Managing Finance (FINA6000): Case Analysis Report on Two Companies

VerifiedAdded on 2022/09/15

|17

|2392

|16

Report

AI Summary

This report presents a comprehensive financial analysis of National Australia Bank (NAB) and Nib Holdings Limited (NHF) for the period of 2014-2018, fulfilling the requirements of a FINA6000 assignment. The analysis includes a comparative evaluation of the companies' financial performance, focusing on profitability, liquidity, and investment ratios. The report delves into the capital structure of each company, assessing debt-to-equity ratios and the weighted average cost of capital (WACC). Furthermore, the report employs the dividend discount model to value the shares of both companies, offering investment recommendations based on the findings. The executive summary provides an overview of the stakeholders involved in financial analysis of the quantitative information presented in the financial statements so as to arrive at varied business decisions such as to invest in the shares of the company or not. The tools of ratio analysis, WACC, and dividend discount models have been used to compare the financial performances of the companies. The report concludes with a recommendation on which company's shares would be a better investment.

Managing Finance

Assessment 3 - Case Analysis

Assessment 3 - Case Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINA6000 Managing Finance 1

Executive Summary

The stakeholders engage in the financial analysis of the quantitative information

presented in the financial statements so as to arrive at varied business decisions such as to

invest in the shares of the company or not. In addition it aids in the comparative evaluation of

the performances with the industry benchmarks, along with the trend analysis. The tools of

ratio analysis, WACC, Dividend Discount Models have been used to compare the finanicl

performances of the companies National Australia Bank and Nib Holdings Limited for the

years 2041-2018. It has been assessed that the NAB has a better overall standing.

Executive Summary

The stakeholders engage in the financial analysis of the quantitative information

presented in the financial statements so as to arrive at varied business decisions such as to

invest in the shares of the company or not. In addition it aids in the comparative evaluation of

the performances with the industry benchmarks, along with the trend analysis. The tools of

ratio analysis, WACC, Dividend Discount Models have been used to compare the finanicl

performances of the companies National Australia Bank and Nib Holdings Limited for the

years 2041-2018. It has been assessed that the NAB has a better overall standing.

FINA6000 Managing Finance 2

Contents

Introduction...........................................................................................................................................3

Overview...........................................................................................................................................3

Purpose of the report..........................................................................................................................3

Analysis.................................................................................................................................................3

Background of the companies............................................................................................................3

Profitability, Liquidity and Investment ratios....................................................................................4

Profitability Ratios.........................................................................................................................4

Liquidity Ratios.............................................................................................................................7

Investment Ratios..........................................................................................................................7

Analysis of the capital structure.........................................................................................................8

Historical weighted average cost of capital........................................................................................9

Valuation of the shares of the companies..........................................................................................9

Recommendation and Conclusion.........................................................................................................9

Contents

Introduction...........................................................................................................................................3

Overview...........................................................................................................................................3

Purpose of the report..........................................................................................................................3

Analysis.................................................................................................................................................3

Background of the companies............................................................................................................3

Profitability, Liquidity and Investment ratios....................................................................................4

Profitability Ratios.........................................................................................................................4

Liquidity Ratios.............................................................................................................................7

Investment Ratios..........................................................................................................................7

Analysis of the capital structure.........................................................................................................8

Historical weighted average cost of capital........................................................................................9

Valuation of the shares of the companies..........................................................................................9

Recommendation and Conclusion.........................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINA6000 Managing Finance 3

Introduction

Overview

The preparation of the financial statements is vital as the same aids in the decision

making of the varied stakeholders of a business. The analysis of the financial statements of an

entity is vital in order to examine the trends of the financial performance as well as the

comparison of the performance in relation to the market as well as the competitors in the

same industry (Edmonds, 2013). The two entities chosen to demonstrate the techniques and

the significance of the financial analysis are the “National Australia Bank” and “Nib

Holdings Limited.”

Purpose of the report

The objective of the report is to conduct an evaluation of the financial statements of

the mentioned entities that would aid in commenting on the progress for the financial years

from 2014 to 2018. In addition, the decision would be made on the choice of the shares

among the two companies for the purpose of the investments therein. The varied financial

tools that would aid in the evaluation are the ratios, weighted average cost of capital and the

valuation models.

Analysis

Background of the companies

The international banking group namely the National Australia Bank Limited (NAB)

was originally founded in the year 1893 and has operations in Australia, New Zealand, Asia,

Europe and the United States. The organisation is engaged in financial sector with key

services being offered as the banking services, housing and general finance, credit and card

Introduction

Overview

The preparation of the financial statements is vital as the same aids in the decision

making of the varied stakeholders of a business. The analysis of the financial statements of an

entity is vital in order to examine the trends of the financial performance as well as the

comparison of the performance in relation to the market as well as the competitors in the

same industry (Edmonds, 2013). The two entities chosen to demonstrate the techniques and

the significance of the financial analysis are the “National Australia Bank” and “Nib

Holdings Limited.”

Purpose of the report

The objective of the report is to conduct an evaluation of the financial statements of

the mentioned entities that would aid in commenting on the progress for the financial years

from 2014 to 2018. In addition, the decision would be made on the choice of the shares

among the two companies for the purpose of the investments therein. The varied financial

tools that would aid in the evaluation are the ratios, weighted average cost of capital and the

valuation models.

Analysis

Background of the companies

The international banking group namely the National Australia Bank Limited (NAB)

was originally founded in the year 1893 and has operations in Australia, New Zealand, Asia,

Europe and the United States. The organisation is engaged in financial sector with key

services being offered as the banking services, housing and general finance, credit and card

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINA6000 Managing Finance 4

facilities, international and investment banking, leasing, wealth and funds management, and

others. The shares of the company are traded on the Australian Stock Exchange under the

symbol of “NAB.AU.”

The company Nibs Holdings Limited as founded in the year 2007 is health and

medical insurance company based at Australia. The Company is engaged in the operation of

private health insurance for residents of Australia, New Zealand and the students and

international visitors to Australia. The Company’s shares are listed on the Australian Stock

Exchange under the symbol, “NHF.AU.”

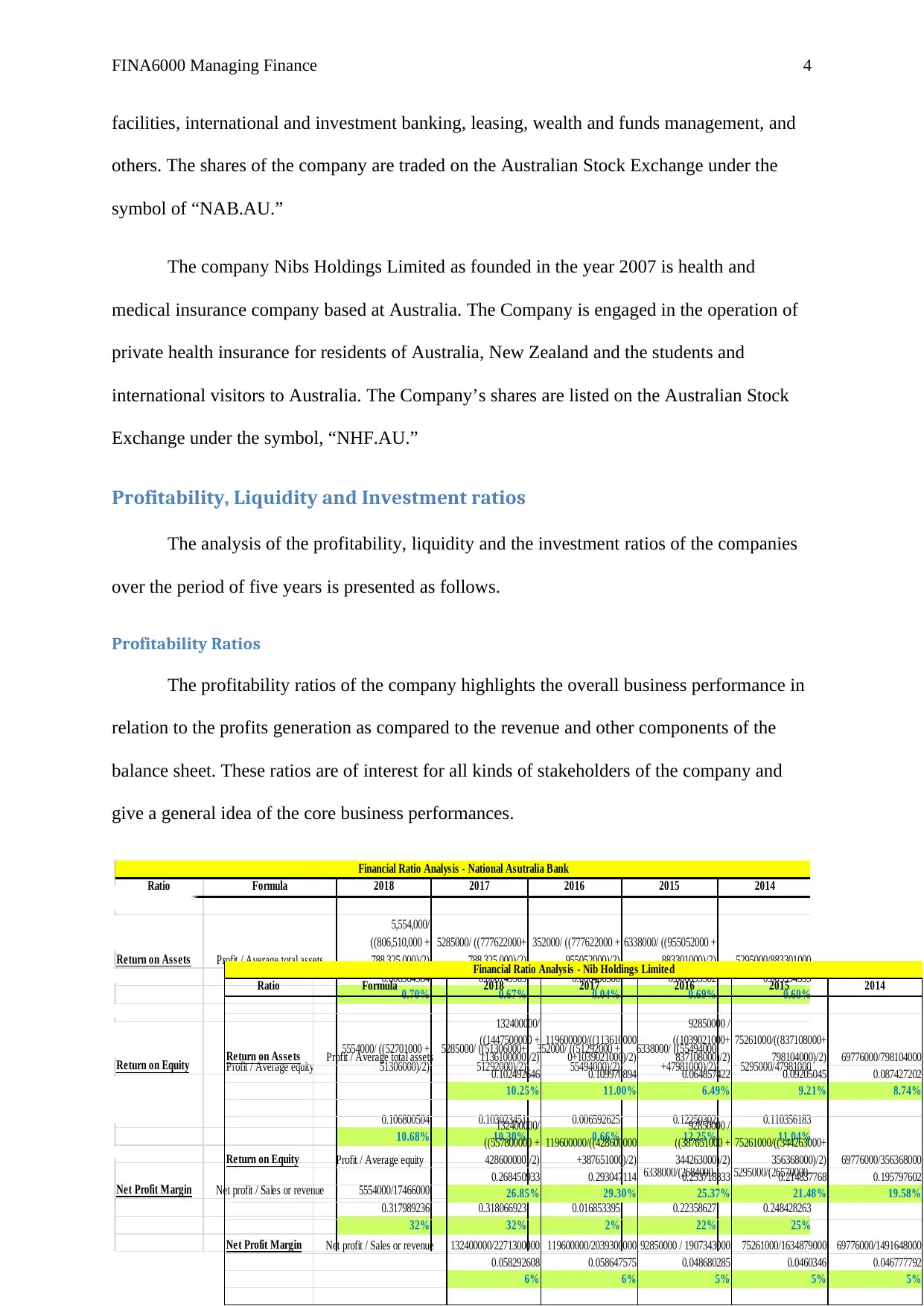

Profitability, Liquidity and Investment ratios

The analysis of the profitability, liquidity and the investment ratios of the companies

over the period of five years is presented as follows.

Profitability Ratios

The profitability ratios of the company highlights the overall business performance in

relation to the profits generation as compared to the revenue and other components of the

balance sheet. These ratios are of interest for all kinds of stakeholders of the company and

give a general idea of the core business performances.

Ratio Formula 2018 2017 2016 2015 2014

Return on Assets Profit / Average total assets

5,554,000/

((806,510,000 +

788,325,000)/2)

5285000/ ((777622000+

788,325,000)/2)

352000/ ((777622000 +

955052000)/2)

6338000/ ((955052000 +

883301000)/2) 5295000/883301000

0.006964984 0.006749909 0.000406308 0.006895302 0.005994559

0.70% 0.67% 0.04% 0.69% 0.60%

Return on Equity Profit / Average equity

5554000/ ((52701000 +

51306000)/2)

5285000/ ((51306000+

51292000)/2)

352000/ ((51292000 +

55494000)/2)

6338000/ ((55494000

+47981000)/2) 5295000/47981000

0.106800504 0.103023451 0.006592625 0.12250302 0.110356183

10.68% 10.30% 0.66% 12.25% 11.04%

Net Profit Margin Net profit / Sales or revenue 5554000/17466000 5285000/ 16616000 352000/ 20886000

6338000/(2684000-

5707000)

5295000/(26570000-

5256000)

0.317989236 0.318066923 0.016853395 0.22358627 0.248428263

32% 32% 2% 22% 25%

Financial Ratio Analysis - National Asutralia Bank

Ratio Formula 2018 2017 2016 2015 2014

Return on Assets Profit / Average total assets

132400000/

((1447500000 +

1136100000)/2)

119600000/((113610000

0+1039021000)/2)

92850000 /

((1039021000+

837108000)/2)

75261000/((837108000+

798104000)/2) 69776000/798104000

0.102492646 0.109970894 0.064857422 0.09205045 0.087427202

10.25% 11.00% 6.49% 9.21% 8.74%

Return on Equity Profit / Average equity

132400000/

((557800000 +

428600000)/2)

119600000/((428600000

+387651000)/2)

92850000 /

((387651000 +

344263000)/2)

75261000/((344263000+

356368000)/2) 69776000/356368000

0.268450933 0.293047114 0.253718333 0.214837768 0.195797602

26.85% 29.30% 25.37% 21.48% 19.58%

Net Profit Margin Net profit / Sales or revenue 132400000/2271300000 119600000/2039300000 92850000 / 1907343000 75261000/1634879000 69776000/1491648000

0.058292608 0.058647575 0.048680285 0.0460346 0.046777792

6% 6% 5% 5% 5%

Financial Ratio Analysis - Nib Holdings Limited

facilities, international and investment banking, leasing, wealth and funds management, and

others. The shares of the company are traded on the Australian Stock Exchange under the

symbol of “NAB.AU.”

The company Nibs Holdings Limited as founded in the year 2007 is health and

medical insurance company based at Australia. The Company is engaged in the operation of

private health insurance for residents of Australia, New Zealand and the students and

international visitors to Australia. The Company’s shares are listed on the Australian Stock

Exchange under the symbol, “NHF.AU.”

Profitability, Liquidity and Investment ratios

The analysis of the profitability, liquidity and the investment ratios of the companies

over the period of five years is presented as follows.

Profitability Ratios

The profitability ratios of the company highlights the overall business performance in

relation to the profits generation as compared to the revenue and other components of the

balance sheet. These ratios are of interest for all kinds of stakeholders of the company and

give a general idea of the core business performances.

Ratio Formula 2018 2017 2016 2015 2014

Return on Assets Profit / Average total assets

5,554,000/

((806,510,000 +

788,325,000)/2)

5285000/ ((777622000+

788,325,000)/2)

352000/ ((777622000 +

955052000)/2)

6338000/ ((955052000 +

883301000)/2) 5295000/883301000

0.006964984 0.006749909 0.000406308 0.006895302 0.005994559

0.70% 0.67% 0.04% 0.69% 0.60%

Return on Equity Profit / Average equity

5554000/ ((52701000 +

51306000)/2)

5285000/ ((51306000+

51292000)/2)

352000/ ((51292000 +

55494000)/2)

6338000/ ((55494000

+47981000)/2) 5295000/47981000

0.106800504 0.103023451 0.006592625 0.12250302 0.110356183

10.68% 10.30% 0.66% 12.25% 11.04%

Net Profit Margin Net profit / Sales or revenue 5554000/17466000 5285000/ 16616000 352000/ 20886000

6338000/(2684000-

5707000)

5295000/(26570000-

5256000)

0.317989236 0.318066923 0.016853395 0.22358627 0.248428263

32% 32% 2% 22% 25%

Financial Ratio Analysis - National Asutralia Bank

Ratio Formula 2018 2017 2016 2015 2014

Return on Assets Profit / Average total assets

132400000/

((1447500000 +

1136100000)/2)

119600000/((113610000

0+1039021000)/2)

92850000 /

((1039021000+

837108000)/2)

75261000/((837108000+

798104000)/2) 69776000/798104000

0.102492646 0.109970894 0.064857422 0.09205045 0.087427202

10.25% 11.00% 6.49% 9.21% 8.74%

Return on Equity Profit / Average equity

132400000/

((557800000 +

428600000)/2)

119600000/((428600000

+387651000)/2)

92850000 /

((387651000 +

344263000)/2)

75261000/((344263000+

356368000)/2) 69776000/356368000

0.268450933 0.293047114 0.253718333 0.214837768 0.195797602

26.85% 29.30% 25.37% 21.48% 19.58%

Net Profit Margin Net profit / Sales or revenue 132400000/2271300000 119600000/2039300000 92850000 / 1907343000 75261000/1634879000 69776000/1491648000

0.058292608 0.058647575 0.048680285 0.0460346 0.046777792

6% 6% 5% 5% 5%

Financial Ratio Analysis - Nib Holdings Limited

FINA6000 Managing Finance 5

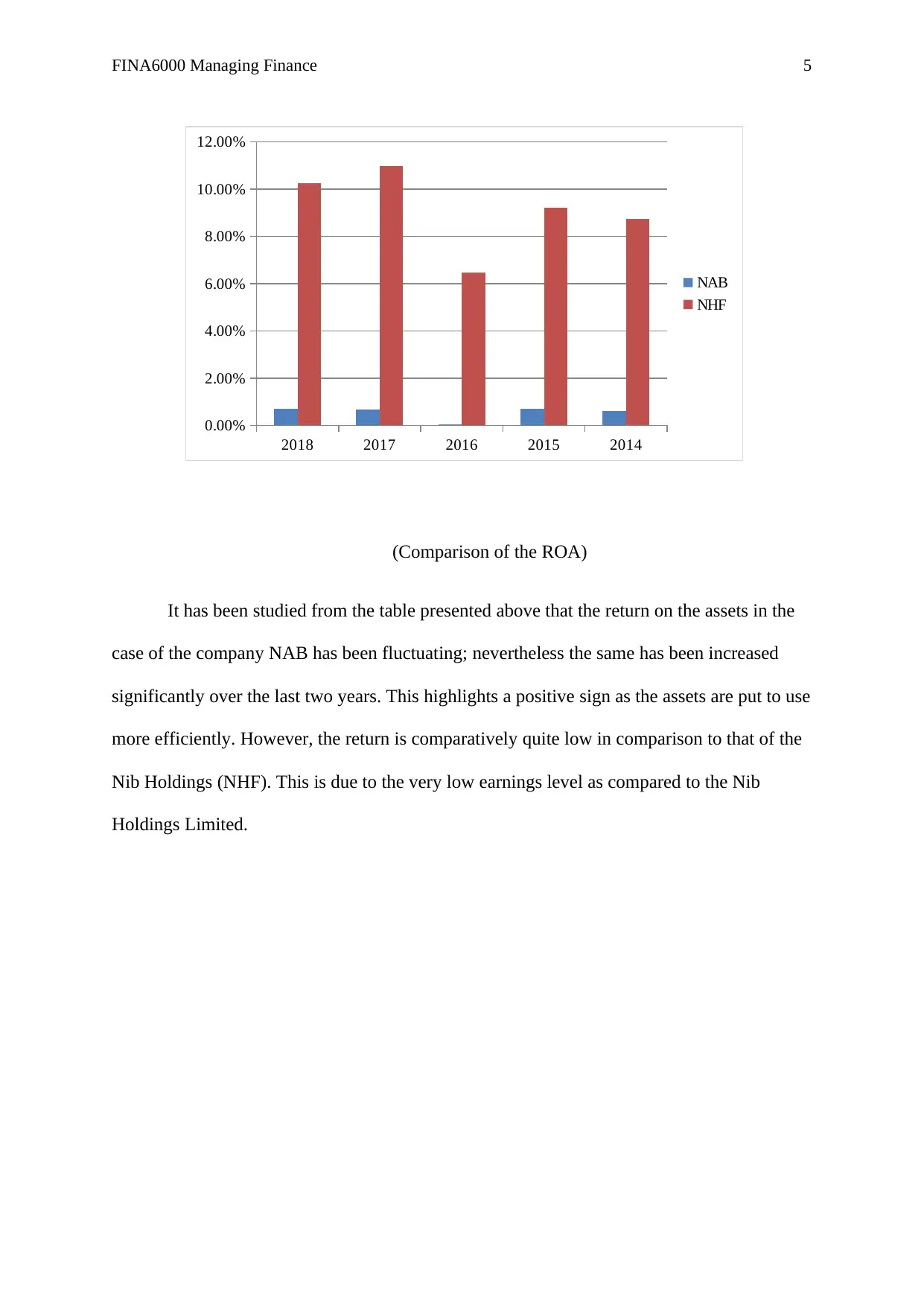

(Comparison of the ROA)

It has been studied from the table presented above that the return on the assets in the

case of the company NAB has been fluctuating; nevertheless the same has been increased

significantly over the last two years. This highlights a positive sign as the assets are put to use

more efficiently. However, the return is comparatively quite low in comparison to that of the

Nib Holdings (NHF). This is due to the very low earnings level as compared to the Nib

Holdings Limited.

2018 2017 2016 2015 2014

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

NAB

NHF

(Comparison of the ROA)

It has been studied from the table presented above that the return on the assets in the

case of the company NAB has been fluctuating; nevertheless the same has been increased

significantly over the last two years. This highlights a positive sign as the assets are put to use

more efficiently. However, the return is comparatively quite low in comparison to that of the

Nib Holdings (NHF). This is due to the very low earnings level as compared to the Nib

Holdings Limited.

2018 2017 2016 2015 2014

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

NAB

NHF

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINA6000 Managing Finance 6

2018 2017 2016 2015 2014

0%

5%

10%

15%

20%

25%

30%

35%

NAB

NHF

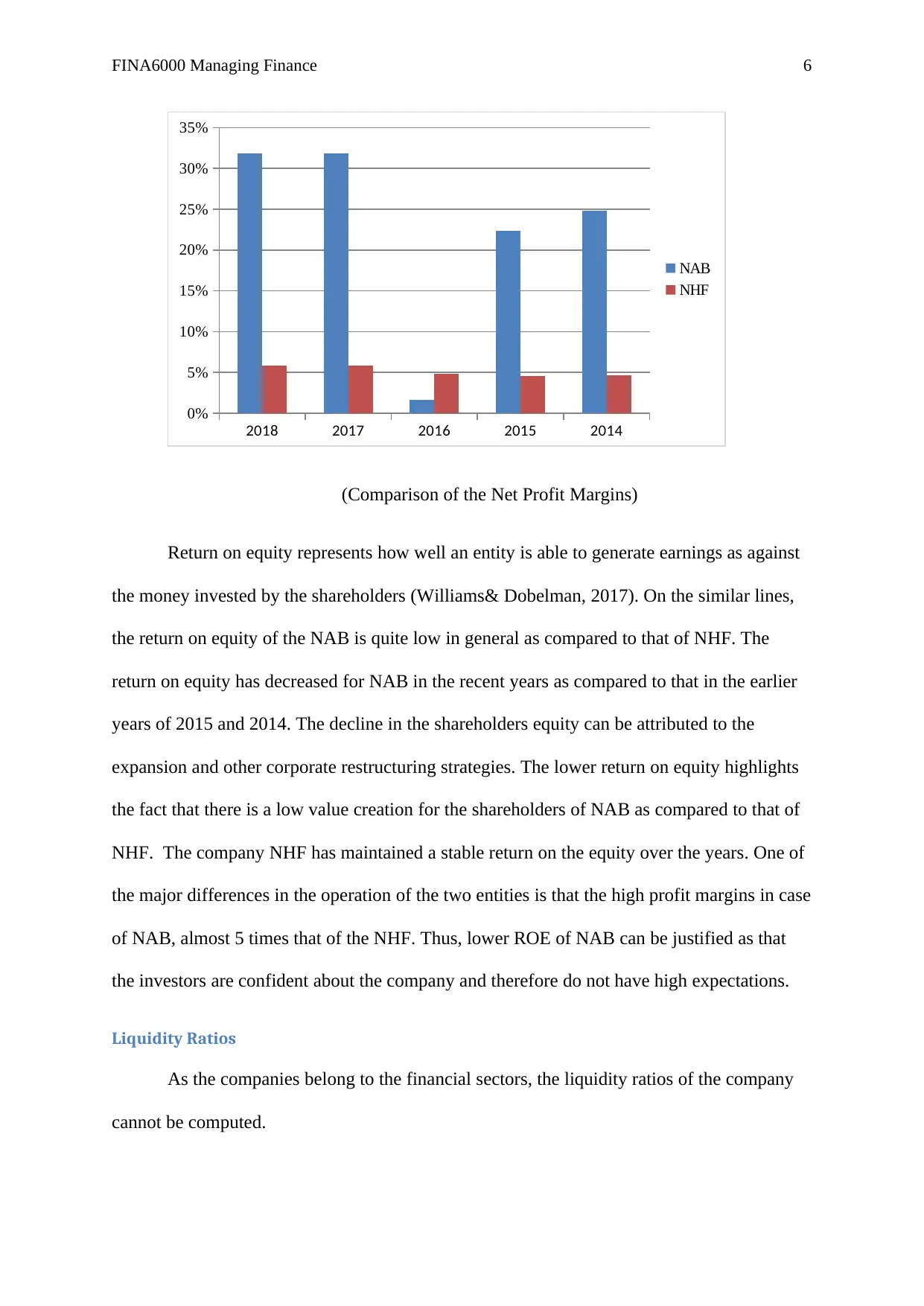

(Comparison of the Net Profit Margins)

Return on equity represents how well an entity is able to generate earnings as against

the money invested by the shareholders (Williams& Dobelman, 2017). On the similar lines,

the return on equity of the NAB is quite low in general as compared to that of NHF. The

return on equity has decreased for NAB in the recent years as compared to that in the earlier

years of 2015 and 2014. The decline in the shareholders equity can be attributed to the

expansion and other corporate restructuring strategies. The lower return on equity highlights

the fact that there is a low value creation for the shareholders of NAB as compared to that of

NHF. The company NHF has maintained a stable return on the equity over the years. One of

the major differences in the operation of the two entities is that the high profit margins in case

of NAB, almost 5 times that of the NHF. Thus, lower ROE of NAB can be justified as that

the investors are confident about the company and therefore do not have high expectations.

Liquidity Ratios

As the companies belong to the financial sectors, the liquidity ratios of the company

cannot be computed.

2018 2017 2016 2015 2014

0%

5%

10%

15%

20%

25%

30%

35%

NAB

NHF

(Comparison of the Net Profit Margins)

Return on equity represents how well an entity is able to generate earnings as against

the money invested by the shareholders (Williams& Dobelman, 2017). On the similar lines,

the return on equity of the NAB is quite low in general as compared to that of NHF. The

return on equity has decreased for NAB in the recent years as compared to that in the earlier

years of 2015 and 2014. The decline in the shareholders equity can be attributed to the

expansion and other corporate restructuring strategies. The lower return on equity highlights

the fact that there is a low value creation for the shareholders of NAB as compared to that of

NHF. The company NHF has maintained a stable return on the equity over the years. One of

the major differences in the operation of the two entities is that the high profit margins in case

of NAB, almost 5 times that of the NHF. Thus, lower ROE of NAB can be justified as that

the investors are confident about the company and therefore do not have high expectations.

Liquidity Ratios

As the companies belong to the financial sectors, the liquidity ratios of the company

cannot be computed.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINA6000 Managing Finance 7

Investment Ratios

These ratios are of prime interest for the present and the prospective investors of a

company. These group of ratios highlight the market standing of the company and the

expectations of the shareholders together with the influence of the external business

environment on the stock of the company (Robinson et al. 2015). The comparative

investment ratios are provided hereunder.

Ratio Formula 2018 2017 2016 2015 2014

Earnings per share

Net income

availabel to equity

shareholders/

Number of shares 5454000/2709460 5187000/2664511 228000 /2596957 6338000/2438782 5295000/2329985

2.012947229 1.946698663 0.087795062 2.598838273 2.272546819

2.01 1.95 0.09 2.60 2.27

Dividend Payout Ratio DPS/EPS 0.99/2.01 0.99/1.95 0.99/0.09 0.380769231 0.99/2.27

0.492537313 0.507692308 11 0.380769231 0.436123348

49% 51% 1100.00% 38.08% 43.61%

Financial Ratio Analysis - NAB

Ratio Formula 2018 2017 2016 2015 2014

Earnings per share

Net income

availabel to equity

shareholders/

Number of shares132400000/450600000 119600000/439000000 92850000 / 439004000 75261000/439004182 69776000/439004182

0.293830448 0.272437358 0.21150149 0.171435725 0.158941538

0.29 0.27 0.21 0.17 0.16

Dividend Payout Ratio DPS/EPS 0.11/0.29 0.105/0.27 0.09/0.21 0.06/0.17 0.1475/0.16

0.379310345 0.388888889 0.428571429 0.352941176 0.921875

37.93% 38.89% 42.86% 35.29% 92.19%

Financial Ratio Analysis - Nib Holdings Limited

Investment Ratios

These ratios are of prime interest for the present and the prospective investors of a

company. These group of ratios highlight the market standing of the company and the

expectations of the shareholders together with the influence of the external business

environment on the stock of the company (Robinson et al. 2015). The comparative

investment ratios are provided hereunder.

Ratio Formula 2018 2017 2016 2015 2014

Earnings per share

Net income

availabel to equity

shareholders/

Number of shares 5454000/2709460 5187000/2664511 228000 /2596957 6338000/2438782 5295000/2329985

2.012947229 1.946698663 0.087795062 2.598838273 2.272546819

2.01 1.95 0.09 2.60 2.27

Dividend Payout Ratio DPS/EPS 0.99/2.01 0.99/1.95 0.99/0.09 0.380769231 0.99/2.27

0.492537313 0.507692308 11 0.380769231 0.436123348

49% 51% 1100.00% 38.08% 43.61%

Financial Ratio Analysis - NAB

Ratio Formula 2018 2017 2016 2015 2014

Earnings per share

Net income

availabel to equity

shareholders/

Number of shares132400000/450600000 119600000/439000000 92850000 / 439004000 75261000/439004182 69776000/439004182

0.293830448 0.272437358 0.21150149 0.171435725 0.158941538

0.29 0.27 0.21 0.17 0.16

Dividend Payout Ratio DPS/EPS 0.11/0.29 0.105/0.27 0.09/0.21 0.06/0.17 0.1475/0.16

0.379310345 0.388888889 0.428571429 0.352941176 0.921875

37.93% 38.89% 42.86% 35.29% 92.19%

Financial Ratio Analysis - Nib Holdings Limited

FINA6000 Managing Finance 8

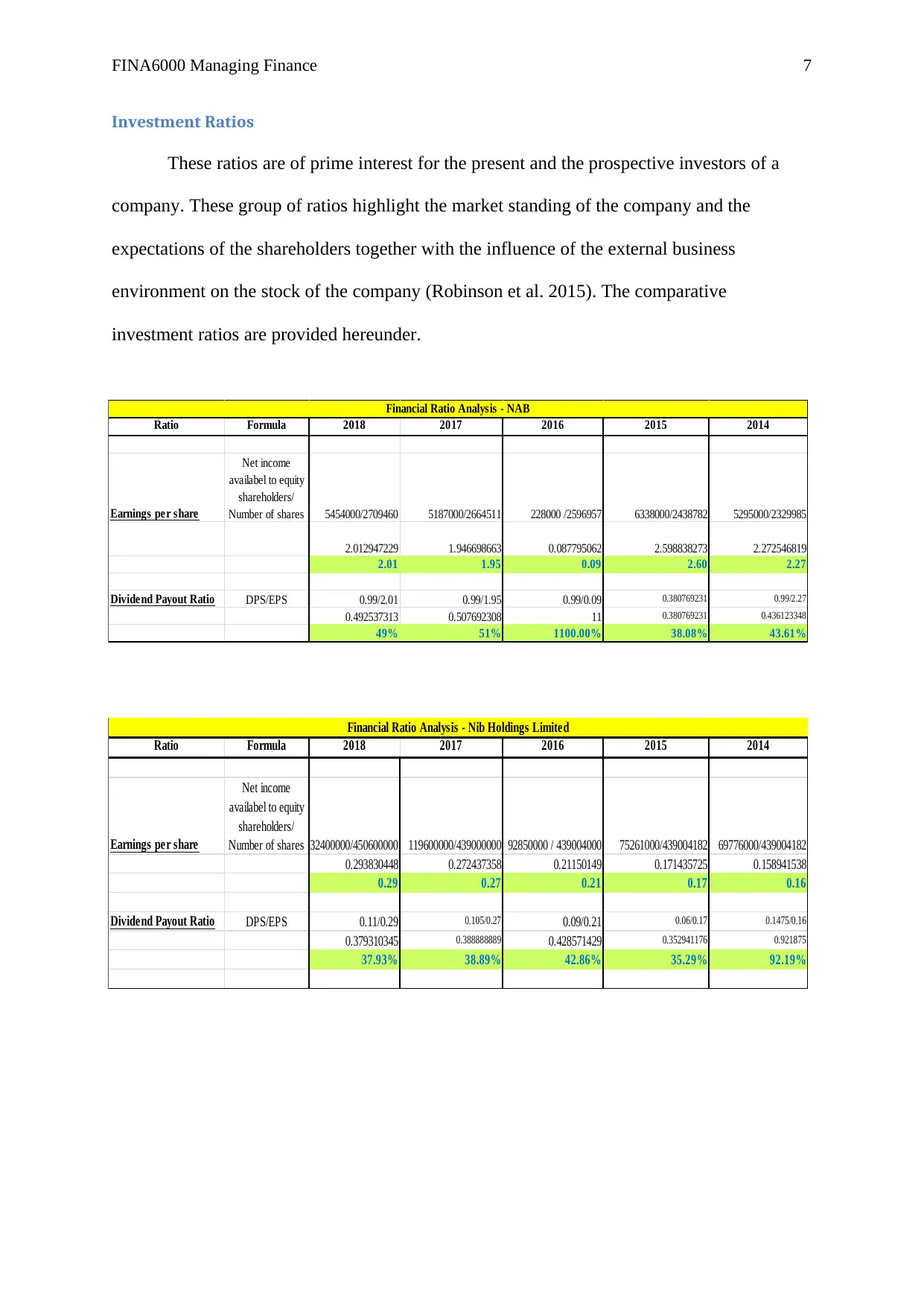

(Comparison of the EPS)

As assessed from the calculations above, the high net profit margins of the NAB are

also evident in the form of the high Earning per share for the company as compared to the

NHF. In addition, there is a high dividend payout ratio for the NAB over the years as

compared to NHF, except the year 2016. Thus, from the point of view of the investment,

stable streams of earnings are present in the shares of the NAB and the earnings are

fluctuating in the case of NHF. This is a positive sign for the NAB and the high goodwill

over the years together with a strong asset base can be regarded as the chief reasons for the

same.

Analysis of the capital structure

One of the major business decisions is regarding the components of the capital

structure of an organisation. This is because the changes in the levels of debt and equity

accordingly influence the levels of the business risk and the probabilities of the financial

distress (Delen, Kuzey & Uyar, 2013). Two key ratios that have been computed to assess the

capital structure of the companies over the years is the “Debt to Equity” and “Equity” ratios.

It is to be noted that the debt to equity ratio has been computed taking the total liabilities

2018 2017 2016 2015 2014

0.00

0.50

1.00

1.50

2.00

2.50

3.00

NAB

NHF

(Comparison of the EPS)

As assessed from the calculations above, the high net profit margins of the NAB are

also evident in the form of the high Earning per share for the company as compared to the

NHF. In addition, there is a high dividend payout ratio for the NAB over the years as

compared to NHF, except the year 2016. Thus, from the point of view of the investment,

stable streams of earnings are present in the shares of the NAB and the earnings are

fluctuating in the case of NHF. This is a positive sign for the NAB and the high goodwill

over the years together with a strong asset base can be regarded as the chief reasons for the

same.

Analysis of the capital structure

One of the major business decisions is regarding the components of the capital

structure of an organisation. This is because the changes in the levels of debt and equity

accordingly influence the levels of the business risk and the probabilities of the financial

distress (Delen, Kuzey & Uyar, 2013). Two key ratios that have been computed to assess the

capital structure of the companies over the years is the “Debt to Equity” and “Equity” ratios.

It is to be noted that the debt to equity ratio has been computed taking the total liabilities

2018 2017 2016 2015 2014

0.00

0.50

1.00

1.50

2.00

2.50

3.00

NAB

NHF

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

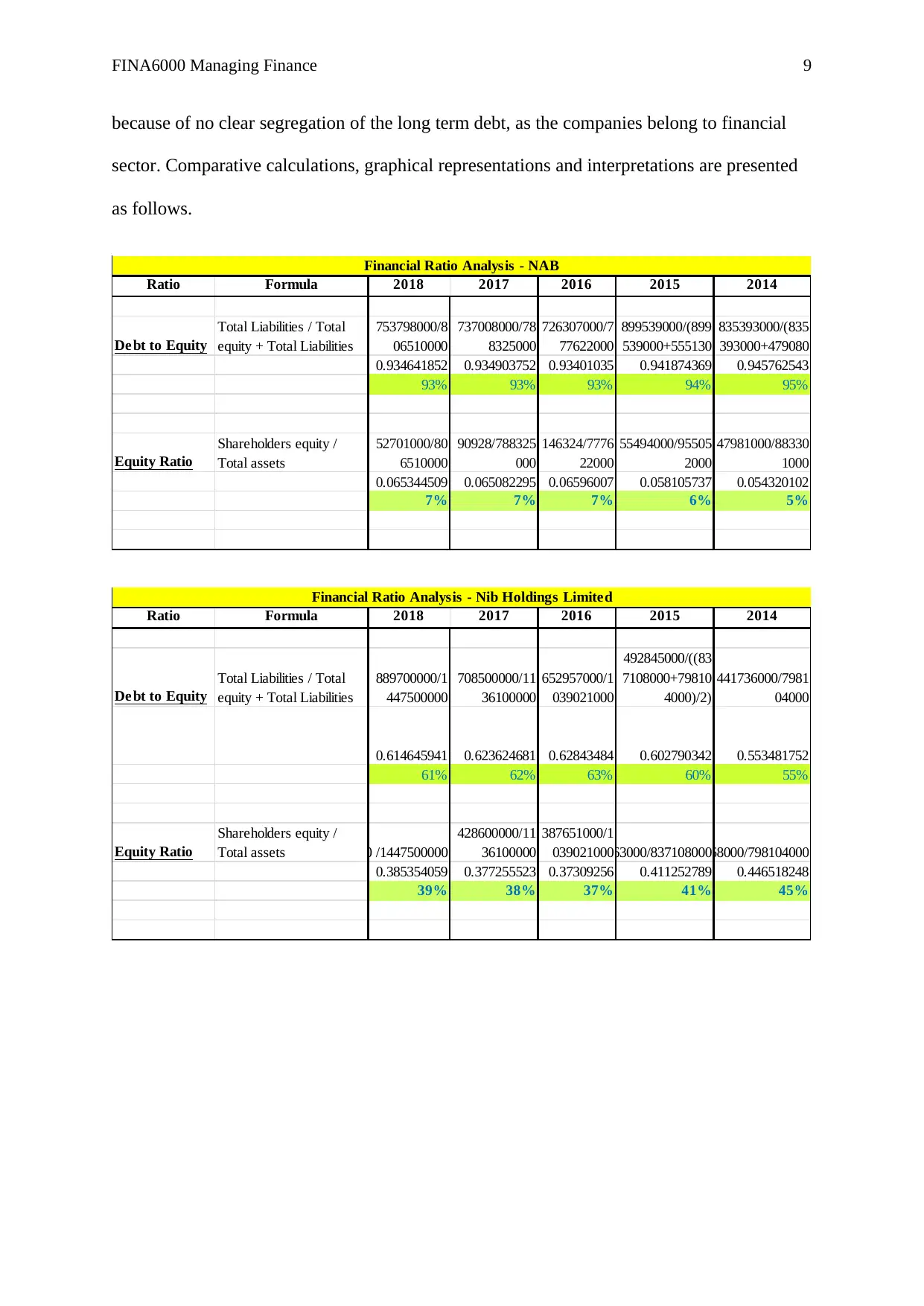

FINA6000 Managing Finance 9

because of no clear segregation of the long term debt, as the companies belong to financial

sector. Comparative calculations, graphical representations and interpretations are presented

as follows.

Ratio Formula 2018 2017 2016 2015 2014

Debt to Equity

Total Liabilities / Total

equity + Total Liabilities

753798000/8

06510000

737008000/78

8325000

726307000/7

77622000

899539000/(899

539000+555130

835393000/(835

393000+479080

0.934641852 0.934903752 0.93401035 0.941874369 0.945762543

93% 93% 93% 94% 95%

Equity Ratio

Shareholders equity /

Total assets

52701000/80

6510000

90928/788325

000

146324/7776

22000

55494000/95505

2000

47981000/88330

1000

0.065344509 0.065082295 0.06596007 0.058105737 0.054320102

7% 7% 7% 6% 5%

Financial Ratio Analysis - NAB

Ratio Formula 2018 2017 2016 2015 2014

Debt to Equity

Total Liabilities / Total

equity + Total Liabilities

889700000/1

447500000

708500000/11

36100000

652957000/1

039021000

492845000/((83

7108000+79810

4000)/2)

441736000/7981

04000

0.614645941 0.623624681 0.62843484 0.602790342 0.553481752

61% 62% 63% 60% 55%

Equity Ratio

Shareholders equity /

Total assets 557800000 /1447500000

428600000/11

36100000

387651000/1

039021000344263000/837108000356368000/798104000

0.385354059 0.377255523 0.37309256 0.411252789 0.446518248

39% 38% 37% 41% 45%

Financial Ratio Analysis - Nib Holdings Limited

because of no clear segregation of the long term debt, as the companies belong to financial

sector. Comparative calculations, graphical representations and interpretations are presented

as follows.

Ratio Formula 2018 2017 2016 2015 2014

Debt to Equity

Total Liabilities / Total

equity + Total Liabilities

753798000/8

06510000

737008000/78

8325000

726307000/7

77622000

899539000/(899

539000+555130

835393000/(835

393000+479080

0.934641852 0.934903752 0.93401035 0.941874369 0.945762543

93% 93% 93% 94% 95%

Equity Ratio

Shareholders equity /

Total assets

52701000/80

6510000

90928/788325

000

146324/7776

22000

55494000/95505

2000

47981000/88330

1000

0.065344509 0.065082295 0.06596007 0.058105737 0.054320102

7% 7% 7% 6% 5%

Financial Ratio Analysis - NAB

Ratio Formula 2018 2017 2016 2015 2014

Debt to Equity

Total Liabilities / Total

equity + Total Liabilities

889700000/1

447500000

708500000/11

36100000

652957000/1

039021000

492845000/((83

7108000+79810

4000)/2)

441736000/7981

04000

0.614645941 0.623624681 0.62843484 0.602790342 0.553481752

61% 62% 63% 60% 55%

Equity Ratio

Shareholders equity /

Total assets 557800000 /1447500000

428600000/11

36100000

387651000/1

039021000344263000/837108000356368000/798104000

0.385354059 0.377255523 0.37309256 0.411252789 0.446518248

39% 38% 37% 41% 45%

Financial Ratio Analysis - Nib Holdings Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINA6000 Managing Finance 10

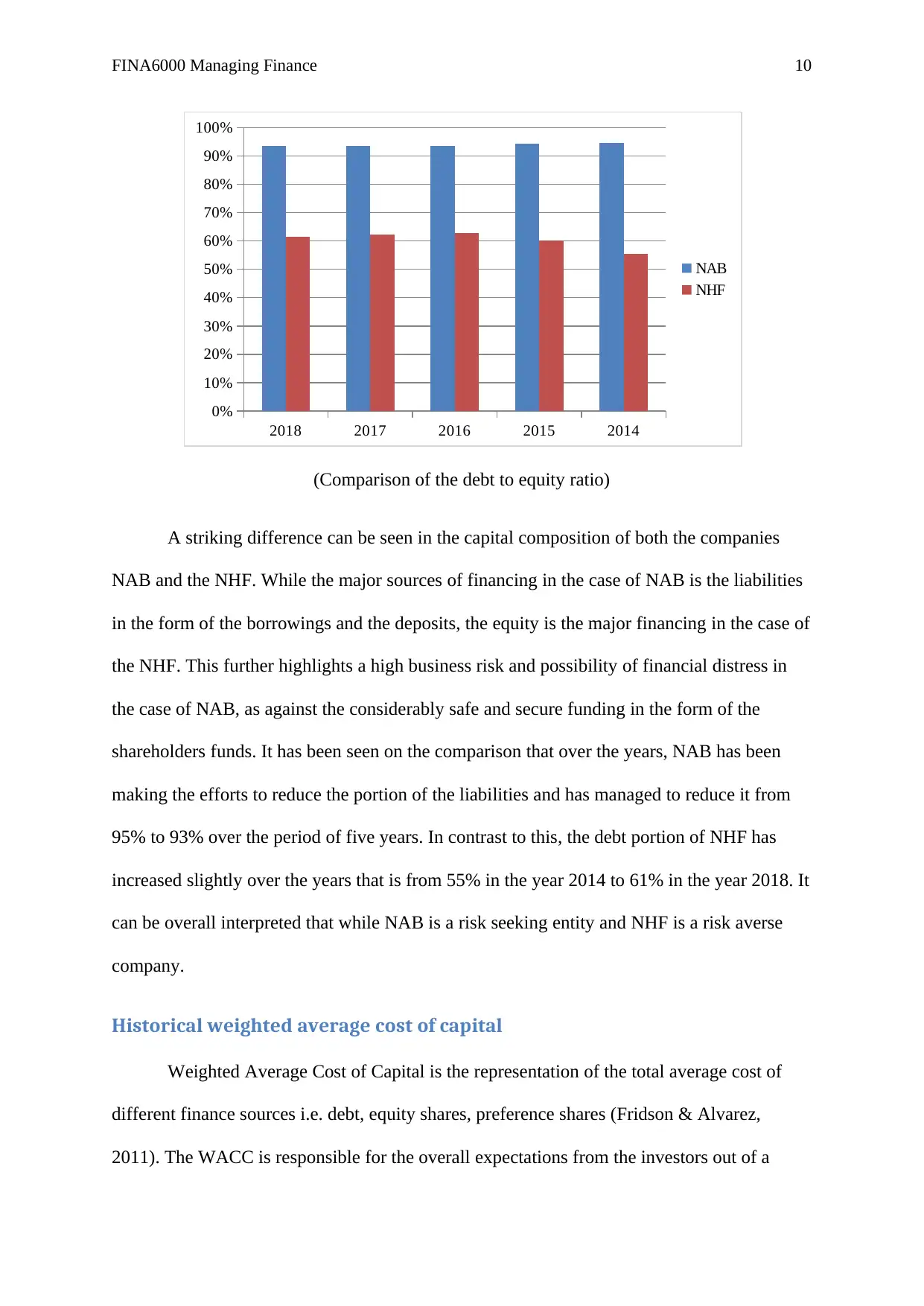

(Comparison of the debt to equity ratio)

A striking difference can be seen in the capital composition of both the companies

NAB and the NHF. While the major sources of financing in the case of NAB is the liabilities

in the form of the borrowings and the deposits, the equity is the major financing in the case of

the NHF. This further highlights a high business risk and possibility of financial distress in

the case of NAB, as against the considerably safe and secure funding in the form of the

shareholders funds. It has been seen on the comparison that over the years, NAB has been

making the efforts to reduce the portion of the liabilities and has managed to reduce it from

95% to 93% over the period of five years. In contrast to this, the debt portion of NHF has

increased slightly over the years that is from 55% in the year 2014 to 61% in the year 2018. It

can be overall interpreted that while NAB is a risk seeking entity and NHF is a risk averse

company.

Historical weighted average cost of capital

Weighted Average Cost of Capital is the representation of the total average cost of

different finance sources i.e. debt, equity shares, preference shares (Fridson & Alvarez,

2011). The WACC is responsible for the overall expectations from the investors out of a

2018 2017 2016 2015 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NAB

NHF

(Comparison of the debt to equity ratio)

A striking difference can be seen in the capital composition of both the companies

NAB and the NHF. While the major sources of financing in the case of NAB is the liabilities

in the form of the borrowings and the deposits, the equity is the major financing in the case of

the NHF. This further highlights a high business risk and possibility of financial distress in

the case of NAB, as against the considerably safe and secure funding in the form of the

shareholders funds. It has been seen on the comparison that over the years, NAB has been

making the efforts to reduce the portion of the liabilities and has managed to reduce it from

95% to 93% over the period of five years. In contrast to this, the debt portion of NHF has

increased slightly over the years that is from 55% in the year 2014 to 61% in the year 2018. It

can be overall interpreted that while NAB is a risk seeking entity and NHF is a risk averse

company.

Historical weighted average cost of capital

Weighted Average Cost of Capital is the representation of the total average cost of

different finance sources i.e. debt, equity shares, preference shares (Fridson & Alvarez,

2011). The WACC is responsible for the overall expectations from the investors out of a

2018 2017 2016 2015 2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

NAB

NHF

FINA6000 Managing Finance 11

business and thus the demand and supply of the shares tend to move with the expectations

(Ross, et. al, 2014). The rate is significant in the case of the investment appraisal evaluations.

The computation is based on either the book value weights of the sources of finance or the

market value weights (Pogue, 2010). The first step calls for the determination of the effective

rate of return of every source of finance. The second step calls for the apportionment of

weights to the respective rates as determined in the first step. The formula for the same can be

expressed as follows.

K = Ke(V e / ¿+V d ) + Kd(V d / ¿+V d)

Where,

K = WACC

V e= Book value weight of equity

V d = Book value weight of debt

Ke= Cost of equity

Kd= After tax cost of debt

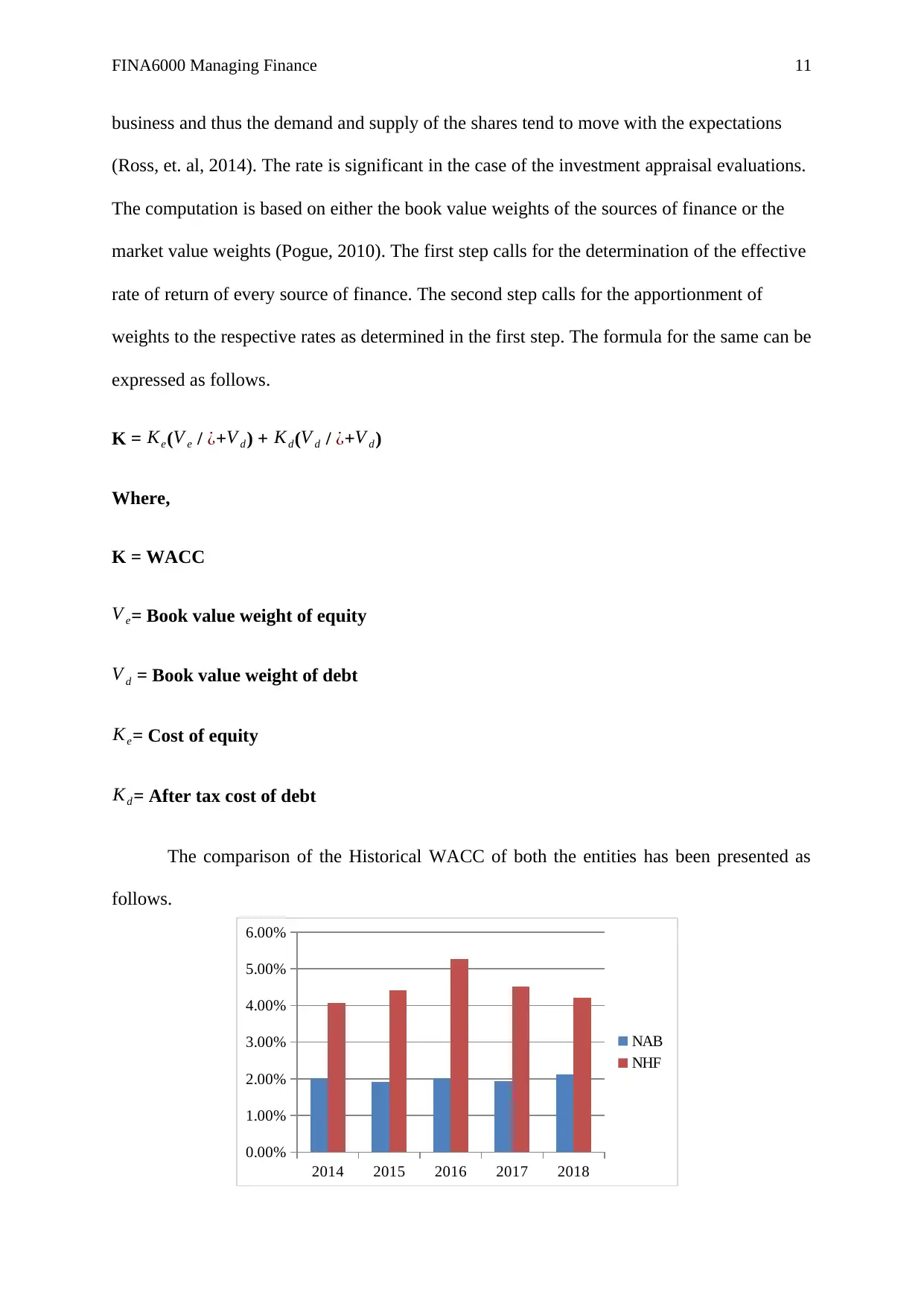

The comparison of the Historical WACC of both the entities has been presented as

follows.

2014 2015 2016 2017 2018

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

NAB

NHF

business and thus the demand and supply of the shares tend to move with the expectations

(Ross, et. al, 2014). The rate is significant in the case of the investment appraisal evaluations.

The computation is based on either the book value weights of the sources of finance or the

market value weights (Pogue, 2010). The first step calls for the determination of the effective

rate of return of every source of finance. The second step calls for the apportionment of

weights to the respective rates as determined in the first step. The formula for the same can be

expressed as follows.

K = Ke(V e / ¿+V d ) + Kd(V d / ¿+V d)

Where,

K = WACC

V e= Book value weight of equity

V d = Book value weight of debt

Ke= Cost of equity

Kd= After tax cost of debt

The comparison of the Historical WACC of both the entities has been presented as

follows.

2014 2015 2016 2017 2018

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

NAB

NHF

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.