Case Study: Applied Corporate Finance (FIN342) - Dick Smith Group

VerifiedAdded on 2023/06/05

|26

|8472

|352

Case Study

AI Summary

This assignment presents a detailed analysis of the financial performance of Dick Smith Group (DSG) for the six-month period leading up to its voluntary administration in January 2016. The analysis reveals a consistent pattern of net losses, particularly exacerbated in November and December 2015 due to significant inventory obsolescence and heavy discounting. The report highlights key financial indicators such as declining sales, negative gross profits in certain months, and substantial EBITDA losses. A significant impairment charge on inventory further contributed to the company's financial distress, ultimately leading to the appointment of administrators. The case study utilizes data from administrator reports and other publicly available information to provide a comprehensive understanding of the factors contributing to DSG's financial collapse.

Applied Corporate Finance

(FIN342)

Assignment2

Total marks: 100

Personal ID: [Enteryour PersonalID]

I have read the Assignment Guide in the ‘General assessment information’ and have applied the

word count principles to my work.

My word count for this assignment is: [Enter your word count] words

Your assignment should be loaded into KapLearn by 11.30 pm on the due date.

All times are based on AEDT/AEST time zones.

Refer to ‘Time remaining’ on the ‘Assignment’ page in KapLearn to ensure you submit

your assignment by the specified due date and time.

Checklist

I have completed my assignment using Word.

I have completed my assignment using Calibri, Arial, Times New Roman or Verdana fonts.

I have added my Personal ID on this page.

I have added my word count on this page.

I have added my Personal ID in front of the filename in the footer on the second page.

I have saved the file to be uploaded as PersonalID_FIN342_AS2_v3A2.

Each question of my assignment is within the word limit guidelines for that question as per the

‘General assessment information’ (Assessment Assignment General assessment information).

My assignment file size is no larger than 2 MB.

If tables were required, they are visible as text, not as links or images.

I have not removed the marking grid from the footer.

I have submitted my assignment as per the instructions in KapLearn.

(FIN342)

Assignment2

Total marks: 100

Personal ID: [Enteryour PersonalID]

I have read the Assignment Guide in the ‘General assessment information’ and have applied the

word count principles to my work.

My word count for this assignment is: [Enter your word count] words

Your assignment should be loaded into KapLearn by 11.30 pm on the due date.

All times are based on AEDT/AEST time zones.

Refer to ‘Time remaining’ on the ‘Assignment’ page in KapLearn to ensure you submit

your assignment by the specified due date and time.

Checklist

I have completed my assignment using Word.

I have completed my assignment using Calibri, Arial, Times New Roman or Verdana fonts.

I have added my Personal ID on this page.

I have added my word count on this page.

I have added my Personal ID in front of the filename in the footer on the second page.

I have saved the file to be uploaded as PersonalID_FIN342_AS2_v3A2.

Each question of my assignment is within the word limit guidelines for that question as per the

‘General assessment information’ (Assessment Assignment General assessment information).

My assignment file size is no larger than 2 MB.

If tables were required, they are visible as text, not as links or images.

I have not removed the marking grid from the footer.

I have submitted my assignment as per the instructions in KapLearn.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marker feedback

Comment on overall performance:

For marker use only.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 2 © Kaplan Higher Education

Comment on overall performance:

For marker use only.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 2 © Kaplan Higher Education

Instructions to students

• This assignment covers all topics of this subject and accounts for 50% of your final grade.

• There are three (3) questions in this assignment. You should answer all questions.

• The overall word limit for the assignment is 4500 words. Marks will only be awarded for answers up

to the word limit (plus 10%) for each question. Any material written after this will not be counted

towards your mark for that question. Headings, quotes and references within the body of the answer

are included in the word count. Numerical tables, calculations, and reference lists are not included.

For more information on word counts and their rationale, go to Assessment Assignment

General assessment information.

• Your report should be concise and specific and should contain only the relevant information as specified

in each question. You may set out your report in point form where appropriate.

• Ensure you answer the question asked (i.e. take note of the specific requirements of the question).

• The emphasis of this assignment is on evaluating and analysing financial and other data and information.

• Further research is required beyond the information contained in the subject materials and textbook.

• Important note: Do not approach anyone associated with Dick Smith Group of Companies (‘DSG’)

directly for information. Refer to the details provided regarding recommended information sources in

the introduction to this assignment. You may also use other information sources identified through your

independent research.

• Refer to the Criteria-based Marking Guide for guidelines on what is expected for each question.

• The ‘General assessment information’ section in KapLearn contains information about format and

presentation, word limits, citations and referencing, collusion, plagiarism and other policies,

useful resources, submitting your assignment and accessing your results.

• Answers are to be in your own words. Reference and cite all your sources (within the text of your

answer) when quoting or using material from external sources. Include a reference list at the end ofyour

assignment. Refer to the ‘Referencing and Citations Guide’ available from the ‘Library Learning Hub’ in

KapLearn for further information on referencing.

• Indicative weightings are noted beside each question. Use these weightings to assist you with your

allocation of time and resources. The weightings indicate the relative importance of each question.

• State all assumptions used in providing your answer.

• Requests for special consideration or information pertaining to special consideration written in the body

ofthe assignment will not be considered by the marker. Refer to the ‘special consideration’ section of

the Assessment Policy on Kaplan’s website for more information.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 3 © Kaplan Higher Education

• This assignment covers all topics of this subject and accounts for 50% of your final grade.

• There are three (3) questions in this assignment. You should answer all questions.

• The overall word limit for the assignment is 4500 words. Marks will only be awarded for answers up

to the word limit (plus 10%) for each question. Any material written after this will not be counted

towards your mark for that question. Headings, quotes and references within the body of the answer

are included in the word count. Numerical tables, calculations, and reference lists are not included.

For more information on word counts and their rationale, go to Assessment Assignment

General assessment information.

• Your report should be concise and specific and should contain only the relevant information as specified

in each question. You may set out your report in point form where appropriate.

• Ensure you answer the question asked (i.e. take note of the specific requirements of the question).

• The emphasis of this assignment is on evaluating and analysing financial and other data and information.

• Further research is required beyond the information contained in the subject materials and textbook.

• Important note: Do not approach anyone associated with Dick Smith Group of Companies (‘DSG’)

directly for information. Refer to the details provided regarding recommended information sources in

the introduction to this assignment. You may also use other information sources identified through your

independent research.

• Refer to the Criteria-based Marking Guide for guidelines on what is expected for each question.

• The ‘General assessment information’ section in KapLearn contains information about format and

presentation, word limits, citations and referencing, collusion, plagiarism and other policies,

useful resources, submitting your assignment and accessing your results.

• Answers are to be in your own words. Reference and cite all your sources (within the text of your

answer) when quoting or using material from external sources. Include a reference list at the end ofyour

assignment. Refer to the ‘Referencing and Citations Guide’ available from the ‘Library Learning Hub’ in

KapLearn for further information on referencing.

• Indicative weightings are noted beside each question. Use these weightings to assist you with your

allocation of time and resources. The weightings indicate the relative importance of each question.

• State all assumptions used in providing your answer.

• Requests for special consideration or information pertaining to special consideration written in the body

ofthe assignment will not be considered by the marker. Refer to the ‘special consideration’ section of

the Assessment Policy on Kaplan’s website for more information.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 3 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Learning outcomes (LO) mapping Marks

1. Discuss the objectives and processes of corporate financial management and apply them in

a practical setting. 0

2. Evaluate corporate financial management strategies. 40

3. Propose the key financial issues surrounding the creation of shareholder value. 20

4. Integrate the key theories that inform the fundraising and capital structure management

process. 10

5. Compare the roles of the key stakeholders and decision makers in a corporation’s financial

management. 30

Total marks 100

Criteria-based Marking Guide

The Criteria-based Marking Guide, provided at the end of each question, is designed to assist students to

understand what is expected of them in each question and to let them know how their performance will be

judged. It provides advice about the criteria used in the marking of the question and what discriminates

between an excellent, satisfactory and unsatisfactory answer.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 4 © Kaplan Higher Education

1. Discuss the objectives and processes of corporate financial management and apply them in

a practical setting. 0

2. Evaluate corporate financial management strategies. 40

3. Propose the key financial issues surrounding the creation of shareholder value. 20

4. Integrate the key theories that inform the fundraising and capital structure management

process. 10

5. Compare the roles of the key stakeholders and decision makers in a corporation’s financial

management. 30

Total marks 100

Criteria-based Marking Guide

The Criteria-based Marking Guide, provided at the end of each question, is designed to assist students to

understand what is expected of them in each question and to let them know how their performance will be

judged. It provides advice about the criteria used in the marking of the question and what discriminates

between an excellent, satisfactory and unsatisfactory answer.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 4 © Kaplan Higher Education

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case Study: Dick Smith Group

This assignment gives you the opportunity to apply the material covered in ‘Applied Corporate Finance’

(FIN342) to an Australian company that has had a mixed history of success and failure in the Australian

marketplace.

The Dick Smith Group of companies (‘DSG’) has had a high profile in the financial press since late 2015.

Hence, it represents a good case study to use to analyse a number of corporate financial management

issues relevant to this subject.

Dick Smith Holdings Limited (ASX Code: DSH) is the holding company of the Dick Smith Group (‘DSG’) that

consists of 11 wholly owned subsidiaries. DSH is the ASX code for Dick Smith Group of Companies (DSG).

In this assignment, Dick Smith,DSG and DSH are used interchangeably to mean the same entity. DSG

operated the consumer electronics retail stores and an online consumer electronics retail business

throughout Australia and New Zealand, operating from more than 390 locations with at least 3,000

employees. The majority of the network was branded as ‘Dick Smith’ stores but also incorporated ‘Move’

bannered stores, ‘Electronics Powered by Dick Smith’ outlets in David Jones stores, and commercial and

online businesses.

The company was founded in 1968 by Mr Dick Smith and owned by him and his wife until 1982.

Woolworths Limited purchased Dick Smith Electronics in 1982 and then sold the company to Anchorage

Capital Partners in 2012, which floated DSG on the Australian Securities Exchange (ASX) in 2013.The IPO

was successful and the share price remained stable at near the offer price of AUD2.20 per share.

In 2015, concerns emerged about trading performance, inventory management and buyer rebates and

their collective impact on cash flow.The share price weakened dramatically.

By December 2015, the share price had fallen 80%. On 4 January 2016, DSH (and associated entities)

was placed into voluntary administration by the Board. Subsequently, a syndicate of lenders appointed

Ferrier Hodgson as receiversand managers.The online operations and Dick Smith brand were sold to Kogan

(May 2016) and the remainder of the business was liquidated.

Recommended information sources

The following information sources may assist you:

• DSG prospectus, annual reports and financial statements — available for download from the DatAnalysis

Premium database in KapLearn under ‘Library’ using the stock code ‘DSH’.

Note: Where there is conflicting data within different reports use the later reports.

• DSG investor communications and presentations — available for download from the DatAnalysis

Premium database in KapLearn under ‘Library’ using the stock code ‘DSH’.

• Other articles and reports on Dick Smith Group of Companies available online.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 5 © Kaplan Higher Education

This assignment gives you the opportunity to apply the material covered in ‘Applied Corporate Finance’

(FIN342) to an Australian company that has had a mixed history of success and failure in the Australian

marketplace.

The Dick Smith Group of companies (‘DSG’) has had a high profile in the financial press since late 2015.

Hence, it represents a good case study to use to analyse a number of corporate financial management

issues relevant to this subject.

Dick Smith Holdings Limited (ASX Code: DSH) is the holding company of the Dick Smith Group (‘DSG’) that

consists of 11 wholly owned subsidiaries. DSH is the ASX code for Dick Smith Group of Companies (DSG).

In this assignment, Dick Smith,DSG and DSH are used interchangeably to mean the same entity. DSG

operated the consumer electronics retail stores and an online consumer electronics retail business

throughout Australia and New Zealand, operating from more than 390 locations with at least 3,000

employees. The majority of the network was branded as ‘Dick Smith’ stores but also incorporated ‘Move’

bannered stores, ‘Electronics Powered by Dick Smith’ outlets in David Jones stores, and commercial and

online businesses.

The company was founded in 1968 by Mr Dick Smith and owned by him and his wife until 1982.

Woolworths Limited purchased Dick Smith Electronics in 1982 and then sold the company to Anchorage

Capital Partners in 2012, which floated DSG on the Australian Securities Exchange (ASX) in 2013.The IPO

was successful and the share price remained stable at near the offer price of AUD2.20 per share.

In 2015, concerns emerged about trading performance, inventory management and buyer rebates and

their collective impact on cash flow.The share price weakened dramatically.

By December 2015, the share price had fallen 80%. On 4 January 2016, DSH (and associated entities)

was placed into voluntary administration by the Board. Subsequently, a syndicate of lenders appointed

Ferrier Hodgson as receiversand managers.The online operations and Dick Smith brand were sold to Kogan

(May 2016) and the remainder of the business was liquidated.

Recommended information sources

The following information sources may assist you:

• DSG prospectus, annual reports and financial statements — available for download from the DatAnalysis

Premium database in KapLearn under ‘Library’ using the stock code ‘DSH’.

Note: Where there is conflicting data within different reports use the later reports.

• DSG investor communications and presentations — available for download from the DatAnalysis

Premium database in KapLearn under ‘Library’ using the stock code ‘DSH’.

• Other articles and reports on Dick Smith Group of Companies available online.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 5 © Kaplan Higher Education

Question 1 Analysis of financial performance (20marks | word limit: 700 words)

Analyse the financial performance of DSG for the six-month period from 30 June 2015 and comment on key

factors that led to the voluntary appointment of administrators on 04 January 2016.(20marks)

Criteria-based Marking Guide for Question 1

Excellent Satisfactory Unsatisfactory

• rigorous analysis of financial

performance data

• measures of financial

performance addressed and are

all relevant, appropriate and

accurate

• analysis and data presented in a

clear and logical manner

• adheres to word limit

requirements

• reasonable analysis of financial

performance data

• measures of financial

performance addressed and are

mostly relevant, appropriate and

accurate

• analysis and data presented in a

reader-friendly manner

• inadequate analysis of financial

performance data

• little or no specific measures of

financial performance addressed;

or measures not

relevant/appropriate/accurate

• poorly presented information

• not attempted

(Range: 20marks) (Range: 15–20marks) (Range: 10–14marks) (Range: 0–9 marks)

Insert your answertoQuestion 1below this line

According to the report produced by the administrator of Dick Smith Group, McGrathNicol, in July 2015

sales of DSG was 97.2 million dollars. Gross profit in the month was 17.1 million dollars. Net profit after tax

was – 1.3 million dollars (net loss).

In August 2015, sales of DSG were $ 93.9 million; gross profit was $ 17 million; and net profit after tax was

- .3 million dollars (McGrathNicol, 2016).

In September 2015, sales of DSG were $ 131.1 million; gross profit was $ 37.2 million; and net profit after

tax was $ 1.6 million.

In October 2015, sales of DSG were $ 89 million; gross profit was $14.8 million; and net profit after tax was -

$3.4 million (net loss).

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 6 © Kaplan Higher Education

Analyse the financial performance of DSG for the six-month period from 30 June 2015 and comment on key

factors that led to the voluntary appointment of administrators on 04 January 2016.(20marks)

Criteria-based Marking Guide for Question 1

Excellent Satisfactory Unsatisfactory

• rigorous analysis of financial

performance data

• measures of financial

performance addressed and are

all relevant, appropriate and

accurate

• analysis and data presented in a

clear and logical manner

• adheres to word limit

requirements

• reasonable analysis of financial

performance data

• measures of financial

performance addressed and are

mostly relevant, appropriate and

accurate

• analysis and data presented in a

reader-friendly manner

• inadequate analysis of financial

performance data

• little or no specific measures of

financial performance addressed;

or measures not

relevant/appropriate/accurate

• poorly presented information

• not attempted

(Range: 20marks) (Range: 15–20marks) (Range: 10–14marks) (Range: 0–9 marks)

Insert your answertoQuestion 1below this line

According to the report produced by the administrator of Dick Smith Group, McGrathNicol, in July 2015

sales of DSG was 97.2 million dollars. Gross profit in the month was 17.1 million dollars. Net profit after tax

was – 1.3 million dollars (net loss).

In August 2015, sales of DSG were $ 93.9 million; gross profit was $ 17 million; and net profit after tax was

- .3 million dollars (McGrathNicol, 2016).

In September 2015, sales of DSG were $ 131.1 million; gross profit was $ 37.2 million; and net profit after

tax was $ 1.6 million.

In October 2015, sales of DSG were $ 89 million; gross profit was $14.8 million; and net profit after tax was -

$3.4 million (net loss).

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 6 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In November 2015, sales of DSG were $85.2 million; gross profit was – 46.4 million; net profit after tax was

– 42.8 million dollars.

In December 2015, sales of DSG were $ 200.1 million dollars; gross profit was 13.8 million; net profit after

tax was – 70.5 million dollars.

It can be seen that DSG posted net loss in each month in the six month period after June 2015. The month

of November 2015 was particularly bad. In this month it was unable to post gross profit. This means that

the cost of sales was more than the revenue from the sales. This happened because the company had to

give huge discounts to clear its obsolete inventory. Heavy discounts were given in both November 2015 and

December 2015 to clear the inventory. Total loss reported by the company in the months of November and

December, 2015 was $113 million.

EBITDA (Earnings before interest, taxes, Depreciation, and Amortization) losses in the six month period

were $114 million.

Inventory of the company had become so obsolete that an impairment charge of $60 million had to be

taken on the value of the inventory.

Net cash inflow in the six month period after June 2015 was $ 1.7 million. So the company was able to

generate positive net cash inflows in the six month period even after the losses.

Cash & cash equivalents of DSG on 31st December 2015 stood at $31.2 million. Total debt that was due to

mature over the next one year stood at $ 20.2 million.

Key factors that led to voluntary appointment of administrators on 4th January 2016 were:

1. Very low cash flow generated by operations.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 7 © Kaplan Higher Education

– 42.8 million dollars.

In December 2015, sales of DSG were $ 200.1 million dollars; gross profit was 13.8 million; net profit after

tax was – 70.5 million dollars.

It can be seen that DSG posted net loss in each month in the six month period after June 2015. The month

of November 2015 was particularly bad. In this month it was unable to post gross profit. This means that

the cost of sales was more than the revenue from the sales. This happened because the company had to

give huge discounts to clear its obsolete inventory. Heavy discounts were given in both November 2015 and

December 2015 to clear the inventory. Total loss reported by the company in the months of November and

December, 2015 was $113 million.

EBITDA (Earnings before interest, taxes, Depreciation, and Amortization) losses in the six month period

were $114 million.

Inventory of the company had become so obsolete that an impairment charge of $60 million had to be

taken on the value of the inventory.

Net cash inflow in the six month period after June 2015 was $ 1.7 million. So the company was able to

generate positive net cash inflows in the six month period even after the losses.

Cash & cash equivalents of DSG on 31st December 2015 stood at $31.2 million. Total debt that was due to

mature over the next one year stood at $ 20.2 million.

Key factors that led to voluntary appointment of administrators on 4th January 2016 were:

1. Very low cash flow generated by operations.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 7 © Kaplan Higher Education

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Insufficient cash balance to purchase new stock.

3. Delays in payment to operational suppliers.

4. Onerous lease obligations.

5. Obsolete inventory of stock.

End of answers to Question 1

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 8 © Kaplan Higher Education

3. Delays in payment to operational suppliers.

4. Onerous lease obligations.

5. Obsolete inventory of stock.

End of answers to Question 1

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 8 © Kaplan Higher Education

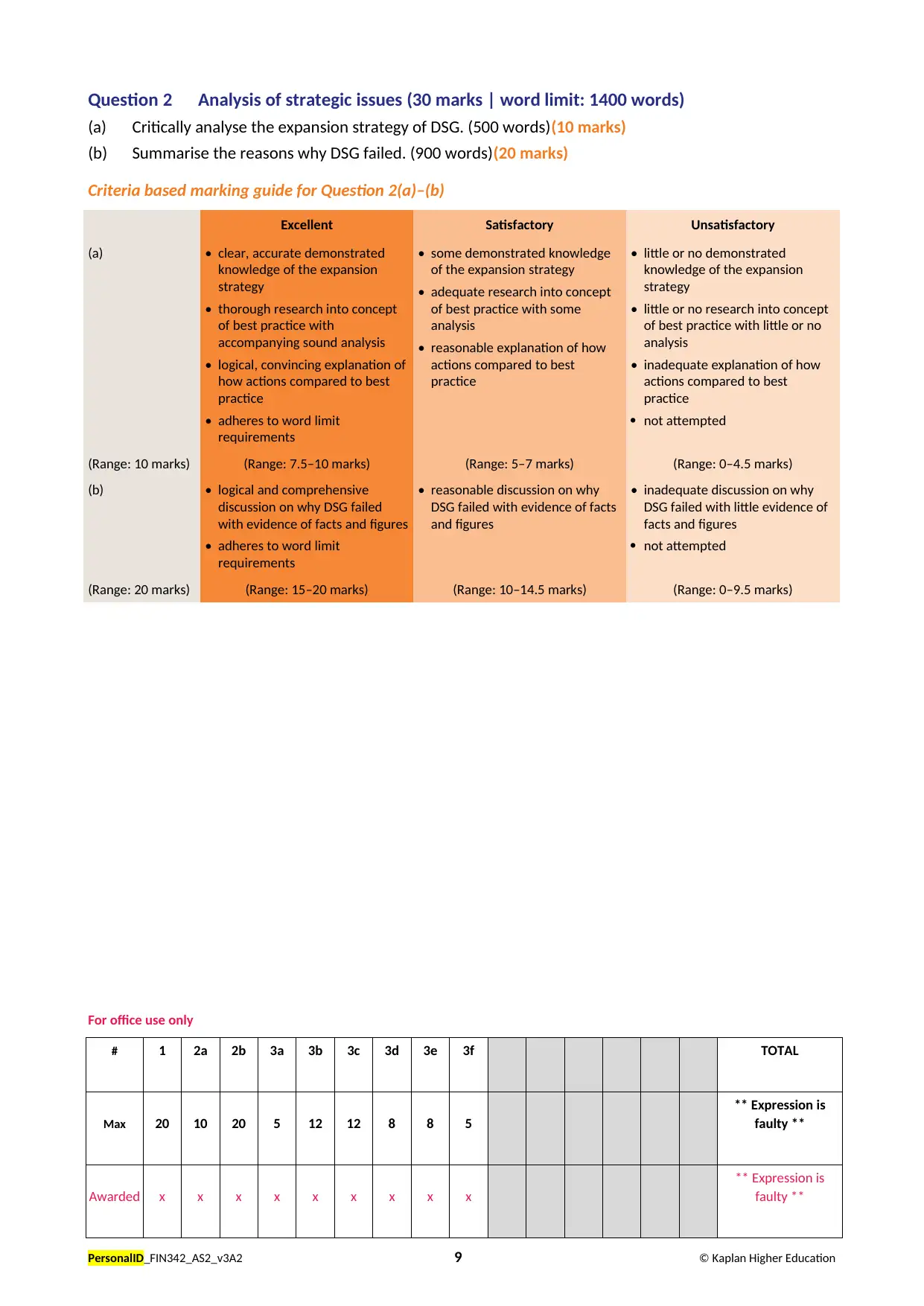

Question 2 Analysis of strategic issues (30 marks | word limit: 1400 words)

(a) Critically analyse the expansion strategy of DSG. (500 words)(10 marks)

(b) Summarise the reasons why DSG failed. (900 words)(20 marks)

Criteria based marking guide for Question 2(a)–(b)

Excellent Satisfactory Unsatisfactory

(a) • clear, accurate demonstrated

knowledge of the expansion

strategy

• thorough research into concept

of best practice with

accompanying sound analysis

• logical, convincing explanation of

how actions compared to best

practice

• adheres to word limit

requirements

• some demonstrated knowledge

of the expansion strategy

• adequate research into concept

of best practice with some

analysis

• reasonable explanation of how

actions compared to best

practice

• little or no demonstrated

knowledge of the expansion

strategy

• little or no research into concept

of best practice with little or no

analysis

• inadequate explanation of how

actions compared to best

practice

not attempted

(Range: 10 marks) (Range: 7.5–10 marks) (Range: 5–7 marks) (Range: 0–4.5 marks)

(b) • logical and comprehensive

discussion on why DSG failed

with evidence of facts and figures

• adheres to word limit

requirements

• reasonable discussion on why

DSG failed with evidence of facts

and figures

• inadequate discussion on why

DSG failed with little evidence of

facts and figures

not attempted

(Range: 20 marks) (Range: 15–20 marks) (Range: 10–14.5 marks) (Range: 0–9.5 marks)

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 9 © Kaplan Higher Education

(a) Critically analyse the expansion strategy of DSG. (500 words)(10 marks)

(b) Summarise the reasons why DSG failed. (900 words)(20 marks)

Criteria based marking guide for Question 2(a)–(b)

Excellent Satisfactory Unsatisfactory

(a) • clear, accurate demonstrated

knowledge of the expansion

strategy

• thorough research into concept

of best practice with

accompanying sound analysis

• logical, convincing explanation of

how actions compared to best

practice

• adheres to word limit

requirements

• some demonstrated knowledge

of the expansion strategy

• adequate research into concept

of best practice with some

analysis

• reasonable explanation of how

actions compared to best

practice

• little or no demonstrated

knowledge of the expansion

strategy

• little or no research into concept

of best practice with little or no

analysis

• inadequate explanation of how

actions compared to best

practice

not attempted

(Range: 10 marks) (Range: 7.5–10 marks) (Range: 5–7 marks) (Range: 0–4.5 marks)

(b) • logical and comprehensive

discussion on why DSG failed

with evidence of facts and figures

• adheres to word limit

requirements

• reasonable discussion on why

DSG failed with evidence of facts

and figures

• inadequate discussion on why

DSG failed with little evidence of

facts and figures

not attempted

(Range: 20 marks) (Range: 15–20 marks) (Range: 10–14.5 marks) (Range: 0–9.5 marks)

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 9 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Insert your answers to Question 2(a)–(b) below this line

2(a)

DSG’s core activity was operating consumer electronics retail stores in New Zealand and Australia.

These brick-and-mortar stores were complemented by an online retail store. In 2013 DSG got listed

at the Australian Securities Exchange (Anchorage Capital Partners, 2013). Post this IPO listing the

company embarked on an expansion plan. The expansion strategy was mainly organic in nature.

Organic means that it involves opening new stores of the company for expansion. Inorganic route is

where a company acquires other companies for achieving expansion. So DSG started a new chain of

retail stores under the Move brand. It entered into a partnership with David Jones to run and

operate retail stores under the David Jones brand. “Move by Dick Smith,” stores opened up in duty

free locations at airports. It also showed some inorganic expansion, when it purchased the Mac 1

stores in September 2014. Mac 1 stores were resellers of Apple products (McGrathNicol, 2016).

To finance this expansion strategy, DSG used both internal cash reserves and also borrowed. Use of

internal cash reserves ultimately led to decline in cash balances. Due to this decline in cash

balances it was later on unable to pay its suppliers in a timely manner. It also found it difficult to

pay back the obligations on its debt.

One of the objectives behind this expansion strategy was to enable DSG to target different market

segments. This in turn would increase its sales.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 10 © Kaplan Higher Education

2(a)

DSG’s core activity was operating consumer electronics retail stores in New Zealand and Australia.

These brick-and-mortar stores were complemented by an online retail store. In 2013 DSG got listed

at the Australian Securities Exchange (Anchorage Capital Partners, 2013). Post this IPO listing the

company embarked on an expansion plan. The expansion strategy was mainly organic in nature.

Organic means that it involves opening new stores of the company for expansion. Inorganic route is

where a company acquires other companies for achieving expansion. So DSG started a new chain of

retail stores under the Move brand. It entered into a partnership with David Jones to run and

operate retail stores under the David Jones brand. “Move by Dick Smith,” stores opened up in duty

free locations at airports. It also showed some inorganic expansion, when it purchased the Mac 1

stores in September 2014. Mac 1 stores were resellers of Apple products (McGrathNicol, 2016).

To finance this expansion strategy, DSG used both internal cash reserves and also borrowed. Use of

internal cash reserves ultimately led to decline in cash balances. Due to this decline in cash

balances it was later on unable to pay its suppliers in a timely manner. It also found it difficult to

pay back the obligations on its debt.

One of the objectives behind this expansion strategy was to enable DSG to target different market

segments. This in turn would increase its sales.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 10 © Kaplan Higher Education

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2(b)

DSG failed because a number of reasons. The main reasons were:

1. Market related factors: Market related factors played an important role in this failure. High

competition in the consumer electronics retail industry in Australia and New Zealand resulted

in erosion of profit margins of DSG (Blanchard, 2017). It was unable to control its overhead

expenses. Its overhead expenses were on average, 9% higher than those of its competitors.

Among the nine key competitors in the consumer electronics retail market DSG had maximal

number of stores at 394 stores. But it was only the sixth largest player with just 9% of the

market share. JB Hi-Fi, the market leader, had 26% market share with just 187 stores. DSG’s

store network expansion strategy did not translate into proportionate increase in sales.

Competition also intensified because of the coming of online retailers. These retailers were

able to sell products at lower prices to customers because of their lower cost base and more

flexible inventory management capabilities. Increase in life cycle of personal computers (PCs)

also contributed to the troubles of DSG. They lowered demands for PCs for office use. Office

sales were important as they contributed to 40% of the total sales of DSG.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 11 © Kaplan Higher Education

DSG failed because a number of reasons. The main reasons were:

1. Market related factors: Market related factors played an important role in this failure. High

competition in the consumer electronics retail industry in Australia and New Zealand resulted

in erosion of profit margins of DSG (Blanchard, 2017). It was unable to control its overhead

expenses. Its overhead expenses were on average, 9% higher than those of its competitors.

Among the nine key competitors in the consumer electronics retail market DSG had maximal

number of stores at 394 stores. But it was only the sixth largest player with just 9% of the

market share. JB Hi-Fi, the market leader, had 26% market share with just 187 stores. DSG’s

store network expansion strategy did not translate into proportionate increase in sales.

Competition also intensified because of the coming of online retailers. These retailers were

able to sell products at lower prices to customers because of their lower cost base and more

flexible inventory management capabilities. Increase in life cycle of personal computers (PCs)

also contributed to the troubles of DSG. They lowered demands for PCs for office use. Office

sales were important as they contributed to 40% of the total sales of DSG.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 11 © Kaplan Higher Education

2. Failure of the expansion strategy: Another reason of failure was aggressive expansion using

internal cash reserves and external debt. This resulted in deterioration of the financial health of

the company. It continued to open new stores while same store sales continued to decline. This

expansion strategy resulted in reduction of returns on invested capital of DSG. At the same

time it considerably increased the debt burden or leverage of the company, thereby increasing

its financial risk. The company’ total debt increased to $ 127 million from $ 71 million in the six

month period between June 2015 and December 2015 (McGrathNicol, 2016). These borrowings

were raised as the company was unable to raise enough cash to pay its suppliers; meet its

capital expenditure requirements. While it was facing this cash crunch it also paid dividends to

its shareholders. This worsened its slide.

3. Purchasing decisions: The management of DSG bought stocks for the stores on the basis of

rebates given by suppliers, and not on the basis of customer demand. This ultimately resulted

in the company having items in its stock that did not have much customer demand.

4. Inventory management: The Company built huge inventory. Due to rapid technological

innovation and changing customer preferences because of this innovation, the inventory of the

company soon became obsolete. Ultimately it had to dispose a large part of this inventory at

heavily discounted prices. It also had to take a $ 60 million write-down on its inventory

(McGrathNicol, 2016). The obsolescence of items in the inventory of DSG can be assessed from

the fact that even during the peak Christmas shopping season of 2014, the company was not

able to reduce its inventory by a significant amount.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 12 © Kaplan Higher Education

internal cash reserves and external debt. This resulted in deterioration of the financial health of

the company. It continued to open new stores while same store sales continued to decline. This

expansion strategy resulted in reduction of returns on invested capital of DSG. At the same

time it considerably increased the debt burden or leverage of the company, thereby increasing

its financial risk. The company’ total debt increased to $ 127 million from $ 71 million in the six

month period between June 2015 and December 2015 (McGrathNicol, 2016). These borrowings

were raised as the company was unable to raise enough cash to pay its suppliers; meet its

capital expenditure requirements. While it was facing this cash crunch it also paid dividends to

its shareholders. This worsened its slide.

3. Purchasing decisions: The management of DSG bought stocks for the stores on the basis of

rebates given by suppliers, and not on the basis of customer demand. This ultimately resulted

in the company having items in its stock that did not have much customer demand.

4. Inventory management: The Company built huge inventory. Due to rapid technological

innovation and changing customer preferences because of this innovation, the inventory of the

company soon became obsolete. Ultimately it had to dispose a large part of this inventory at

heavily discounted prices. It also had to take a $ 60 million write-down on its inventory

(McGrathNicol, 2016). The obsolescence of items in the inventory of DSG can be assessed from

the fact that even during the peak Christmas shopping season of 2014, the company was not

able to reduce its inventory by a significant amount.

For office use only

# 1 2a 2b 3a 3b 3c 3d 3e 3f TOTAL

Max 20 10 20 5 12 12 8 8 5

** Expression is

faulty **

Awarded x x x x x x x x x

** Expression is

faulty **

PersonalID_FIN342_AS2_v3A2 12 © Kaplan Higher Education

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.