FIN5006 British Taxation: Comprehensive Analysis of Tax Liabilities

VerifiedAdded on 2023/06/18

|8

|1018

|239

Homework Assignment

AI Summary

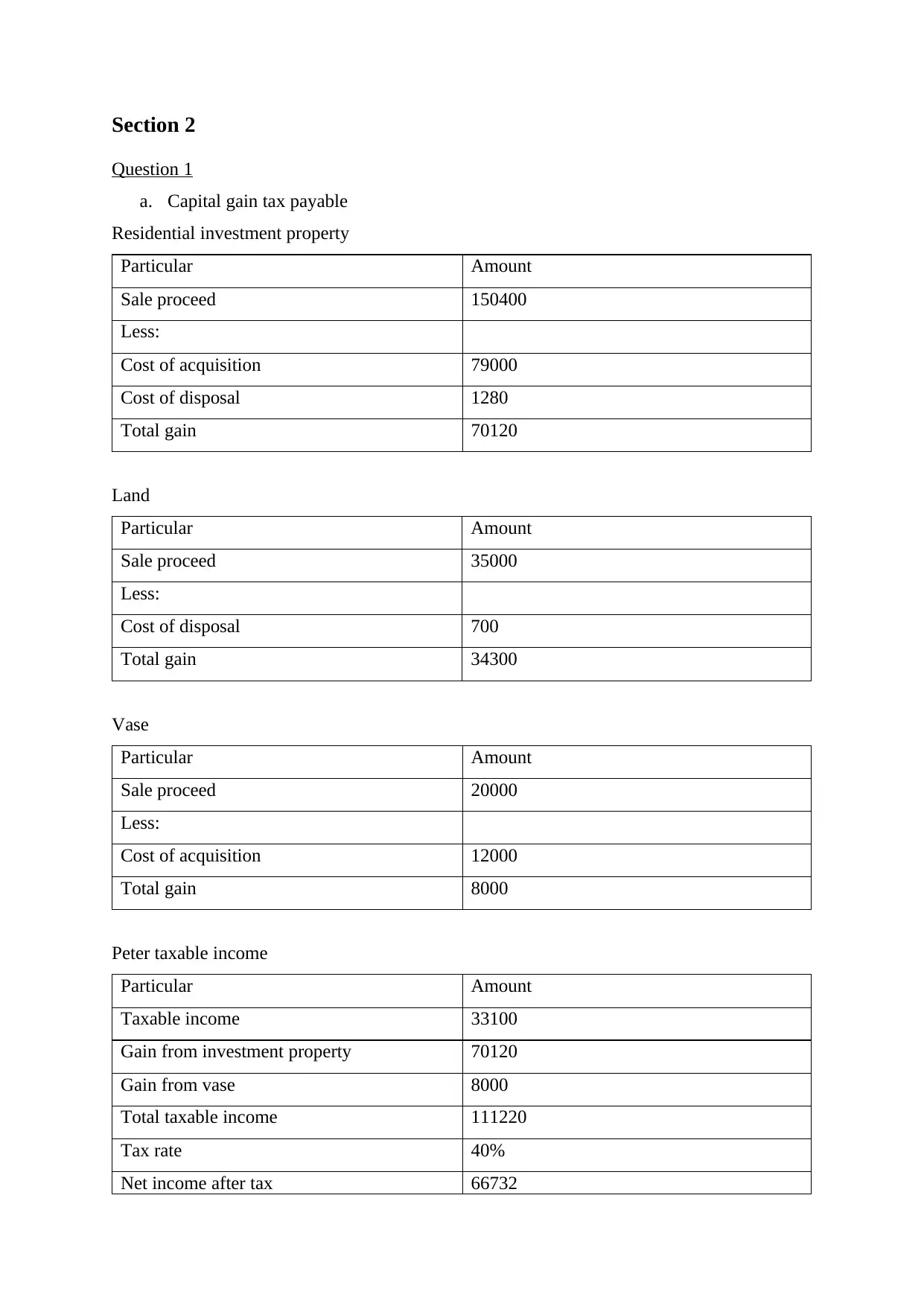

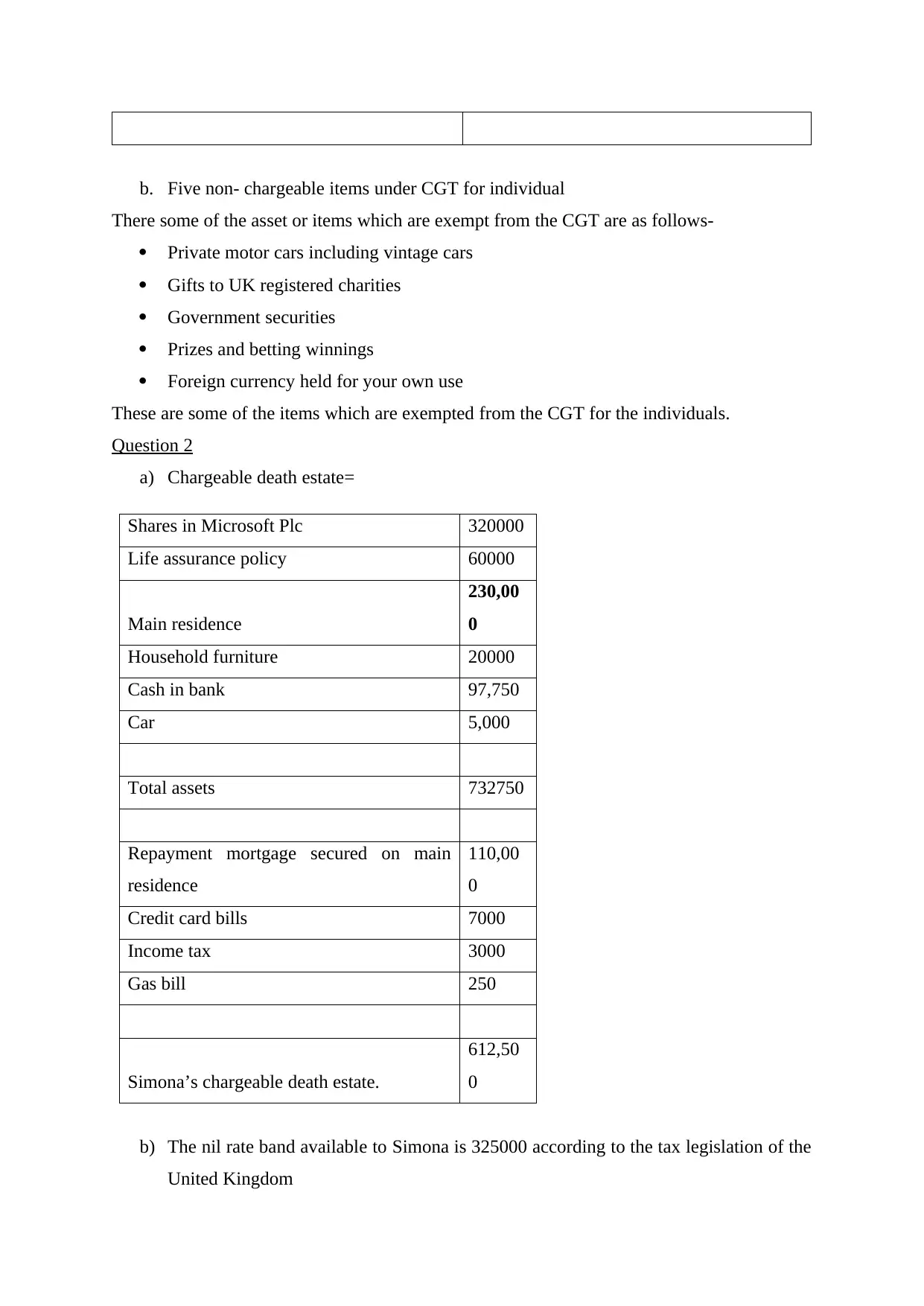

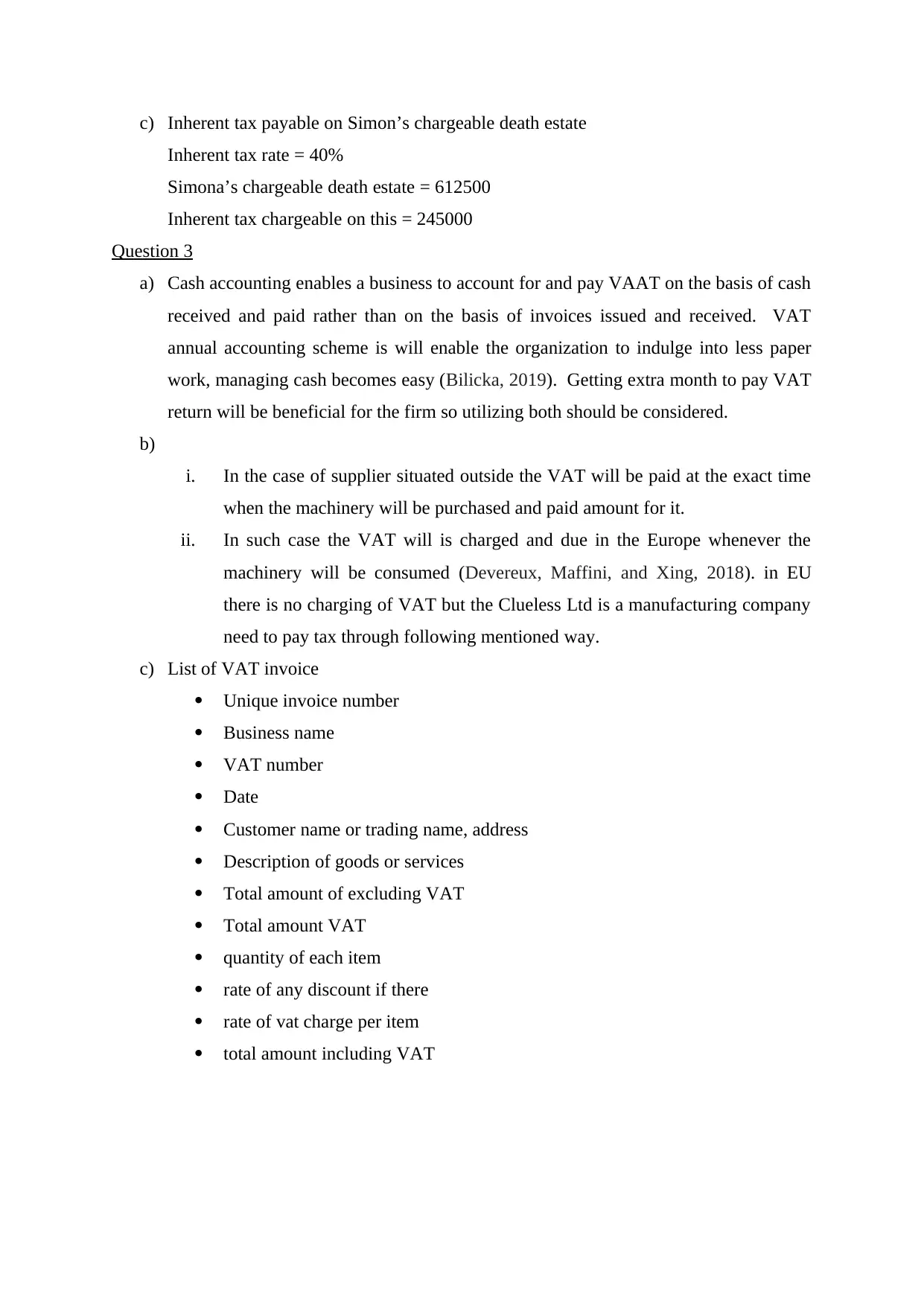

This assignment solution provides a detailed analysis of British taxation, covering key areas such as income tax for self-employed individuals and employees, corporation tax liabilities, capital gains tax (CGT) implications for individuals, and inheritance tax. It includes computations for taxable trading profits, class 1, 2, and 4 National Insurance Contributions (NIC), and corporation tax rates. Furthermore, the assignment addresses CGT exemptions, inheritance tax nil rate bands, and VAT considerations for businesses, including cash accounting and VAT invoice requirements. The solutions are based on current UK tax legislation and include calculations and explanations to meet the assignment's learning outcomes. Desklib offers more solved assignments and resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.