Accounting Project Report: Analysis, Transactions, and Ethics

VerifiedAdded on 2021/04/21

|8

|1448

|145

Project

AI Summary

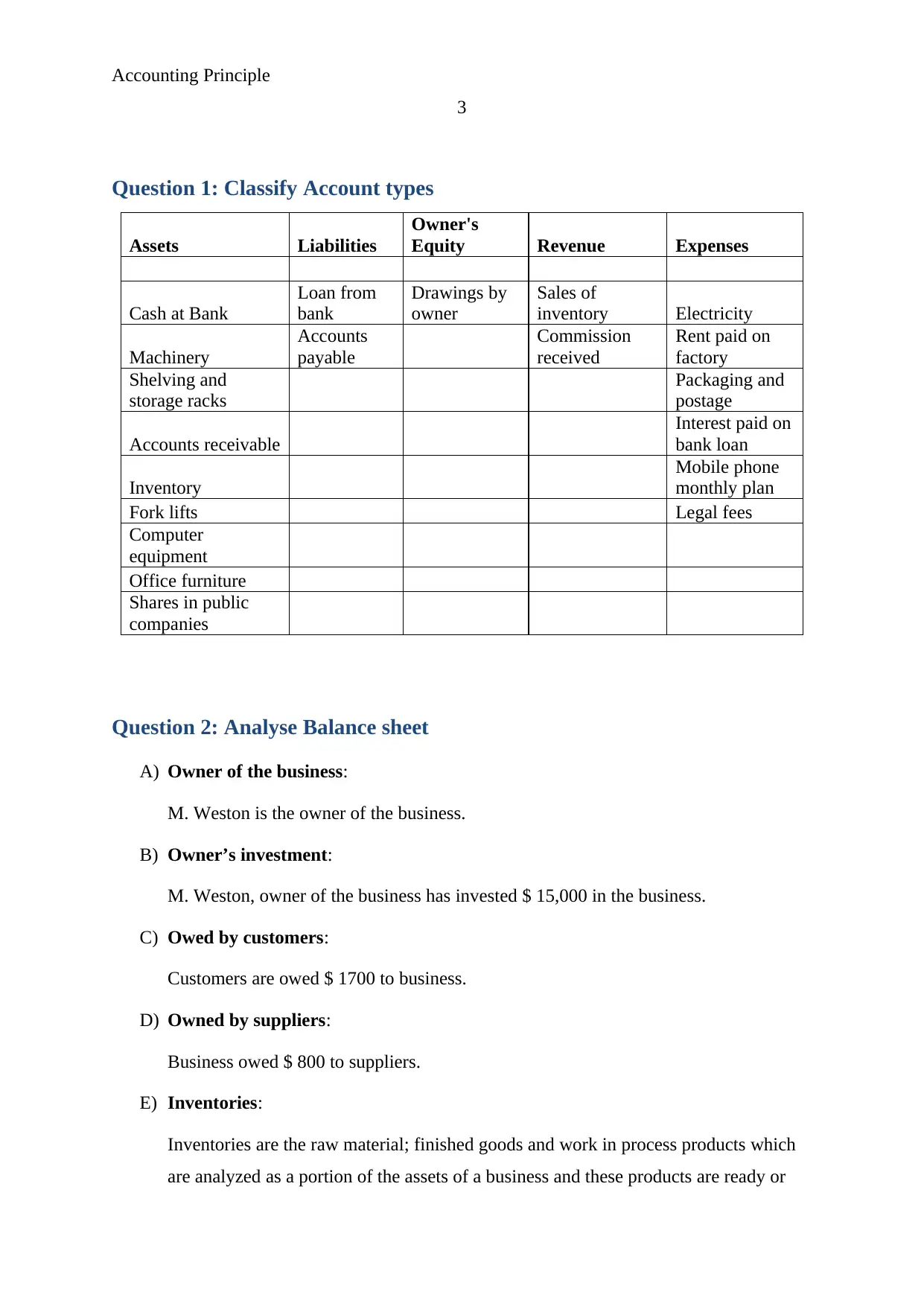

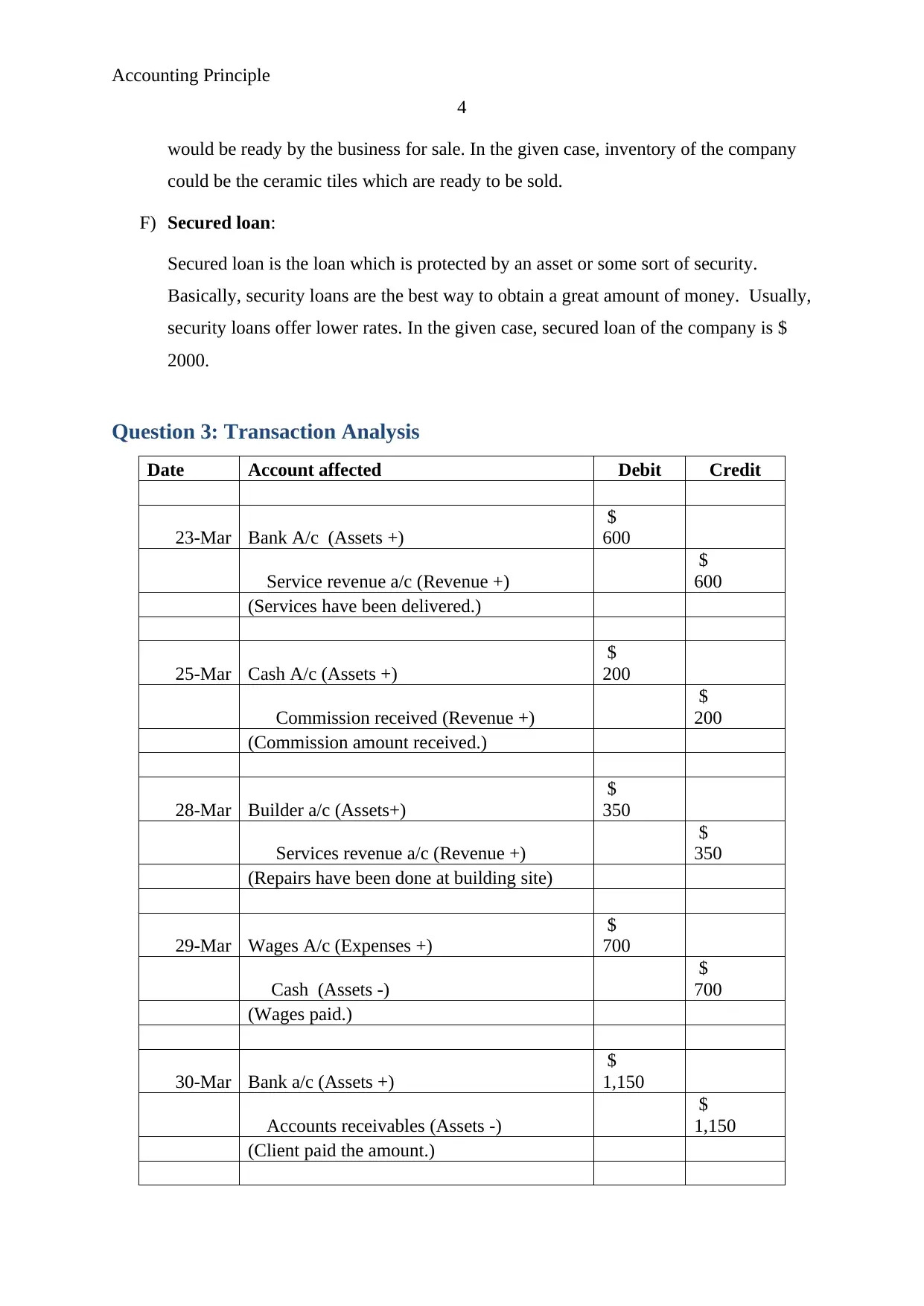

This project report analyzes accounting principles through several key questions. It begins by classifying various account types, including assets, liabilities, owner's equity, revenue, and expenses, providing examples for each. The report then analyzes a balance sheet, identifying the owner, owner's investment, amounts owed by and to customers and suppliers, inventory, and a secured loan. Next, the report presents a transaction analysis, detailing debits and credits for various financial events. The report also explores accounting ethics, discussing integrity, objectivity, confidentiality, professional competence, and professional behavior. Finally, the report includes a reverse engineering analysis of transactions. The report concludes with a list of references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.