Final Accounts: Sole Traders and Partnerships - Accounting Principles

VerifiedAdded on 2021/01/01

|16

|4669

|274

Homework Assignment

AI Summary

This assignment delves into the preparation of final accounts for both sole traders and partnerships, emphasizing the importance of accurate financial reporting. It explores the process of closing accounts and producing a trial balance, highlighting the limitations of preparing final accounts from a trial balance. The assignment covers methods for constructing accounts from incomplete records and the reasons for imbalances resulting from incorrect double entries, as well as inconsistencies within the data. It examines the key components of final accounts for a sole trader, including the statement of profit and loss and the statement of financial position. Furthermore, the assignment details the components of partnership agreements and partnership accounts, including the statement of profit and loss appropriation account, allocation of profit, and capital/current accounts. The content also covers the statement of balance sheet.

Prepare final accounts for sole

traders and partnerships

traders and partnerships

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Reasons for closing off accounts and producing a trial balance ..........................................3

1.2 The process, limitation of preparing a set of final accounts from a trial balance ................3

1.3 Methods of constructing accounts from incomplete records................................................4

1.4 Reasons for Imbalances resulting from incorrect double entries..........................................4

1.5 Reasons for incomplete records arising from insufficient data and inconsistencies within the

data provided ..............................................................................................................................4

TASK 2.................................................................................................................................................5

2.3 Sales and purchase leader control accounts .........................................................................6

2.4 Account balances using Mark Ups and margins .................................................................6

TASK 3.................................................................................................................................................6

3.1 Components of set of finals accounts for a sole trader ........................................................6

3.2 Statement of profit and loss .................................................................................................7

3.3 Statement of financial position ............................................................................................8

TASK 4.................................................................................................................................................9

4.1 Key components of partnership agreement...........................................................................9

4.2 Key components of partnership accounts ...........................................................................9

TASK 5...............................................................................................................................................10

5.1 statement of profit and loss appropriation account ............................................................10

5.2 Allocation of profit to partners after allowing interest on capital and drawing .................11

5.3 capital account and current for each partner......................................................................12

TASK 6 ..............................................................................................................................................13

6.1 and 6.2 statement of balance sheet.....................................................................................13

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Reasons for closing off accounts and producing a trial balance ..........................................3

1.2 The process, limitation of preparing a set of final accounts from a trial balance ................3

1.3 Methods of constructing accounts from incomplete records................................................4

1.4 Reasons for Imbalances resulting from incorrect double entries..........................................4

1.5 Reasons for incomplete records arising from insufficient data and inconsistencies within the

data provided ..............................................................................................................................4

TASK 2.................................................................................................................................................5

2.3 Sales and purchase leader control accounts .........................................................................6

2.4 Account balances using Mark Ups and margins .................................................................6

TASK 3.................................................................................................................................................6

3.1 Components of set of finals accounts for a sole trader ........................................................6

3.2 Statement of profit and loss .................................................................................................7

3.3 Statement of financial position ............................................................................................8

TASK 4.................................................................................................................................................9

4.1 Key components of partnership agreement...........................................................................9

4.2 Key components of partnership accounts ...........................................................................9

TASK 5...............................................................................................................................................10

5.1 statement of profit and loss appropriation account ............................................................10

5.2 Allocation of profit to partners after allowing interest on capital and drawing .................11

5.3 capital account and current for each partner......................................................................12

TASK 6 ..............................................................................................................................................13

6.1 and 6.2 statement of balance sheet.....................................................................................13

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

INTRODUCTION

Final accounts provide the information about the business profitability by preparing the final

accounts such as profit and loss account, balance sheet etc. This assignment is based on the

preparation of the final accounts of the sole trader and partnership. This study will include

importance and process of preparing the final accounts. Moreover, this study will include the

preparation of the final accounts by using the information provided in the study. Furthermore, this

study will include the sole trader final accounts which will consist of profit and loss of the business,

statement of financial position etc. Also, it will include the final account of partnership which will

consist of their capital and current accounts.

TASK 1

1.1 Reasons for closing off accounts and producing a trial balance

Trial balance is prepared on the basis of the closing off the accounts present in the ledger as

this statement is prepared for identifying the error present in the ledger account which is identified

by considering the closing balance of the account prepared. The trial balance includes the debit and

credit closing balances to determine the difference in the account balances. Balances relating to

expenses and assets are presented on the debit column whereas the incomes and liabilities are

shown on the credit side of the trial balance (Gransby, 2018). The main reason of the closing of the

account is to bring the temporary account balance to zero. The closing of account assists in

providing the excess of surplus balance either on debit or credit side of the account which helps in

preparing the trial balance as this balance are considered for preparing the trial balance. The ledger

account are close to determine the closing balance which is used in preparing the statements for the

next accounting period. The trial balance is prepared to identify if there is any mistake in preparing

the ledger accounts.

1.2 The process, limitation of preparing a set of final accounts from a trial balance

The Final accounts are prepared on the basis of Trial balance which assist in providing the

information about the accuracy of the transaction present in the ledger account. It assists in

identifying the error in the ledger account. The process of final account start with recording the

information from the trial balance in to the income statement (LEUCIUC, 2018). First the expense

which are shown in the trial balance are recorded on the debit side of the trading and profit and loss

Final accounts provide the information about the business profitability by preparing the final

accounts such as profit and loss account, balance sheet etc. This assignment is based on the

preparation of the final accounts of the sole trader and partnership. This study will include

importance and process of preparing the final accounts. Moreover, this study will include the

preparation of the final accounts by using the information provided in the study. Furthermore, this

study will include the sole trader final accounts which will consist of profit and loss of the business,

statement of financial position etc. Also, it will include the final account of partnership which will

consist of their capital and current accounts.

TASK 1

1.1 Reasons for closing off accounts and producing a trial balance

Trial balance is prepared on the basis of the closing off the accounts present in the ledger as

this statement is prepared for identifying the error present in the ledger account which is identified

by considering the closing balance of the account prepared. The trial balance includes the debit and

credit closing balances to determine the difference in the account balances. Balances relating to

expenses and assets are presented on the debit column whereas the incomes and liabilities are

shown on the credit side of the trial balance (Gransby, 2018). The main reason of the closing of the

account is to bring the temporary account balance to zero. The closing of account assists in

providing the excess of surplus balance either on debit or credit side of the account which helps in

preparing the trial balance as this balance are considered for preparing the trial balance. The ledger

account are close to determine the closing balance which is used in preparing the statements for the

next accounting period. The trial balance is prepared to identify if there is any mistake in preparing

the ledger accounts.

1.2 The process, limitation of preparing a set of final accounts from a trial balance

The Final accounts are prepared on the basis of Trial balance which assist in providing the

information about the accuracy of the transaction present in the ledger account. It assists in

identifying the error in the ledger account. The process of final account start with recording the

information from the trial balance in to the income statement (LEUCIUC, 2018). First the expense

which are shown in the trial balance are recorded on the debit side of the trading and profit and loss

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statement. Then the incomes in the trial balance are recorded on the credit side of the profit and loss

account that assist in identifying the net profit of the period. Moreover, the other debit balance of

the trial balance are shown on the assets side of balance sheet and the credit balances are shown on

the liabilities side on the balance sheet that assist in identify the financial position of the business on

the specific date. By preparing the final accounts from the trial balance can affect the final accounts

as if the ledgers are prepared in the wrong manner then the trial balance will show the inaccurate

balances which will reduce the accuracy of the final accounts as it will not show the profit and

financial position of the firm (ACCOUNTS FOR INCOMPLETE RECORDS, 2017). If there is error

of omission in the trial balance will affect the final accounts and will do not reflect the true and fair

position of the financial statement.

1.3 Methods of constructing accounts from incomplete records

Incomplete records of the company are those for which the company does not have the

accurate information. Account for these records are prepared using the accounting equations.

Moreover, For preparing the accounts one aspect of transaction is recorded. The profit and loss

statement is prepared by preparing the statement of affairs at the beginning and at the end of

period. Moreover, the statement of assets and liabilities is prepared at the beginning and end to

ascertain the change in capital. The incomplete records is the situation in which the organisation

does not use double entry method of bookkeeping. The single -entry method is used in constructing

accounts from the incomplete records. In the incomplete record only the personal accounts are

considered. Single- entry system in which either one- sided or no entry is made. In this method of

preparing accounts record of cash and personal accounts of debtors and creditors are maintained

properly (Nuthall and Old, 2017). In this system information relating to assets, liabilities, incomes

and expenses is partially recorded. This method is unsystematic of recording transactions and to

determine the net profit information collected from the original vouchers such as sales invoice etc.

Ass per this method the profit is estimated as the information is incomplete due to which the profit

or loss recorded is estimated.

1.4 Reasons for Imbalances resulting from incorrect double entries.

The incorrect entries in the journal accounts result into unequal balances due to which the

final accounts prepared are inaccurate and does not contain the true information relating to the

transactions. The main reasons of the imbalances includes the misappropriation of the amount in the

double entries will give the inaccurate balances which will affect the final accounts and thus the

profit and loss statement will not show the correct not profit (Rant and et.al., 2017). Moreover, the

incorrect transaction in the journal will cause the finals accounts to be inappropriate. Furthermore,

account that assist in identifying the net profit of the period. Moreover, the other debit balance of

the trial balance are shown on the assets side of balance sheet and the credit balances are shown on

the liabilities side on the balance sheet that assist in identify the financial position of the business on

the specific date. By preparing the final accounts from the trial balance can affect the final accounts

as if the ledgers are prepared in the wrong manner then the trial balance will show the inaccurate

balances which will reduce the accuracy of the final accounts as it will not show the profit and

financial position of the firm (ACCOUNTS FOR INCOMPLETE RECORDS, 2017). If there is error

of omission in the trial balance will affect the final accounts and will do not reflect the true and fair

position of the financial statement.

1.3 Methods of constructing accounts from incomplete records

Incomplete records of the company are those for which the company does not have the

accurate information. Account for these records are prepared using the accounting equations.

Moreover, For preparing the accounts one aspect of transaction is recorded. The profit and loss

statement is prepared by preparing the statement of affairs at the beginning and at the end of

period. Moreover, the statement of assets and liabilities is prepared at the beginning and end to

ascertain the change in capital. The incomplete records is the situation in which the organisation

does not use double entry method of bookkeeping. The single -entry method is used in constructing

accounts from the incomplete records. In the incomplete record only the personal accounts are

considered. Single- entry system in which either one- sided or no entry is made. In this method of

preparing accounts record of cash and personal accounts of debtors and creditors are maintained

properly (Nuthall and Old, 2017). In this system information relating to assets, liabilities, incomes

and expenses is partially recorded. This method is unsystematic of recording transactions and to

determine the net profit information collected from the original vouchers such as sales invoice etc.

Ass per this method the profit is estimated as the information is incomplete due to which the profit

or loss recorded is estimated.

1.4 Reasons for Imbalances resulting from incorrect double entries.

The incorrect entries in the journal accounts result into unequal balances due to which the

final accounts prepared are inaccurate and does not contain the true information relating to the

transactions. The main reasons of the imbalances includes the misappropriation of the amount in the

double entries will give the inaccurate balances which will affect the final accounts and thus the

profit and loss statement will not show the correct not profit (Rant and et.al., 2017). Moreover, the

incorrect transaction in the journal will cause the finals accounts to be inappropriate. Furthermore,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The imbalances may be due to data damages or the information is incomplete which may affect the

final accounts and will show the inaccurate information in the balance sheet and profit and loss

statement (Pyo, Wood and Kim, 2016). Also, The difference in balance of accounts can be caused

due to wrong entry and omission of the entry which will give wrong trial balance and thus the

whole accounting process will be go wrong and will show the amount which is inaccurate.

1.5 Reasons for incomplete records arising from insufficient data and inconsistencies within the

data provided

The reasons for maintaining incomplete records is due to lack of knowledge regarding the

accounting principles. Another reasons for incompleteness is due to data loss due to theft, fire etc.

which make the information incomplete and this the organisation have insufficient data for

preparing the final accounts (ACCOUNTS FOR INCOMPLETE RECORDS, 2017). The reason for

incompleteness of the data is that maintaining records using double – entry system is expensive.

Moreover, maintaining incomplete records consumes fewer time due to which many organisations

prefer to use this method. Using single – entry methods is convenient due to which the information

is recorded incompletely. The incomplete record have fewer data due to which the organisation

does not have appropriate net profit. This system is ineffective for maintaining record as its reduce

the accuracy of the final accounts. This system is effective for sole trader as they have less

transaction due to which there is no need of double entry system. The incompleteness of the data

effect the final accounts as it does not provide the accurate financial position of the firm.

TASK 2

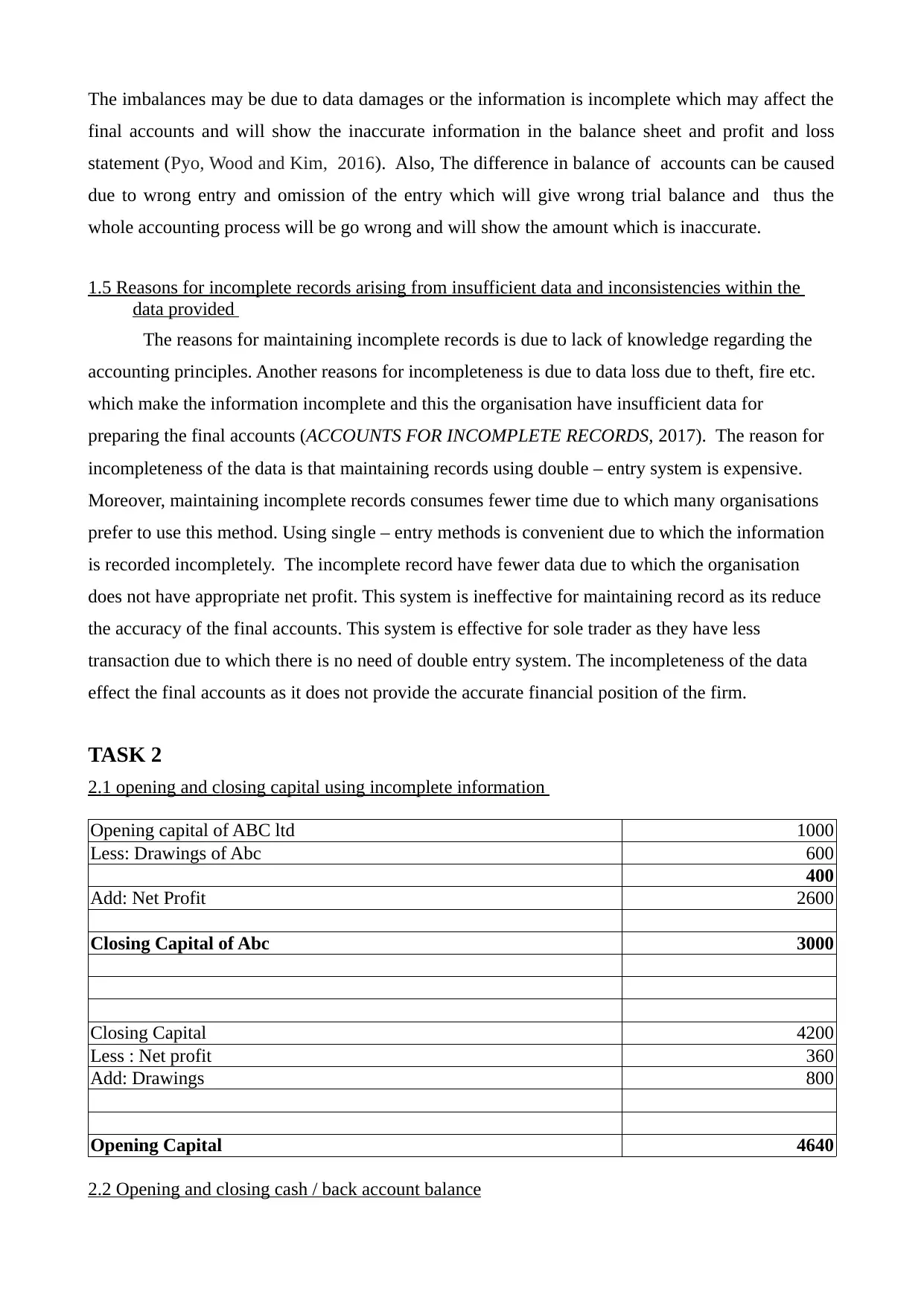

2.1 opening and closing capital using incomplete information

Opening capital of ABC ltd 1000

Less: Drawings of Abc 600

400

Add: Net Profit 2600

Closing Capital of Abc 3000

Closing Capital 4200

Less : Net profit 360

Add: Drawings 800

Opening Capital 4640

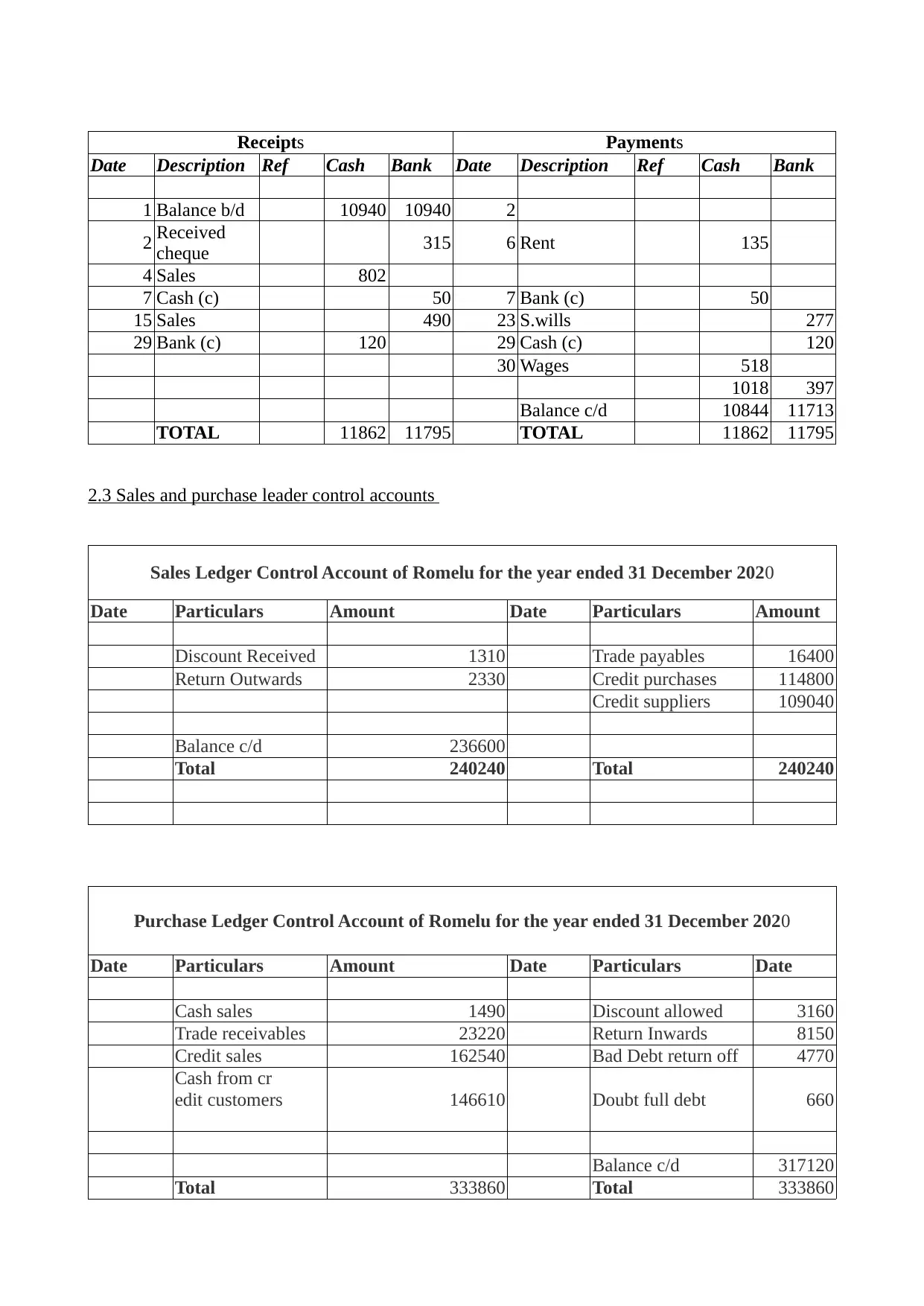

2.2 Opening and closing cash / back account balance

final accounts and will show the inaccurate information in the balance sheet and profit and loss

statement (Pyo, Wood and Kim, 2016). Also, The difference in balance of accounts can be caused

due to wrong entry and omission of the entry which will give wrong trial balance and thus the

whole accounting process will be go wrong and will show the amount which is inaccurate.

1.5 Reasons for incomplete records arising from insufficient data and inconsistencies within the

data provided

The reasons for maintaining incomplete records is due to lack of knowledge regarding the

accounting principles. Another reasons for incompleteness is due to data loss due to theft, fire etc.

which make the information incomplete and this the organisation have insufficient data for

preparing the final accounts (ACCOUNTS FOR INCOMPLETE RECORDS, 2017). The reason for

incompleteness of the data is that maintaining records using double – entry system is expensive.

Moreover, maintaining incomplete records consumes fewer time due to which many organisations

prefer to use this method. Using single – entry methods is convenient due to which the information

is recorded incompletely. The incomplete record have fewer data due to which the organisation

does not have appropriate net profit. This system is ineffective for maintaining record as its reduce

the accuracy of the final accounts. This system is effective for sole trader as they have less

transaction due to which there is no need of double entry system. The incompleteness of the data

effect the final accounts as it does not provide the accurate financial position of the firm.

TASK 2

2.1 opening and closing capital using incomplete information

Opening capital of ABC ltd 1000

Less: Drawings of Abc 600

400

Add: Net Profit 2600

Closing Capital of Abc 3000

Closing Capital 4200

Less : Net profit 360

Add: Drawings 800

Opening Capital 4640

2.2 Opening and closing cash / back account balance

Receipts Payments

Date Description Ref Cash Bank Date Description Ref Cash Bank

1 Balance b/d 10940 10940 2

2 Received

cheque 315 6 Rent 135

4 Sales 802

7 Cash (c) 50 7 Bank (c) 50

15 Sales 490 23 S.wills 277

29 Bank (c) 120 29 Cash (c) 120

30 Wages 518

1018 397

Balance c/d 10844 11713

TOTAL 11862 11795 TOTAL 11862 11795

2.3 Sales and purchase leader control accounts

Sales Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Amount

Discount Received 1310 Trade payables 16400

Return Outwards 2330 Credit purchases 114800

Credit suppliers 109040

Balance c/d 236600

Total 240240 Total 240240

Purchase Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Date

Cash sales 1490 Discount allowed 3160

Trade receivables 23220 Return Inwards 8150

Credit sales 162540 Bad Debt return off 4770

Cash from cr

edit customers 146610 Doubt full debt 660

Balance c/d 317120

Total 333860 Total 333860

Date Description Ref Cash Bank Date Description Ref Cash Bank

1 Balance b/d 10940 10940 2

2 Received

cheque 315 6 Rent 135

4 Sales 802

7 Cash (c) 50 7 Bank (c) 50

15 Sales 490 23 S.wills 277

29 Bank (c) 120 29 Cash (c) 120

30 Wages 518

1018 397

Balance c/d 10844 11713

TOTAL 11862 11795 TOTAL 11862 11795

2.3 Sales and purchase leader control accounts

Sales Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Amount

Discount Received 1310 Trade payables 16400

Return Outwards 2330 Credit purchases 114800

Credit suppliers 109040

Balance c/d 236600

Total 240240 Total 240240

Purchase Ledger Control Account of Romelu for the year ended 31 December 2020

Date Particulars Amount Date Particulars Date

Cash sales 1490 Discount allowed 3160

Trade receivables 23220 Return Inwards 8150

Credit sales 162540 Bad Debt return off 4770

Cash from cr

edit customers 146610 Doubt full debt 660

Balance c/d 317120

Total 333860 Total 333860

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.4 Account balances using Mark Ups and margins

Margin is equal to profit earned by the company whereas mark up is the amount by which

the cost of product is increased to derive the selling price. Margin is the sales less cost of good sold

for example, if the selling price of the product is $100 and cost $70 then its margin is $30 or margin

percentage is 30%. Markup is the amount by which the cost of the product is increased to determine

the selling price For example, If the markup is $30 and the cost is $70 then the selling price of the

product is $100.

TASK 3

3.1 Components of set of finals accounts for a sole trader

Sole traders are the people that own single business such as shops, factories, local franchises

etc. The sole traders have the benefit to own the profit earned by the business. The final accounts of

the sole traders includes trading and profit and loss accounts which is prepared to determine the

profitability of the business by recording the incomes and expenses for the period (Trader, 2017).

Another component of the sole trader final accounts includes the balance sheet which consist of

assets and liabilities of the business and the owners’ capital. Balance sheet assist in providing the

information to the owner regarding its financial position. The trading and profit and loss account

includes the incomes and expenses for the period which assist in identifying the profitability of the

business by subtracting the expenses from the incomes. Balance sheets of the sole trader provide the

information regarding its assets and liability which help the traders in identifying its financial

position. Balance sheet includes assets, liabilities, capital etc.

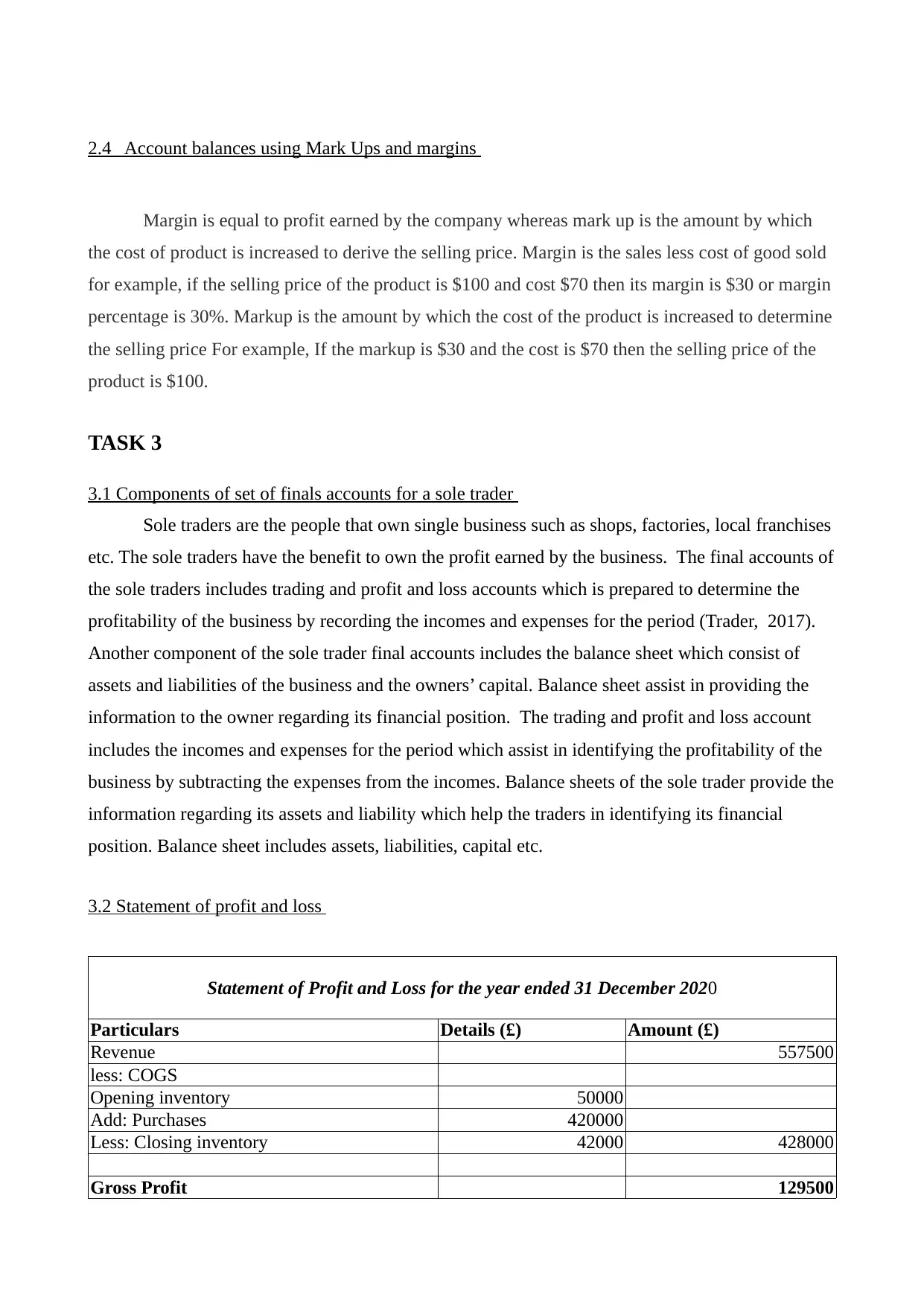

3.2 Statement of profit and loss

Statement of Profit and Loss for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Revenue 557500

less: COGS

Opening inventory 50000

Add: Purchases 420000

Less: Closing inventory 42000 428000

Gross Profit 129500

Margin is equal to profit earned by the company whereas mark up is the amount by which

the cost of product is increased to derive the selling price. Margin is the sales less cost of good sold

for example, if the selling price of the product is $100 and cost $70 then its margin is $30 or margin

percentage is 30%. Markup is the amount by which the cost of the product is increased to determine

the selling price For example, If the markup is $30 and the cost is $70 then the selling price of the

product is $100.

TASK 3

3.1 Components of set of finals accounts for a sole trader

Sole traders are the people that own single business such as shops, factories, local franchises

etc. The sole traders have the benefit to own the profit earned by the business. The final accounts of

the sole traders includes trading and profit and loss accounts which is prepared to determine the

profitability of the business by recording the incomes and expenses for the period (Trader, 2017).

Another component of the sole trader final accounts includes the balance sheet which consist of

assets and liabilities of the business and the owners’ capital. Balance sheet assist in providing the

information to the owner regarding its financial position. The trading and profit and loss account

includes the incomes and expenses for the period which assist in identifying the profitability of the

business by subtracting the expenses from the incomes. Balance sheets of the sole trader provide the

information regarding its assets and liability which help the traders in identifying its financial

position. Balance sheet includes assets, liabilities, capital etc.

3.2 Statement of profit and loss

Statement of Profit and Loss for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Revenue 557500

less: COGS

Opening inventory 50000

Add: Purchases 420000

Less: Closing inventory 42000 428000

Gross Profit 129500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating Expenses

Shop wages less payment of shop wages 33300-200 33100

Expenses for shop 6200

Telephone expenses less accural of telephone

expenses 600-100 500

Interest Paid 8000

Expenses for travel 550

Discount (received-allowed) 900-450 450

Disposal of Non-current asset 250

depriciation on premises 15000-5000 10000

depriciation on shop 14400-6400 8000

Irrecoverable debts 500

Allowance for doubt full debt 250

adjustment for allowance for doubtfull debt

adjustment for allowance for doubtfull debt 50 800

Total operating expenses 67850

Operating Profit 61650

Less: VAT 3250

Net Profit 58400

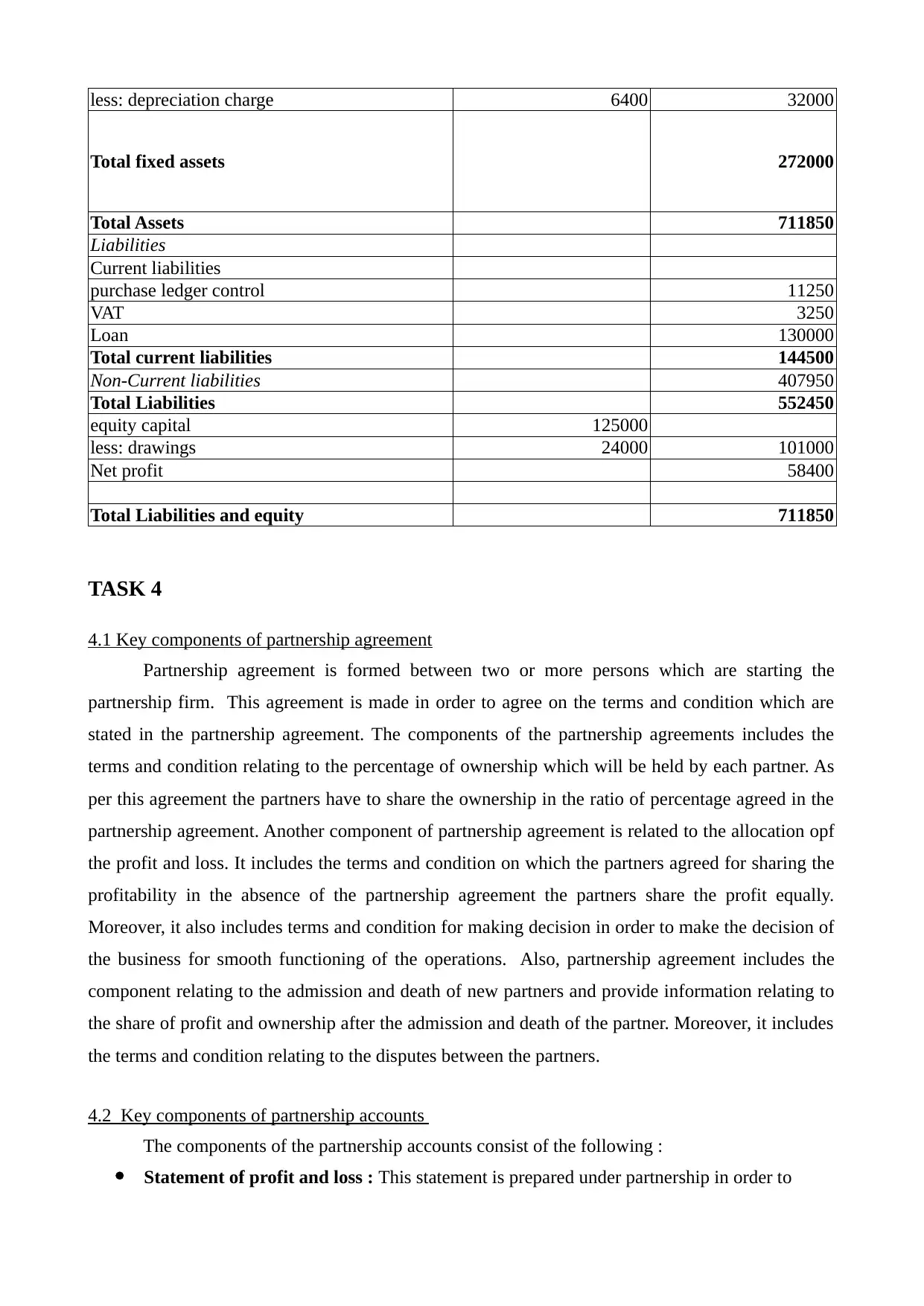

3.3 Statement of financial position

Statement of financial position for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Assets

Current assets:

Inventories 428000

Opening inventory 50000

add: purchases 420000

less: closing inventory 42000

sales ledger account 10000 9200

Less: Irrecoverable debt 500

Add: Allowance for doubtfull debt 250

Add: adjusted doubtfull debt 50

Bank 2650

Total Current assets 439850

Fixed assets

premises 250000

accumulated depreciation 15000

depreciation charge 5000 240000

Shop fitting at cost 40000

less: accumulated depreciation 14400

Shop wages less payment of shop wages 33300-200 33100

Expenses for shop 6200

Telephone expenses less accural of telephone

expenses 600-100 500

Interest Paid 8000

Expenses for travel 550

Discount (received-allowed) 900-450 450

Disposal of Non-current asset 250

depriciation on premises 15000-5000 10000

depriciation on shop 14400-6400 8000

Irrecoverable debts 500

Allowance for doubt full debt 250

adjustment for allowance for doubtfull debt

adjustment for allowance for doubtfull debt 50 800

Total operating expenses 67850

Operating Profit 61650

Less: VAT 3250

Net Profit 58400

3.3 Statement of financial position

Statement of financial position for the year ended 31 December 2020

Particulars Details (£) Amount (£)

Assets

Current assets:

Inventories 428000

Opening inventory 50000

add: purchases 420000

less: closing inventory 42000

sales ledger account 10000 9200

Less: Irrecoverable debt 500

Add: Allowance for doubtfull debt 250

Add: adjusted doubtfull debt 50

Bank 2650

Total Current assets 439850

Fixed assets

premises 250000

accumulated depreciation 15000

depreciation charge 5000 240000

Shop fitting at cost 40000

less: accumulated depreciation 14400

less: depreciation charge 6400 32000

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

VAT 3250

Loan 130000

Total current liabilities 144500

Non-Current liabilities 407950

Total Liabilities 552450

equity capital 125000

less: drawings 24000 101000

Net profit 58400

Total Liabilities and equity 711850

TASK 4

4.1 Key components of partnership agreement

Partnership agreement is formed between two or more persons which are starting the

partnership firm. This agreement is made in order to agree on the terms and condition which are

stated in the partnership agreement. The components of the partnership agreements includes the

terms and condition relating to the percentage of ownership which will be held by each partner. As

per this agreement the partners have to share the ownership in the ratio of percentage agreed in the

partnership agreement. Another component of partnership agreement is related to the allocation opf

the profit and loss. It includes the terms and condition on which the partners agreed for sharing the

profitability in the absence of the partnership agreement the partners share the profit equally.

Moreover, it also includes terms and condition for making decision in order to make the decision of

the business for smooth functioning of the operations. Also, partnership agreement includes the

component relating to the admission and death of new partners and provide information relating to

the share of profit and ownership after the admission and death of the partner. Moreover, it includes

the terms and condition relating to the disputes between the partners.

4.2 Key components of partnership accounts

The components of the partnership accounts consist of the following :

Statement of profit and loss : This statement is prepared under partnership in order to

Total fixed assets 272000

Total Assets 711850

Liabilities

Current liabilities

purchase ledger control 11250

VAT 3250

Loan 130000

Total current liabilities 144500

Non-Current liabilities 407950

Total Liabilities 552450

equity capital 125000

less: drawings 24000 101000

Net profit 58400

Total Liabilities and equity 711850

TASK 4

4.1 Key components of partnership agreement

Partnership agreement is formed between two or more persons which are starting the

partnership firm. This agreement is made in order to agree on the terms and condition which are

stated in the partnership agreement. The components of the partnership agreements includes the

terms and condition relating to the percentage of ownership which will be held by each partner. As

per this agreement the partners have to share the ownership in the ratio of percentage agreed in the

partnership agreement. Another component of partnership agreement is related to the allocation opf

the profit and loss. It includes the terms and condition on which the partners agreed for sharing the

profitability in the absence of the partnership agreement the partners share the profit equally.

Moreover, it also includes terms and condition for making decision in order to make the decision of

the business for smooth functioning of the operations. Also, partnership agreement includes the

component relating to the admission and death of new partners and provide information relating to

the share of profit and ownership after the admission and death of the partner. Moreover, it includes

the terms and condition relating to the disputes between the partners.

4.2 Key components of partnership accounts

The components of the partnership accounts consist of the following :

Statement of profit and loss : This statement is prepared under partnership in order to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

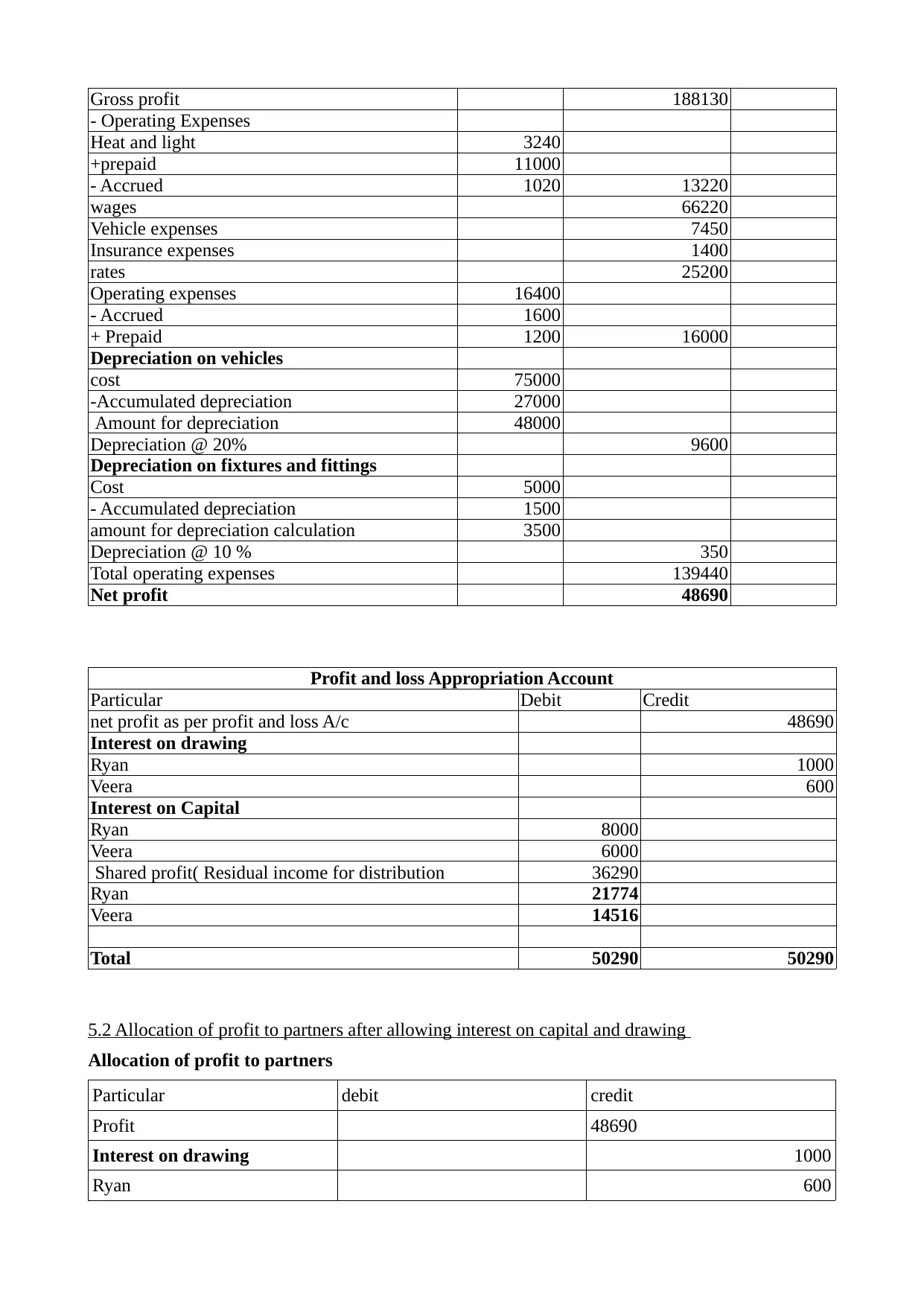

identify the profitability of the firm. It consists of expenses and incomes which are recorded

on the debit and credit side of the statement. After recording the incomes and expenses from

the trial balances the expenses are subtracted from the incomes to determine the net profit.

Partnership Appropriation Account : It is prepared by the partnership firm in order to

identify the share of profit. It assists in allocating the profit for the period. The partnership

appropriation take into consideration net profit earned on the basis of profit and loss

account, interest on capital, interest on drawings, salary to partners , partners commission

etc. This assist in identifying the residual value of the profit which will be distributed to the

partners. And then the profit is shared between the partner as per their sharing ratio.

Goodwill account : This account is prepared to show the amount of goodwill brought on

the admission of the new partner, Goodwill at the retirement of the partner etc. The opening

goodwill is debited in the account and after this the treatment of goodwill is made which

assist in identifying the closing balance of the goodwill which is shown on the assets side as

intangible assets.

Partner's Current account : The current account is prepared when there is fixed capital

and all the adjustment relating to interest in capital, interest on drawings, salary, commission

is done in this account. If the current account shows the debit balance they appear on the

assets side of the balance sheet. If it shows the credit balance it appears on the liabilities

side.

Partner's capital accounts : The capital accounts as per the fixed capital includes the

capital brought by the partners and the additional capital brought and withdrawn is adjusted

in this account (Surahyo, 2018). In fluctuation method the partner's capital account includes

the treatment of the interest on capital, interest on drawing, salary , commission etc.

Statement of financial position : It includes the assets and liabilities of the partnership

firm. This statement is prepared in to identify the financial position of the firm. Assets are

recorded on the debit side whereas liabilities are recorded at the credit side.

TASK 5

5.1 statement of profit and loss appropriation account

Working notes

Profit and loss Account

Particular Amount Total

Sales 812540 812540

-COGS 624410

on the debit and credit side of the statement. After recording the incomes and expenses from

the trial balances the expenses are subtracted from the incomes to determine the net profit.

Partnership Appropriation Account : It is prepared by the partnership firm in order to

identify the share of profit. It assists in allocating the profit for the period. The partnership

appropriation take into consideration net profit earned on the basis of profit and loss

account, interest on capital, interest on drawings, salary to partners , partners commission

etc. This assist in identifying the residual value of the profit which will be distributed to the

partners. And then the profit is shared between the partner as per their sharing ratio.

Goodwill account : This account is prepared to show the amount of goodwill brought on

the admission of the new partner, Goodwill at the retirement of the partner etc. The opening

goodwill is debited in the account and after this the treatment of goodwill is made which

assist in identifying the closing balance of the goodwill which is shown on the assets side as

intangible assets.

Partner's Current account : The current account is prepared when there is fixed capital

and all the adjustment relating to interest in capital, interest on drawings, salary, commission

is done in this account. If the current account shows the debit balance they appear on the

assets side of the balance sheet. If it shows the credit balance it appears on the liabilities

side.

Partner's capital accounts : The capital accounts as per the fixed capital includes the

capital brought by the partners and the additional capital brought and withdrawn is adjusted

in this account (Surahyo, 2018). In fluctuation method the partner's capital account includes

the treatment of the interest on capital, interest on drawing, salary , commission etc.

Statement of financial position : It includes the assets and liabilities of the partnership

firm. This statement is prepared in to identify the financial position of the firm. Assets are

recorded on the debit side whereas liabilities are recorded at the credit side.

TASK 5

5.1 statement of profit and loss appropriation account

Working notes

Profit and loss Account

Particular Amount Total

Sales 812540 812540

-COGS 624410

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross profit 188130

- Operating Expenses

Heat and light 3240

+prepaid 11000

- Accrued 1020 13220

wages 66220

Vehicle expenses 7450

Insurance expenses 1400

rates 25200

Operating expenses 16400

- Accrued 1600

+ Prepaid 1200 16000

Depreciation on vehicles

cost 75000

-Accumulated depreciation 27000

Amount for depreciation 48000

Depreciation @ 20% 9600

Depreciation on fixtures and fittings

Cost 5000

- Accumulated depreciation 1500

amount for depreciation calculation 3500

Depreciation @ 10 % 350

Total operating expenses 139440

Net profit 48690

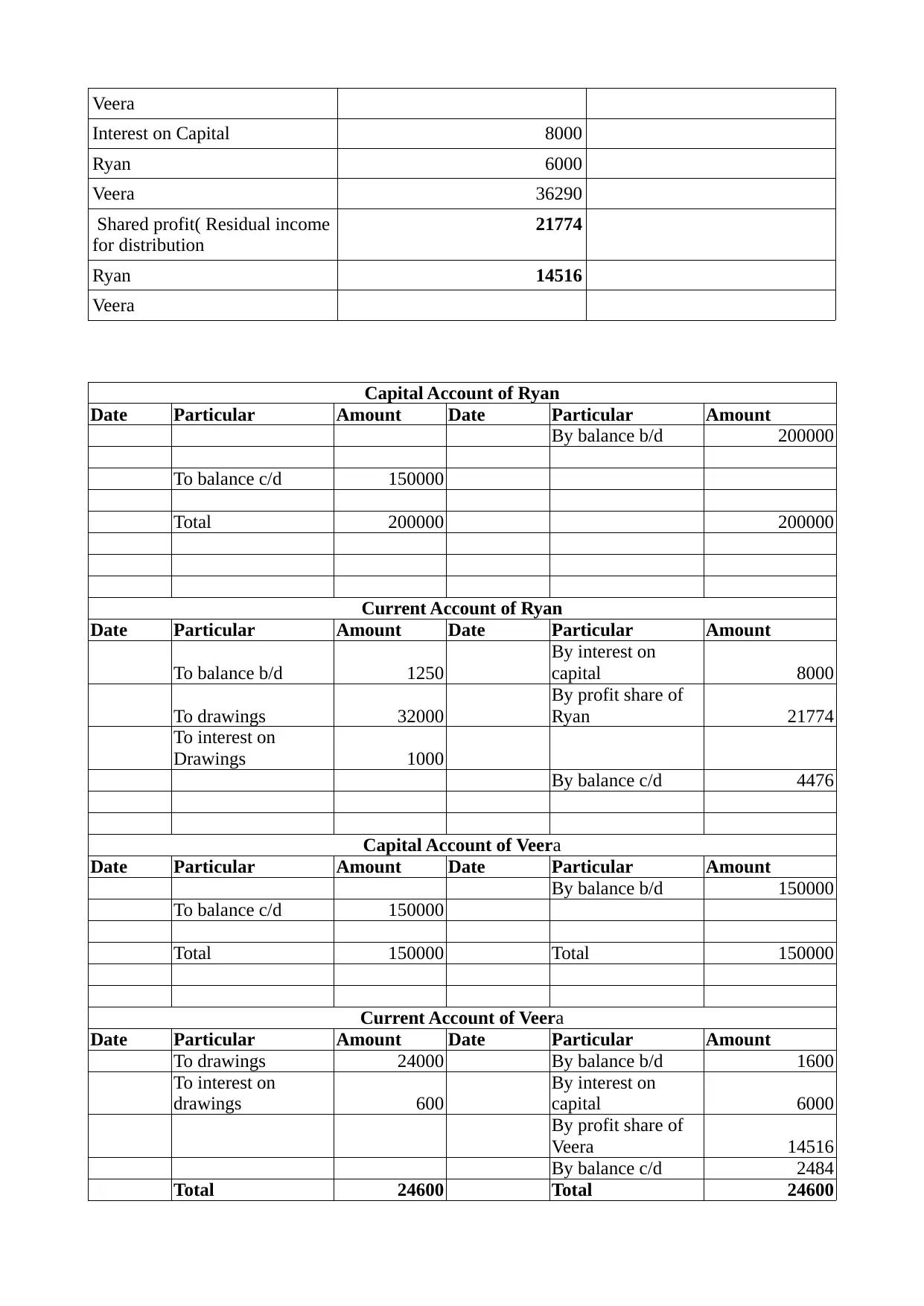

Profit and loss Appropriation Account

Particular Debit Credit

net profit as per profit and loss A/c 48690

Interest on drawing

Ryan 1000

Veera 600

Interest on Capital

Ryan 8000

Veera 6000

Shared profit( Residual income for distribution 36290

Ryan 21774

Veera 14516

Total 50290 50290

5.2 Allocation of profit to partners after allowing interest on capital and drawing

Allocation of profit to partners

Particular debit credit

Profit 48690

Interest on drawing 1000

Ryan 600

- Operating Expenses

Heat and light 3240

+prepaid 11000

- Accrued 1020 13220

wages 66220

Vehicle expenses 7450

Insurance expenses 1400

rates 25200

Operating expenses 16400

- Accrued 1600

+ Prepaid 1200 16000

Depreciation on vehicles

cost 75000

-Accumulated depreciation 27000

Amount for depreciation 48000

Depreciation @ 20% 9600

Depreciation on fixtures and fittings

Cost 5000

- Accumulated depreciation 1500

amount for depreciation calculation 3500

Depreciation @ 10 % 350

Total operating expenses 139440

Net profit 48690

Profit and loss Appropriation Account

Particular Debit Credit

net profit as per profit and loss A/c 48690

Interest on drawing

Ryan 1000

Veera 600

Interest on Capital

Ryan 8000

Veera 6000

Shared profit( Residual income for distribution 36290

Ryan 21774

Veera 14516

Total 50290 50290

5.2 Allocation of profit to partners after allowing interest on capital and drawing

Allocation of profit to partners

Particular debit credit

Profit 48690

Interest on drawing 1000

Ryan 600

Veera

Interest on Capital 8000

Ryan 6000

Veera 36290

Shared profit( Residual income

for distribution

21774

Ryan 14516

Veera

Capital Account of Ryan

Date Particular Amount Date Particular Amount

By balance b/d 200000

To balance c/d 150000

Total 200000 200000

Current Account of Ryan

Date Particular Amount Date Particular Amount

To balance b/d 1250

By interest on

capital 8000

To drawings 32000

By profit share of

Ryan 21774

To interest on

Drawings 1000

By balance c/d 4476

Capital Account of Veera

Date Particular Amount Date Particular Amount

By balance b/d 150000

To balance c/d 150000

Total 150000 Total 150000

Current Account of Veera

Date Particular Amount Date Particular Amount

To drawings 24000 By balance b/d 1600

To interest on

drawings 600

By interest on

capital 6000

By profit share of

Veera 14516

By balance c/d 2484

Total 24600 Total 24600

Interest on Capital 8000

Ryan 6000

Veera 36290

Shared profit( Residual income

for distribution

21774

Ryan 14516

Veera

Capital Account of Ryan

Date Particular Amount Date Particular Amount

By balance b/d 200000

To balance c/d 150000

Total 200000 200000

Current Account of Ryan

Date Particular Amount Date Particular Amount

To balance b/d 1250

By interest on

capital 8000

To drawings 32000

By profit share of

Ryan 21774

To interest on

Drawings 1000

By balance c/d 4476

Capital Account of Veera

Date Particular Amount Date Particular Amount

By balance b/d 150000

To balance c/d 150000

Total 150000 Total 150000

Current Account of Veera

Date Particular Amount Date Particular Amount

To drawings 24000 By balance b/d 1600

To interest on

drawings 600

By interest on

capital 6000

By profit share of

Veera 14516

By balance c/d 2484

Total 24600 Total 24600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.