation savings of the couple are transferred between generations

in an effective manner, asserts Barkoczy, (2013).

(c) Retirement Income

A SMSF is the right source for paying its members their benefits as a retirement income

stream. This also includes the transition from the Accumulation Phase to the Retirement

Income Phase. Moreover, as Herbert and Dorothy will be the fund trustees, they can

tailor-make their payments for meeting their financial needs, says Marsden, (2010).

Case Study Conclusion

This paper firmly believes that the dispositions made here are for the betterment of

Herbert and Dorothy. The SMSF is the single, most effective, source of fund

management, which can prove to be a boon for the couple in planning their long-term

(as well as short-term) wealth management strategies.

LIST OF REFERENCES

Ault, H. J., Arnold, B. J. and Gest, G. 2010. Comparative income taxation: a structural

analysis. 3rd ed. Kluwer Law International, Amsterdam.

Barkoczy, S. 2013. Foundations of Taxation Law 2012, 5th ed. CCH Australia Limited,

North Ryde, NSW.

Barkoczy, S. 2015. Australian Tax Case book, 12th ed. CCH Australia Limited, North

Ryde, NSW.

the superannuation savings are the largest asset or, in some cases, the second largest

asset, after the individual’s family home, it becomes prudent for the authorities to

ensure that the superannuation savings of the couple are transferred between generations

in an effective manner, asserts Barkoczy, (2013).

(c) Retirement Income

A SMSF is the right source for paying its members their benefits as a retirement income

stream. This also includes the transition from the Accumulation Phase to the Retirement

Income Phase. Moreover, as Herbert and Dorothy will be the fund trustees, they can

tailor-make their payments for meeting their financial needs, says Marsden, (2010).

Case Study Conclusion

This paper firmly believes that the dispositions made here are for the betterment of

Herbert and Dorothy. The SMSF is the single, most effective, source of fund

management, which can prove to be a boon for the couple in planning their long-term

(as well as short-term) wealth management strategies.

LIST OF REFERENCES

Ault, H. J., Arnold, B. J. and Gest, G. 2010. Comparative income taxation: a structural

analysis. 3rd ed. Kluwer Law International, Amsterdam.

Barkoczy, S. 2013. Foundations of Taxation Law 2012, 5th ed. CCH Australia Limited,

North Ryde, NSW.

Barkoczy, S. 2015. Australian Tax Case book, 12th ed. CCH Australia Limited, North

Ryde, NSW.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page8

CCH. 2015. Australian Master Tax Guide 2015. CCH Australia Limited, Sydney, NSW.

Deutsch, R., Friezer, M., Fullerton, I., Gibson, M., Hanley, P. and Snape, T. (2011)

Australian tax handbook. Thomson Reuters, Pyrmont, NSW.

Low and Middle Income Tax Offset. Retrieved on 5th October, 2018 from

https://atotaxrates.info/tax-offset/low-and-middle-income-tax-offset/

Marsden, S. J. 2010. Australian Master Bookkeepers Guide, 3rd ed. CCH Australia

Limited, Sydney, NSW.

Nethercott, L., Devos, K. and Richardson, G. 2010. Australian taxation study manual:

questions and suggested solutions, 20th ed. CCH Australia Limited, Sydney, NSW.

Renton, N. E. 2012. Family Trusts: A Plain English Guide for Australian Families of

Average Means, 4th ed. John Wiley & Sons, Milton, QLD.

Smith, B. and Koken, E. 2011.The Superannuation Handbook. John Wiley & Sons,

Milton, QLD.

CCH. 2015. Australian Master Tax Guide 2015. CCH Australia Limited, Sydney, NSW.

Deutsch, R., Friezer, M., Fullerton, I., Gibson, M., Hanley, P. and Snape, T. (2011)

Australian tax handbook. Thomson Reuters, Pyrmont, NSW.

Low and Middle Income Tax Offset. Retrieved on 5th October, 2018 from

https://atotaxrates.info/tax-offset/low-and-middle-income-tax-offset/

Marsden, S. J. 2010. Australian Master Bookkeepers Guide, 3rd ed. CCH Australia

Limited, Sydney, NSW.

Nethercott, L., Devos, K. and Richardson, G. 2010. Australian taxation study manual:

questions and suggested solutions, 20th ed. CCH Australia Limited, Sydney, NSW.

Renton, N. E. 2012. Family Trusts: A Plain English Guide for Australian Families of

Average Means, 4th ed. John Wiley & Sons, Milton, QLD.

Smith, B. and Koken, E. 2011.The Superannuation Handbook. John Wiley & Sons,

Milton, QLD.

Page9

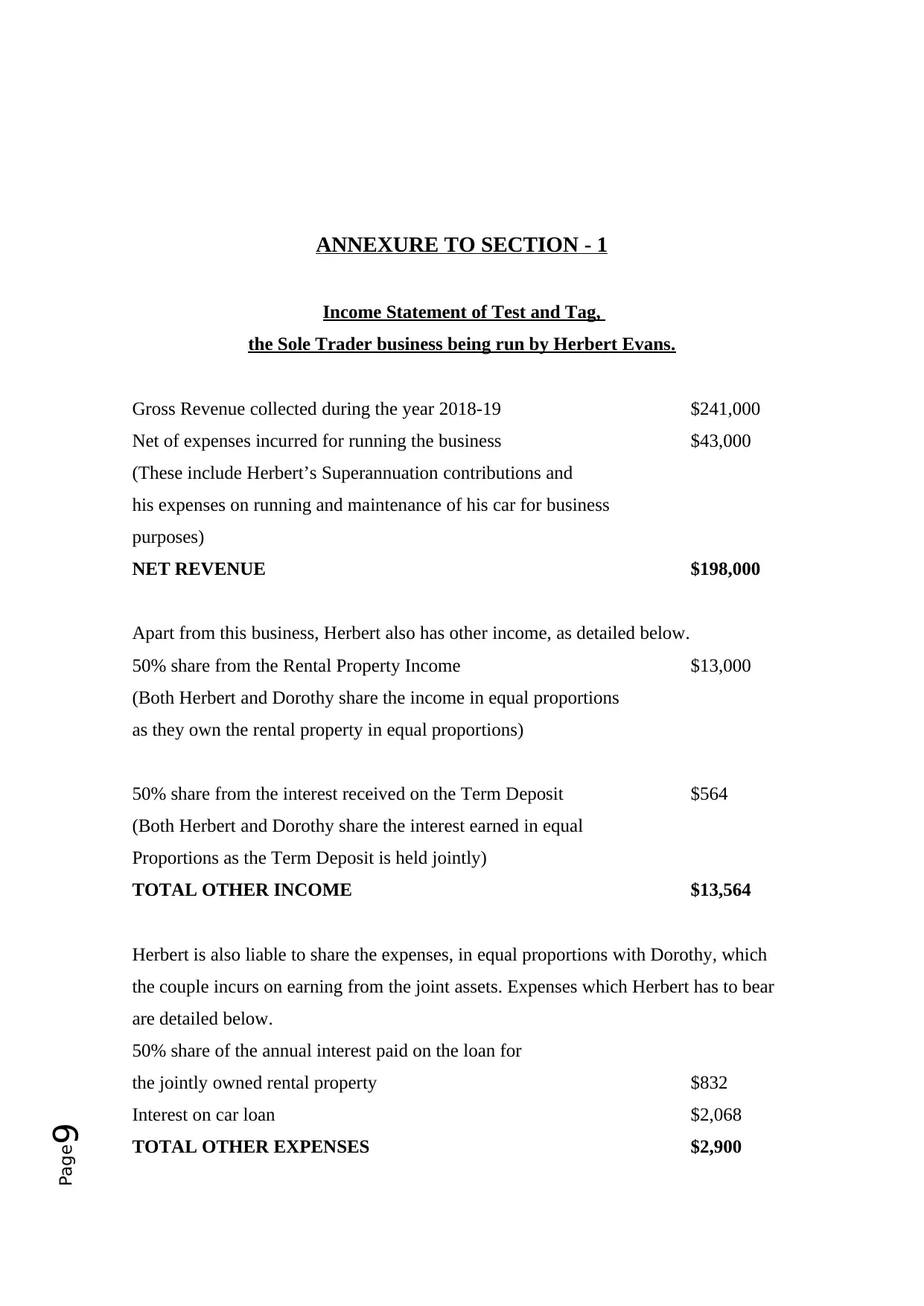

ANNEXURE TO SECTION - 1

Income Statement of Test and Tag,

the Sole Trader business being run by Herbert Evans.

Gross Revenue collected during the year 2018-19 $241,000

Net of expenses incurred for running the business $43,000

(These include Herbert’s Superannuation contributions and

his expenses on running and maintenance of his car for business

purposes)

NET REVENUE $198,000

Apart from this business, Herbert also has other income, as detailed below.

50% share from the Rental Property Income $13,000

(Both Herbert and Dorothy share the income in equal proportions

as they own the rental property in equal proportions)

50% share from the interest received on the Term Deposit $564

(Both Herbert and Dorothy share the interest earned in equal

Proportions as the Term Deposit is held jointly)

TOTAL OTHER INCOME $13,564

Herbert is also liable to share the expenses, in equal proportions with Dorothy, which

the couple incurs on earning from the joint assets. Expenses which Herbert has to bear

are detailed below.

50% share of the annual interest paid on the loan for

the jointly owned rental property $832

Interest on car loan $2,068

TOTAL OTHER EXPENSES $2,900

ANNEXURE TO SECTION - 1

Income Statement of Test and Tag,

the Sole Trader business being run by Herbert Evans.

Gross Revenue collected during the year 2018-19 $241,000

Net of expenses incurred for running the business $43,000

(These include Herbert’s Superannuation contributions and

his expenses on running and maintenance of his car for business

purposes)

NET REVENUE $198,000

Apart from this business, Herbert also has other income, as detailed below.

50% share from the Rental Property Income $13,000

(Both Herbert and Dorothy share the income in equal proportions

as they own the rental property in equal proportions)

50% share from the interest received on the Term Deposit $564

(Both Herbert and Dorothy share the interest earned in equal

Proportions as the Term Deposit is held jointly)

TOTAL OTHER INCOME $13,564

Herbert is also liable to share the expenses, in equal proportions with Dorothy, which

the couple incurs on earning from the joint assets. Expenses which Herbert has to bear

are detailed below.

50% share of the annual interest paid on the loan for

the jointly owned rental property $832

Interest on car loan $2,068

TOTAL OTHER EXPENSES $2,900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Page10

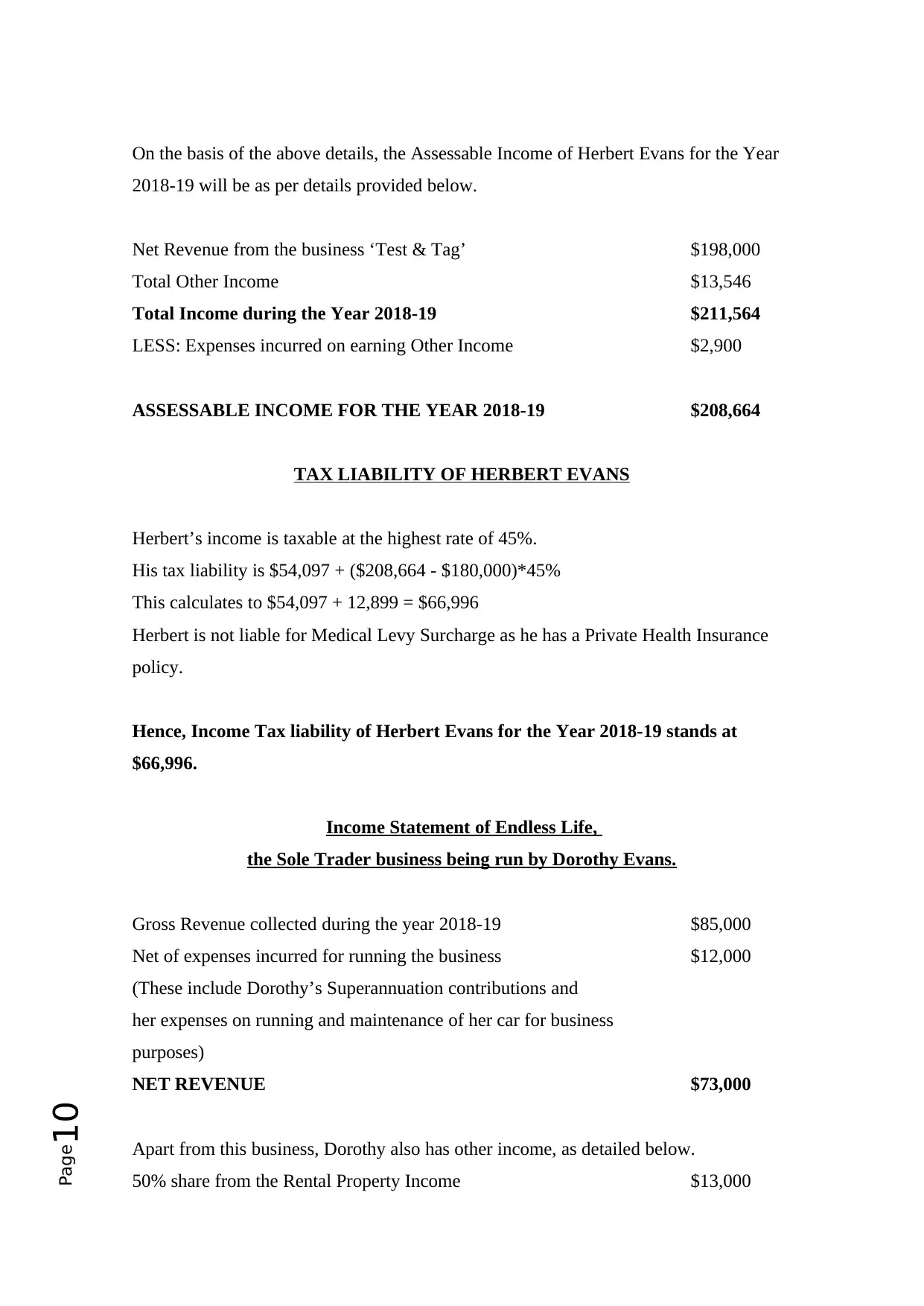

On the basis of the above details, the Assessable Income of Herbert Evans for the Year

2018-19 will be as per details provided below.

Net Revenue from the business ‘Test & Tag’ $198,000

Total Other Income $13,546

Total Income during the Year 2018-19 $211,564

LESS: Expenses incurred on earning Other Income $2,900

ASSESSABLE INCOME FOR THE YEAR 2018-19 $208,664

TAX LIABILITY OF HERBERT EVANS

Herbert’s income is taxable at the highest rate of 45%.

His tax liability is $54,097 + ($208,664 - $180,000)*45%

This calculates to $54,097 + 12,899 = $66,996

Herbert is not liable for Medical Levy Surcharge as he has a Private Health Insurance

policy.

Hence, Income Tax liability of Herbert Evans for the Year 2018-19 stands at

$66,996.

Income Statement of Endless Life,

the Sole Trader business being run by Dorothy Evans.

Gross Revenue collected during the year 2018-19 $85,000

Net of expenses incurred for running the business $12,000

(These include Dorothy’s Superannuation contributions and

her expenses on running and maintenance of her car for business

purposes)

NET REVENUE $73,000

Apart from this business, Dorothy also has other income, as detailed below.

50% share from the Rental Property Income $13,000

On the basis of the above details, the Assessable Income of Herbert Evans for the Year

2018-19 will be as per details provided below.

Net Revenue from the business ‘Test & Tag’ $198,000

Total Other Income $13,546

Total Income during the Year 2018-19 $211,564

LESS: Expenses incurred on earning Other Income $2,900

ASSESSABLE INCOME FOR THE YEAR 2018-19 $208,664

TAX LIABILITY OF HERBERT EVANS

Herbert’s income is taxable at the highest rate of 45%.

His tax liability is $54,097 + ($208,664 - $180,000)*45%

This calculates to $54,097 + 12,899 = $66,996

Herbert is not liable for Medical Levy Surcharge as he has a Private Health Insurance

policy.

Hence, Income Tax liability of Herbert Evans for the Year 2018-19 stands at

$66,996.

Income Statement of Endless Life,

the Sole Trader business being run by Dorothy Evans.

Gross Revenue collected during the year 2018-19 $85,000

Net of expenses incurred for running the business $12,000

(These include Dorothy’s Superannuation contributions and

her expenses on running and maintenance of her car for business

purposes)

NET REVENUE $73,000

Apart from this business, Dorothy also has other income, as detailed below.

50% share from the Rental Property Income $13,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Page11

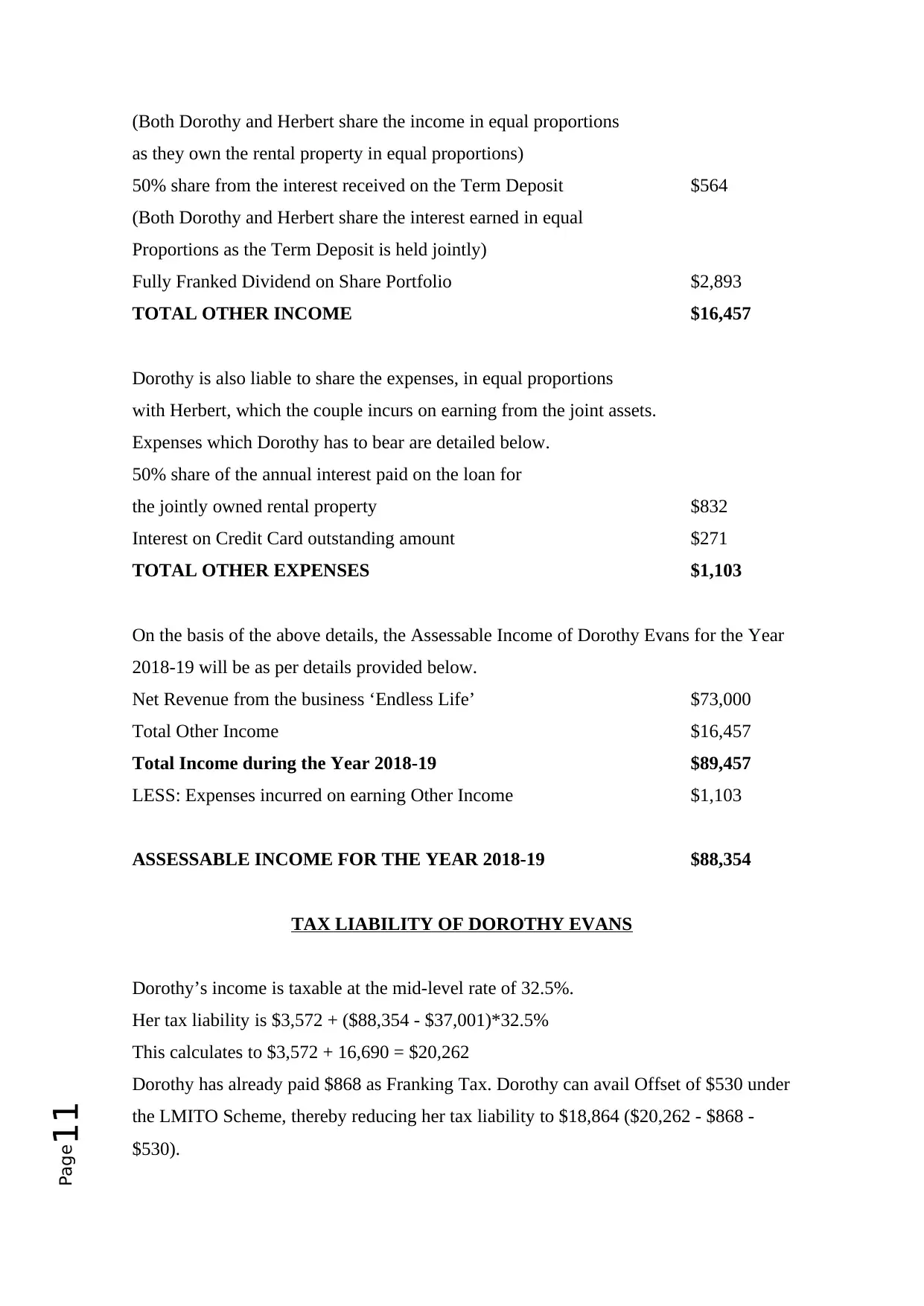

(Both Dorothy and Herbert share the income in equal proportions

as they own the rental property in equal proportions)

50% share from the interest received on the Term Deposit $564

(Both Dorothy and Herbert share the interest earned in equal

Proportions as the Term Deposit is held jointly)

Fully Franked Dividend on Share Portfolio $2,893

TOTAL OTHER INCOME $16,457

Dorothy is also liable to share the expenses, in equal proportions

with Herbert, which the couple incurs on earning from the joint assets.

Expenses which Dorothy has to bear are detailed below.

50% share of the annual interest paid on the loan for

the jointly owned rental property $832

Interest on Credit Card outstanding amount $271

TOTAL OTHER EXPENSES $1,103

On the basis of the above details, the Assessable Income of Dorothy Evans for the Year

2018-19 will be as per details provided below.

Net Revenue from the business ‘Endless Life’ $73,000

Total Other Income $16,457

Total Income during the Year 2018-19 $89,457

LESS: Expenses incurred on earning Other Income $1,103

ASSESSABLE INCOME FOR THE YEAR 2018-19 $88,354

TAX LIABILITY OF DOROTHY EVANS

Dorothy’s income is taxable at the mid-level rate of 32.5%.

Her tax liability is $3,572 + ($88,354 - $37,001)*32.5%

This calculates to $3,572 + 16,690 = $20,262

Dorothy has already paid $868 as Franking Tax. Dorothy can avail Offset of $530 under

the LMITO Scheme, thereby reducing her tax liability to $18,864 ($20,262 - $868 -

$530).

(Both Dorothy and Herbert share the income in equal proportions

as they own the rental property in equal proportions)

50% share from the interest received on the Term Deposit $564

(Both Dorothy and Herbert share the interest earned in equal

Proportions as the Term Deposit is held jointly)

Fully Franked Dividend on Share Portfolio $2,893

TOTAL OTHER INCOME $16,457

Dorothy is also liable to share the expenses, in equal proportions

with Herbert, which the couple incurs on earning from the joint assets.

Expenses which Dorothy has to bear are detailed below.

50% share of the annual interest paid on the loan for

the jointly owned rental property $832

Interest on Credit Card outstanding amount $271

TOTAL OTHER EXPENSES $1,103

On the basis of the above details, the Assessable Income of Dorothy Evans for the Year

2018-19 will be as per details provided below.

Net Revenue from the business ‘Endless Life’ $73,000

Total Other Income $16,457

Total Income during the Year 2018-19 $89,457

LESS: Expenses incurred on earning Other Income $1,103

ASSESSABLE INCOME FOR THE YEAR 2018-19 $88,354

TAX LIABILITY OF DOROTHY EVANS

Dorothy’s income is taxable at the mid-level rate of 32.5%.

Her tax liability is $3,572 + ($88,354 - $37,001)*32.5%

This calculates to $3,572 + 16,690 = $20,262

Dorothy has already paid $868 as Franking Tax. Dorothy can avail Offset of $530 under

the LMITO Scheme, thereby reducing her tax liability to $18,864 ($20,262 - $868 -

$530).

Page12

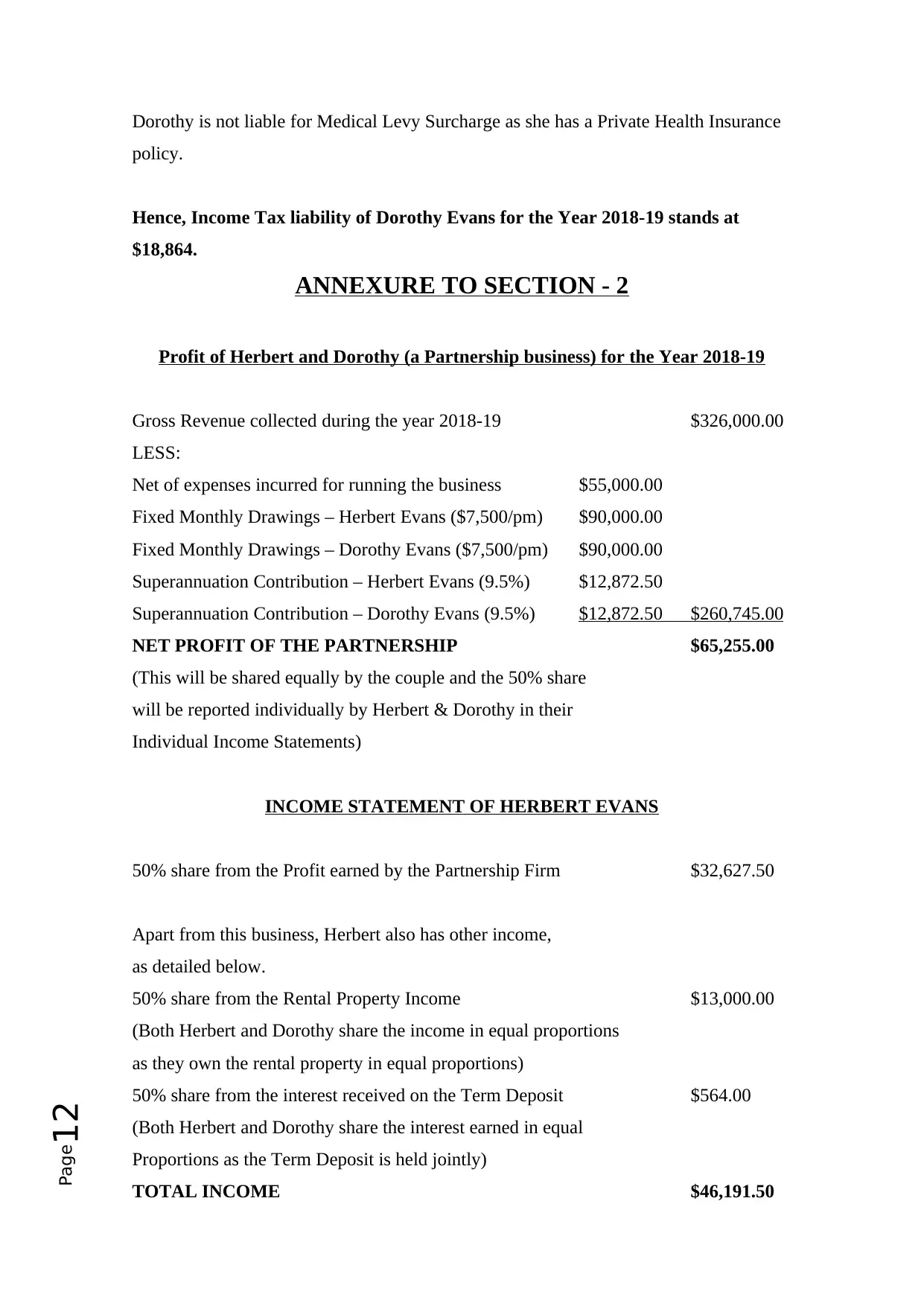

Dorothy is not liable for Medical Levy Surcharge as she has a Private Health Insurance

policy.

Hence, Income Tax liability of Dorothy Evans for the Year 2018-19 stands at

$18,864.

ANNEXURE TO SECTION - 2

Profit of Herbert and Dorothy (a Partnership business) for the Year 2018-19

Gross Revenue collected during the year 2018-19 $326,000.00

LESS:

Net of expenses incurred for running the business $55,000.00

Fixed Monthly Drawings – Herbert Evans ($7,500/pm) $90,000.00

Fixed Monthly Drawings – Dorothy Evans ($7,500/pm) $90,000.00

Superannuation Contribution – Herbert Evans (9.5%) $12,872.50

Superannuation Contribution – Dorothy Evans (9.5%) $12,872.50 $260,745.00

NET PROFIT OF THE PARTNERSHIP $65,255.00

(This will be shared equally by the couple and the 50% share

will be reported individually by Herbert & Dorothy in their

Individual Income Statements)

INCOME STATEMENT OF HERBERT EVANS

50% share from the Profit earned by the Partnership Firm $32,627.50

Apart from this business, Herbert also has other income,

as detailed below.

50% share from the Rental Property Income $13,000.00

(Both Herbert and Dorothy share the income in equal proportions

as they own the rental property in equal proportions)

50% share from the interest received on the Term Deposit $564.00

(Both Herbert and Dorothy share the interest earned in equal

Proportions as the Term Deposit is held jointly)

TOTAL INCOME $46,191.50

Dorothy is not liable for Medical Levy Surcharge as she has a Private Health Insurance

policy.

Hence, Income Tax liability of Dorothy Evans for the Year 2018-19 stands at

$18,864.

ANNEXURE TO SECTION - 2

Profit of Herbert and Dorothy (a Partnership business) for the Year 2018-19

Gross Revenue collected during the year 2018-19 $326,000.00

LESS:

Net of expenses incurred for running the business $55,000.00

Fixed Monthly Drawings – Herbert Evans ($7,500/pm) $90,000.00

Fixed Monthly Drawings – Dorothy Evans ($7,500/pm) $90,000.00

Superannuation Contribution – Herbert Evans (9.5%) $12,872.50

Superannuation Contribution – Dorothy Evans (9.5%) $12,872.50 $260,745.00

NET PROFIT OF THE PARTNERSHIP $65,255.00

(This will be shared equally by the couple and the 50% share

will be reported individually by Herbert & Dorothy in their

Individual Income Statements)

INCOME STATEMENT OF HERBERT EVANS

50% share from the Profit earned by the Partnership Firm $32,627.50

Apart from this business, Herbert also has other income,

as detailed below.

50% share from the Rental Property Income $13,000.00

(Both Herbert and Dorothy share the income in equal proportions

as they own the rental property in equal proportions)

50% share from the interest received on the Term Deposit $564.00

(Both Herbert and Dorothy share the interest earned in equal

Proportions as the Term Deposit is held jointly)

TOTAL INCOME $46,191.50

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.