Detailed Solution for Finance and Accounting Exam (Alpha Group)

VerifiedAdded on 2022/12/28

|13

|2076

|68

Homework Assignment

AI Summary

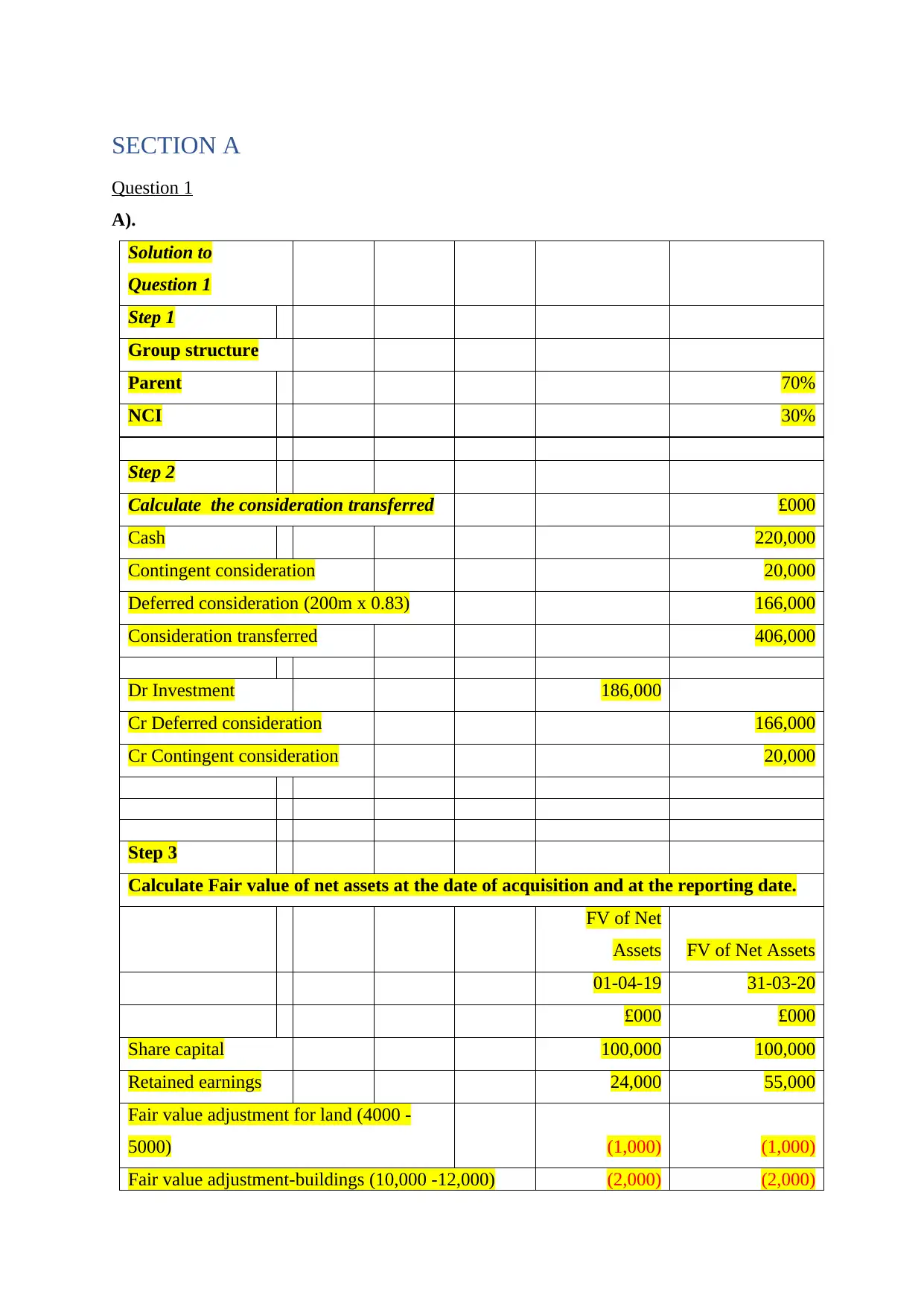

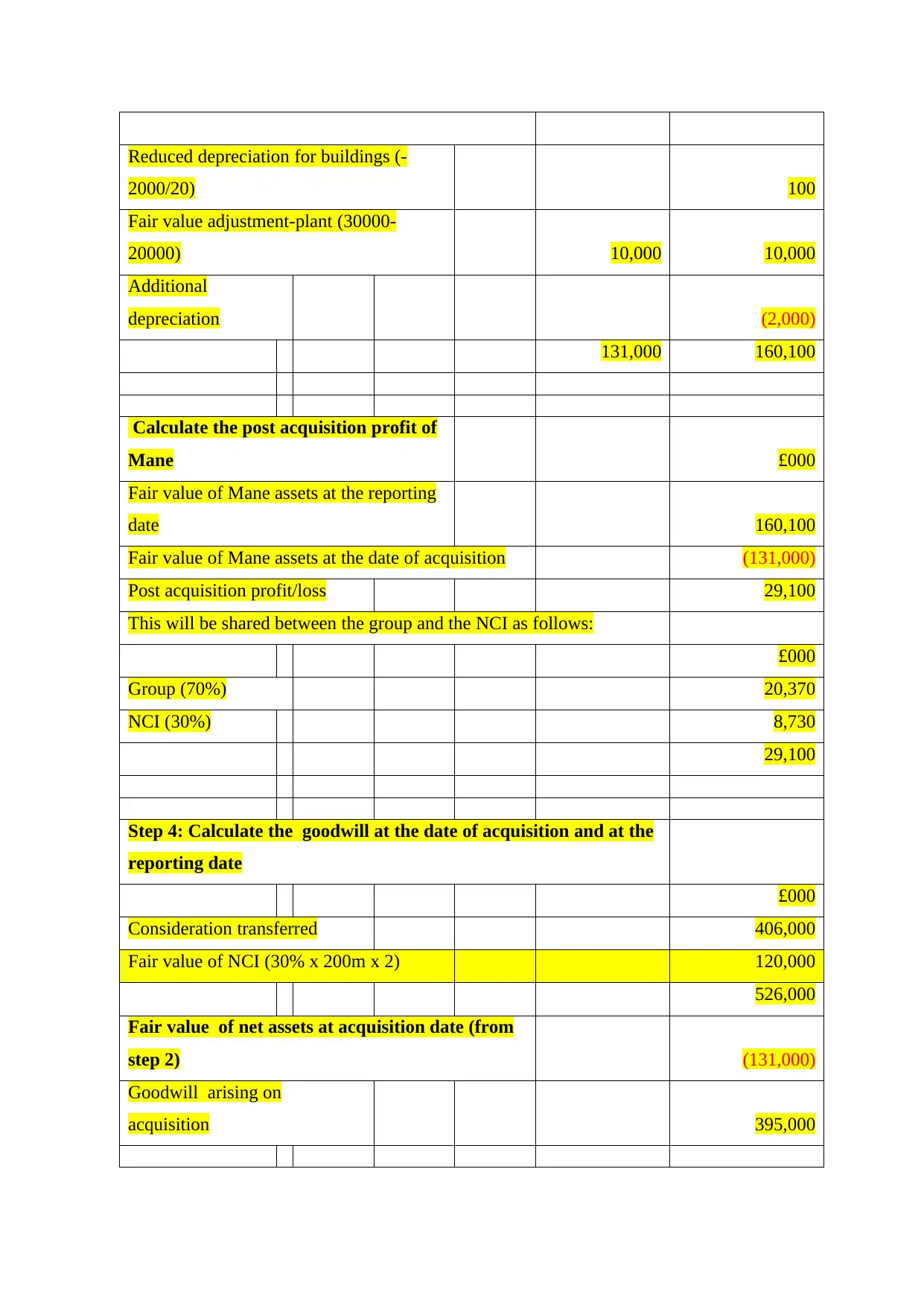

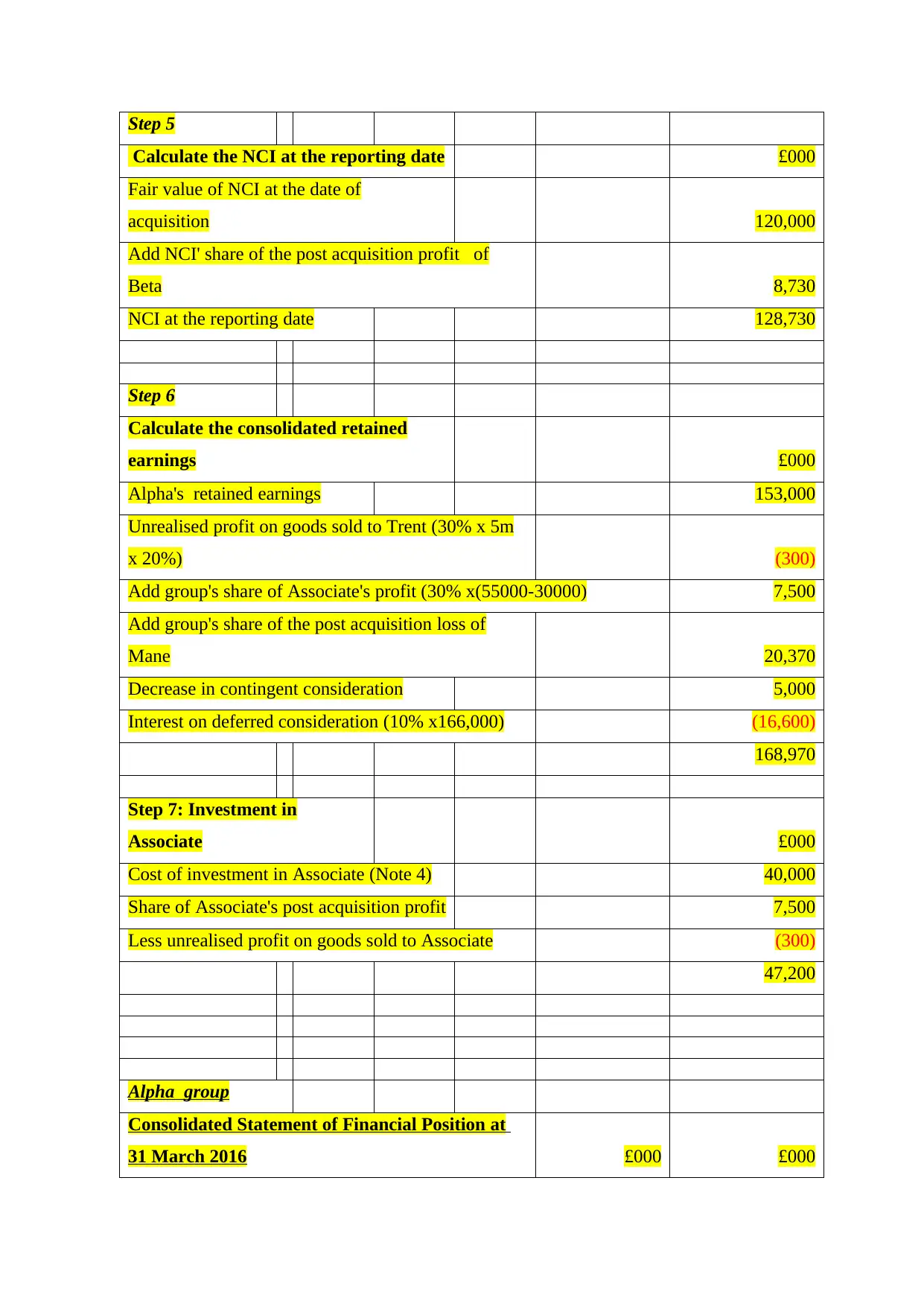

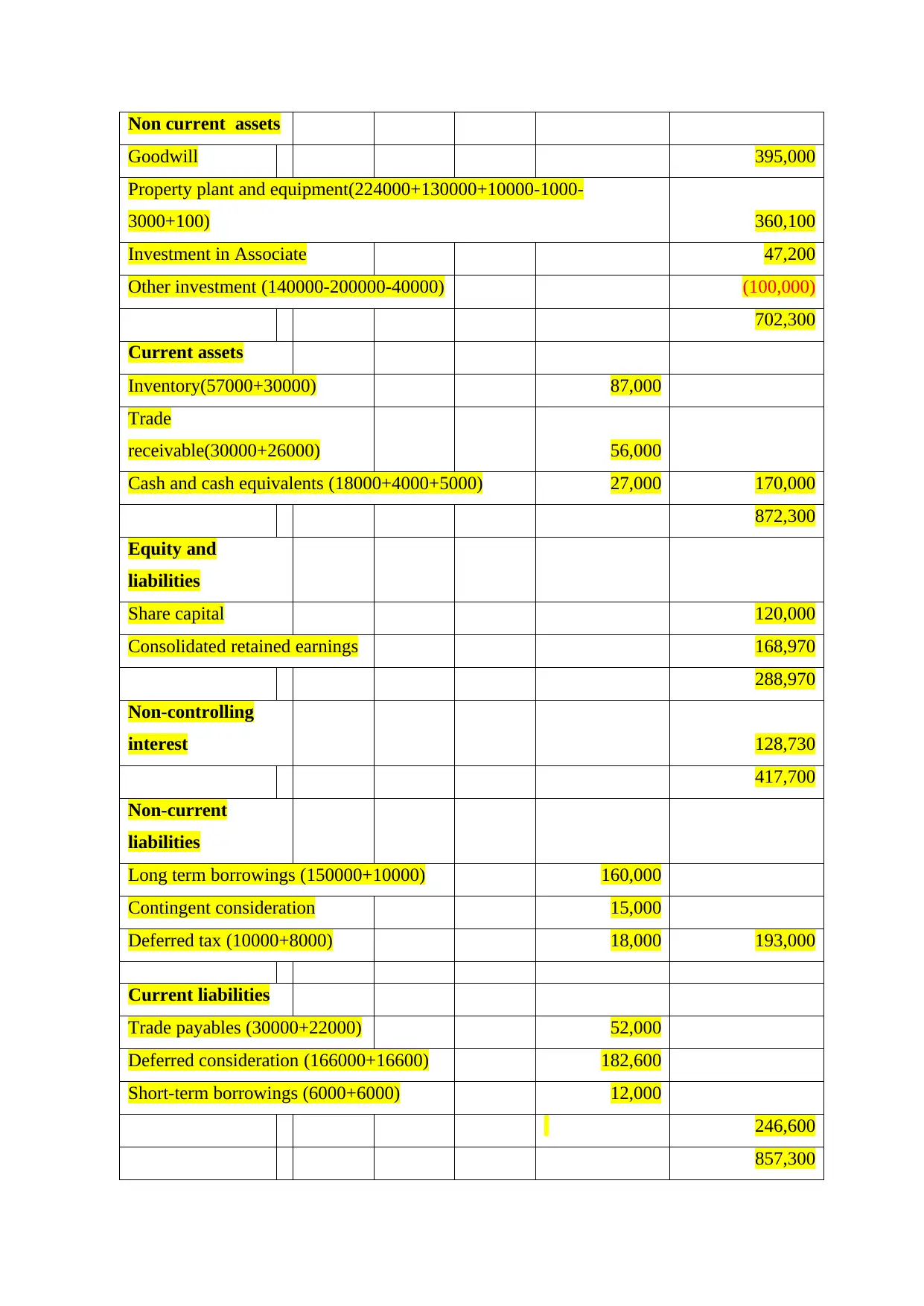

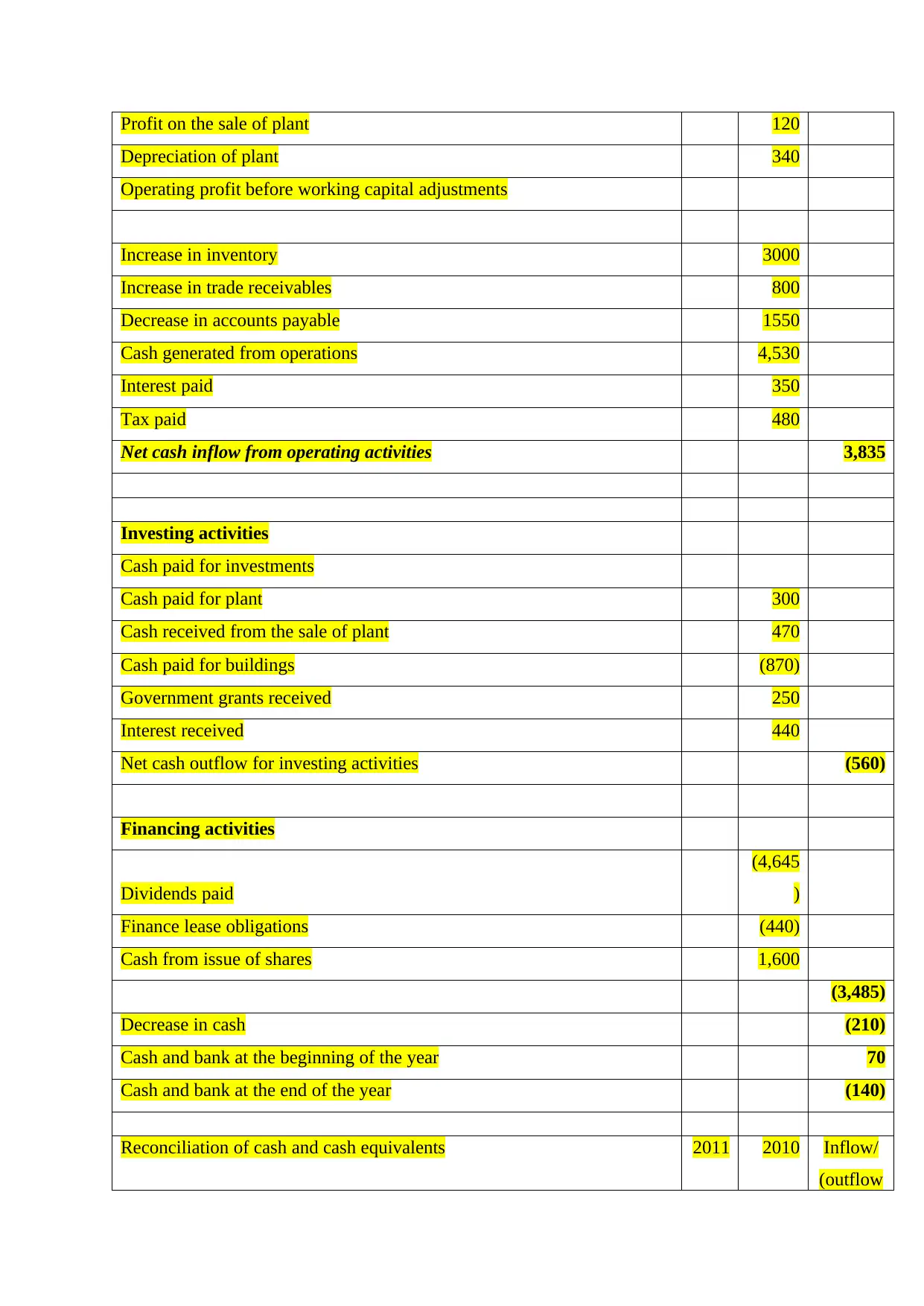

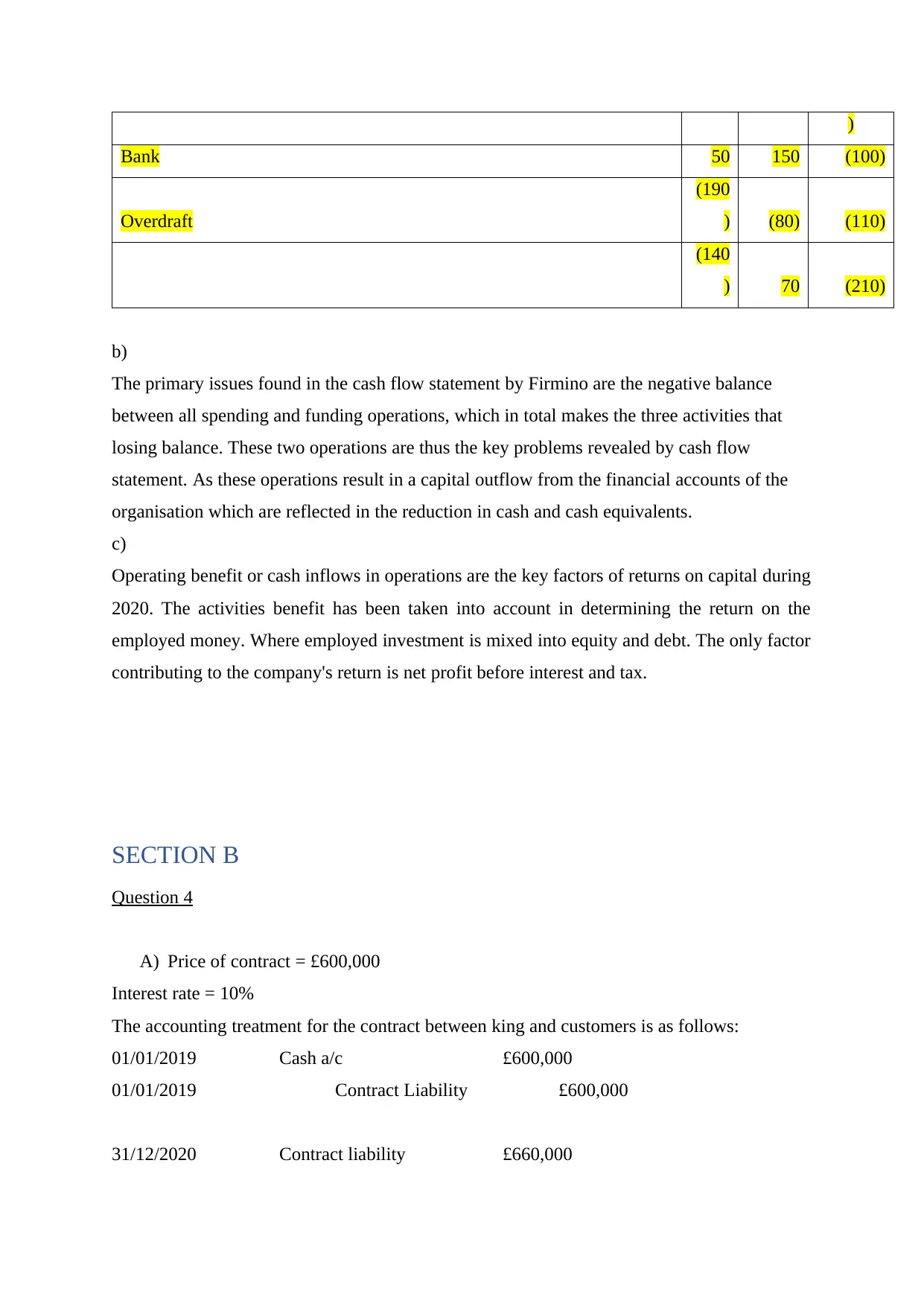

This document presents a comprehensive solution to a finance exam, addressing various accounting and financial reporting concepts. The solution includes detailed calculations and explanations for questions related to consolidation, cash flow statements, and accounting treatments under IFRS. The solution covers topics such as the calculation of goodwill, non-controlling interest, and consolidated retained earnings. It analyzes cash flow statements, identifies key issues, and explains the impact of operating activities on capital returns. Furthermore, it provides accounting treatments for contracts, commission rates, and depreciation, and offers guidance on currency selection and the accounting for specific transactions, including patent and land acquisitions, and revenue recognition. The document provides a complete guide to the accounting treatment of contracts and depreciation and addresses the selection of functional currency and accounting for specific transactions.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.