Final Accounts Report: Sole Traders and Partnerships - Analysis

VerifiedAdded on 2020/12/24

|19

|4559

|74

Report

AI Summary

This report provides a detailed exploration of final accounts, covering both sole traders and partnerships. It begins with an introduction to the importance of final accounts, emphasizing their role in assessing a business's profitability and financial position. The report then delves into the practical aspects, including the process of preparing final accounts from a trial balance, addressing limitations, and methods for handling incomplete records. It also covers the reasons behind imbalances and the challenges arising from insufficient data. The report proceeds to illustrate the preparation of financial records from incomplete information, including calculations for opening and closing balances, the creation of sales and purchase ledger control accounts, and the application of markups and margins. Furthermore, the report produces final accounts for sole traders, outlining the components of a set of final accounts and demonstrating the preparation of profit and loss statements and balance sheets. The report further examines the legislative and accounting requirements for partnerships, detailing key components of partnership agreements and accounts. It includes the preparation of profit and loss appropriation accounts and the allocation of profit, along with the creation of capital and current accounts for each partner, and concludes with an analysis of the statement of financial position relating to partnerships.

Final accounts for Sole traders and

Partnerships

Partnerships

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1. Undertaking the need, process to prepare the final accounts...........................................1

1.1. Identifying the reasons for closing off accounts and producing trail balance......................1

1.2. Explaining the process, limitation of preparing set of final accounts from trail balance.....1

1.3. The methods of preparing accounts from incomplete records.............................................2

1.4. Reasons of imbalances occurs from incorrect double entries..............................................2

1.5. Reasons for incomplete records arising from insufficient and inconsistent data.................3

TASK 2. Preparing accounts records from incomplete information...............................................4

2.1. Calculating opening and/or closing accounts from incomplete information.......................4

2.2. Calculating closing and opening cash/bank accounts balance.............................................4

2.3. Preparing sales and purchase ledger control accounts with help of correct sales, purchase

and bank amount.........................................................................................................................5

2.4. Calculating account balances using mark ups and margins.................................................6

TASK 3. Produces final accounts for sole traders...........................................................................6

3.1. Describing the components of a set of final accounts for a sole trader................................6

3.2. Preparing statement of Profit and loss accounts..................................................................7

3.3. Preparing statement of financial position or balance sheet..................................................8

TASK4. Understanding legislative and accounting requirements for partnership..........................9

4.1. Describing the key components of partnership agreement..................................................9

4.2. Describing components of partnership accounts................................................................10

TASK5. Preparing statement of profit and lost appropriation account.........................................10

5.1. Preparing statement of profit and loss appropriation account of a partnership..................10

5.2. Identifying the allocation of profit to partners after giving interest for capital, interest on

borrowing and salary.................................................................................................................12

5.3. Preparing Capital ans current account for each partner.....................................................13

TASK 6. Statement of financial position relating to partnership...................................................14

6.1. and 6.2. Statement of financial position with drawing......................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1. Undertaking the need, process to prepare the final accounts...........................................1

1.1. Identifying the reasons for closing off accounts and producing trail balance......................1

1.2. Explaining the process, limitation of preparing set of final accounts from trail balance.....1

1.3. The methods of preparing accounts from incomplete records.............................................2

1.4. Reasons of imbalances occurs from incorrect double entries..............................................2

1.5. Reasons for incomplete records arising from insufficient and inconsistent data.................3

TASK 2. Preparing accounts records from incomplete information...............................................4

2.1. Calculating opening and/or closing accounts from incomplete information.......................4

2.2. Calculating closing and opening cash/bank accounts balance.............................................4

2.3. Preparing sales and purchase ledger control accounts with help of correct sales, purchase

and bank amount.........................................................................................................................5

2.4. Calculating account balances using mark ups and margins.................................................6

TASK 3. Produces final accounts for sole traders...........................................................................6

3.1. Describing the components of a set of final accounts for a sole trader................................6

3.2. Preparing statement of Profit and loss accounts..................................................................7

3.3. Preparing statement of financial position or balance sheet..................................................8

TASK4. Understanding legislative and accounting requirements for partnership..........................9

4.1. Describing the key components of partnership agreement..................................................9

4.2. Describing components of partnership accounts................................................................10

TASK5. Preparing statement of profit and lost appropriation account.........................................10

5.1. Preparing statement of profit and loss appropriation account of a partnership..................10

5.2. Identifying the allocation of profit to partners after giving interest for capital, interest on

borrowing and salary.................................................................................................................12

5.3. Preparing Capital ans current account for each partner.....................................................13

TASK 6. Statement of financial position relating to partnership...................................................14

6.1. and 6.2. Statement of financial position with drawing......................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Final accounts of a business are essential to give a general idea regarding the profitability

and financial position of company to its management and other stakeholders of a specific period.

These final accounts have to be prepared as per the specific guidelines and standards as per the

GAAP. Every business organisation which are registered has to prepare the final accounts. This

final accounts are prepared in all type of businesses whether sole trader or partnership. Final

accounts differers as per the difference in operations of organisation. The present report will help

in understanding preparation and needs of final accounts. The importance and requirement,

process of final accounts will be explained. report will elaborate the process of preparing trail

balance. Further, various calculation will be done of preparing accounting records from

incomplete information. The final accounts for the sole traders like profit and loss, balance sheet

will be produced. Furthermore, various calculation of the final accounts will be done for sole

trader and partnership business.

TASK 1. Undertaking the need, process to prepare the final accounts.

1.1. Identifying the reasons for closing off accounts and producing trail balance.

The closing entries are done for the temporary accounts such as revenue and expenses,

this are essential for the preparation of the financial statements of the company (Bellomo and

et.al., 2012). The reason to closing off such accounts is to be ensured that this accounts shows nil

balance at the starting of the following year. This closing entries are also the retained earning

accounts of company shoe increases from prior year and decreases from dividend payment and

expenses. Trail balance is the list of all closing balances of ledger accounts on a certain date.

Trail balance is the first step towards the preparation financial statement. Trail Balances acts a a

working sheet for the preparation of financial statement. The main purpose of preparing trail

balance is to locate any errors and to be ensures that the entries in accounts are mathematically

correct.

1.2. Explaining the process, limitation of preparing set of final accounts from trail balance.

Trail balance has some limitation as it only confirms that the amount of debit balance is

equals to the credit side balance. Trail balance shown no information if any transactions have

been recorded or not (What is a Trial Balance? , 2019). It can not detect any errors of double

posting has been done of an account.

1

Final accounts of a business are essential to give a general idea regarding the profitability

and financial position of company to its management and other stakeholders of a specific period.

These final accounts have to be prepared as per the specific guidelines and standards as per the

GAAP. Every business organisation which are registered has to prepare the final accounts. This

final accounts are prepared in all type of businesses whether sole trader or partnership. Final

accounts differers as per the difference in operations of organisation. The present report will help

in understanding preparation and needs of final accounts. The importance and requirement,

process of final accounts will be explained. report will elaborate the process of preparing trail

balance. Further, various calculation will be done of preparing accounting records from

incomplete information. The final accounts for the sole traders like profit and loss, balance sheet

will be produced. Furthermore, various calculation of the final accounts will be done for sole

trader and partnership business.

TASK 1. Undertaking the need, process to prepare the final accounts.

1.1. Identifying the reasons for closing off accounts and producing trail balance.

The closing entries are done for the temporary accounts such as revenue and expenses,

this are essential for the preparation of the financial statements of the company (Bellomo and

et.al., 2012). The reason to closing off such accounts is to be ensured that this accounts shows nil

balance at the starting of the following year. This closing entries are also the retained earning

accounts of company shoe increases from prior year and decreases from dividend payment and

expenses. Trail balance is the list of all closing balances of ledger accounts on a certain date.

Trail balance is the first step towards the preparation financial statement. Trail Balances acts a a

working sheet for the preparation of financial statement. The main purpose of preparing trail

balance is to locate any errors and to be ensures that the entries in accounts are mathematically

correct.

1.2. Explaining the process, limitation of preparing set of final accounts from trail balance.

Trail balance has some limitation as it only confirms that the amount of debit balance is

equals to the credit side balance. Trail balance shown no information if any transactions have

been recorded or not (What is a Trial Balance? , 2019). It can not detect any errors of double

posting has been done of an account.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The process of trail balance is done at the end of the financial year, the trail balance is

prepared by extracting the ledger accounts (Graham, Raedy and Shackelford, 2012). Trail

balance is prepared by posting the closing balance of ledger accounts in the trail balance on debit

and credit side respectively. A trail balance is also been said that a statement of sum total of

credit and debit side of various accounts to review the mathematical exactness of the books. It is

foremost important that the trail balance balance is correct and free from any errors, as it is the

base on which the final accounts of the company will prepared.

1.3. The methods of preparing accounts from incomplete records.

In double book keeping method, incomplete record is the record of only one side

transaction or no entry of that transaction. In incomplete record, information regarding assets,

liabilities, expense and revenue is partially recorded (Saeys and et.al., 2012). In case of

incomplete records, following are the methods through which accounts can be prepared:

In case of missing opening capital, it can be ascertained by preparing the statements of

affairs.

In case of missing or incomplete credit purchase, it can be found by preparing the total

creditors accounts.

Likewise, credit sales can be found by preparing the total debtors accounts.

Total creditors amount will help in giving information of payment to creditors.

Bank Reconciliation statement is also a method that assist in constructing accounts with

incomplete record.

Cash and bank related accounts can be prepared by ascertained by preparing cash-book

summary that records all the payments and receipts

1.4. Reasons of imbalances occurs from incorrect double entries.

Trail balance is the the statement which balance the business book at the end of financial

or accounting year. This statement complies when all the transactions of business from journals

to ledger accounts (Fujita, 2017). Assets and expenses of accounts will be posted in debit side of

trail balance whereas liabilities, capital and income accounts will be posted to the credit side of

the trail balance. If the account are correctly extracted in ledger accounts and posted correctly in

trail balance. Than , the debit side of trail balance must be equal to or match to the credit sum

2

prepared by extracting the ledger accounts (Graham, Raedy and Shackelford, 2012). Trail

balance is prepared by posting the closing balance of ledger accounts in the trail balance on debit

and credit side respectively. A trail balance is also been said that a statement of sum total of

credit and debit side of various accounts to review the mathematical exactness of the books. It is

foremost important that the trail balance balance is correct and free from any errors, as it is the

base on which the final accounts of the company will prepared.

1.3. The methods of preparing accounts from incomplete records.

In double book keeping method, incomplete record is the record of only one side

transaction or no entry of that transaction. In incomplete record, information regarding assets,

liabilities, expense and revenue is partially recorded (Saeys and et.al., 2012). In case of

incomplete records, following are the methods through which accounts can be prepared:

In case of missing opening capital, it can be ascertained by preparing the statements of

affairs.

In case of missing or incomplete credit purchase, it can be found by preparing the total

creditors accounts.

Likewise, credit sales can be found by preparing the total debtors accounts.

Total creditors amount will help in giving information of payment to creditors.

Bank Reconciliation statement is also a method that assist in constructing accounts with

incomplete record.

Cash and bank related accounts can be prepared by ascertained by preparing cash-book

summary that records all the payments and receipts

1.4. Reasons of imbalances occurs from incorrect double entries.

Trail balance is the the statement which balance the business book at the end of financial

or accounting year. This statement complies when all the transactions of business from journals

to ledger accounts (Fujita, 2017). Assets and expenses of accounts will be posted in debit side of

trail balance whereas liabilities, capital and income accounts will be posted to the credit side of

the trail balance. If the account are correctly extracted in ledger accounts and posted correctly in

trail balance. Than , the debit side of trail balance must be equal to or match to the credit sum

2

total of trail balance. In case of any imbalances occurs, it has to be omitted as trial balance is the

first step in preparing the final accounts of the company. The reasons for imbalances in trail

balance can be as follows:

Imbalance can occur if any transaction has been posted on one side of an account and

omitted to posted on other side of account.

Wrong entry of amount in ledger accounts will results in imbalance trail balance.

Another reason of imbalance might be, wrong entry of credit amount in debit side or vice

versa in journals accounts.

1.5. Reasons for incomplete records arising from insufficient and inconsistent data.

There are two system of maintaining accounting records, double entry book keeping and

single entry book keeping, maintaining accounting records through single entry is known as

incomplete records. Under the single entry system only cash accounts, debtor and creditors

accounts are maintained properly (Toms, 2016). They the accounts of expenses, income, assets

and liabilities. The information provided through such incomplete records are incomplete and not

so reliable. Such incomplete records can cause problems to the company at the time of audit of

financial statement and for future year planning off business. It is essential to identify the reasons

of incomplete records in order to rectify them on time. Following are the reasons of incomplete

records:

Unintentional failure to records: most often such errors occurs when employee or accountant

forget to post any entry of transaction in book of accounts. It happens when on person is

responsible to manage all accounting procedures, it likely that such mistakes may occurs.

Data Loss: small business which depends on the paper work for recording data suffers from the

loss of data. Many companies are moved from paper work to computer process in order to record

transaction from data (May, 2013). It helps in preventing loss of data.

Intentional manipulation: Accountant sometimes trying to perpetrate fraud or wants to steal

from the company also neglect some transaction to get records in books.

TASK 2. Preparing accounts records from incomplete information.

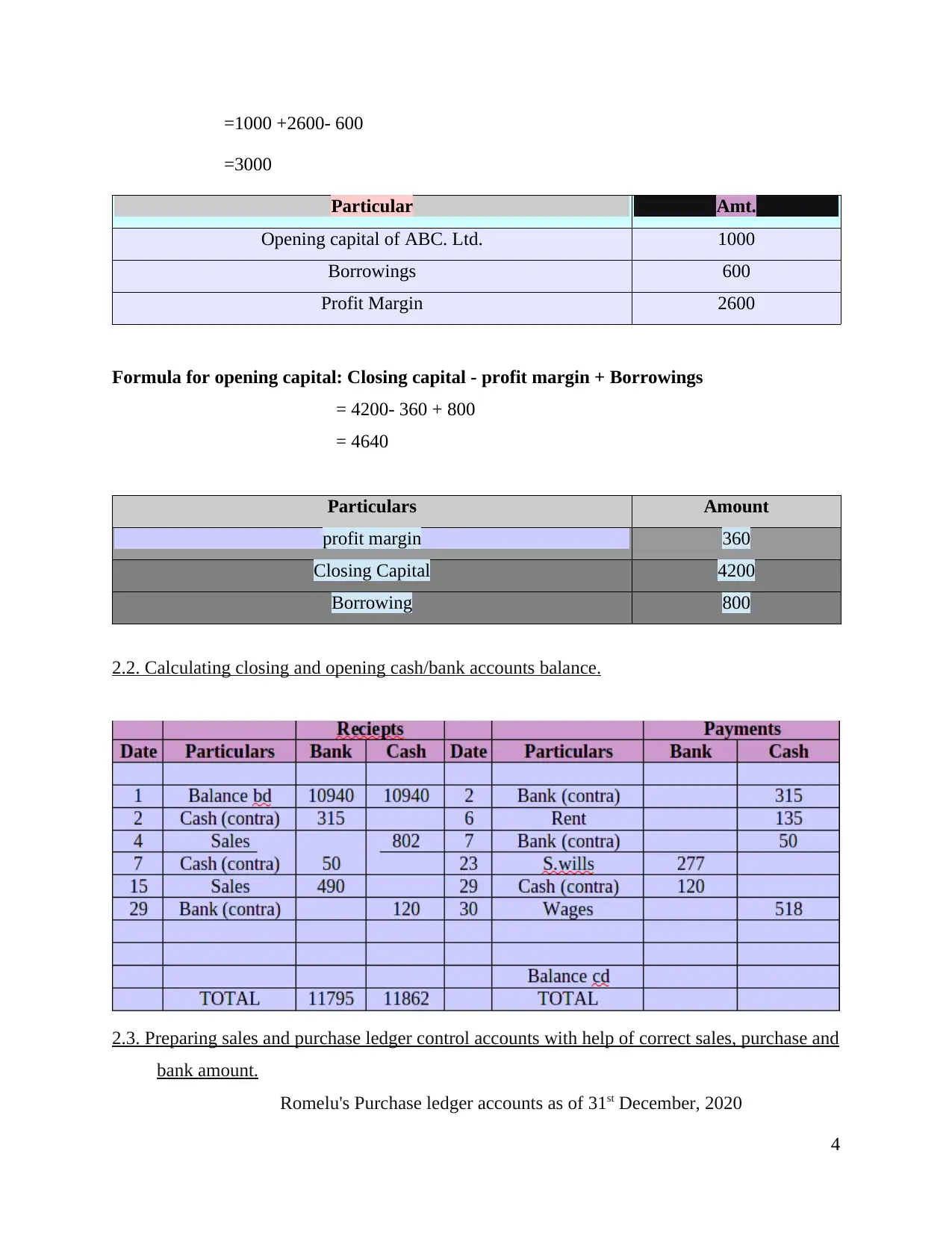

2.1. Calculating opening and/or closing accounts from incomplete information.

Formula of closing capital: opening capital + profit margin - Borrowings

3

first step in preparing the final accounts of the company. The reasons for imbalances in trail

balance can be as follows:

Imbalance can occur if any transaction has been posted on one side of an account and

omitted to posted on other side of account.

Wrong entry of amount in ledger accounts will results in imbalance trail balance.

Another reason of imbalance might be, wrong entry of credit amount in debit side or vice

versa in journals accounts.

1.5. Reasons for incomplete records arising from insufficient and inconsistent data.

There are two system of maintaining accounting records, double entry book keeping and

single entry book keeping, maintaining accounting records through single entry is known as

incomplete records. Under the single entry system only cash accounts, debtor and creditors

accounts are maintained properly (Toms, 2016). They the accounts of expenses, income, assets

and liabilities. The information provided through such incomplete records are incomplete and not

so reliable. Such incomplete records can cause problems to the company at the time of audit of

financial statement and for future year planning off business. It is essential to identify the reasons

of incomplete records in order to rectify them on time. Following are the reasons of incomplete

records:

Unintentional failure to records: most often such errors occurs when employee or accountant

forget to post any entry of transaction in book of accounts. It happens when on person is

responsible to manage all accounting procedures, it likely that such mistakes may occurs.

Data Loss: small business which depends on the paper work for recording data suffers from the

loss of data. Many companies are moved from paper work to computer process in order to record

transaction from data (May, 2013). It helps in preventing loss of data.

Intentional manipulation: Accountant sometimes trying to perpetrate fraud or wants to steal

from the company also neglect some transaction to get records in books.

TASK 2. Preparing accounts records from incomplete information.

2.1. Calculating opening and/or closing accounts from incomplete information.

Formula of closing capital: opening capital + profit margin - Borrowings

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=1000 +2600- 600

=3000

Particular Amt.

Opening capital of ABC. Ltd. 1000

Borrowings 600

Profit Margin 2600

Formula for opening capital: Closing capital - profit margin + Borrowings

= 4200- 360 + 800

= 4640

Particulars Amount

profit margin 360

Closing Capital 4200

Borrowing 800

2.2. Calculating closing and opening cash/bank accounts balance.

2.3. Preparing sales and purchase ledger control accounts with help of correct sales, purchase and

bank amount.

Romelu's Purchase ledger accounts as of 31st December, 2020

4

=3000

Particular Amt.

Opening capital of ABC. Ltd. 1000

Borrowings 600

Profit Margin 2600

Formula for opening capital: Closing capital - profit margin + Borrowings

= 4200- 360 + 800

= 4640

Particulars Amount

profit margin 360

Closing Capital 4200

Borrowing 800

2.2. Calculating closing and opening cash/bank accounts balance.

2.3. Preparing sales and purchase ledger control accounts with help of correct sales, purchase and

bank amount.

Romelu's Purchase ledger accounts as of 31st December, 2020

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

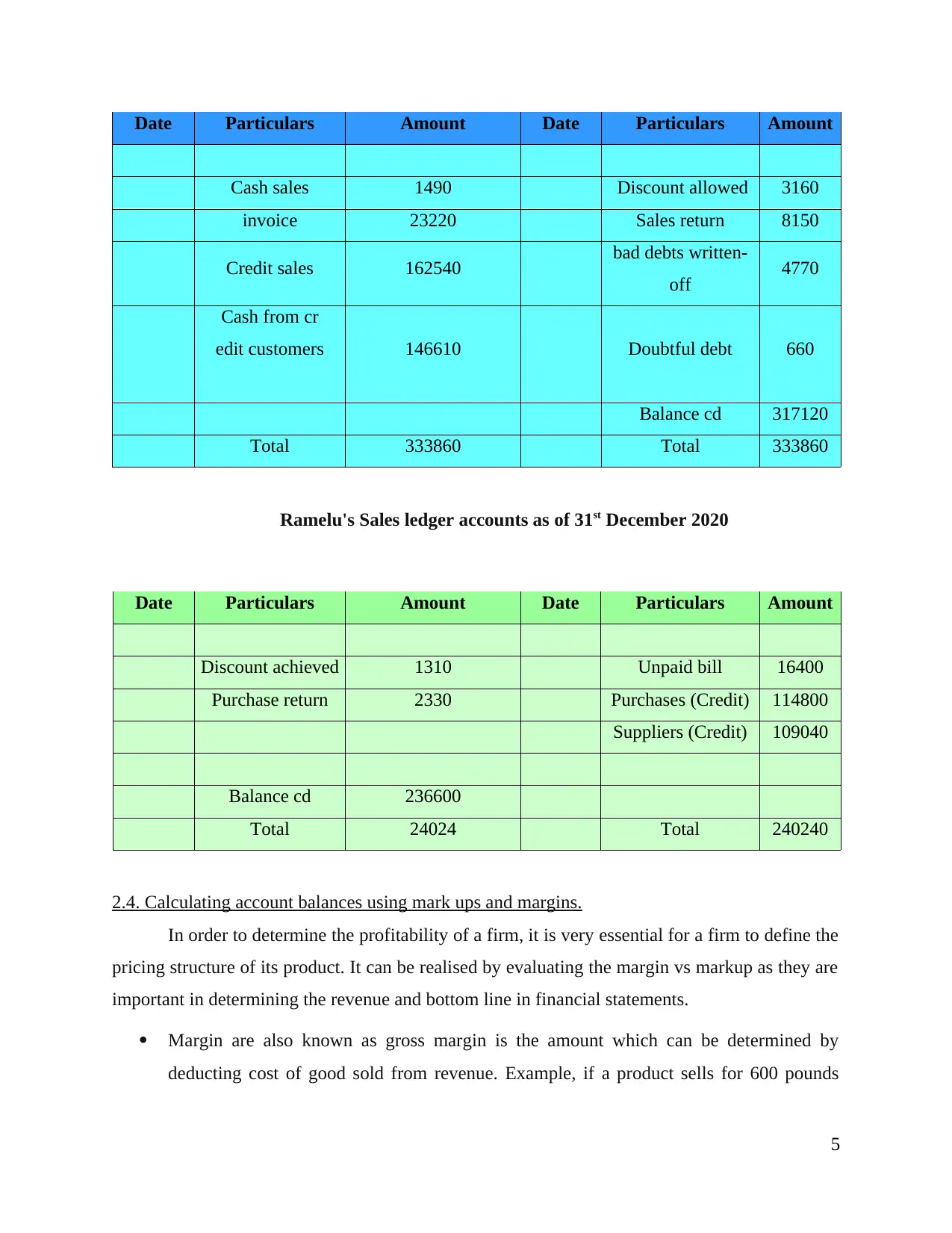

Date Particulars Amount Date Particulars Amount

Cash sales 1490 Discount allowed 3160

invoice 23220 Sales return 8150

Credit sales 162540 bad debts written-

off 4770

Cash from cr

edit customers 146610 Doubtful debt 660

Balance cd 317120

Total 333860 Total 333860

Ramelu's Sales ledger accounts as of 31st December 2020

Date Particulars Amount Date Particulars Amount

Discount achieved 1310 Unpaid bill 16400

Purchase return 2330 Purchases (Credit) 114800

Suppliers (Credit) 109040

Balance cd 236600

Total 24024 Total 240240

2.4. Calculating account balances using mark ups and margins.

In order to determine the profitability of a firm, it is very essential for a firm to define the

pricing structure of its product. It can be realised by evaluating the margin vs markup as they are

important in determining the revenue and bottom line in financial statements.

Margin are also known as gross margin is the amount which can be determined by

deducting cost of good sold from revenue. Example, if a product sells for 600 pounds

5

Cash sales 1490 Discount allowed 3160

invoice 23220 Sales return 8150

Credit sales 162540 bad debts written-

off 4770

Cash from cr

edit customers 146610 Doubtful debt 660

Balance cd 317120

Total 333860 Total 333860

Ramelu's Sales ledger accounts as of 31st December 2020

Date Particulars Amount Date Particulars Amount

Discount achieved 1310 Unpaid bill 16400

Purchase return 2330 Purchases (Credit) 114800

Suppliers (Credit) 109040

Balance cd 236600

Total 24024 Total 240240

2.4. Calculating account balances using mark ups and margins.

In order to determine the profitability of a firm, it is very essential for a firm to define the

pricing structure of its product. It can be realised by evaluating the margin vs markup as they are

important in determining the revenue and bottom line in financial statements.

Margin are also known as gross margin is the amount which can be determined by

deducting cost of good sold from revenue. Example, if a product sells for 600 pounds

5

cost its costs 450 pounds to manufacture than the margin will be 150 pounds. Gross

margin usually expressed in percentage.

Mark-up is the amount that has to be added to the manufacturing cost of product in order

to determine the selling price of that product (Corlett, 2015). Example, a markup of a

product is 150 pounds which cost is 450 will be sold at 600 pounds.

Both margin and markup is different accounting which has different perceptive of

considering business profit.

TASK 3. Produces final accounts for sole traders.

3.1. Describing the components of a set of final accounts for a sole trader.

A sole-proprietorship is the business that is owned and run by an individual. It is the

simplest form of a business as it is not a legal entity (Weygandt, Kimmel and Kieso, 2015).

There is only one person who is responsible for all the loss and profits. A sole trader is

responsible for:

Keeping all the records of the business sales and expenses.

Sending the self-assessment tax every year.

Paying income tax on the profit earned.

Final accounts of sole-trader are prepared the end of each accounting year, it assist in

providing the idea of the financial performance and position of a company. The main three

components of final accounts of sole-trader are as follows:

Trading accounts: This accounts help in ascertaining the gross profit or gross loss

arising from the buying and selling of goods (Hall, 2012). This accounts helped in

tracking the net sales and direct cost of good sold and balance of this accounts which help

in ascertaining the gross profit or loss.

Profit and loss accounts: it is one of the important final accounts which is calculated to

determine the net profit or loss of the company in an accounting year. Profit and loss

account are also known as income statement. Under this account, the gross profit or loss

determined in trading account and net profit is determined by deducting all the indirect

6

margin usually expressed in percentage.

Mark-up is the amount that has to be added to the manufacturing cost of product in order

to determine the selling price of that product (Corlett, 2015). Example, a markup of a

product is 150 pounds which cost is 450 will be sold at 600 pounds.

Both margin and markup is different accounting which has different perceptive of

considering business profit.

TASK 3. Produces final accounts for sole traders.

3.1. Describing the components of a set of final accounts for a sole trader.

A sole-proprietorship is the business that is owned and run by an individual. It is the

simplest form of a business as it is not a legal entity (Weygandt, Kimmel and Kieso, 2015).

There is only one person who is responsible for all the loss and profits. A sole trader is

responsible for:

Keeping all the records of the business sales and expenses.

Sending the self-assessment tax every year.

Paying income tax on the profit earned.

Final accounts of sole-trader are prepared the end of each accounting year, it assist in

providing the idea of the financial performance and position of a company. The main three

components of final accounts of sole-trader are as follows:

Trading accounts: This accounts help in ascertaining the gross profit or gross loss

arising from the buying and selling of goods (Hall, 2012). This accounts helped in

tracking the net sales and direct cost of good sold and balance of this accounts which help

in ascertaining the gross profit or loss.

Profit and loss accounts: it is one of the important final accounts which is calculated to

determine the net profit or loss of the company in an accounting year. Profit and loss

account are also known as income statement. Under this account, the gross profit or loss

determined in trading account and net profit is determined by deducting all the indirect

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses from the gross profit which will results in finding the net profit or loss occurred

in a particular financial year to sole trader.

Financial position statement: It is the important statement which shows the financial

position of a company at particular time. This statement is known as balance sheet which

on one side shows the trader's property and possessions and on the other side all his

liabilities. The Statement reflects the assets and liabilities side which determine what the

company have what it owe to others (DRURY, 2013). Balance sheet of the company will

be said to be accurate when the asset side will match to the liability side.

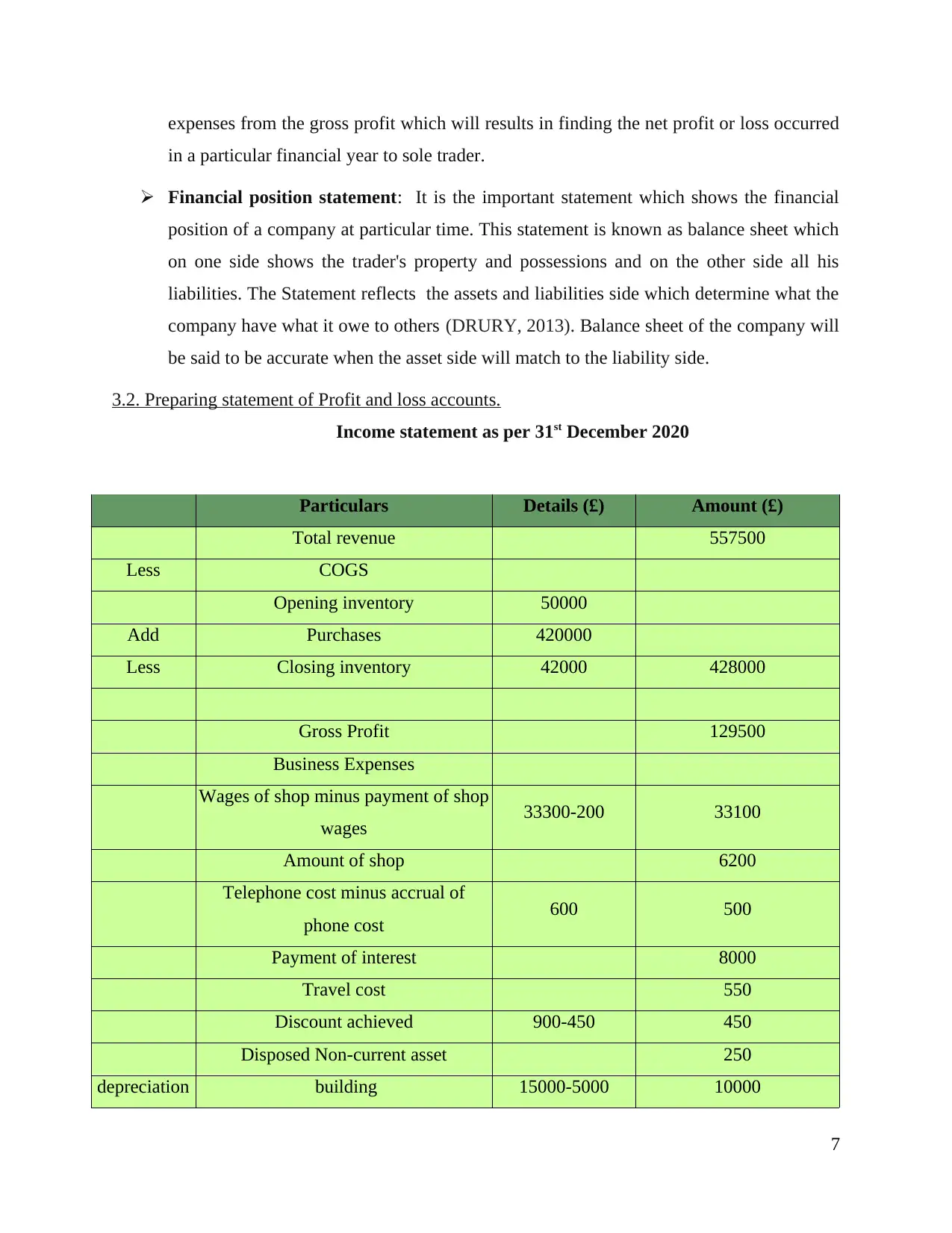

3.2. Preparing statement of Profit and loss accounts.

Income statement as per 31st December 2020

Particulars Details (£) Amount (£)

Total revenue 557500

Less COGS

Opening inventory 50000

Add Purchases 420000

Less Closing inventory 42000 428000

Gross Profit 129500

Business Expenses

Wages of shop minus payment of shop

wages 33300-200 33100

Amount of shop 6200

Telephone cost minus accrual of

phone cost 600 500

Payment of interest 8000

Travel cost 550

Discount achieved 900-450 450

Disposed Non-current asset 250

depreciation building 15000-5000 10000

7

in a particular financial year to sole trader.

Financial position statement: It is the important statement which shows the financial

position of a company at particular time. This statement is known as balance sheet which

on one side shows the trader's property and possessions and on the other side all his

liabilities. The Statement reflects the assets and liabilities side which determine what the

company have what it owe to others (DRURY, 2013). Balance sheet of the company will

be said to be accurate when the asset side will match to the liability side.

3.2. Preparing statement of Profit and loss accounts.

Income statement as per 31st December 2020

Particulars Details (£) Amount (£)

Total revenue 557500

Less COGS

Opening inventory 50000

Add Purchases 420000

Less Closing inventory 42000 428000

Gross Profit 129500

Business Expenses

Wages of shop minus payment of shop

wages 33300-200 33100

Amount of shop 6200

Telephone cost minus accrual of

phone cost 600 500

Payment of interest 8000

Travel cost 550

Discount achieved 900-450 450

Disposed Non-current asset 250

depreciation building 15000-5000 10000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

depreciation shop 14400-6400 8000

Bad debt written off 500

Allowance of doubtful debt 250

adjustment related to allowance for

doubtful debt 50 800

Sum of business expenses 67850

Operating profit 61650

Less Value added tax 3250

Net profit 58400

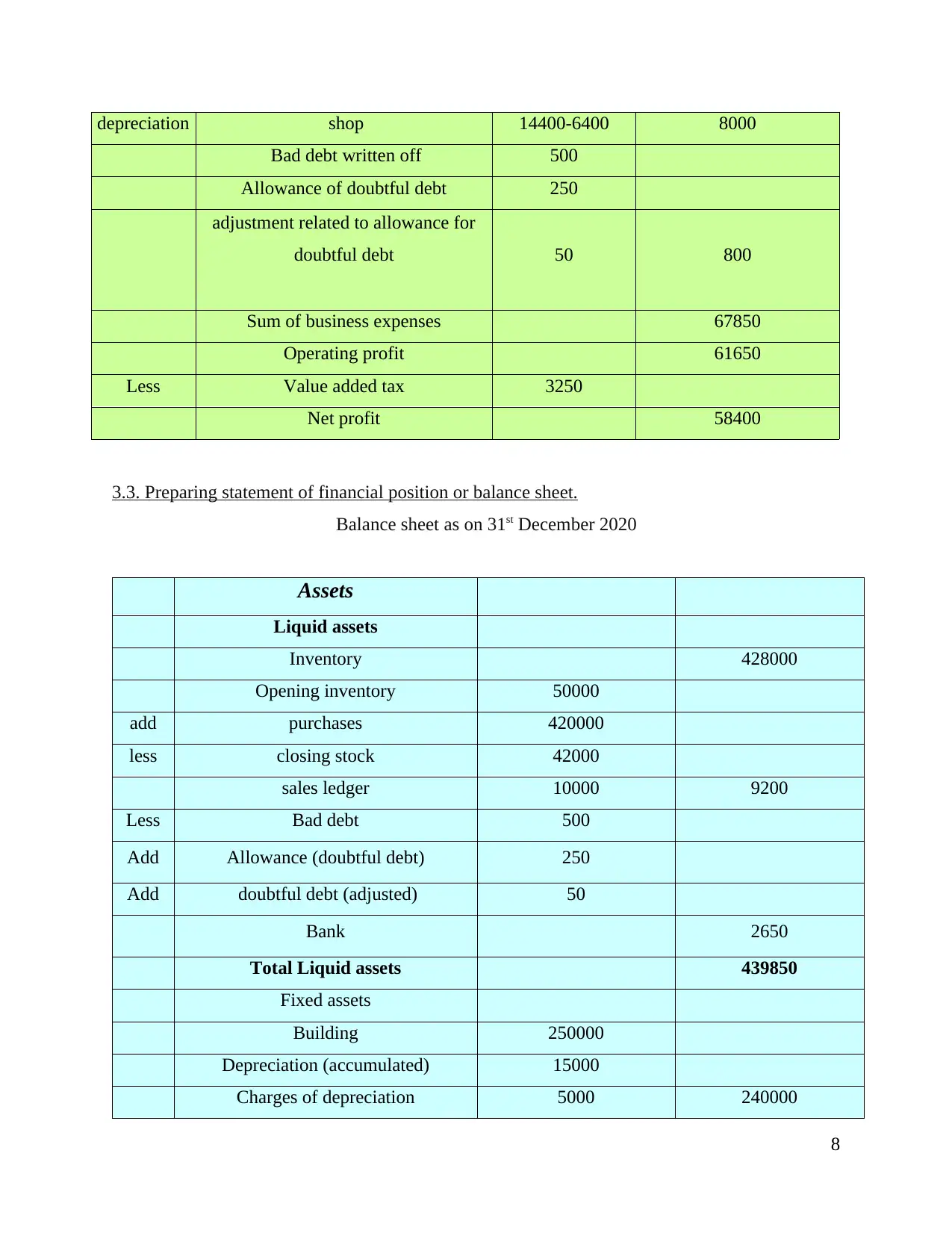

3.3. Preparing statement of financial position or balance sheet.

Balance sheet as on 31st December 2020

Assets

Liquid assets

Inventory 428000

Opening inventory 50000

add purchases 420000

less closing stock 42000

sales ledger 10000 9200

Less Bad debt 500

Add Allowance (doubtful debt) 250

Add doubtful debt (adjusted) 50

Bank 2650

Total Liquid assets 439850

Fixed assets

Building 250000

Depreciation (accumulated) 15000

Charges of depreciation 5000 240000

8

Bad debt written off 500

Allowance of doubtful debt 250

adjustment related to allowance for

doubtful debt 50 800

Sum of business expenses 67850

Operating profit 61650

Less Value added tax 3250

Net profit 58400

3.3. Preparing statement of financial position or balance sheet.

Balance sheet as on 31st December 2020

Assets

Liquid assets

Inventory 428000

Opening inventory 50000

add purchases 420000

less closing stock 42000

sales ledger 10000 9200

Less Bad debt 500

Add Allowance (doubtful debt) 250

Add doubtful debt (adjusted) 50

Bank 2650

Total Liquid assets 439850

Fixed assets

Building 250000

Depreciation (accumulated) 15000

Charges of depreciation 5000 240000

8

Cost for fitting shop 40000

less Depreciation (accumulated) 14400

less Charges for depreciation 6400 32000

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

VAT 3250

Borrowing 130000

Total current liabilities 144500

Non-Current 407950

Total Liabilities 552450

Equities 125000

less Borrowing 24000 101000

Net profit 58400

Total Liabilities and equity 711850

TASK4. Understanding legislative and accounting requirements for

partnership.

4.1. Describing the key components of partnership agreement.

Partnership can be defines as the relation between two or more persons who have agreed

to share profit and loss from the business that are carried by them. Partnership agreement is

designed to protect the interest of the partners, these agreement have two most important purpose

are dispute resolution and the business structure. The main components of partnership agreement

are:

9

less Depreciation (accumulated) 14400

less Charges for depreciation 6400 32000

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

VAT 3250

Borrowing 130000

Total current liabilities 144500

Non-Current 407950

Total Liabilities 552450

Equities 125000

less Borrowing 24000 101000

Net profit 58400

Total Liabilities and equity 711850

TASK4. Understanding legislative and accounting requirements for

partnership.

4.1. Describing the key components of partnership agreement.

Partnership can be defines as the relation between two or more persons who have agreed

to share profit and loss from the business that are carried by them. Partnership agreement is

designed to protect the interest of the partners, these agreement have two most important purpose

are dispute resolution and the business structure. The main components of partnership agreement

are:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.