Final Accounts for Sole Traders and Partnerships - ACC 101, Semester 1

VerifiedAdded on 2020/10/22

|20

|4820

|483

Report

AI Summary

This report provides a detailed examination of final accounts for sole traders and partnerships. It begins by outlining the necessity and procedures involved in preparing final accounts, including closing entries and trial balance generation. The report then delves into accounting records for incomplete data, methods for constructing accounts, and the impact of incorrect double entries. It further explores the components of final accounts for sole traders, including the statement of profit or loss and the statement of financial position. The report also covers the legislative and accounting requirements for partnerships, focusing on partnership agreements, accounts, the statement of profit or loss appropriation account, and the preparation of capital and current accounts. Finally, it discusses the statement of financial position related to a partnership, including the calculation of closing balances and the preparation of the financial position statement, all in compliance with partnership agreements. The report concludes by summarizing the key aspects of preparing final accounts for sole traders and partnerships.

PREPARE FINAL ACCOUNTS

FOR SOLE TRADERS AND

PARTNERSHIPS

FOR SOLE TRADERS AND

PARTNERSHIPS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

1. Need and process involved for preparation of final accounts......................................................4

1.1 Identifying reasons for closing off accounts and generating trial balance............................4

1.2 Explaining process and limitation of setting final accounts through trial balance...............5

1.3 Describing methods for constructing accounts from incomplete records.............................6

1.4 Reasons for imbalances outcome through incorrect double entries......................................6

1.5 Reasons for incomplete records arise through insufficient data along with inconsistency...7

2. Accounting records for incomplete records.................................................................................7

2.1 Calculating closing and opening capital with incomplete information.................................7

2.2 Calculating closing and opening cash/bank account balance................................................8

2.3 Preparing sales and purchase ledger control accounts with correct sales, purchase and

bank figures.................................................................................................................................8

2.4 Calculating account balances with application of mark ups and margins.............................9

3. Final accounts for sole traders.....................................................................................................9

3.1 Describing components of final accounts for sole trader......................................................9

3.2 Statement of profit or loss...................................................................................................10

3.3 Statement of financial position............................................................................................11

4. Legislative and accounting requirements for partnerships........................................................12

4.1 Describing key components of partnership agreements......................................................12

4.2 Describing key components of partnership accounts..........................................................13

5. Statement of profit or loss appropriation account......................................................................13

5.1 Preparing statement of profit or loss appropriation account for a partnership....................13

5.2 Identifying allocation of profit to partners after allowing for interest on capital, interest on

drawings and any salary paid to partner....................................................................................14

5.3 Preparing capital and current accounts for each partner.....................................................16

6. Statement of financial position relating to a partnership...........................................................17

6.1 and 6.2 Calculating closing balance on every partner's current and capital accounts with

drawings and preparing statement of financial position with compliance of partnership

agreement..................................................................................................................................17

INTRODUCTION...........................................................................................................................4

1. Need and process involved for preparation of final accounts......................................................4

1.1 Identifying reasons for closing off accounts and generating trial balance............................4

1.2 Explaining process and limitation of setting final accounts through trial balance...............5

1.3 Describing methods for constructing accounts from incomplete records.............................6

1.4 Reasons for imbalances outcome through incorrect double entries......................................6

1.5 Reasons for incomplete records arise through insufficient data along with inconsistency...7

2. Accounting records for incomplete records.................................................................................7

2.1 Calculating closing and opening capital with incomplete information.................................7

2.2 Calculating closing and opening cash/bank account balance................................................8

2.3 Preparing sales and purchase ledger control accounts with correct sales, purchase and

bank figures.................................................................................................................................8

2.4 Calculating account balances with application of mark ups and margins.............................9

3. Final accounts for sole traders.....................................................................................................9

3.1 Describing components of final accounts for sole trader......................................................9

3.2 Statement of profit or loss...................................................................................................10

3.3 Statement of financial position............................................................................................11

4. Legislative and accounting requirements for partnerships........................................................12

4.1 Describing key components of partnership agreements......................................................12

4.2 Describing key components of partnership accounts..........................................................13

5. Statement of profit or loss appropriation account......................................................................13

5.1 Preparing statement of profit or loss appropriation account for a partnership....................13

5.2 Identifying allocation of profit to partners after allowing for interest on capital, interest on

drawings and any salary paid to partner....................................................................................14

5.3 Preparing capital and current accounts for each partner.....................................................16

6. Statement of financial position relating to a partnership...........................................................17

6.1 and 6.2 Calculating closing balance on every partner's current and capital accounts with

drawings and preparing statement of financial position with compliance of partnership

agreement..................................................................................................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

REFERENCES..............................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Final accounts helps in providing actual picture of financial position of any business. It

helps in reflecting information related to profit and loss created through business or not within

accounting period. The present report will discuss about need and process engaged for purpose

of preparing final accounts. In the same series, it will articulate about accounting records through

incomplete information along with producing accounting records with context of sole traders.

There will description on basis of components of final accounts and preparation of both balance

sheet along with income statement. This report will be giving appropriate understanding about

accounting and legislative requirements for partnerships agreement and accounts as well.

Furthermore, it will discuss about preparation of statement of profit and loss appropriation

account, capital and current account. Lastly, there will statement of financial positions related to

partnership with calculation of closing balance.

1. Need and process involved for preparation of final accounts

1.1 Identifying reasons for closing off accounts and generating trial balance

Reason for Closing off accounts: The closing entries of temporary accounts like

expense and revenue accounts. These closing entries are traced after preparation of financial

statements for particular accounting year. The main reason behind closing entries is for ensuring

about every expense and revenue account should begin with next accounting year with nil

balance (Quinn and Gibney, 2018). The closing entries are traced in such aspect where

organization's retained earning account reflects actual increase from prior year along with

decrement in payment of dividends and expenses. In this aspect, it has requirement where debt

and credit is entered in temporary accounts with presence of debit and credit balance

respectively. The debit amount which is entered should be exactly similar to credit balance as its

objective is to get zero as account balance.

Reason for producing trial balance: Trial balance is formed for purpose of checking

arithmetical accuracy with context of ledger accounts. It lists the ending balance of every ledger

as if total of credit and debit on trial balance does not match then it indicates that some

transactions are recorded in general ledger are not balanced in proper format. In the similar

aspect, it helps in locating errors and for purpose of preparing financial statements. Trial balance

is considered as summary of every ledger in specific accounting period as it is very effective tool

for comparison. It is very easy for comparing balances of current year with past period. The data

4

Final accounts helps in providing actual picture of financial position of any business. It

helps in reflecting information related to profit and loss created through business or not within

accounting period. The present report will discuss about need and process engaged for purpose

of preparing final accounts. In the same series, it will articulate about accounting records through

incomplete information along with producing accounting records with context of sole traders.

There will description on basis of components of final accounts and preparation of both balance

sheet along with income statement. This report will be giving appropriate understanding about

accounting and legislative requirements for partnerships agreement and accounts as well.

Furthermore, it will discuss about preparation of statement of profit and loss appropriation

account, capital and current account. Lastly, there will statement of financial positions related to

partnership with calculation of closing balance.

1. Need and process involved for preparation of final accounts

1.1 Identifying reasons for closing off accounts and generating trial balance

Reason for Closing off accounts: The closing entries of temporary accounts like

expense and revenue accounts. These closing entries are traced after preparation of financial

statements for particular accounting year. The main reason behind closing entries is for ensuring

about every expense and revenue account should begin with next accounting year with nil

balance (Quinn and Gibney, 2018). The closing entries are traced in such aspect where

organization's retained earning account reflects actual increase from prior year along with

decrement in payment of dividends and expenses. In this aspect, it has requirement where debt

and credit is entered in temporary accounts with presence of debit and credit balance

respectively. The debit amount which is entered should be exactly similar to credit balance as its

objective is to get zero as account balance.

Reason for producing trial balance: Trial balance is formed for purpose of checking

arithmetical accuracy with context of ledger accounts. It lists the ending balance of every ledger

as if total of credit and debit on trial balance does not match then it indicates that some

transactions are recorded in general ledger are not balanced in proper format. In the similar

aspect, it helps in locating errors and for purpose of preparing financial statements. Trial balance

is considered as summary of every ledger in specific accounting period as it is very effective tool

for comparison. It is very easy for comparing balances of current year with past period. The data

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is gathered on manual basis with objective of comparison as it consumes more time

comparatively to used trial balance.

1.2 Explaining process and limitation of setting final accounts through trial balance

Final accounts is referred as ending account balances of organization as it is used for

framing financial statements as it reveals about outcome of business within specific duration.

Final accounts comprises income statement and balance sheet as well as there is need of huge

analysis within particular database and to identify outcome which helps in operational and to

govern task of business (La Follette, Deur and González, 2018). There will be application of

information on basis of operating expenses and income produced by business with context of

business sales and operations.

Process:

Initiate with tracing information through trial balance in profit and loss statement and

balance sheet.

First debit balance of trial balance is moved to debit side of income statement or in

statement of financial position.

Furthermore, Credit amount is credited in credit side of balance sheet and profit and loss

ststement.

In this aspect, there will be identification of net margin and loss then balance sheet will

be framed. However, there is need of information on basis of assets, equities and liabilities over

the year. Henceforth, total liabilities and amount will match then it could be elaborated that

application of right technique and methods for framing business's final accounts (Purpose of the

Trial Balance in Accounting, 2019).

Limitation of setting final accounts with help of trial balance

Generally, trial balance reflects arithmetical accuracy about entries of accounting as trial

balance is formed with closing balances of ledger and aggregate of both debit and credit side

matches then it is correct account. There are various errors which could not be directly disclosed

through trial balance which impacts entire final accounts are stated below:

Omission of entry in subsidiary or day book: If any voucher is not reflected in day

book then it will not impact sum of trial balance.

5

comparatively to used trial balance.

1.2 Explaining process and limitation of setting final accounts through trial balance

Final accounts is referred as ending account balances of organization as it is used for

framing financial statements as it reveals about outcome of business within specific duration.

Final accounts comprises income statement and balance sheet as well as there is need of huge

analysis within particular database and to identify outcome which helps in operational and to

govern task of business (La Follette, Deur and González, 2018). There will be application of

information on basis of operating expenses and income produced by business with context of

business sales and operations.

Process:

Initiate with tracing information through trial balance in profit and loss statement and

balance sheet.

First debit balance of trial balance is moved to debit side of income statement or in

statement of financial position.

Furthermore, Credit amount is credited in credit side of balance sheet and profit and loss

ststement.

In this aspect, there will be identification of net margin and loss then balance sheet will

be framed. However, there is need of information on basis of assets, equities and liabilities over

the year. Henceforth, total liabilities and amount will match then it could be elaborated that

application of right technique and methods for framing business's final accounts (Purpose of the

Trial Balance in Accounting, 2019).

Limitation of setting final accounts with help of trial balance

Generally, trial balance reflects arithmetical accuracy about entries of accounting as trial

balance is formed with closing balances of ledger and aggregate of both debit and credit side

matches then it is correct account. There are various errors which could not be directly disclosed

through trial balance which impacts entire final accounts are stated below:

Omission of entry in subsidiary or day book: If any voucher is not reflected in day

book then it will not impact sum of trial balance.

5

Wrong amount in day book: During any entry in day book, if any wrong amount is

stated at primary stage then this error will be not disclosed where total of trial balance is

agreed.

Errors of principles: If there is absence of proper allocation of account head during

preparation of journal voucher is referred as error of principles.

Henceforth, these errors will directly impact final accounts and will lead to mismatch in

amount of assets and liabilities. In the same series, its outcome will be over utilising time of

professionals along with resources of corporation as well.

1.3 Describing methods for constructing accounts from incomplete records

Accounting records are not strictly considered as per double entry system is replicated as

incomplete records. Generally, it is referred as single entry system as it is misnomer due to no

such system for purpose of maintaining records. Therefore, it is also not a shortcut method or

alternative for double entry system. It is a mechanism for purpose of maintaining records where

some transactions are traced with appropriate credits and debits with one sided or with no entry.

Usually, in this system cash record along with appropriate maintenance of personal account of

creditors and debtors where information is on basis of expense, assets, liabilities and revenue is

traced partially (Bigoni, Aloisi and Funnell, 2018). Thus, these are replicated as incomplete

records. This is unsystematic method for tracing transactions where transactions are not recorded

as per well defined rules but with context of convenience. In the similar aspect, accounting

equation is other method which is foundation of double entry accounting system and to construct

accounts through incomplete records. On the contrary, transaction under double entry system are

traced by considering both aspects.

1.4 Reasons for imbalances outcome through incorrect double entries

It is summary of all debits or credit total in every account. Generally, there is use of

initial and unadjusted trial balance for ensuring total debt is equalised to total credit along with

ensuring about underlying transactions in perfect balance. As the initial point for purpose of

adjusting entries it would up bring information in trial balance with compliance of accounting

framework like Generally Accepted accounting principles and standards of international

financial reporting. This unadjusted trial balance might contain numerous errors such as:

6

stated at primary stage then this error will be not disclosed where total of trial balance is

agreed.

Errors of principles: If there is absence of proper allocation of account head during

preparation of journal voucher is referred as error of principles.

Henceforth, these errors will directly impact final accounts and will lead to mismatch in

amount of assets and liabilities. In the same series, its outcome will be over utilising time of

professionals along with resources of corporation as well.

1.3 Describing methods for constructing accounts from incomplete records

Accounting records are not strictly considered as per double entry system is replicated as

incomplete records. Generally, it is referred as single entry system as it is misnomer due to no

such system for purpose of maintaining records. Therefore, it is also not a shortcut method or

alternative for double entry system. It is a mechanism for purpose of maintaining records where

some transactions are traced with appropriate credits and debits with one sided or with no entry.

Usually, in this system cash record along with appropriate maintenance of personal account of

creditors and debtors where information is on basis of expense, assets, liabilities and revenue is

traced partially (Bigoni, Aloisi and Funnell, 2018). Thus, these are replicated as incomplete

records. This is unsystematic method for tracing transactions where transactions are not recorded

as per well defined rules but with context of convenience. In the similar aspect, accounting

equation is other method which is foundation of double entry accounting system and to construct

accounts through incomplete records. On the contrary, transaction under double entry system are

traced by considering both aspects.

1.4 Reasons for imbalances outcome through incorrect double entries

It is summary of all debits or credit total in every account. Generally, there is use of

initial and unadjusted trial balance for ensuring total debt is equalised to total credit along with

ensuring about underlying transactions in perfect balance. As the initial point for purpose of

adjusting entries it would up bring information in trial balance with compliance of accounting

framework like Generally Accepted accounting principles and standards of international

financial reporting. This unadjusted trial balance might contain numerous errors such as:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The credit total is accidentally entered in debit column or vice versa situation. In this

aspect, it will overstate single side of trial balance along with understating other and

yielding of unbalanced trial balance (Imbalances in trial balance, 2019).

The wrong numbers is copies as common error framed from time to time. These mistakes

would cause the debits and credit totals for slipping out of balance.

1.5 Reasons for incomplete records arise through insufficient data along with inconsistency

Incomplete accounting records could cause various issues while reporting to IRS in audits

of financial statements and planning for coming years. The main reason behind incomplete

record is because of lack of knowledge on basis of accounting principles and data loss because of

theft, fire etc. Further, incompleteness of data is to maintain records with application of double

entry system which is very expensive and single entry is convenient where information is traced

on whole aspect. There are various organizations which are moving to paperless accounting

records and numerous transactions are directly processed via computer, owners of small business

are undertaking different steps for purpose preserving data. The best method for helping to

preventing data loss is for creating redundant and frequent software backups of its accounting

data on regular or frequent aspect along with backup copy of data must be off site. Further, it

guards against data loss through natural disaster or theft as well.

There is absence of knowledge with reference to accounting concepts and principles.

Where double entry system is expensive method for purpose of maintaining financial accounts.

In the same series, maintaining these incomplete records consumes less time. Henceforth, it is

highly convenient for maintaining these records as per single entry system (Kunsek and Djokic,

2018). The data incompleteness directly impact final accounts as it does not give appropriate

financial position of business unit.

2. Accounting records for incomplete records

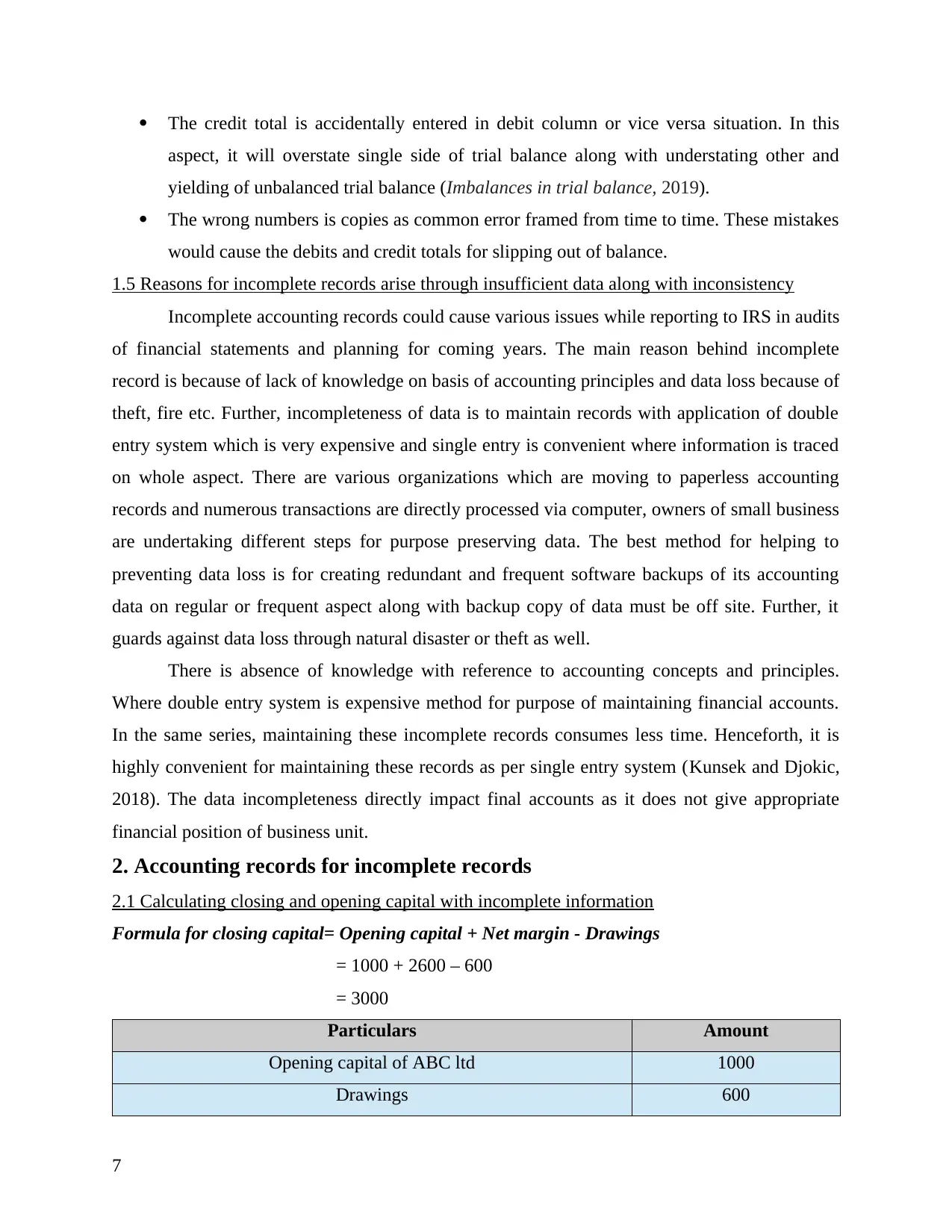

2.1 Calculating closing and opening capital with incomplete information

Formula for closing capital= Opening capital + Net margin - Drawings

= 1000 + 2600 – 600

= 3000

Particulars Amount

Opening capital of ABC ltd 1000

Drawings 600

7

aspect, it will overstate single side of trial balance along with understating other and

yielding of unbalanced trial balance (Imbalances in trial balance, 2019).

The wrong numbers is copies as common error framed from time to time. These mistakes

would cause the debits and credit totals for slipping out of balance.

1.5 Reasons for incomplete records arise through insufficient data along with inconsistency

Incomplete accounting records could cause various issues while reporting to IRS in audits

of financial statements and planning for coming years. The main reason behind incomplete

record is because of lack of knowledge on basis of accounting principles and data loss because of

theft, fire etc. Further, incompleteness of data is to maintain records with application of double

entry system which is very expensive and single entry is convenient where information is traced

on whole aspect. There are various organizations which are moving to paperless accounting

records and numerous transactions are directly processed via computer, owners of small business

are undertaking different steps for purpose preserving data. The best method for helping to

preventing data loss is for creating redundant and frequent software backups of its accounting

data on regular or frequent aspect along with backup copy of data must be off site. Further, it

guards against data loss through natural disaster or theft as well.

There is absence of knowledge with reference to accounting concepts and principles.

Where double entry system is expensive method for purpose of maintaining financial accounts.

In the same series, maintaining these incomplete records consumes less time. Henceforth, it is

highly convenient for maintaining these records as per single entry system (Kunsek and Djokic,

2018). The data incompleteness directly impact final accounts as it does not give appropriate

financial position of business unit.

2. Accounting records for incomplete records

2.1 Calculating closing and opening capital with incomplete information

Formula for closing capital= Opening capital + Net margin - Drawings

= 1000 + 2600 – 600

= 3000

Particulars Amount

Opening capital of ABC ltd 1000

Drawings 600

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Margin 2600

Formula for opening capital= Closing capital - Net margin + Drawings

= 4200 – 360 + 800

= 4640

Particulars Amount

Net margin 360

Closing Capital 4200

Drawings 800

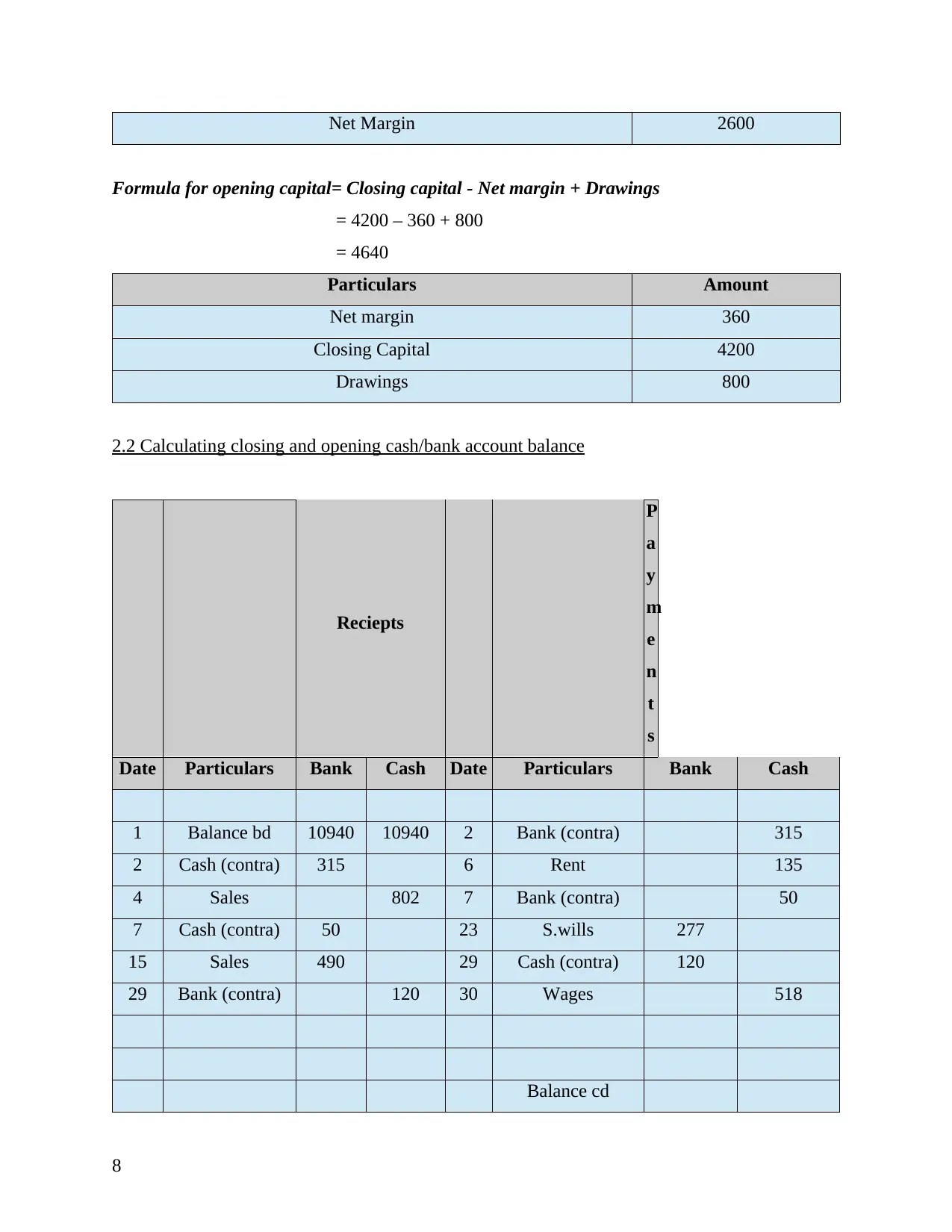

2.2 Calculating closing and opening cash/bank account balance

Reciepts

P

a

y

m

e

n

t

s

Date Particulars Bank Cash Date Particulars Bank Cash

1 Balance bd 10940 10940 2 Bank (contra) 315

2 Cash (contra) 315 6 Rent 135

4 Sales 802 7 Bank (contra) 50

7 Cash (contra) 50 23 S.wills 277

15 Sales 490 29 Cash (contra) 120

29 Bank (contra) 120 30 Wages 518

Balance cd

8

Formula for opening capital= Closing capital - Net margin + Drawings

= 4200 – 360 + 800

= 4640

Particulars Amount

Net margin 360

Closing Capital 4200

Drawings 800

2.2 Calculating closing and opening cash/bank account balance

Reciepts

P

a

y

m

e

n

t

s

Date Particulars Bank Cash Date Particulars Bank Cash

1 Balance bd 10940 10940 2 Bank (contra) 315

2 Cash (contra) 315 6 Rent 135

4 Sales 802 7 Bank (contra) 50

7 Cash (contra) 50 23 S.wills 277

15 Sales 490 29 Cash (contra) 120

29 Bank (contra) 120 30 Wages 518

Balance cd

8

TOTAL 11795 11862 TOTAL

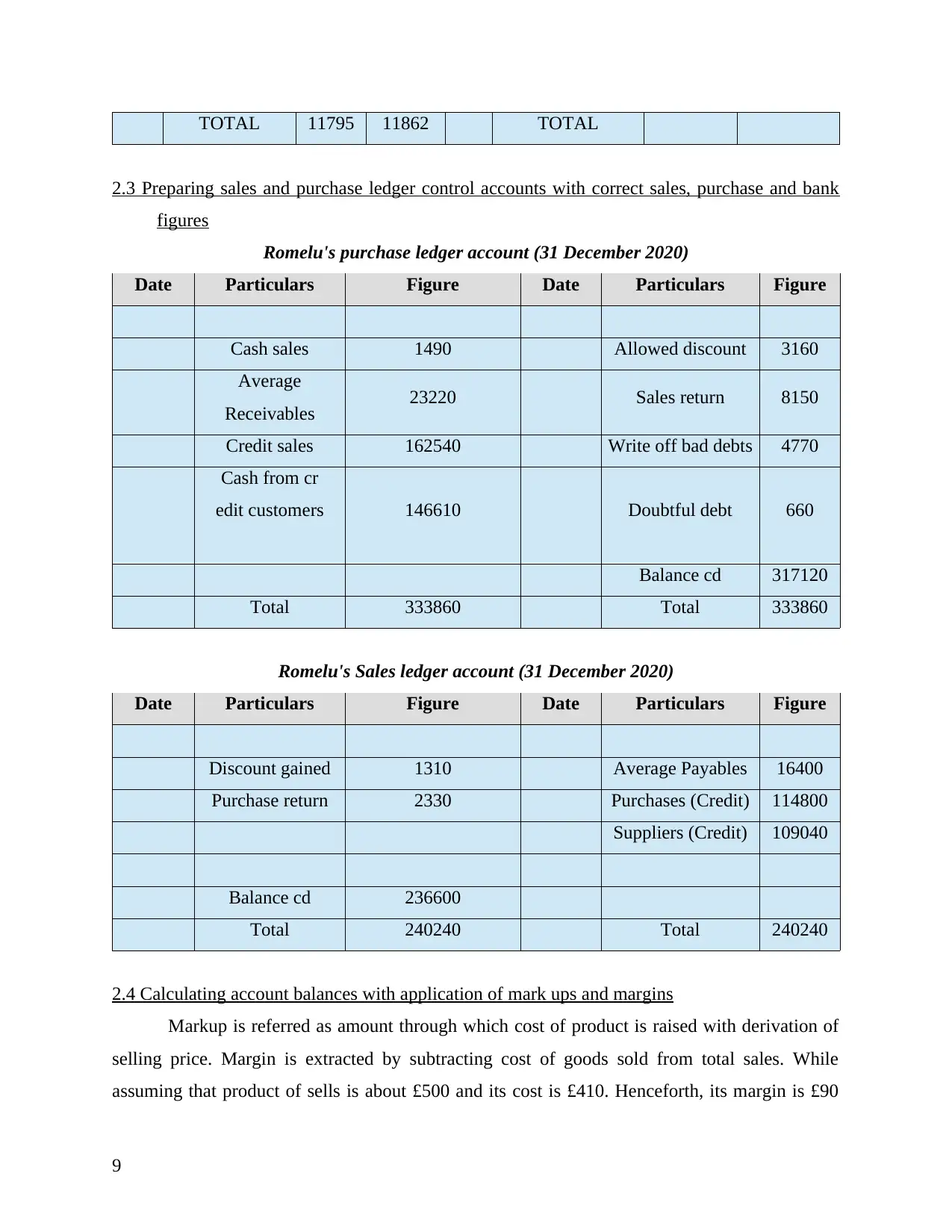

2.3 Preparing sales and purchase ledger control accounts with correct sales, purchase and bank

figures

Romelu's purchase ledger account (31 December 2020)

Date Particulars Figure Date Particulars Figure

Cash sales 1490 Allowed discount 3160

Average

Receivables 23220 Sales return 8150

Credit sales 162540 Write off bad debts 4770

Cash from cr

edit customers 146610 Doubtful debt 660

Balance cd 317120

Total 333860 Total 333860

Romelu's Sales ledger account (31 December 2020)

Date Particulars Figure Date Particulars Figure

Discount gained 1310 Average Payables 16400

Purchase return 2330 Purchases (Credit) 114800

Suppliers (Credit) 109040

Balance cd 236600

Total 240240 Total 240240

2.4 Calculating account balances with application of mark ups and margins

Markup is referred as amount through which cost of product is raised with derivation of

selling price. Margin is extracted by subtracting cost of goods sold from total sales. While

assuming that product of sells is about £500 and its cost is £410. Henceforth, its margin is £90

9

2.3 Preparing sales and purchase ledger control accounts with correct sales, purchase and bank

figures

Romelu's purchase ledger account (31 December 2020)

Date Particulars Figure Date Particulars Figure

Cash sales 1490 Allowed discount 3160

Average

Receivables 23220 Sales return 8150

Credit sales 162540 Write off bad debts 4770

Cash from cr

edit customers 146610 Doubtful debt 660

Balance cd 317120

Total 333860 Total 333860

Romelu's Sales ledger account (31 December 2020)

Date Particulars Figure Date Particulars Figure

Discount gained 1310 Average Payables 16400

Purchase return 2330 Purchases (Credit) 114800

Suppliers (Credit) 109040

Balance cd 236600

Total 240240 Total 240240

2.4 Calculating account balances with application of mark ups and margins

Markup is referred as amount through which cost of product is raised with derivation of

selling price. Margin is extracted by subtracting cost of goods sold from total sales. While

assuming that product of sells is about £500 and its cost is £410. Henceforth, its margin is £90

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and could be replicated as 90%. For instance, its markup of £90 from £410 with yield cost is

£500.

3. Final accounts for sole traders

3.1 Describing components of final accounts for sole trader

Final accounts are formed at year ending as it provides precise idea on basis of financial

position of organization to its management, owners and other interested parties. It consists of

three important components such as:

Trading account

Profit and loss account

Balance sheet

Trading account: It is considered as initial stage for process of preparing final accounts.

It reflects gross margin and loss within accounting year. Its main components are services and

sales rendered in credit side. It traces net sales and direct cost of goods sold and balance of this

account is disclosed through gross loss and profit. Usually, it is based on matching cost of goods

sold and selling price of services and goods.

Profit and Loss account: It is prepared for calculating net profit and loss and gathered

for ascertaining excess gains over huge losses and vice versa situation. It is second stage with

context to final accounts and related to specific accounting period in the year end. For purpose of

preparing this account, accrual basis of accounting is followed and account is directly credited

with income and gross profit through other relevant sources and debited with indirect losses and

expenses as well (Madalina and Adriana, 2018). The purpose of preparing profit and loss is to

ascertain net profit, control over expenses and comparison with profit of past year.

Statement of financial position: It is considered as last step of final account as it is not

any account as it does not have any debit or credit side. However, it has liabilities and asset side

as it reflects what is owned by business and what it owes to others with context of assets and

liabilities. Every asset and liability is reflected on their respective sides as similar to trial balance,

sum of asset should be equal to sum of liability side due to presence of double entry with context

of each transaction.

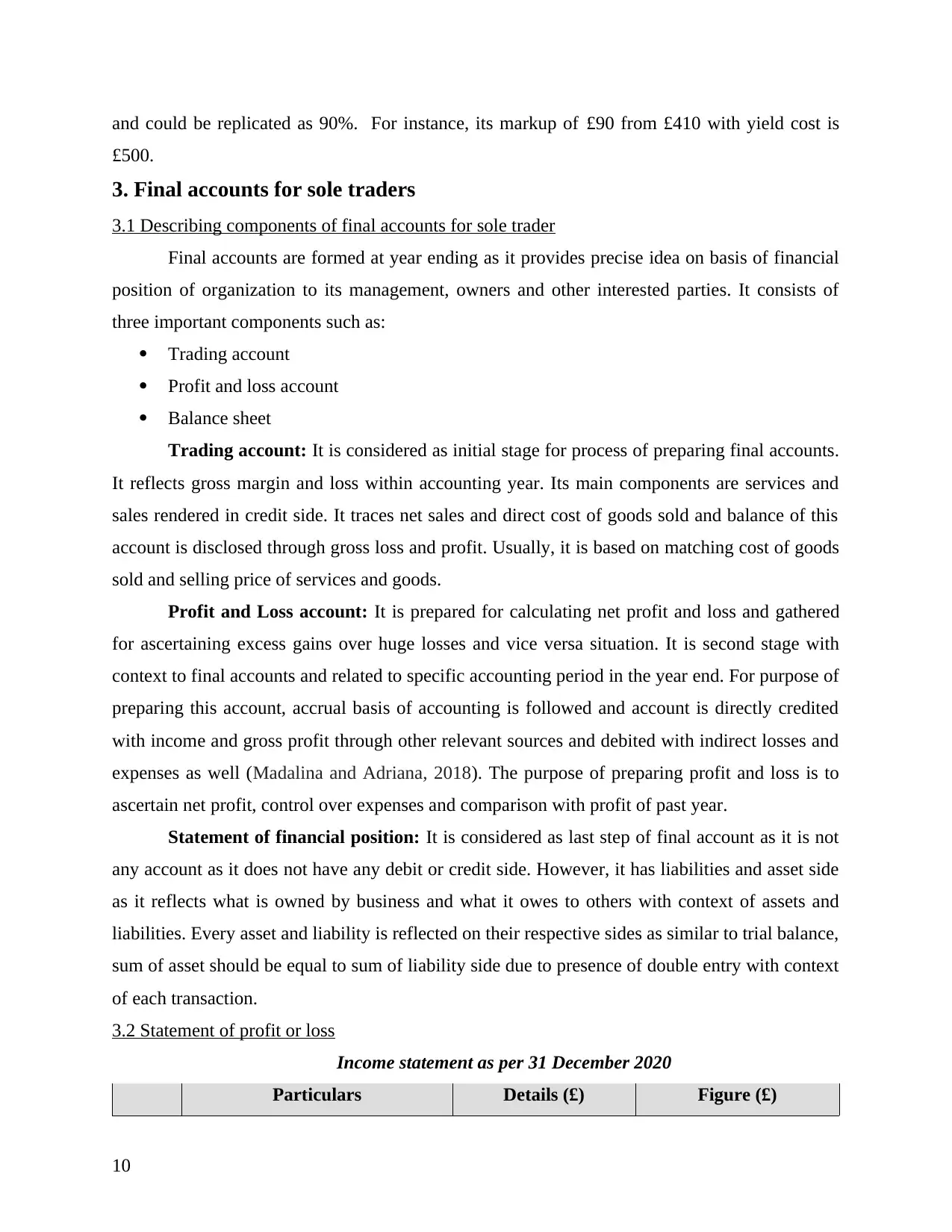

3.2 Statement of profit or loss

Income statement as per 31 December 2020

Particulars Details (£) Figure (£)

10

£500.

3. Final accounts for sole traders

3.1 Describing components of final accounts for sole trader

Final accounts are formed at year ending as it provides precise idea on basis of financial

position of organization to its management, owners and other interested parties. It consists of

three important components such as:

Trading account

Profit and loss account

Balance sheet

Trading account: It is considered as initial stage for process of preparing final accounts.

It reflects gross margin and loss within accounting year. Its main components are services and

sales rendered in credit side. It traces net sales and direct cost of goods sold and balance of this

account is disclosed through gross loss and profit. Usually, it is based on matching cost of goods

sold and selling price of services and goods.

Profit and Loss account: It is prepared for calculating net profit and loss and gathered

for ascertaining excess gains over huge losses and vice versa situation. It is second stage with

context to final accounts and related to specific accounting period in the year end. For purpose of

preparing this account, accrual basis of accounting is followed and account is directly credited

with income and gross profit through other relevant sources and debited with indirect losses and

expenses as well (Madalina and Adriana, 2018). The purpose of preparing profit and loss is to

ascertain net profit, control over expenses and comparison with profit of past year.

Statement of financial position: It is considered as last step of final account as it is not

any account as it does not have any debit or credit side. However, it has liabilities and asset side

as it reflects what is owned by business and what it owes to others with context of assets and

liabilities. Every asset and liability is reflected on their respective sides as similar to trial balance,

sum of asset should be equal to sum of liability side due to presence of double entry with context

of each transaction.

3.2 Statement of profit or loss

Income statement as per 31 December 2020

Particulars Details (£) Figure (£)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total revenue 557500

Less Cost of goods sold

Opening stock 50000

Add Purchases 420000

Less Closing stock 42000 428000

Gross margin 129500

Operating Expenses

Wages of shop minus payment of

shop wages 33300-200 33100

Cost of shop 6200

Telephone expenses minu accural

of telephone cost 600-100 500

Payment of interest 8000

Travel cost 550

Discount gained 900-450 450

Disposed Non-current asset 250

deprecia

tion premises 15000-5000 10000

deprecia

tion shop 14400-6400 8000

Debts not recoverable 500

Allowance of doubtful debt 250

adjustment related to allowance for

doubtful debt 50 800

Sum of Operating expenses 67850

Operating margin 61650

Less Value added tax 3250

Net Profit margin 58400

11

Less Cost of goods sold

Opening stock 50000

Add Purchases 420000

Less Closing stock 42000 428000

Gross margin 129500

Operating Expenses

Wages of shop minus payment of

shop wages 33300-200 33100

Cost of shop 6200

Telephone expenses minu accural

of telephone cost 600-100 500

Payment of interest 8000

Travel cost 550

Discount gained 900-450 450

Disposed Non-current asset 250

deprecia

tion premises 15000-5000 10000

deprecia

tion shop 14400-6400 8000

Debts not recoverable 500

Allowance of doubtful debt 250

adjustment related to allowance for

doubtful debt 50 800

Sum of Operating expenses 67850

Operating margin 61650

Less Value added tax 3250

Net Profit margin 58400

11

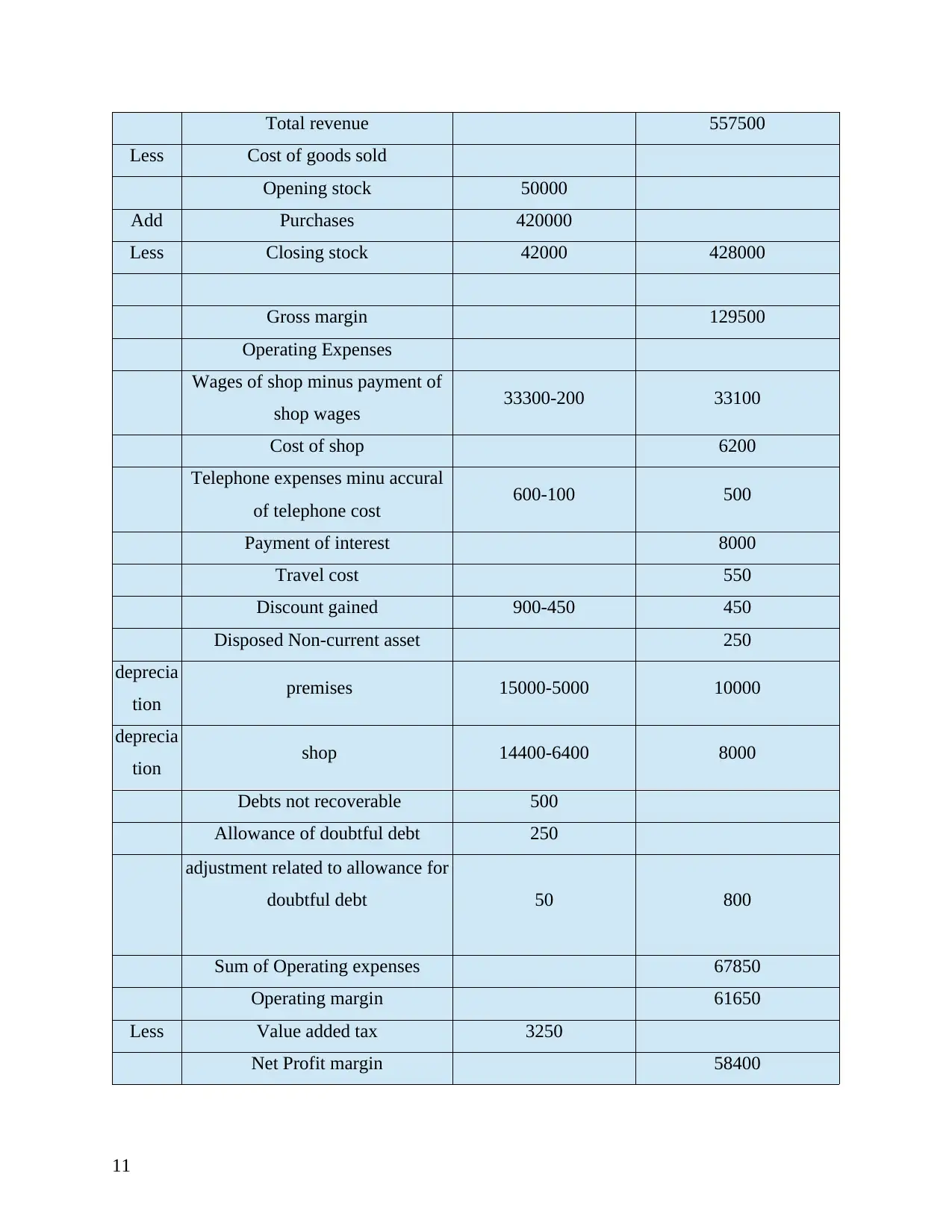

3.3 Statement of financial position

Balance sheet as on 31 December 2020

Particulars Details (£) Figure(£)

Assets

Current assets

Stock 428000

Opening stock 50000

add purchases 420000

less closing inventory 42000

sales ledger 10000 9200

Less Irrecoverable debt 500

Add Allowance (doubtful deb)t 250

Add doubtful debt (adjusted) 50

Bank 2650

Total Current assets 439850

Fixed assets

premises 250000

Depreciation (accumulated) 15000

Charges of depreciation 5000 240000

Cost for fitting shop 40000

less Depreciation (accumulated) 14400

less Charges for depreciation 6400 32000

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

Value added tax 3250

12

Balance sheet as on 31 December 2020

Particulars Details (£) Figure(£)

Assets

Current assets

Stock 428000

Opening stock 50000

add purchases 420000

less closing inventory 42000

sales ledger 10000 9200

Less Irrecoverable debt 500

Add Allowance (doubtful deb)t 250

Add doubtful debt (adjusted) 50

Bank 2650

Total Current assets 439850

Fixed assets

premises 250000

Depreciation (accumulated) 15000

Charges of depreciation 5000 240000

Cost for fitting shop 40000

less Depreciation (accumulated) 14400

less Charges for depreciation 6400 32000

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

Value added tax 3250

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.