FINA200 Fall 2018: Personal Finance, Investment & Retirement Case

VerifiedAdded on 2023/05/30

|9

|2459

|411

Case Study

AI Summary

This FINA200 Personal Finance case study from Fall 2018 explores various financial planning scenarios. It includes multiple-choice questions and mini-cases covering topics such as the Home Buyer’s Plan (HBP), mutual fund investments, Management Expense Ratios (MER), Term to 100 insurance, and credit scores. The mini-cases delve into TFSA contributions, capital gains calculations, OAS claw-backs, estate planning issues, and mortgage calculations including down payments, loan-to-value ratios, and mortgage default insurance. The solutions provide detailed calculations and explanations for each scenario, offering insights into investment decisions, tax implications, and retirement planning strategies. The document also includes relevant tax tables and time value of money formulas to aid in problem-solving. This assignment is available on Desklib, where students can find more solved assignments and past papers.

Page 1 of 9

Section I: Six (6) Multiple-Choice Questions (6 marks - 1 mark each)

Highlight your response.

1) Neil and Sandra each borrowed from their Registered Retirement Savings Plan (RRSP) under

the Home Buyer’s Plan (HBP) for the down payment on the purchase of their first home. If Neil

and Sandra withdrew the maximum that is permitted under the HBP program, and have a

conventional mortgage (minimum required), what is the value of the home that they are

looking to purchase?

a) $250,000

b) $275,000

c) $125,000

d) $100,000

e) $150,000

2) Jake is looking to invest $15,000 in XYZ mutual fund, how many mutual fund shares could he

purchase if the Net Asset Value (NAV) of the fund was $43, and the fund had a front-end load

of 3%?

a) 328 shares

b) 323 shares

c) 349 shares

d) 338 shares

e) 330 shares

3) The Management Expense Ratio (MER) for mutual funds states how much you pay a fund in

percentage terms every year to manage your money. As the percentage appears small, most

do not notice it, but Canadians have the highest average MER’s and these fees take a bite into

returns. If you invested $15,000 in the Bank of Montreal BMO US Equity A mutual fund, how

much are you paying the fund to manage your money? (Go to www.morningstar.ca, a great

investment research site; find the mutual fund BMO US Equity A to respond to the mutual

fund question.)

a) $500.00

b) $275.50

c) $373.50

d) $250.35

e) $150.75

4) Heidi is looking to invest in the Bank of Montreal BMO US Equity A mutual fund. She knows

that it takes a minimum of $500 as the initial investment to get into the fund but is wondering

what the minimum investment thereafter is as well as the 8th top investment holding? (Go to

www.morningstar.ca, a great investment research site; find the mutual fund BMO US Equity A

to respond to the mutual fund question.)

a) $50CAD; Apple Inc.

b) $500CAD; Apple Inc.

c) $50US; Microsoft Corp.

d) $500US; Alphabet Inc.

e) $50CAD; Walmart Inc.

Section I: Six (6) Multiple-Choice Questions (6 marks - 1 mark each)

Highlight your response.

1) Neil and Sandra each borrowed from their Registered Retirement Savings Plan (RRSP) under

the Home Buyer’s Plan (HBP) for the down payment on the purchase of their first home. If Neil

and Sandra withdrew the maximum that is permitted under the HBP program, and have a

conventional mortgage (minimum required), what is the value of the home that they are

looking to purchase?

a) $250,000

b) $275,000

c) $125,000

d) $100,000

e) $150,000

2) Jake is looking to invest $15,000 in XYZ mutual fund, how many mutual fund shares could he

purchase if the Net Asset Value (NAV) of the fund was $43, and the fund had a front-end load

of 3%?

a) 328 shares

b) 323 shares

c) 349 shares

d) 338 shares

e) 330 shares

3) The Management Expense Ratio (MER) for mutual funds states how much you pay a fund in

percentage terms every year to manage your money. As the percentage appears small, most

do not notice it, but Canadians have the highest average MER’s and these fees take a bite into

returns. If you invested $15,000 in the Bank of Montreal BMO US Equity A mutual fund, how

much are you paying the fund to manage your money? (Go to www.morningstar.ca, a great

investment research site; find the mutual fund BMO US Equity A to respond to the mutual

fund question.)

a) $500.00

b) $275.50

c) $373.50

d) $250.35

e) $150.75

4) Heidi is looking to invest in the Bank of Montreal BMO US Equity A mutual fund. She knows

that it takes a minimum of $500 as the initial investment to get into the fund but is wondering

what the minimum investment thereafter is as well as the 8th top investment holding? (Go to

www.morningstar.ca, a great investment research site; find the mutual fund BMO US Equity A

to respond to the mutual fund question.)

a) $50CAD; Apple Inc.

b) $500CAD; Apple Inc.

c) $50US; Microsoft Corp.

d) $500US; Alphabet Inc.

e) $50CAD; Walmart Inc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section II: Five (5) Mini-Cases (14 marks)

Please write (or highlight, where required) your response in the template or space

provided.

Mini-Case A:

Question 1: (3 marks)

Rory had always maximized his yearly contributions to his Tax-Free Savings Account (TFSA), including

his latest contribution on February 1, 2018. He was going to use this money to finance his first home.

This account only held one stock which he knew was risky but felt that it was the only way to ever

own a home. Unfortunately, instead of having it grow to $200,000 like he had hoped, he lost all of his

money with the company going bankrupt on November 15, 2018.

a) What is the earliest date that Rory can start to recontribute to his TFSA without triggering a

penalty? (1 mark)

January 1, 2019___________________________________________

b) Based on your response regarding the date in a), what is the amount that Rory can contribute

to his TFSA? (1 mark)

$5,500_____________________________________________________________________

Page 2 of 9

5) Which statement is incorrect with regards to Term To 100 Insurance?

a) Permanent life insurance policy

b) Policy does not build cash value

c) Pay more for premiums as you age

d) No longer need to pay premiums if the policyholder lives past the age of 100

e) Premium does not include a savings component

6) Which of the following can influence your credit score?

a) Sex

b) Race

c) Length of relationship with creditors

d) Religion

e) Marital status

Section I completed, continue to Section II.

Please write (or highlight, where required) your response in the template or space

provided.

Mini-Case A:

Question 1: (3 marks)

Rory had always maximized his yearly contributions to his Tax-Free Savings Account (TFSA), including

his latest contribution on February 1, 2018. He was going to use this money to finance his first home.

This account only held one stock which he knew was risky but felt that it was the only way to ever

own a home. Unfortunately, instead of having it grow to $200,000 like he had hoped, he lost all of his

money with the company going bankrupt on November 15, 2018.

a) What is the earliest date that Rory can start to recontribute to his TFSA without triggering a

penalty? (1 mark)

January 1, 2019___________________________________________

b) Based on your response regarding the date in a), what is the amount that Rory can contribute

to his TFSA? (1 mark)

$5,500_____________________________________________________________________

Page 2 of 9

5) Which statement is incorrect with regards to Term To 100 Insurance?

a) Permanent life insurance policy

b) Policy does not build cash value

c) Pay more for premiums as you age

d) No longer need to pay premiums if the policyholder lives past the age of 100

e) Premium does not include a savings component

6) Which of the following can influence your credit score?

a) Sex

b) Race

c) Length of relationship with creditors

d) Religion

e) Marital status

Section I completed, continue to Section II.

c) Since Rory lost all of his money in his TFSA, he has decided to use the money from his

Registered Retirement Savings Plan (RRSP) and withdraw the maximum under the Home

Buyer’s Plan (HBP) for a down payment on his first home. What is the maximum that Rory can

withdraw from his RRSP under the HBP? (.5 mark)

$ 25,000______________________________________________________________

d) Under the Home Buyer’s Plan (HBP), what is the minimum that Rory must pay back each year

into his RRSP?

(.5 mark)

$1,666.67____________________________________________________________________

Mini-Case B:

Question 1: (2 marks – 1 mark each)

On December 1, 2017, Jacky purchased 10,000 shares of the CIBC Dividend Growth fund for

$12,300; in addition, she had to pay a commission of $50 on the purchase date. She decided to sell it

a year later when the share price rose to $5/share. She was however disappointed to hear that she

had to again pay another commission of $55 on the sale.

a) Calculate her capital gain and her taxable capital gain. (1 mark - .5 mark each)

Calculation of the capital gain: (.5 mark)

Capital gains = 50000 – 12300 – 50 -55 = $ 37,595

Calculation of the taxable capital gain: (.5 mark)

Since, only 50% of capital gains are included, hence taxable capital gains = 0.5*37,595 =

$18,797.50

b) Jacky had a net capital loss of $2,500 (capital loss of $5,000) from a previous year. Taking

Jacky’s information in 1a) and the net capital loss into consideration, if Jacky is in a 41%

marginal tax bracket, what is the amount of tax that Jacky would pay on the sale of CIBC

Dividend Growth? (1 mark)

Taxes payable calculation: (1 mark)

Net taxable capital gains in current year = 18797.50 – 2500 = $16.297.5

Amount of tax paid on the sale of CIBC dividend growth = 0.41*$16.297.5 = $6,681.98

Mini-Case C:

Question 1: (5 marks)

Gerry retired from IBM on January 1, 2018 at age 65 where he had worked in the Montreal office

since he was 20 years old. He has a few questions for you as he heard that you were taking a Personal

Finance course at Concordia.

a) Gerry’s IBM pension is $80,000/year, his annual Quebec Pension Plan (QPP) is $12,000

and his annual Old Age Security pension is $7,000. He is concerned about the Old Age

Page 3 of 9

Registered Retirement Savings Plan (RRSP) and withdraw the maximum under the Home

Buyer’s Plan (HBP) for a down payment on his first home. What is the maximum that Rory can

withdraw from his RRSP under the HBP? (.5 mark)

$ 25,000______________________________________________________________

d) Under the Home Buyer’s Plan (HBP), what is the minimum that Rory must pay back each year

into his RRSP?

(.5 mark)

$1,666.67____________________________________________________________________

Mini-Case B:

Question 1: (2 marks – 1 mark each)

On December 1, 2017, Jacky purchased 10,000 shares of the CIBC Dividend Growth fund for

$12,300; in addition, she had to pay a commission of $50 on the purchase date. She decided to sell it

a year later when the share price rose to $5/share. She was however disappointed to hear that she

had to again pay another commission of $55 on the sale.

a) Calculate her capital gain and her taxable capital gain. (1 mark - .5 mark each)

Calculation of the capital gain: (.5 mark)

Capital gains = 50000 – 12300 – 50 -55 = $ 37,595

Calculation of the taxable capital gain: (.5 mark)

Since, only 50% of capital gains are included, hence taxable capital gains = 0.5*37,595 =

$18,797.50

b) Jacky had a net capital loss of $2,500 (capital loss of $5,000) from a previous year. Taking

Jacky’s information in 1a) and the net capital loss into consideration, if Jacky is in a 41%

marginal tax bracket, what is the amount of tax that Jacky would pay on the sale of CIBC

Dividend Growth? (1 mark)

Taxes payable calculation: (1 mark)

Net taxable capital gains in current year = 18797.50 – 2500 = $16.297.5

Amount of tax paid on the sale of CIBC dividend growth = 0.41*$16.297.5 = $6,681.98

Mini-Case C:

Question 1: (5 marks)

Gerry retired from IBM on January 1, 2018 at age 65 where he had worked in the Montreal office

since he was 20 years old. He has a few questions for you as he heard that you were taking a Personal

Finance course at Concordia.

a) Gerry’s IBM pension is $80,000/year, his annual Quebec Pension Plan (QPP) is $12,000

and his annual Old Age Security pension is $7,000. He is concerned about the Old Age

Page 3 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Security (OAS) claw-back. Calculate if Gerry will be impacted by the OAS claw-back and if

so, the amount of repayment? (1 mark - .5 mark each)

Gerry’s calculation: (1 mark - .5 mark each)

Gerry would be impacted by the OAS claw-back since the taxable income of Gerry tends to

exceed the minimum threshold value.

Total taxable income = 80000 + 12000 + 7000 = $ 99,000

For the period between July 2017 to July 2018, the minimum threshold is $73,756.

Hence, repayment under claw-back = (99000- 73,756)*15% = $3,786.6 per annum

b) Gerry has not done any Estate planning since his wife died 10 years ago but since his

three adult children are no longer on speaking terms, he thought it would be a good idea

to write a Will. He knows that his handwriting is not the greatest but figures that his kids

will finally come together to try to figure it out. Gerry hid the Will in a coat pocket deep

inside his closet; he chose a coat that he no longer wears. Gerry named his best friend Alf

as Liquidator but has not yet told him nor has he told him where the Will is, as Alf is 85

years old and hasn’t been feeling well lately. Gerry also put precious coins that he has

been collecting in the lining of the same coat.

Give six (6) problems that could arise?

(3 marks - .5 marks each)

1) Alf may not survive when there is a need to execute the will.

2) Alf may not want to act as the liquidator as consent has not been obtained and Gerry has

not been obtained Alf about the will.

3) Considering the will is hidden in a coat pocket which he longer wears and this coat is kept

deep in the closet, it may be assumed that no will actually exists.

4) The will may not be considered as legal considering that it has not been signed by any

witnesses.

5) Since the will is handwritten, hence reading the will may be an issue owing to which it may

not be executed.

6) There is no instruction letter which states the key financial documents and the underlying

assets that Gerry has.

c) Which kind of Will would you recommend to Gerry and why? (1 mark- .5 mark each)

Page 4 of 9

so, the amount of repayment? (1 mark - .5 mark each)

Gerry’s calculation: (1 mark - .5 mark each)

Gerry would be impacted by the OAS claw-back since the taxable income of Gerry tends to

exceed the minimum threshold value.

Total taxable income = 80000 + 12000 + 7000 = $ 99,000

For the period between July 2017 to July 2018, the minimum threshold is $73,756.

Hence, repayment under claw-back = (99000- 73,756)*15% = $3,786.6 per annum

b) Gerry has not done any Estate planning since his wife died 10 years ago but since his

three adult children are no longer on speaking terms, he thought it would be a good idea

to write a Will. He knows that his handwriting is not the greatest but figures that his kids

will finally come together to try to figure it out. Gerry hid the Will in a coat pocket deep

inside his closet; he chose a coat that he no longer wears. Gerry named his best friend Alf

as Liquidator but has not yet told him nor has he told him where the Will is, as Alf is 85

years old and hasn’t been feeling well lately. Gerry also put precious coins that he has

been collecting in the lining of the same coat.

Give six (6) problems that could arise?

(3 marks - .5 marks each)

1) Alf may not survive when there is a need to execute the will.

2) Alf may not want to act as the liquidator as consent has not been obtained and Gerry has

not been obtained Alf about the will.

3) Considering the will is hidden in a coat pocket which he longer wears and this coat is kept

deep in the closet, it may be assumed that no will actually exists.

4) The will may not be considered as legal considering that it has not been signed by any

witnesses.

5) Since the will is handwritten, hence reading the will may be an issue owing to which it may

not be executed.

6) There is no instruction letter which states the key financial documents and the underlying

assets that Gerry has.

c) Which kind of Will would you recommend to Gerry and why? (1 mark- .5 mark each)

Page 4 of 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It would be suggested that Notarial will is suitable considering that it is completed in the

presence of a lawyer and is widely done in Quebec. This gives legality of the will and makes it

enforceable.

Mini-Case D:

Question 1: (4 marks)

Harvey and Melanie are looking to buy a house as they are tired of renting and not being able to

make the changes that they want on the current rented apartment. Harvey is in construction and

enjoys home renovations yet feels restricted on a rental property. The minimum down payment in

Canada is 5% for a home under $500,000. In addition, for down payments of less than 20%, home

buyers are required to purchase mortgage default insurance. Canada Mortgage Housing Corporation

(CMHC) offers this type of insurance. The premium can be paid in a single lump sum or it can be

added to the mortgage and included in monthly payments. Harvey and Melanie have decided to pay

it as a part of their mortgage. They are currently looking at a property valued at $400,000 and can put

$45,000 as a down payment. Based on the information that Harvey and Melanie have provided,

calculate the following:

a) Calculate their down payment as a percentage of the home price: (1 mark)

Calculation: (1 mark)

Down payment amount that Harvey and Melanie can afford = $ 45,000

Value of property = $ 400,000

Hence down payment as a% of home price = (45000/400000)*100 = 11.25%

b) Calculate the mortgage amount required: (1 mark)

Calculation: (1 mark)

Mortgage amount required = Home Price – Down payment = 400,000 – 45,000 = $ 355,000

c) Calculate the Loan to Value ratio: (1 mark)

Calculation: (1 mark)

Loan taken for the home = $ 355,000

Home price = $ 400,000

Loan to value ratio = (355000/400000)*100 = 88.75%

Page 5 of 9

presence of a lawyer and is widely done in Quebec. This gives legality of the will and makes it

enforceable.

Mini-Case D:

Question 1: (4 marks)

Harvey and Melanie are looking to buy a house as they are tired of renting and not being able to

make the changes that they want on the current rented apartment. Harvey is in construction and

enjoys home renovations yet feels restricted on a rental property. The minimum down payment in

Canada is 5% for a home under $500,000. In addition, for down payments of less than 20%, home

buyers are required to purchase mortgage default insurance. Canada Mortgage Housing Corporation

(CMHC) offers this type of insurance. The premium can be paid in a single lump sum or it can be

added to the mortgage and included in monthly payments. Harvey and Melanie have decided to pay

it as a part of their mortgage. They are currently looking at a property valued at $400,000 and can put

$45,000 as a down payment. Based on the information that Harvey and Melanie have provided,

calculate the following:

a) Calculate their down payment as a percentage of the home price: (1 mark)

Calculation: (1 mark)

Down payment amount that Harvey and Melanie can afford = $ 45,000

Value of property = $ 400,000

Hence down payment as a% of home price = (45000/400000)*100 = 11.25%

b) Calculate the mortgage amount required: (1 mark)

Calculation: (1 mark)

Mortgage amount required = Home Price – Down payment = 400,000 – 45,000 = $ 355,000

c) Calculate the Loan to Value ratio: (1 mark)

Calculation: (1 mark)

Loan taken for the home = $ 355,000

Home price = $ 400,000

Loan to value ratio = (355000/400000)*100 = 88.75%

Page 5 of 9

d) Harvey and Melanie know they need default mortgage insurance which is another 3.1%

added cost to them. Calculate the revised mortgage amount as they have decided to add

this insurance to their mortgage. (1 mark)

Calculation: (1 mark)

Default mortgage insurance amount = 3.1% * Mortgage amount = (3.1/100)*$355,000 =$ 11,005

Revised mortgage amount = Original mortgage amount + Default mortgage insurance amount =

355,000 + 11,005 = $366,005

The End

Page 6 of 9

added cost to them. Calculate the revised mortgage amount as they have decided to add

this insurance to their mortgage. (1 mark)

Calculation: (1 mark)

Default mortgage insurance amount = 3.1% * Mortgage amount = (3.1/100)*$355,000 =$ 11,005

Revised mortgage amount = Original mortgage amount + Default mortgage insurance amount =

355,000 + 11,005 = $366,005

The End

Page 6 of 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

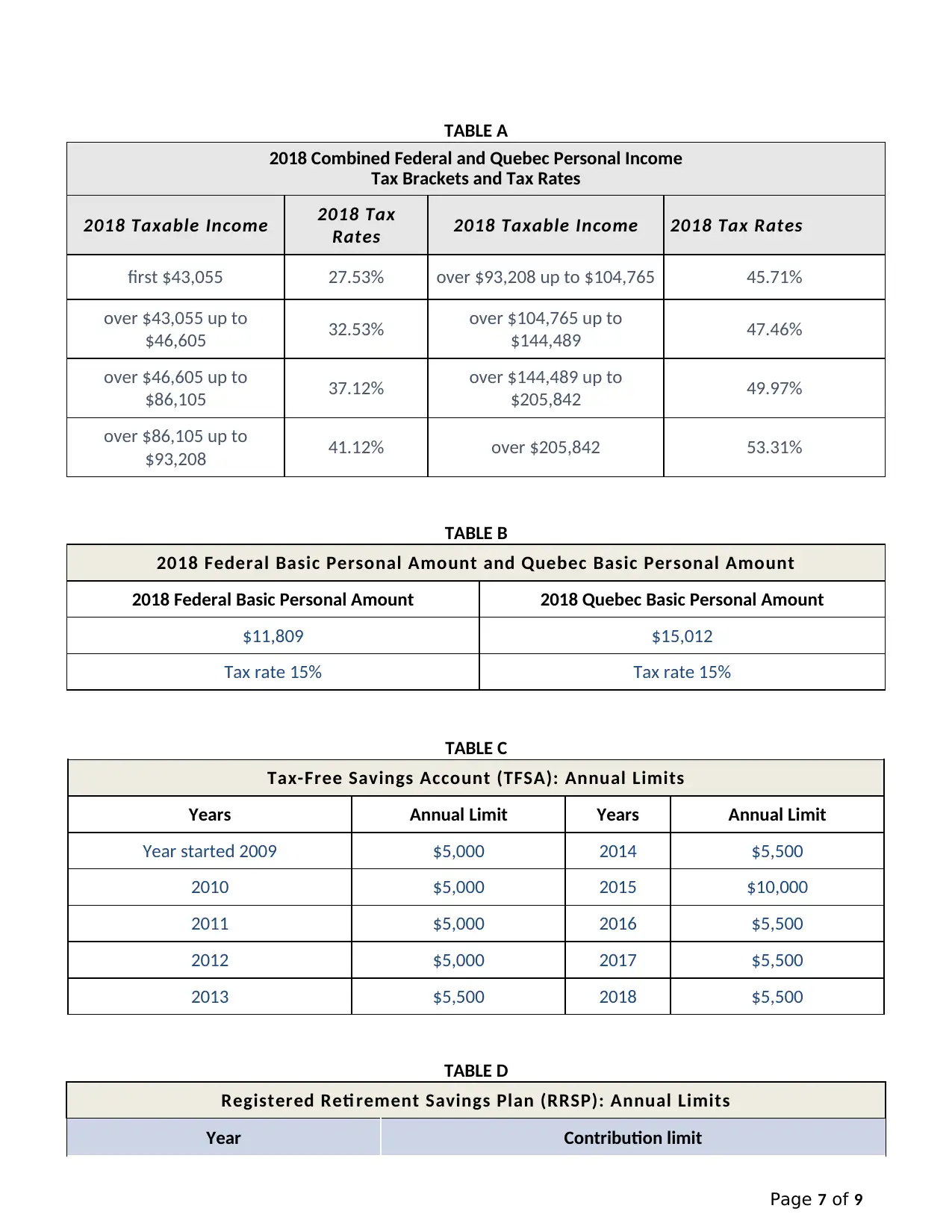

TABLE A

2018 Combined Federal and Quebec Personal Income

Tax Brackets and Tax Rates

2018 Taxable Income 2018 Tax

Rates 2018 Taxable Income 2018 Tax Rates

first $43,055 27.53% over $93,208 up to $104,765 45.71%

over $43,055 up to

$46,605 32.53% over $104,765 up to

$144,489 47.46%

over $46,605 up to

$86,105 37.12% over $144,489 up to

$205,842 49.97%

over $86,105 up to

$93,208 41.12% over $205,842 53.31%

TABLE B

2018 Federal Basic Personal Amount and Quebec Basic Personal Amount

2018 Federal Basic Personal Amount 2018 Quebec Basic Personal Amount

$11,809 $15,012

Tax rate 15% Tax rate 15%

TABLE C

Tax-Free Savings Account (TFSA): Annual Limits

Years Annual Limit Years Annual Limit

Year started 2009 $5,000 2014 $5,500

2010 $5,000 2015 $10,000

2011 $5,000 2016 $5,500

2012 $5,000 2017 $5,500

2013 $5,500 2018 $5,500

TABLE D

Registered Reti rement Savings Plan (RRSP): Annual Limits

Year Contribution limit

Page 7 of 9

2018 Combined Federal and Quebec Personal Income

Tax Brackets and Tax Rates

2018 Taxable Income 2018 Tax

Rates 2018 Taxable Income 2018 Tax Rates

first $43,055 27.53% over $93,208 up to $104,765 45.71%

over $43,055 up to

$46,605 32.53% over $104,765 up to

$144,489 47.46%

over $46,605 up to

$86,105 37.12% over $144,489 up to

$205,842 49.97%

over $86,105 up to

$93,208 41.12% over $205,842 53.31%

TABLE B

2018 Federal Basic Personal Amount and Quebec Basic Personal Amount

2018 Federal Basic Personal Amount 2018 Quebec Basic Personal Amount

$11,809 $15,012

Tax rate 15% Tax rate 15%

TABLE C

Tax-Free Savings Account (TFSA): Annual Limits

Years Annual Limit Years Annual Limit

Year started 2009 $5,000 2014 $5,500

2010 $5,000 2015 $10,000

2011 $5,000 2016 $5,500

2012 $5,000 2017 $5,500

2013 $5,500 2018 $5,500

TABLE D

Registered Reti rement Savings Plan (RRSP): Annual Limits

Year Contribution limit

Page 7 of 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

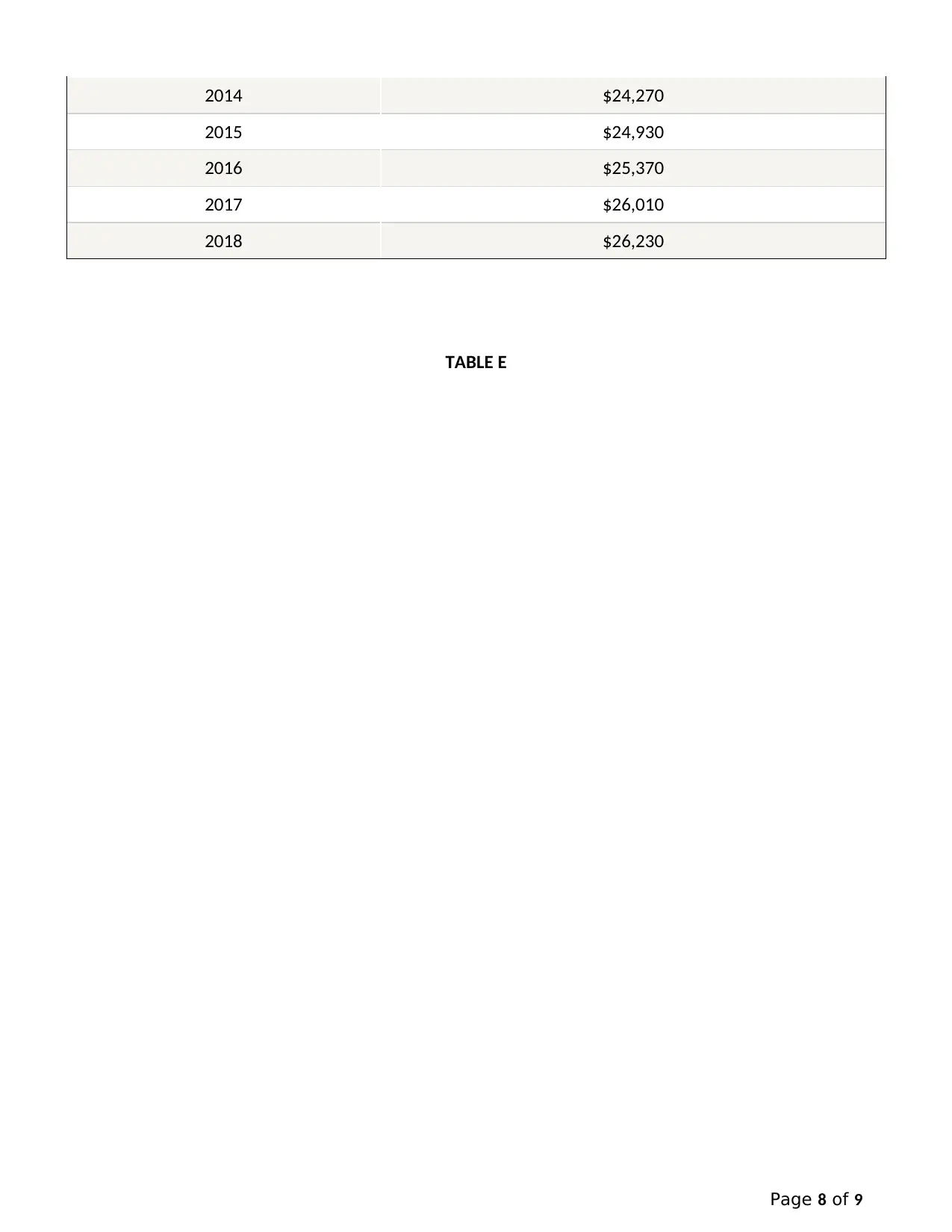

2014 $24,270

2015 $24,930

2016 $25,370

2017 $26,010

2018 $26,230

TABLE E

Page 8 of 9

2015 $24,930

2016 $25,370

2017 $26,010

2018 $26,230

TABLE E

Page 8 of 9

Page 9 of 9

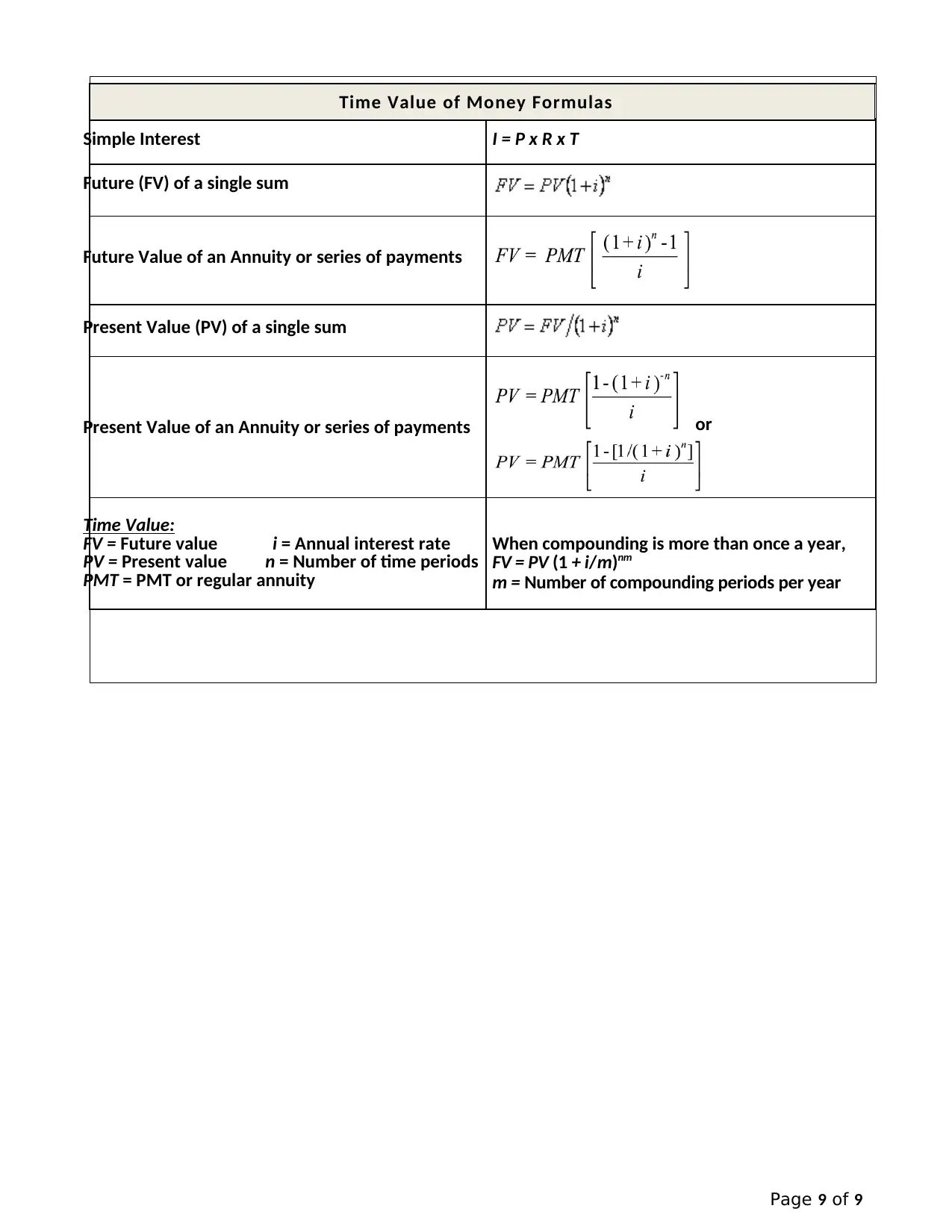

Time Value of Money Formulas

Simple Interest I = P x R x T

Future (FV) of a single sum

Future Value of an Annuity or series of payments

Present Value (PV) of a single sum

Present Value of an Annuity or series of payments or

Time Value:

FV = Future value i = Annual interest rate

PV = Present value n = Number of time periods

PMT = PMT or regular annuity

When compounding is more than once a year,

FV = PV (1 + i/m)nm

m = Number of compounding periods per year

Time Value of Money Formulas

Simple Interest I = P x R x T

Future (FV) of a single sum

Future Value of an Annuity or series of payments

Present Value (PV) of a single sum

Present Value of an Annuity or series of payments or

Time Value:

FV = Future value i = Annual interest rate

PV = Present value n = Number of time periods

PMT = PMT or regular annuity

When compounding is more than once a year,

FV = PV (1 + i/m)nm

m = Number of compounding periods per year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.