Consolidation of Financial Statements for FinalHeadache Ltd.

VerifiedAdded on 2020/04/01

|17

|4138

|69

AI Summary

This assignment focuses on the consolidation of FinalHeadache Ltd's financial statements with its subsidiary Solutions Ltd as of 30 June 2019. Students will apply AASB 10 standards to assess business combinations, considering both full and partial goodwill methods. The task involves preparing consolidated profit or loss and balance sheet statements, addressing intercompany transactions such as unrealized profits in inventories and dividends received. References include authoritative sources on accounting for business combinations and goodwill. This exercise aims to enhance understanding of financial consolidation processes and the application of relevant accounting standards.

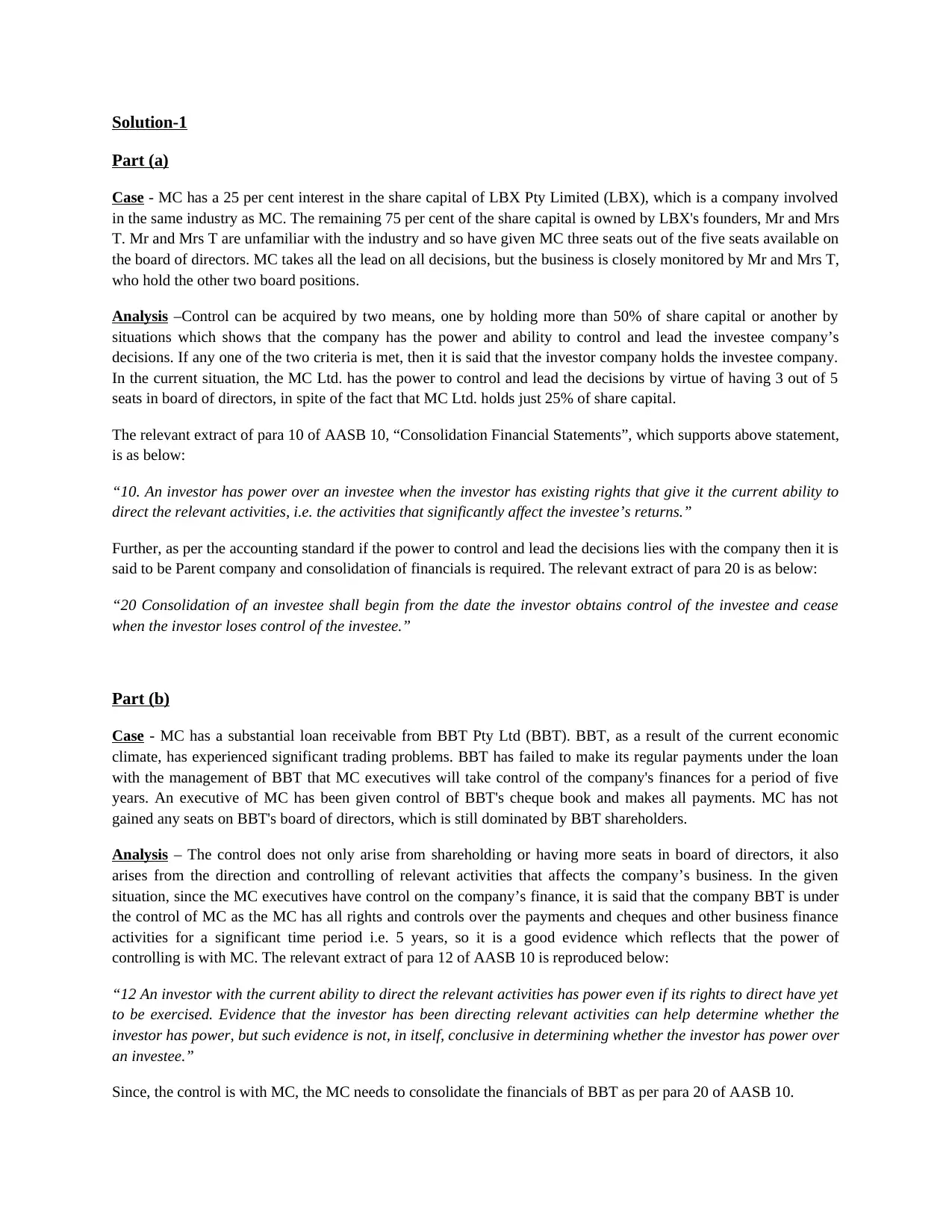

Solution-1

Part (a)

Case - MC has a 25 per cent interest in the share capital of LBX Pty Limited (LBX), which is a company involved

in the same industry as MC. The remaining 75 per cent of the share capital is owned by LBX's founders, Mr and Mrs

T. Mr and Mrs T are unfamiliar with the industry and so have given MC three seats out of the five seats available on

the board of directors. MC takes all the lead on all decisions, but the business is closely monitored by Mr and Mrs T,

who hold the other two board positions.

Analysis –Control can be acquired by two means, one by holding more than 50% of share capital or another by

situations which shows that the company has the power and ability to control and lead the investee company’s

decisions. If any one of the two criteria is met, then it is said that the investor company holds the investee company.

In the current situation, the MC Ltd. has the power to control and lead the decisions by virtue of having 3 out of 5

seats in board of directors, in spite of the fact that MC Ltd. holds just 25% of share capital.

The relevant extract of para 10 of AASB 10, “Consolidation Financial Statements”, which supports above statement,

is as below:

“10. An investor has power over an investee when the investor has existing rights that give it the current ability to

direct the relevant activities, i.e. the activities that significantly affect the investee’s returns.”

Further, as per the accounting standard if the power to control and lead the decisions lies with the company then it is

said to be Parent company and consolidation of financials is required. The relevant extract of para 20 is as below:

“20 Consolidation of an investee shall begin from the date the investor obtains control of the investee and cease

when the investor loses control of the investee.”

Part (b)

Case - MC has a substantial loan receivable from BBT Pty Ltd (BBT). BBT, as a result of the current economic

climate, has experienced significant trading problems. BBT has failed to make its regular payments under the loan

with the management of BBT that MC executives will take control of the company's finances for a period of five

years. An executive of MC has been given control of BBT's cheque book and makes all payments. MC has not

gained any seats on BBT's board of directors, which is still dominated by BBT shareholders.

Analysis – The control does not only arise from shareholding or having more seats in board of directors, it also

arises from the direction and controlling of relevant activities that affects the company’s business. In the given

situation, since the MC executives have control on the company’s finance, it is said that the company BBT is under

the control of MC as the MC has all rights and controls over the payments and cheques and other business finance

activities for a significant time period i.e. 5 years, so it is a good evidence which reflects that the power of

controlling is with MC. The relevant extract of para 12 of AASB 10 is reproduced below:

“12 An investor with the current ability to direct the relevant activities has power even if its rights to direct have yet

to be exercised. Evidence that the investor has been directing relevant activities can help determine whether the

investor has power, but such evidence is not, in itself, conclusive in determining whether the investor has power over

an investee.”

Since, the control is with MC, the MC needs to consolidate the financials of BBT as per para 20 of AASB 10.

Part (a)

Case - MC has a 25 per cent interest in the share capital of LBX Pty Limited (LBX), which is a company involved

in the same industry as MC. The remaining 75 per cent of the share capital is owned by LBX's founders, Mr and Mrs

T. Mr and Mrs T are unfamiliar with the industry and so have given MC three seats out of the five seats available on

the board of directors. MC takes all the lead on all decisions, but the business is closely monitored by Mr and Mrs T,

who hold the other two board positions.

Analysis –Control can be acquired by two means, one by holding more than 50% of share capital or another by

situations which shows that the company has the power and ability to control and lead the investee company’s

decisions. If any one of the two criteria is met, then it is said that the investor company holds the investee company.

In the current situation, the MC Ltd. has the power to control and lead the decisions by virtue of having 3 out of 5

seats in board of directors, in spite of the fact that MC Ltd. holds just 25% of share capital.

The relevant extract of para 10 of AASB 10, “Consolidation Financial Statements”, which supports above statement,

is as below:

“10. An investor has power over an investee when the investor has existing rights that give it the current ability to

direct the relevant activities, i.e. the activities that significantly affect the investee’s returns.”

Further, as per the accounting standard if the power to control and lead the decisions lies with the company then it is

said to be Parent company and consolidation of financials is required. The relevant extract of para 20 is as below:

“20 Consolidation of an investee shall begin from the date the investor obtains control of the investee and cease

when the investor loses control of the investee.”

Part (b)

Case - MC has a substantial loan receivable from BBT Pty Ltd (BBT). BBT, as a result of the current economic

climate, has experienced significant trading problems. BBT has failed to make its regular payments under the loan

with the management of BBT that MC executives will take control of the company's finances for a period of five

years. An executive of MC has been given control of BBT's cheque book and makes all payments. MC has not

gained any seats on BBT's board of directors, which is still dominated by BBT shareholders.

Analysis – The control does not only arise from shareholding or having more seats in board of directors, it also

arises from the direction and controlling of relevant activities that affects the company’s business. In the given

situation, since the MC executives have control on the company’s finance, it is said that the company BBT is under

the control of MC as the MC has all rights and controls over the payments and cheques and other business finance

activities for a significant time period i.e. 5 years, so it is a good evidence which reflects that the power of

controlling is with MC. The relevant extract of para 12 of AASB 10 is reproduced below:

“12 An investor with the current ability to direct the relevant activities has power even if its rights to direct have yet

to be exercised. Evidence that the investor has been directing relevant activities can help determine whether the

investor has power, but such evidence is not, in itself, conclusive in determining whether the investor has power over

an investee.”

Since, the control is with MC, the MC needs to consolidate the financials of BBT as per para 20 of AASB 10.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

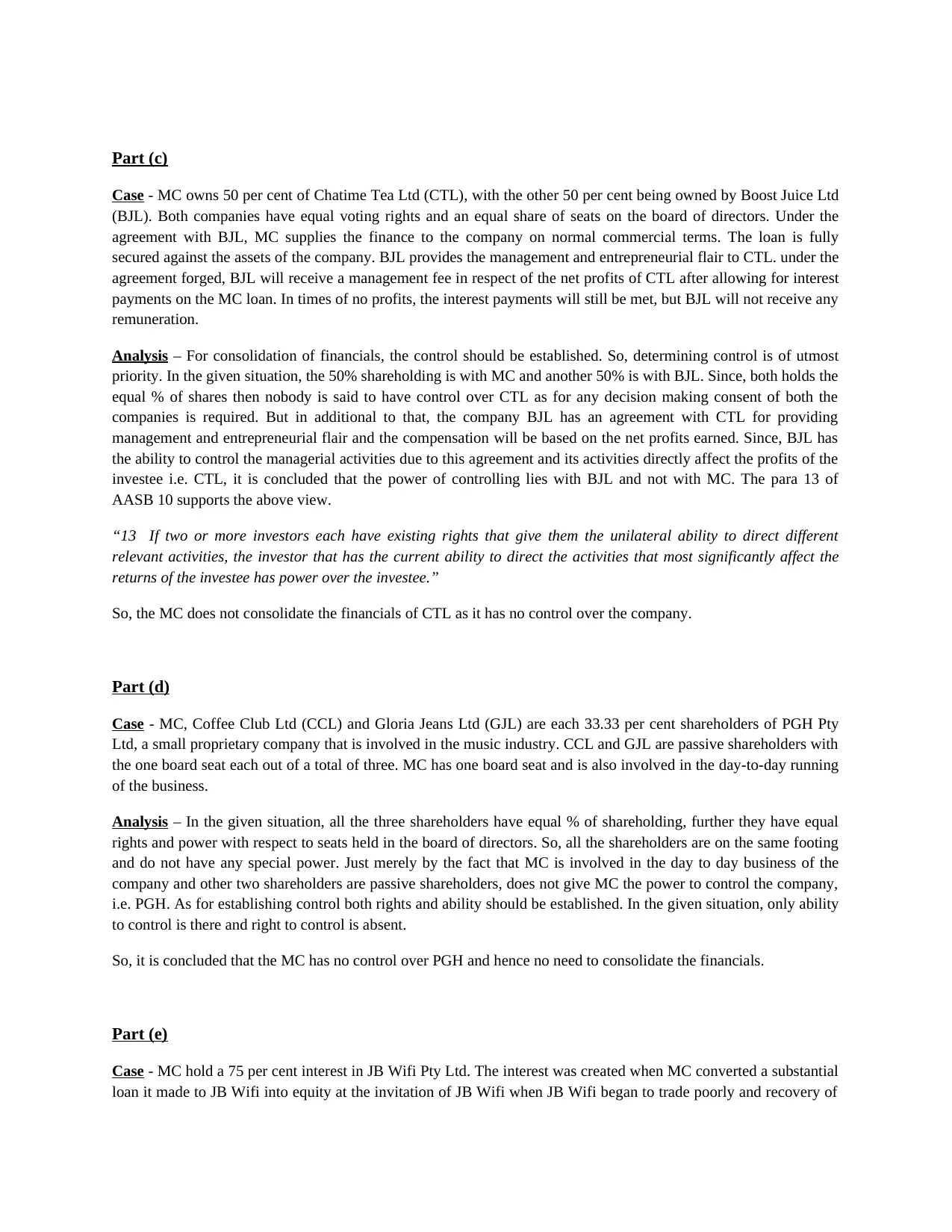

Part (c)

Case - MC owns 50 per cent of Chatime Tea Ltd (CTL), with the other 50 per cent being owned by Boost Juice Ltd

(BJL). Both companies have equal voting rights and an equal share of seats on the board of directors. Under the

agreement with BJL, MC supplies the finance to the company on normal commercial terms. The loan is fully

secured against the assets of the company. BJL provides the management and entrepreneurial flair to CTL. under the

agreement forged, BJL will receive a management fee in respect of the net profits of CTL after allowing for interest

payments on the MC loan. In times of no profits, the interest payments will still be met, but BJL will not receive any

remuneration.

Analysis – For consolidation of financials, the control should be established. So, determining control is of utmost

priority. In the given situation, the 50% shareholding is with MC and another 50% is with BJL. Since, both holds the

equal % of shares then nobody is said to have control over CTL as for any decision making consent of both the

companies is required. But in additional to that, the company BJL has an agreement with CTL for providing

management and entrepreneurial flair and the compensation will be based on the net profits earned. Since, BJL has

the ability to control the managerial activities due to this agreement and its activities directly affect the profits of the

investee i.e. CTL, it is concluded that the power of controlling lies with BJL and not with MC. The para 13 of

AASB 10 supports the above view.

“13 If two or more investors each have existing rights that give them the unilateral ability to direct different

relevant activities, the investor that has the current ability to direct the activities that most significantly affect the

returns of the investee has power over the investee.”

So, the MC does not consolidate the financials of CTL as it has no control over the company.

Part (d)

Case - MC, Coffee Club Ltd (CCL) and Gloria Jeans Ltd (GJL) are each 33.33 per cent shareholders of PGH Pty

Ltd, a small proprietary company that is involved in the music industry. CCL and GJL are passive shareholders with

the one board seat each out of a total of three. MC has one board seat and is also involved in the day-to-day running

of the business.

Analysis – In the given situation, all the three shareholders have equal % of shareholding, further they have equal

rights and power with respect to seats held in the board of directors. So, all the shareholders are on the same footing

and do not have any special power. Just merely by the fact that MC is involved in the day to day business of the

company and other two shareholders are passive shareholders, does not give MC the power to control the company,

i.e. PGH. As for establishing control both rights and ability should be established. In the given situation, only ability

to control is there and right to control is absent.

So, it is concluded that the MC has no control over PGH and hence no need to consolidate the financials.

Part (e)

Case - MC hold a 75 per cent interest in JB Wifi Pty Ltd. The interest was created when MC converted a substantial

loan it made to JB Wifi into equity at the invitation of JB Wifi when JB Wifi began to trade poorly and recovery of

Case - MC owns 50 per cent of Chatime Tea Ltd (CTL), with the other 50 per cent being owned by Boost Juice Ltd

(BJL). Both companies have equal voting rights and an equal share of seats on the board of directors. Under the

agreement with BJL, MC supplies the finance to the company on normal commercial terms. The loan is fully

secured against the assets of the company. BJL provides the management and entrepreneurial flair to CTL. under the

agreement forged, BJL will receive a management fee in respect of the net profits of CTL after allowing for interest

payments on the MC loan. In times of no profits, the interest payments will still be met, but BJL will not receive any

remuneration.

Analysis – For consolidation of financials, the control should be established. So, determining control is of utmost

priority. In the given situation, the 50% shareholding is with MC and another 50% is with BJL. Since, both holds the

equal % of shares then nobody is said to have control over CTL as for any decision making consent of both the

companies is required. But in additional to that, the company BJL has an agreement with CTL for providing

management and entrepreneurial flair and the compensation will be based on the net profits earned. Since, BJL has

the ability to control the managerial activities due to this agreement and its activities directly affect the profits of the

investee i.e. CTL, it is concluded that the power of controlling lies with BJL and not with MC. The para 13 of

AASB 10 supports the above view.

“13 If two or more investors each have existing rights that give them the unilateral ability to direct different

relevant activities, the investor that has the current ability to direct the activities that most significantly affect the

returns of the investee has power over the investee.”

So, the MC does not consolidate the financials of CTL as it has no control over the company.

Part (d)

Case - MC, Coffee Club Ltd (CCL) and Gloria Jeans Ltd (GJL) are each 33.33 per cent shareholders of PGH Pty

Ltd, a small proprietary company that is involved in the music industry. CCL and GJL are passive shareholders with

the one board seat each out of a total of three. MC has one board seat and is also involved in the day-to-day running

of the business.

Analysis – In the given situation, all the three shareholders have equal % of shareholding, further they have equal

rights and power with respect to seats held in the board of directors. So, all the shareholders are on the same footing

and do not have any special power. Just merely by the fact that MC is involved in the day to day business of the

company and other two shareholders are passive shareholders, does not give MC the power to control the company,

i.e. PGH. As for establishing control both rights and ability should be established. In the given situation, only ability

to control is there and right to control is absent.

So, it is concluded that the MC has no control over PGH and hence no need to consolidate the financials.

Part (e)

Case - MC hold a 75 per cent interest in JB Wifi Pty Ltd. The interest was created when MC converted a substantial

loan it made to JB Wifi into equity at the invitation of JB Wifi when JB Wifi began to trade poorly and recovery of

the loan seemed uncertain. JB Wifi has a large deficiency in net assets and has been consolidated for many years.

MC is a passive investor, having no seats on the board of directors and no say in the financing or operating decisions

of JB Wifi.

Analysis – Power and rights go hand in hand. When an investor holds significant shareholding, i.e. more than 50%

then it is said that the investor has power to control the investee. As in the major decisions, the investor’s decision

will prevail due to large % of shareholding. In the given situation, the MC holds 75% of shares of JB Wifi and due

to this shareholding the MC has right to take conclusive decision of every transactions irrespective of the fact that he

is involved in the business of JB or not. The para 11 of AASB 10, also states that,

“11 Power arises from rights. Sometimes assessing power is straightforward, such as when power over an investee

is obtained directly and solely from the voting rights granted by equity instruments such as shares, and can be

assessed by considering the voting rights from those shareholdings. In other cases, the assessment will be more

complex and require more than one factor to be considered, for example when power results from one or more

contractual arrangements.”

MC is a passive investor, having no seats on the board of directors and no say in the financing or operating decisions

of JB Wifi.

Analysis – Power and rights go hand in hand. When an investor holds significant shareholding, i.e. more than 50%

then it is said that the investor has power to control the investee. As in the major decisions, the investor’s decision

will prevail due to large % of shareholding. In the given situation, the MC holds 75% of shares of JB Wifi and due

to this shareholding the MC has right to take conclusive decision of every transactions irrespective of the fact that he

is involved in the business of JB or not. The para 11 of AASB 10, also states that,

“11 Power arises from rights. Sometimes assessing power is straightforward, such as when power over an investee

is obtained directly and solely from the voting rights granted by equity instruments such as shares, and can be

assessed by considering the voting rights from those shareholdings. In other cases, the assessment will be more

complex and require more than one factor to be considered, for example when power results from one or more

contractual arrangements.”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

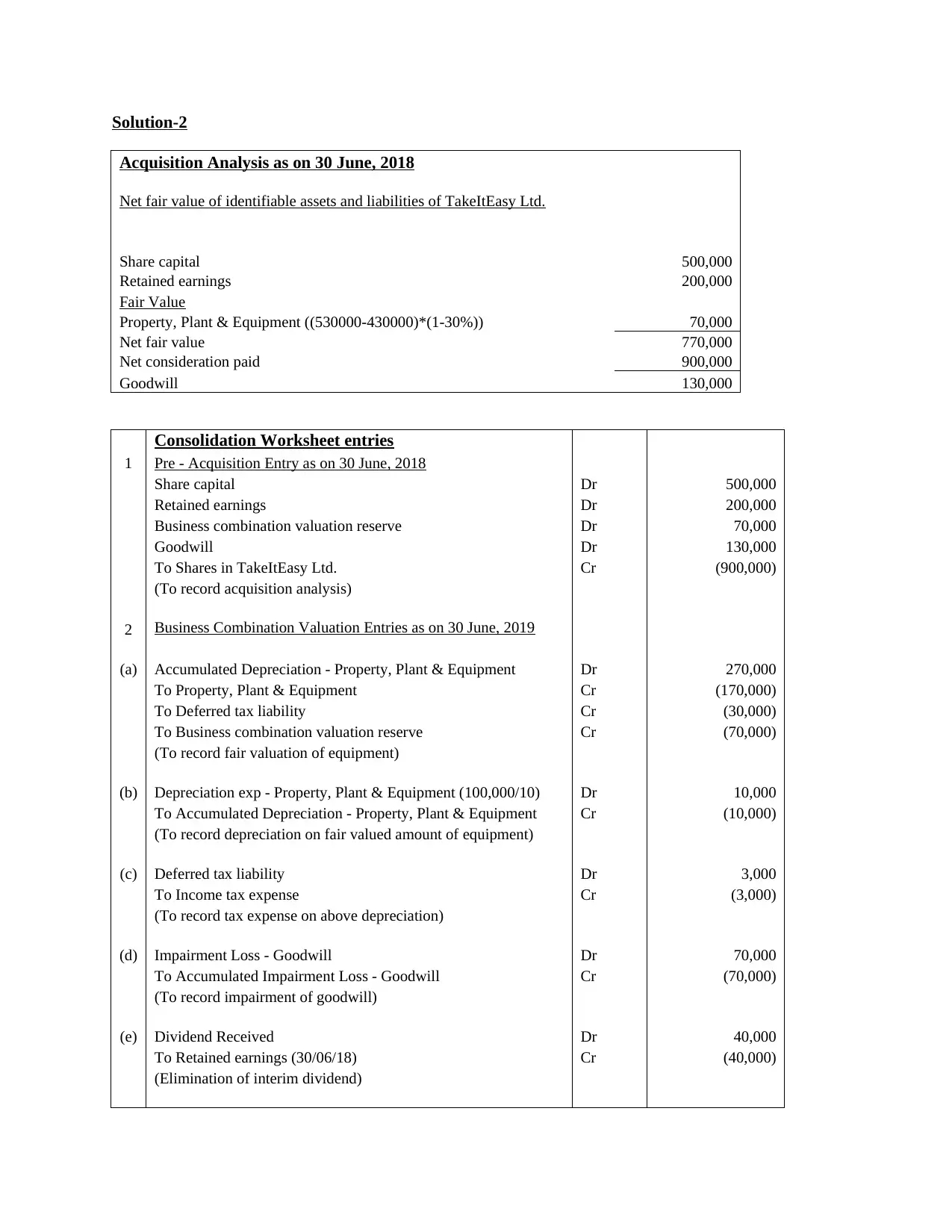

Solution-2

Acquisition Analysis as on 30 June, 2018

Net fair value of identifiable assets and liabilities of TakeItEasy Ltd.

Share capital 500,000

Retained earnings 200,000

Fair Value

Property, Plant & Equipment ((530000-430000)*(1-30%)) 70,000

Net fair value 770,000

Net consideration paid 900,000

Goodwill 130,000

Consolidation Worksheet entries

1 Pre - Acquisition Entry as on 30 June, 2018

Share capital Dr 500,000

Retained earnings Dr 200,000

Business combination valuation reserve Dr 70,000

Goodwill Dr 130,000

To Shares in TakeItEasy Ltd. Cr (900,000)

(To record acquisition analysis)

2 Business Combination Valuation Entries as on 30 June, 2019

(a) Accumulated Depreciation - Property, Plant & Equipment Dr 270,000

To Property, Plant & Equipment Cr (170,000)

To Deferred tax liability Cr (30,000)

To Business combination valuation reserve Cr (70,000)

(To record fair valuation of equipment)

(b) Depreciation exp - Property, Plant & Equipment (100,000/10) Dr 10,000

To Accumulated Depreciation - Property, Plant & Equipment Cr (10,000)

(To record depreciation on fair valued amount of equipment)

(c) Deferred tax liability Dr 3,000

To Income tax expense Cr (3,000)

(To record tax expense on above depreciation)

(d) Impairment Loss - Goodwill Dr 70,000

To Accumulated Impairment Loss - Goodwill Cr (70,000)

(To record impairment of goodwill)

(e) Dividend Received Dr 40,000

To Retained earnings (30/06/18) Cr (40,000)

(Elimination of interim dividend)

Acquisition Analysis as on 30 June, 2018

Net fair value of identifiable assets and liabilities of TakeItEasy Ltd.

Share capital 500,000

Retained earnings 200,000

Fair Value

Property, Plant & Equipment ((530000-430000)*(1-30%)) 70,000

Net fair value 770,000

Net consideration paid 900,000

Goodwill 130,000

Consolidation Worksheet entries

1 Pre - Acquisition Entry as on 30 June, 2018

Share capital Dr 500,000

Retained earnings Dr 200,000

Business combination valuation reserve Dr 70,000

Goodwill Dr 130,000

To Shares in TakeItEasy Ltd. Cr (900,000)

(To record acquisition analysis)

2 Business Combination Valuation Entries as on 30 June, 2019

(a) Accumulated Depreciation - Property, Plant & Equipment Dr 270,000

To Property, Plant & Equipment Cr (170,000)

To Deferred tax liability Cr (30,000)

To Business combination valuation reserve Cr (70,000)

(To record fair valuation of equipment)

(b) Depreciation exp - Property, Plant & Equipment (100,000/10) Dr 10,000

To Accumulated Depreciation - Property, Plant & Equipment Cr (10,000)

(To record depreciation on fair valued amount of equipment)

(c) Deferred tax liability Dr 3,000

To Income tax expense Cr (3,000)

(To record tax expense on above depreciation)

(d) Impairment Loss - Goodwill Dr 70,000

To Accumulated Impairment Loss - Goodwill Cr (70,000)

(To record impairment of goodwill)

(e) Dividend Received Dr 40,000

To Retained earnings (30/06/18) Cr (40,000)

(Elimination of interim dividend)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

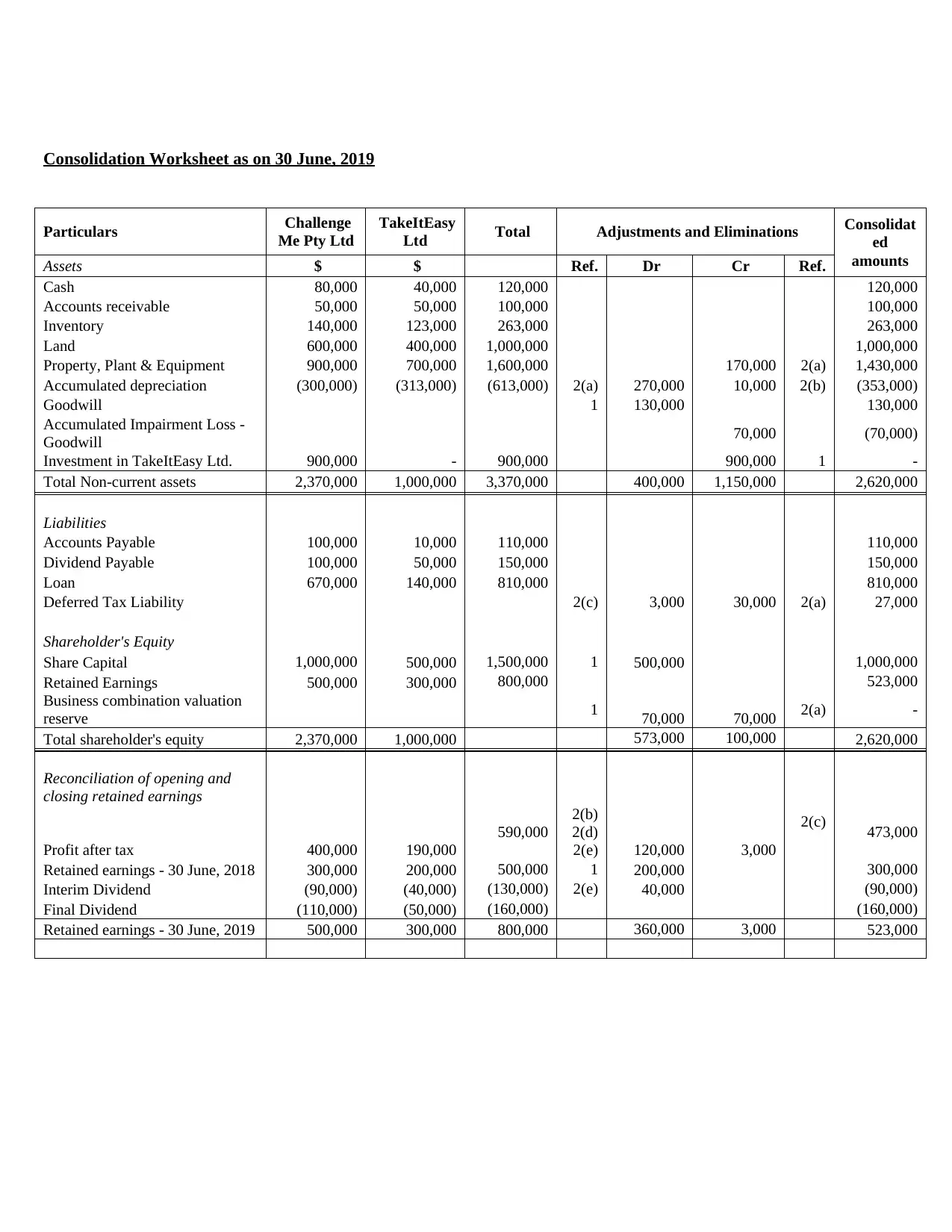

Consolidation Worksheet as on 30 June, 2019

Particulars Challenge

Me Pty Ltd

TakeItEasy

Ltd Total Adjustments and Eliminations Consolidat

ed

amountsAssets $ $ Ref. Dr Cr Ref.

Cash 80,000 40,000 120,000 120,000

Accounts receivable 50,000 50,000 100,000 100,000

Inventory 140,000 123,000 263,000 263,000

Land 600,000 400,000 1,000,000 1,000,000

Property, Plant & Equipment 900,000 700,000 1,600,000 170,000 2(a) 1,430,000

Accumulated depreciation (300,000) (313,000) (613,000) 2(a) 270,000 10,000 2(b) (353,000)

Goodwill 1 130,000 130,000

Accumulated Impairment Loss -

Goodwill 70,000 (70,000)

Investment in TakeItEasy Ltd. 900,000 - 900,000 900,000 1 -

Total Non-current assets 2,370,000 1,000,000 3,370,000 400,000 1,150,000 2,620,000

Liabilities

Accounts Payable 100,000 10,000 110,000 110,000

Dividend Payable 100,000 50,000 150,000 150,000

Loan 670,000 140,000 810,000 810,000

Deferred Tax Liability 2(c) 3,000 30,000 2(a) 27,000

Shareholder's Equity

Share Capital 1,000,000 500,000 1,500,000 1 500,000 1,000,000

Retained Earnings 500,000 300,000 800,000 523,000

Business combination valuation

reserve 1 70,000 70,000 2(a) -

Total shareholder's equity 2,370,000 1,000,000 573,000 100,000 2,620,000

Reconciliation of opening and

closing retained earnings

Profit after tax 400,000 190,000

590,000

2(b)

2(d)

2(e) 120,000 3,000

2(c) 473,000

Retained earnings - 30 June, 2018 300,000 200,000 500,000 1 200,000 300,000

Interim Dividend (90,000) (40,000) (130,000) 2(e) 40,000 (90,000)

Final Dividend (110,000) (50,000) (160,000) (160,000)

Retained earnings - 30 June, 2019 500,000 300,000 800,000 360,000 3,000 523,000

Particulars Challenge

Me Pty Ltd

TakeItEasy

Ltd Total Adjustments and Eliminations Consolidat

ed

amountsAssets $ $ Ref. Dr Cr Ref.

Cash 80,000 40,000 120,000 120,000

Accounts receivable 50,000 50,000 100,000 100,000

Inventory 140,000 123,000 263,000 263,000

Land 600,000 400,000 1,000,000 1,000,000

Property, Plant & Equipment 900,000 700,000 1,600,000 170,000 2(a) 1,430,000

Accumulated depreciation (300,000) (313,000) (613,000) 2(a) 270,000 10,000 2(b) (353,000)

Goodwill 1 130,000 130,000

Accumulated Impairment Loss -

Goodwill 70,000 (70,000)

Investment in TakeItEasy Ltd. 900,000 - 900,000 900,000 1 -

Total Non-current assets 2,370,000 1,000,000 3,370,000 400,000 1,150,000 2,620,000

Liabilities

Accounts Payable 100,000 10,000 110,000 110,000

Dividend Payable 100,000 50,000 150,000 150,000

Loan 670,000 140,000 810,000 810,000

Deferred Tax Liability 2(c) 3,000 30,000 2(a) 27,000

Shareholder's Equity

Share Capital 1,000,000 500,000 1,500,000 1 500,000 1,000,000

Retained Earnings 500,000 300,000 800,000 523,000

Business combination valuation

reserve 1 70,000 70,000 2(a) -

Total shareholder's equity 2,370,000 1,000,000 573,000 100,000 2,620,000

Reconciliation of opening and

closing retained earnings

Profit after tax 400,000 190,000

590,000

2(b)

2(d)

2(e) 120,000 3,000

2(c) 473,000

Retained earnings - 30 June, 2018 300,000 200,000 500,000 1 200,000 300,000

Interim Dividend (90,000) (40,000) (130,000) 2(e) 40,000 (90,000)

Final Dividend (110,000) (50,000) (160,000) (160,000)

Retained earnings - 30 June, 2019 500,000 300,000 800,000 360,000 3,000 523,000

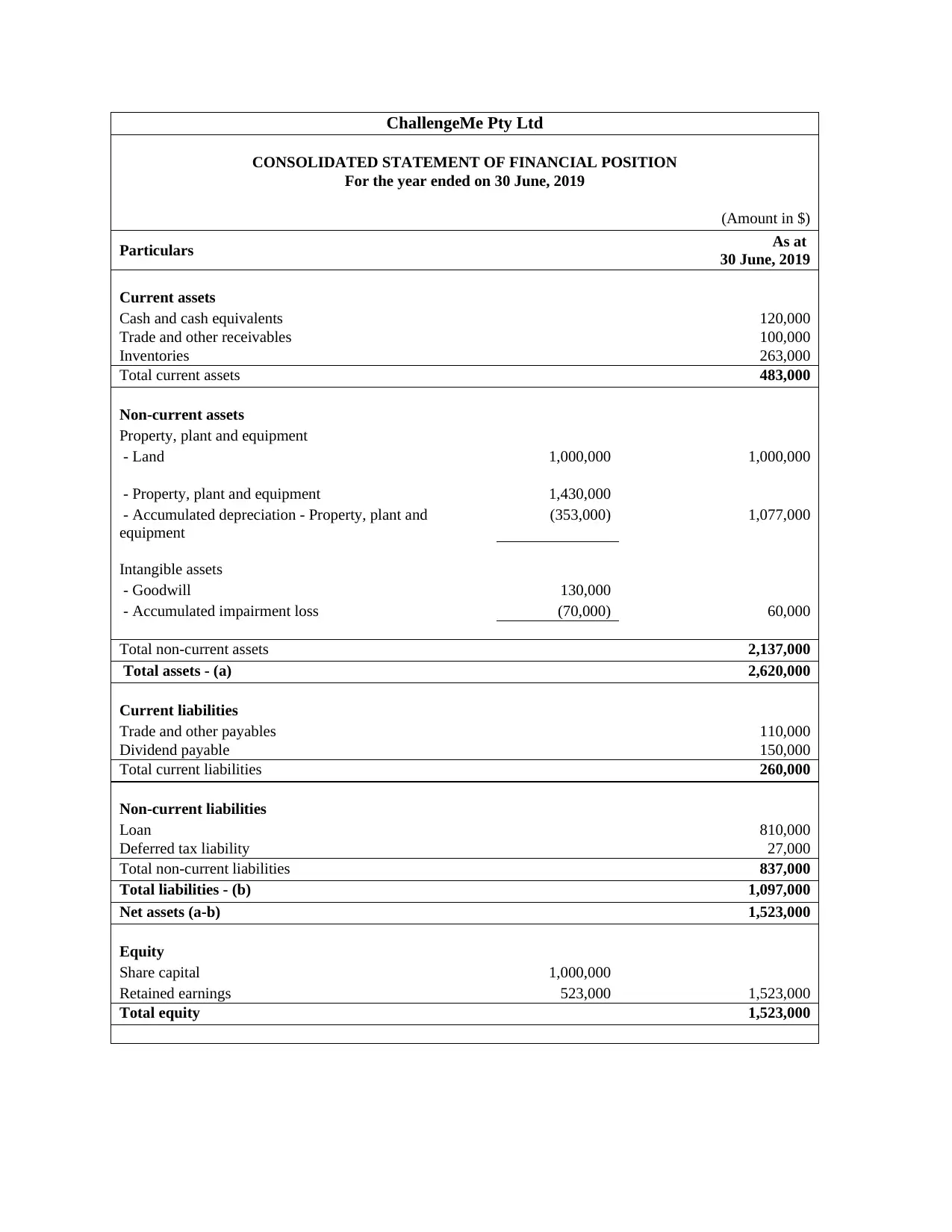

ChallengeMe Pty Ltd

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

For the year ended on 30 June, 2019

(Amount in $)

Particulars As at

30 June, 2019

Current assets

Cash and cash equivalents 120,000

Trade and other receivables 100,000

Inventories 263,000

Total current assets 483,000

Non-current assets

Property, plant and equipment

- Land 1,000,000 1,000,000

- Property, plant and equipment 1,430,000

- Accumulated depreciation - Property, plant and

equipment

(353,000) 1,077,000

Intangible assets

- Goodwill 130,000

- Accumulated impairment loss (70,000) 60,000

Total non-current assets 2,137,000

Total assets - (a) 2,620,000

Current liabilities

Trade and other payables 110,000

Dividend payable 150,000

Total current liabilities 260,000

Non-current liabilities

Loan 810,000

Deferred tax liability 27,000

Total non-current liabilities 837,000

Total liabilities - (b) 1,097,000

Net assets (a-b) 1,523,000

Equity

Share capital 1,000,000

Retained earnings 523,000 1,523,000

Total equity 1,523,000

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

For the year ended on 30 June, 2019

(Amount in $)

Particulars As at

30 June, 2019

Current assets

Cash and cash equivalents 120,000

Trade and other receivables 100,000

Inventories 263,000

Total current assets 483,000

Non-current assets

Property, plant and equipment

- Land 1,000,000 1,000,000

- Property, plant and equipment 1,430,000

- Accumulated depreciation - Property, plant and

equipment

(353,000) 1,077,000

Intangible assets

- Goodwill 130,000

- Accumulated impairment loss (70,000) 60,000

Total non-current assets 2,137,000

Total assets - (a) 2,620,000

Current liabilities

Trade and other payables 110,000

Dividend payable 150,000

Total current liabilities 260,000

Non-current liabilities

Loan 810,000

Deferred tax liability 27,000

Total non-current liabilities 837,000

Total liabilities - (b) 1,097,000

Net assets (a-b) 1,523,000

Equity

Share capital 1,000,000

Retained earnings 523,000 1,523,000

Total equity 1,523,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

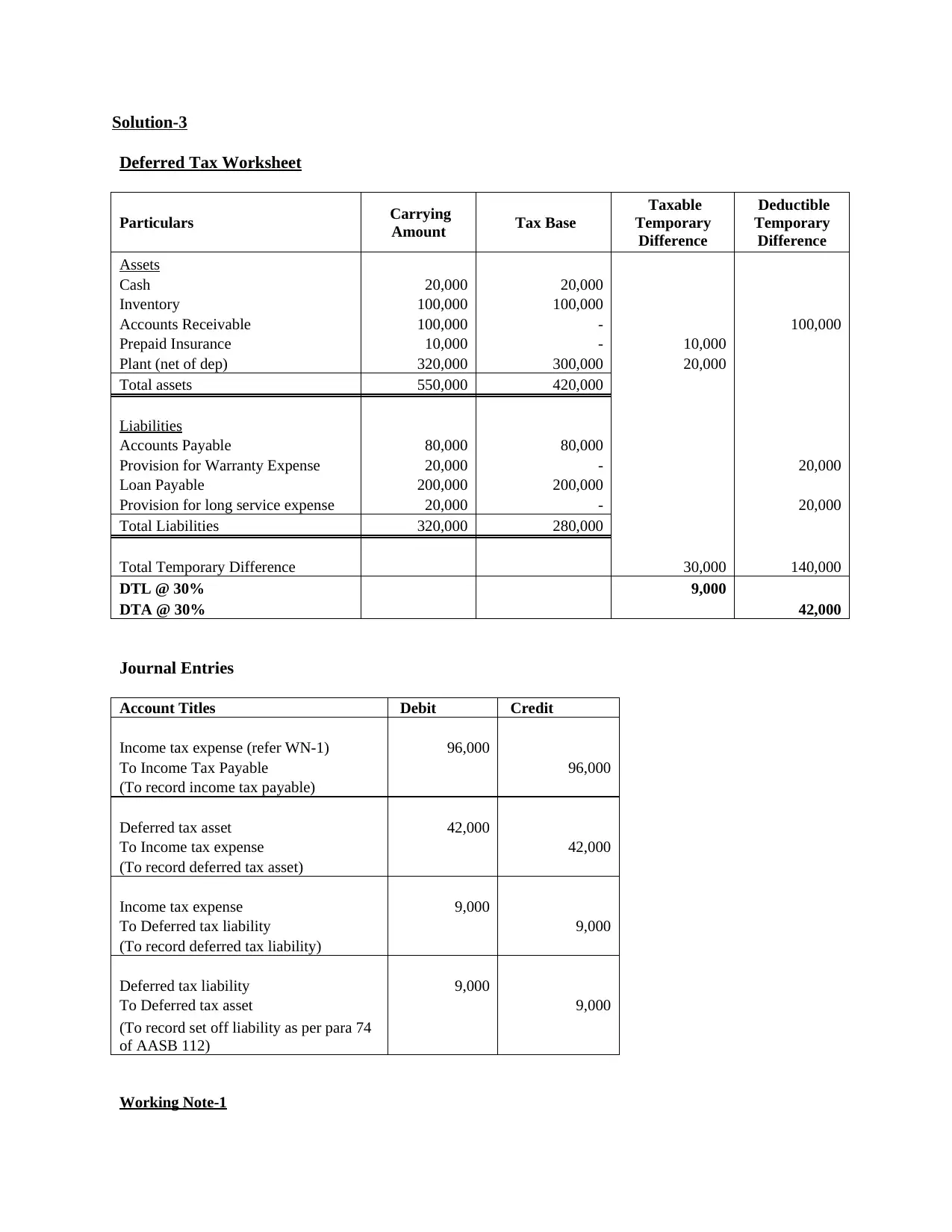

Solution-3

Deferred Tax Worksheet

Particulars Carrying

Amount Tax Base

Taxable

Temporary

Difference

Deductible

Temporary

Difference

Assets

Cash 20,000 20,000

Inventory 100,000 100,000

Accounts Receivable 100,000 - 100,000

Prepaid Insurance 10,000 - 10,000

Plant (net of dep) 320,000 300,000 20,000

Total assets 550,000 420,000

Liabilities

Accounts Payable 80,000 80,000

Provision for Warranty Expense 20,000 - 20,000

Loan Payable 200,000 200,000

Provision for long service expense 20,000 - 20,000

Total Liabilities 320,000 280,000

Total Temporary Difference 30,000 140,000

DTL @ 30% 9,000

DTA @ 30% 42,000

Journal Entries

Account Titles Debit Credit

Income tax expense (refer WN-1) 96,000

To Income Tax Payable 96,000

(To record income tax payable)

Deferred tax asset 42,000

To Income tax expense 42,000

(To record deferred tax asset)

Income tax expense 9,000

To Deferred tax liability 9,000

(To record deferred tax liability)

Deferred tax liability 9,000

To Deferred tax asset 9,000

(To record set off liability as per para 74

of AASB 112)

Working Note-1

Deferred Tax Worksheet

Particulars Carrying

Amount Tax Base

Taxable

Temporary

Difference

Deductible

Temporary

Difference

Assets

Cash 20,000 20,000

Inventory 100,000 100,000

Accounts Receivable 100,000 - 100,000

Prepaid Insurance 10,000 - 10,000

Plant (net of dep) 320,000 300,000 20,000

Total assets 550,000 420,000

Liabilities

Accounts Payable 80,000 80,000

Provision for Warranty Expense 20,000 - 20,000

Loan Payable 200,000 200,000

Provision for long service expense 20,000 - 20,000

Total Liabilities 320,000 280,000

Total Temporary Difference 30,000 140,000

DTL @ 30% 9,000

DTA @ 30% 42,000

Journal Entries

Account Titles Debit Credit

Income tax expense (refer WN-1) 96,000

To Income Tax Payable 96,000

(To record income tax payable)

Deferred tax asset 42,000

To Income tax expense 42,000

(To record deferred tax asset)

Income tax expense 9,000

To Deferred tax liability 9,000

(To record deferred tax liability)

Deferred tax liability 9,000

To Deferred tax asset 9,000

(To record set off liability as per para 74

of AASB 112)

Working Note-1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

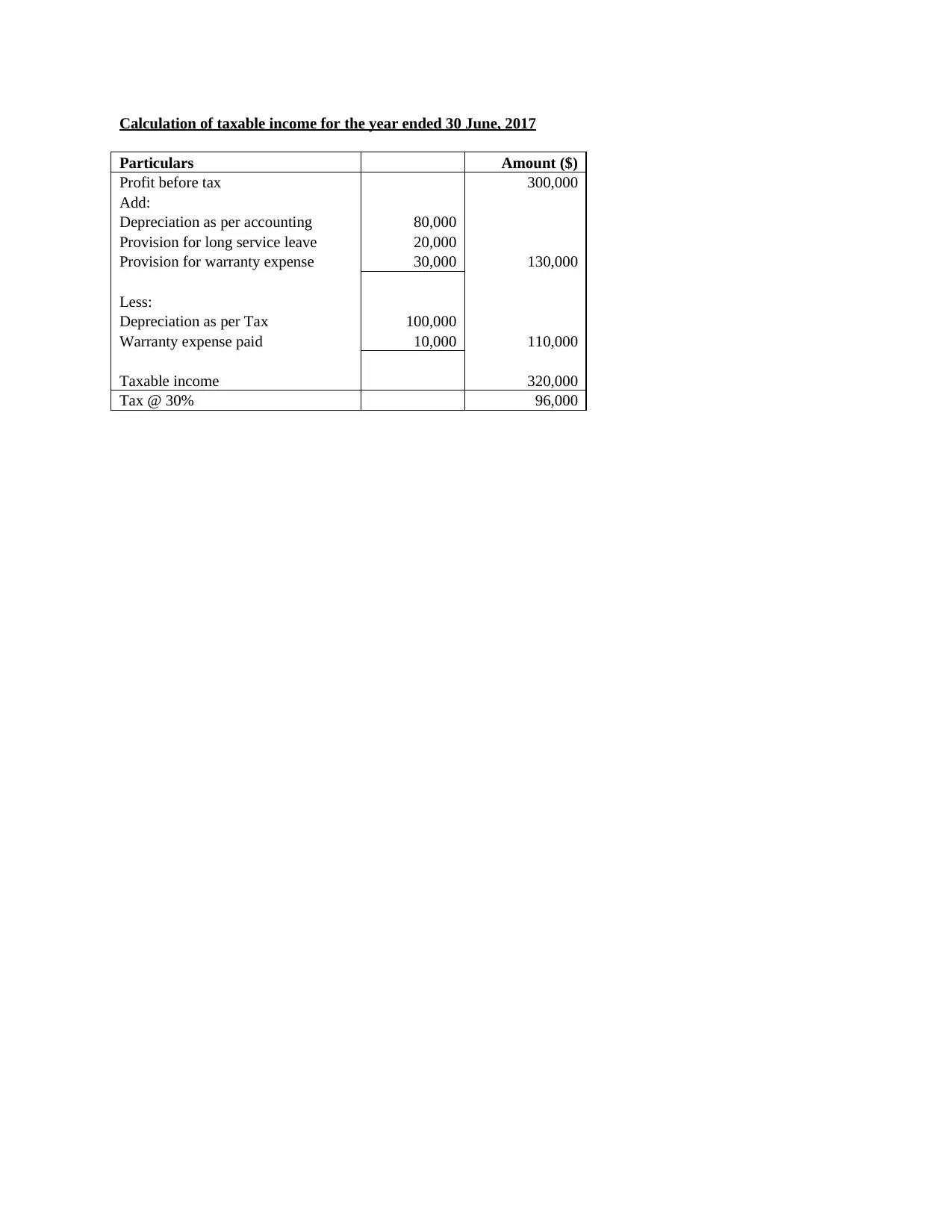

Calculation of taxable income for the year ended 30 June, 2017

Particulars Amount ($)

Profit before tax 300,000

Add:

Depreciation as per accounting 80,000

Provision for long service leave 20,000

Provision for warranty expense 30,000 130,000

Less:

Depreciation as per Tax 100,000

Warranty expense paid 10,000 110,000

Taxable income 320,000

Tax @ 30% 96,000

Particulars Amount ($)

Profit before tax 300,000

Add:

Depreciation as per accounting 80,000

Provision for long service leave 20,000

Provision for warranty expense 30,000 130,000

Less:

Depreciation as per Tax 100,000

Warranty expense paid 10,000 110,000

Taxable income 320,000

Tax @ 30% 96,000

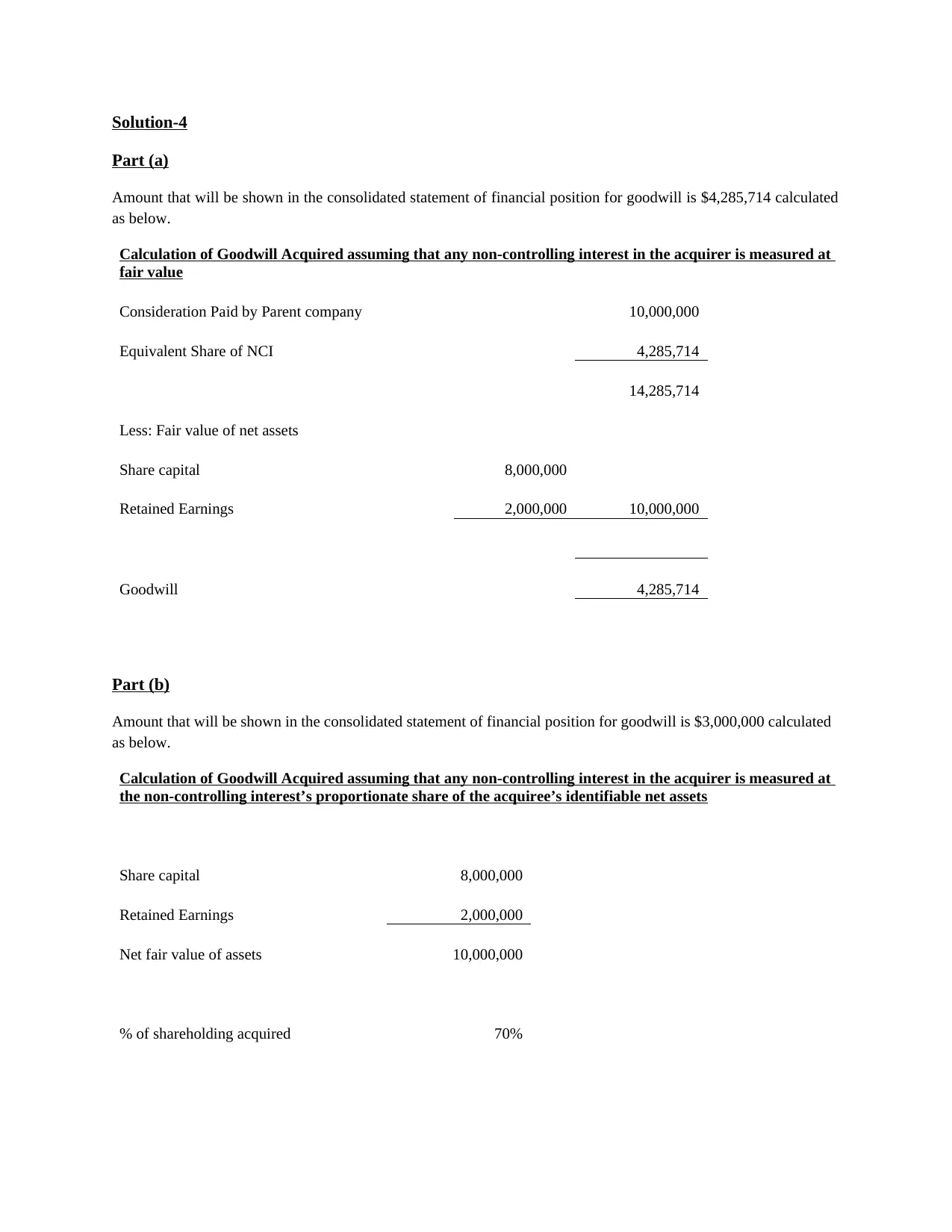

Solution-4

Part (a)

Amount that will be shown in the consolidated statement of financial position for goodwill is $4,285,714 calculated

as below.

Calculation of Goodwill Acquired assuming that any non-controlling interest in the acquirer is measured at

fair value

Consideration Paid by Parent company 10,000,000

Equivalent Share of NCI 4,285,714

14,285,714

Less: Fair value of net assets

Share capital 8,000,000

Retained Earnings 2,000,000 10,000,000

Goodwill 4,285,714

Part (b)

Amount that will be shown in the consolidated statement of financial position for goodwill is $3,000,000 calculated

as below.

Calculation of Goodwill Acquired assuming that any non-controlling interest in the acquirer is measured at

the non-controlling interest’s proportionate share of the acquiree’s identifiable net assets

Share capital 8,000,000

Retained Earnings 2,000,000

Net fair value of assets 10,000,000

% of shareholding acquired 70%

Part (a)

Amount that will be shown in the consolidated statement of financial position for goodwill is $4,285,714 calculated

as below.

Calculation of Goodwill Acquired assuming that any non-controlling interest in the acquirer is measured at

fair value

Consideration Paid by Parent company 10,000,000

Equivalent Share of NCI 4,285,714

14,285,714

Less: Fair value of net assets

Share capital 8,000,000

Retained Earnings 2,000,000 10,000,000

Goodwill 4,285,714

Part (b)

Amount that will be shown in the consolidated statement of financial position for goodwill is $3,000,000 calculated

as below.

Calculation of Goodwill Acquired assuming that any non-controlling interest in the acquirer is measured at

the non-controlling interest’s proportionate share of the acquiree’s identifiable net assets

Share capital 8,000,000

Retained Earnings 2,000,000

Net fair value of assets 10,000,000

% of shareholding acquired 70%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

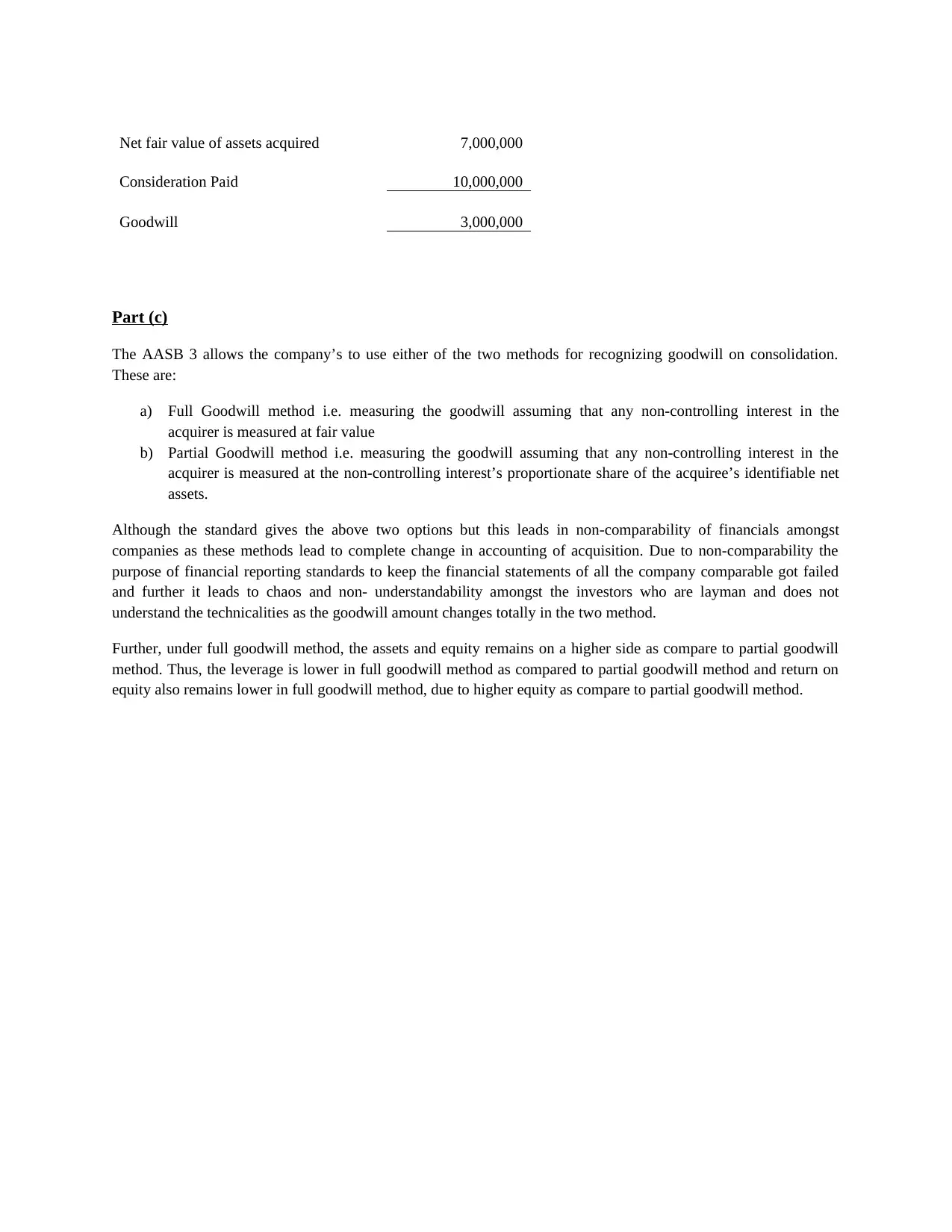

Net fair value of assets acquired 7,000,000

Consideration Paid 10,000,000

Goodwill 3,000,000

Part (c)

The AASB 3 allows the company’s to use either of the two methods for recognizing goodwill on consolidation.

These are:

a) Full Goodwill method i.e. measuring the goodwill assuming that any non-controlling interest in the

acquirer is measured at fair value

b) Partial Goodwill method i.e. measuring the goodwill assuming that any non-controlling interest in the

acquirer is measured at the non-controlling interest’s proportionate share of the acquiree’s identifiable net

assets.

Although the standard gives the above two options but this leads in non-comparability of financials amongst

companies as these methods lead to complete change in accounting of acquisition. Due to non-comparability the

purpose of financial reporting standards to keep the financial statements of all the company comparable got failed

and further it leads to chaos and non- understandability amongst the investors who are layman and does not

understand the technicalities as the goodwill amount changes totally in the two method.

Further, under full goodwill method, the assets and equity remains on a higher side as compare to partial goodwill

method. Thus, the leverage is lower in full goodwill method as compared to partial goodwill method and return on

equity also remains lower in full goodwill method, due to higher equity as compare to partial goodwill method.

Consideration Paid 10,000,000

Goodwill 3,000,000

Part (c)

The AASB 3 allows the company’s to use either of the two methods for recognizing goodwill on consolidation.

These are:

a) Full Goodwill method i.e. measuring the goodwill assuming that any non-controlling interest in the

acquirer is measured at fair value

b) Partial Goodwill method i.e. measuring the goodwill assuming that any non-controlling interest in the

acquirer is measured at the non-controlling interest’s proportionate share of the acquiree’s identifiable net

assets.

Although the standard gives the above two options but this leads in non-comparability of financials amongst

companies as these methods lead to complete change in accounting of acquisition. Due to non-comparability the

purpose of financial reporting standards to keep the financial statements of all the company comparable got failed

and further it leads to chaos and non- understandability amongst the investors who are layman and does not

understand the technicalities as the goodwill amount changes totally in the two method.

Further, under full goodwill method, the assets and equity remains on a higher side as compare to partial goodwill

method. Thus, the leverage is lower in full goodwill method as compared to partial goodwill method and return on

equity also remains lower in full goodwill method, due to higher equity as compare to partial goodwill method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

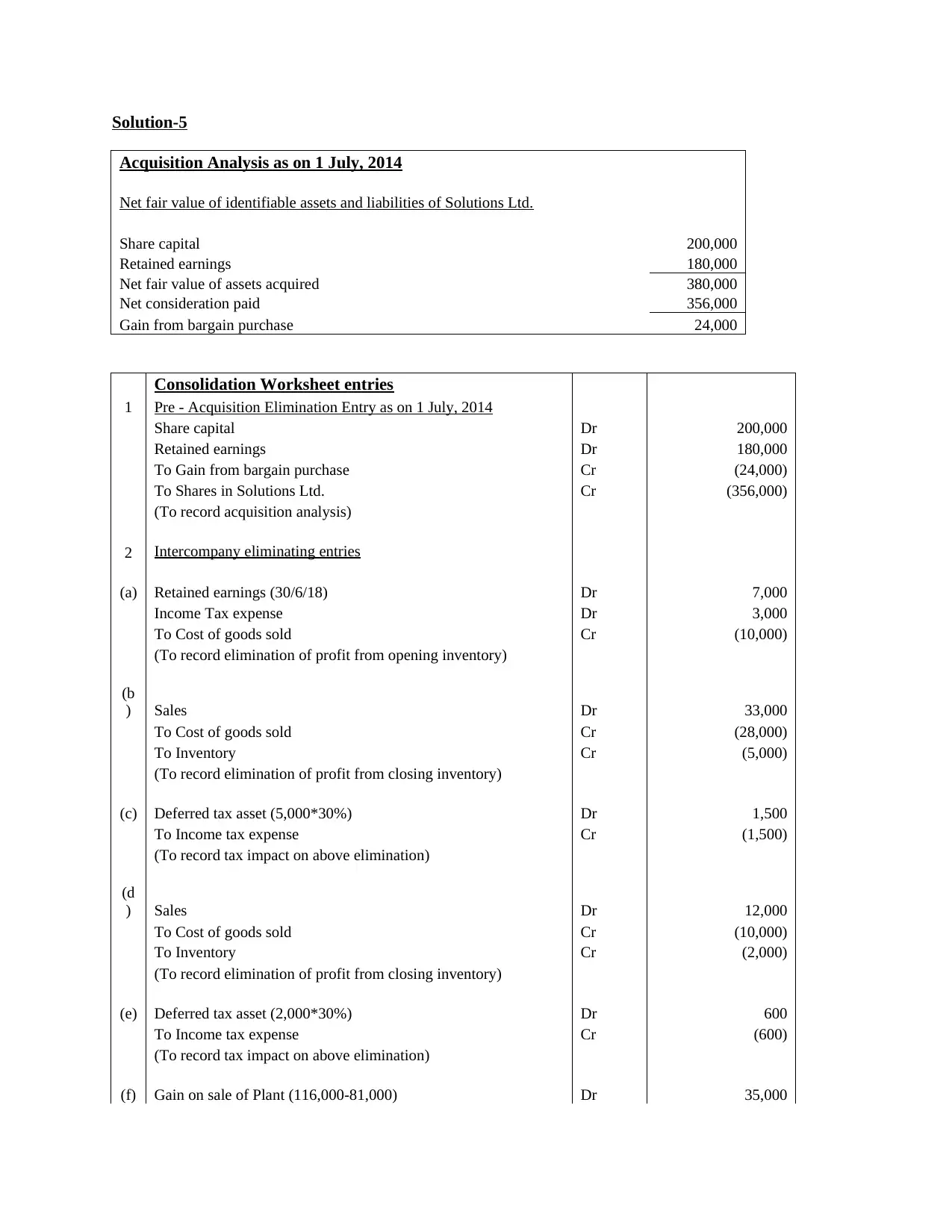

Solution-5

Acquisition Analysis as on 1 July, 2014

Net fair value of identifiable assets and liabilities of Solutions Ltd.

Share capital 200,000

Retained earnings 180,000

Net fair value of assets acquired 380,000

Net consideration paid 356,000

Gain from bargain purchase 24,000

Consolidation Worksheet entries

1 Pre - Acquisition Elimination Entry as on 1 July, 2014

Share capital Dr 200,000

Retained earnings Dr 180,000

To Gain from bargain purchase Cr (24,000)

To Shares in Solutions Ltd. Cr (356,000)

(To record acquisition analysis)

2 Intercompany eliminating entries

(a) Retained earnings (30/6/18) Dr 7,000

Income Tax expense Dr 3,000

To Cost of goods sold Cr (10,000)

(To record elimination of profit from opening inventory)

(b

) Sales Dr 33,000

To Cost of goods sold Cr (28,000)

To Inventory Cr (5,000)

(To record elimination of profit from closing inventory)

(c) Deferred tax asset (5,000*30%) Dr 1,500

To Income tax expense Cr (1,500)

(To record tax impact on above elimination)

(d

) Sales Dr 12,000

To Cost of goods sold Cr (10,000)

To Inventory Cr (2,000)

(To record elimination of profit from closing inventory)

(e) Deferred tax asset (2,000*30%) Dr 600

To Income tax expense Cr (600)

(To record tax impact on above elimination)

(f) Gain on sale of Plant (116,000-81,000) Dr 35,000

Acquisition Analysis as on 1 July, 2014

Net fair value of identifiable assets and liabilities of Solutions Ltd.

Share capital 200,000

Retained earnings 180,000

Net fair value of assets acquired 380,000

Net consideration paid 356,000

Gain from bargain purchase 24,000

Consolidation Worksheet entries

1 Pre - Acquisition Elimination Entry as on 1 July, 2014

Share capital Dr 200,000

Retained earnings Dr 180,000

To Gain from bargain purchase Cr (24,000)

To Shares in Solutions Ltd. Cr (356,000)

(To record acquisition analysis)

2 Intercompany eliminating entries

(a) Retained earnings (30/6/18) Dr 7,000

Income Tax expense Dr 3,000

To Cost of goods sold Cr (10,000)

(To record elimination of profit from opening inventory)

(b

) Sales Dr 33,000

To Cost of goods sold Cr (28,000)

To Inventory Cr (5,000)

(To record elimination of profit from closing inventory)

(c) Deferred tax asset (5,000*30%) Dr 1,500

To Income tax expense Cr (1,500)

(To record tax impact on above elimination)

(d

) Sales Dr 12,000

To Cost of goods sold Cr (10,000)

To Inventory Cr (2,000)

(To record elimination of profit from closing inventory)

(e) Deferred tax asset (2,000*30%) Dr 600

To Income tax expense Cr (600)

(To record tax impact on above elimination)

(f) Gain on sale of Plant (116,000-81,000) Dr 35,000

Plant Cr (35,000)

(To record elimination of gain on sale of plant)

(g

) Deferred tax asset (35,000*30%) Dr 10,500

To Income tax expense Cr (10,500)

(To record tax impact on above elimination)

(h

) Accumulated Depreciation - Plant (35,000/6) Dr 5,833

To Depreciation expense Cr (5,833)

(To record elimination of depreciation on excess amount)

(i) Management fee revenue Dr 26,500

To Management fee expenses Cr (26,500)

(To eliminate the management fee incomes and expenses)

(j) Dividends received from Solutions Ltd Dr 93,000

To Dividend Paid Cr (93,000)

(To record inter-company elimination of dividend)

(To record elimination of gain on sale of plant)

(g

) Deferred tax asset (35,000*30%) Dr 10,500

To Income tax expense Cr (10,500)

(To record tax impact on above elimination)

(h

) Accumulated Depreciation - Plant (35,000/6) Dr 5,833

To Depreciation expense Cr (5,833)

(To record elimination of depreciation on excess amount)

(i) Management fee revenue Dr 26,500

To Management fee expenses Cr (26,500)

(To eliminate the management fee incomes and expenses)

(j) Dividends received from Solutions Ltd Dr 93,000

To Dividend Paid Cr (93,000)

(To record inter-company elimination of dividend)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.