Final Accounts: Detailed Preparation for Sole Traders and Partnerships

VerifiedAdded on 2020/10/22

|15

|4244

|167

Report

AI Summary

This report provides a detailed examination of final accounts, focusing on the specific requirements for sole traders and partnerships. It begins with an introduction to final accounts, emphasizing their role in assessing a business's profitability and financial standing. The report explores the process of preparing final accounts, including the creation of trading accounts, profit and loss statements, and balance sheets. It also addresses the importance of trial balances and the methods for constructing accounts from incomplete records. Furthermore, the report delves into the components of partnership agreements and the key elements of partnership accounts. It includes the preparation of profit and loss appropriation accounts and the determination of profit allocation among partners. Finally, the report covers the closing balances of partners' capital and current accounts and the preparation of a statement of financial position for partnerships. The report also covers the calculation of closing capital, opening capital, and the cash/bank account balance, and explains mark-up and margin calculations. The report also explains the components of final accounts for sole traders and partnerships.

Prepare Final accounts

for sole traders and

Partnership

for sole traders and

Partnership

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Need and process involved in preparation of final accounts...................................................1

1.1 Reason for preparing the trial balance...................................................................................2

1.2 Process and limitation of Preparation of final accounts from a trial balance........................2

1.3 Methods for constructing accounts from incomplete records................................................3

1.4 Reason for imbalances resulting from double entries............................................................3

1.5 Reason for incomplete records...............................................................................................3

TASK 2............................................................................................................................................4

2.1 Closing capital of ABC Ltd. .................................................................................................4

2.2 Calculation of the opening and/or closing cash/bank account balance .................................4

2.3 Preparation of Purchase and Sales ledger Control.................................................................5

2.4 what is mark up and margin...................................................................................................6

TASK 3............................................................................................................................................6

3.1 Describe the components of a set of final account for sole trader.........................................6

3.2 Preparation of Trading and P&L account..............................................................................6

3.3 Preparation of Balance Sheet.................................................................................................7

4.1 Key components of partnership agreement............................................................................8

4.2 Key components of partnership accounts..............................................................................9

TASK 5..........................................................................................................................................10

5.1 Profit and loss account and profit and loss appropriation account......................................10

5.2 Determination of profit and loss to partners........................................................................11

5.3 Capital and current account and .........................................................................................11

TASK 6..........................................................................................................................................11

6.1 Closing balance of each partner from its capital and current account.................................11

6.2 Statement of financial position............................................................................................12

CONCLUSIONS ...........................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Need and process involved in preparation of final accounts...................................................1

1.1 Reason for preparing the trial balance...................................................................................2

1.2 Process and limitation of Preparation of final accounts from a trial balance........................2

1.3 Methods for constructing accounts from incomplete records................................................3

1.4 Reason for imbalances resulting from double entries............................................................3

1.5 Reason for incomplete records...............................................................................................3

TASK 2............................................................................................................................................4

2.1 Closing capital of ABC Ltd. .................................................................................................4

2.2 Calculation of the opening and/or closing cash/bank account balance .................................4

2.3 Preparation of Purchase and Sales ledger Control.................................................................5

2.4 what is mark up and margin...................................................................................................6

TASK 3............................................................................................................................................6

3.1 Describe the components of a set of final account for sole trader.........................................6

3.2 Preparation of Trading and P&L account..............................................................................6

3.3 Preparation of Balance Sheet.................................................................................................7

4.1 Key components of partnership agreement............................................................................8

4.2 Key components of partnership accounts..............................................................................9

TASK 5..........................................................................................................................................10

5.1 Profit and loss account and profit and loss appropriation account......................................10

5.2 Determination of profit and loss to partners........................................................................11

5.3 Capital and current account and .........................................................................................11

TASK 6..........................................................................................................................................11

6.1 Closing balance of each partner from its capital and current account.................................11

6.2 Statement of financial position............................................................................................12

CONCLUSIONS ...........................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Final accounts are those statements which gives insight about profitability and financial

position of business. Sole traders are those individual who own, manage and run an enterprise

wholly single handedly. Partnership is the when two or more than two people comes together for

a common purpose is called partnership. They share their profit and loss on an agreement. If

there is no agreement than partners usually share it equally. There is process for preparing final

accounts which is being explained in this report. The accounting records has been prepared from

given information. As final accounts has been prepared for sole traders. Apart from this the

legislative and accounting requirements for partnership has been explained in this report. Beside

this P&L appropriation account is also being prepared in this report. As statement of financial

position for partnership

TASK 1

1. Need and process involved in preparation of final accounts

Final accounts gives detailed information regarding profitability and financial position of

organisations. These accounts are prepared at the final stage of an accounting cycle. These

accounts are used by the different external and internal parties for various purposes. It has a

complete process which is first transaction are recorded in Journal then it transferred to ledger

and balanced. The final accounts comprises of three statements which are trading accounts, profit

and loss accounts and Balance sheet. These are described as below:

Trading Accounts:

It is the first account which is prepared as a final accounts and prepared to ascertain profit

or loss incurred during an accounting period. There are different items which are recorded in

debit and credit side of this accounts. As on debit side of trading account it includes items as

opening stock, purchase and all direct expenses are recorded on debit side of this account

(McLaughlin, 2018).

Profit and Loss Account:

After preparation of trading account a profit and loss account is prepared which is also

known as an income statement. This statement is prepared to ascertain the profit an loss of the

business. This statement begin with the gross profit or gross loss being transferred from the

trading accounts. The debit side of profit and loss statement records all the indirect expenses like

1

Final accounts are those statements which gives insight about profitability and financial

position of business. Sole traders are those individual who own, manage and run an enterprise

wholly single handedly. Partnership is the when two or more than two people comes together for

a common purpose is called partnership. They share their profit and loss on an agreement. If

there is no agreement than partners usually share it equally. There is process for preparing final

accounts which is being explained in this report. The accounting records has been prepared from

given information. As final accounts has been prepared for sole traders. Apart from this the

legislative and accounting requirements for partnership has been explained in this report. Beside

this P&L appropriation account is also being prepared in this report. As statement of financial

position for partnership

TASK 1

1. Need and process involved in preparation of final accounts

Final accounts gives detailed information regarding profitability and financial position of

organisations. These accounts are prepared at the final stage of an accounting cycle. These

accounts are used by the different external and internal parties for various purposes. It has a

complete process which is first transaction are recorded in Journal then it transferred to ledger

and balanced. The final accounts comprises of three statements which are trading accounts, profit

and loss accounts and Balance sheet. These are described as below:

Trading Accounts:

It is the first account which is prepared as a final accounts and prepared to ascertain profit

or loss incurred during an accounting period. There are different items which are recorded in

debit and credit side of this accounts. As on debit side of trading account it includes items as

opening stock, purchase and all direct expenses are recorded on debit side of this account

(McLaughlin, 2018).

Profit and Loss Account:

After preparation of trading account a profit and loss account is prepared which is also

known as an income statement. This statement is prepared to ascertain the profit an loss of the

business. This statement begin with the gross profit or gross loss being transferred from the

trading accounts. The debit side of profit and loss statement records all the indirect expenses like

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

salary, rent and stationery etc. and credit side records all indirect incomes of business like

dividend received on shares and profit on sale of assets etc.

Balance Sheet:

Balance sheet is last statement of final accounts which is prepared to ascertain the

financial position of firm. It consist of capital, assets and liabilities of a business. As it is a

statement so there is no debit and credit side. On left side all liabilities are recorded and on right

side all assets are recorded.

1.1 Reason for preparing the trial balance

Trial balance is list of all the general ledger accounts which contained in ledger of

business. As all the ledger accounts are being closed on ending of every financial year so there

balance can be matched and they can be re open for upcoming financial year. The basic reason

for making trial balance is company tries to detect any mathematical errors which have occurred

in double entry accounting system. If the total of debit is equal to credit than trial balance is

considered to be balanced. As there should not be any mathematical error in the ledgers (May,

2013).

1.2 Process and limitation of Preparation of final accounts from a trial balance

There are following points which should be noted while preparing final accounts, these

are as follows:

One should prepare the trial balance first and if there is a difference between the Trial

Balance then it will be shown in Suspense A/c and shown in Balance Sheet.

The items which are appeared at outside the trial balances known as adjustment and have

to be shown at two places.

As Debit side item of trial balance will be appear at debit side of trading or p&l or on the

Assets side of Balance sheet.

All accounting which are related with the Purchases, Sales, Purchase return and sales

returns shown in trading account. And all direct expenses will appear at debit side of

trading account. As remaining expenses will appear at Profit and loss account.

As if trial balance is not given in question then items like discounts, commission and rent

will be treated as expense.

The limitation of this is that it it does not point out all types of errors of business. It

means that trial balance does not assure the 100% accuracy. As errors like posting entry in

2

dividend received on shares and profit on sale of assets etc.

Balance Sheet:

Balance sheet is last statement of final accounts which is prepared to ascertain the

financial position of firm. It consist of capital, assets and liabilities of a business. As it is a

statement so there is no debit and credit side. On left side all liabilities are recorded and on right

side all assets are recorded.

1.1 Reason for preparing the trial balance

Trial balance is list of all the general ledger accounts which contained in ledger of

business. As all the ledger accounts are being closed on ending of every financial year so there

balance can be matched and they can be re open for upcoming financial year. The basic reason

for making trial balance is company tries to detect any mathematical errors which have occurred

in double entry accounting system. If the total of debit is equal to credit than trial balance is

considered to be balanced. As there should not be any mathematical error in the ledgers (May,

2013).

1.2 Process and limitation of Preparation of final accounts from a trial balance

There are following points which should be noted while preparing final accounts, these

are as follows:

One should prepare the trial balance first and if there is a difference between the Trial

Balance then it will be shown in Suspense A/c and shown in Balance Sheet.

The items which are appeared at outside the trial balances known as adjustment and have

to be shown at two places.

As Debit side item of trial balance will be appear at debit side of trading or p&l or on the

Assets side of Balance sheet.

All accounting which are related with the Purchases, Sales, Purchase return and sales

returns shown in trading account. And all direct expenses will appear at debit side of

trading account. As remaining expenses will appear at Profit and loss account.

As if trial balance is not given in question then items like discounts, commission and rent

will be treated as expense.

The limitation of this is that it it does not point out all types of errors of business. It

means that trial balance does not assure the 100% accuracy. As errors like posting entry in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

correct side but wrong account and wrong amount entered in day book all these kinds of errors

are not shown in trial balance (Janda, Rausser and Strielkowski, 2013).

1.3 Methods for constructing accounts from incomplete records

Accounting records which are not kept according to double entry system are known as

incomplete records. There are various methods for preparing accounts from incomplete records

these are as follows:

The accounting equation:

If company have detail of assets and liabilities then it can use the accounting equation to

work out the value of capital. Assets minus liabilities equal to capital.

Control Accounts:

If company have missing balance on accounts then one can use control accounts. It

includes the control accounts like bank control account with all details. As account balance will

not balance as its missing information and balancing figure will be assumed to be missing

balance.

Markup Method:

With the help of markup margin percentage and have figure of sales then one can know

cost of goods sold (Hoffmann and Zuelch, 2014).

1.4 Reason for imbalances resulting from double entries

As there can be mismatch in amount which arises from the mistake in double entries. The

error can be due to wrong amount entered in either debit side or credit side. And error can be

arisen due to omission of any entry. As due to errors of principal like an item is posted to the

correct side of wrong type of account. Due to posting error like one record is not posted at all or

record is incorrectly posted to another account. All these can be reason for imbalances in double

entries.

1.5 Reason for incomplete records

Incomplete records refers to those who maintain the accounting records on single entry

system. Basically small firms like grocery shops, general stores and food joints maintains the

records on single entry system. The reason for inconsistency and insufficient data is lack of

knowledge of accounting principles. Basically one reason can be that maintaining incomplete

records consume less time also. People consider it as more convenient to maintain records as per

3

are not shown in trial balance (Janda, Rausser and Strielkowski, 2013).

1.3 Methods for constructing accounts from incomplete records

Accounting records which are not kept according to double entry system are known as

incomplete records. There are various methods for preparing accounts from incomplete records

these are as follows:

The accounting equation:

If company have detail of assets and liabilities then it can use the accounting equation to

work out the value of capital. Assets minus liabilities equal to capital.

Control Accounts:

If company have missing balance on accounts then one can use control accounts. It

includes the control accounts like bank control account with all details. As account balance will

not balance as its missing information and balancing figure will be assumed to be missing

balance.

Markup Method:

With the help of markup margin percentage and have figure of sales then one can know

cost of goods sold (Hoffmann and Zuelch, 2014).

1.4 Reason for imbalances resulting from double entries

As there can be mismatch in amount which arises from the mistake in double entries. The

error can be due to wrong amount entered in either debit side or credit side. And error can be

arisen due to omission of any entry. As due to errors of principal like an item is posted to the

correct side of wrong type of account. Due to posting error like one record is not posted at all or

record is incorrectly posted to another account. All these can be reason for imbalances in double

entries.

1.5 Reason for incomplete records

Incomplete records refers to those who maintain the accounting records on single entry

system. Basically small firms like grocery shops, general stores and food joints maintains the

records on single entry system. The reason for inconsistency and insufficient data is lack of

knowledge of accounting principles. Basically one reason can be that maintaining incomplete

records consume less time also. People consider it as more convenient to maintain records as per

3

single entry system. As people does not maintain data on regular basis which leads to

inconsistencies of data. So these are the some reason for incomplete records which arises from

insufficient and inconsistencies (Gupta, 2013).

TASK 2

2.1 Closing capital of ABC Ltd.

Closing capital:

Closing capital is amount which is put with capital after that added together.

Opening capital - GBP 1000

Drawings - GBP 600

Net profit – GBP 2600

Closing capital = Opening capital + profit – Drawings

Closing capital = 1000+2600-600

Closing capital = GBP 3000

II) Calculation of opening capital

Opening capital is adjusted balance which is presented toward the begining of a

bookkeeping period.

Profit – GBP 360

Closing capital – GBP 4200

Drawing – GBP 800

Opening capital: 4200+360-800

Opening capital = GBP 3760

2.2 Calculation of the opening and/or closing cash/bank account balance

Double Column Cash Book

Dr.

(Receipt)

Cr.

(Payment)

Date Description

P

R Cash Bank Date Description

P

R

Cash Bank

1 balance b/d 10940 6 Rent paid 135

4

inconsistencies of data. So these are the some reason for incomplete records which arises from

insufficient and inconsistencies (Gupta, 2013).

TASK 2

2.1 Closing capital of ABC Ltd.

Closing capital:

Closing capital is amount which is put with capital after that added together.

Opening capital - GBP 1000

Drawings - GBP 600

Net profit – GBP 2600

Closing capital = Opening capital + profit – Drawings

Closing capital = 1000+2600-600

Closing capital = GBP 3000

II) Calculation of opening capital

Opening capital is adjusted balance which is presented toward the begining of a

bookkeeping period.

Profit – GBP 360

Closing capital – GBP 4200

Drawing – GBP 800

Opening capital: 4200+360-800

Opening capital = GBP 3760

2.2 Calculation of the opening and/or closing cash/bank account balance

Double Column Cash Book

Dr.

(Receipt)

Cr.

(Payment)

Date Description

P

R Cash Bank Date Description

P

R

Cash Bank

1 balance b/d 10940 6 Rent paid 135

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2 M.Boon 315

4 sales 802

7 cash c 50 7 bank c 50

15 sales 490 23 S. Wills 277

29 Bank c 120 29 Cash c 120

30 wages 518

balance c/d 319 11298

Total 972 11745 972 11745

01/10/18 balance b/d 319 11298

2.3 Preparation of Purchase and Sales ledger Control

Purchase ledger control:

This account gives the information about how much amount is business owe to its

supplier. All the transaction which are related with supplier are recorded in this ledger account

(Gilbert and Pfuderer, 2014).

Sales ledger control:

Sales ledger control shows the amount owed to a organisation by its customers within a

given time period. It is the total of accounts receivables. It is a part of balance sheet and current

assets also.

Purchase ledger control

Particulars Amount Particulars Amount

Discount received 1310 Balance b/d 16400

Return outward 2330 Credit purchase 114800

Paid to creditors 109040

balance c/d 18520

131200 131200

Sales ledger control

Particulars Amount Particulars Amount

Balance B/d 23220 Cash sales 1490

5

4 sales 802

7 cash c 50 7 bank c 50

15 sales 490 23 S. Wills 277

29 Bank c 120 29 Cash c 120

30 wages 518

balance c/d 319 11298

Total 972 11745 972 11745

01/10/18 balance b/d 319 11298

2.3 Preparation of Purchase and Sales ledger Control

Purchase ledger control:

This account gives the information about how much amount is business owe to its

supplier. All the transaction which are related with supplier are recorded in this ledger account

(Gilbert and Pfuderer, 2014).

Sales ledger control:

Sales ledger control shows the amount owed to a organisation by its customers within a

given time period. It is the total of accounts receivables. It is a part of balance sheet and current

assets also.

Purchase ledger control

Particulars Amount Particulars Amount

Discount received 1310 Balance b/d 16400

Return outward 2330 Credit purchase 114800

Paid to creditors 109040

balance c/d 18520

131200 131200

Sales ledger control

Particulars Amount Particulars Amount

Balance B/d 23220 Cash sales 1490

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Credit sales 162540 Discount allowed 3160

Sales return 8150

bad debt written off 4770

Received form debtors 146610

Balance c/d (b.f.) 21580

185760 185760

2.4 what is mark up and margin

Mark up:

Mark up method is helpful in the calculation of sales and cost of goods sold. As if mark

up margin is given and sales is given then one can calculate cost of goods sold easily. Mark up is

basically difference between the selling price of goods and its cost (Fooks and Gilmore, 2014).

Margin:

Margin is the money which left after deducting cost of goods sold from net sales.

TASK 3

3.1 Describe the components of a set of final account for sole trader

Sole traders are people who runs their business on their own, they run shops, factories,

farms and other local franchises etc. As these business are generally small because owners

usually invest small or limited amount in their businesses. People set up as a sole trader, as some

needs independence and they do not want to any other person in decision making process. As

one can easily register its business as sole trader by using owner's name or any other trading

name. The final accounts of sole trader includes trading and profit and loss account which gives

detail about profit or loss of business. And includes Balance Sheet which includes assets and

liabilities of business. As final accounts can be produced once a year in order to give information

to owner on how the business is progressing. The trading and profit and loss account shows the

income like rent received and expenditure like rent. The difference between income and expense

is net profit or net loss of the business (Christensen and Feltham, 2012).

3.2 Preparation of Trading and P&L account

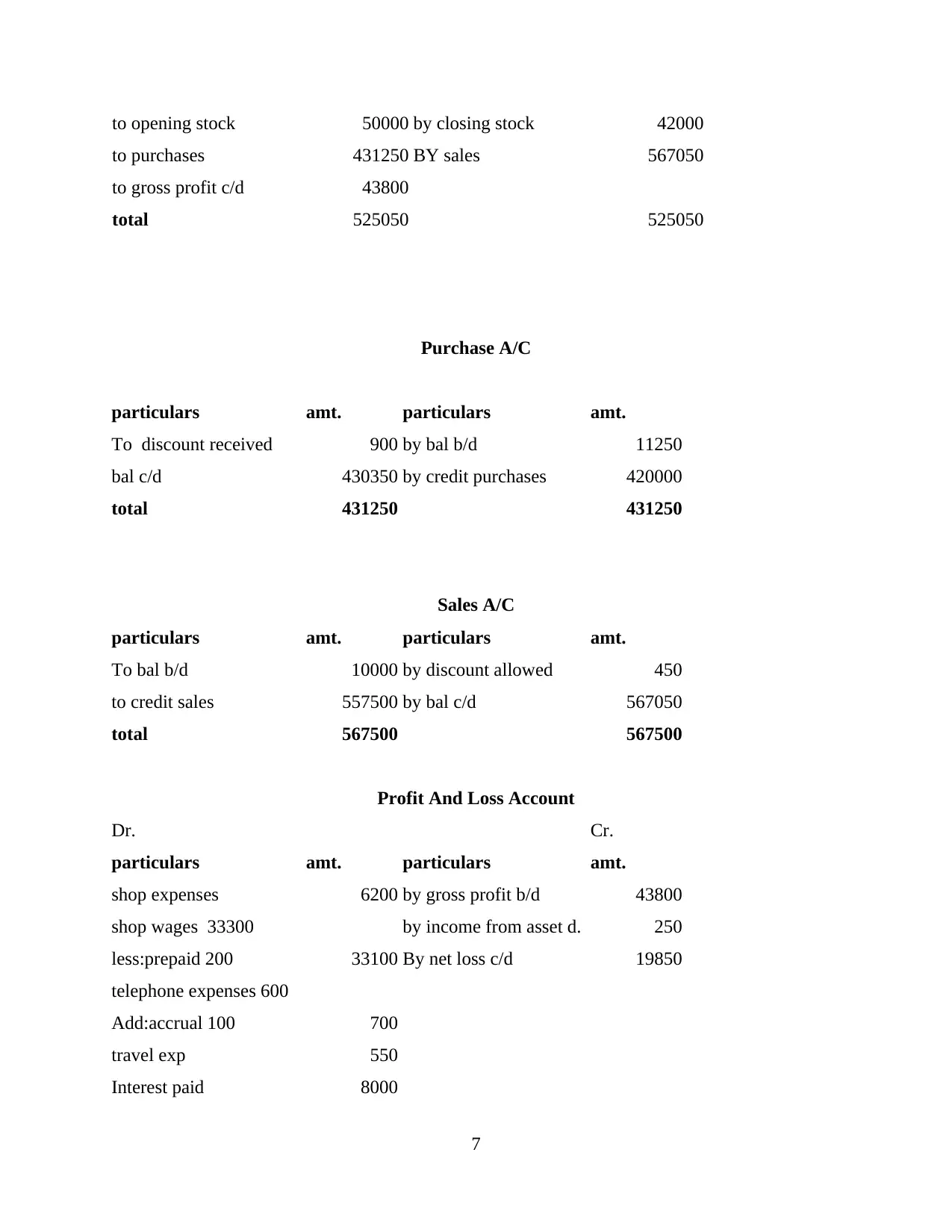

Trading A/C

particulars amt. particulars amt.

6

Sales return 8150

bad debt written off 4770

Received form debtors 146610

Balance c/d (b.f.) 21580

185760 185760

2.4 what is mark up and margin

Mark up:

Mark up method is helpful in the calculation of sales and cost of goods sold. As if mark

up margin is given and sales is given then one can calculate cost of goods sold easily. Mark up is

basically difference between the selling price of goods and its cost (Fooks and Gilmore, 2014).

Margin:

Margin is the money which left after deducting cost of goods sold from net sales.

TASK 3

3.1 Describe the components of a set of final account for sole trader

Sole traders are people who runs their business on their own, they run shops, factories,

farms and other local franchises etc. As these business are generally small because owners

usually invest small or limited amount in their businesses. People set up as a sole trader, as some

needs independence and they do not want to any other person in decision making process. As

one can easily register its business as sole trader by using owner's name or any other trading

name. The final accounts of sole trader includes trading and profit and loss account which gives

detail about profit or loss of business. And includes Balance Sheet which includes assets and

liabilities of business. As final accounts can be produced once a year in order to give information

to owner on how the business is progressing. The trading and profit and loss account shows the

income like rent received and expenditure like rent. The difference between income and expense

is net profit or net loss of the business (Christensen and Feltham, 2012).

3.2 Preparation of Trading and P&L account

Trading A/C

particulars amt. particulars amt.

6

to opening stock 50000 by closing stock 42000

to purchases 431250 BY sales 567050

to gross profit c/d 43800

total 525050 525050

Purchase A/C

particulars amt. particulars amt.

To discount received 900 by bal b/d 11250

bal c/d 430350 by credit purchases 420000

total 431250 431250

Sales A/C

particulars amt. particulars amt.

To bal b/d 10000 by discount allowed 450

to credit sales 557500 by bal c/d 567050

total 567500 567500

Profit And Loss Account

Dr. Cr.

particulars amt. particulars amt.

shop expenses 6200 by gross profit b/d 43800

shop wages 33300 by income from asset d. 250

less:prepaid 200 33100 By net loss c/d 19850

telephone expenses 600

Add:accrual 100 700

travel exp 550

Interest paid 8000

7

to purchases 431250 BY sales 567050

to gross profit c/d 43800

total 525050 525050

Purchase A/C

particulars amt. particulars amt.

To discount received 900 by bal b/d 11250

bal c/d 430350 by credit purchases 420000

total 431250 431250

Sales A/C

particulars amt. particulars amt.

To bal b/d 10000 by discount allowed 450

to credit sales 557500 by bal c/d 567050

total 567500 567500

Profit And Loss Account

Dr. Cr.

particulars amt. particulars amt.

shop expenses 6200 by gross profit b/d 43800

shop wages 33300 by income from asset d. 250

less:prepaid 200 33100 By net loss c/d 19850

telephone expenses 600

Add:accrual 100 700

travel exp 550

Interest paid 8000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Dep:pre:5000

+fitings 6400 11400

bad debts: 500

add: bad debt allow 200 700

Tax exp. 3250

total 63900 63900

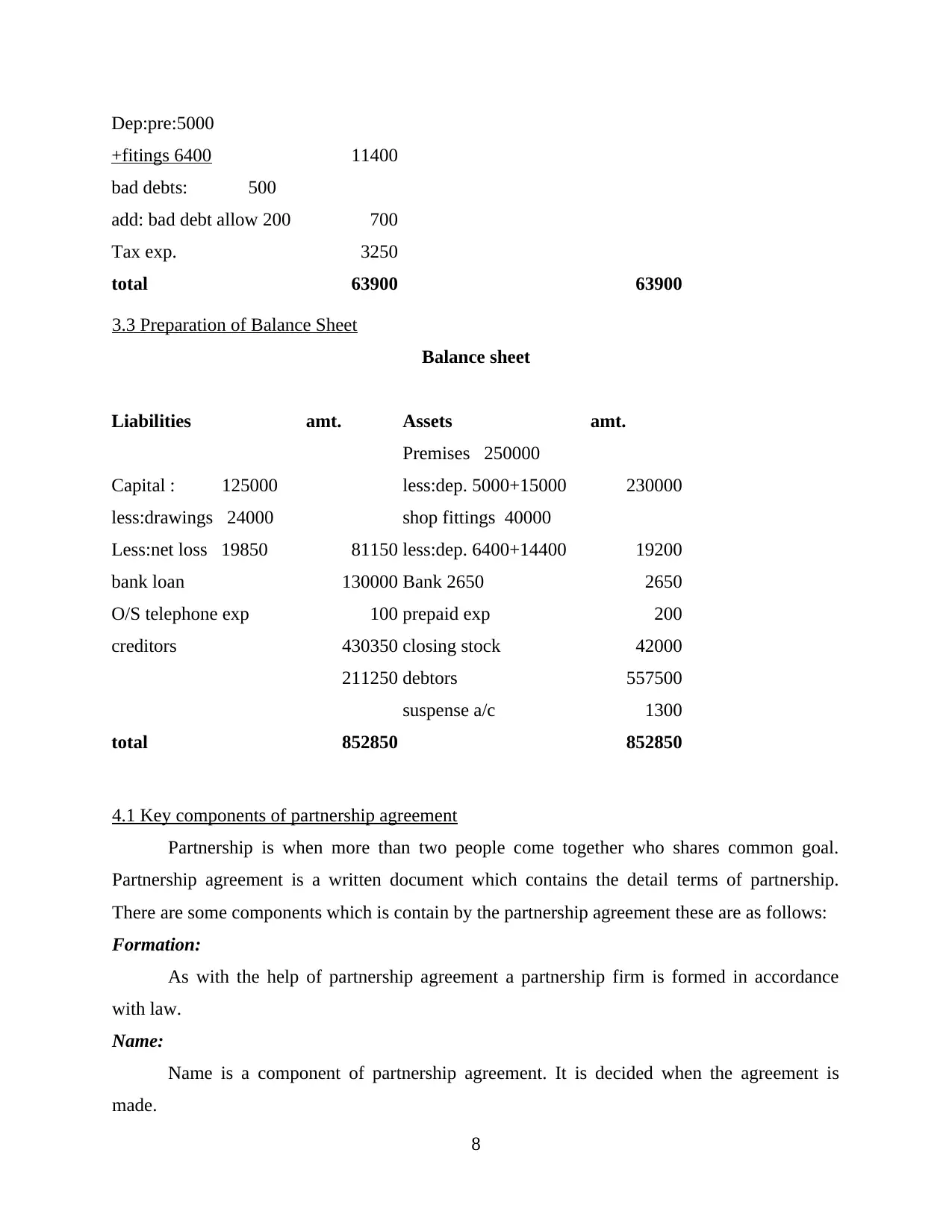

3.3 Preparation of Balance Sheet

Balance sheet

Liabilities amt. Assets amt.

Premises 250000

Capital : 125000 less:dep. 5000+15000 230000

less:drawings 24000 shop fittings 40000

Less:net loss 19850 81150 less:dep. 6400+14400 19200

bank loan 130000 Bank 2650 2650

O/S telephone exp 100 prepaid exp 200

creditors 430350 closing stock 42000

211250 debtors 557500

suspense a/c 1300

total 852850 852850

4.1 Key components of partnership agreement

Partnership is when more than two people come together who shares common goal.

Partnership agreement is a written document which contains the detail terms of partnership.

There are some components which is contain by the partnership agreement these are as follows:

Formation:

As with the help of partnership agreement a partnership firm is formed in accordance

with law.

Name:

Name is a component of partnership agreement. It is decided when the agreement is

made.

8

+fitings 6400 11400

bad debts: 500

add: bad debt allow 200 700

Tax exp. 3250

total 63900 63900

3.3 Preparation of Balance Sheet

Balance sheet

Liabilities amt. Assets amt.

Premises 250000

Capital : 125000 less:dep. 5000+15000 230000

less:drawings 24000 shop fittings 40000

Less:net loss 19850 81150 less:dep. 6400+14400 19200

bank loan 130000 Bank 2650 2650

O/S telephone exp 100 prepaid exp 200

creditors 430350 closing stock 42000

211250 debtors 557500

suspense a/c 1300

total 852850 852850

4.1 Key components of partnership agreement

Partnership is when more than two people come together who shares common goal.

Partnership agreement is a written document which contains the detail terms of partnership.

There are some components which is contain by the partnership agreement these are as follows:

Formation:

As with the help of partnership agreement a partnership firm is formed in accordance

with law.

Name:

Name is a component of partnership agreement. It is decided when the agreement is

made.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purpose:

The purpose define aim of business. As purpose of partnership should be define in

agreement and it should be legal also (Chambersed., 2014).

Term:

The term refers to the definitive date of starting time of partnership and its continuation is

provided in agreement.

Place of business:

The place of business is location where office of partnership firm will be located.

Capital Contributors:

Capital is amount of money which is invested by partners in order to start their business.

It can be in cash or any property which partners can invest while starting business.

Allocation of profit and loss

It is very important component of partnership agreement. The profit and loss sharing ratio

is mentioned in this agreement.

Resolve of conflicts:

The conflicts can be arisen in partnership firm so there should be a clause in agreement in

order to resolving conflicts so partners does not need to head to court (Schaltegger and Zvezdov,

2013).

Partnership Dissolution:

There are various causes for dissolution of partnership firm and one is if its in agreement.

As in this clause partners indicate how assets are distributed between partners in case of

dissolution.

4.2 Key components of partnership accounts

There are different components of partnership accounts, these are as follows:

Statement of profit and loss:

Profit and loss or income statement is prepared for ascertaining the profit and loss of

partnership firm. As debit side of account will contain the indirect expenses of business and

credit side contains the indirect income.

Partnership appropriation account:

It is used for distribution and allocation of net profits among partners, reserves and

dividend. It is prepared by mainly by partnership firms. It have carry forward balance from

9

The purpose define aim of business. As purpose of partnership should be define in

agreement and it should be legal also (Chambersed., 2014).

Term:

The term refers to the definitive date of starting time of partnership and its continuation is

provided in agreement.

Place of business:

The place of business is location where office of partnership firm will be located.

Capital Contributors:

Capital is amount of money which is invested by partners in order to start their business.

It can be in cash or any property which partners can invest while starting business.

Allocation of profit and loss

It is very important component of partnership agreement. The profit and loss sharing ratio

is mentioned in this agreement.

Resolve of conflicts:

The conflicts can be arisen in partnership firm so there should be a clause in agreement in

order to resolving conflicts so partners does not need to head to court (Schaltegger and Zvezdov,

2013).

Partnership Dissolution:

There are various causes for dissolution of partnership firm and one is if its in agreement.

As in this clause partners indicate how assets are distributed between partners in case of

dissolution.

4.2 Key components of partnership accounts

There are different components of partnership accounts, these are as follows:

Statement of profit and loss:

Profit and loss or income statement is prepared for ascertaining the profit and loss of

partnership firm. As debit side of account will contain the indirect expenses of business and

credit side contains the indirect income.

Partnership appropriation account:

It is used for distribution and allocation of net profits among partners, reserves and

dividend. It is prepared by mainly by partnership firms. It have carry forward balance from

9

previous accounting period. This account is prepared after preparation profit and loss account. It

does not follows the matching principle of accounts (Barrow, Barrow and Brown, 2012).

Goodwill:

Goodwill is an intangible asset of business. It represents non physical items that add to a

company's value but can not be find easily. It is the amount by which fair value of net assets

exceeds book value of net assets. It arises due to factors like location, customer base and market

position of business.

Partner's Current account:

This is prepared when the capital is fixed in firm. It includes transaction like interest on

drawings, salary and interest on capital. The balance of this account fluctuate every year. As

balance of this account can be both debit and credit.

Partner's capital account:

The partners capital account is maintained in two ways which are as follows:

Fixed Capital Account:

Under this method the amount invested by partners keep same until additional capital is

brought in business. As only capital introduced or withdrawn by partners is recorded in this

account (Bain and Band, 2016).

Fluctuating Capital account:

In this only capital account is maintained and all entries which are related with the

drawing, interest on drawing, interest on capital, salary, commission etc. are recorded in capital

accounts.

Statement of financial position:

This shows the actual position of business. As Balance sheet is made at the end of

accounting year.

TASK 5

5.1 Profit and loss account and profit and loss appropriation account

Profit and loss a/c

particulars amt. particulars amt.

10

does not follows the matching principle of accounts (Barrow, Barrow and Brown, 2012).

Goodwill:

Goodwill is an intangible asset of business. It represents non physical items that add to a

company's value but can not be find easily. It is the amount by which fair value of net assets

exceeds book value of net assets. It arises due to factors like location, customer base and market

position of business.

Partner's Current account:

This is prepared when the capital is fixed in firm. It includes transaction like interest on

drawings, salary and interest on capital. The balance of this account fluctuate every year. As

balance of this account can be both debit and credit.

Partner's capital account:

The partners capital account is maintained in two ways which are as follows:

Fixed Capital Account:

Under this method the amount invested by partners keep same until additional capital is

brought in business. As only capital introduced or withdrawn by partners is recorded in this

account (Bain and Band, 2016).

Fluctuating Capital account:

In this only capital account is maintained and all entries which are related with the

drawing, interest on drawing, interest on capital, salary, commission etc. are recorded in capital

accounts.

Statement of financial position:

This shows the actual position of business. As Balance sheet is made at the end of

accounting year.

TASK 5

5.1 Profit and loss account and profit and loss appropriation account

Profit and loss a/c

particulars amt. particulars amt.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.