Final Accounts: Preparation for Sole Traders and Partnerships

VerifiedAdded on 2020/12/18

|17

|4244

|309

Report

AI Summary

This report delves into the preparation and analysis of final accounts for sole traders and partnerships. It begins with the reasons for closing off accounts and producing a trial balance, discussing the processes and limitations of preparing final accounts, and exploring methods of constructing accounts from incomplete records. The report then covers the calculation of opening and closing capital, as well as opening and closing cash/bank accounts, alongside the preparation of sales and purchase ledger control accounts, and the concepts of markups and margins. It further elaborates on the components of final accounts, including the statement of profit and loss and the statement of financial position. The report extends to partnership accounts, outlining key components of partnership agreements and accounts, the statement of profit and loss appropriation account, and the allocation of profit to partners, including capital and current accounts. Finally, it addresses the calculation of closing balances for each partner's capital and current account and the construction of the statement of financial position. The report concludes with a comprehensive overview of the key aspects of final account preparation and analysis for both sole traders and partnerships.

Prepare final accounts for sole

traders and partnerships

traders and partnerships

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Reasons for closing off and producing trial balance.............................................................1

1.2 Process and limitation of preparing final accounts...............................................................1

1.3 Methods of constructing accounts from incomplete records................................................2

1.4 Reasons for imbalance resulting from incorrect double entries............................................2

1.5 Reasons for incomplete records arising from insufficient data ............................................3

TASK 2............................................................................................................................................3

2.1 Calculation of opening and closing capital...........................................................................3

2.2 Calculation of opening and closing cash/ bank account......................................................4

2.3 Preparation of sales and purchase ledger control account....................................................5

2.4 Mark ups and margins...........................................................................................................6

TASK 3............................................................................................................................................6

3.1 Components of a set of final accounts..................................................................................6

3.2 statement of profit and loss...................................................................................................7

3.3 statement of financial position..............................................................................................8

TASK 4............................................................................................................................................9

4.1 Key components of partnership agreement...........................................................................9

4.2 Key components of partnership accounts...........................................................................10

TASK 5..........................................................................................................................................11

5.1 Statement of profit and loss appropriation account ............................................................11

5.2 The allocation of profit to partners after allowing for interest on capital, interest on

drawings and any salary paid to partner(s)...............................................................................12

5.3 capital and current accounts for each partner......................................................................12

TASK 6..........................................................................................................................................12

6.1 Calculation of closing balance of each partner's capital and current account.....................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Reasons for closing off and producing trial balance.............................................................1

1.2 Process and limitation of preparing final accounts...............................................................1

1.3 Methods of constructing accounts from incomplete records................................................2

1.4 Reasons for imbalance resulting from incorrect double entries............................................2

1.5 Reasons for incomplete records arising from insufficient data ............................................3

TASK 2............................................................................................................................................3

2.1 Calculation of opening and closing capital...........................................................................3

2.2 Calculation of opening and closing cash/ bank account......................................................4

2.3 Preparation of sales and purchase ledger control account....................................................5

2.4 Mark ups and margins...........................................................................................................6

TASK 3............................................................................................................................................6

3.1 Components of a set of final accounts..................................................................................6

3.2 statement of profit and loss...................................................................................................7

3.3 statement of financial position..............................................................................................8

TASK 4............................................................................................................................................9

4.1 Key components of partnership agreement...........................................................................9

4.2 Key components of partnership accounts...........................................................................10

TASK 5..........................................................................................................................................11

5.1 Statement of profit and loss appropriation account ............................................................11

5.2 The allocation of profit to partners after allowing for interest on capital, interest on

drawings and any salary paid to partner(s)...............................................................................12

5.3 capital and current accounts for each partner......................................................................12

TASK 6..........................................................................................................................................12

6.1 Calculation of closing balance of each partner's capital and current account.....................12

6.2 Statement of financial position............................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Final accounts are the financial statements that are required to analyse organisational

performance, position and financial health (Bain and Band, 2016). It guides the owners to make

appropriate decisions so that business can be operated effectively. Final accounts of partnership

firms and sole proprietorship are same but the profits are divided differently. The ratio of profit

distribution in partnership firms are pre decided by the partners. In a sole proprietorship firm all

the profit will be owned by owner of organization. This report is based on final accounts of sole

trader and partnership firm. Sole trader is the single owner of the company so only income

statement and balance sheet will be generated and in partnership firm with these accounts capital

and current account of partners also prepared. This assignment aims at need and process of

preparing final accounts from incomplete accounting records. Statement of profit and loss

account and financial positions relating to partnership have been created under this report.

TASK 1

1.1 Reasons for closing off and producing trial balance

The main reasons behind closing of revenue and expense accounts is that all accounts can

be recreated next year with zero balance base. The purpose is also to transfer the balances of

temporary accounts to permanent accounts. In closing process only expenses, revenues and

dividend accounts are closed because if their balance is being carried forward by the organisation

than this may create more liabilities (Barrow,Barrow and Brown, 2012).

Trial balance if prepared by the companies to detect mathematical errors in journal or

ledgers. It is also created to prove that all the debit balances are equal to credit balances. If the

total of both the amounts does not match than it depicts that there is an error in the ledger

accounts. Partners or owner of the firm formulate trail balance to analyse arithmetical accuracy

of the transactions.

1.2 Process and limitation of preparing final accounts

Trial balance is prepared for checking the mathematical accuracy. It is a statement in

which all balances of accounts are recorded. First of all, accounts of all the ledgers have been

closed , subsidiary and cash as well as bank account. After that a three column statement is

generated in which balances of all the accounts are recorded. That statement includes particulars,

1

Final accounts are the financial statements that are required to analyse organisational

performance, position and financial health (Bain and Band, 2016). It guides the owners to make

appropriate decisions so that business can be operated effectively. Final accounts of partnership

firms and sole proprietorship are same but the profits are divided differently. The ratio of profit

distribution in partnership firms are pre decided by the partners. In a sole proprietorship firm all

the profit will be owned by owner of organization. This report is based on final accounts of sole

trader and partnership firm. Sole trader is the single owner of the company so only income

statement and balance sheet will be generated and in partnership firm with these accounts capital

and current account of partners also prepared. This assignment aims at need and process of

preparing final accounts from incomplete accounting records. Statement of profit and loss

account and financial positions relating to partnership have been created under this report.

TASK 1

1.1 Reasons for closing off and producing trial balance

The main reasons behind closing of revenue and expense accounts is that all accounts can

be recreated next year with zero balance base. The purpose is also to transfer the balances of

temporary accounts to permanent accounts. In closing process only expenses, revenues and

dividend accounts are closed because if their balance is being carried forward by the organisation

than this may create more liabilities (Barrow,Barrow and Brown, 2012).

Trial balance if prepared by the companies to detect mathematical errors in journal or

ledgers. It is also created to prove that all the debit balances are equal to credit balances. If the

total of both the amounts does not match than it depicts that there is an error in the ledger

accounts. Partners or owner of the firm formulate trail balance to analyse arithmetical accuracy

of the transactions.

1.2 Process and limitation of preparing final accounts

Trial balance is prepared for checking the mathematical accuracy. It is a statement in

which all balances of accounts are recorded. First of all, accounts of all the ledgers have been

closed , subsidiary and cash as well as bank account. After that a three column statement is

generated in which balances of all the accounts are recorded. That statement includes particulars,

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

debit and credit columns. If at last credit and debit side of trial balance is not same then there will

be arithmetical error.

Limitation of preparing a trial balance:

It only focus on errors not the reasons behind the errors.

It only shows arithmetical errors.

Errors are not detected if appropriate accounting principles are not followed by the

accountant.

It does not pay attention toward double posting of any entry by mistake.

Ignores the posting of right amount in wrong account.

1.3 Methods of constructing accounts from incomplete records

There are various methods that are used to formulate accounts with the help of

incomplete record. These methods are as follows:

The accounting equation: This method is used by the accountants if the value of capital

is not provided by the client (Bennett, Schaltegger and Zvezdov, 2013). According to this

method, total liabilities subtracting from total assets and difference will denote the total capital.

That equation is called as accounting equation and method of formulate accounts from

incomplete records.

Control accounts: If balance of different accounts are missed than control account

method can be used in this condition. In this method a control account is being completed by the

accountants for example in bank control account the account will be created with the help of

available information and the balance of credit and debit side will be assumed as the missing

information.

Markup or margin method: In this method markup or margin percentage is used by the

accountant in which missing information is calculated with the help of margin percentage

method (Chambers, 2014). If the amount of sales and percentage of margin is available. Then

cost of sales can be calculated with the help of sales and percentage of margin putting them in

margin percentage method.

1.4 Reasons for imbalance resulting from incorrect double entries

The following mentioned are some of the major reasons behind the imbalance from

incorrect entries:

2

be arithmetical error.

Limitation of preparing a trial balance:

It only focus on errors not the reasons behind the errors.

It only shows arithmetical errors.

Errors are not detected if appropriate accounting principles are not followed by the

accountant.

It does not pay attention toward double posting of any entry by mistake.

Ignores the posting of right amount in wrong account.

1.3 Methods of constructing accounts from incomplete records

There are various methods that are used to formulate accounts with the help of

incomplete record. These methods are as follows:

The accounting equation: This method is used by the accountants if the value of capital

is not provided by the client (Bennett, Schaltegger and Zvezdov, 2013). According to this

method, total liabilities subtracting from total assets and difference will denote the total capital.

That equation is called as accounting equation and method of formulate accounts from

incomplete records.

Control accounts: If balance of different accounts are missed than control account

method can be used in this condition. In this method a control account is being completed by the

accountants for example in bank control account the account will be created with the help of

available information and the balance of credit and debit side will be assumed as the missing

information.

Markup or margin method: In this method markup or margin percentage is used by the

accountant in which missing information is calculated with the help of margin percentage

method (Chambers, 2014). If the amount of sales and percentage of margin is available. Then

cost of sales can be calculated with the help of sales and percentage of margin putting them in

margin percentage method.

1.4 Reasons for imbalance resulting from incorrect double entries

The following mentioned are some of the major reasons behind the imbalance from

incorrect entries:

2

If the amount is recorded in only one account but not recorded in another related account.

For example if cash purchases amount is recorded in purchase account but not recorded

in sales account than it may create a imbalance.

Incorrect amount posted in wrong account caused for imbalance in trial balance. For

example, amount of rent account posted in wages account by incorrect amount.

If particular entry is posted twice than it will cause unbalancing problem in trial balance.

1.5 Reasons for incomplete records arising from insufficient data

All of the reasons are explained for incomplete records that may be arise due to

insufficient data are as follows:

Abnormal failure in records: The problem occur when any employee forgot to record

transaction unintentionally (Christensen and Feltham, 2012). When accountants are not

able to follow appropriate accounting principles then this problem also may occur .

Data loss: As in today's world paper work moved to accounting software to record

transactions. It also caused for the problem of data loss, because if employees sometime

forgot to save data in accounting software.

Employees turnover: sometimes workers leave an business organization than

intentionally or by mistake they take accounting record with them that lead the company

to the problem of inconsistent or insufficient data.

Intentional manipulation: Business owners make mistakes in the books of accounting

while recording transactions to manipulate the accounts to save tax or any other purpose.

TASK 2

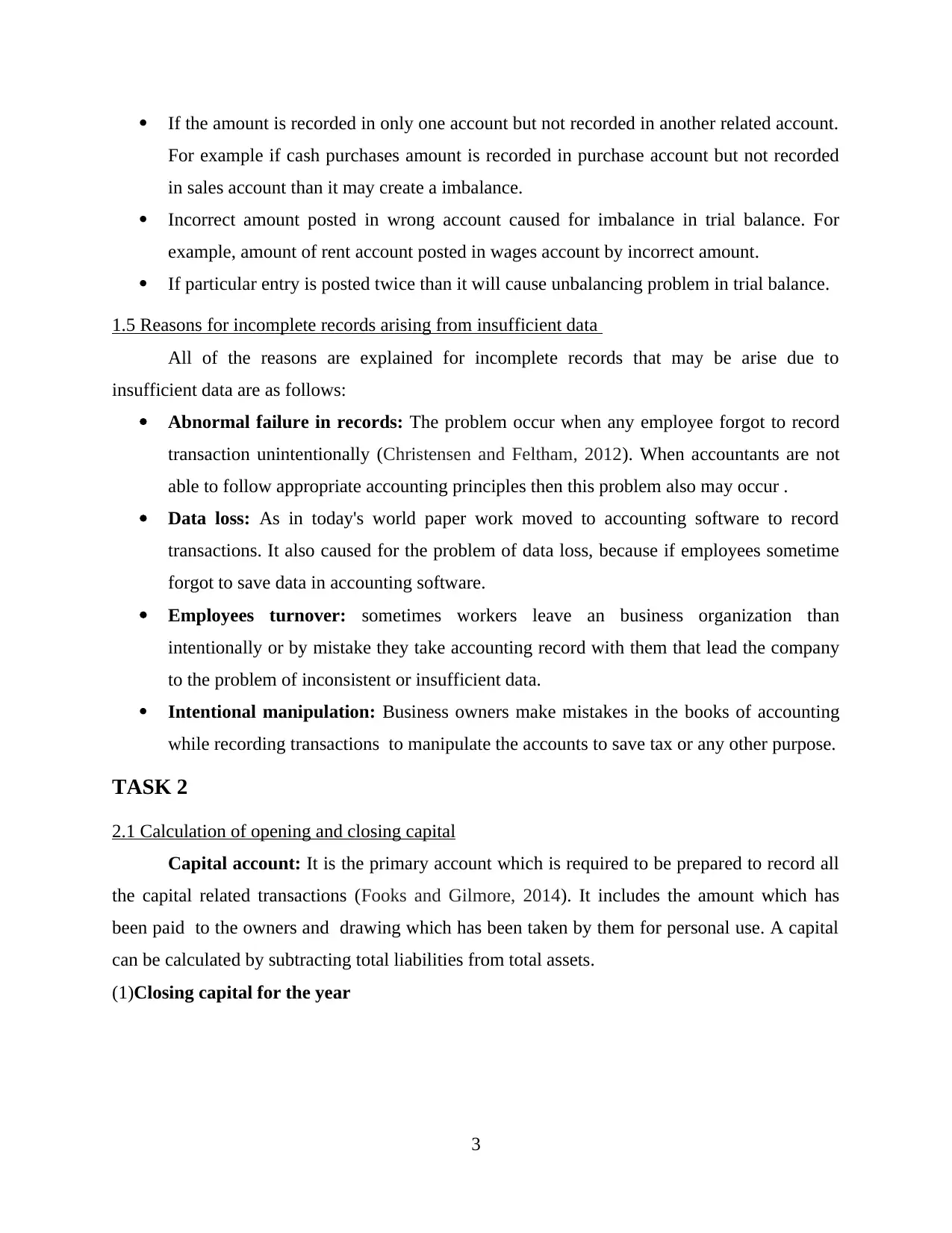

2.1 Calculation of opening and closing capital

Capital account: It is the primary account which is required to be prepared to record all

the capital related transactions (Fooks and Gilmore, 2014). It includes the amount which has

been paid to the owners and drawing which has been taken by them for personal use. A capital

can be calculated by subtracting total liabilities from total assets.

(1)Closing capital for the year

3

For example if cash purchases amount is recorded in purchase account but not recorded

in sales account than it may create a imbalance.

Incorrect amount posted in wrong account caused for imbalance in trial balance. For

example, amount of rent account posted in wages account by incorrect amount.

If particular entry is posted twice than it will cause unbalancing problem in trial balance.

1.5 Reasons for incomplete records arising from insufficient data

All of the reasons are explained for incomplete records that may be arise due to

insufficient data are as follows:

Abnormal failure in records: The problem occur when any employee forgot to record

transaction unintentionally (Christensen and Feltham, 2012). When accountants are not

able to follow appropriate accounting principles then this problem also may occur .

Data loss: As in today's world paper work moved to accounting software to record

transactions. It also caused for the problem of data loss, because if employees sometime

forgot to save data in accounting software.

Employees turnover: sometimes workers leave an business organization than

intentionally or by mistake they take accounting record with them that lead the company

to the problem of inconsistent or insufficient data.

Intentional manipulation: Business owners make mistakes in the books of accounting

while recording transactions to manipulate the accounts to save tax or any other purpose.

TASK 2

2.1 Calculation of opening and closing capital

Capital account: It is the primary account which is required to be prepared to record all

the capital related transactions (Fooks and Gilmore, 2014). It includes the amount which has

been paid to the owners and drawing which has been taken by them for personal use. A capital

can be calculated by subtracting total liabilities from total assets.

(1)Closing capital for the year

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital Account

Particulars Amount Particulars Amount

To drawings 600 By balance b/d 1000

To balance c/d (b.f.) 3000 By net profits 2600

3600 3600

From the above calculation the closing capital fro the yeas has been determined which is

3000.

(2).Opening capital for the period

Capital Account

Particulars Amount Particulars Amount

To drawings 800 To balance b/d (b.f.) 4640

To balance c/d 4200 By net profits 360

5000 5000

Opening capital has been calculated with the help of above mentioned ledger. Opening

capital is 4650.

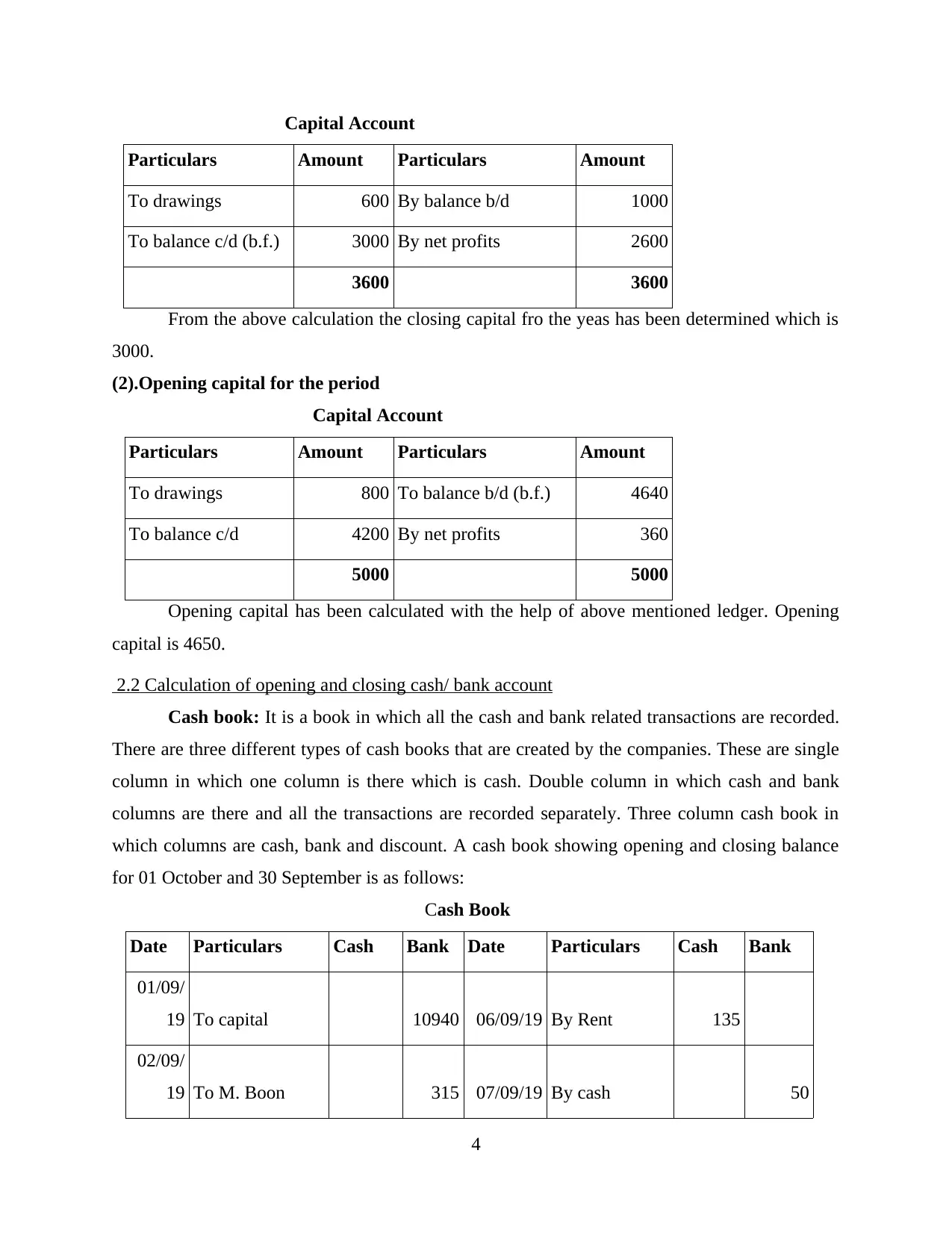

2.2 Calculation of opening and closing cash/ bank account

Cash book: It is a book in which all the cash and bank related transactions are recorded.

There are three different types of cash books that are created by the companies. These are single

column in which one column is there which is cash. Double column in which cash and bank

columns are there and all the transactions are recorded separately. Three column cash book in

which columns are cash, bank and discount. A cash book showing opening and closing balance

for 01 October and 30 September is as follows:

Cash Book

Date Particulars Cash Bank Date Particulars Cash Bank

01/09/

19 To capital 10940 06/09/19 By Rent 135

02/09/

19 To M. Boon 315 07/09/19 By cash 50

4

Particulars Amount Particulars Amount

To drawings 600 By balance b/d 1000

To balance c/d (b.f.) 3000 By net profits 2600

3600 3600

From the above calculation the closing capital fro the yeas has been determined which is

3000.

(2).Opening capital for the period

Capital Account

Particulars Amount Particulars Amount

To drawings 800 To balance b/d (b.f.) 4640

To balance c/d 4200 By net profits 360

5000 5000

Opening capital has been calculated with the help of above mentioned ledger. Opening

capital is 4650.

2.2 Calculation of opening and closing cash/ bank account

Cash book: It is a book in which all the cash and bank related transactions are recorded.

There are three different types of cash books that are created by the companies. These are single

column in which one column is there which is cash. Double column in which cash and bank

columns are there and all the transactions are recorded separately. Three column cash book in

which columns are cash, bank and discount. A cash book showing opening and closing balance

for 01 October and 30 September is as follows:

Cash Book

Date Particulars Cash Bank Date Particulars Cash Bank

01/09/

19 To capital 10940 06/09/19 By Rent 135

02/09/

19 To M. Boon 315 07/09/19 By cash 50

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

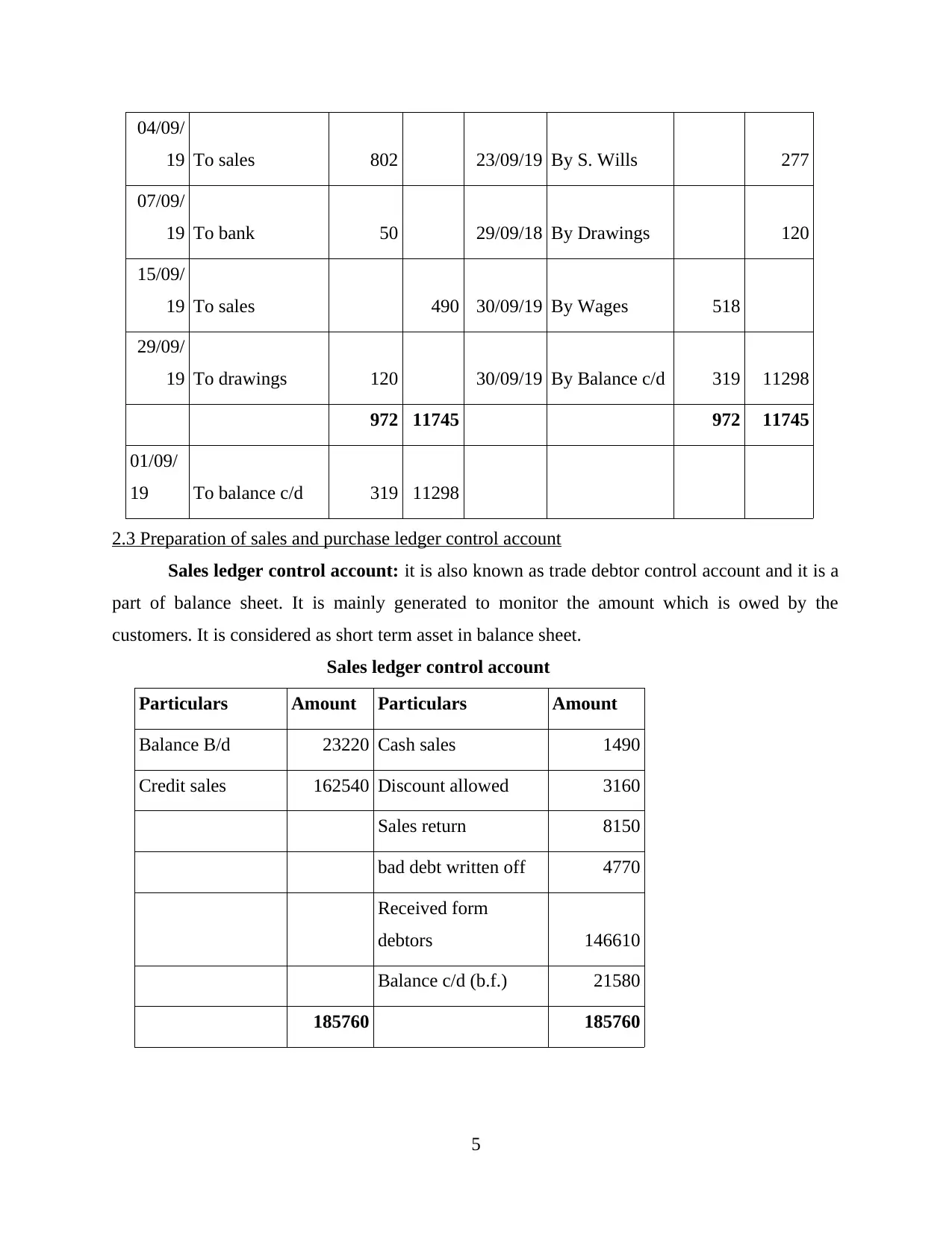

04/09/

19 To sales 802 23/09/19 By S. Wills 277

07/09/

19 To bank 50 29/09/18 By Drawings 120

15/09/

19 To sales 490 30/09/19 By Wages 518

29/09/

19 To drawings 120 30/09/19 By Balance c/d 319 11298

972 11745 972 11745

01/09/

19 To balance c/d 319 11298

2.3 Preparation of sales and purchase ledger control account

Sales ledger control account: it is also known as trade debtor control account and it is a

part of balance sheet. It is mainly generated to monitor the amount which is owed by the

customers. It is considered as short term asset in balance sheet.

Sales ledger control account

Particulars Amount Particulars Amount

Balance B/d 23220 Cash sales 1490

Credit sales 162540 Discount allowed 3160

Sales return 8150

bad debt written off 4770

Received form

debtors 146610

Balance c/d (b.f.) 21580

185760 185760

5

19 To sales 802 23/09/19 By S. Wills 277

07/09/

19 To bank 50 29/09/18 By Drawings 120

15/09/

19 To sales 490 30/09/19 By Wages 518

29/09/

19 To drawings 120 30/09/19 By Balance c/d 319 11298

972 11745 972 11745

01/09/

19 To balance c/d 319 11298

2.3 Preparation of sales and purchase ledger control account

Sales ledger control account: it is also known as trade debtor control account and it is a

part of balance sheet. It is mainly generated to monitor the amount which is owed by the

customers. It is considered as short term asset in balance sheet.

Sales ledger control account

Particulars Amount Particulars Amount

Balance B/d 23220 Cash sales 1490

Credit sales 162540 Discount allowed 3160

Sales return 8150

bad debt written off 4770

Received form

debtors 146610

Balance c/d (b.f.) 21580

185760 185760

5

Closing balance of sales ledger control account is 21580. an amount of 370 has been

subtracted from total receipts from debtors because it was written off last year. Total amount has

been shown is 146610 (146980-370 = 146610).

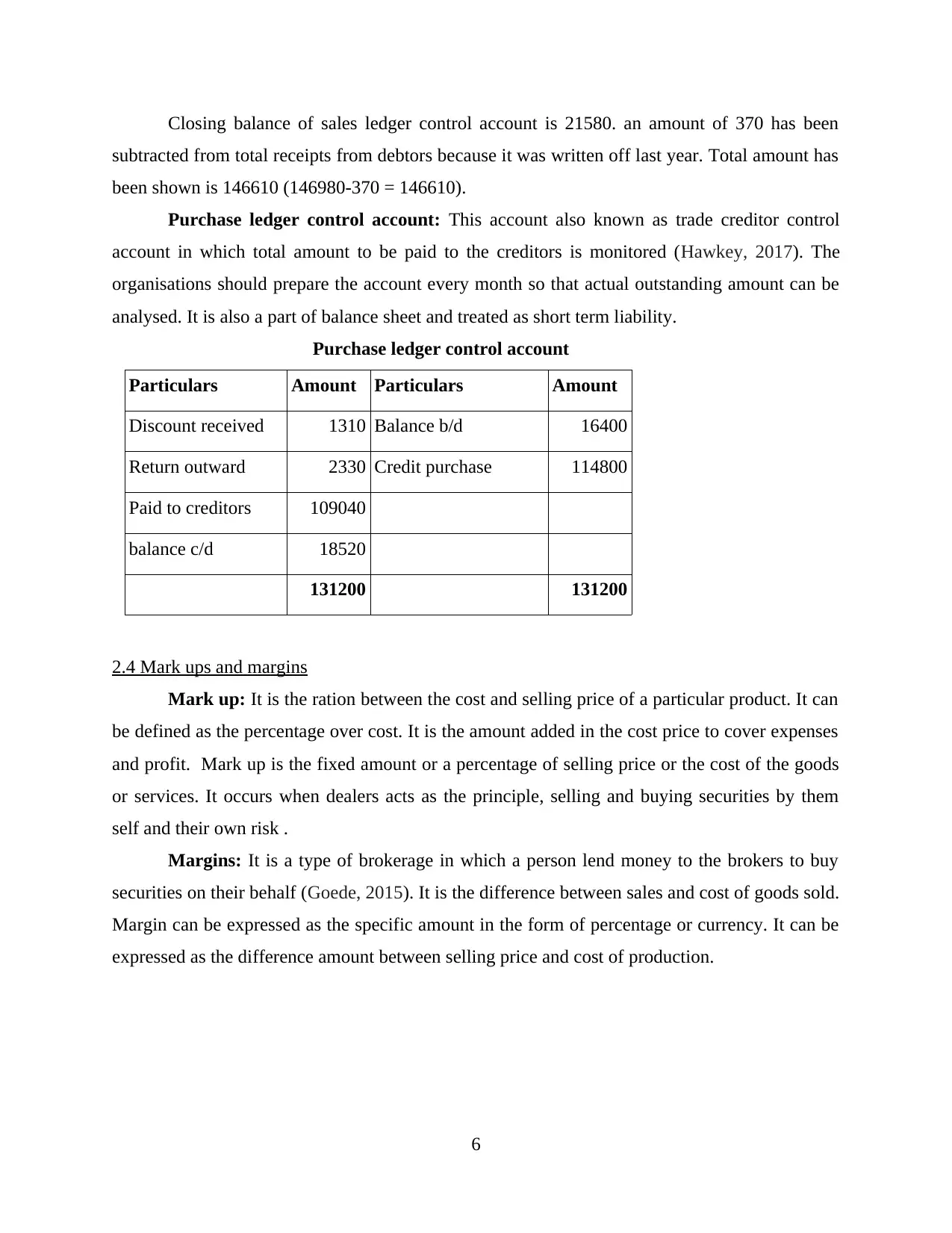

Purchase ledger control account: This account also known as trade creditor control

account in which total amount to be paid to the creditors is monitored (Hawkey, 2017). The

organisations should prepare the account every month so that actual outstanding amount can be

analysed. It is also a part of balance sheet and treated as short term liability.

Purchase ledger control account

Particulars Amount Particulars Amount

Discount received 1310 Balance b/d 16400

Return outward 2330 Credit purchase 114800

Paid to creditors 109040

balance c/d 18520

131200 131200

2.4 Mark ups and margins

Mark up: It is the ration between the cost and selling price of a particular product. It can

be defined as the percentage over cost. It is the amount added in the cost price to cover expenses

and profit. Mark up is the fixed amount or a percentage of selling price or the cost of the goods

or services. It occurs when dealers acts as the principle, selling and buying securities by them

self and their own risk .

Margins: It is a type of brokerage in which a person lend money to the brokers to buy

securities on their behalf (Goede, 2015). It is the difference between sales and cost of goods sold.

Margin can be expressed as the specific amount in the form of percentage or currency. It can be

expressed as the difference amount between selling price and cost of production.

6

subtracted from total receipts from debtors because it was written off last year. Total amount has

been shown is 146610 (146980-370 = 146610).

Purchase ledger control account: This account also known as trade creditor control

account in which total amount to be paid to the creditors is monitored (Hawkey, 2017). The

organisations should prepare the account every month so that actual outstanding amount can be

analysed. It is also a part of balance sheet and treated as short term liability.

Purchase ledger control account

Particulars Amount Particulars Amount

Discount received 1310 Balance b/d 16400

Return outward 2330 Credit purchase 114800

Paid to creditors 109040

balance c/d 18520

131200 131200

2.4 Mark ups and margins

Mark up: It is the ration between the cost and selling price of a particular product. It can

be defined as the percentage over cost. It is the amount added in the cost price to cover expenses

and profit. Mark up is the fixed amount or a percentage of selling price or the cost of the goods

or services. It occurs when dealers acts as the principle, selling and buying securities by them

self and their own risk .

Margins: It is a type of brokerage in which a person lend money to the brokers to buy

securities on their behalf (Goede, 2015). It is the difference between sales and cost of goods sold.

Margin can be expressed as the specific amount in the form of percentage or currency. It can be

expressed as the difference amount between selling price and cost of production.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

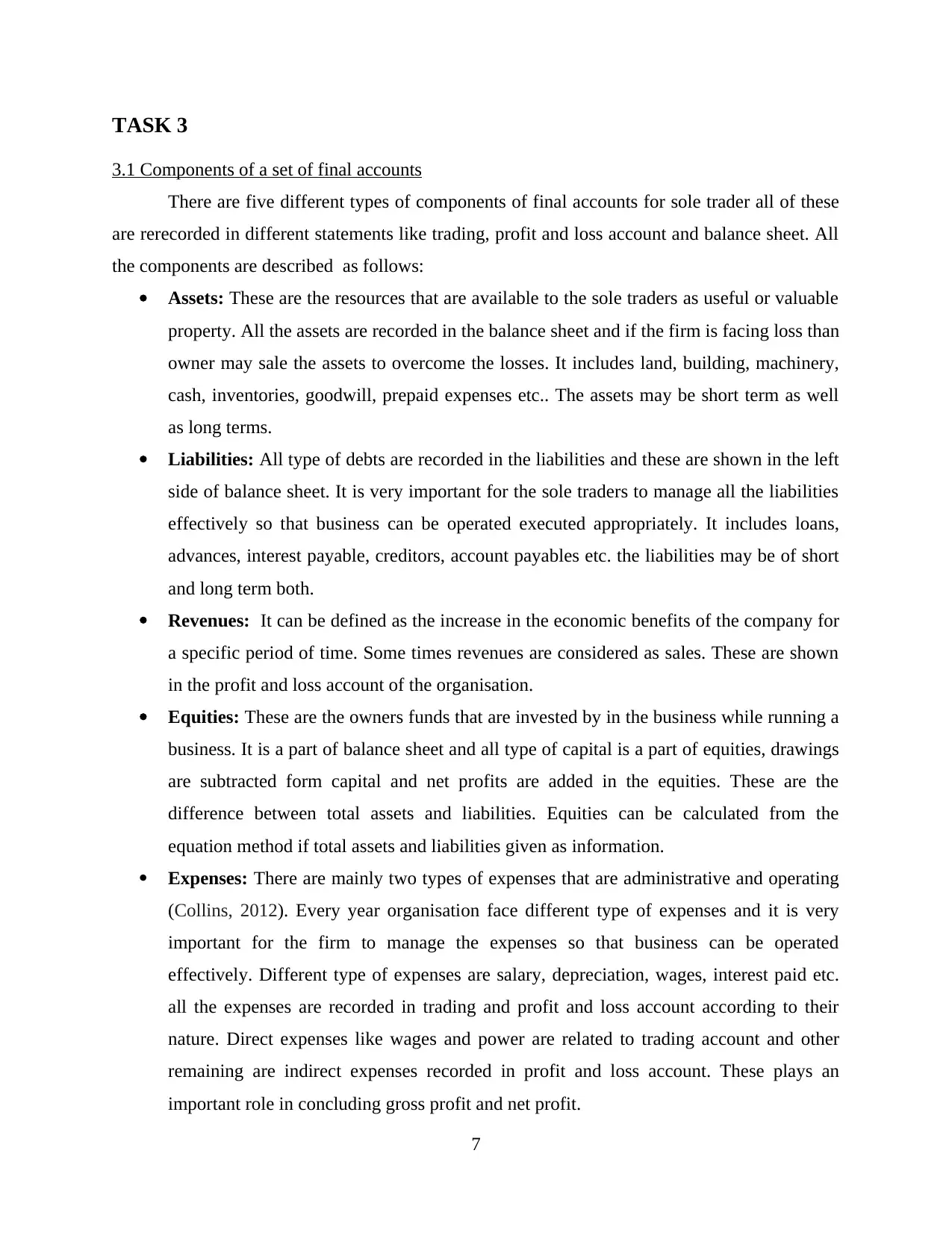

3.1 Components of a set of final accounts

There are five different types of components of final accounts for sole trader all of these

are rerecorded in different statements like trading, profit and loss account and balance sheet. All

the components are described as follows:

Assets: These are the resources that are available to the sole traders as useful or valuable

property. All the assets are recorded in the balance sheet and if the firm is facing loss than

owner may sale the assets to overcome the losses. It includes land, building, machinery,

cash, inventories, goodwill, prepaid expenses etc.. The assets may be short term as well

as long terms.

Liabilities: All type of debts are recorded in the liabilities and these are shown in the left

side of balance sheet. It is very important for the sole traders to manage all the liabilities

effectively so that business can be operated executed appropriately. It includes loans,

advances, interest payable, creditors, account payables etc. the liabilities may be of short

and long term both.

Revenues: It can be defined as the increase in the economic benefits of the company for

a specific period of time. Some times revenues are considered as sales. These are shown

in the profit and loss account of the organisation.

Equities: These are the owners funds that are invested by in the business while running a

business. It is a part of balance sheet and all type of capital is a part of equities, drawings

are subtracted form capital and net profits are added in the equities. These are the

difference between total assets and liabilities. Equities can be calculated from the

equation method if total assets and liabilities given as information.

Expenses: There are mainly two types of expenses that are administrative and operating

(Collins, 2012). Every year organisation face different type of expenses and it is very

important for the firm to manage the expenses so that business can be operated

effectively. Different type of expenses are salary, depreciation, wages, interest paid etc.

all the expenses are recorded in trading and profit and loss account according to their

nature. Direct expenses like wages and power are related to trading account and other

remaining are indirect expenses recorded in profit and loss account. These plays an

important role in concluding gross profit and net profit.

7

3.1 Components of a set of final accounts

There are five different types of components of final accounts for sole trader all of these

are rerecorded in different statements like trading, profit and loss account and balance sheet. All

the components are described as follows:

Assets: These are the resources that are available to the sole traders as useful or valuable

property. All the assets are recorded in the balance sheet and if the firm is facing loss than

owner may sale the assets to overcome the losses. It includes land, building, machinery,

cash, inventories, goodwill, prepaid expenses etc.. The assets may be short term as well

as long terms.

Liabilities: All type of debts are recorded in the liabilities and these are shown in the left

side of balance sheet. It is very important for the sole traders to manage all the liabilities

effectively so that business can be operated executed appropriately. It includes loans,

advances, interest payable, creditors, account payables etc. the liabilities may be of short

and long term both.

Revenues: It can be defined as the increase in the economic benefits of the company for

a specific period of time. Some times revenues are considered as sales. These are shown

in the profit and loss account of the organisation.

Equities: These are the owners funds that are invested by in the business while running a

business. It is a part of balance sheet and all type of capital is a part of equities, drawings

are subtracted form capital and net profits are added in the equities. These are the

difference between total assets and liabilities. Equities can be calculated from the

equation method if total assets and liabilities given as information.

Expenses: There are mainly two types of expenses that are administrative and operating

(Collins, 2012). Every year organisation face different type of expenses and it is very

important for the firm to manage the expenses so that business can be operated

effectively. Different type of expenses are salary, depreciation, wages, interest paid etc.

all the expenses are recorded in trading and profit and loss account according to their

nature. Direct expenses like wages and power are related to trading account and other

remaining are indirect expenses recorded in profit and loss account. These plays an

important role in concluding gross profit and net profit.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

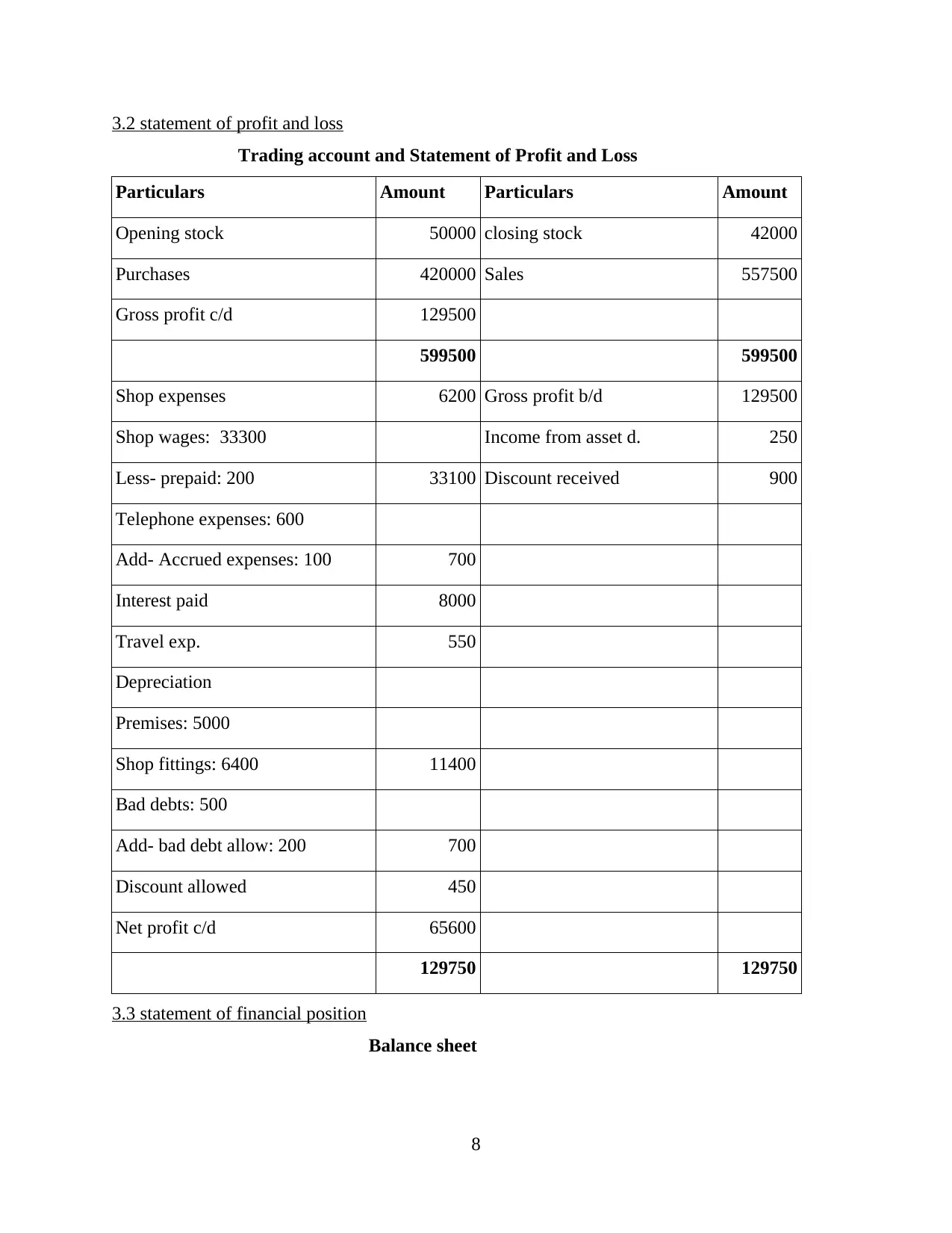

3.2 statement of profit and loss

Trading account and Statement of Profit and Loss

Particulars Amount Particulars Amount

Opening stock 50000 closing stock 42000

Purchases 420000 Sales 557500

Gross profit c/d 129500

599500 599500

Shop expenses 6200 Gross profit b/d 129500

Shop wages: 33300 Income from asset d. 250

Less- prepaid: 200 33100 Discount received 900

Telephone expenses: 600

Add- Accrued expenses: 100 700

Interest paid 8000

Travel exp. 550

Depreciation

Premises: 5000

Shop fittings: 6400 11400

Bad debts: 500

Add- bad debt allow: 200 700

Discount allowed 450

Net profit c/d 65600

129750 129750

3.3 statement of financial position

Balance sheet

8

Trading account and Statement of Profit and Loss

Particulars Amount Particulars Amount

Opening stock 50000 closing stock 42000

Purchases 420000 Sales 557500

Gross profit c/d 129500

599500 599500

Shop expenses 6200 Gross profit b/d 129500

Shop wages: 33300 Income from asset d. 250

Less- prepaid: 200 33100 Discount received 900

Telephone expenses: 600

Add- Accrued expenses: 100 700

Interest paid 8000

Travel exp. 550

Depreciation

Premises: 5000

Shop fittings: 6400 11400

Bad debts: 500

Add- bad debt allow: 200 700

Discount allowed 450

Net profit c/d 65600

129750 129750

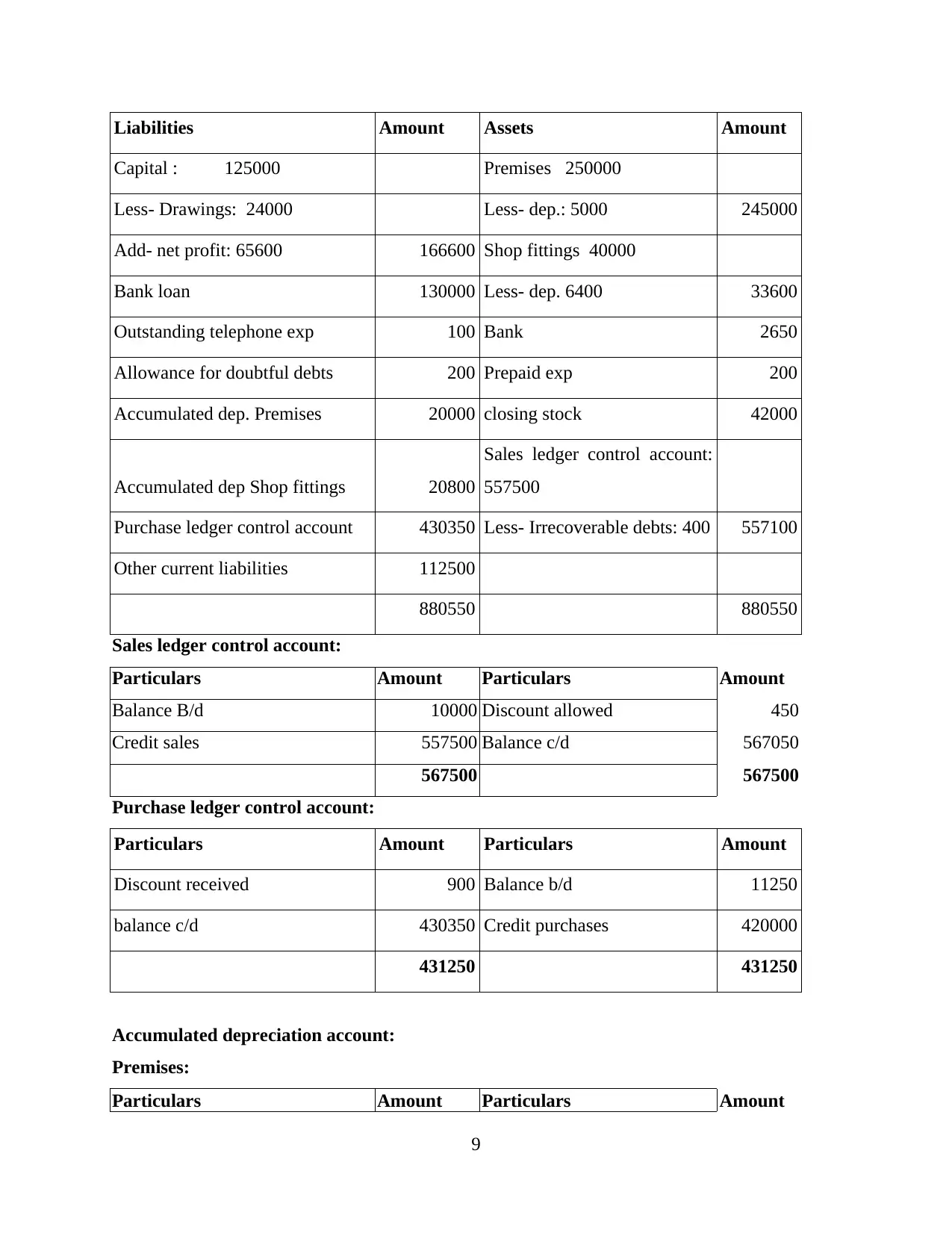

3.3 statement of financial position

Balance sheet

8

Liabilities Amount Assets Amount

Capital : 125000 Premises 250000

Less- Drawings: 24000 Less- dep.: 5000 245000

Add- net profit: 65600 166600 Shop fittings 40000

Bank loan 130000 Less- dep. 6400 33600

Outstanding telephone exp 100 Bank 2650

Allowance for doubtful debts 200 Prepaid exp 200

Accumulated dep. Premises 20000 closing stock 42000

Accumulated dep Shop fittings 20800

Sales ledger control account:

557500

Purchase ledger control account 430350 Less- Irrecoverable debts: 400 557100

Other current liabilities 112500

880550 880550

Sales ledger control account:

Particulars Amount Particulars Amount

Balance B/d 10000 Discount allowed 450

Credit sales 557500 Balance c/d 567050

567500 567500

Purchase ledger control account:

Particulars Amount Particulars Amount

Discount received 900 Balance b/d 11250

balance c/d 430350 Credit purchases 420000

431250 431250

Accumulated depreciation account:

Premises:

Particulars Amount Particulars Amount

9

Capital : 125000 Premises 250000

Less- Drawings: 24000 Less- dep.: 5000 245000

Add- net profit: 65600 166600 Shop fittings 40000

Bank loan 130000 Less- dep. 6400 33600

Outstanding telephone exp 100 Bank 2650

Allowance for doubtful debts 200 Prepaid exp 200

Accumulated dep. Premises 20000 closing stock 42000

Accumulated dep Shop fittings 20800

Sales ledger control account:

557500

Purchase ledger control account 430350 Less- Irrecoverable debts: 400 557100

Other current liabilities 112500

880550 880550

Sales ledger control account:

Particulars Amount Particulars Amount

Balance B/d 10000 Discount allowed 450

Credit sales 557500 Balance c/d 567050

567500 567500

Purchase ledger control account:

Particulars Amount Particulars Amount

Discount received 900 Balance b/d 11250

balance c/d 430350 Credit purchases 420000

431250 431250

Accumulated depreciation account:

Premises:

Particulars Amount Particulars Amount

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.