Finance Case Study: Investment Options, Bond Valuation, and Sukuk

VerifiedAdded on 2022/12/20

|7

|1725

|1

Case Study

AI Summary

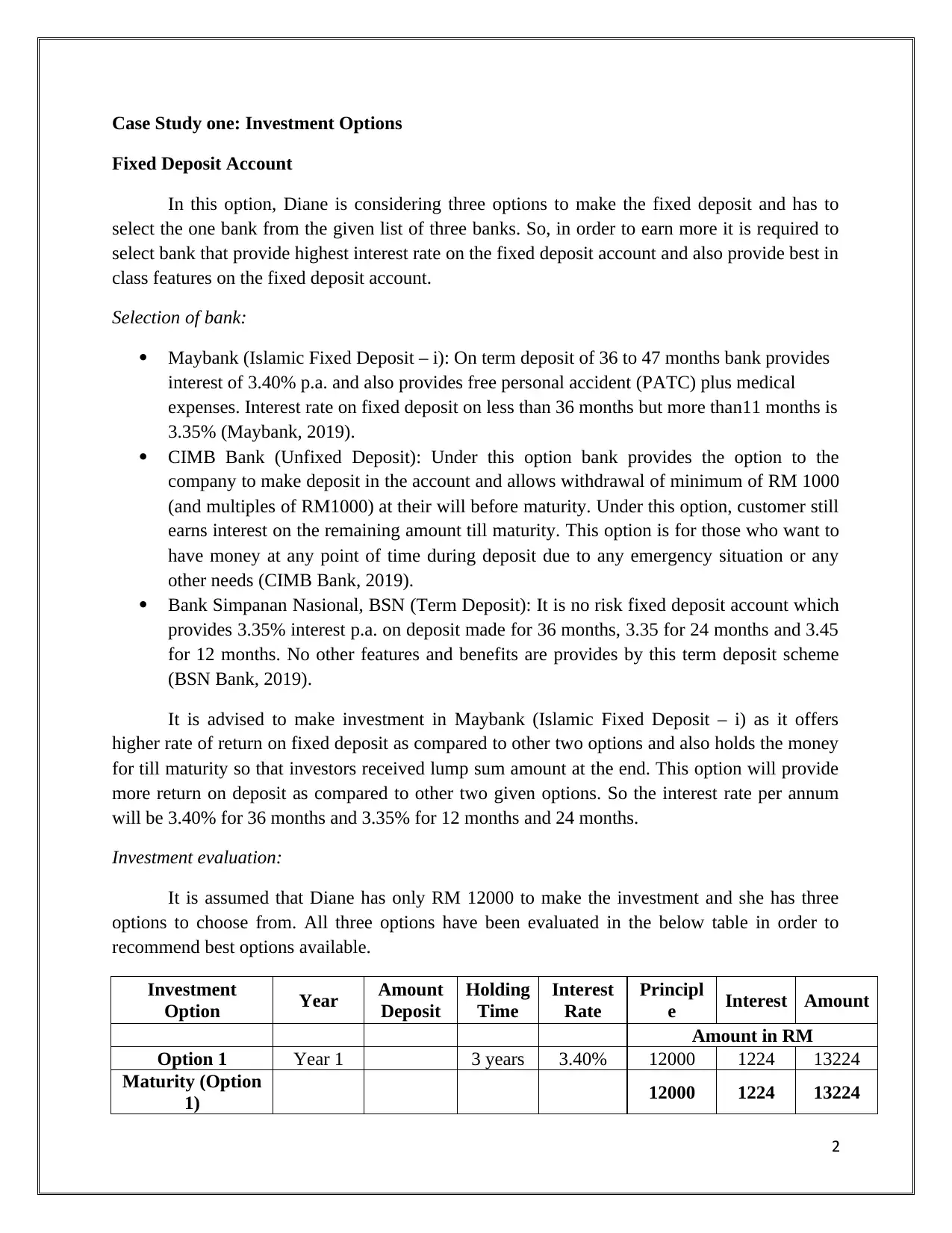

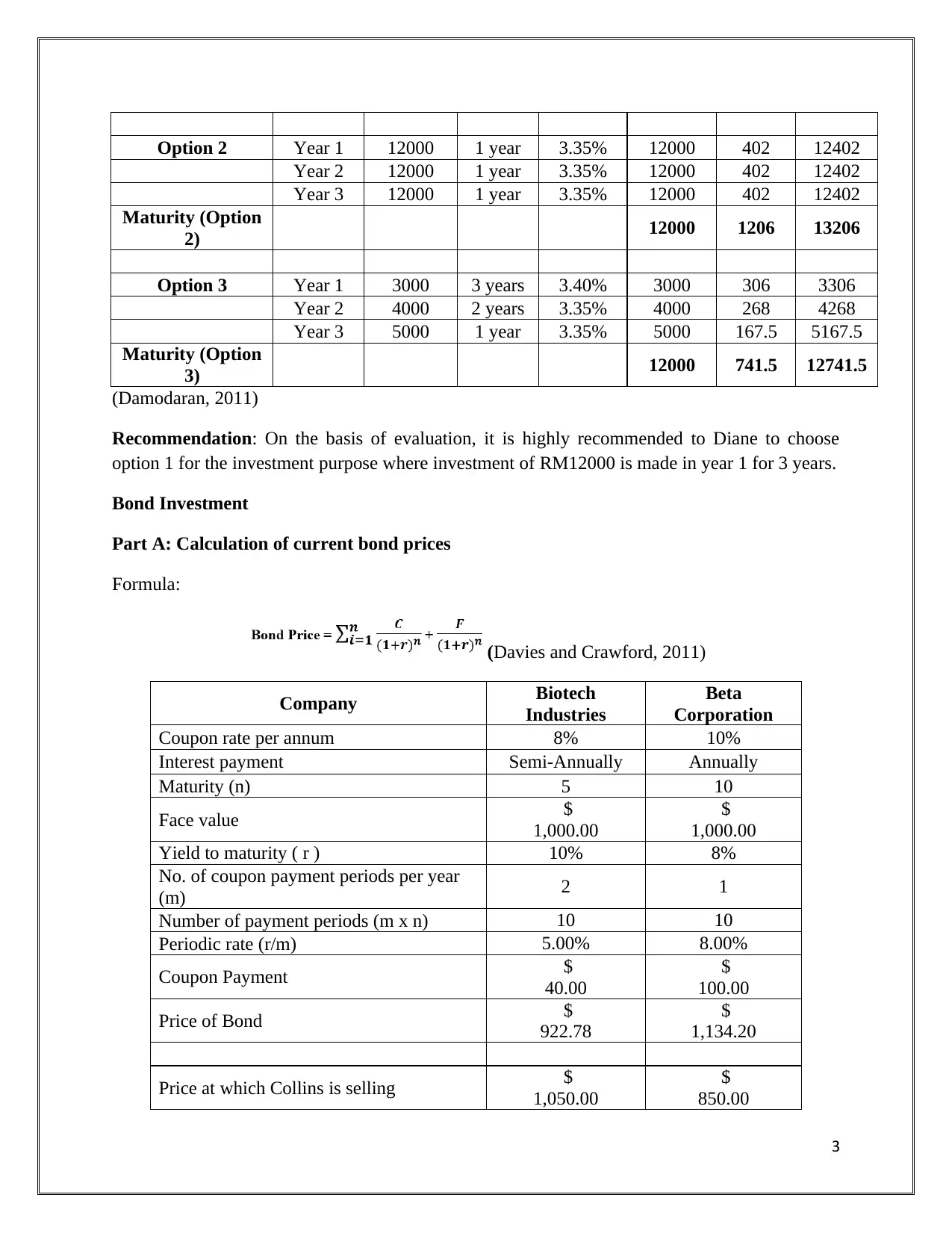

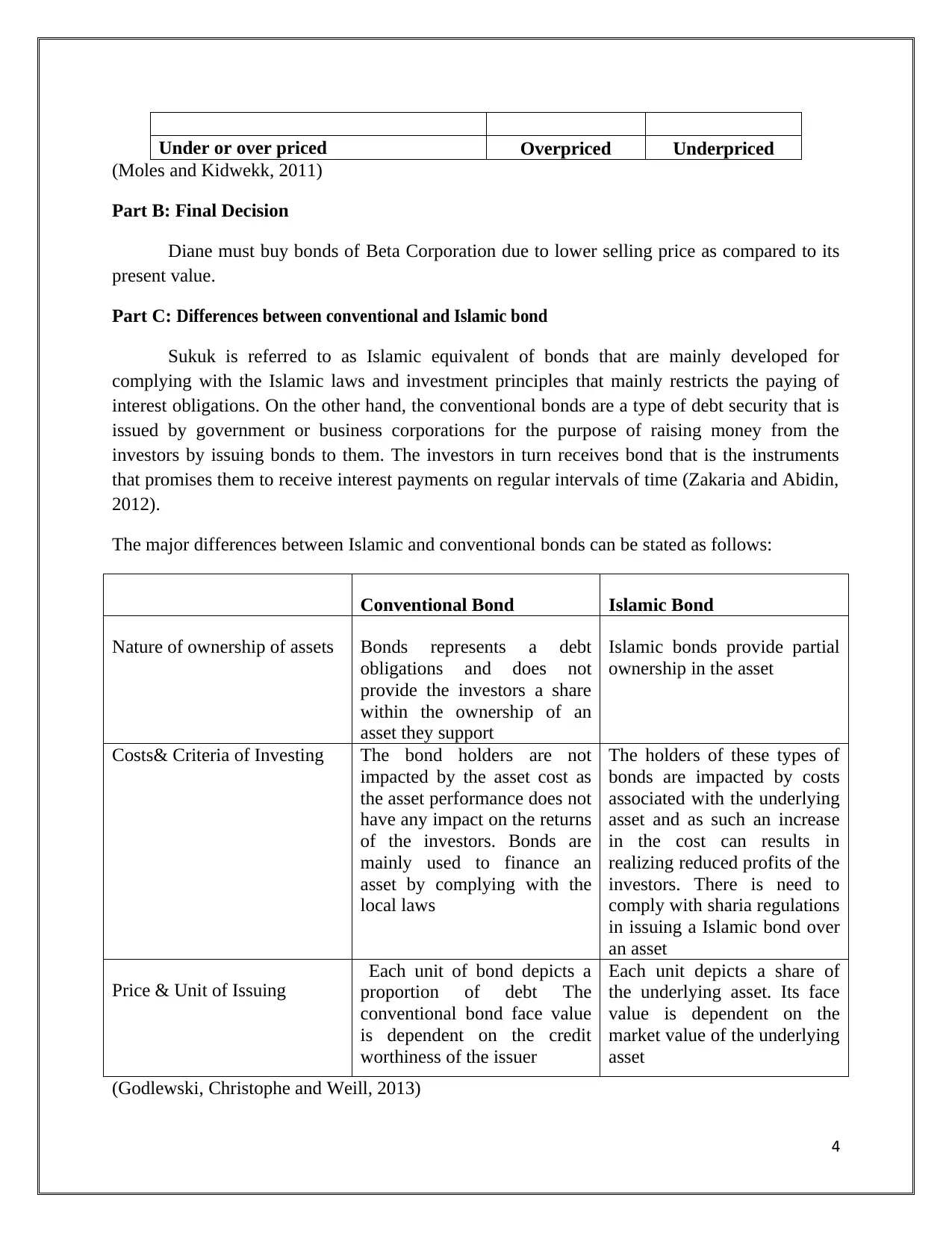

This individual assignment for FIN40104 focuses on financial analysis through two case studies. The first case study evaluates investment options for a fixed deposit account, comparing Maybank, CIMB Bank, and Bank Simpanan Nasional, and recommending the most profitable choice based on interest rates and features. It also includes calculations of current bond prices for Biotech Industries and Beta Corporation, determining whether bonds are under- or overpriced, and a comparison of conventional and Islamic bonds (Sukuk). The second case study examines financing options for a company expanding its manufacturing operations, analyzing the use of bank loans and bonds as sources of debt financing, and highlighting their advantages within a capital structure framework. The assignment draws on various financial concepts and theories, including interest rate calculations, bond valuation formulas, and the differences between conventional and Islamic financial instruments, and provides recommendations based on the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.