Financial Accounting and Reporting Assignment Solutions

VerifiedAdded on 2023/01/05

|11

|1360

|73

Homework Assignment

AI Summary

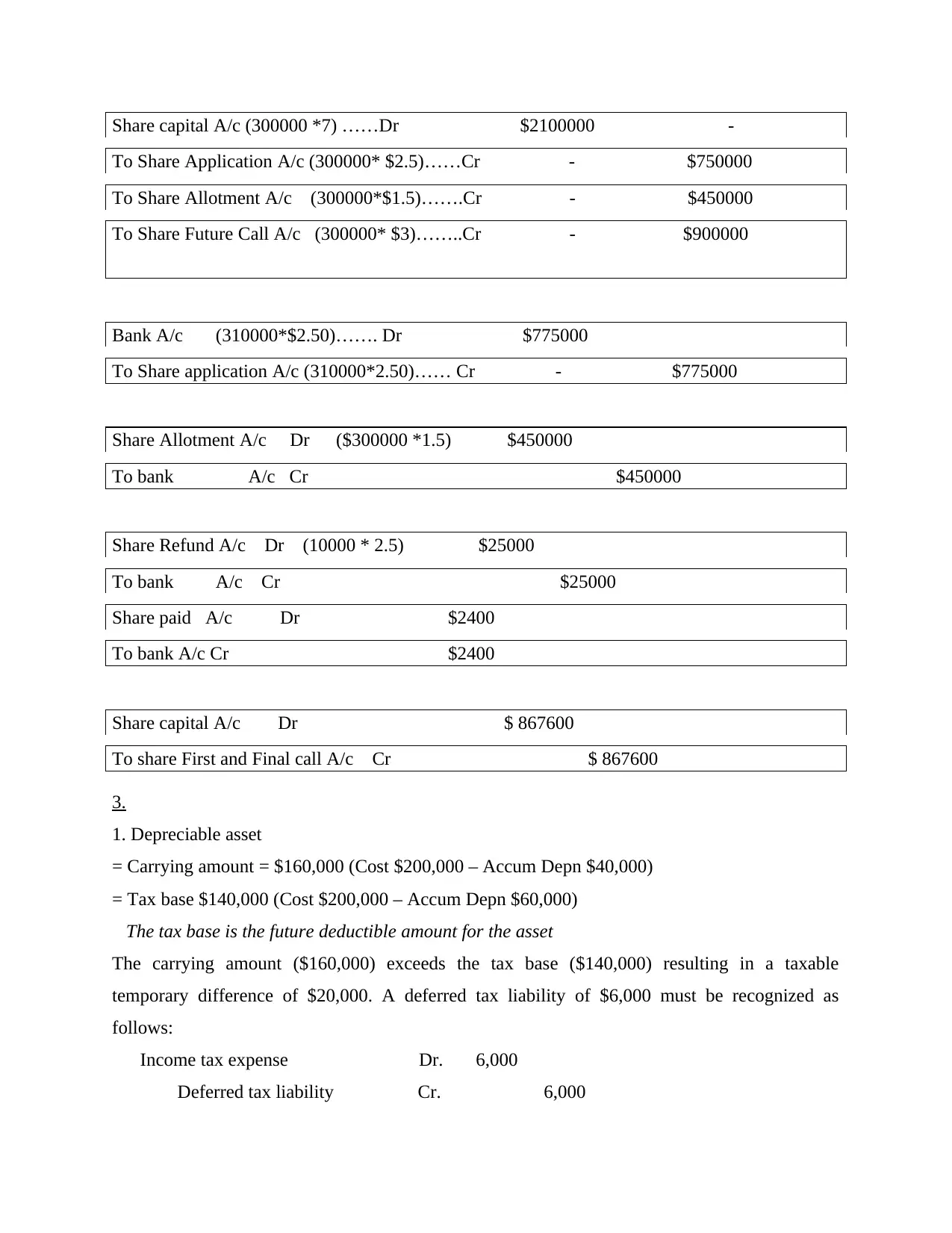

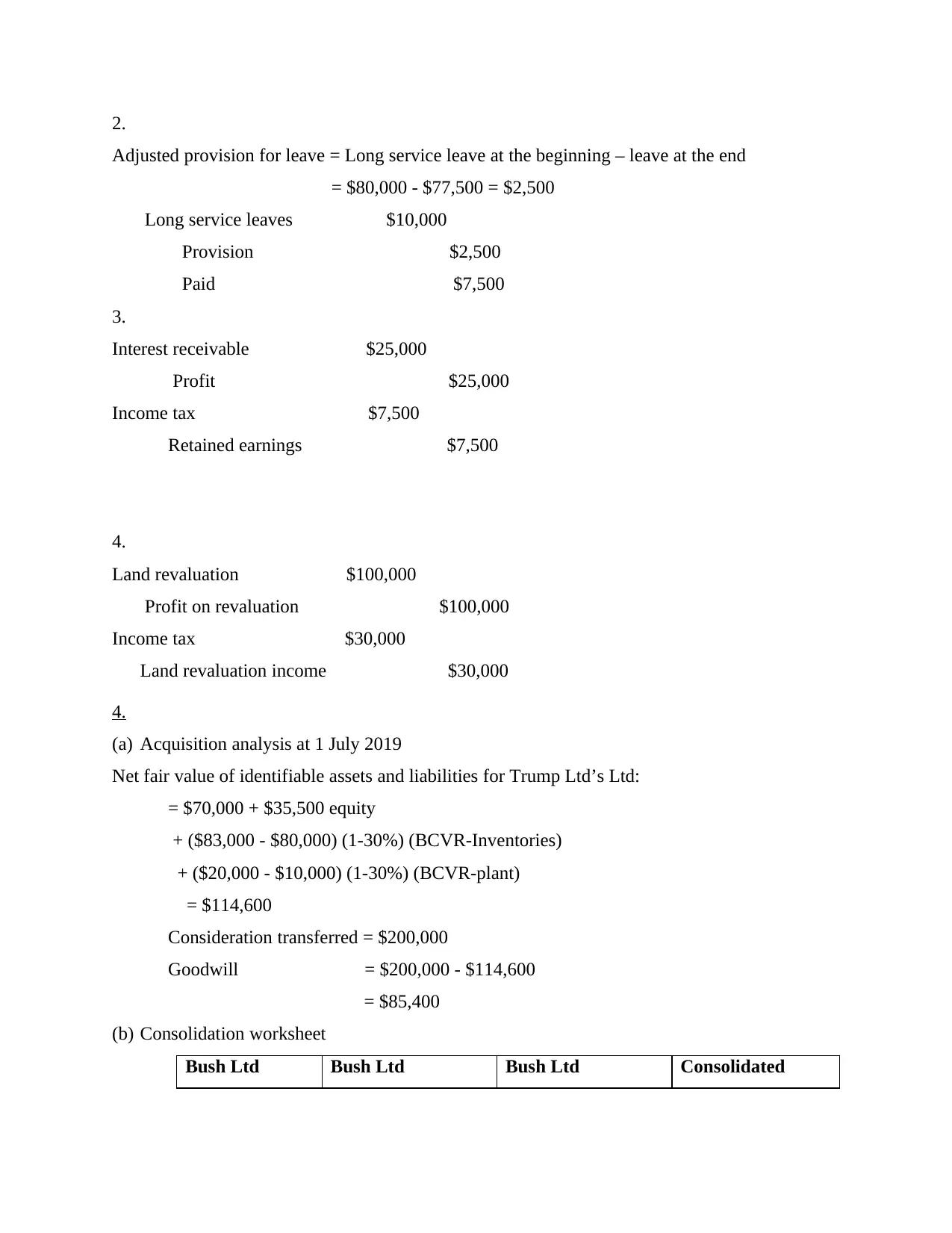

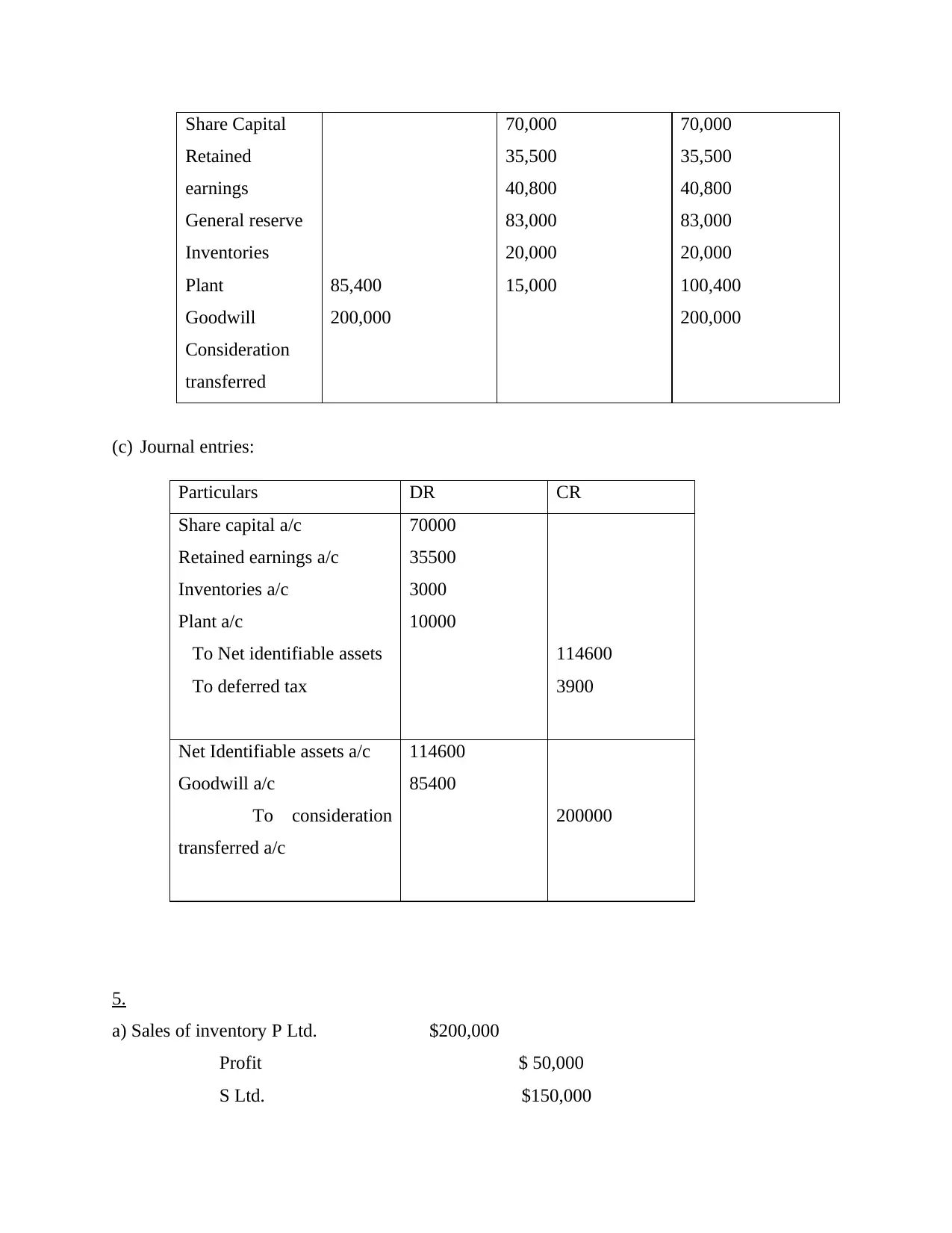

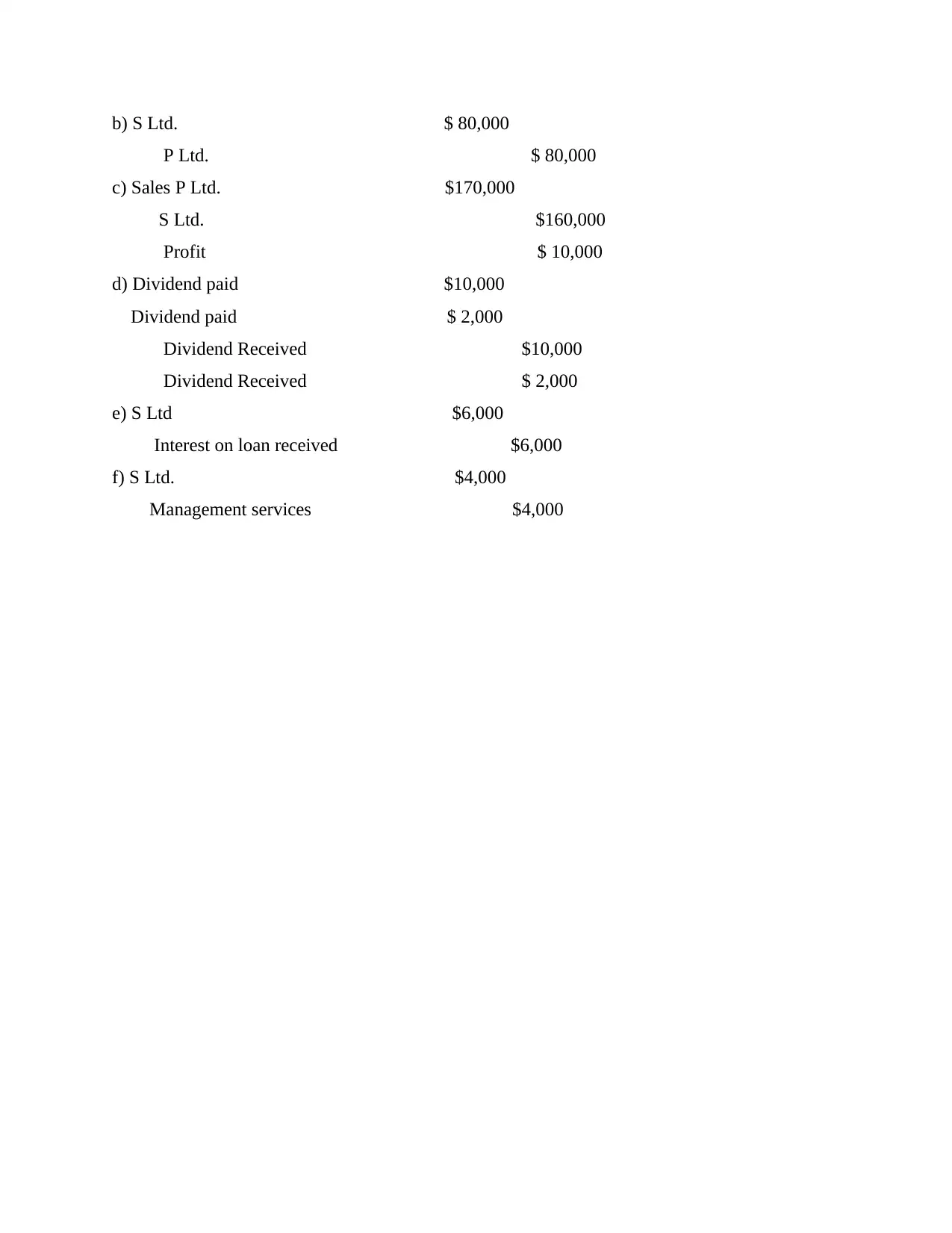

This assignment solution addresses several key concepts in financial accounting and reporting. It begins with an explanation of preference shares, differentiating them from debt and equity, and discussing their accounting treatment. The solution then delves into deferred tax assets and liabilities, explaining how they arise from temporary differences and their impact on corporate tax expenses. It also includes a discussion on true and fair view in financial reporting, ensuring the accuracy and fairness of financial statements. Further, the assignment explores scenarios where a company may be wound up by a court, outlining the relevant conditions. It also covers the accounting for events occurring after the reporting period, distinguishing between adjusting and non-adjusting events. The assignment provides journal entries for share capital transactions, along with calculations for depreciation, provision for leave, interest receivable, and land revaluation. Finally, it presents a consolidation worksheet and related journal entries, addressing topics such as acquisition analysis and the elimination of intercompany transactions. The provided solutions cover a wide range of financial accounting topics, including preference shares, deferred taxes, and consolidation.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.