Final Account Preparation: Sole Traders, Partnerships and Accounting

VerifiedAdded on 2020/10/22

|19

|4543

|287

Report

AI Summary

This report comprehensively examines the preparation of final accounts for both sole traders and partnerships, covering crucial aspects such as the evaluation of needs, the processes involved, and the limitations encountered. It delves into the construction of accounts from incomplete records, explaining methods like the accounting equation and control accounts. The report also addresses the reasons for imbalances due to incorrect double entries and the challenges arising from insufficient or inconsistent data. Furthermore, it provides detailed calculations for opening and closing capital, cash/bank balances, and account balances using markup and margin methods. The report also includes the components of financial statements, including the statement of profit and loss, the statement of financial position, and the statement of profit and loss appropriation account. Finally, it explains the legislative and accounting requirements for partnerships, including partnership agreements and the determination of partner profits, along with the preparation of capital and current accounts.

PREPARE FINAL ACCOUNT

FOR SOLE TRADERS AND

PARTNERSHIP

FOR SOLE TRADERS AND

PARTNERSHIP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Evaluating need and process involved in preparation of final accounts......................................1

1.1 identification of reason for closing off accounts and producing trial balance.................1

1.2 explanation of process and limitations for preparing set of final accounts from trial

balance....................................................................................................................................2

1.3 methods which involved in constructing accounts from incomplete records...................2

1.4 explanation of reasons for imbalances resulting from incorrect double entries...............3

1.5 description of reasons for incomplete records arising from insufficient data and

inconsistencies within data provided......................................................................................3

2. Preparation of accounting records from incomplete information................................................4

2.1 calculation of opening and closing capital.......................................................................4

2.2 Calculation of opening and closing Cash/Bank balances.................................................4

2.4 calculation of account balances using marks ups and margins........................................5

3.2 Statement of profit and loss..............................................................................................6

3.3 Statement of financial position.........................................................................................7

4. Explanation on legislative and accounting requirements for partnerships..................................8

4.1 Description of key components of partnership agreement...............................................8

4.2 Description of key components of partnership accounts..................................................9

5. Statement of profit and loss appropriation account...................................................................10

5.1 statement of profit and loss appropriation account.........................................................10

5.2 determining profit for each partners after all deduction ................................................11

5.3 capital and current accounts for each partner.................................................................13

6. Statement of financial potion relating to each partner ..............................................................14

6.1 and 6.2 calculation of closing balance of each partner and statements of financial position

..............................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

1. Evaluating need and process involved in preparation of final accounts......................................1

1.1 identification of reason for closing off accounts and producing trial balance.................1

1.2 explanation of process and limitations for preparing set of final accounts from trial

balance....................................................................................................................................2

1.3 methods which involved in constructing accounts from incomplete records...................2

1.4 explanation of reasons for imbalances resulting from incorrect double entries...............3

1.5 description of reasons for incomplete records arising from insufficient data and

inconsistencies within data provided......................................................................................3

2. Preparation of accounting records from incomplete information................................................4

2.1 calculation of opening and closing capital.......................................................................4

2.2 Calculation of opening and closing Cash/Bank balances.................................................4

2.4 calculation of account balances using marks ups and margins........................................5

3.2 Statement of profit and loss..............................................................................................6

3.3 Statement of financial position.........................................................................................7

4. Explanation on legislative and accounting requirements for partnerships..................................8

4.1 Description of key components of partnership agreement...............................................8

4.2 Description of key components of partnership accounts..................................................9

5. Statement of profit and loss appropriation account...................................................................10

5.1 statement of profit and loss appropriation account.........................................................10

5.2 determining profit for each partners after all deduction ................................................11

5.3 capital and current accounts for each partner.................................................................13

6. Statement of financial potion relating to each partner ..............................................................14

6.1 and 6.2 calculation of closing balance of each partner and statements of financial position

..............................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In order to measure income earned during a financial year and to measure financial

position it is necessary to establish final accounts in both sole trader and partnership business.

This assessment will develop to provide effective understanding of key components which used

in preparing final accounts and partnership account in business. Moreover, method of

constructing accounts from incomplete records and reasons for imbalance resulting in incorrect

double entries will also be explained in this report.

1. Evaluating need and process involved in preparation of final accounts

1.1 identification of reason for closing off accounts and producing trial balance

Reason behind closing off accounts while preparing final accounts of company is to

ensure that revenue and expenses account of year will open with zero balance in next financial

year (Xie and et.al., 2018). When financial statements of companies get prepared then only

closing entries are recorded. Recording closing entries must require that debit balance recorded

in trial balance must have credit balance so that it get write off for next financial year.

Trial balance produced by companies in order to find accurateness of mathematical data

in books of accounts. If debit balance of trail balance will not get matched at the end then it

means that there is a big mathematical mistake. Therefore, reason for producing trail balance is

as follows-

Helpful in finding transposition error- Trial balance helps in finding transposition

error so that different between total of debit balance will get matched with credit

balance. It is helpful in finding error of commission. For example: written of wrong

amount 525 as 552.

Helpful in finding Mis-calculation error- this is the type of error which get

happened due to poor calculation power. Trial balance is the tool which helps in

finding such types of error by finding difference of total debit balances with credit

balances.

Helpful to find Duplication Error- Trail balance helps in finding error which

sometimes recorded two times. Therefore, it will help in reducing such types of error

while preparing final accounts.

1

In order to measure income earned during a financial year and to measure financial

position it is necessary to establish final accounts in both sole trader and partnership business.

This assessment will develop to provide effective understanding of key components which used

in preparing final accounts and partnership account in business. Moreover, method of

constructing accounts from incomplete records and reasons for imbalance resulting in incorrect

double entries will also be explained in this report.

1. Evaluating need and process involved in preparation of final accounts

1.1 identification of reason for closing off accounts and producing trial balance

Reason behind closing off accounts while preparing final accounts of company is to

ensure that revenue and expenses account of year will open with zero balance in next financial

year (Xie and et.al., 2018). When financial statements of companies get prepared then only

closing entries are recorded. Recording closing entries must require that debit balance recorded

in trial balance must have credit balance so that it get write off for next financial year.

Trial balance produced by companies in order to find accurateness of mathematical data

in books of accounts. If debit balance of trail balance will not get matched at the end then it

means that there is a big mathematical mistake. Therefore, reason for producing trail balance is

as follows-

Helpful in finding transposition error- Trial balance helps in finding transposition

error so that different between total of debit balance will get matched with credit

balance. It is helpful in finding error of commission. For example: written of wrong

amount 525 as 552.

Helpful in finding Mis-calculation error- this is the type of error which get

happened due to poor calculation power. Trial balance is the tool which helps in

finding such types of error by finding difference of total debit balances with credit

balances.

Helpful to find Duplication Error- Trail balance helps in finding error which

sometimes recorded two times. Therefore, it will help in reducing such types of error

while preparing final accounts.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2 explanation of process and limitations for preparing set of final accounts from trial balance

Trial balance is known for list of all debit and credit accounts of any entity. It is prepared

after all the transaction in a given period have been journalised and get posted in general ledger

account. Once trial balance gets prepared, next step is to prepare financial statements (Vollmer,

2018).

Financial statements get prepared with the use of revenue and expense accounts from trail

balance. All the debit balances of trail balances will be recorded in financial statements as

indirect expenses. Further, with the use of net profit and net loss, financial position of company

gets prepared.

Financial position of company gets prepared by involving and re-arranging items and

accounts in trail balance. By eliminating from trial balance of all accounts excepts for assets,

liabilities and equity for preparing and matching financial position of the company.

Its limitations:

Very first and major limitation regarding the process of making final accounts from

trial balance if any type of error got develop while preparing trial balance then whole

final accounts of any type of entity prepared in wrong way

Trail balance does not show any kind of omission, errors or not posting any entry.

1.3 methods which involved in constructing accounts from incomplete records

Accounting records which are not maintained or kept in accordance with double entry

system of book keeping system then it will be considered as incomplete records. It is

unsystematic method for recording particular transactions (Umoru and Bala, 2018). If certain

accounts will get prepared through incomplete records then information which generated through

such accounts will not provide accuracy. Such accounts are also not comparable and capable

because of lack in uniformity. Therefore, in order to present accounts of company with

incomplete records, three types of process get involved which are as follows-

The accounting equation:

If there is no proper information regarding value of capital but there are some details of

assets and liabilities then this accounting equation method will get used to work out the value of

capital. The formula to compute capital in this method is

capital = total assets – total liabilities

2

Trial balance is known for list of all debit and credit accounts of any entity. It is prepared

after all the transaction in a given period have been journalised and get posted in general ledger

account. Once trial balance gets prepared, next step is to prepare financial statements (Vollmer,

2018).

Financial statements get prepared with the use of revenue and expense accounts from trail

balance. All the debit balances of trail balances will be recorded in financial statements as

indirect expenses. Further, with the use of net profit and net loss, financial position of company

gets prepared.

Financial position of company gets prepared by involving and re-arranging items and

accounts in trail balance. By eliminating from trial balance of all accounts excepts for assets,

liabilities and equity for preparing and matching financial position of the company.

Its limitations:

Very first and major limitation regarding the process of making final accounts from

trial balance if any type of error got develop while preparing trial balance then whole

final accounts of any type of entity prepared in wrong way

Trail balance does not show any kind of omission, errors or not posting any entry.

1.3 methods which involved in constructing accounts from incomplete records

Accounting records which are not maintained or kept in accordance with double entry

system of book keeping system then it will be considered as incomplete records. It is

unsystematic method for recording particular transactions (Umoru and Bala, 2018). If certain

accounts will get prepared through incomplete records then information which generated through

such accounts will not provide accuracy. Such accounts are also not comparable and capable

because of lack in uniformity. Therefore, in order to present accounts of company with

incomplete records, three types of process get involved which are as follows-

The accounting equation:

If there is no proper information regarding value of capital but there are some details of

assets and liabilities then this accounting equation method will get used to work out the value of

capital. The formula to compute capital in this method is

capital = total assets – total liabilities

2

Control accounts:

if there are missing balances from accounts then control accounts method will get used. It

involves completing the accounts such as bank control account will the incomplete details.

Balancing figure which get generated through this method will be considered as missing balance.

Markup or margin method:

This method will get adopted by any type of entity when they have appropriate sales

figure and to know amount of cost of goods sold. This method is considered as handy for

working with incomplete accounts. Through this method, as much as information will get

generated.

1.4 explanation of reasons for imbalances resulting from incorrect double entries

Accounting error in double entry book system may get occur with number of reasons.

Error in accounting error causes trial balance not to balance. With incorrect double entries, final

accounts will not get prepared with accuracy (Campos and et.al., 2019). Journal entries will

prepare accurately and will also interpret wrong due to incorrect double entries.

Error of reversal may get occur with incorrect double entry. It gets occur when a

transaction that must be posted as debit side will get recorded in credit side of the accounts. This

will result in imbalance of trial and ledger balances. Wrongly applies of accounting principle

also leads in imbalances of accounts. It gets happened when entry of expense recorded as entry

of asset. An error is made while entering a transaction will also result in imbalances of accounts.

These are the reasons which result from incorrect double entries.

1.5 description of reasons for incomplete records arising from insufficient data and

inconsistencies within data provided

Records which maintain through the use of single entry system is known as incomplete

records. If there is a lack in maintaining and preserving sufficient data of any type of entity then

it will result in showing incomplete records. (BELLO, 2018). The reason of incomplete data

arises from insufficient data are:

Unintentional failure to record: It happens when accountant forget or miss to post any entry or

transaction in books of accounts.

3

if there are missing balances from accounts then control accounts method will get used. It

involves completing the accounts such as bank control account will the incomplete details.

Balancing figure which get generated through this method will be considered as missing balance.

Markup or margin method:

This method will get adopted by any type of entity when they have appropriate sales

figure and to know amount of cost of goods sold. This method is considered as handy for

working with incomplete accounts. Through this method, as much as information will get

generated.

1.4 explanation of reasons for imbalances resulting from incorrect double entries

Accounting error in double entry book system may get occur with number of reasons.

Error in accounting error causes trial balance not to balance. With incorrect double entries, final

accounts will not get prepared with accuracy (Campos and et.al., 2019). Journal entries will

prepare accurately and will also interpret wrong due to incorrect double entries.

Error of reversal may get occur with incorrect double entry. It gets occur when a

transaction that must be posted as debit side will get recorded in credit side of the accounts. This

will result in imbalance of trial and ledger balances. Wrongly applies of accounting principle

also leads in imbalances of accounts. It gets happened when entry of expense recorded as entry

of asset. An error is made while entering a transaction will also result in imbalances of accounts.

These are the reasons which result from incorrect double entries.

1.5 description of reasons for incomplete records arising from insufficient data and

inconsistencies within data provided

Records which maintain through the use of single entry system is known as incomplete

records. If there is a lack in maintaining and preserving sufficient data of any type of entity then

it will result in showing incomplete records. (BELLO, 2018). The reason of incomplete data

arises from insufficient data are:

Unintentional failure to record: It happens when accountant forget or miss to post any entry or

transaction in books of accounts.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Data Loss: the businesses which depends on paper work many times suffers from loss of data,

unrecorded transaction etc. businesses are moving to computer process which helps in preventing

such omissions.

Intentional manipulation: some times, employees that are going to leave the company or

intended to such fraudulent activities does this errors intentionally.

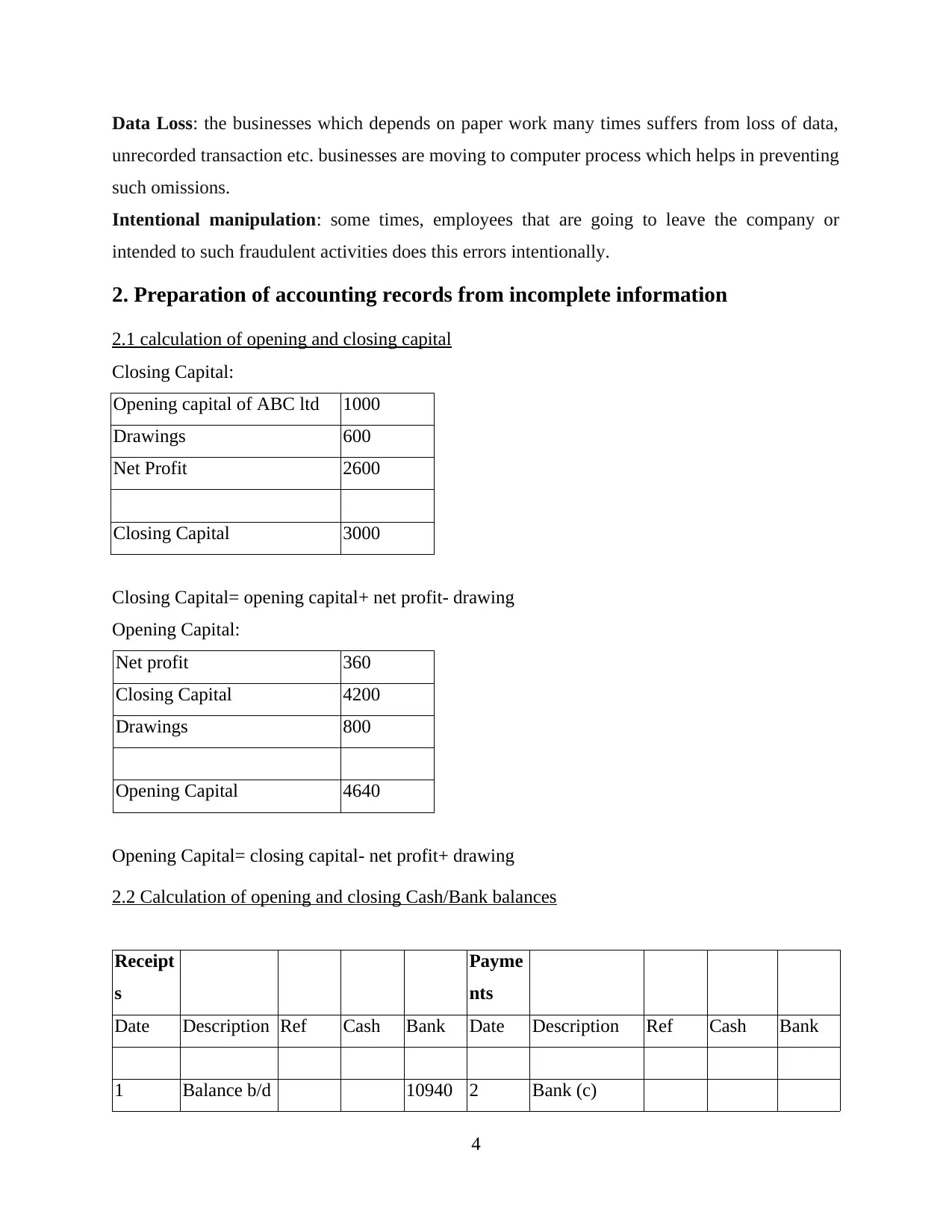

2. Preparation of accounting records from incomplete information

2.1 calculation of opening and closing capital

Closing Capital:

Opening capital of ABC ltd 1000

Drawings 600

Net Profit 2600

Closing Capital 3000

Closing Capital= opening capital+ net profit- drawing

Opening Capital:

Net profit 360

Closing Capital 4200

Drawings 800

Opening Capital 4640

Opening Capital= closing capital- net profit+ drawing

2.2 Calculation of opening and closing Cash/Bank balances

Receipt

s

Payme

nts

Date Description Ref Cash Bank Date Description Ref Cash Bank

1 Balance b/d 10940 2 Bank (c)

4

unrecorded transaction etc. businesses are moving to computer process which helps in preventing

such omissions.

Intentional manipulation: some times, employees that are going to leave the company or

intended to such fraudulent activities does this errors intentionally.

2. Preparation of accounting records from incomplete information

2.1 calculation of opening and closing capital

Closing Capital:

Opening capital of ABC ltd 1000

Drawings 600

Net Profit 2600

Closing Capital 3000

Closing Capital= opening capital+ net profit- drawing

Opening Capital:

Net profit 360

Closing Capital 4200

Drawings 800

Opening Capital 4640

Opening Capital= closing capital- net profit+ drawing

2.2 Calculation of opening and closing Cash/Bank balances

Receipt

s

Payme

nts

Date Description Ref Cash Bank Date Description Ref Cash Bank

1 Balance b/d 10940 2 Bank (c)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

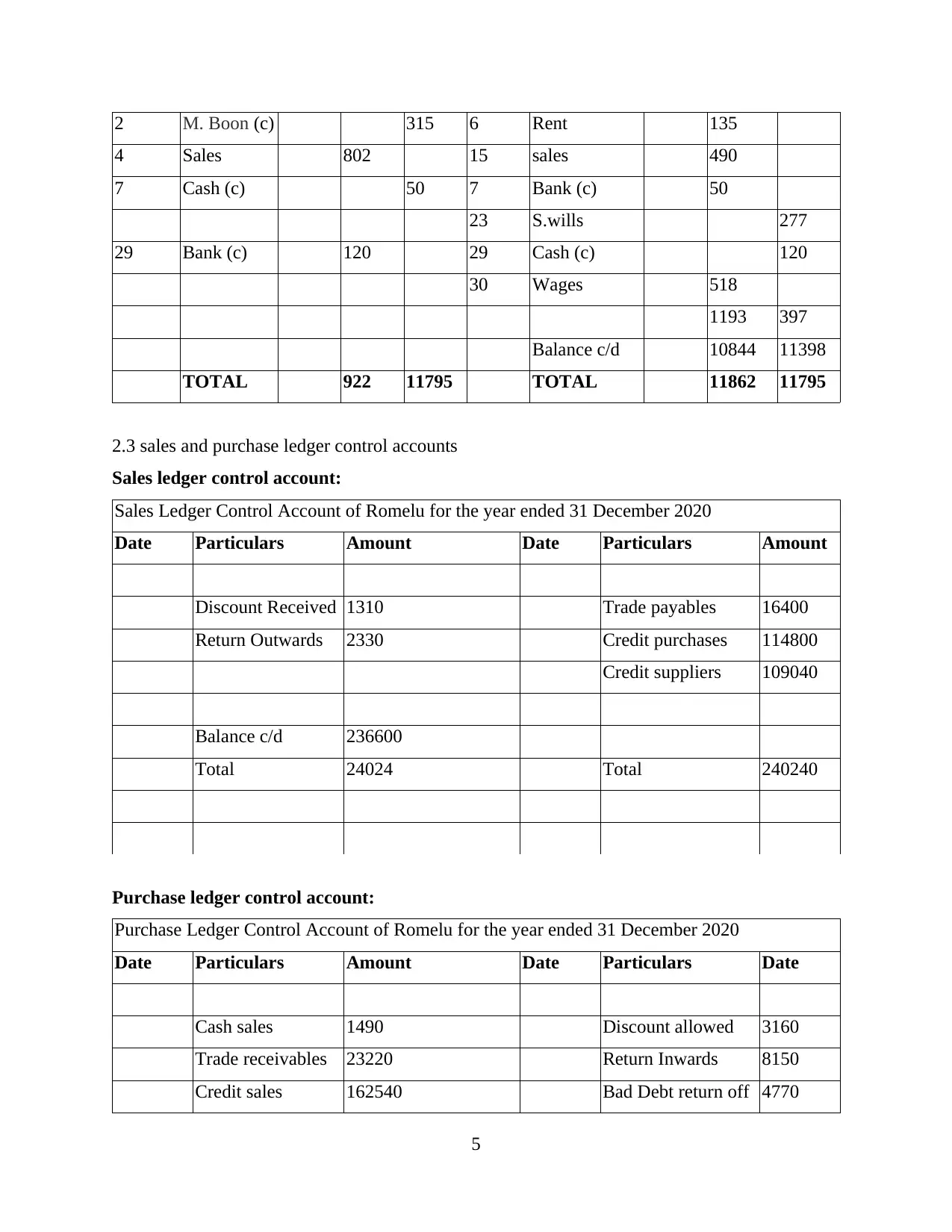

2 M. Boon (c) 315 6 Rent 135

4 Sales 802 15 sales 490

7 Cash (c) 50 7 Bank (c) 50

23 S.wills 277

29 Bank (c) 120 29 Cash (c) 120

30 Wages 518

1193 397

Balance c/d 10844 11398

TOTAL 922 11795 TOTAL 11862 11795

2.3 sales and purchase ledger control accounts

Sales ledger control account:

Sales Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Amount

Discount Received 1310 Trade payables 16400

Return Outwards 2330 Credit purchases 114800

Credit suppliers 109040

Balance c/d 236600

Total 24024 Total 240240

Purchase ledger control account:

Purchase Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Date

Cash sales 1490 Discount allowed 3160

Trade receivables 23220 Return Inwards 8150

Credit sales 162540 Bad Debt return off 4770

5

4 Sales 802 15 sales 490

7 Cash (c) 50 7 Bank (c) 50

23 S.wills 277

29 Bank (c) 120 29 Cash (c) 120

30 Wages 518

1193 397

Balance c/d 10844 11398

TOTAL 922 11795 TOTAL 11862 11795

2.3 sales and purchase ledger control accounts

Sales ledger control account:

Sales Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Amount

Discount Received 1310 Trade payables 16400

Return Outwards 2330 Credit purchases 114800

Credit suppliers 109040

Balance c/d 236600

Total 24024 Total 240240

Purchase ledger control account:

Purchase Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Date

Cash sales 1490 Discount allowed 3160

Trade receivables 23220 Return Inwards 8150

Credit sales 162540 Bad Debt return off 4770

5

Cash from cr-

edit customers

146610 Doubtfull debt 660

Balance c/d 317120

Total 333860 Total 333860

2.4 calculation of account balances using marks ups and margins

Margin= sales – COGS. For example: let the product of sells for £200 and costs £120. Then its

margin is £80

Markup is the amount by which cost of product is increased for deriving its selling price. For

example: markup of £80 from the £120 cost yields is £200.

3. Final accounts for sole traders

3.1 explanation of components for set of final accounts for sale trader

The final accounts of sole trader consist of trading, profit & loss account and a balance

sheet (Bernstein, 2018). Final accounts of sole trader often produced more than once in a year

which is in accordance with owner. Therefore, explanation of three components are as follows-

Trail Balance:

It is the first and foremost key component in set of final account for sole trader. It is

starting point in order to prepare set of final accounts. Figures which are recorded in trail balance

will get used in making final accounts of sole trader. In order to detect mathematical error which

have occurred in system of double entry, trial balance will prepare by sole trader.

Trading and profit and loss account:

Reason behind preparing this set of accounts is to measure income of a business which

has received in financial year by selling goods and by providing appropriate services. These

accounts also help in measuring expenses which have incurred throughout the year. Difference

which measured with income and expense will result in net profit of business which belongs to

owner.

Balance Sheet:

It is known as snapshot of the business at particular date. It is used by sole trader in order

to meet its financial position (Statement of Financial Position, 2018). Generally, two

6

edit customers

146610 Doubtfull debt 660

Balance c/d 317120

Total 333860 Total 333860

2.4 calculation of account balances using marks ups and margins

Margin= sales – COGS. For example: let the product of sells for £200 and costs £120. Then its

margin is £80

Markup is the amount by which cost of product is increased for deriving its selling price. For

example: markup of £80 from the £120 cost yields is £200.

3. Final accounts for sole traders

3.1 explanation of components for set of final accounts for sale trader

The final accounts of sole trader consist of trading, profit & loss account and a balance

sheet (Bernstein, 2018). Final accounts of sole trader often produced more than once in a year

which is in accordance with owner. Therefore, explanation of three components are as follows-

Trail Balance:

It is the first and foremost key component in set of final account for sole trader. It is

starting point in order to prepare set of final accounts. Figures which are recorded in trail balance

will get used in making final accounts of sole trader. In order to detect mathematical error which

have occurred in system of double entry, trial balance will prepare by sole trader.

Trading and profit and loss account:

Reason behind preparing this set of accounts is to measure income of a business which

has received in financial year by selling goods and by providing appropriate services. These

accounts also help in measuring expenses which have incurred throughout the year. Difference

which measured with income and expense will result in net profit of business which belongs to

owner.

Balance Sheet:

It is known as snapshot of the business at particular date. It is used by sole trader in order

to meet its financial position (Statement of Financial Position, 2018). Generally, two

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

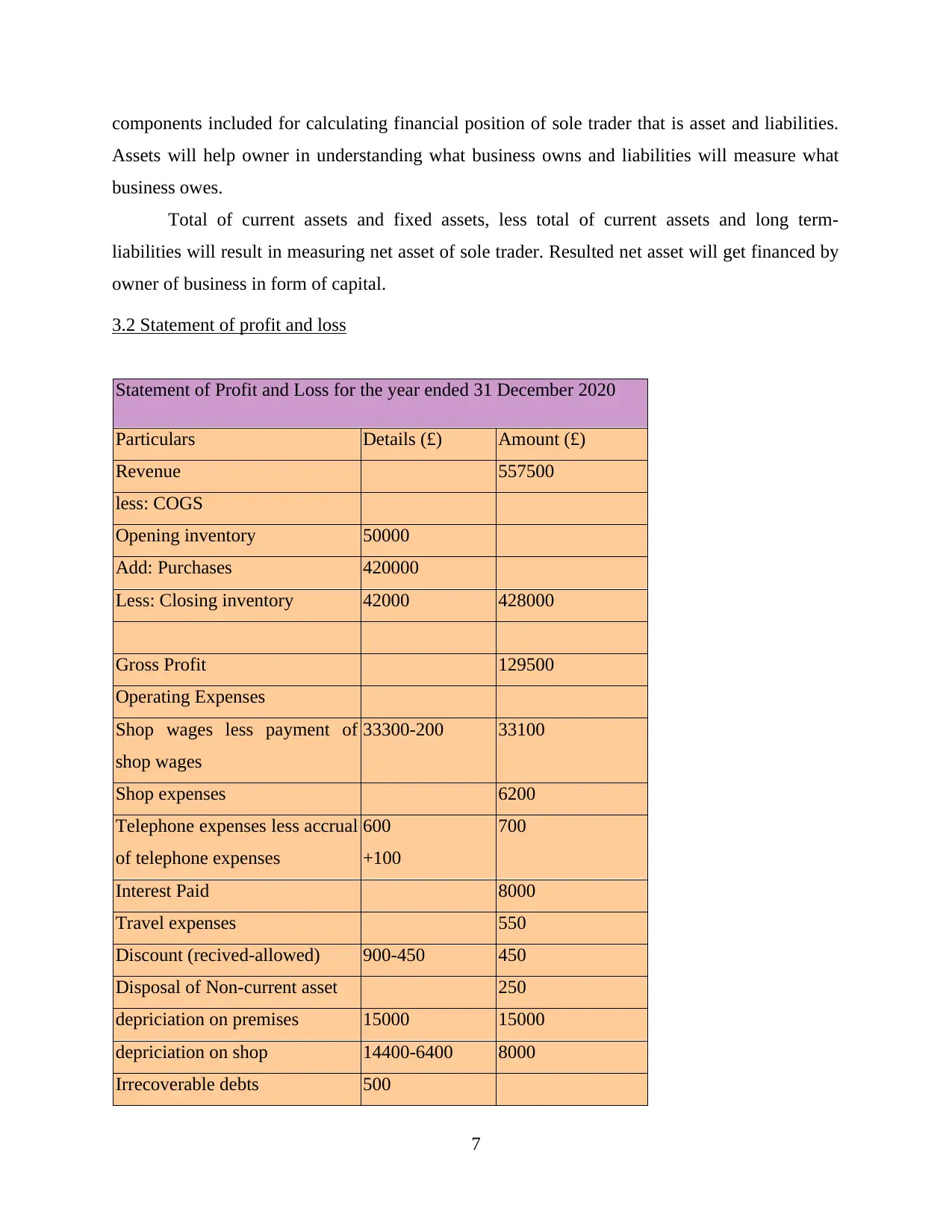

components included for calculating financial position of sole trader that is asset and liabilities.

Assets will help owner in understanding what business owns and liabilities will measure what

business owes.

Total of current assets and fixed assets, less total of current assets and long term-

liabilities will result in measuring net asset of sole trader. Resulted net asset will get financed by

owner of business in form of capital.

3.2 Statement of profit and loss

Statement of Profit and Loss for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Revenue 557500

less: COGS

Opening inventory 50000

Add: Purchases 420000

Less: Closing inventory 42000 428000

Gross Profit 129500

Operating Expenses

Shop wages less payment of

shop wages

33300-200 33100

Shop expenses 6200

Telephone expenses less accrual

of telephone expenses

600

+100

700

Interest Paid 8000

Travel expenses 550

Discount (recived-allowed) 900-450 450

Disposal of Non-current asset 250

depriciation on premises 15000 15000

depriciation on shop 14400-6400 8000

Irrecoverable debts 500

7

Assets will help owner in understanding what business owns and liabilities will measure what

business owes.

Total of current assets and fixed assets, less total of current assets and long term-

liabilities will result in measuring net asset of sole trader. Resulted net asset will get financed by

owner of business in form of capital.

3.2 Statement of profit and loss

Statement of Profit and Loss for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Revenue 557500

less: COGS

Opening inventory 50000

Add: Purchases 420000

Less: Closing inventory 42000 428000

Gross Profit 129500

Operating Expenses

Shop wages less payment of

shop wages

33300-200 33100

Shop expenses 6200

Telephone expenses less accrual

of telephone expenses

600

+100

700

Interest Paid 8000

Travel expenses 550

Discount (recived-allowed) 900-450 450

Disposal of Non-current asset 250

depriciation on premises 15000 15000

depriciation on shop 14400-6400 8000

Irrecoverable debts 500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Allowance for doubt full debt 250

adjustment for allowance for

doubtfull debt

50 800

Total operating expenses 72950

Operating Profit 61650

Less: VAT 3250

Net Profit 58400

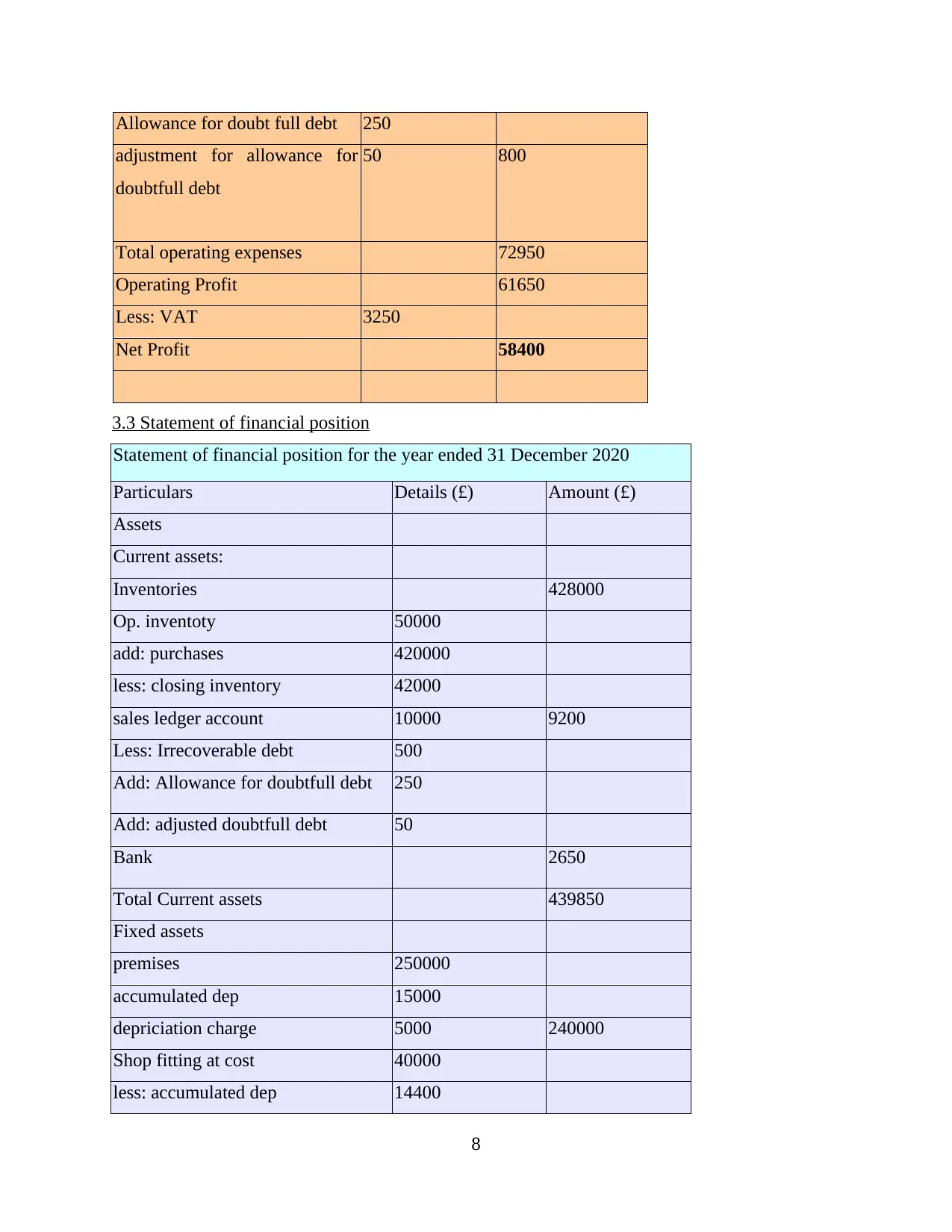

3.3 Statement of financial position

Statement of financial position for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Assets

Current assets:

Inventories 428000

Op. inventoty 50000

add: purchases 420000

less: closing inventory 42000

sales ledger account 10000 9200

Less: Irrecoverable debt 500

Add: Allowance for doubtfull debt 250

Add: adjusted doubtfull debt 50

Bank 2650

Total Current assets 439850

Fixed assets

premises 250000

accumulated dep 15000

depriciation charge 5000 240000

Shop fitting at cost 40000

less: accumulated dep 14400

8

adjustment for allowance for

doubtfull debt

50 800

Total operating expenses 72950

Operating Profit 61650

Less: VAT 3250

Net Profit 58400

3.3 Statement of financial position

Statement of financial position for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Assets

Current assets:

Inventories 428000

Op. inventoty 50000

add: purchases 420000

less: closing inventory 42000

sales ledger account 10000 9200

Less: Irrecoverable debt 500

Add: Allowance for doubtfull debt 250

Add: adjusted doubtfull debt 50

Bank 2650

Total Current assets 439850

Fixed assets

premises 250000

accumulated dep 15000

depriciation charge 5000 240000

Shop fitting at cost 40000

less: accumulated dep 14400

8

less: depriciation charge 6400 32000

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

VAT 3250

Loan 130000

Total current liabilities 144500

Non-Current liabilities 407950

Total Liabilities 552450

equity capital 125000

less: drawings 24000 101000

Net profit 58400

Total Liabilities and equity 711850

4. Explanation on legislative and accounting requirements for partnerships

4.1 Description of key components of partnership agreement

Partnership agreement is they legal protection for members who have agreed in forming

business partnership. It is type of document without which member have to rely on federal and

state laws in order to distribute their profits and loss (Gransby, 2018). It defines nature of

business and personal liability which carried by each member. Components of partnership

agreement is as follows-

Ownership- this component defines each percentage of company which has owned

by each partner. Percentage of profit sharing ratio between partners in order to

distribute profit and loss will get recognised in this component.

9

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

VAT 3250

Loan 130000

Total current liabilities 144500

Non-Current liabilities 407950

Total Liabilities 552450

equity capital 125000

less: drawings 24000 101000

Net profit 58400

Total Liabilities and equity 711850

4. Explanation on legislative and accounting requirements for partnerships

4.1 Description of key components of partnership agreement

Partnership agreement is they legal protection for members who have agreed in forming

business partnership. It is type of document without which member have to rely on federal and

state laws in order to distribute their profits and loss (Gransby, 2018). It defines nature of

business and personal liability which carried by each member. Components of partnership

agreement is as follows-

Ownership- this component defines each percentage of company which has owned

by each partner. Percentage of profit sharing ratio between partners in order to

distribute profit and loss will get recognised in this component.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.