Loyola University SCPS Finance 371 Midterm Exam: Part 1 Analysis

VerifiedAdded on 2023/04/26

|2

|440

|427

Homework Assignment

AI Summary

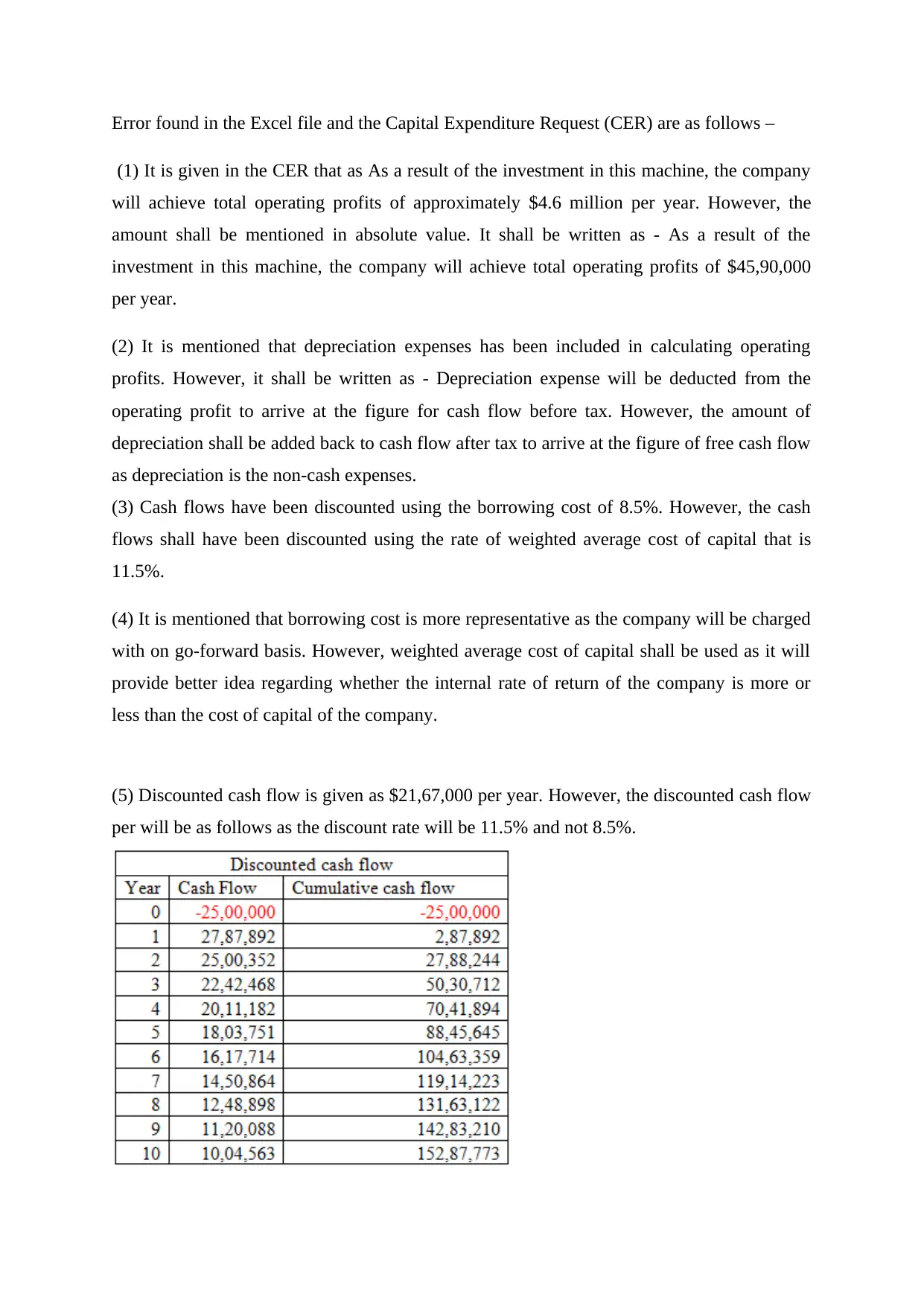

This assignment solution addresses a finance midterm exam from Loyola University of Chicago's SCPS Finance 371 course. The assignment requires the identification of errors in a Capital Expenditure Request (CER) and accompanying Excel spreadsheets related to a capital investment decision. The solution meticulously identifies ten key mistakes in the original CER and spreadsheet calculations, covering areas like operating profit presentation, depreciation handling, discount rate application (WACC vs. borrowing cost), and the calculation of discounted cash flow, payback periods, and internal rate of return. The provided solution includes a corrected Excel spreadsheet and a revised CER write-up reflecting the accurate calculations, ensuring financial metrics are correctly computed using the weighted average cost of capital (WACC) and proper accounting for depreciation. Furthermore, the solution presents detailed financial information, including machine costs, output calculations, and profit margins, all adjusted to reflect the corrected data.

1 out of 2

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.