FIN4001 Finance Report: Investment, Governance & Budgeting Analysis

VerifiedAdded on 2023/06/12

|15

|3109

|299

Report

AI Summary

This report provides a comprehensive analysis of key finance concepts, starting with a capital budgeting exercise for CyberScore Plc, evaluating two mutually exclusive projects using NPV, WACC, and payback period methods to recommend the optimal investment. It further explores the relationship between corporate governance and corporate social responsibility, highlighting their similarities and differences, and outlines the performance criteria for non-executive directors. Finally, the report discusses the advantages and limitations of traditional budgeting systems, including their role in control, organizational culture, planning, and decentralization, while also addressing inefficiencies and the time-consuming nature of budget preparation. This document is available on Desklib, a platform offering a range of study tools and resources for students.

Running head: INTRODUCTION TO FINANCE

Introduction to Finance

Name of the Student:

Name of the University:

Author’s Note:

Introduction to Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INTRODUCTION TO FINANCE

Executive Summary

The assignment consists of three parts which are which deals with different topics. The first part

deals with the business of CyberScore Plc which is thinking of investing in tow mutually

exclusive project. For such a purpose the technique of capital budgeting is to be applied and

methods such NPV analysis, WACC and payback period of the business is to be calculated. The

second part of the assignment throws light on the relationship between corporate governance and

corporate social responsibility. The last part of the assignment deals with the benefits and

limitations which is faced by traditional budgeting system.

INTRODUCTION TO FINANCE

Executive Summary

The assignment consists of three parts which are which deals with different topics. The first part

deals with the business of CyberScore Plc which is thinking of investing in tow mutually

exclusive project. For such a purpose the technique of capital budgeting is to be applied and

methods such NPV analysis, WACC and payback period of the business is to be calculated. The

second part of the assignment throws light on the relationship between corporate governance and

corporate social responsibility. The last part of the assignment deals with the benefits and

limitations which is faced by traditional budgeting system.

2

INTRODUCTION TO FINANCE

Table of Contents

Answer to Question 1......................................................................................................................3

Capital Budgeting and Weighted Average Cost of Capital.........................................................3

Requirement (a)...........................................................................................................................3

Requirement (b)...........................................................................................................................3

Requirement (c)...........................................................................................................................4

Requirement (d)...........................................................................................................................4

Requirement (e)...........................................................................................................................5

Answer to Question 2......................................................................................................................6

Relation Between Corporate Governance and Corporate Social Responsibility.........................6

Performance Criteria of Non-Executive Director........................................................................7

Answer to Question 3......................................................................................................................8

Advantages of Traditional Budgeting..........................................................................................8

Limitations of Traditional Budgeting System...........................................................................10

Reference.......................................................................................................................................13

INTRODUCTION TO FINANCE

Table of Contents

Answer to Question 1......................................................................................................................3

Capital Budgeting and Weighted Average Cost of Capital.........................................................3

Requirement (a)...........................................................................................................................3

Requirement (b)...........................................................................................................................3

Requirement (c)...........................................................................................................................4

Requirement (d)...........................................................................................................................4

Requirement (e)...........................................................................................................................5

Answer to Question 2......................................................................................................................6

Relation Between Corporate Governance and Corporate Social Responsibility.........................6

Performance Criteria of Non-Executive Director........................................................................7

Answer to Question 3......................................................................................................................8

Advantages of Traditional Budgeting..........................................................................................8

Limitations of Traditional Budgeting System...........................................................................10

Reference.......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INTRODUCTION TO FINANCE

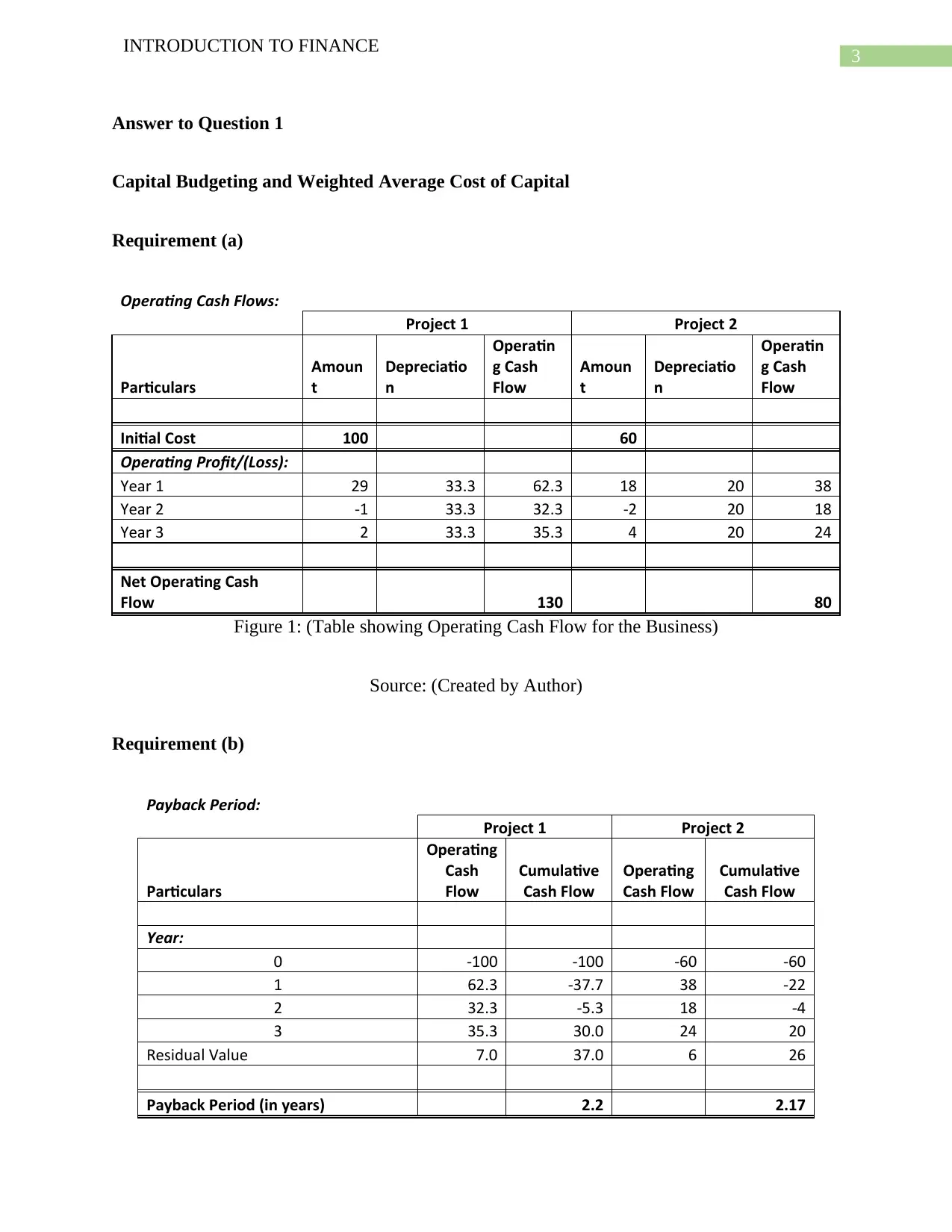

Answer to Question 1

Capital Budgeting and Weighted Average Cost of Capital

Requirement (a)

Operating Cash Flows:

Project 1 Project 2

Particulars

Amoun

t

Depreciatio

n

Operatin

g Cash

Flow

Amoun

t

Depreciatio

n

Operatin

g Cash

Flow

Initial Cost 100 60

Operating Profit/(Loss):

Year 1 29 33.3 62.3 18 20 38

Year 2 -1 33.3 32.3 -2 20 18

Year 3 2 33.3 35.3 4 20 24

Net Operating Cash

Flow 130 80

Figure 1: (Table showing Operating Cash Flow for the Business)

Source: (Created by Author)

Requirement (b)

Payback Period:

Project 1 Project 2

Particulars

Operating

Cash

Flow

Cumulative

Cash Flow

Operating

Cash Flow

Cumulative

Cash Flow

Year:

0 -100 -100 -60 -60

1 62.3 -37.7 38 -22

2 32.3 -5.3 18 -4

3 35.3 30.0 24 20

Residual Value 7.0 37.0 6 26

Payback Period (in years) 2.2 2.17

INTRODUCTION TO FINANCE

Answer to Question 1

Capital Budgeting and Weighted Average Cost of Capital

Requirement (a)

Operating Cash Flows:

Project 1 Project 2

Particulars

Amoun

t

Depreciatio

n

Operatin

g Cash

Flow

Amoun

t

Depreciatio

n

Operatin

g Cash

Flow

Initial Cost 100 60

Operating Profit/(Loss):

Year 1 29 33.3 62.3 18 20 38

Year 2 -1 33.3 32.3 -2 20 18

Year 3 2 33.3 35.3 4 20 24

Net Operating Cash

Flow 130 80

Figure 1: (Table showing Operating Cash Flow for the Business)

Source: (Created by Author)

Requirement (b)

Payback Period:

Project 1 Project 2

Particulars

Operating

Cash

Flow

Cumulative

Cash Flow

Operating

Cash Flow

Cumulative

Cash Flow

Year:

0 -100 -100 -60 -60

1 62.3 -37.7 38 -22

2 32.3 -5.3 18 -4

3 35.3 30.0 24 20

Residual Value 7.0 37.0 6 26

Payback Period (in years) 2.2 2.17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INTRODUCTION TO FINANCE

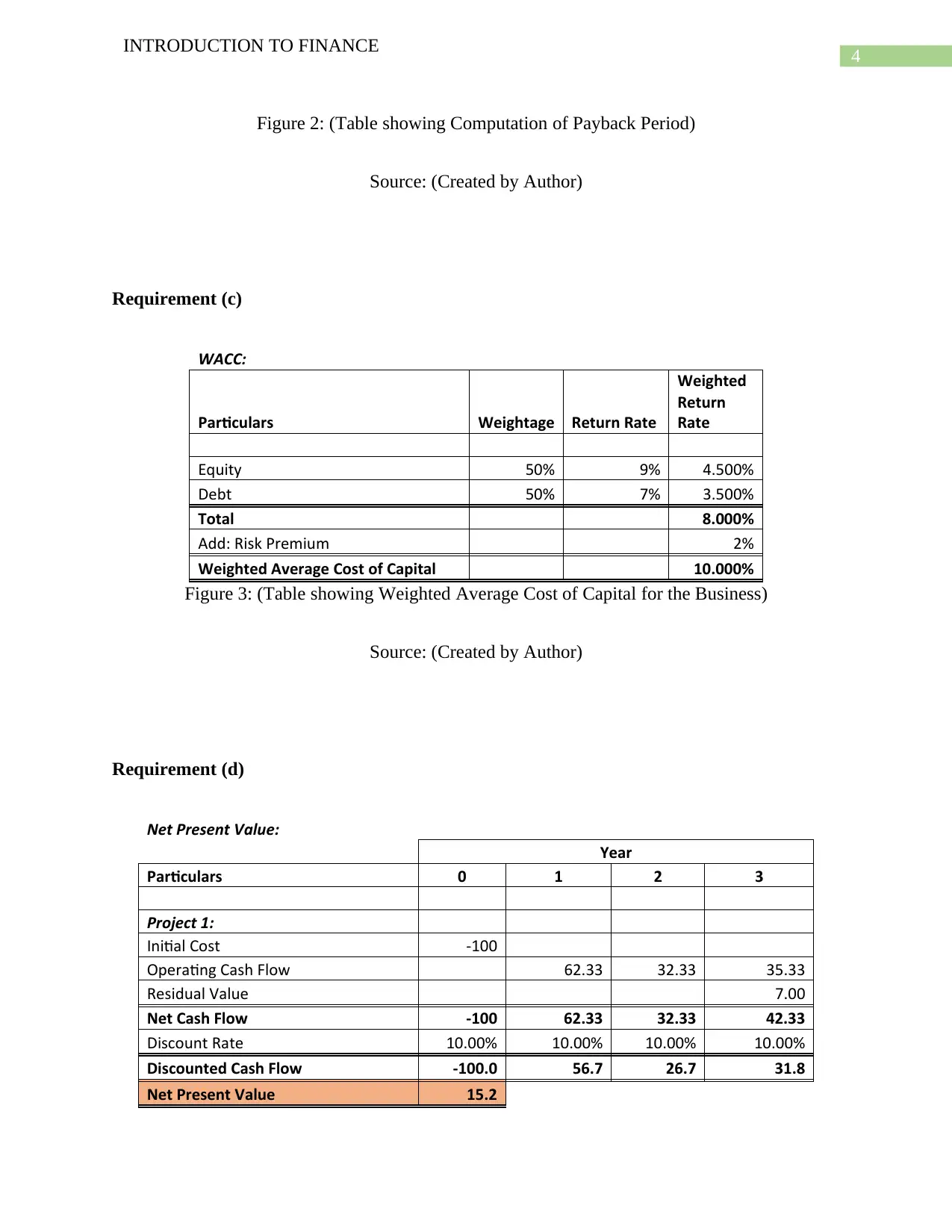

Figure 2: (Table showing Computation of Payback Period)

Source: (Created by Author)

Requirement (c)

WACC:

Particulars Weightage Return Rate

Weighted

Return

Rate

Equity 50% 9% 4.500%

Debt 50% 7% 3.500%

Total 8.000%

Add: Risk Premium 2%

Weighted Average Cost of Capital 10.000%

Figure 3: (Table showing Weighted Average Cost of Capital for the Business)

Source: (Created by Author)

Requirement (d)

Net Present Value:

Year

Particulars 0 1 2 3

Project 1:

Initial Cost -100

Operating Cash Flow 62.33 32.33 35.33

Residual Value 7.00

Net Cash Flow -100 62.33 32.33 42.33

Discount Rate 10.00% 10.00% 10.00% 10.00%

Discounted Cash Flow -100.0 56.7 26.7 31.8

Net Present Value 15.2

INTRODUCTION TO FINANCE

Figure 2: (Table showing Computation of Payback Period)

Source: (Created by Author)

Requirement (c)

WACC:

Particulars Weightage Return Rate

Weighted

Return

Rate

Equity 50% 9% 4.500%

Debt 50% 7% 3.500%

Total 8.000%

Add: Risk Premium 2%

Weighted Average Cost of Capital 10.000%

Figure 3: (Table showing Weighted Average Cost of Capital for the Business)

Source: (Created by Author)

Requirement (d)

Net Present Value:

Year

Particulars 0 1 2 3

Project 1:

Initial Cost -100

Operating Cash Flow 62.33 32.33 35.33

Residual Value 7.00

Net Cash Flow -100 62.33 32.33 42.33

Discount Rate 10.00% 10.00% 10.00% 10.00%

Discounted Cash Flow -100.0 56.7 26.7 31.8

Net Present Value 15.2

5

INTRODUCTION TO FINANCE

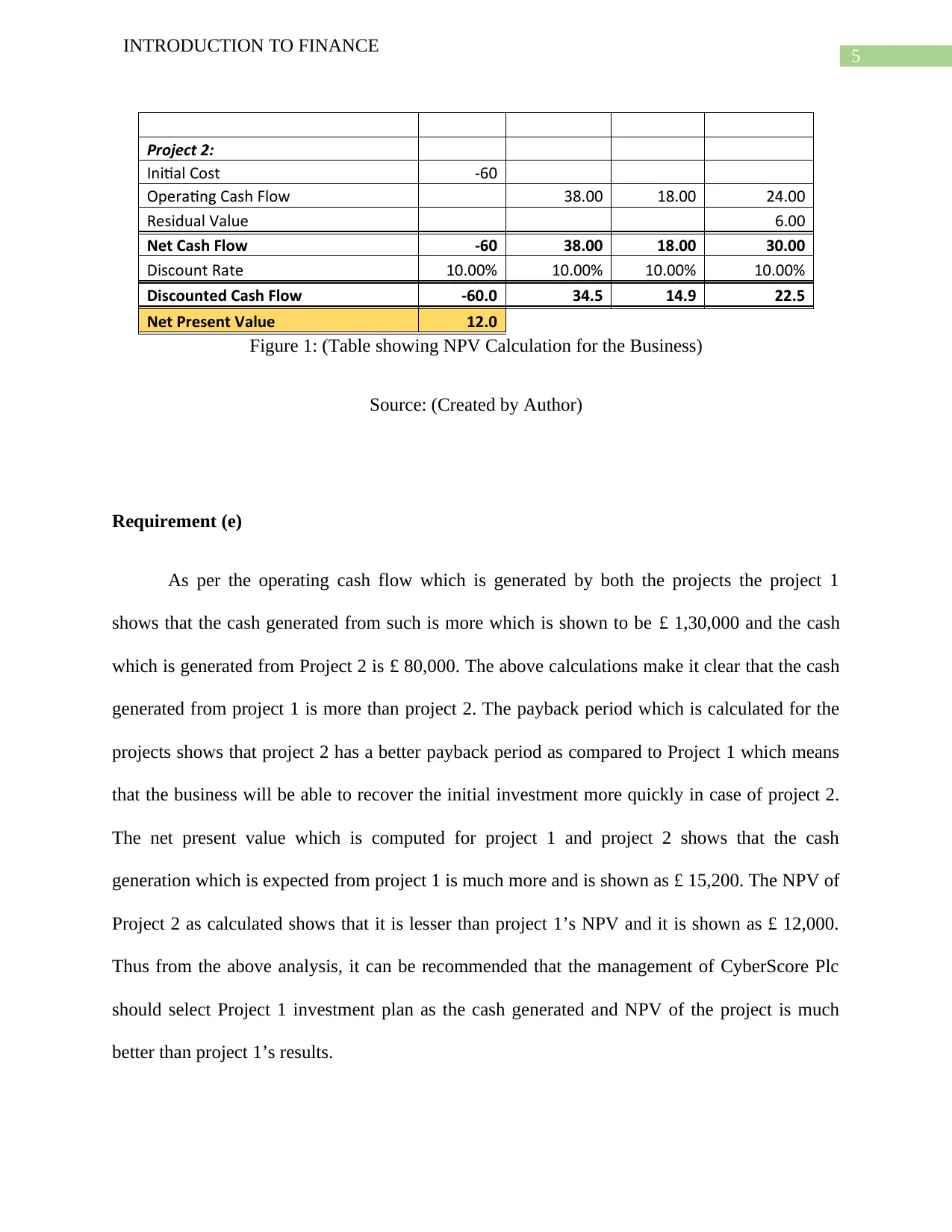

Project 2:

Initial Cost -60

Operating Cash Flow 38.00 18.00 24.00

Residual Value 6.00

Net Cash Flow -60 38.00 18.00 30.00

Discount Rate 10.00% 10.00% 10.00% 10.00%

Discounted Cash Flow -60.0 34.5 14.9 22.5

Net Present Value 12.0

Figure 1: (Table showing NPV Calculation for the Business)

Source: (Created by Author)

Requirement (e)

As per the operating cash flow which is generated by both the projects the project 1

shows that the cash generated from such is more which is shown to be £ 1,30,000 and the cash

which is generated from Project 2 is £ 80,000. The above calculations make it clear that the cash

generated from project 1 is more than project 2. The payback period which is calculated for the

projects shows that project 2 has a better payback period as compared to Project 1 which means

that the business will be able to recover the initial investment more quickly in case of project 2.

The net present value which is computed for project 1 and project 2 shows that the cash

generation which is expected from project 1 is much more and is shown as £ 15,200. The NPV of

Project 2 as calculated shows that it is lesser than project 1’s NPV and it is shown as £ 12,000.

Thus from the above analysis, it can be recommended that the management of CyberScore Plc

should select Project 1 investment plan as the cash generated and NPV of the project is much

better than project 1’s results.

INTRODUCTION TO FINANCE

Project 2:

Initial Cost -60

Operating Cash Flow 38.00 18.00 24.00

Residual Value 6.00

Net Cash Flow -60 38.00 18.00 30.00

Discount Rate 10.00% 10.00% 10.00% 10.00%

Discounted Cash Flow -60.0 34.5 14.9 22.5

Net Present Value 12.0

Figure 1: (Table showing NPV Calculation for the Business)

Source: (Created by Author)

Requirement (e)

As per the operating cash flow which is generated by both the projects the project 1

shows that the cash generated from such is more which is shown to be £ 1,30,000 and the cash

which is generated from Project 2 is £ 80,000. The above calculations make it clear that the cash

generated from project 1 is more than project 2. The payback period which is calculated for the

projects shows that project 2 has a better payback period as compared to Project 1 which means

that the business will be able to recover the initial investment more quickly in case of project 2.

The net present value which is computed for project 1 and project 2 shows that the cash

generation which is expected from project 1 is much more and is shown as £ 15,200. The NPV of

Project 2 as calculated shows that it is lesser than project 1’s NPV and it is shown as £ 12,000.

Thus from the above analysis, it can be recommended that the management of CyberScore Plc

should select Project 1 investment plan as the cash generated and NPV of the project is much

better than project 1’s results.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INTRODUCTION TO FINANCE

Answer to Question 2

Relation Between Corporate Governance and Corporate Social Responsibility

The term corporate Governance and Corporate Social Responsibility is used

simultaneously by many organization but there exists a major difference between the two

concepts. There exists a relationship between the two concepts but the same can be established if

the two concepts are understood in its full meaning. Corporate Governance may be defined as the

balance which the business needs to have between the economic goals and social goals and

between communal goals and individual goals (Tricker and Tricker 2015). The framework

establishes set of rules which facilitates efficient use of resources for the activities of the

business and the business accept full accountability for such activities. The aim of the corporate

governance framework is to promote ethical norms and align the interest of individuals

On the other hand, Corporate Social Responsibility states that the business should carry

our its operations in such a manner that is ethical and the activities of the business should affect

the ability of the future generation to produce similar profits. The concept is concerned with the

business acting in the best interest of the society and also maintain the ethical standards of the

business (Schwartz 2017). The concepts states that the business is responsible to the stakeholders

which includes creditors, investors, money lenders, suppliers and the society at large and always

act in the best interest of the society (Servaes and Tamayo 2013). The relationship which can be

established between Corporate Governance and Corporate Social Responsibility are discussed

below:

The CSR policies of the business are gradually be included in the Corporate Governance

Framework of the business.

INTRODUCTION TO FINANCE

Answer to Question 2

Relation Between Corporate Governance and Corporate Social Responsibility

The term corporate Governance and Corporate Social Responsibility is used

simultaneously by many organization but there exists a major difference between the two

concepts. There exists a relationship between the two concepts but the same can be established if

the two concepts are understood in its full meaning. Corporate Governance may be defined as the

balance which the business needs to have between the economic goals and social goals and

between communal goals and individual goals (Tricker and Tricker 2015). The framework

establishes set of rules which facilitates efficient use of resources for the activities of the

business and the business accept full accountability for such activities. The aim of the corporate

governance framework is to promote ethical norms and align the interest of individuals

On the other hand, Corporate Social Responsibility states that the business should carry

our its operations in such a manner that is ethical and the activities of the business should affect

the ability of the future generation to produce similar profits. The concept is concerned with the

business acting in the best interest of the society and also maintain the ethical standards of the

business (Schwartz 2017). The concepts states that the business is responsible to the stakeholders

which includes creditors, investors, money lenders, suppliers and the society at large and always

act in the best interest of the society (Servaes and Tamayo 2013). The relationship which can be

established between Corporate Governance and Corporate Social Responsibility are discussed

below:

The CSR policies of the business are gradually be included in the Corporate Governance

Framework of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

INTRODUCTION TO FINANCE

Both Corporate Governance and CSR policies of the business focuses on ethical

standards of the business and the responsiveness which the business has towards its

stakeholders and related to the environment where the business carries out its operations

(Cheng, Ioannou and Serafeim 2014).

Another similarity between the two concepts is that both Corporate Governance and CSR

policies of the business if effectively followed by the business results in building a better

reputation of the company in the market and is also directly related with the level of

performance which the business can achieve (Bhattacharya et al. 2015).

The policies which are associated with CSR is related with legal and regulatory

mechanisms whereas Corporate Governance is an effective control mechanism which the

company can develop within the scopa of which the company takes important decisions

of the business.

Performance Criteria of Non-Executive Director

The non-executive managers of the business are responsible for the overall management

of the business and are also members of the board of directors of the business. The performance

criteria of the non-executive director of the business are discussed below:

The non-executive directors of the business are responsible to make the executive

directors and the management responsible to the stakeholders of the business. The non-

executive directors of the business can supervise such accountability by taking part in the

meeting of the board of directors and formulation of company’s strategies.

The performance of the non-executive director can be judged by the level of

independence which he has in the management of the company. The non-executive

INTRODUCTION TO FINANCE

Both Corporate Governance and CSR policies of the business focuses on ethical

standards of the business and the responsiveness which the business has towards its

stakeholders and related to the environment where the business carries out its operations

(Cheng, Ioannou and Serafeim 2014).

Another similarity between the two concepts is that both Corporate Governance and CSR

policies of the business if effectively followed by the business results in building a better

reputation of the company in the market and is also directly related with the level of

performance which the business can achieve (Bhattacharya et al. 2015).

The policies which are associated with CSR is related with legal and regulatory

mechanisms whereas Corporate Governance is an effective control mechanism which the

company can develop within the scopa of which the company takes important decisions

of the business.

Performance Criteria of Non-Executive Director

The non-executive managers of the business are responsible for the overall management

of the business and are also members of the board of directors of the business. The performance

criteria of the non-executive director of the business are discussed below:

The non-executive directors of the business are responsible to make the executive

directors and the management responsible to the stakeholders of the business. The non-

executive directors of the business can supervise such accountability by taking part in the

meeting of the board of directors and formulation of company’s strategies.

The performance of the non-executive director can be judged by the level of

independence which he has in the management of the company. The non-executive

8

INTRODUCTION TO FINANCE

directors of the business are responsible for overall management of the company and also

involved in the decision-making process of the company (Bach 2013). The non-executive

directors of the business also need to ensure that the independence principle is not

affected in any way.

The performance of the non-executive directors of the business also depends on the time

which is spent by the directors in the overall and day to day management of the business.

The non-executive directors are expected to commit a significant amount of time in the

oversight of the business (Ntim et al. 2015). The non-executive directors of the business

are also expected to disclose any time commitments which the directors have during any

period.

The performance of the non-executive directors is also measured in terms of the valuable

inputs which they provide in the decision-making process of the business and their active

involvement in day to day management of the business.

In addition to this, the performance of the non-executive directors of the business is

anticipated to be resourceful and have external contacts which can be valuable for the

management of the business. The non-executive directors of the business are to suggest

all the business strategies which can be beneficial for the business.

Answer to Question 3

Advantages of Traditional Budgeting

Traditional Budgeting may be defined as the process wherein the last year’s budget is

taken as a base in order to prepare the current year’s budget. The management only makes

necessary changes in the previous budgets and this prepares the current year’s budget of the

INTRODUCTION TO FINANCE

directors of the business are responsible for overall management of the company and also

involved in the decision-making process of the company (Bach 2013). The non-executive

directors of the business also need to ensure that the independence principle is not

affected in any way.

The performance of the non-executive directors of the business also depends on the time

which is spent by the directors in the overall and day to day management of the business.

The non-executive directors are expected to commit a significant amount of time in the

oversight of the business (Ntim et al. 2015). The non-executive directors of the business

are also expected to disclose any time commitments which the directors have during any

period.

The performance of the non-executive directors is also measured in terms of the valuable

inputs which they provide in the decision-making process of the business and their active

involvement in day to day management of the business.

In addition to this, the performance of the non-executive directors of the business is

anticipated to be resourceful and have external contacts which can be valuable for the

management of the business. The non-executive directors of the business are to suggest

all the business strategies which can be beneficial for the business.

Answer to Question 3

Advantages of Traditional Budgeting

Traditional Budgeting may be defined as the process wherein the last year’s budget is

taken as a base in order to prepare the current year’s budget. The management only makes

necessary changes in the previous budgets and this prepares the current year’s budget of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

INTRODUCTION TO FINANCE

business. For the preparation of such a budget the management considers factors such as

inflation rate, consumer demand and the present market situation (Réka, Ştefan and Daniel

2014).

The advantages which can be effectively pointed out for traditional budgets are explained

below in details:

Framework of Control: The most common advantage of any budgets is that it can be

used as a tool for exercising control over the business and also be used form

measuring the performance of the business. In other words traditional budgeting

forms a framework of control which can be help the management to promote

effectiveness of the management process and also manage the activities of the

business much easier and also promote stability.

Forms a part of the organizational Culture: The budgets which are prepared by the

management forms a part of the organizational culture of the business. Budgeting

practices are widely used in the business and also universally applicable to every

department of the company. Traditional Budgeting is still widely used in finance, cost

and operations department and forms a part of the regular activity of the business

(Sandalgaard and Nikolaj Bukh 2014).

Planning and Forecasting: Traditional Budgeting enables the business to forecast the

expenses and revenues which the business expects to generate during the year and

also facilitates comparison between the actuals results of the previous year (Dudin et

al. 2015). The budgets are considered to be important tools with the help of which the

management can exercise control and also measure the performance of the business.

INTRODUCTION TO FINANCE

business. For the preparation of such a budget the management considers factors such as

inflation rate, consumer demand and the present market situation (Réka, Ştefan and Daniel

2014).

The advantages which can be effectively pointed out for traditional budgets are explained

below in details:

Framework of Control: The most common advantage of any budgets is that it can be

used as a tool for exercising control over the business and also be used form

measuring the performance of the business. In other words traditional budgeting

forms a framework of control which can be help the management to promote

effectiveness of the management process and also manage the activities of the

business much easier and also promote stability.

Forms a part of the organizational Culture: The budgets which are prepared by the

management forms a part of the organizational culture of the business. Budgeting

practices are widely used in the business and also universally applicable to every

department of the company. Traditional Budgeting is still widely used in finance, cost

and operations department and forms a part of the regular activity of the business

(Sandalgaard and Nikolaj Bukh 2014).

Planning and Forecasting: Traditional Budgeting enables the business to forecast the

expenses and revenues which the business expects to generate during the year and

also facilitates comparison between the actuals results of the previous year (Dudin et

al. 2015). The budgets are considered to be important tools with the help of which the

management can exercise control and also measure the performance of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INTRODUCTION TO FINANCE

Facilitates Decentralization: Some of the industries which are operating such as

banking sector and other financial organization recognizes that the business will

greatly benefit if the business is allowed to be decentralize (Wildavsky 2017).

Therefore, the method of budgeting and budget cost centers give the managers the

freedom to run their business as per the planned process and also ensure that the

management is pursuing the goals which are established by the business.

Other advantages: In addition to the above mention advantages, there are also certain

mixed advantages which traditional budgeting system provides in a business. The

system of budgeting provides the business an opportunity to plan for all contingencies

or losses which the business faces effectively (Lorain, García Domonte and Sastre

Peláez 2015). The budgets which are prepared by the management provides a general

guideline on the basis of which various departments in the business can stick the plan

of the management while conducting day to day operations of the business.

Limitations of Traditional Budgeting System

The traditional budgeting system also faces certain limitations which are discussed below

in details:

Inefficiency: The formulation of a traditional budgets takes too much time of the

management and also the resources available to the company is also utilized in excess.

The time which is spent in the preparation of the budget is not considered to be

productive time used by the management by a majority member of the business (Zeller

and Metzger 2013). The main reasons for the excess time which is taken for the

INTRODUCTION TO FINANCE

Facilitates Decentralization: Some of the industries which are operating such as

banking sector and other financial organization recognizes that the business will

greatly benefit if the business is allowed to be decentralize (Wildavsky 2017).

Therefore, the method of budgeting and budget cost centers give the managers the

freedom to run their business as per the planned process and also ensure that the

management is pursuing the goals which are established by the business.

Other advantages: In addition to the above mention advantages, there are also certain

mixed advantages which traditional budgeting system provides in a business. The

system of budgeting provides the business an opportunity to plan for all contingencies

or losses which the business faces effectively (Lorain, García Domonte and Sastre

Peláez 2015). The budgets which are prepared by the management provides a general

guideline on the basis of which various departments in the business can stick the plan

of the management while conducting day to day operations of the business.

Limitations of Traditional Budgeting System

The traditional budgeting system also faces certain limitations which are discussed below

in details:

Inefficiency: The formulation of a traditional budgets takes too much time of the

management and also the resources available to the company is also utilized in excess.

The time which is spent in the preparation of the budget is not considered to be

productive time used by the management by a majority member of the business (Zeller

and Metzger 2013). The main reasons for the excess time which is taken for the

11

INTRODUCTION TO FINANCE

preparation of the budget can be due to the use of spreadsheets or complex computer-

based software which involves manual entry of data.

Low Change Responsiveness: Any changes which occurs in the market or business

position or budgeting cycle of the business than such changes makes the budget obsolete

in nature. This is due to the fact that the management is unable to incorporate changes in

the budgets which are already prepared by the business. The management is unable to

make regular reviews as the process is very much time consuming in nature. Thus, the

management of the company cannot spend time in resources in updating a budget which

has been affected by changes.

Failure to Motivate Desired Behavior: The traditional budgeting system is not much of a

help when it comes to motivate the employees of the business. The budgets which are

prepared by the business is fixed or flexible but the standard sets are high and from the

view point of the employees are not achievable. This leads to demotivation on the part of

the employees of the business.

Disconnection with Strategic Plan: In many cases the management is so much concerned

with the numbers which are set form the various departments to achieve that the

management of the company misses out the basic purpose which is there for preparation

of the budgets in the first place (Pietrzak 2013). Budgets are generally prepared in order

to ensure that the strategic plans and goals of the business are followed and ultimately

achieved keeping the budgets as the base or guideline. Traditional budgets focus more on

costs reductions for the business rather than value creation for the business which

suggests that the business does not focuses on the strategic plans of the business and such

plans are not given priority.

INTRODUCTION TO FINANCE

preparation of the budget can be due to the use of spreadsheets or complex computer-

based software which involves manual entry of data.

Low Change Responsiveness: Any changes which occurs in the market or business

position or budgeting cycle of the business than such changes makes the budget obsolete

in nature. This is due to the fact that the management is unable to incorporate changes in

the budgets which are already prepared by the business. The management is unable to

make regular reviews as the process is very much time consuming in nature. Thus, the

management of the company cannot spend time in resources in updating a budget which

has been affected by changes.

Failure to Motivate Desired Behavior: The traditional budgeting system is not much of a

help when it comes to motivate the employees of the business. The budgets which are

prepared by the business is fixed or flexible but the standard sets are high and from the

view point of the employees are not achievable. This leads to demotivation on the part of

the employees of the business.

Disconnection with Strategic Plan: In many cases the management is so much concerned

with the numbers which are set form the various departments to achieve that the

management of the company misses out the basic purpose which is there for preparation

of the budgets in the first place (Pietrzak 2013). Budgets are generally prepared in order

to ensure that the strategic plans and goals of the business are followed and ultimately

achieved keeping the budgets as the base or guideline. Traditional budgets focus more on

costs reductions for the business rather than value creation for the business which

suggests that the business does not focuses on the strategic plans of the business and such

plans are not given priority.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.