Finance Report: Coca-Cola Amatil Limited Financial Analysis - Item 2

VerifiedAdded on 2023/06/04

|13

|2006

|423

Report

AI Summary

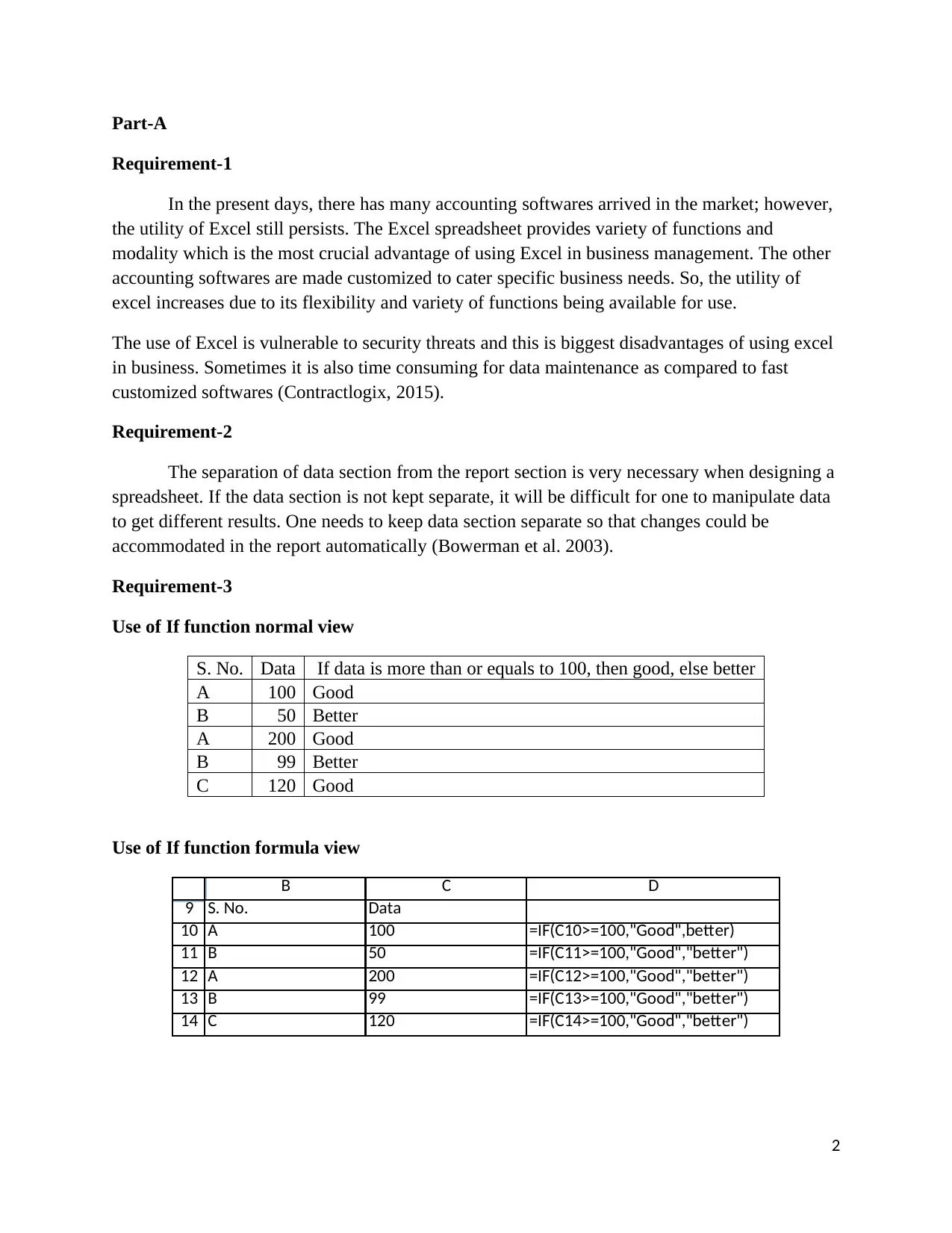

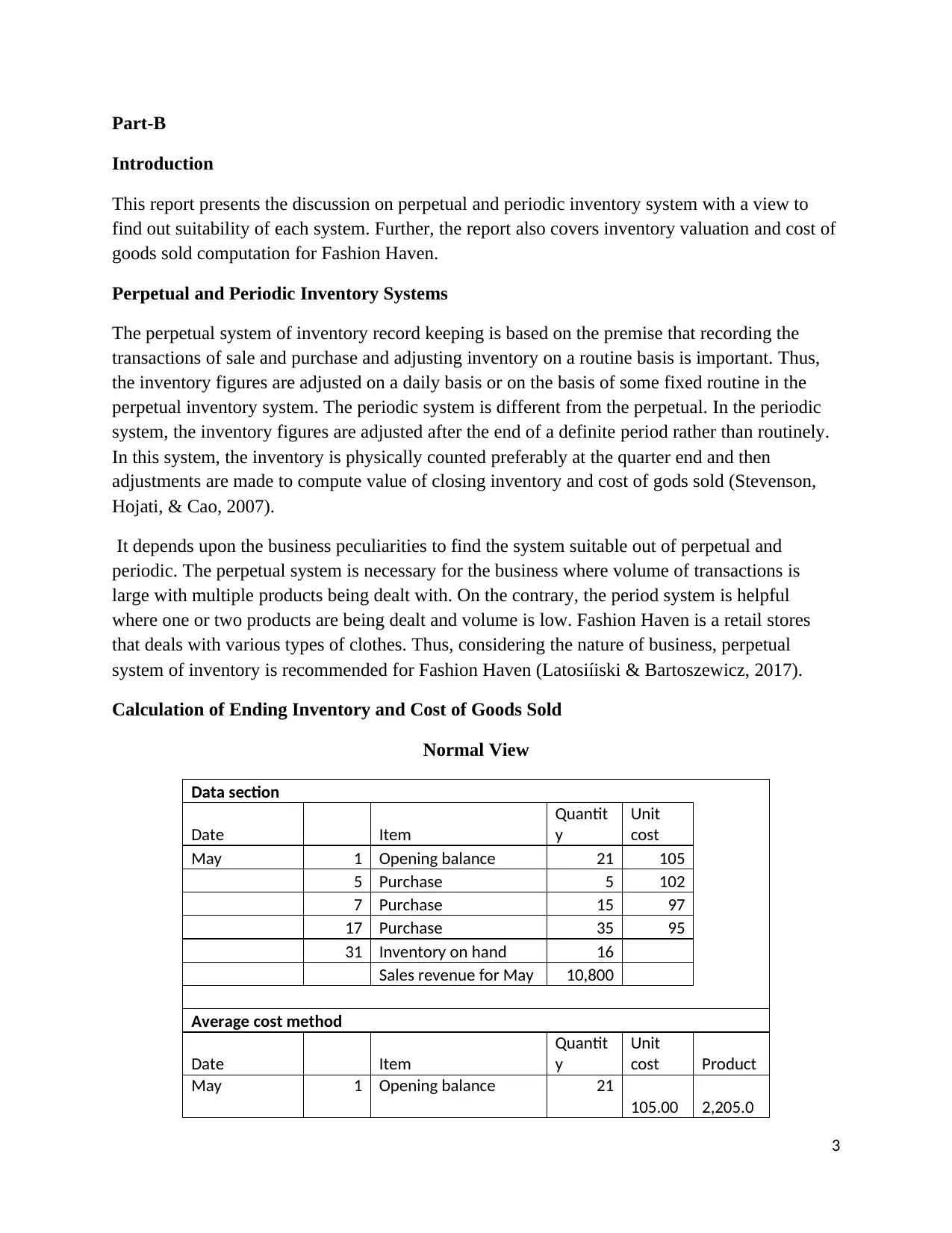

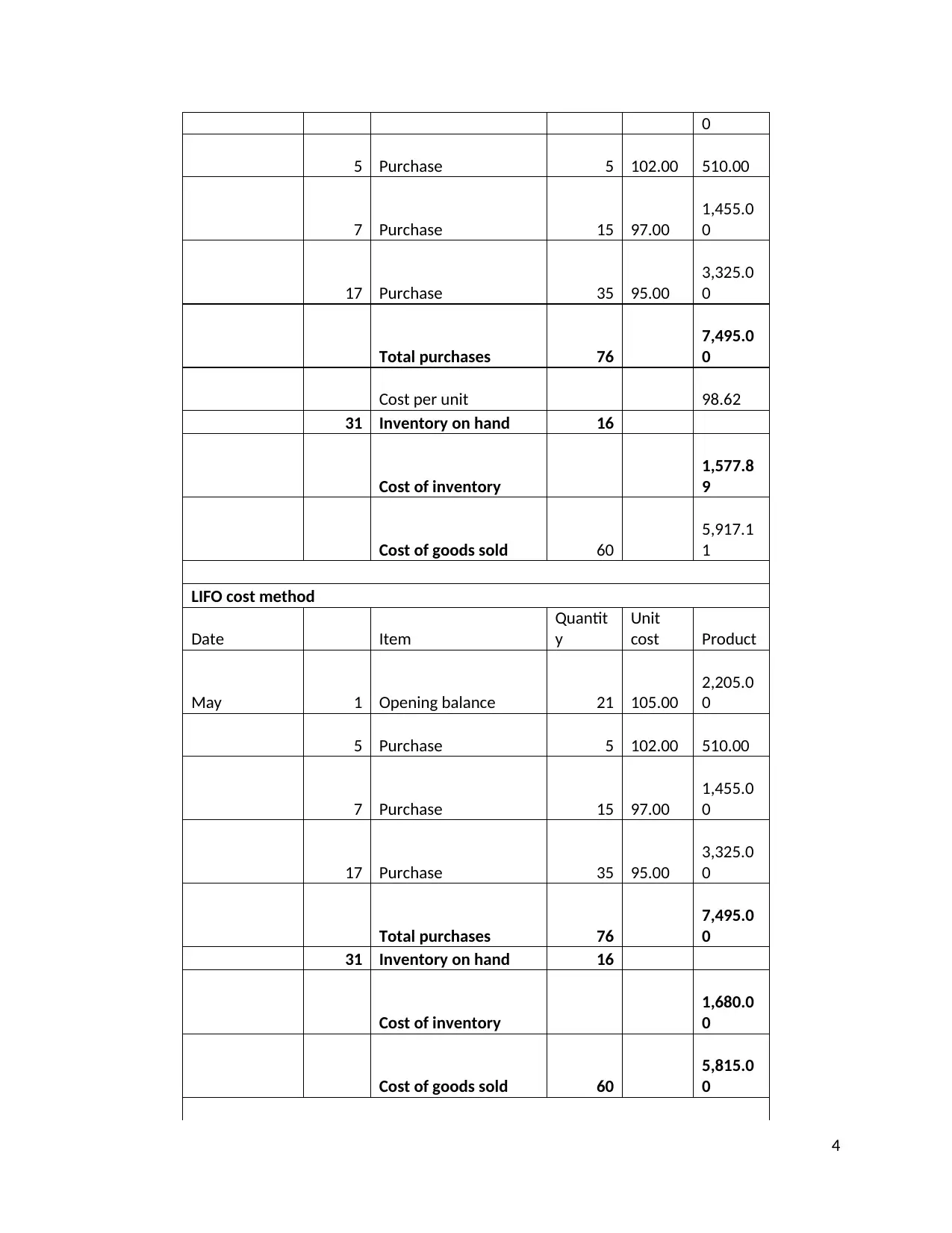

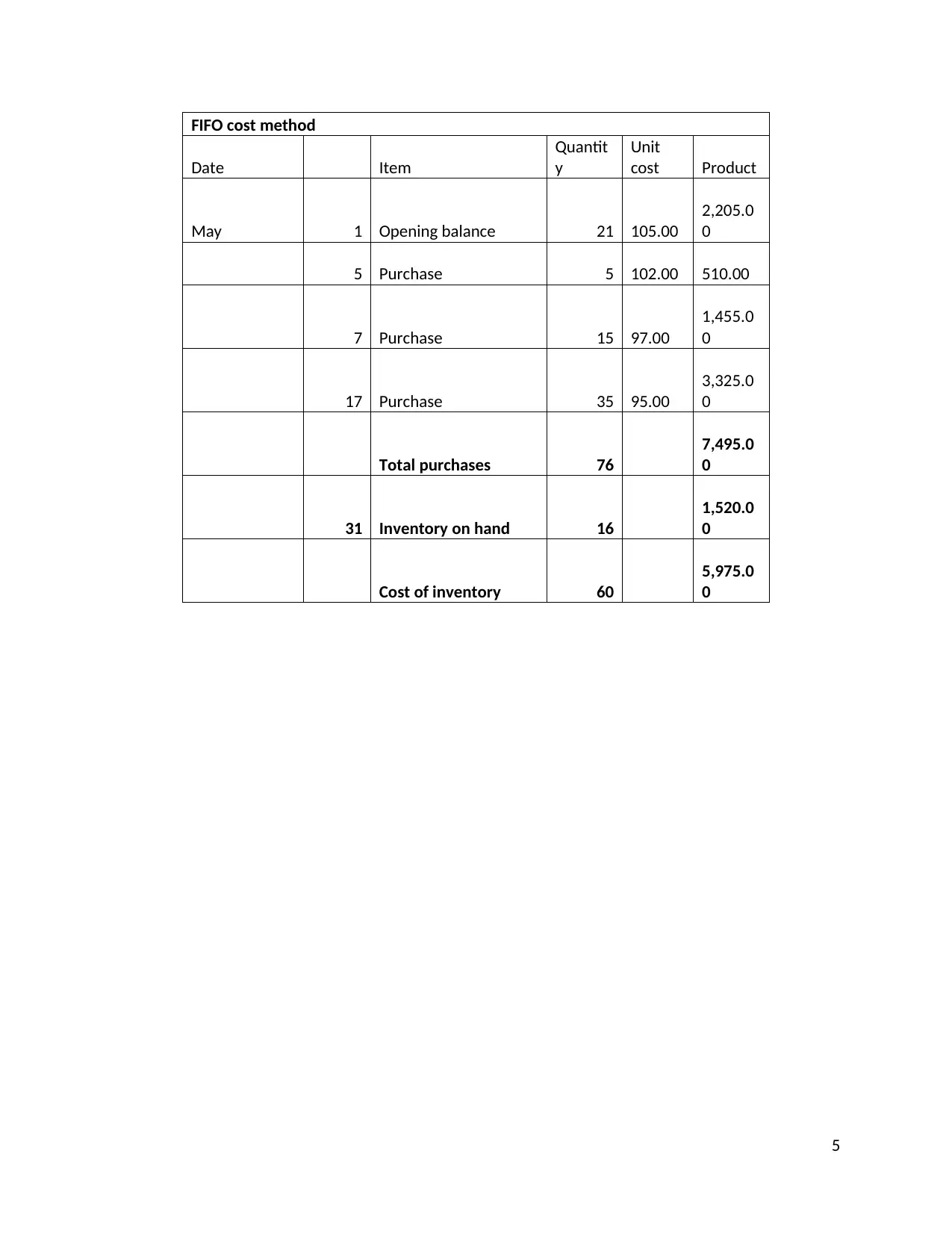

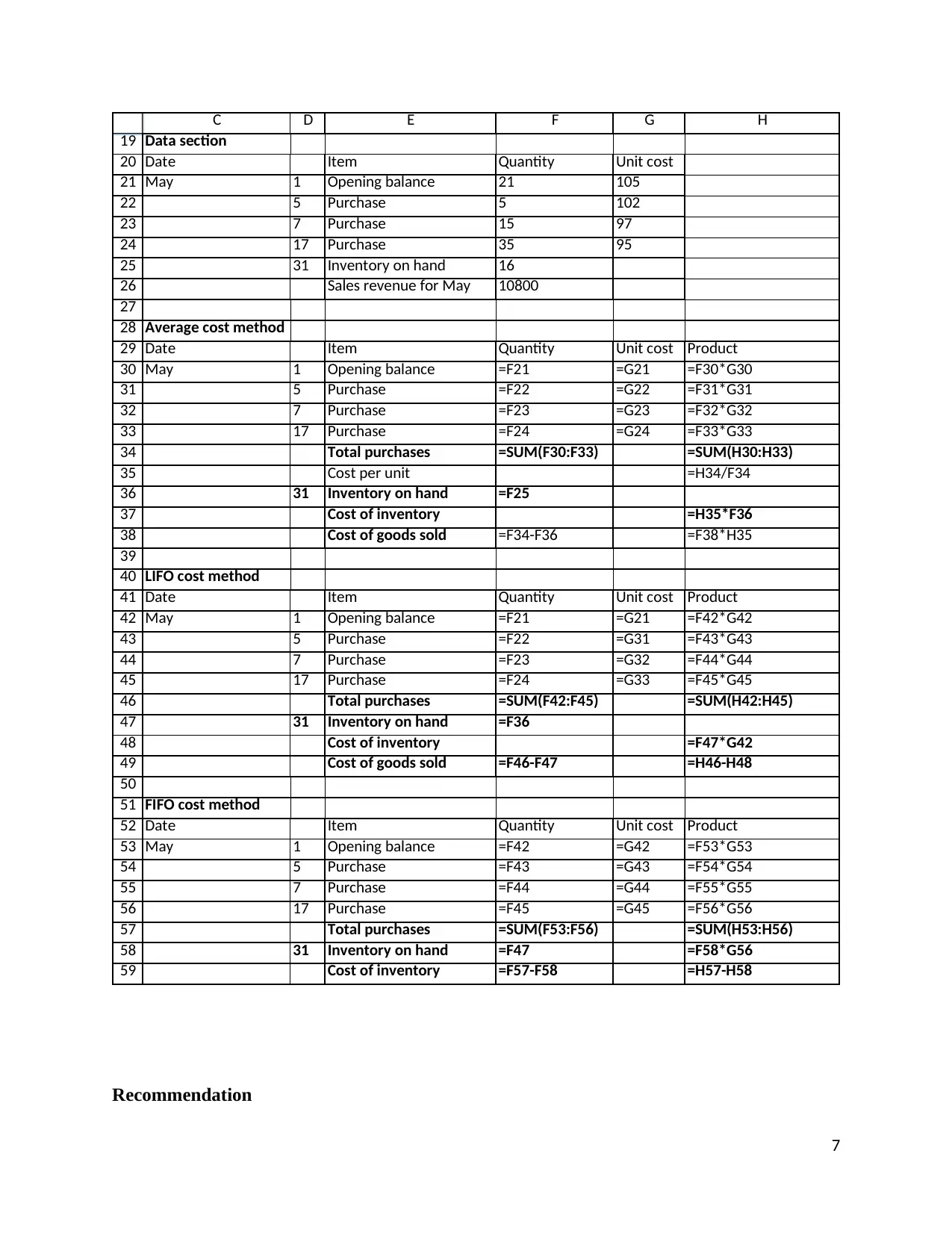

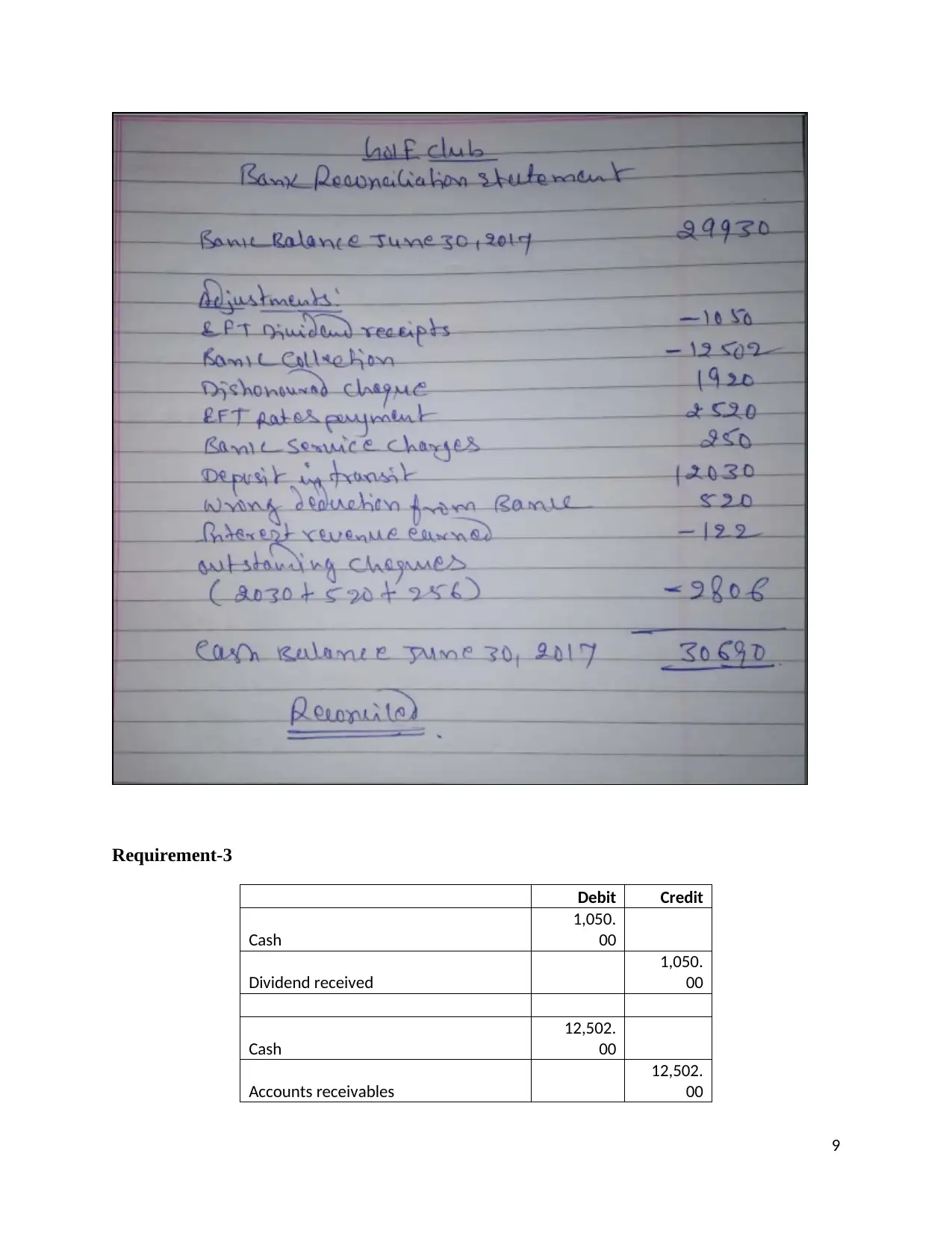

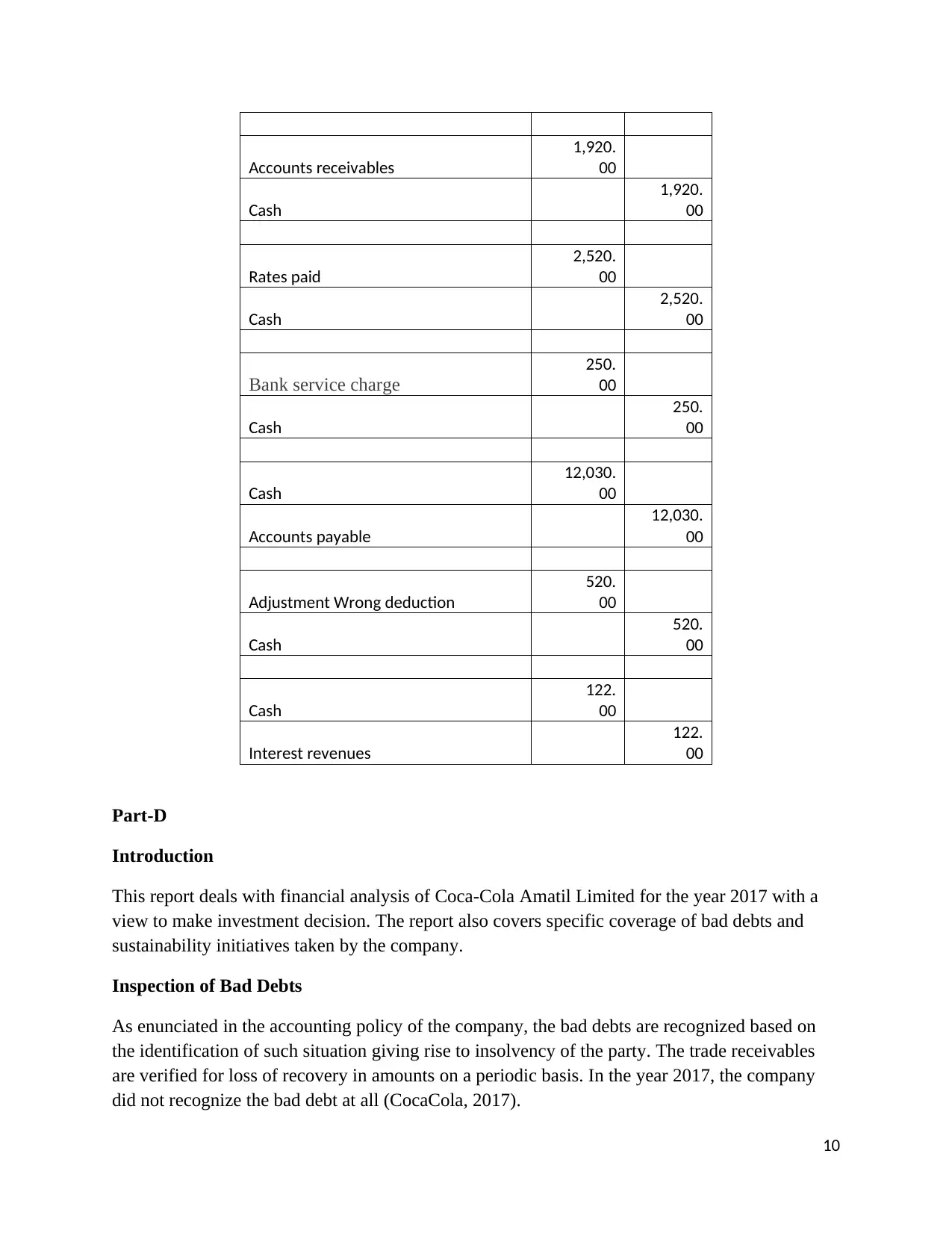

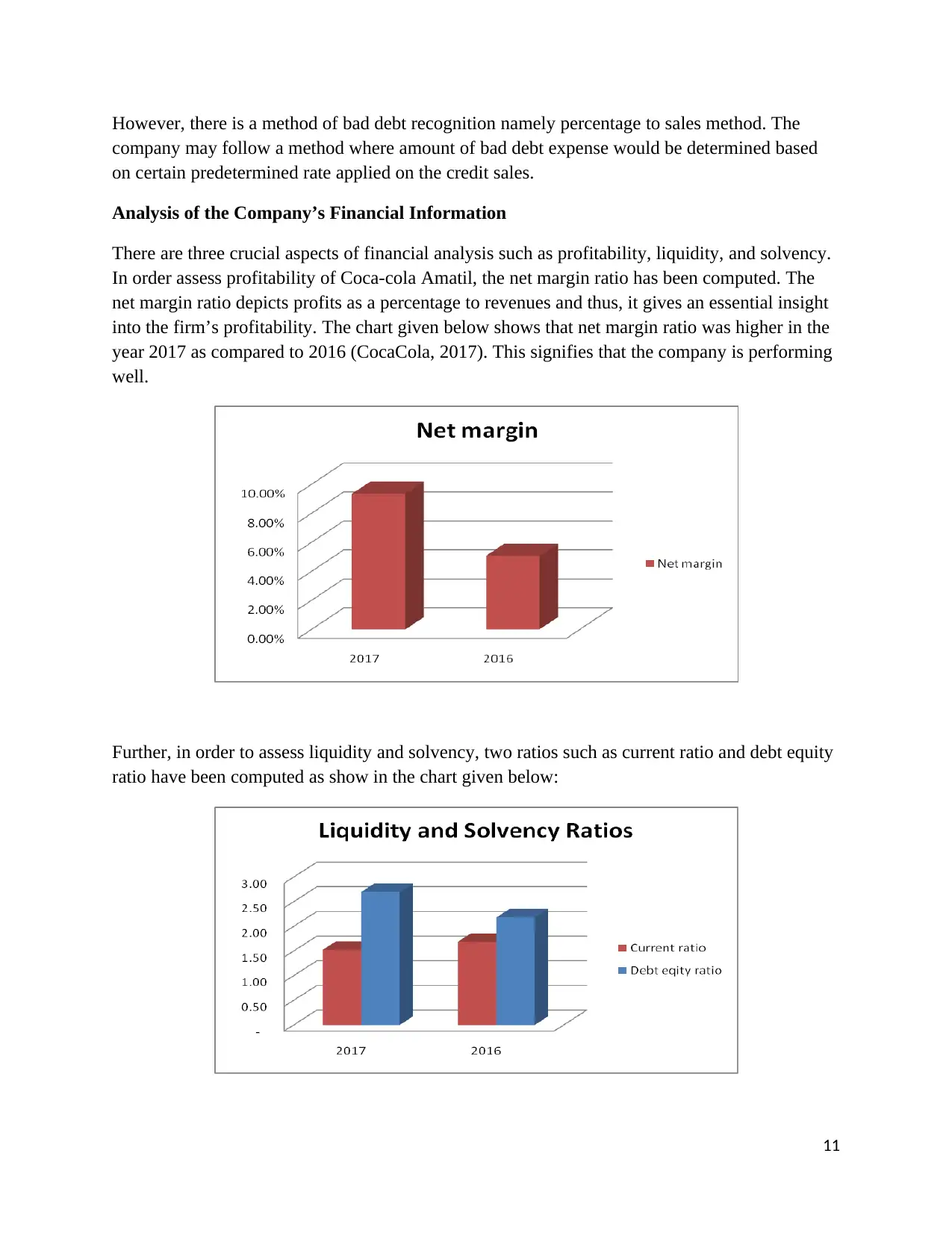

This report presents a comprehensive analysis of financial concepts and applications. Part A explores the continued use of spreadsheets in accounting despite the availability of specialized software, outlining their advantages and disadvantages, along with the importance of separating data and report sections. It demonstrates the use of IF functions and cell referencing within spreadsheets. Part B focuses on inventory management, comparing perpetual and periodic inventory systems and recommending the most suitable system for Fashion Haven. It then calculates ending inventory and cost of goods sold using average cost, LIFO, and FIFO methods. Part C examines bank reconciliation, detailing transactions impacting cash balances and journal entries. Part D provides a financial analysis of Coca-Cola Amatil Limited for 2017, including an inspection of bad debts, an analysis of key financial ratios (profitability, liquidity, and solvency), and a review of the company's sustainability initiatives, concluding with an investment recommendation.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.