Finance Report on ARB Corporation: Materiality and Financial Analysis

VerifiedAdded on 2023/06/07

|16

|3018

|194

Report

AI Summary

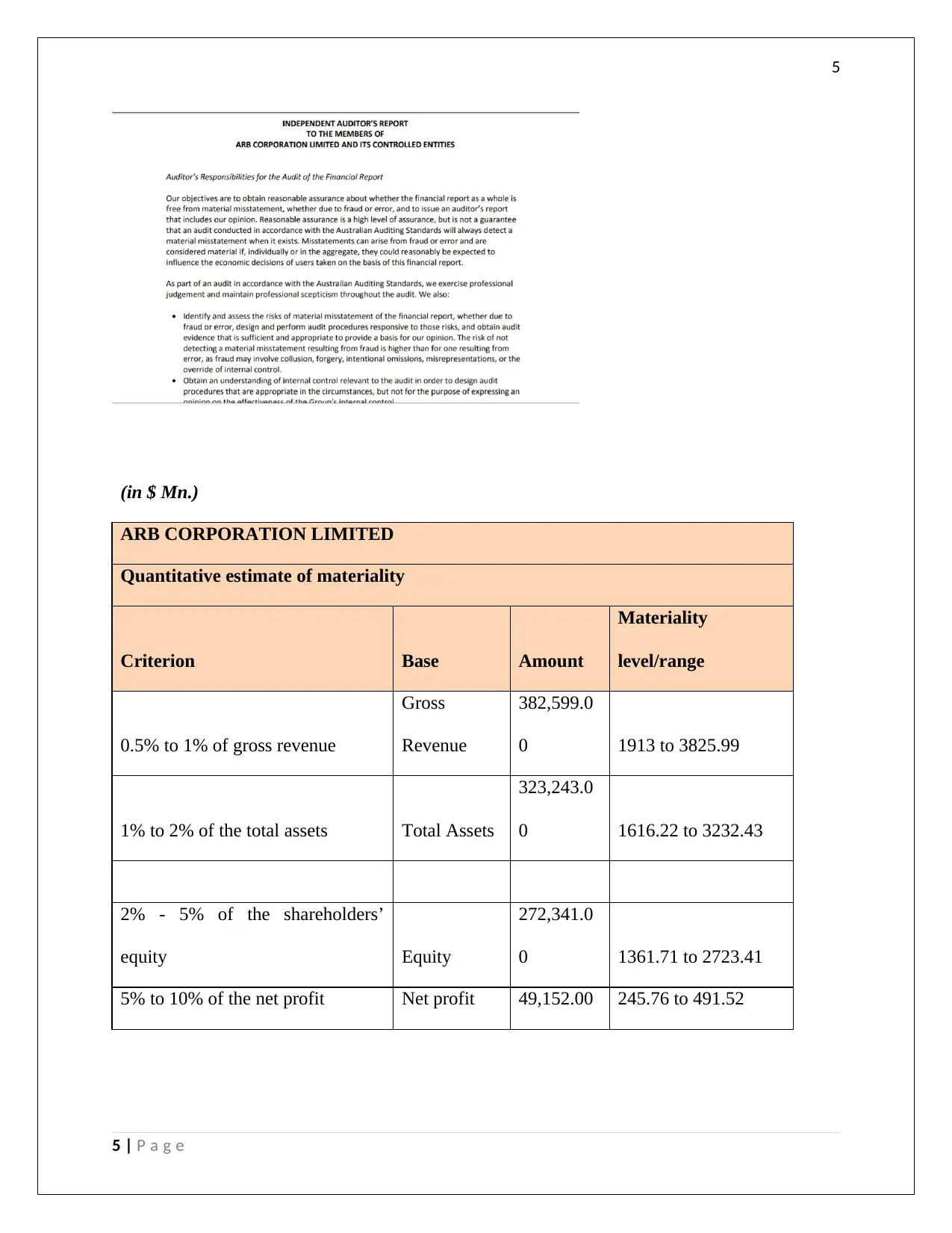

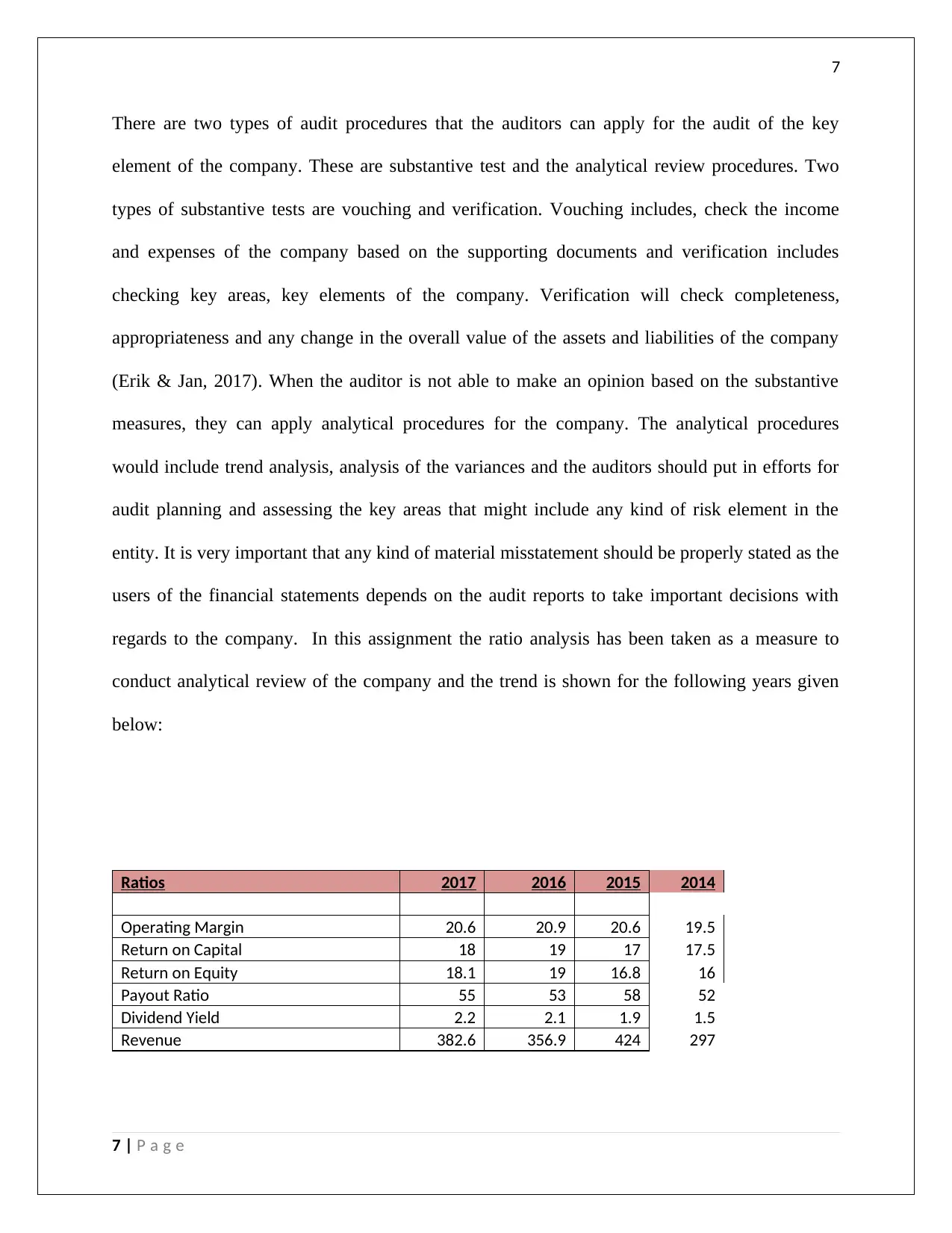

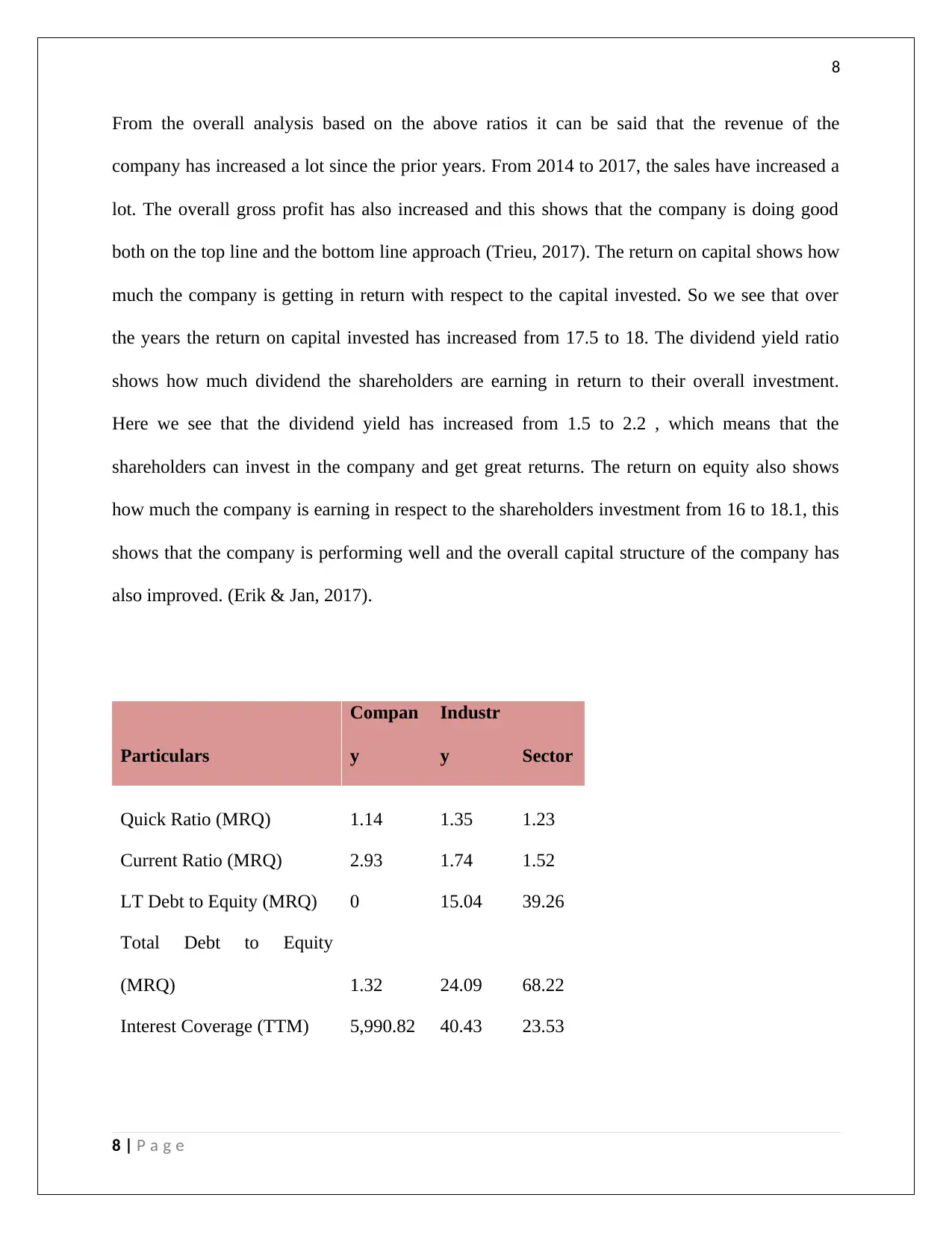

This finance report provides a comprehensive analysis of ARB Corporation's 2017 annual report, focusing on key financial aspects. The report begins with an executive summary and table of contents, followed by a detailed examination of materiality concerns, adhering to ASA 320 guidelines. Materiality levels are calculated based on revenue, total assets, shareholders' equity, and net profit, with a calculated materiality level of $350,000. Section 2 presents a preliminary analytical review, employing ratio analysis to assess the company's financial performance over several years, including operating margin, return on capital, return on equity, payout ratio, and dividend yield. Comparisons are made with industry averages, highlighting areas of strength and potential improvement. Audit assertions and procedures are also discussed. The final section reviews the cash flow statement, analyzing cash flows from operating activities. The report concludes with a discussion of audit risks and relevant assertions. The report is well-structured, providing a solid foundation for students studying finance and auditing.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.