Comprehensive Report: Final Accounts for Sole Traders and Partnerships

VerifiedAdded on 2021/01/02

|21

|3946

|226

Report

AI Summary

This report provides a comprehensive overview of final accounts, focusing on both sole traders and partnerships. It begins by explaining the process of closing accounts and producing a trial balance, discussing the reasons for closing accounts and the importance of the trial balance in ensuring the accuracy of financial entries. The report then addresses the preparation of final accounts from incomplete records, highlighting methods like the statement of affairs and margin and markup methods. It also delves into the causes of imbalances arising from incorrect double entries and incomplete records. The report then details the components of final accounts for sole traders, including the profit and loss account and the statement of financial position. For partnerships, the report explores partnership agreements, the components of partnership accounts, the preparation of profit and loss appropriation accounts, and the allocation of profits. It also covers the preparation of capital and current accounts and the final statement of financial position for partnerships. The report concludes by summarizing key components and providing references for further study.

Prepare Final

Accounts of Sole

Traders and

Partnership

Accounts of Sole

Traders and

Partnership

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. 1 Closing off a/c and producing a trial balance.......................................................................1

1. 2 Process and limitations of preparing a set of final a/c..........................................................2

1. 3 Constructing accounts from incomplete records...................................................................2

1. 4 Reasons for imbalances resulting from incorrect double entries..........................................3

1. 5 Reasons for incomplete records arising from insufficient data ...........................................3

TASK 2............................................................................................................................................4

2 . 1 Closing and opening capital using the incomplete information..........................................4

2 . 2 Opening and closing cash/ bank a/c balance........................................................................5

2 . 3 Sales and purchase ledger control accounts.........................................................................6

TASK 3............................................................................................................................................7

3 . 1 Components of a set of final accounts for a sole trader.......................................................7

3. 2 Formulation of statement of P&L a/c...................................................................................8

3. 3 Statement of financial position............................................................................................9

TASK 4..........................................................................................................................................11

4. 1 Key components of a partnership agreement......................................................................11

4 . 2 Components of partnership accounts ................................................................................12

TASK 5..........................................................................................................................................12

5.1 Preparation of statement of P&L appropriation a/c.............................................................12

5 . 2 Allocation of profits to partners ........................................................................................14

5 . 3 Preparation of capital and current accounts.......................................................................14

TASK 6..........................................................................................................................................15

6. 1 Closing balances on each partner's capital and current accounts........................................15

6.2 Preparation of statement of financial position.....................................................................16

CONCLUSION .............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. 1 Closing off a/c and producing a trial balance.......................................................................1

1. 2 Process and limitations of preparing a set of final a/c..........................................................2

1. 3 Constructing accounts from incomplete records...................................................................2

1. 4 Reasons for imbalances resulting from incorrect double entries..........................................3

1. 5 Reasons for incomplete records arising from insufficient data ...........................................3

TASK 2............................................................................................................................................4

2 . 1 Closing and opening capital using the incomplete information..........................................4

2 . 2 Opening and closing cash/ bank a/c balance........................................................................5

2 . 3 Sales and purchase ledger control accounts.........................................................................6

TASK 3............................................................................................................................................7

3 . 1 Components of a set of final accounts for a sole trader.......................................................7

3. 2 Formulation of statement of P&L a/c...................................................................................8

3. 3 Statement of financial position............................................................................................9

TASK 4..........................................................................................................................................11

4. 1 Key components of a partnership agreement......................................................................11

4 . 2 Components of partnership accounts ................................................................................12

TASK 5..........................................................................................................................................12

5.1 Preparation of statement of P&L appropriation a/c.............................................................12

5 . 2 Allocation of profits to partners ........................................................................................14

5 . 3 Preparation of capital and current accounts.......................................................................14

TASK 6..........................................................................................................................................15

6. 1 Closing balances on each partner's capital and current accounts........................................15

6.2 Preparation of statement of financial position.....................................................................16

CONCLUSION .............................................................................................................................17

REFERENCES..............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Final accounts are prepared by the an individuals and business entities and it provide help

to analyse the financial position of corporation. It is prepared at the last stage of an accounting

cycle and company can know that it is earning profit or not at the end of financial year. . All

profits are acquired by owner of the sole trader and in the partnership firms it is distributed

among the partners as per the partnership deed. The present report discuss about various topics :

reasons for closing off accounts and producing a trail balance, methods of constructing accounts

from incomplete records, prepare sales and purchase ledger control accounts, final accounts for

sole traders, understand the legislative and accounting requirements for partnership. Apart from

this, report discuss about to prepare a statement of profit and loss account and statement of

financial position related to partnership.

TASK 1

1. 1 Closing off a/c and producing a trial balance

Trail balance is prepare by an organisation to check mathematical accuracy while

considering double entry system of accounting. It is generally prepared at the end of reporting

period. It is the process that helps organisation to check whether the particular account is

showing as asset or liability for the business. The main purpose to prepare trial balance is to

know that entries are made appropriate. Reasons to closing off account are as:

All of them are closed because balance has transferred to permanent account from the

temporary account.

To know that business entity is generating profits or losses for a particular period of time,

it can be reason to closing off account.

This also helps the sole traders to check and calculate the transactional summary for the

whole year (Storey and et. al., 2016).

As the entries are transferred to trial balance, it helps in achieving the target of producing

income statement and balance sheet of the company.

To closing entries, it is required.

1

Final accounts are prepared by the an individuals and business entities and it provide help

to analyse the financial position of corporation. It is prepared at the last stage of an accounting

cycle and company can know that it is earning profit or not at the end of financial year. . All

profits are acquired by owner of the sole trader and in the partnership firms it is distributed

among the partners as per the partnership deed. The present report discuss about various topics :

reasons for closing off accounts and producing a trail balance, methods of constructing accounts

from incomplete records, prepare sales and purchase ledger control accounts, final accounts for

sole traders, understand the legislative and accounting requirements for partnership. Apart from

this, report discuss about to prepare a statement of profit and loss account and statement of

financial position related to partnership.

TASK 1

1. 1 Closing off a/c and producing a trial balance

Trail balance is prepare by an organisation to check mathematical accuracy while

considering double entry system of accounting. It is generally prepared at the end of reporting

period. It is the process that helps organisation to check whether the particular account is

showing as asset or liability for the business. The main purpose to prepare trial balance is to

know that entries are made appropriate. Reasons to closing off account are as:

All of them are closed because balance has transferred to permanent account from the

temporary account.

To know that business entity is generating profits or losses for a particular period of time,

it can be reason to closing off account.

This also helps the sole traders to check and calculate the transactional summary for the

whole year (Storey and et. al., 2016).

As the entries are transferred to trial balance, it helps in achieving the target of producing

income statement and balance sheet of the company.

To closing entries, it is required.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. 2 Process and limitations of preparing a set of final a/c

Final accounts are prepared at the end of financial year and it provide help to know the

financial position of an organisation. As a result, corporation can take its important decisions

such as: future expansions and strategies which is helpful for company to get success and

growth. Trail balance is a bookkeeping worksheet which contains the balances of all ledgers are

compiled into credit and debit account. Process of preparing final account are as follows:

Analyse the list of items of trial balance and make necessary adjustments, record all

expenses in debit side of Trading- P&L Account and record the incomes in credit side of

Trading- P&L Account.

Profits are distributed to parters in the case of partnership firm, after that capital and

current accounts are prepared.

In the balance sheet all items related to assets and liabilities are recorded as per its nature.

At the end profits and losses are calculated and transferred to balance sheet (Whiteley,

2017).

Limitations of trial balance while preparing final accounts

If there is any omission of an entry in the day book, then trial balance will not be able to

detect it and final account will be misstated.

Entry posted with wrong account will not be detected by trial balance and therefore final

accounts will be prepared with wrong account only.

Compensatory error will not affect the trial balance but affect the final accounts with

errors and omission.

So there are various limitations of preparing final accounts and it provide false

information so it is necessary to make it as per the desired manner so that errors can be

minimize.

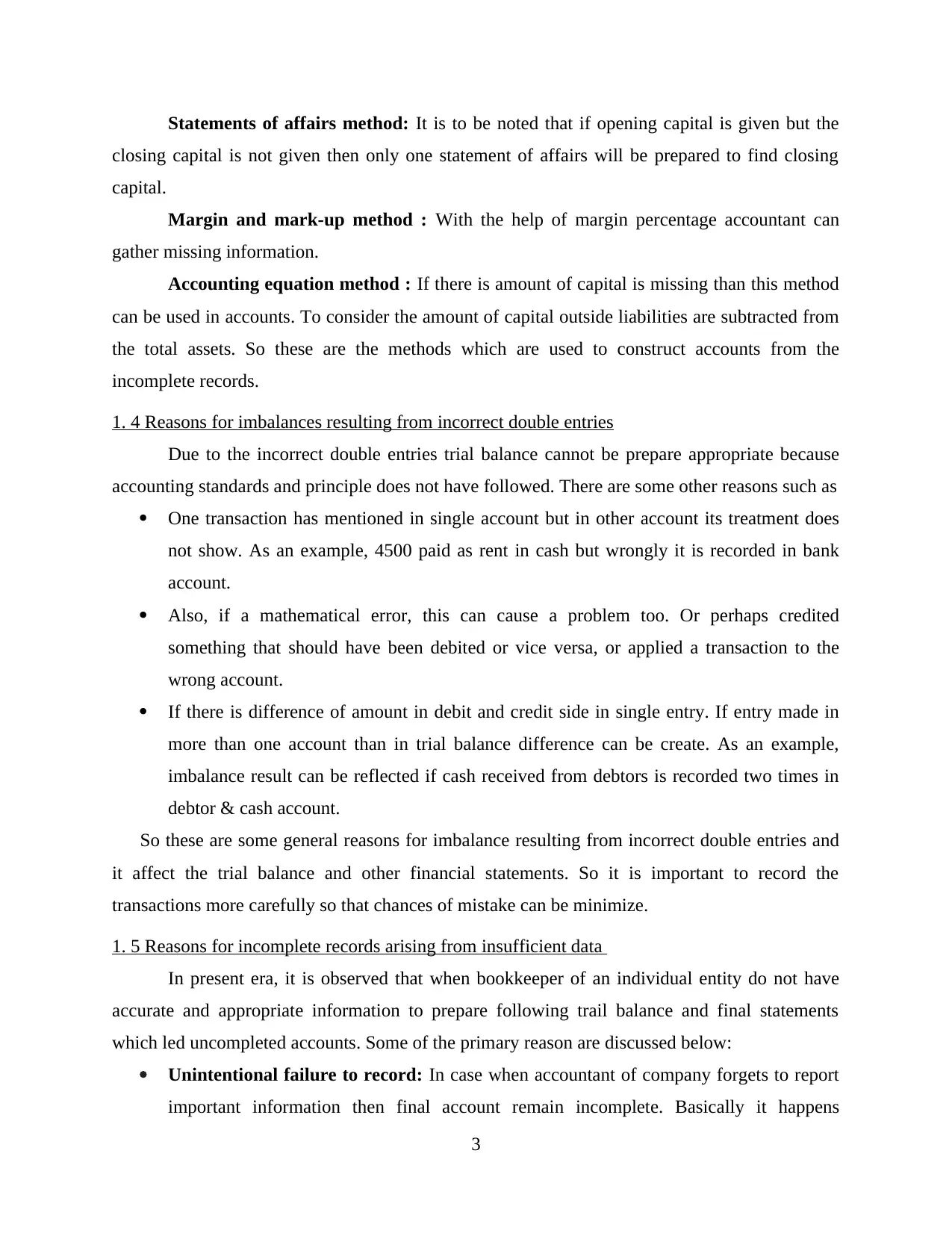

1. 3 Constructing accounts from incomplete records

incomplete records are those which give false information to the reader as a result

financial statements can not be prepare in effective manner. So it is responsibility of an

accountant to record all financial transactions carefully so that chances of errors can be

minimize. There are various methods that helps in preparation of accounts through incomplete

records which includes statement of affairs methods and margin and markup method.

2

Final accounts are prepared at the end of financial year and it provide help to know the

financial position of an organisation. As a result, corporation can take its important decisions

such as: future expansions and strategies which is helpful for company to get success and

growth. Trail balance is a bookkeeping worksheet which contains the balances of all ledgers are

compiled into credit and debit account. Process of preparing final account are as follows:

Analyse the list of items of trial balance and make necessary adjustments, record all

expenses in debit side of Trading- P&L Account and record the incomes in credit side of

Trading- P&L Account.

Profits are distributed to parters in the case of partnership firm, after that capital and

current accounts are prepared.

In the balance sheet all items related to assets and liabilities are recorded as per its nature.

At the end profits and losses are calculated and transferred to balance sheet (Whiteley,

2017).

Limitations of trial balance while preparing final accounts

If there is any omission of an entry in the day book, then trial balance will not be able to

detect it and final account will be misstated.

Entry posted with wrong account will not be detected by trial balance and therefore final

accounts will be prepared with wrong account only.

Compensatory error will not affect the trial balance but affect the final accounts with

errors and omission.

So there are various limitations of preparing final accounts and it provide false

information so it is necessary to make it as per the desired manner so that errors can be

minimize.

1. 3 Constructing accounts from incomplete records

incomplete records are those which give false information to the reader as a result

financial statements can not be prepare in effective manner. So it is responsibility of an

accountant to record all financial transactions carefully so that chances of errors can be

minimize. There are various methods that helps in preparation of accounts through incomplete

records which includes statement of affairs methods and margin and markup method.

2

Statements of affairs method: It is to be noted that if opening capital is given but the

closing capital is not given then only one statement of affairs will be prepared to find closing

capital.

Margin and mark-up method : With the help of margin percentage accountant can

gather missing information.

Accounting equation method : If there is amount of capital is missing than this method

can be used in accounts. To consider the amount of capital outside liabilities are subtracted from

the total assets. So these are the methods which are used to construct accounts from the

incomplete records.

1. 4 Reasons for imbalances resulting from incorrect double entries

Due to the incorrect double entries trial balance cannot be prepare appropriate because

accounting standards and principle does not have followed. There are some other reasons such as

One transaction has mentioned in single account but in other account its treatment does

not show. As an example, 4500 paid as rent in cash but wrongly it is recorded in bank

account.

Also, if a mathematical error, this can cause a problem too. Or perhaps credited

something that should have been debited or vice versa, or applied a transaction to the

wrong account.

If there is difference of amount in debit and credit side in single entry. If entry made in

more than one account than in trial balance difference can be create. As an example,

imbalance result can be reflected if cash received from debtors is recorded two times in

debtor & cash account.

So these are some general reasons for imbalance resulting from incorrect double entries and

it affect the trial balance and other financial statements. So it is important to record the

transactions more carefully so that chances of mistake can be minimize.

1. 5 Reasons for incomplete records arising from insufficient data

In present era, it is observed that when bookkeeper of an individual entity do not have

accurate and appropriate information to prepare following trail balance and final statements

which led uncompleted accounts. Some of the primary reason are discussed below:

Unintentional failure to record: In case when accountant of company forgets to report

important information then final account remain incomplete. Basically it happens

3

closing capital is not given then only one statement of affairs will be prepared to find closing

capital.

Margin and mark-up method : With the help of margin percentage accountant can

gather missing information.

Accounting equation method : If there is amount of capital is missing than this method

can be used in accounts. To consider the amount of capital outside liabilities are subtracted from

the total assets. So these are the methods which are used to construct accounts from the

incomplete records.

1. 4 Reasons for imbalances resulting from incorrect double entries

Due to the incorrect double entries trial balance cannot be prepare appropriate because

accounting standards and principle does not have followed. There are some other reasons such as

One transaction has mentioned in single account but in other account its treatment does

not show. As an example, 4500 paid as rent in cash but wrongly it is recorded in bank

account.

Also, if a mathematical error, this can cause a problem too. Or perhaps credited

something that should have been debited or vice versa, or applied a transaction to the

wrong account.

If there is difference of amount in debit and credit side in single entry. If entry made in

more than one account than in trial balance difference can be create. As an example,

imbalance result can be reflected if cash received from debtors is recorded two times in

debtor & cash account.

So these are some general reasons for imbalance resulting from incorrect double entries and

it affect the trial balance and other financial statements. So it is important to record the

transactions more carefully so that chances of mistake can be minimize.

1. 5 Reasons for incomplete records arising from insufficient data

In present era, it is observed that when bookkeeper of an individual entity do not have

accurate and appropriate information to prepare following trail balance and final statements

which led uncompleted accounts. Some of the primary reason are discussed below:

Unintentional failure to record: In case when accountant of company forgets to report

important information then final account remain incomplete. Basically it happens

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

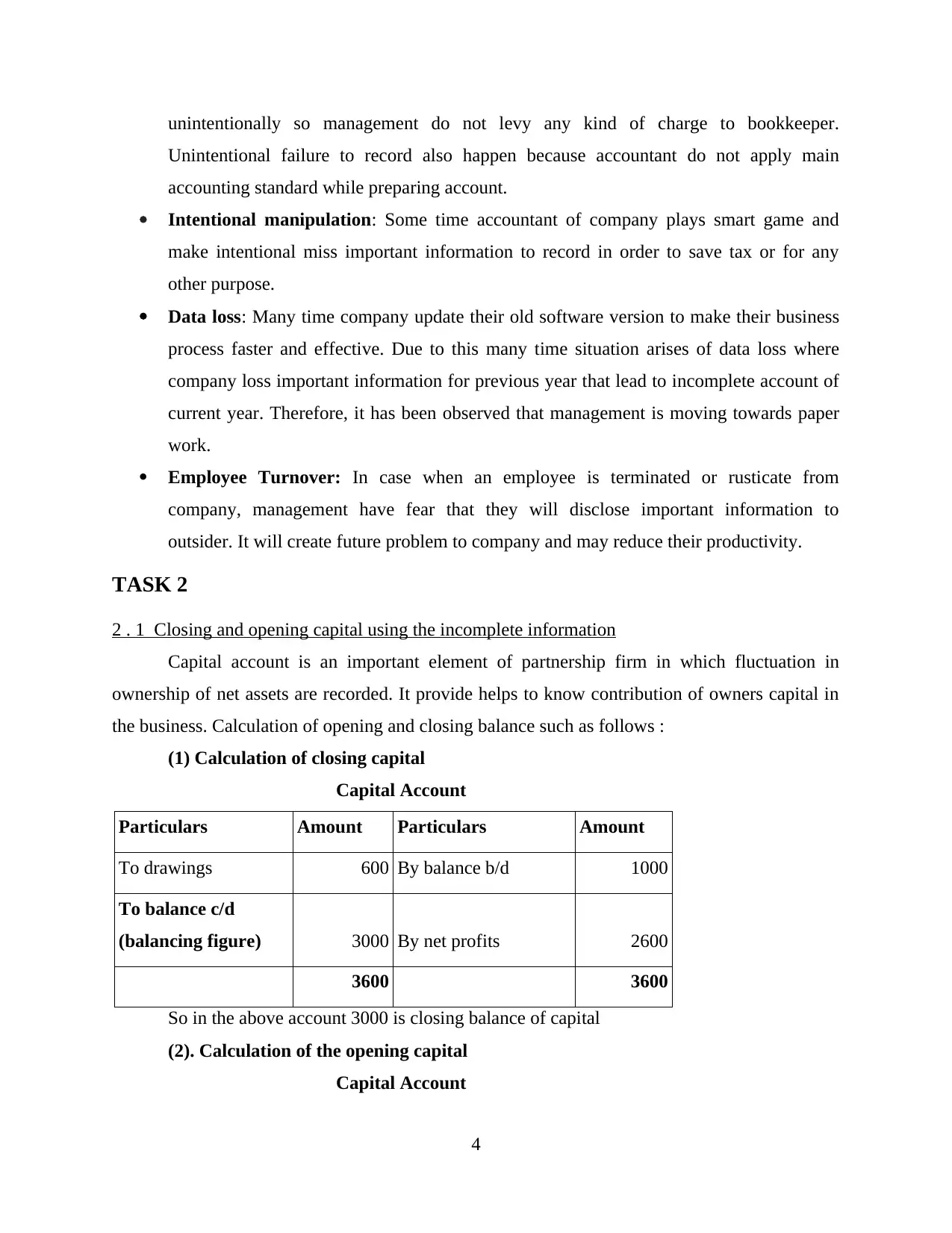

unintentionally so management do not levy any kind of charge to bookkeeper.

Unintentional failure to record also happen because accountant do not apply main

accounting standard while preparing account.

Intentional manipulation: Some time accountant of company plays smart game and

make intentional miss important information to record in order to save tax or for any

other purpose.

Data loss: Many time company update their old software version to make their business

process faster and effective. Due to this many time situation arises of data loss where

company loss important information for previous year that lead to incomplete account of

current year. Therefore, it has been observed that management is moving towards paper

work.

Employee Turnover: In case when an employee is terminated or rusticate from

company, management have fear that they will disclose important information to

outsider. It will create future problem to company and may reduce their productivity.

TASK 2

2 . 1 Closing and opening capital using the incomplete information

Capital account is an important element of partnership firm in which fluctuation in

ownership of net assets are recorded. It provide helps to know contribution of owners capital in

the business. Calculation of opening and closing balance such as follows :

(1) Calculation of closing capital

Capital Account

Particulars Amount Particulars Amount

To drawings 600 By balance b/d 1000

To balance c/d

(balancing figure) 3000 By net profits 2600

3600 3600

So in the above account 3000 is closing balance of capital

(2). Calculation of the opening capital

Capital Account

4

Unintentional failure to record also happen because accountant do not apply main

accounting standard while preparing account.

Intentional manipulation: Some time accountant of company plays smart game and

make intentional miss important information to record in order to save tax or for any

other purpose.

Data loss: Many time company update their old software version to make their business

process faster and effective. Due to this many time situation arises of data loss where

company loss important information for previous year that lead to incomplete account of

current year. Therefore, it has been observed that management is moving towards paper

work.

Employee Turnover: In case when an employee is terminated or rusticate from

company, management have fear that they will disclose important information to

outsider. It will create future problem to company and may reduce their productivity.

TASK 2

2 . 1 Closing and opening capital using the incomplete information

Capital account is an important element of partnership firm in which fluctuation in

ownership of net assets are recorded. It provide helps to know contribution of owners capital in

the business. Calculation of opening and closing balance such as follows :

(1) Calculation of closing capital

Capital Account

Particulars Amount Particulars Amount

To drawings 600 By balance b/d 1000

To balance c/d

(balancing figure) 3000 By net profits 2600

3600 3600

So in the above account 3000 is closing balance of capital

(2). Calculation of the opening capital

Capital Account

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

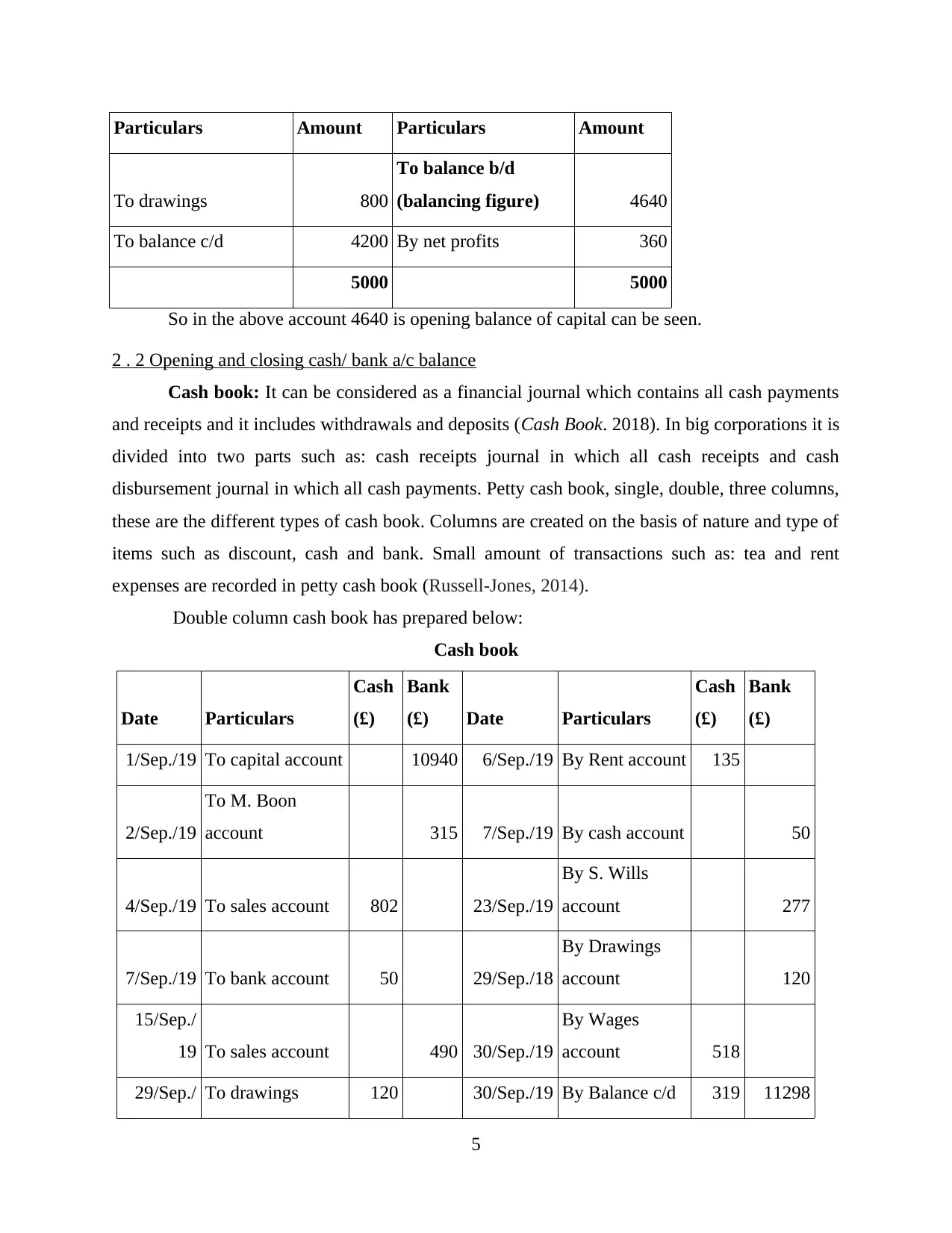

Particulars Amount Particulars Amount

To drawings 800

To balance b/d

(balancing figure) 4640

To balance c/d 4200 By net profits 360

5000 5000

So in the above account 4640 is opening balance of capital can be seen.

2 . 2 Opening and closing cash/ bank a/c balance

Cash book: It can be considered as a financial journal which contains all cash payments

and receipts and it includes withdrawals and deposits (Cash Book. 2018). In big corporations it is

divided into two parts such as: cash receipts journal in which all cash receipts and cash

disbursement journal in which all cash payments. Petty cash book, single, double, three columns,

these are the different types of cash book. Columns are created on the basis of nature and type of

items such as discount, cash and bank. Small amount of transactions such as: tea and rent

expenses are recorded in petty cash book (Russell-Jones, 2014).

Double column cash book has prepared below:

Cash book

Date Particulars

Cash

(£)

Bank

(£) Date Particulars

Cash

(£)

Bank

(£)

1/Sep./19 To capital account 10940 6/Sep./19 By Rent account 135

2/Sep./19

To M. Boon

account 315 7/Sep./19 By cash account 50

4/Sep./19 To sales account 802 23/Sep./19

By S. Wills

account 277

7/Sep./19 To bank account 50 29/Sep./18

By Drawings

account 120

15/Sep./

19 To sales account 490 30/Sep./19

By Wages

account 518

29/Sep./ To drawings 120 30/Sep./19 By Balance c/d 319 11298

5

To drawings 800

To balance b/d

(balancing figure) 4640

To balance c/d 4200 By net profits 360

5000 5000

So in the above account 4640 is opening balance of capital can be seen.

2 . 2 Opening and closing cash/ bank a/c balance

Cash book: It can be considered as a financial journal which contains all cash payments

and receipts and it includes withdrawals and deposits (Cash Book. 2018). In big corporations it is

divided into two parts such as: cash receipts journal in which all cash receipts and cash

disbursement journal in which all cash payments. Petty cash book, single, double, three columns,

these are the different types of cash book. Columns are created on the basis of nature and type of

items such as discount, cash and bank. Small amount of transactions such as: tea and rent

expenses are recorded in petty cash book (Russell-Jones, 2014).

Double column cash book has prepared below:

Cash book

Date Particulars

Cash

(£)

Bank

(£) Date Particulars

Cash

(£)

Bank

(£)

1/Sep./19 To capital account 10940 6/Sep./19 By Rent account 135

2/Sep./19

To M. Boon

account 315 7/Sep./19 By cash account 50

4/Sep./19 To sales account 802 23/Sep./19

By S. Wills

account 277

7/Sep./19 To bank account 50 29/Sep./18

By Drawings

account 120

15/Sep./

19 To sales account 490 30/Sep./19

By Wages

account 518

29/Sep./ To drawings 120 30/Sep./19 By Balance c/d 319 11298

5

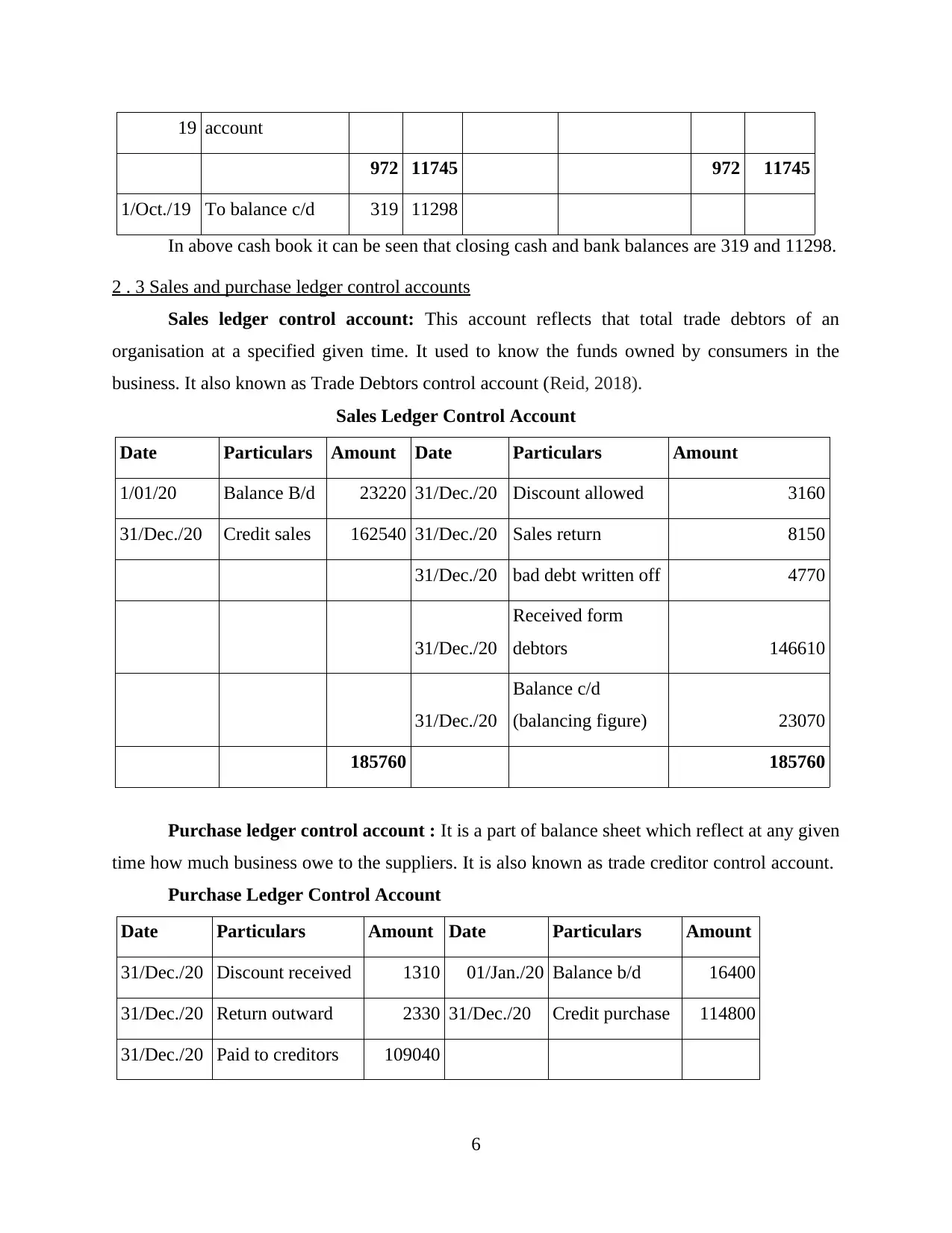

19 account

972 11745 972 11745

1/Oct./19 To balance c/d 319 11298

In above cash book it can be seen that closing cash and bank balances are 319 and 11298.

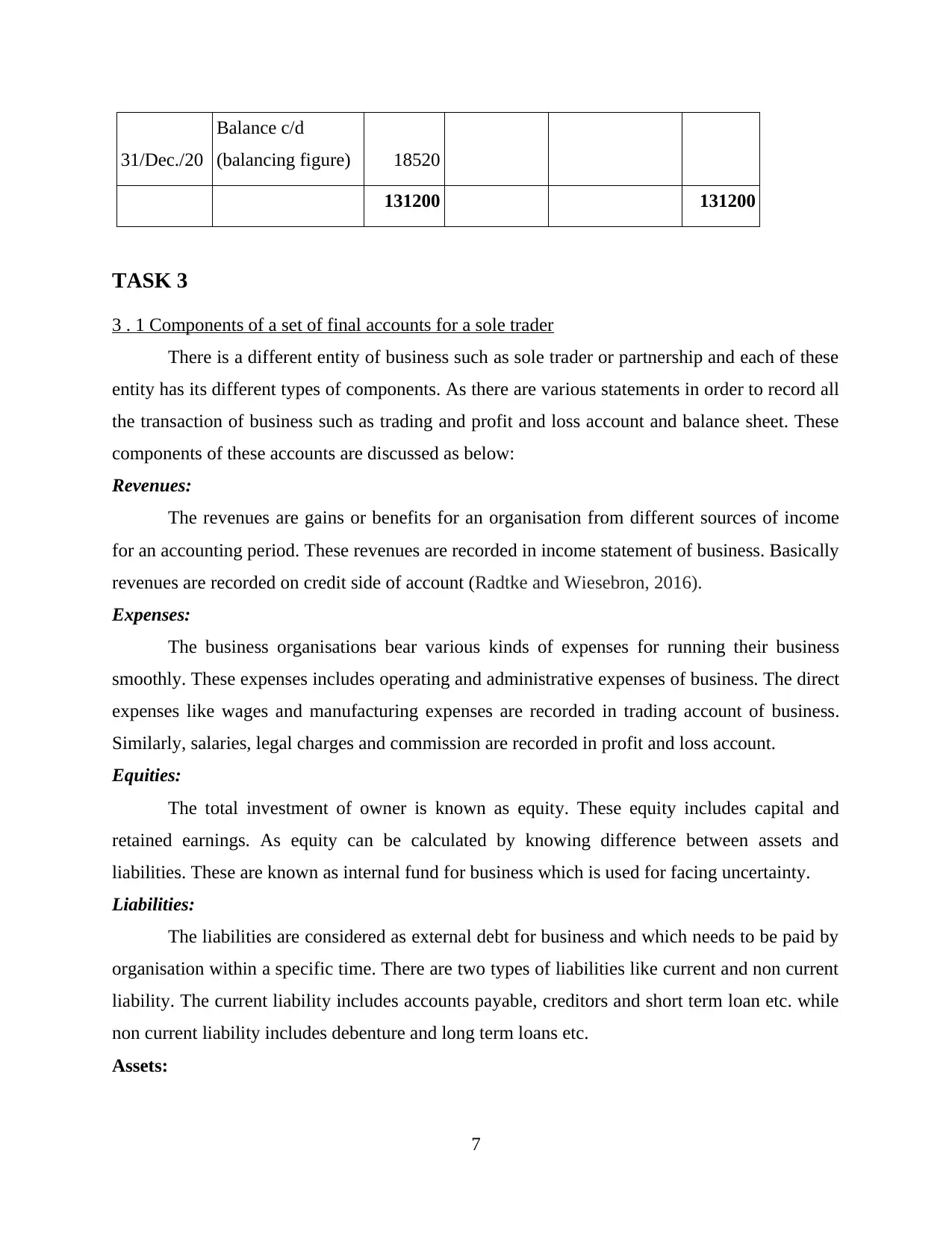

2 . 3 Sales and purchase ledger control accounts

Sales ledger control account: This account reflects that total trade debtors of an

organisation at a specified given time. It used to know the funds owned by consumers in the

business. It also known as Trade Debtors control account (Reid, 2018).

Sales Ledger Control Account

Date Particulars Amount Date Particulars Amount

1/01/20 Balance B/d 23220 31/Dec./20 Discount allowed 3160

31/Dec./20 Credit sales 162540 31/Dec./20 Sales return 8150

31/Dec./20 bad debt written off 4770

31/Dec./20

Received form

debtors 146610

31/Dec./20

Balance c/d

(balancing figure) 23070

185760 185760

Purchase ledger control account : It is a part of balance sheet which reflect at any given

time how much business owe to the suppliers. It is also known as trade creditor control account.

Purchase Ledger Control Account

Date Particulars Amount Date Particulars Amount

31/Dec./20 Discount received 1310 01/Jan./20 Balance b/d 16400

31/Dec./20 Return outward 2330 31/Dec./20 Credit purchase 114800

31/Dec./20 Paid to creditors 109040

6

972 11745 972 11745

1/Oct./19 To balance c/d 319 11298

In above cash book it can be seen that closing cash and bank balances are 319 and 11298.

2 . 3 Sales and purchase ledger control accounts

Sales ledger control account: This account reflects that total trade debtors of an

organisation at a specified given time. It used to know the funds owned by consumers in the

business. It also known as Trade Debtors control account (Reid, 2018).

Sales Ledger Control Account

Date Particulars Amount Date Particulars Amount

1/01/20 Balance B/d 23220 31/Dec./20 Discount allowed 3160

31/Dec./20 Credit sales 162540 31/Dec./20 Sales return 8150

31/Dec./20 bad debt written off 4770

31/Dec./20

Received form

debtors 146610

31/Dec./20

Balance c/d

(balancing figure) 23070

185760 185760

Purchase ledger control account : It is a part of balance sheet which reflect at any given

time how much business owe to the suppliers. It is also known as trade creditor control account.

Purchase Ledger Control Account

Date Particulars Amount Date Particulars Amount

31/Dec./20 Discount received 1310 01/Jan./20 Balance b/d 16400

31/Dec./20 Return outward 2330 31/Dec./20 Credit purchase 114800

31/Dec./20 Paid to creditors 109040

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

31/Dec./20

Balance c/d

(balancing figure) 18520

131200 131200

TASK 3

3 . 1 Components of a set of final accounts for a sole trader

There is a different entity of business such as sole trader or partnership and each of these

entity has its different types of components. As there are various statements in order to record all

the transaction of business such as trading and profit and loss account and balance sheet. These

components of these accounts are discussed as below:

Revenues:

The revenues are gains or benefits for an organisation from different sources of income

for an accounting period. These revenues are recorded in income statement of business. Basically

revenues are recorded on credit side of account (Radtke and Wiesebron, 2016).

Expenses:

The business organisations bear various kinds of expenses for running their business

smoothly. These expenses includes operating and administrative expenses of business. The direct

expenses like wages and manufacturing expenses are recorded in trading account of business.

Similarly, salaries, legal charges and commission are recorded in profit and loss account.

Equities:

The total investment of owner is known as equity. These equity includes capital and

retained earnings. As equity can be calculated by knowing difference between assets and

liabilities. These are known as internal fund for business which is used for facing uncertainty.

Liabilities:

The liabilities are considered as external debt for business and which needs to be paid by

organisation within a specific time. There are two types of liabilities like current and non current

liability. The current liability includes accounts payable, creditors and short term loan etc. while

non current liability includes debenture and long term loans etc.

Assets:

7

Balance c/d

(balancing figure) 18520

131200 131200

TASK 3

3 . 1 Components of a set of final accounts for a sole trader

There is a different entity of business such as sole trader or partnership and each of these

entity has its different types of components. As there are various statements in order to record all

the transaction of business such as trading and profit and loss account and balance sheet. These

components of these accounts are discussed as below:

Revenues:

The revenues are gains or benefits for an organisation from different sources of income

for an accounting period. These revenues are recorded in income statement of business. Basically

revenues are recorded on credit side of account (Radtke and Wiesebron, 2016).

Expenses:

The business organisations bear various kinds of expenses for running their business

smoothly. These expenses includes operating and administrative expenses of business. The direct

expenses like wages and manufacturing expenses are recorded in trading account of business.

Similarly, salaries, legal charges and commission are recorded in profit and loss account.

Equities:

The total investment of owner is known as equity. These equity includes capital and

retained earnings. As equity can be calculated by knowing difference between assets and

liabilities. These are known as internal fund for business which is used for facing uncertainty.

Liabilities:

The liabilities are considered as external debt for business and which needs to be paid by

organisation within a specific time. There are two types of liabilities like current and non current

liability. The current liability includes accounts payable, creditors and short term loan etc. while

non current liability includes debenture and long term loans etc.

Assets:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assets are those items which are recorded in the balance sheet and used for smooth

running business. There are two types of assets in business such as current and non current. The

current assets includes Debtors, Bank and prepaid expenses while non current assets includes the

Land, Buildings and Machinery etc (Paterson, 2016).

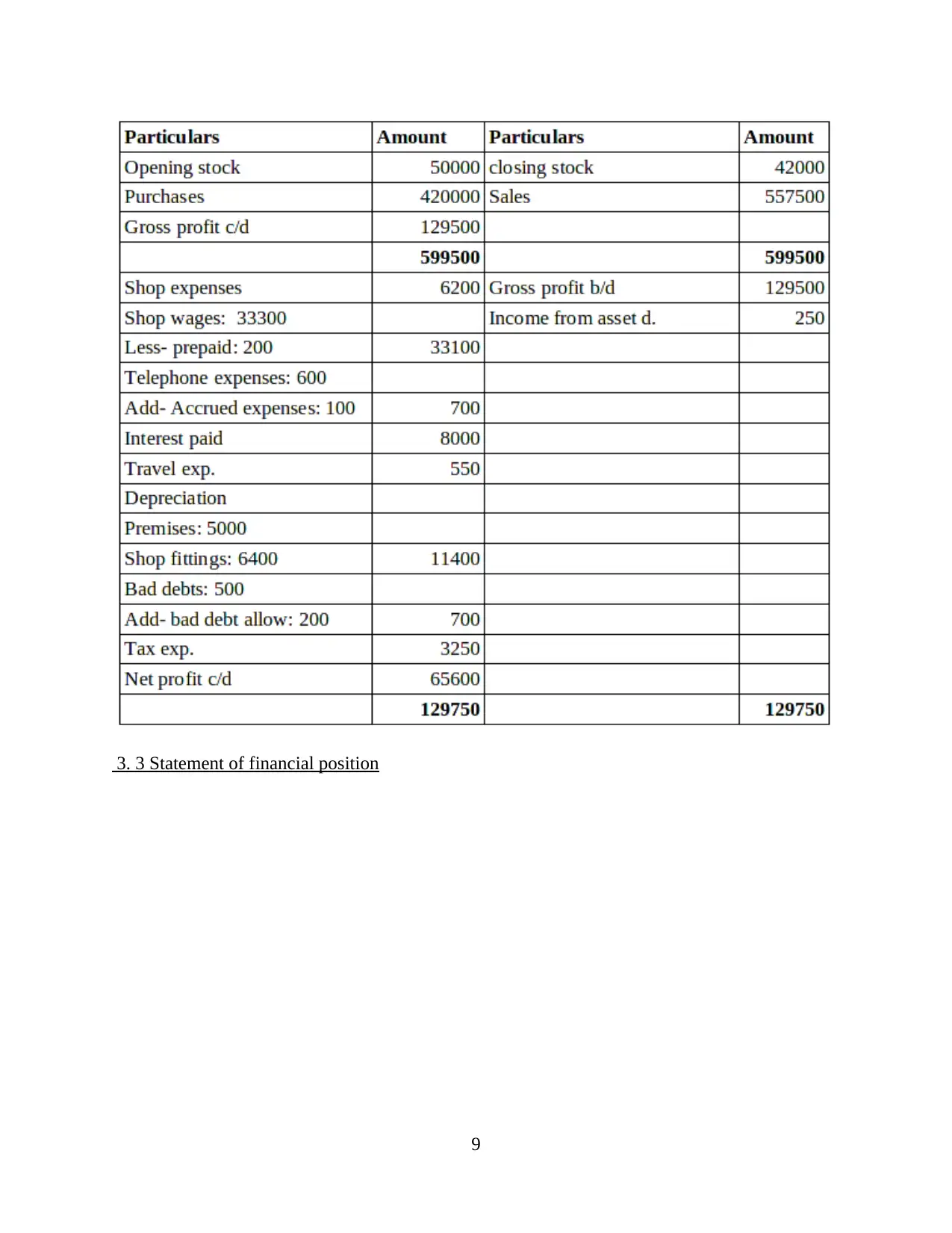

3. 2 Formulation of statement of P&L a/c

Trading and Profit and loss statement

8

running business. There are two types of assets in business such as current and non current. The

current assets includes Debtors, Bank and prepaid expenses while non current assets includes the

Land, Buildings and Machinery etc (Paterson, 2016).

3. 2 Formulation of statement of P&L a/c

Trading and Profit and loss statement

8

3. 3 Statement of financial position

9

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.