FIN3IFM S1 2019 Homework 2: Transaction Exposure and Risk Analysis

VerifiedAdded on 2022/11/14

|9

|1487

|393

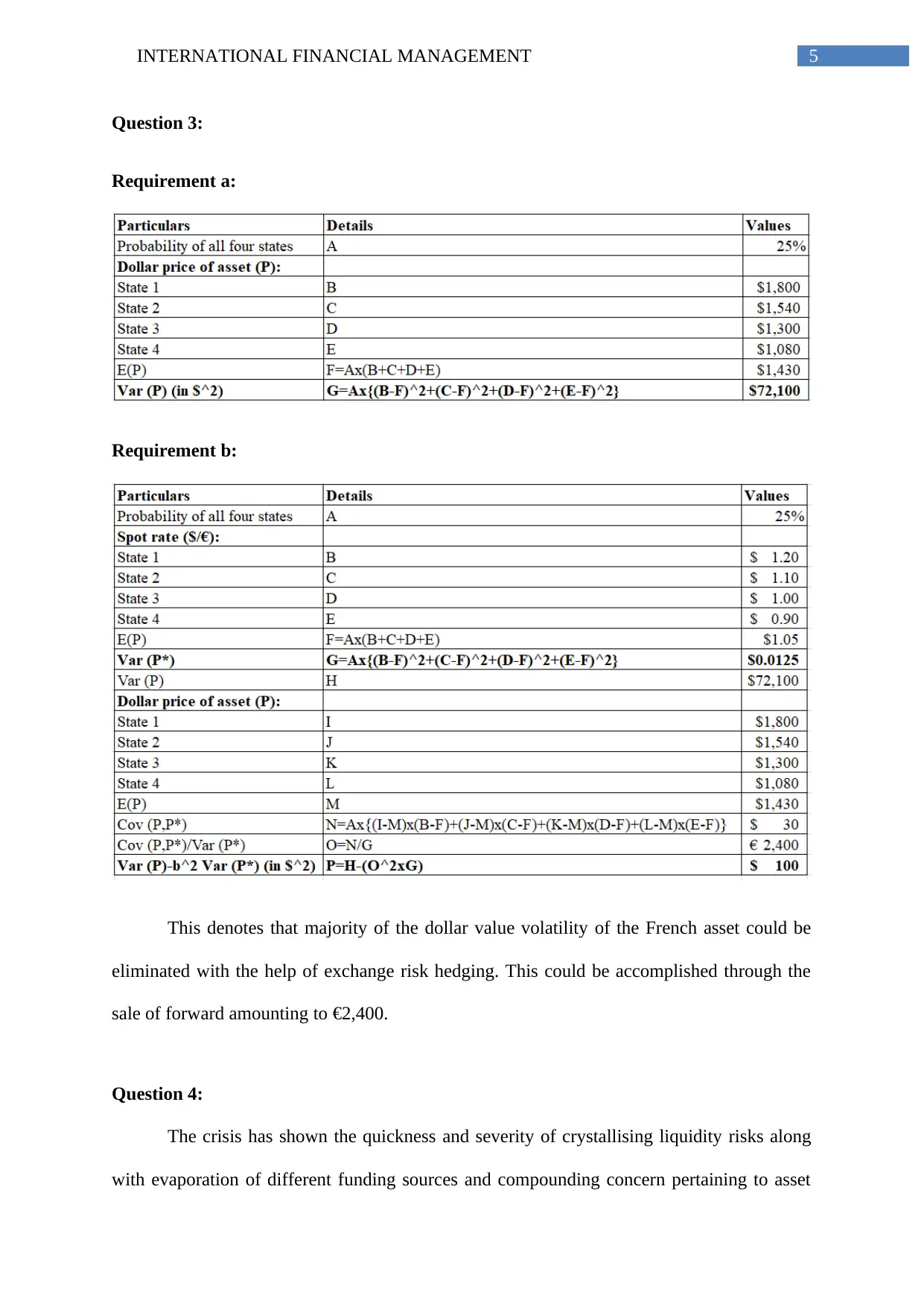

Homework Assignment

AI Summary

This assignment solution delves into key aspects of international financial management, addressing transaction, economic, and translation exposures with relevant examples. It explores the necessity of hedging in imperfect capital markets and calculates net Euro proceeds from a sale, also analyzing exchange risk hedging. Furthermore, it discusses the liquidity risks during the financial crisis, the causes of the 2007 credit crunch, and the roles of structured investment vehicles (SIVs) and collateralized debt obligations (CDOs) in the global financial distress. The document provides a comprehensive overview of these interconnected topics within the realm of international finance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.