Finance Assignment: Acquisition Analysis, NCI and Consolidation

VerifiedAdded on 2022/11/10

|7

|684

|423

Homework Assignment

AI Summary

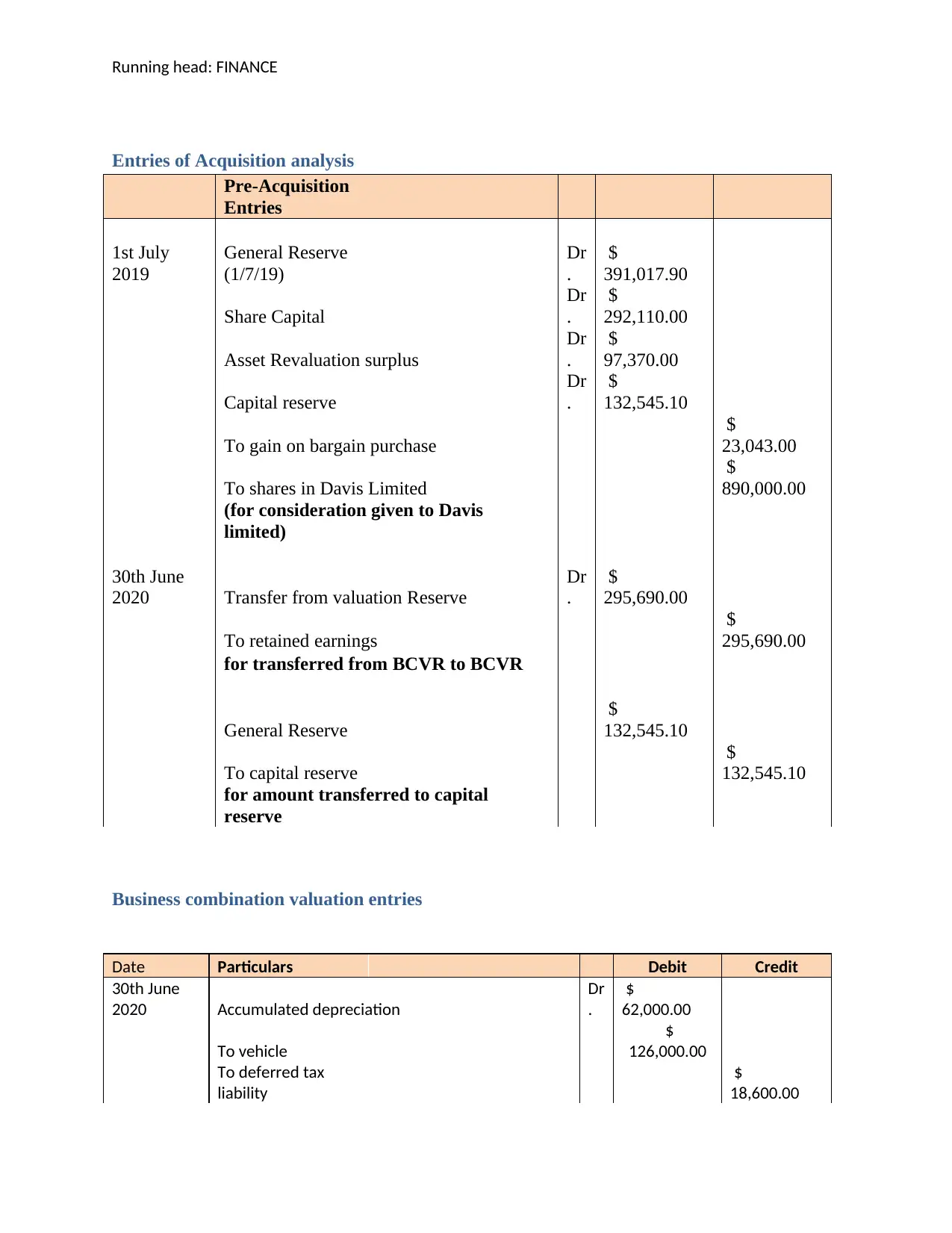

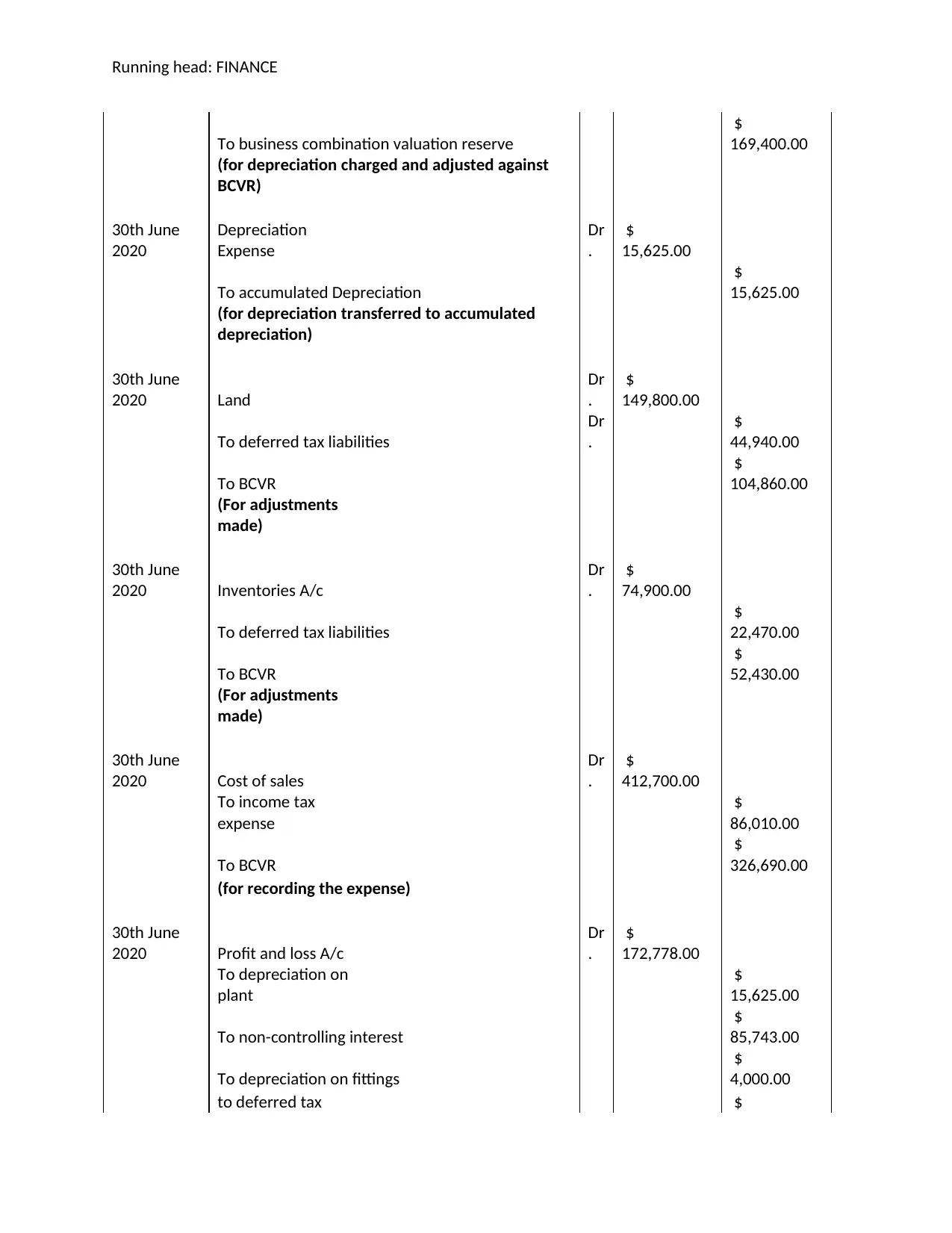

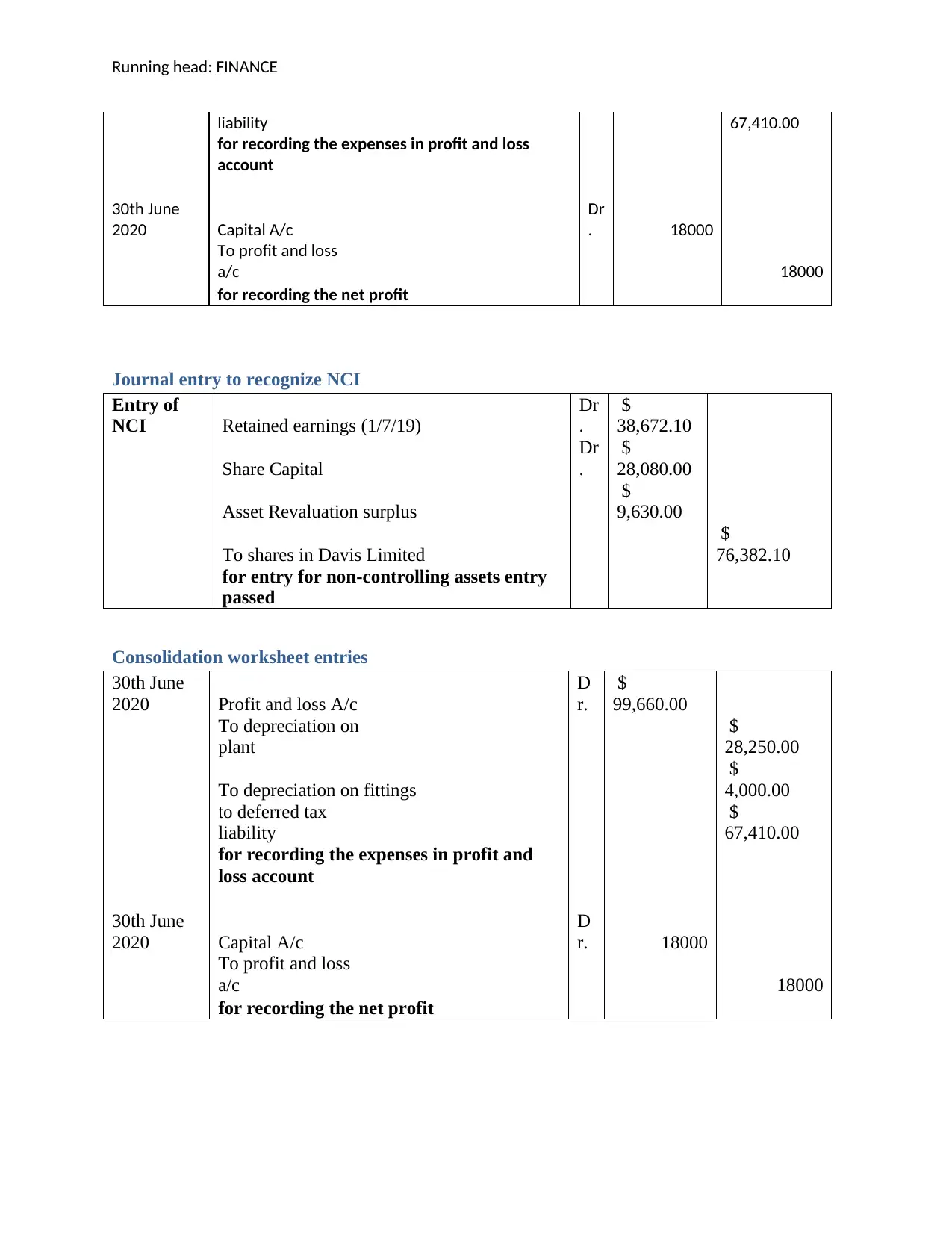

This finance assignment solution provides a comprehensive analysis of acquisition accounting, business combination valuation, and the treatment of Non-Controlling Interest (NCI). It includes pre-acquisition entries, business combination valuation entries, and journal entries to recognize NCI. The solution also features consolidation worksheet entries and a clear explanation of the differences between the partial goodwill method and the full goodwill method. The assignment covers adjustments for depreciation, land, inventories, and cost of sales, along with their impact on deferred tax liabilities and the business combination valuation reserve. The document also explains the impact of the different methods and how they affect the balance sheet and profit and loss account. The provided solution is a valuable resource for students studying financial accounting and consolidation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.