Preparing and Analyzing Final Accounts: Sole Trader & Partnerships

VerifiedAdded on 2020/11/12

|20

|4013

|197

Report

AI Summary

This report delves into the preparation of final accounts for both sole trader and partnership businesses, covering essential aspects of financial accounting. It begins by explaining the reasons for closing accounts and preparing trial balances, followed by the procedures for creating final statements. The report also details methodologies for handling incomplete records, addressing issues arising from incorrect double entries and inconsistent data. Task 2 focuses on practical applications, including preparing accounting records from incomplete data, calculating cash/bank balances, and preparing sales and purchase ledger control accounts. Task 3 outlines the components of final accounts for sole traders, including profit and loss accounts and balance sheets. The report then moves on to partnership accounting, examining key elements of partnership agreements and accounting procedures. Task 5 demonstrates the preparation of a profit and loss appropriation account and profit distribution, while Task 6 addresses the calculation of closing balances for partner capital and current accounts, culminating in the preparation of a balance sheet in compliance with partnership agreements. The report is a comprehensive guide to understanding and preparing final accounts.

PRPARATION OF FINAL

ACCOUNTS OF SOLE

TRADER-SHIP AND

PARTNERSHIP

BUSINESSES

Table of Contents

INTRODUCTION...........................................................................................................................1

ACCOUNTS OF SOLE

TRADER-SHIP AND

PARTNERSHIP

BUSINESSES

Table of Contents

INTRODUCTION...........................................................................................................................1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 1............................................................................................................................................1

1.1 Determining the reasons of closing off accounts and preparing the trial balance ................1

1.2 Examining the of the procedure of preparation of final statements after the preparation of

trial balance .................................................................................................................................2

1.3 Description regarding the methodology of preparing the final accounts from incomplete

records..........................................................................................................................................2

1.4 Logic behind mismatch resulted from the incorrect double entries.......................................3

1.5 Description about the resulting of incomplete records occurs due to incomplete and

inconsistent data .........................................................................................................................3

TASK 2............................................................................................................................................4

2.1 Preparing the accounting records with the help of incomplete data......................................4

2.2 Calculation of opening/closing cash/bank account balance...................................................5

2.3 Preparation of sales and purchase ledger control accounts ...................................................5

TASK 3............................................................................................................................................6

3.1 Components of final accounts of the sole trader....................................................................6

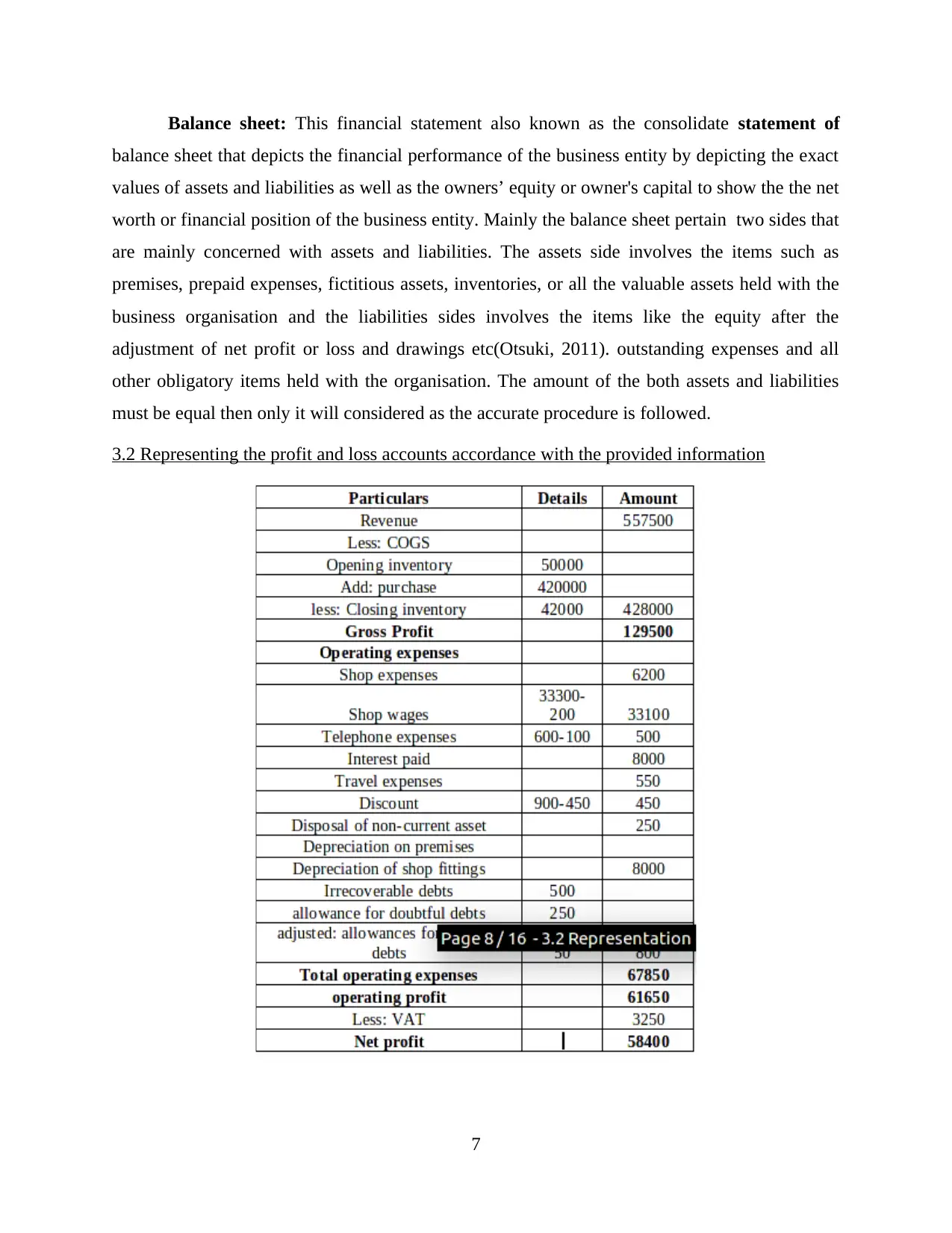

3.2 Representing the profit and loss accounts accordance with the provided information..........7

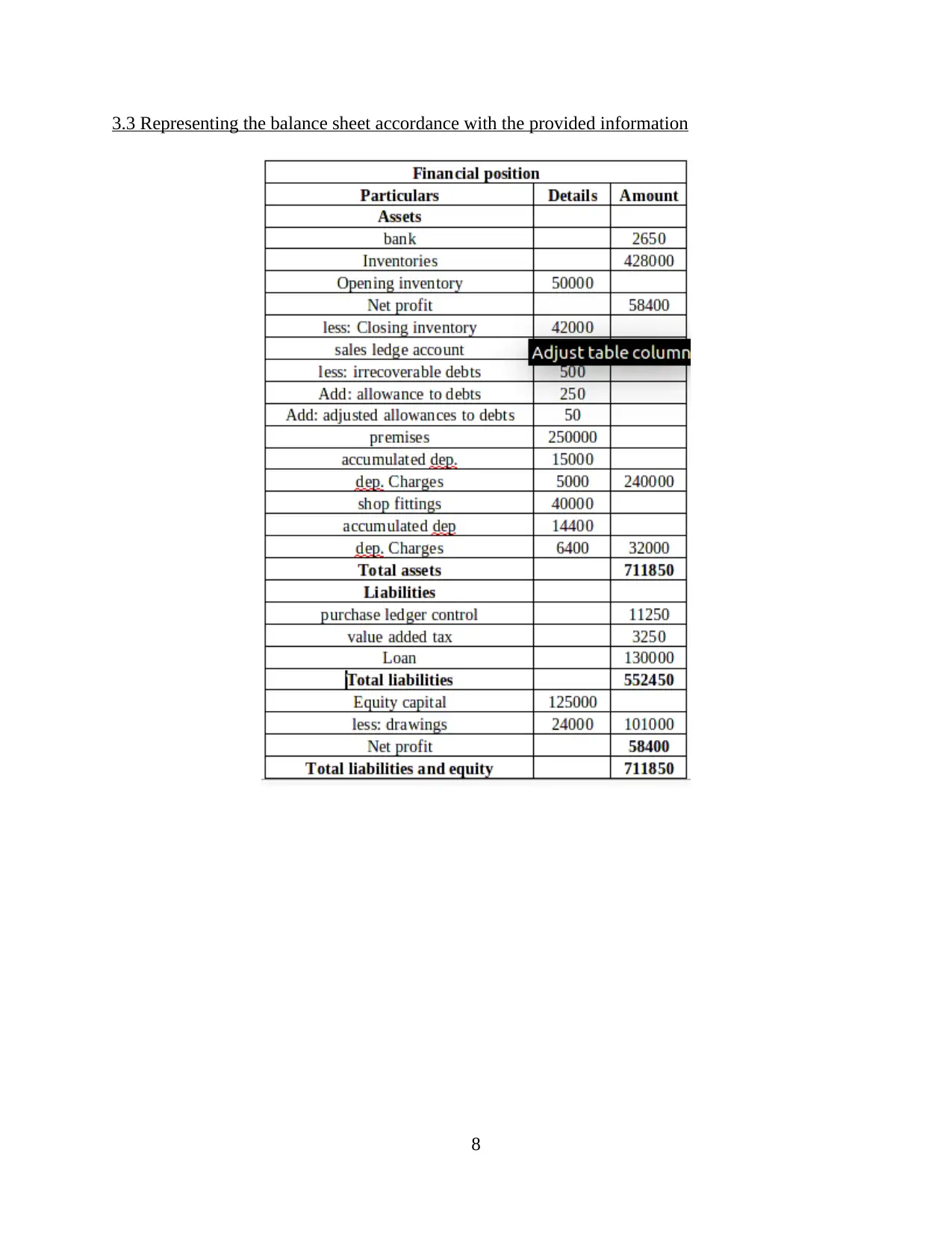

3.3 Representing the balance sheet accordance with the provided information..........................8

TASK 4............................................................................................................................................9

4.1 Examining the key elements pertain under the partnership agreements................................9

4.2 Explaining the key components pertain under partnership accounting procedure ...............9

TASK 5..........................................................................................................................................12

5.1 Preparation of profit and loss appropriation account for the partnership firm....................12

5.2 Determining the profits of partners profits..........................................................................13

TASK 6..........................................................................................................................................14

6.1 & 6.2 Measuring the closing balance on each partner’s current and capital account which

includes drawings and presenting balance sheet in compliance to partnership agreements .....14

CONLUSION................................................................................................................................15

REFERENCES..............................................................................................................................16

1.1 Determining the reasons of closing off accounts and preparing the trial balance ................1

1.2 Examining the of the procedure of preparation of final statements after the preparation of

trial balance .................................................................................................................................2

1.3 Description regarding the methodology of preparing the final accounts from incomplete

records..........................................................................................................................................2

1.4 Logic behind mismatch resulted from the incorrect double entries.......................................3

1.5 Description about the resulting of incomplete records occurs due to incomplete and

inconsistent data .........................................................................................................................3

TASK 2............................................................................................................................................4

2.1 Preparing the accounting records with the help of incomplete data......................................4

2.2 Calculation of opening/closing cash/bank account balance...................................................5

2.3 Preparation of sales and purchase ledger control accounts ...................................................5

TASK 3............................................................................................................................................6

3.1 Components of final accounts of the sole trader....................................................................6

3.2 Representing the profit and loss accounts accordance with the provided information..........7

3.3 Representing the balance sheet accordance with the provided information..........................8

TASK 4............................................................................................................................................9

4.1 Examining the key elements pertain under the partnership agreements................................9

4.2 Explaining the key components pertain under partnership accounting procedure ...............9

TASK 5..........................................................................................................................................12

5.1 Preparation of profit and loss appropriation account for the partnership firm....................12

5.2 Determining the profits of partners profits..........................................................................13

TASK 6..........................................................................................................................................14

6.1 & 6.2 Measuring the closing balance on each partner’s current and capital account which

includes drawings and presenting balance sheet in compliance to partnership agreements .....14

CONLUSION................................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial accounts are considered as the integral part of the accounting terminology and

it's procedure. As no business can operates without the perfect evaluation of the operations of the

business organisation in context of monetary terms(Kennedy, 2011). Only for this reason it is

inevitable to prepare the final accounts accordance with it's principle and concepts. Furthermore

the final accounts of any kind of organisation either sole trading or partnership or company, it

depicts the true financial performance of the organisation. For the purpose of preparing final

accounts all the accounts of debit and credit balance are required to be settle by closing off and

then the process of final accounts begins with the preparation of trial balance that depicts the

accurate amounts all accounts. This report comprises with the description regarding the

preparation of the consolidate statement of profit and loss accounts and the consolidate statement

of balance sheet. Overall, the report pertains the knowledge about the final accounts for sole

trading and partnership businesses.

TASK 1

1.1 Determining the reasons of closing off accounts and preparing the trial balance

At the time of closing of accounting period, the income and expenses accounts must be

transfer to trial balance for the execution. This, is because by doing this, all the revenues and

expenses accounts can be settled with their closing balances at the closing of accounting era. So

from the new accounting era the new accounts or the existing accounts can be starts with their

closing balances and closing off accounts are also beneficial in preparation of P&L account for

the calculation of the Net profit as well as for the preparation of the Balance sheet to know the

accurate and whole business performances(World Bank, 2014). After the preparation of journal

and ledger all the temporary accounts considered to close off, as it is required for preparing of

trial balance.

The Consolidate Trail Balance refers to category of final account kind of statement that is

to be prepare with an aim of recording all monetary transactions which are recorded in journal

the during accounting era and amounts are required to be equal together at the each side. The

reason behind the preparation of trial balance is to quantify the balances of the temporary

accounts that are closed off properly and total of credits and debits are required to be equal in the

closing entries made under the accounting procedure.

1

Financial accounts are considered as the integral part of the accounting terminology and

it's procedure. As no business can operates without the perfect evaluation of the operations of the

business organisation in context of monetary terms(Kennedy, 2011). Only for this reason it is

inevitable to prepare the final accounts accordance with it's principle and concepts. Furthermore

the final accounts of any kind of organisation either sole trading or partnership or company, it

depicts the true financial performance of the organisation. For the purpose of preparing final

accounts all the accounts of debit and credit balance are required to be settle by closing off and

then the process of final accounts begins with the preparation of trial balance that depicts the

accurate amounts all accounts. This report comprises with the description regarding the

preparation of the consolidate statement of profit and loss accounts and the consolidate statement

of balance sheet. Overall, the report pertains the knowledge about the final accounts for sole

trading and partnership businesses.

TASK 1

1.1 Determining the reasons of closing off accounts and preparing the trial balance

At the time of closing of accounting period, the income and expenses accounts must be

transfer to trial balance for the execution. This, is because by doing this, all the revenues and

expenses accounts can be settled with their closing balances at the closing of accounting era. So

from the new accounting era the new accounts or the existing accounts can be starts with their

closing balances and closing off accounts are also beneficial in preparation of P&L account for

the calculation of the Net profit as well as for the preparation of the Balance sheet to know the

accurate and whole business performances(World Bank, 2014). After the preparation of journal

and ledger all the temporary accounts considered to close off, as it is required for preparing of

trial balance.

The Consolidate Trail Balance refers to category of final account kind of statement that is

to be prepare with an aim of recording all monetary transactions which are recorded in journal

the during accounting era and amounts are required to be equal together at the each side. The

reason behind the preparation of trial balance is to quantify the balances of the temporary

accounts that are closed off properly and total of credits and debits are required to be equal in the

closing entries made under the accounting procedure.

1

1.2 Examining the of the procedure of preparation of final statements after the preparation of trial

balance

` “The trial balance depicts the equality of debit balance and credit balances”. The Trial

balance refers to the statement of ledger accounts and their debit and credit balances for the

determination of recording procedure as the debit side and credit side must pertain the equal

balances(Carter, 2013). Trial balance can be termed as the paltry for preparing the further final

accounts. The trial balance accounts is required to be prepare in such a manner that, assets,

liabilities, equity, dividends, revenues and expenses. The appropriate procedure of trial balance

benefited for quantifying the accurate amounts of aspects of Balance sheet and P&L statement

not only this, it helpful in identification of several kinds of errors. The procedure of preparing the

final accounts from the trail balance described underneath:

Understand the nature and adjustments of trail balance transactions and adjustments.

Recording of all debit transactions which are to be recorded in the consolidate statement

of trail balance either on expense side of Trading account or in P&L account account.

Recording of all the credit transactions which are to be recorded in the consolidate

statement of trail balance either on income side of trading account or in P&L or may be

as liabilities in balance sheet must be considered for analysis for preparation of final

statements(Bergkamp and Kogan, 2013).

Posting of all the items, but only after confirming all relevant adjustments of each items

twice as each transaction has two fold effects.

Balancing of trading as well as the P&L A/c for the determination of the Gross profit /

loss and the Net profit/Net Loss .

Add the resulted profit with the balance of capital on the liabilities side of the consolidate

statement of balance sheet.

Take the total of the balance sheet.

1.3 Description regarding the methodology of preparing the final accounts from incomplete

records

Basically only three methods are evolved for the preparation of the final accounts from

the Incomplete records, which are mentioned underneath.

2

balance

` “The trial balance depicts the equality of debit balance and credit balances”. The Trial

balance refers to the statement of ledger accounts and their debit and credit balances for the

determination of recording procedure as the debit side and credit side must pertain the equal

balances(Carter, 2013). Trial balance can be termed as the paltry for preparing the further final

accounts. The trial balance accounts is required to be prepare in such a manner that, assets,

liabilities, equity, dividends, revenues and expenses. The appropriate procedure of trial balance

benefited for quantifying the accurate amounts of aspects of Balance sheet and P&L statement

not only this, it helpful in identification of several kinds of errors. The procedure of preparing the

final accounts from the trail balance described underneath:

Understand the nature and adjustments of trail balance transactions and adjustments.

Recording of all debit transactions which are to be recorded in the consolidate statement

of trail balance either on expense side of Trading account or in P&L account account.

Recording of all the credit transactions which are to be recorded in the consolidate

statement of trail balance either on income side of trading account or in P&L or may be

as liabilities in balance sheet must be considered for analysis for preparation of final

statements(Bergkamp and Kogan, 2013).

Posting of all the items, but only after confirming all relevant adjustments of each items

twice as each transaction has two fold effects.

Balancing of trading as well as the P&L A/c for the determination of the Gross profit /

loss and the Net profit/Net Loss .

Add the resulted profit with the balance of capital on the liabilities side of the consolidate

statement of balance sheet.

Take the total of the balance sheet.

1.3 Description regarding the methodology of preparing the final accounts from incomplete

records

Basically only three methods are evolved for the preparation of the final accounts from

the Incomplete records, which are mentioned underneath.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

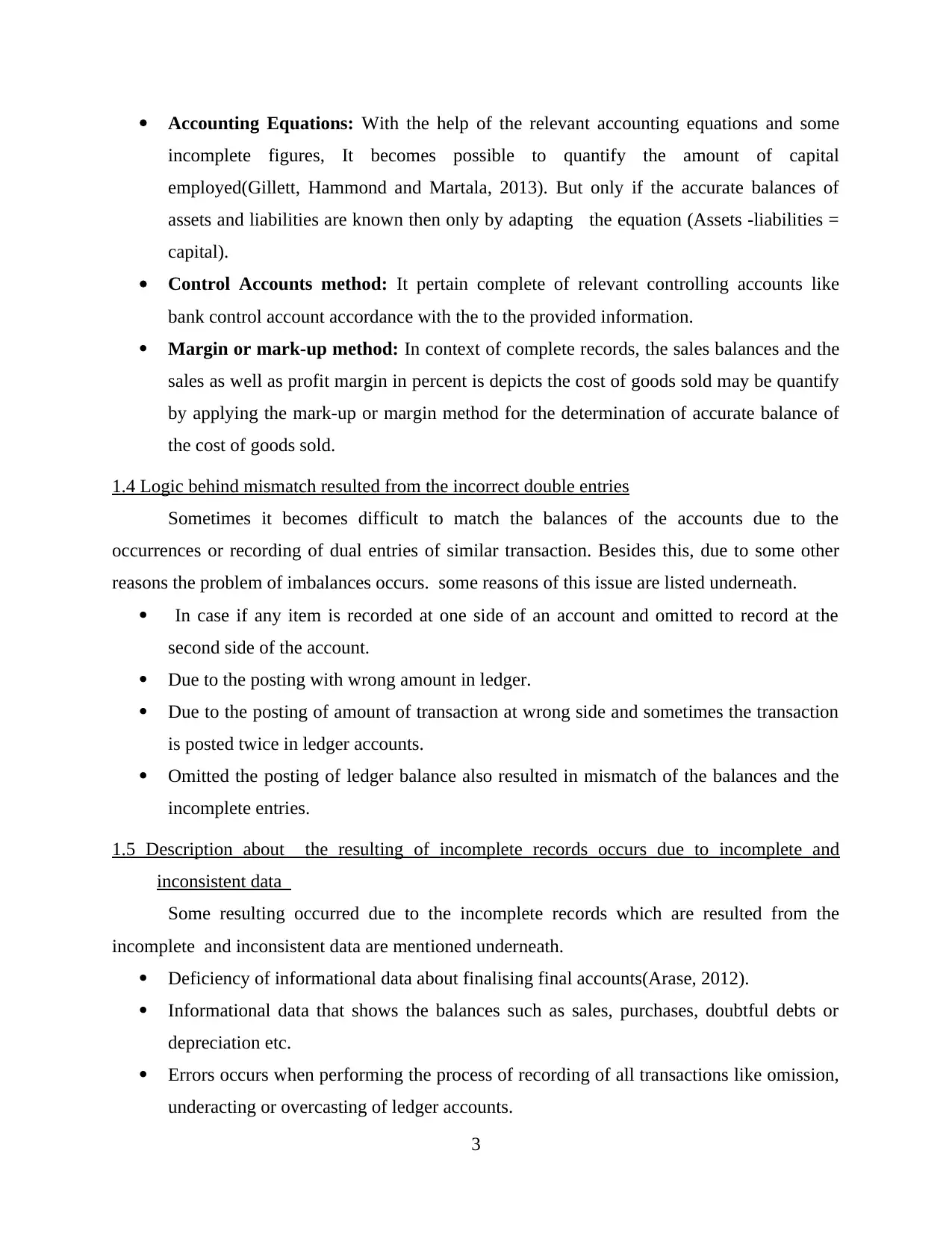

Accounting Equations: With the help of the relevant accounting equations and some

incomplete figures, It becomes possible to quantify the amount of capital

employed(Gillett, Hammond and Martala, 2013). But only if the accurate balances of

assets and liabilities are known then only by adapting the equation (Assets -liabilities =

capital).

Control Accounts method: It pertain complete of relevant controlling accounts like

bank control account accordance with the to the provided information.

Margin or mark-up method: In context of complete records, the sales balances and the

sales as well as profit margin in percent is depicts the cost of goods sold may be quantify

by applying the mark-up or margin method for the determination of accurate balance of

the cost of goods sold.

1.4 Logic behind mismatch resulted from the incorrect double entries

Sometimes it becomes difficult to match the balances of the accounts due to the

occurrences or recording of dual entries of similar transaction. Besides this, due to some other

reasons the problem of imbalances occurs. some reasons of this issue are listed underneath.

In case if any item is recorded at one side of an account and omitted to record at the

second side of the account.

Due to the posting with wrong amount in ledger.

Due to the posting of amount of transaction at wrong side and sometimes the transaction

is posted twice in ledger accounts.

Omitted the posting of ledger balance also resulted in mismatch of the balances and the

incomplete entries.

1.5 Description about the resulting of incomplete records occurs due to incomplete and

inconsistent data

Some resulting occurred due to the incomplete records which are resulted from the

incomplete and inconsistent data are mentioned underneath.

Deficiency of informational data about finalising final accounts(Arase, 2012).

Informational data that shows the balances such as sales, purchases, doubtful debts or

depreciation etc.

Errors occurs when performing the process of recording of all transactions like omission,

underacting or overcasting of ledger accounts.

3

incomplete figures, It becomes possible to quantify the amount of capital

employed(Gillett, Hammond and Martala, 2013). But only if the accurate balances of

assets and liabilities are known then only by adapting the equation (Assets -liabilities =

capital).

Control Accounts method: It pertain complete of relevant controlling accounts like

bank control account accordance with the to the provided information.

Margin or mark-up method: In context of complete records, the sales balances and the

sales as well as profit margin in percent is depicts the cost of goods sold may be quantify

by applying the mark-up or margin method for the determination of accurate balance of

the cost of goods sold.

1.4 Logic behind mismatch resulted from the incorrect double entries

Sometimes it becomes difficult to match the balances of the accounts due to the

occurrences or recording of dual entries of similar transaction. Besides this, due to some other

reasons the problem of imbalances occurs. some reasons of this issue are listed underneath.

In case if any item is recorded at one side of an account and omitted to record at the

second side of the account.

Due to the posting with wrong amount in ledger.

Due to the posting of amount of transaction at wrong side and sometimes the transaction

is posted twice in ledger accounts.

Omitted the posting of ledger balance also resulted in mismatch of the balances and the

incomplete entries.

1.5 Description about the resulting of incomplete records occurs due to incomplete and

inconsistent data

Some resulting occurred due to the incomplete records which are resulted from the

incomplete and inconsistent data are mentioned underneath.

Deficiency of informational data about finalising final accounts(Arase, 2012).

Informational data that shows the balances such as sales, purchases, doubtful debts or

depreciation etc.

Errors occurs when performing the process of recording of all transactions like omission,

underacting or overcasting of ledger accounts.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sometimes occurrences of the errors due to wrong evaluation or quantification of

balances comes under the equity and liabilities side as well as on assets side in

revaluation accounts and in balance sheet.

TASK 2

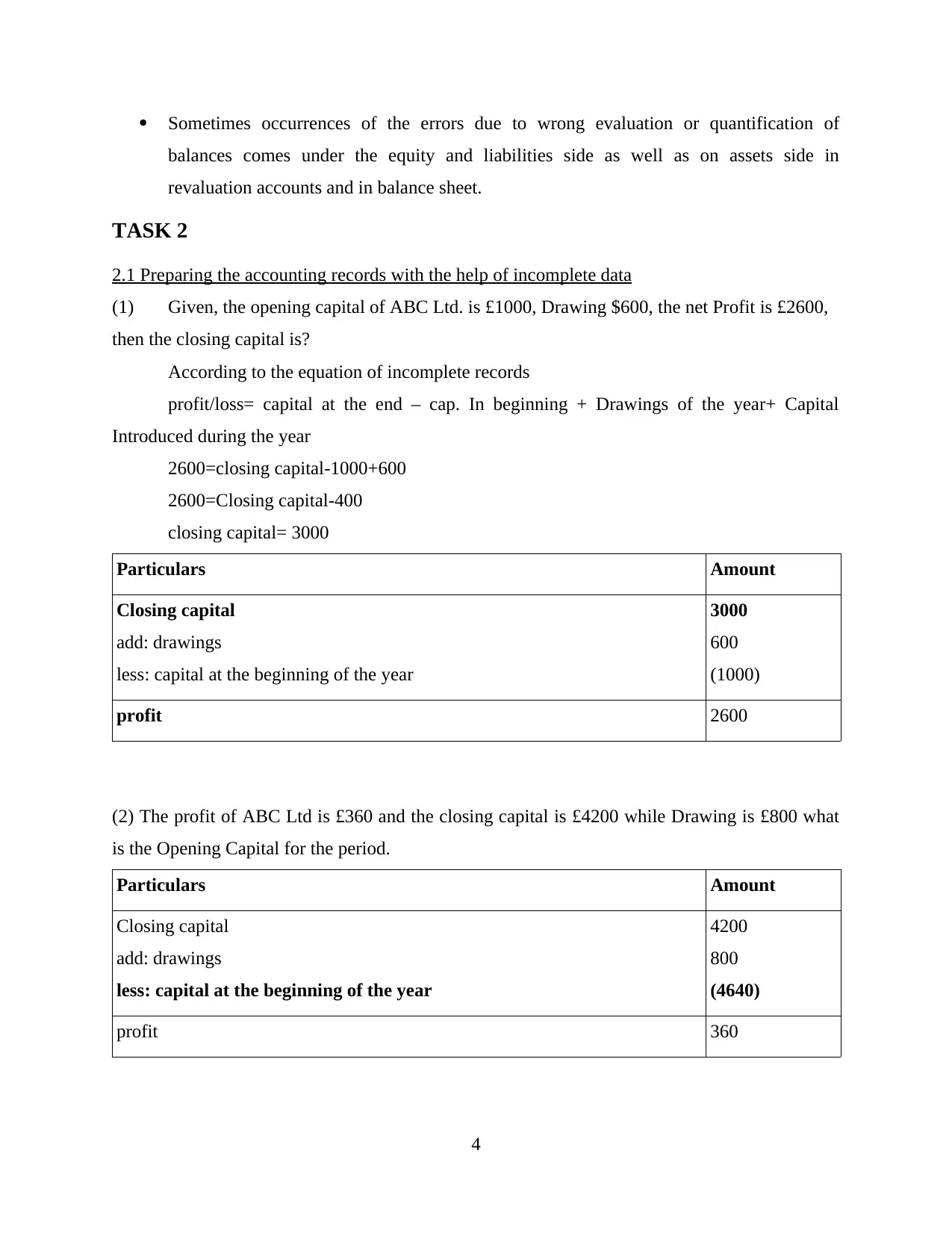

2.1 Preparing the accounting records with the help of incomplete data

(1) Given, the opening capital of ABC Ltd. is £1000, Drawing $600, the net Profit is £2600,

then the closing capital is?

According to the equation of incomplete records

profit/loss= capital at the end – cap. In beginning + Drawings of the year+ Capital

Introduced during the year

2600=closing capital-1000+600

2600=Closing capital-400

closing capital= 3000

Particulars Amount

Closing capital

add: drawings

less: capital at the beginning of the year

3000

600

(1000)

profit 2600

(2) The profit of ABC Ltd is £360 and the closing capital is £4200 while Drawing is £800 what

is the Opening Capital for the period.

Particulars Amount

Closing capital

add: drawings

less: capital at the beginning of the year

4200

800

(4640)

profit 360

4

balances comes under the equity and liabilities side as well as on assets side in

revaluation accounts and in balance sheet.

TASK 2

2.1 Preparing the accounting records with the help of incomplete data

(1) Given, the opening capital of ABC Ltd. is £1000, Drawing $600, the net Profit is £2600,

then the closing capital is?

According to the equation of incomplete records

profit/loss= capital at the end – cap. In beginning + Drawings of the year+ Capital

Introduced during the year

2600=closing capital-1000+600

2600=Closing capital-400

closing capital= 3000

Particulars Amount

Closing capital

add: drawings

less: capital at the beginning of the year

3000

600

(1000)

profit 2600

(2) The profit of ABC Ltd is £360 and the closing capital is £4200 while Drawing is £800 what

is the Opening Capital for the period.

Particulars Amount

Closing capital

add: drawings

less: capital at the beginning of the year

4200

800

(4640)

profit 360

4

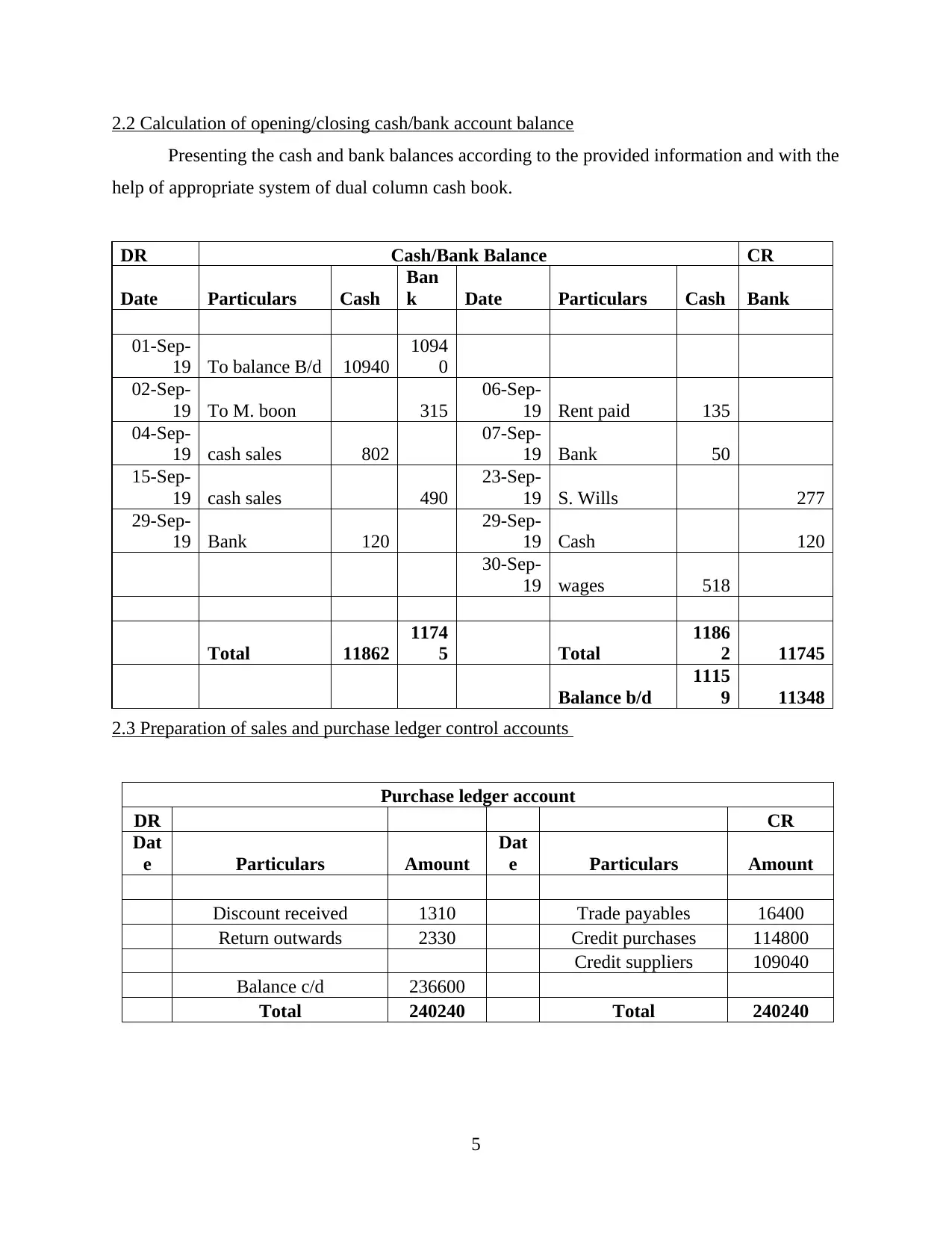

2.2 Calculation of opening/closing cash/bank account balance

Presenting the cash and bank balances according to the provided information and with the

help of appropriate system of dual column cash book.

DR Cash/Bank Balance CR

Date Particulars Cash

Ban

k Date Particulars Cash Bank

01-Sep-

19 To balance B/d 10940

1094

0

02-Sep-

19 To M. boon 315

06-Sep-

19 Rent paid 135

04-Sep-

19 cash sales 802

07-Sep-

19 Bank 50

15-Sep-

19 cash sales 490

23-Sep-

19 S. Wills 277

29-Sep-

19 Bank 120

29-Sep-

19 Cash 120

30-Sep-

19 wages 518

Total 11862

1174

5 Total

1186

2 11745

Balance b/d

1115

9 11348

2.3 Preparation of sales and purchase ledger control accounts

Purchase ledger account

DR CR

Dat

e Particulars Amount

Dat

e Particulars Amount

Discount received 1310 Trade payables 16400

Return outwards 2330 Credit purchases 114800

Credit suppliers 109040

Balance c/d 236600

Total 240240 Total 240240

5

Presenting the cash and bank balances according to the provided information and with the

help of appropriate system of dual column cash book.

DR Cash/Bank Balance CR

Date Particulars Cash

Ban

k Date Particulars Cash Bank

01-Sep-

19 To balance B/d 10940

1094

0

02-Sep-

19 To M. boon 315

06-Sep-

19 Rent paid 135

04-Sep-

19 cash sales 802

07-Sep-

19 Bank 50

15-Sep-

19 cash sales 490

23-Sep-

19 S. Wills 277

29-Sep-

19 Bank 120

29-Sep-

19 Cash 120

30-Sep-

19 wages 518

Total 11862

1174

5 Total

1186

2 11745

Balance b/d

1115

9 11348

2.3 Preparation of sales and purchase ledger control accounts

Purchase ledger account

DR CR

Dat

e Particulars Amount

Dat

e Particulars Amount

Discount received 1310 Trade payables 16400

Return outwards 2330 Credit purchases 114800

Credit suppliers 109040

Balance c/d 236600

Total 240240 Total 240240

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

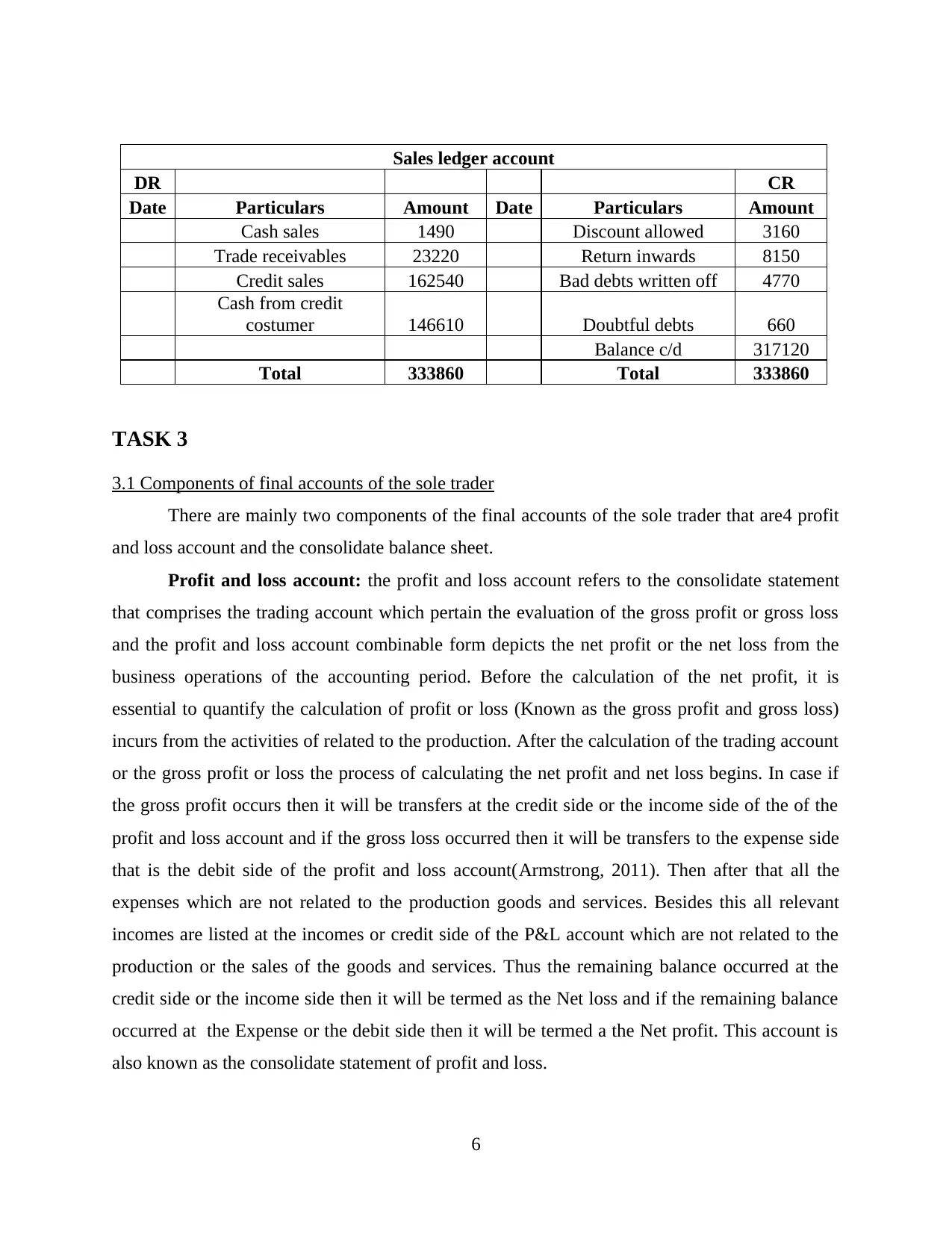

Sales ledger account

DR CR

Date Particulars Amount Date Particulars Amount

Cash sales 1490 Discount allowed 3160

Trade receivables 23220 Return inwards 8150

Credit sales 162540 Bad debts written off 4770

Cash from credit

costumer 146610 Doubtful debts 660

Balance c/d 317120

Total 333860 Total 333860

TASK 3

3.1 Components of final accounts of the sole trader

There are mainly two components of the final accounts of the sole trader that are4 profit

and loss account and the consolidate balance sheet.

Profit and loss account: the profit and loss account refers to the consolidate statement

that comprises the trading account which pertain the evaluation of the gross profit or gross loss

and the profit and loss account combinable form depicts the net profit or the net loss from the

business operations of the accounting period. Before the calculation of the net profit, it is

essential to quantify the calculation of profit or loss (Known as the gross profit and gross loss)

incurs from the activities of related to the production. After the calculation of the trading account

or the gross profit or loss the process of calculating the net profit and net loss begins. In case if

the gross profit occurs then it will be transfers at the credit side or the income side of the of the

profit and loss account and if the gross loss occurred then it will be transfers to the expense side

that is the debit side of the profit and loss account(Armstrong, 2011). Then after that all the

expenses which are not related to the production goods and services. Besides this all relevant

incomes are listed at the incomes or credit side of the P&L account which are not related to the

production or the sales of the goods and services. Thus the remaining balance occurred at the

credit side or the income side then it will be termed as the Net loss and if the remaining balance

occurred at the Expense or the debit side then it will be termed a the Net profit. This account is

also known as the consolidate statement of profit and loss.

6

DR CR

Date Particulars Amount Date Particulars Amount

Cash sales 1490 Discount allowed 3160

Trade receivables 23220 Return inwards 8150

Credit sales 162540 Bad debts written off 4770

Cash from credit

costumer 146610 Doubtful debts 660

Balance c/d 317120

Total 333860 Total 333860

TASK 3

3.1 Components of final accounts of the sole trader

There are mainly two components of the final accounts of the sole trader that are4 profit

and loss account and the consolidate balance sheet.

Profit and loss account: the profit and loss account refers to the consolidate statement

that comprises the trading account which pertain the evaluation of the gross profit or gross loss

and the profit and loss account combinable form depicts the net profit or the net loss from the

business operations of the accounting period. Before the calculation of the net profit, it is

essential to quantify the calculation of profit or loss (Known as the gross profit and gross loss)

incurs from the activities of related to the production. After the calculation of the trading account

or the gross profit or loss the process of calculating the net profit and net loss begins. In case if

the gross profit occurs then it will be transfers at the credit side or the income side of the of the

profit and loss account and if the gross loss occurred then it will be transfers to the expense side

that is the debit side of the profit and loss account(Armstrong, 2011). Then after that all the

expenses which are not related to the production goods and services. Besides this all relevant

incomes are listed at the incomes or credit side of the P&L account which are not related to the

production or the sales of the goods and services. Thus the remaining balance occurred at the

credit side or the income side then it will be termed as the Net loss and if the remaining balance

occurred at the Expense or the debit side then it will be termed a the Net profit. This account is

also known as the consolidate statement of profit and loss.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Balance sheet: This financial statement also known as the consolidate statement of

balance sheet that depicts the financial performance of the business entity by depicting the exact

values of assets and liabilities as well as the owners’ equity or owner's capital to show the the net

worth or financial position of the business entity. Mainly the balance sheet pertain two sides that

are mainly concerned with assets and liabilities. The assets side involves the items such as

premises, prepaid expenses, fictitious assets, inventories, or all the valuable assets held with the

business organisation and the liabilities sides involves the items like the equity after the

adjustment of net profit or loss and drawings etc(Otsuki, 2011). outstanding expenses and all

other obligatory items held with the organisation. The amount of the both assets and liabilities

must be equal then only it will considered as the accurate procedure is followed.

3.2 Representing the profit and loss accounts accordance with the provided information

7

balance sheet that depicts the financial performance of the business entity by depicting the exact

values of assets and liabilities as well as the owners’ equity or owner's capital to show the the net

worth or financial position of the business entity. Mainly the balance sheet pertain two sides that

are mainly concerned with assets and liabilities. The assets side involves the items such as

premises, prepaid expenses, fictitious assets, inventories, or all the valuable assets held with the

business organisation and the liabilities sides involves the items like the equity after the

adjustment of net profit or loss and drawings etc(Otsuki, 2011). outstanding expenses and all

other obligatory items held with the organisation. The amount of the both assets and liabilities

must be equal then only it will considered as the accurate procedure is followed.

3.2 Representing the profit and loss accounts accordance with the provided information

7

3.3 Representing the balance sheet accordance with the provided information

8

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.