ACCT 101: Finance Assignment on Bank Reconciliation and Depreciation

VerifiedAdded on 2020/05/11

|6

|1144

|97

Homework Assignment

AI Summary

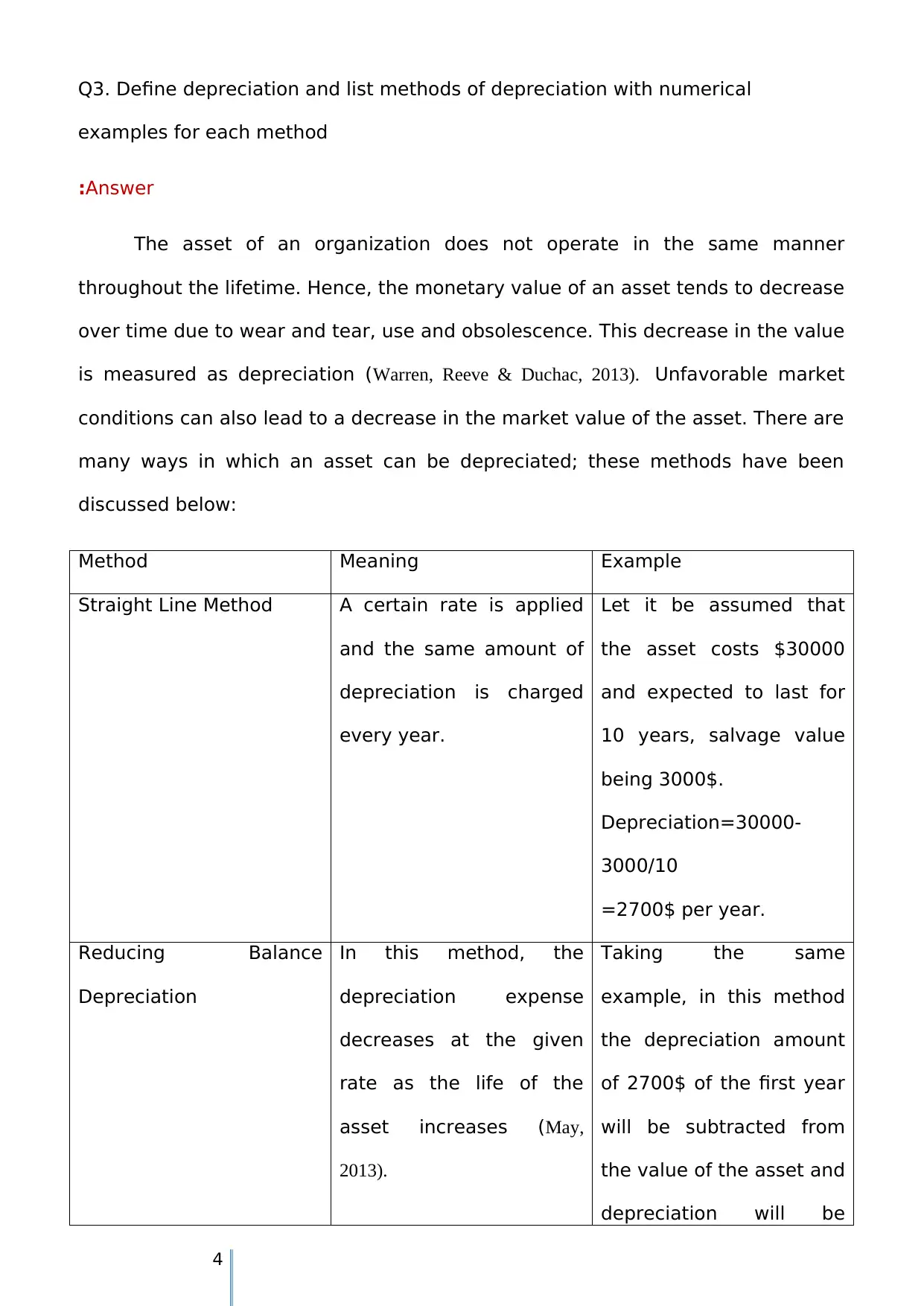

This document presents solutions to an ACCT 101 accounting assignment. The first question explains the importance of a bank reconciliation statement, detailing its role in ensuring accuracy and detecting errors, with real-world examples of discrepancies between cashbook and bank statement balances. The second question delves into accounting for uncollectible accounts receivable, contrasting the direct write-off method with the allowance method, and providing examples to illustrate their application. The third question defines depreciation and outlines various depreciation methods, including straight-line, reducing balance, sum of the years' digits, and units of activity, accompanied by numerical examples for each method to clarify their calculation and impact on asset valuation. The assignment covers key concepts in financial accounting, including bank reconciliation, depreciation, and the treatment of uncollectible accounts receivable.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.