Accounting and Finance: ACC System and Processes Homework Analysis

VerifiedAdded on 2021/05/31

|25

|3510

|82

Homework Assignment

AI Summary

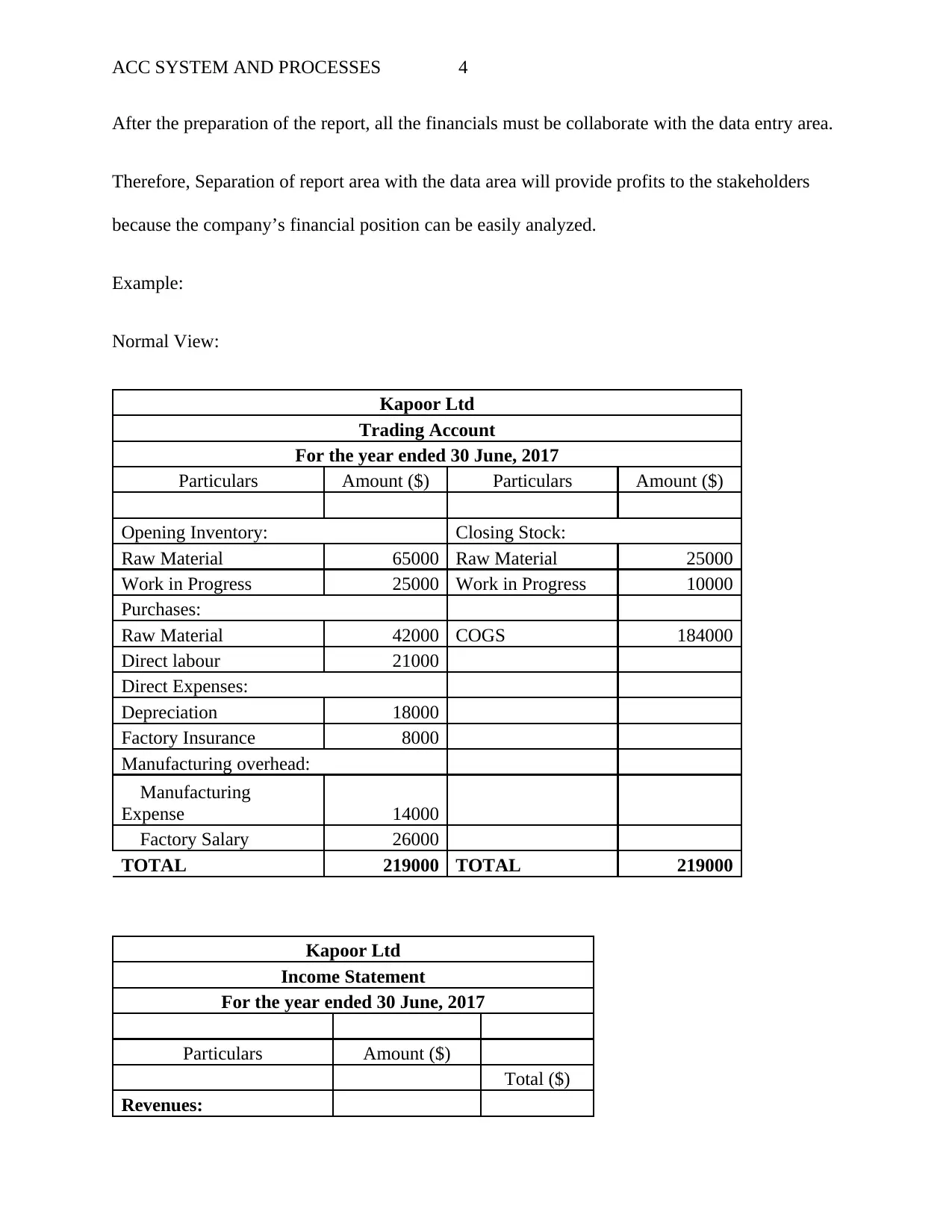

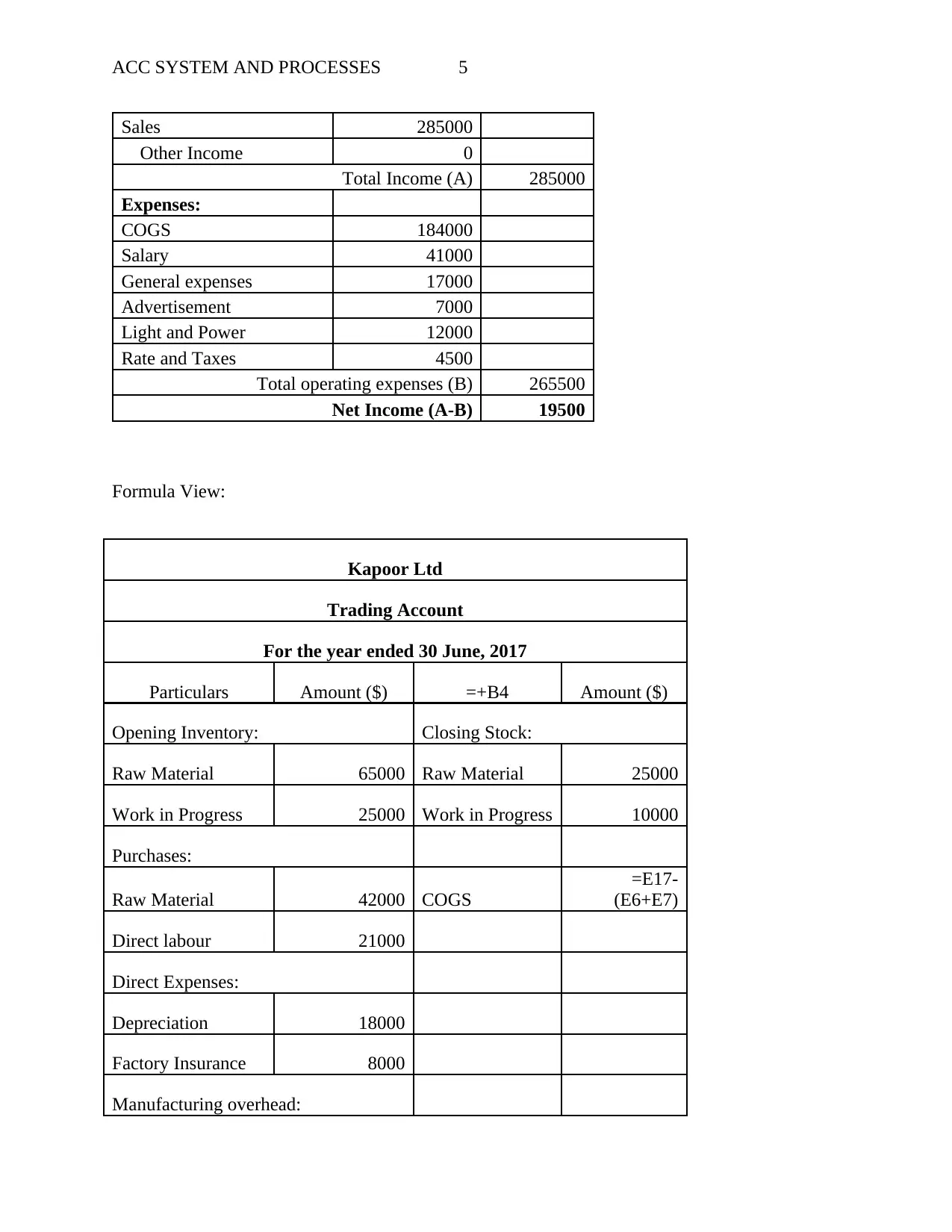

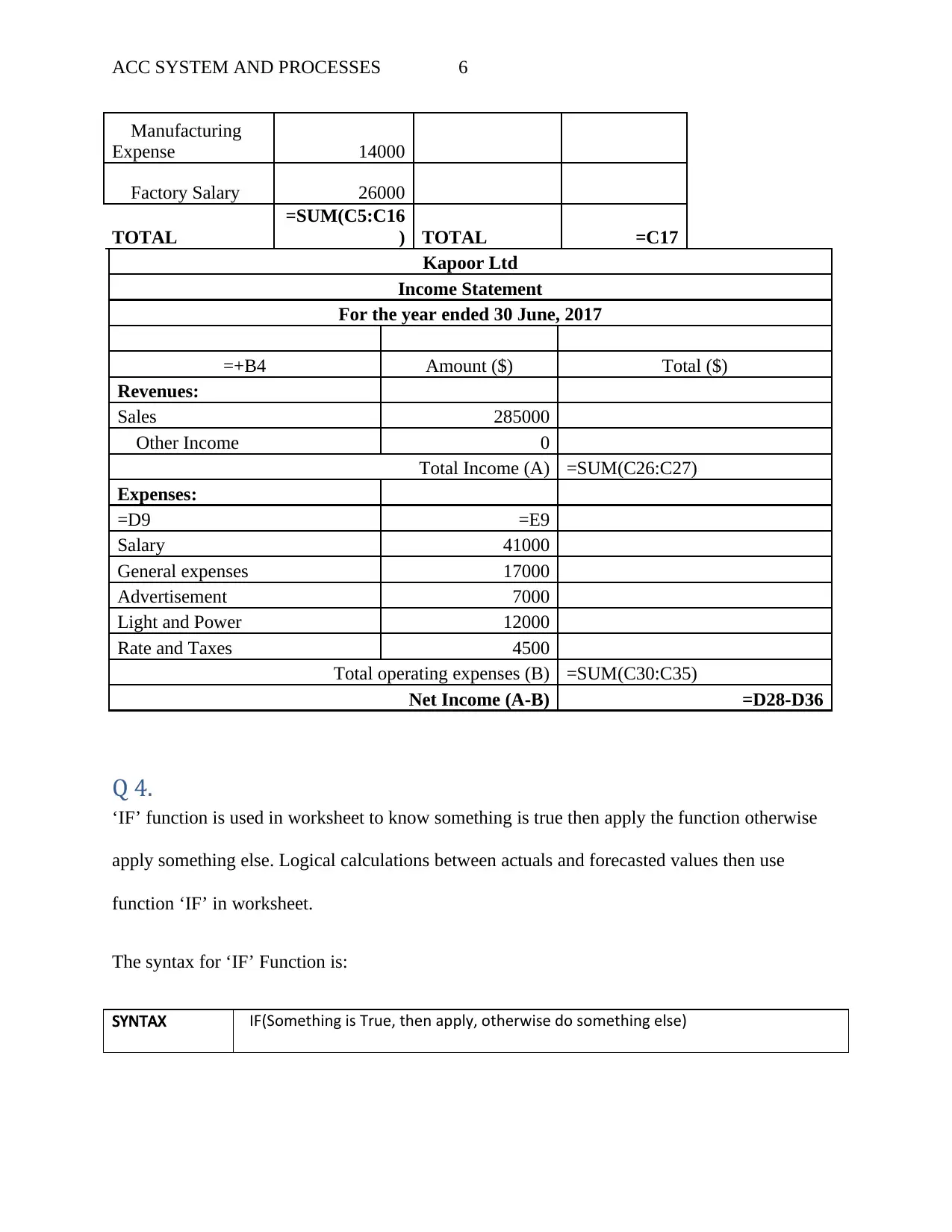

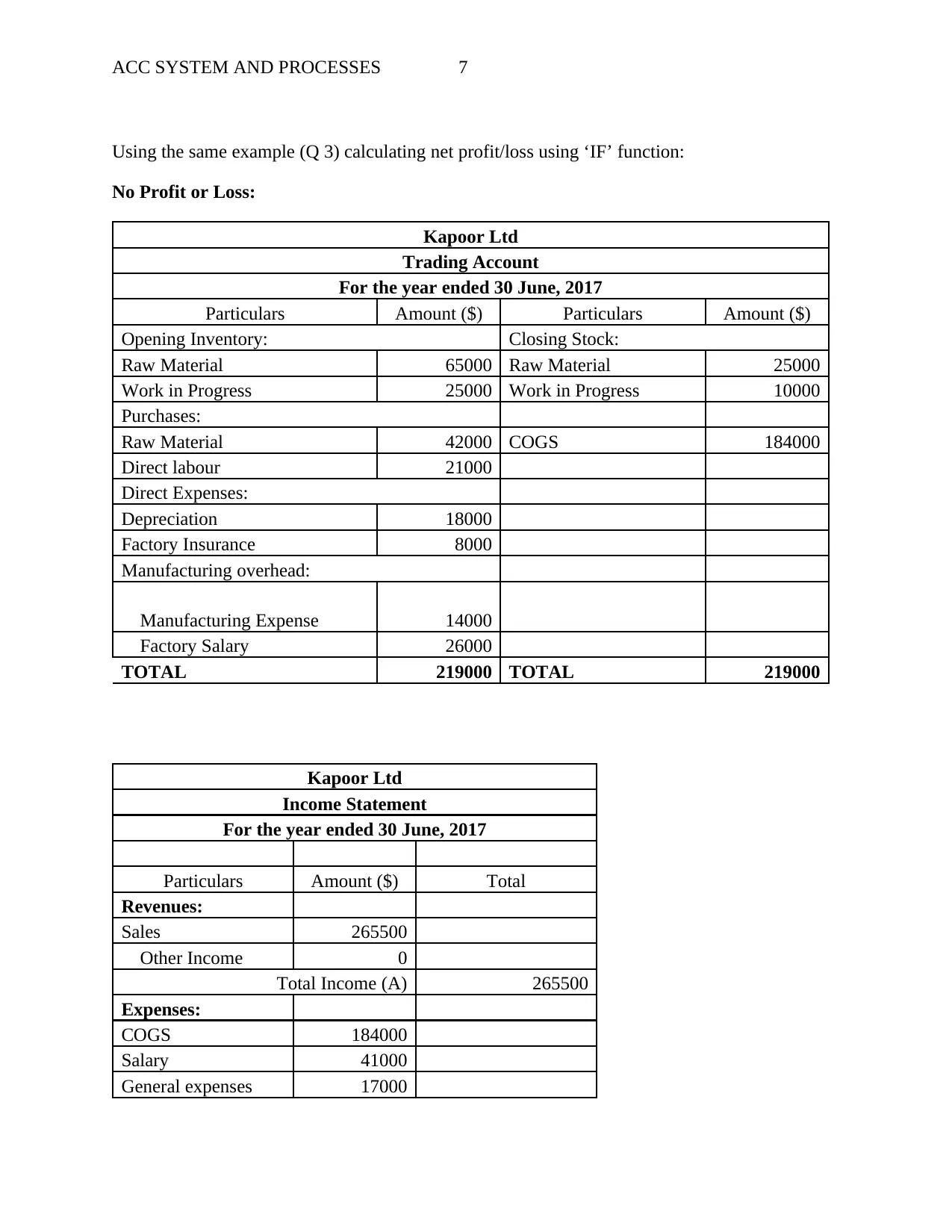

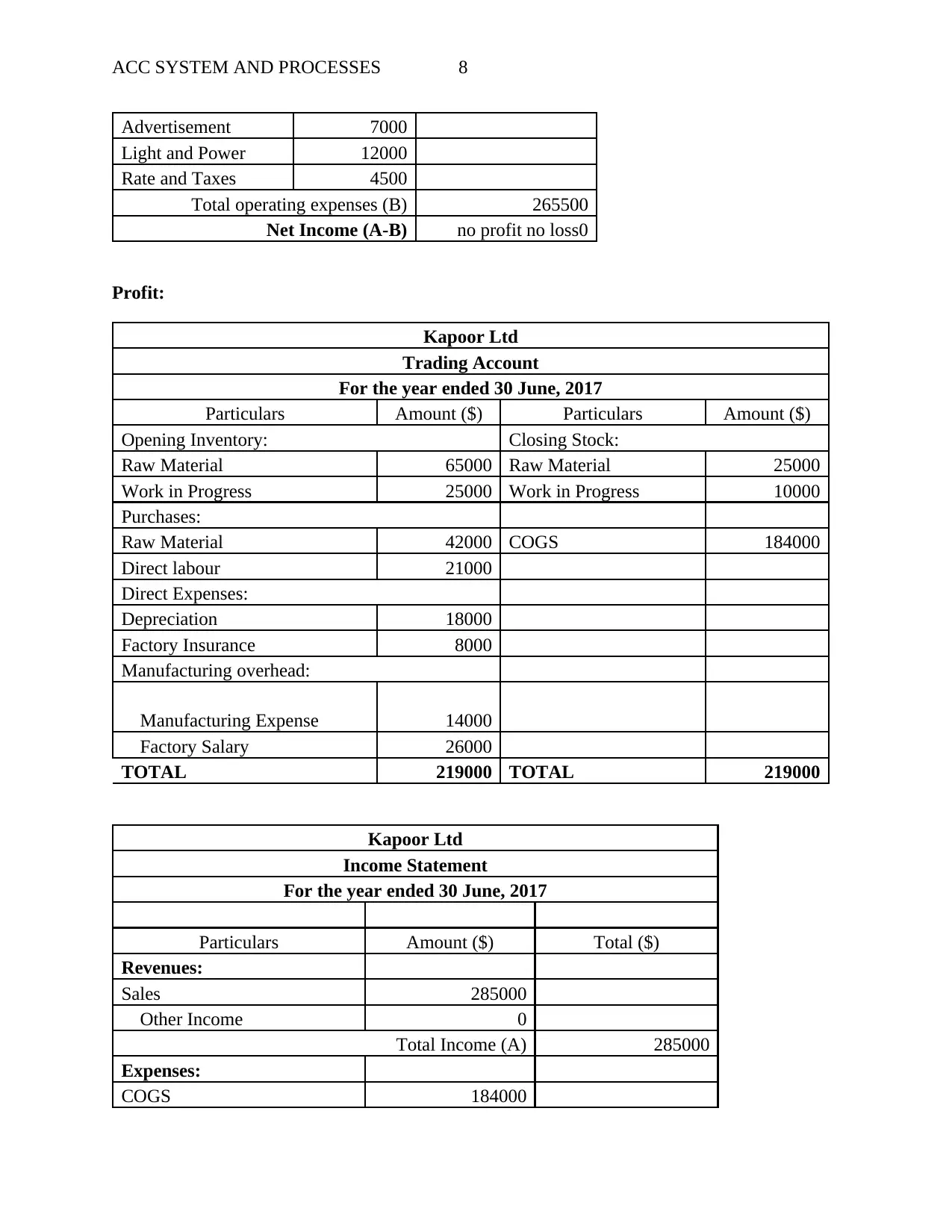

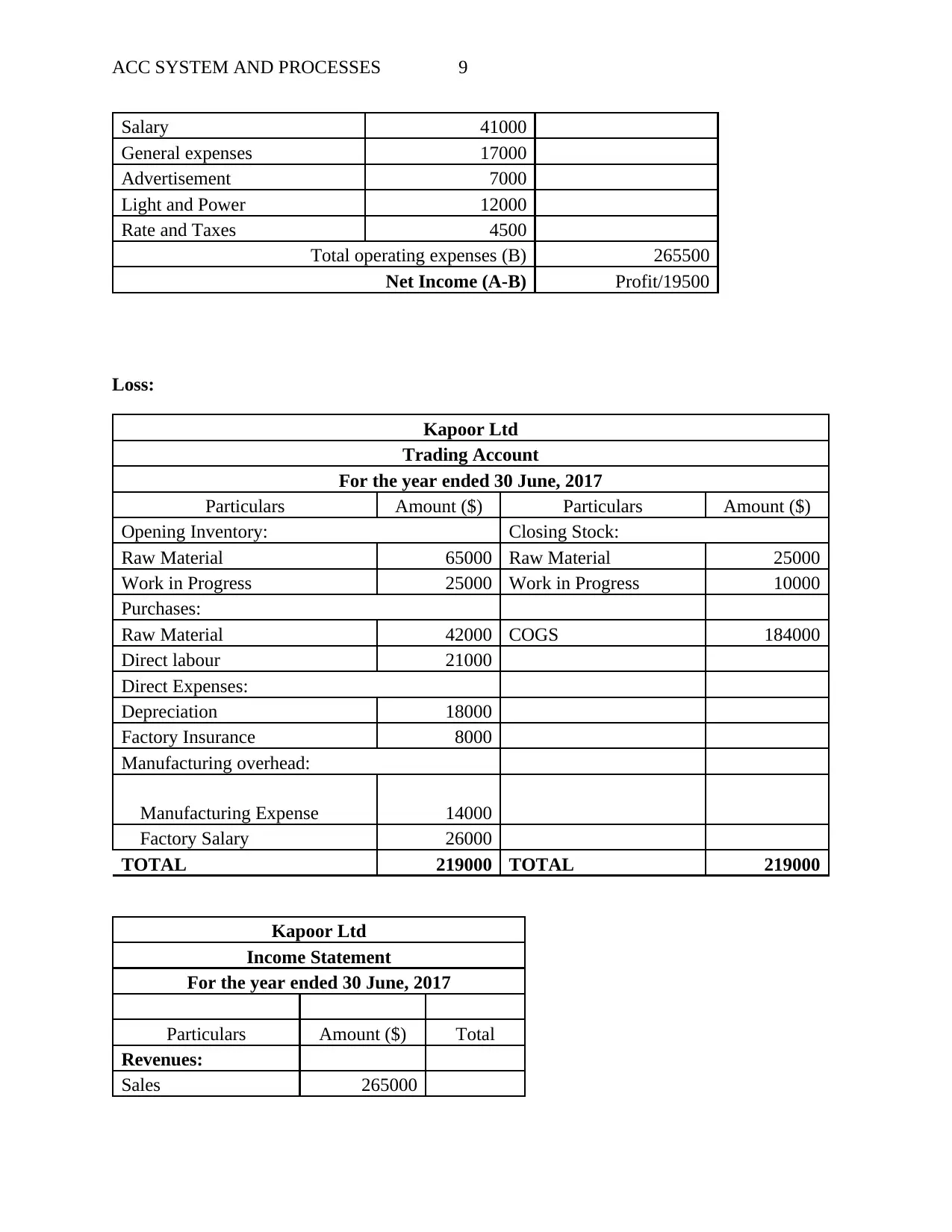

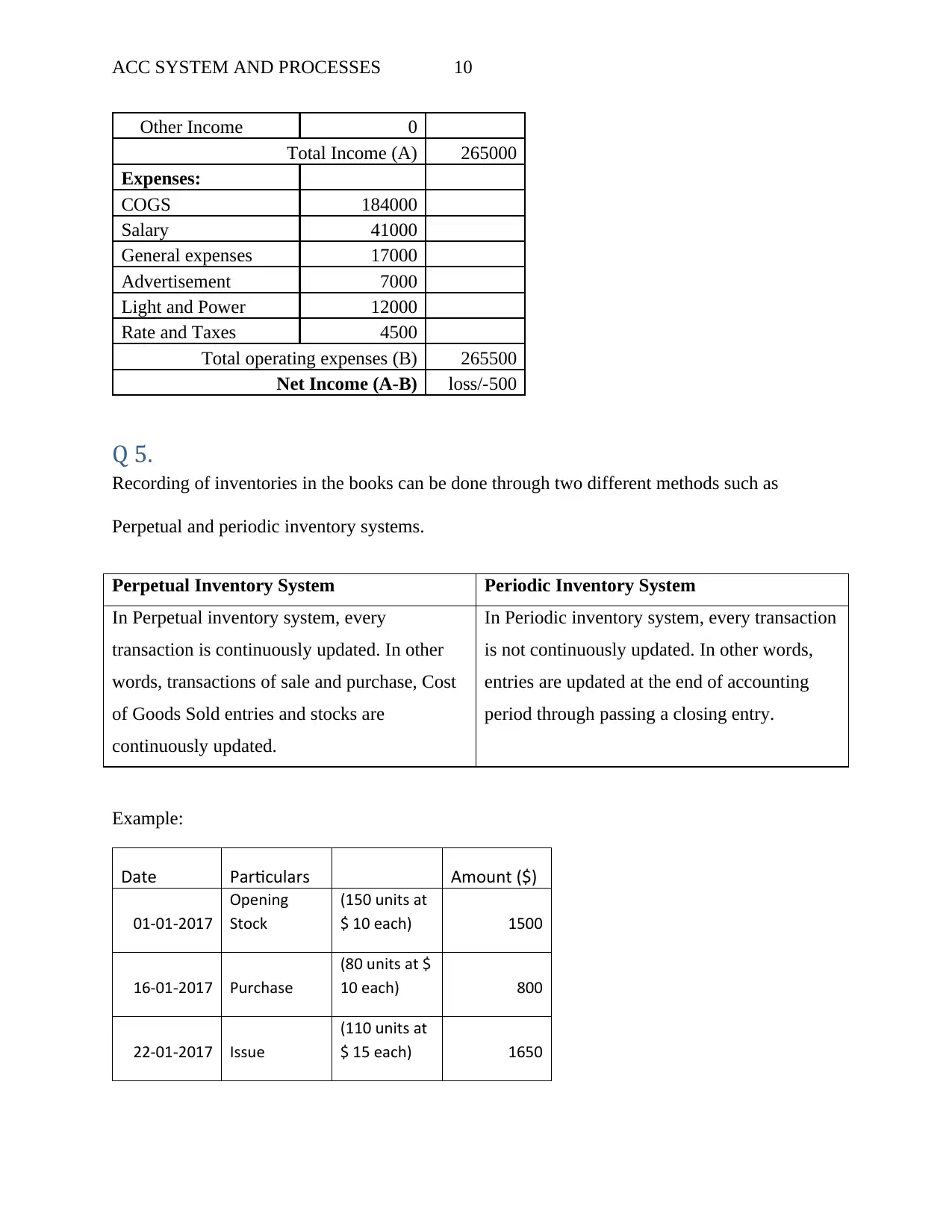

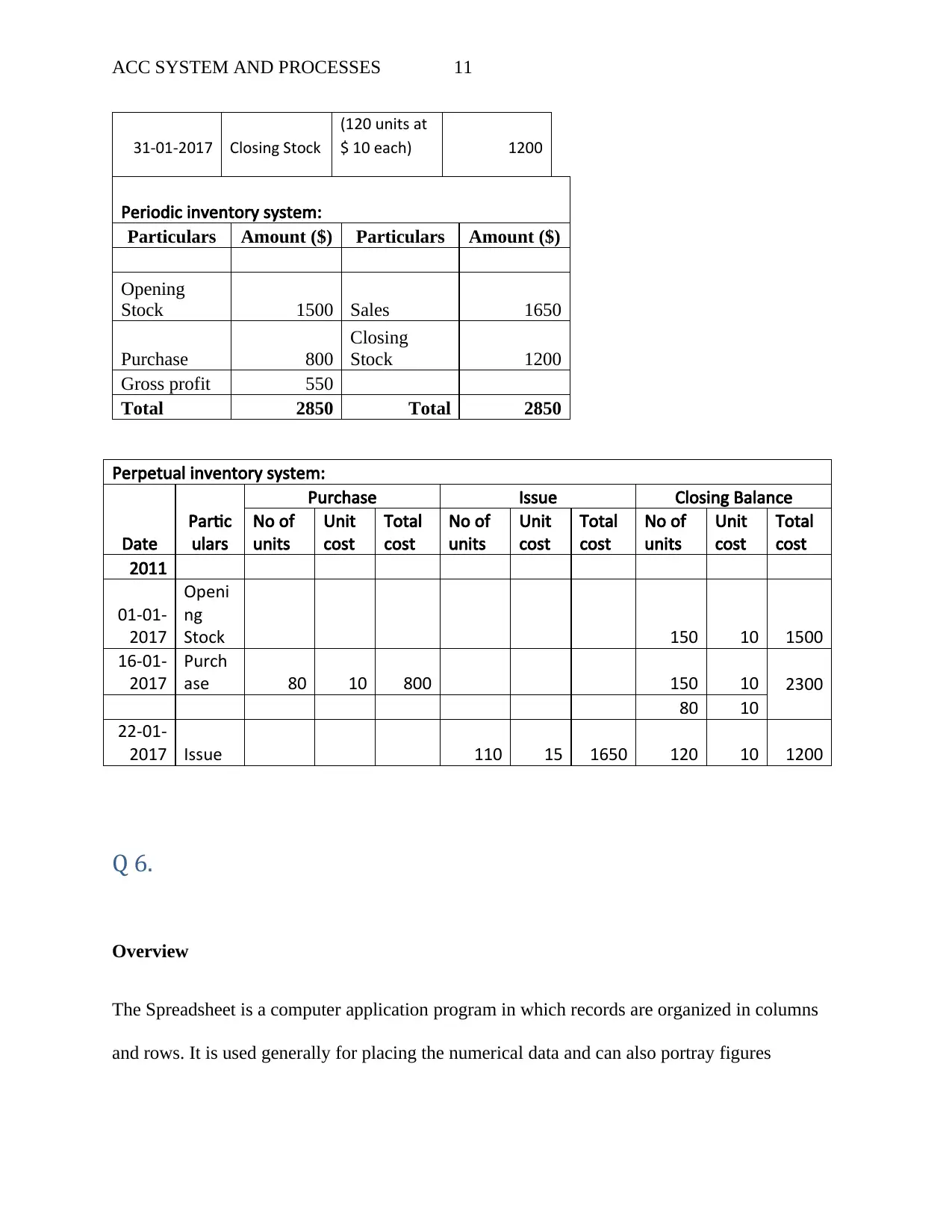

This homework assignment delves into accounting systems and processes, utilizing Microsoft Excel for financial analysis and reporting. The solution begins by explaining naming cell references and their application in calculating net profit. It then addresses the use of parentheses to denote negative figures in financial reports. The assignment further explores the benefits of separating data entry and report areas in accounting spreadsheets, including a detailed example of trading and income statements. The 'IF' function is demonstrated through a net profit/loss calculation. The solution also contrasts perpetual and periodic inventory systems, providing examples. Advantages and disadvantages of using spreadsheets in accounting are outlined, emphasizing accuracy and automation. Finally, the assignment covers inventory valuation methods, specifically average cost, FIFO (First-In, First-Out), and LIFO (Last-In, First-Out), with calculations for cost of goods sold and closing inventory values.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.