Finance in Hospitality: Recipe Cost, Pricing, and BEP Analysis

VerifiedAdded on 2023/04/03

|10

|1546

|78

Report

AI Summary

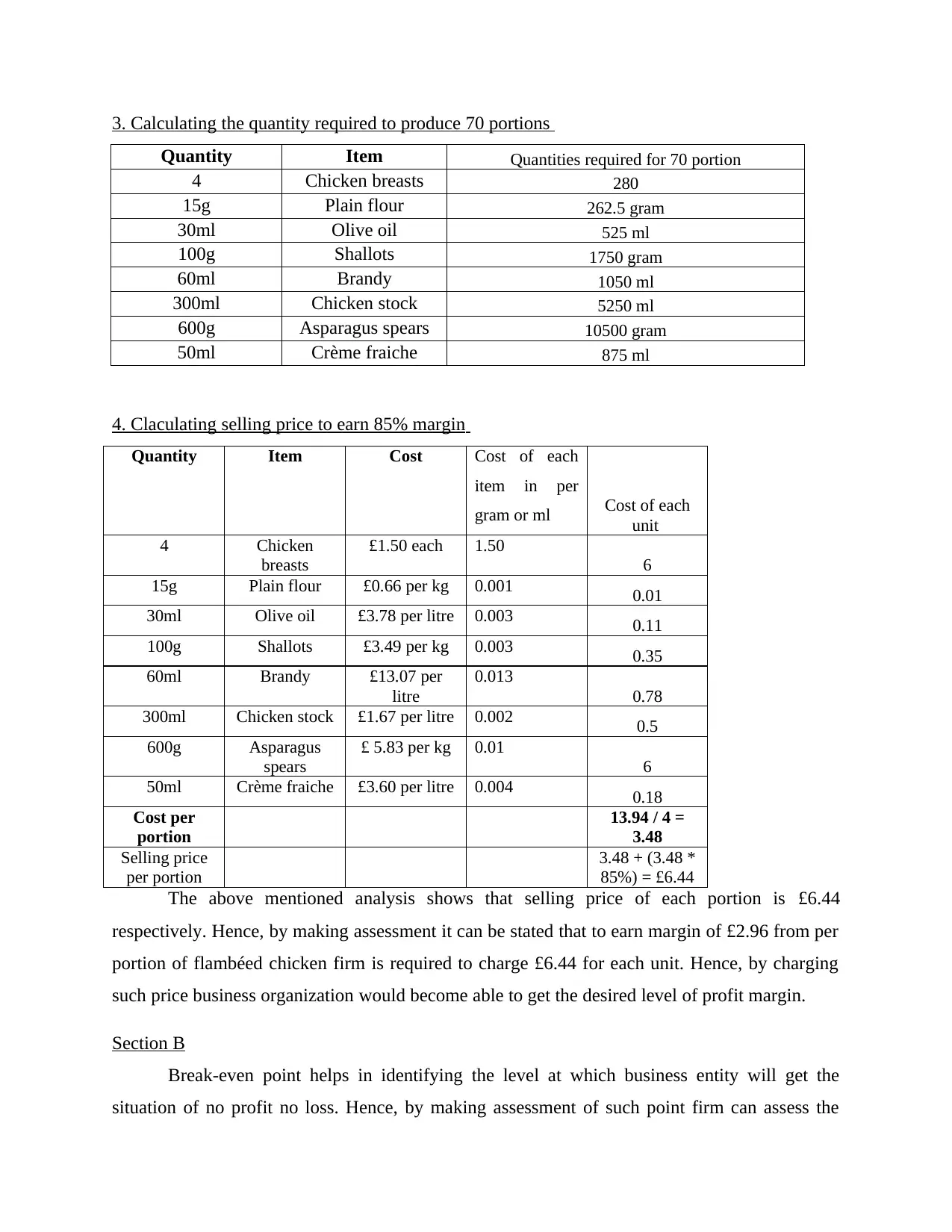

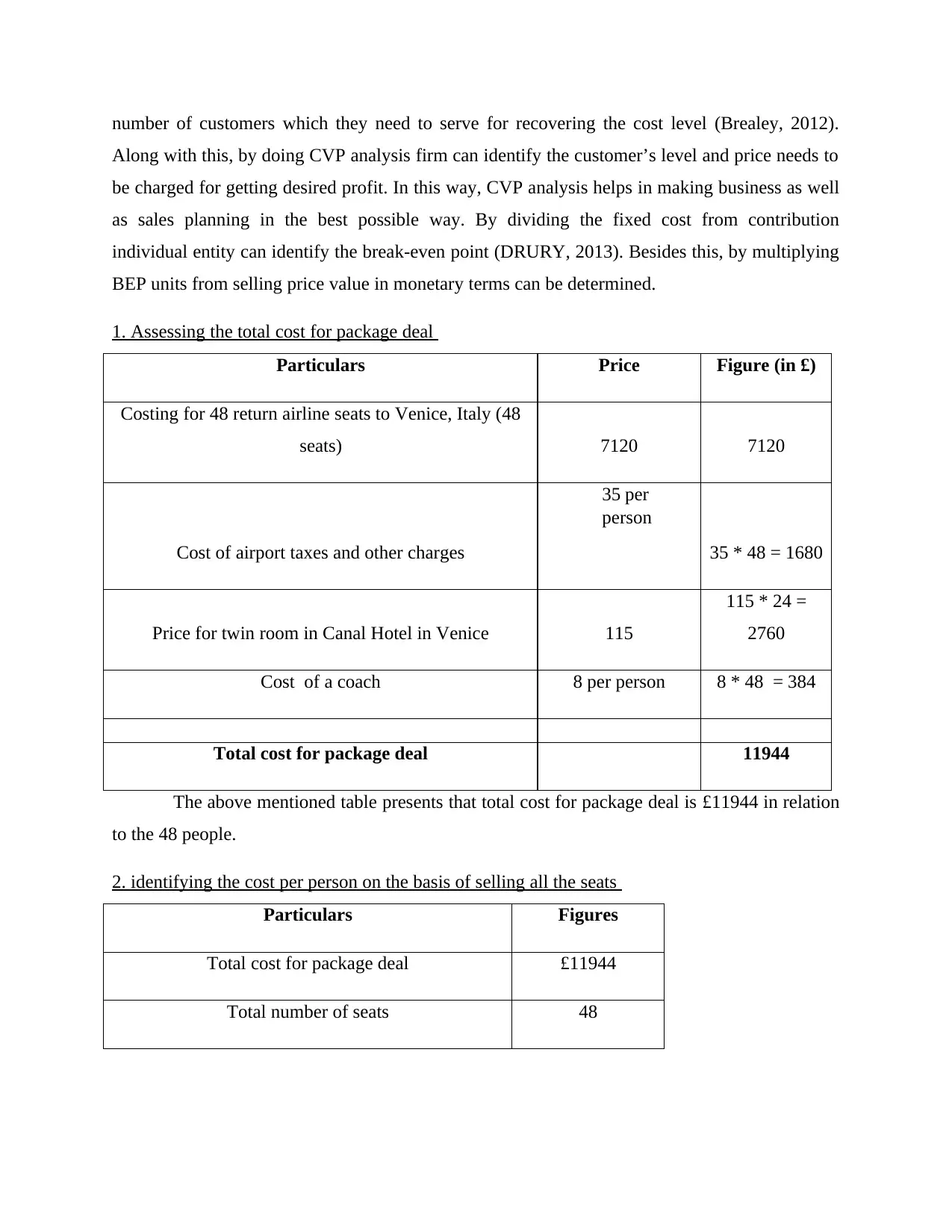

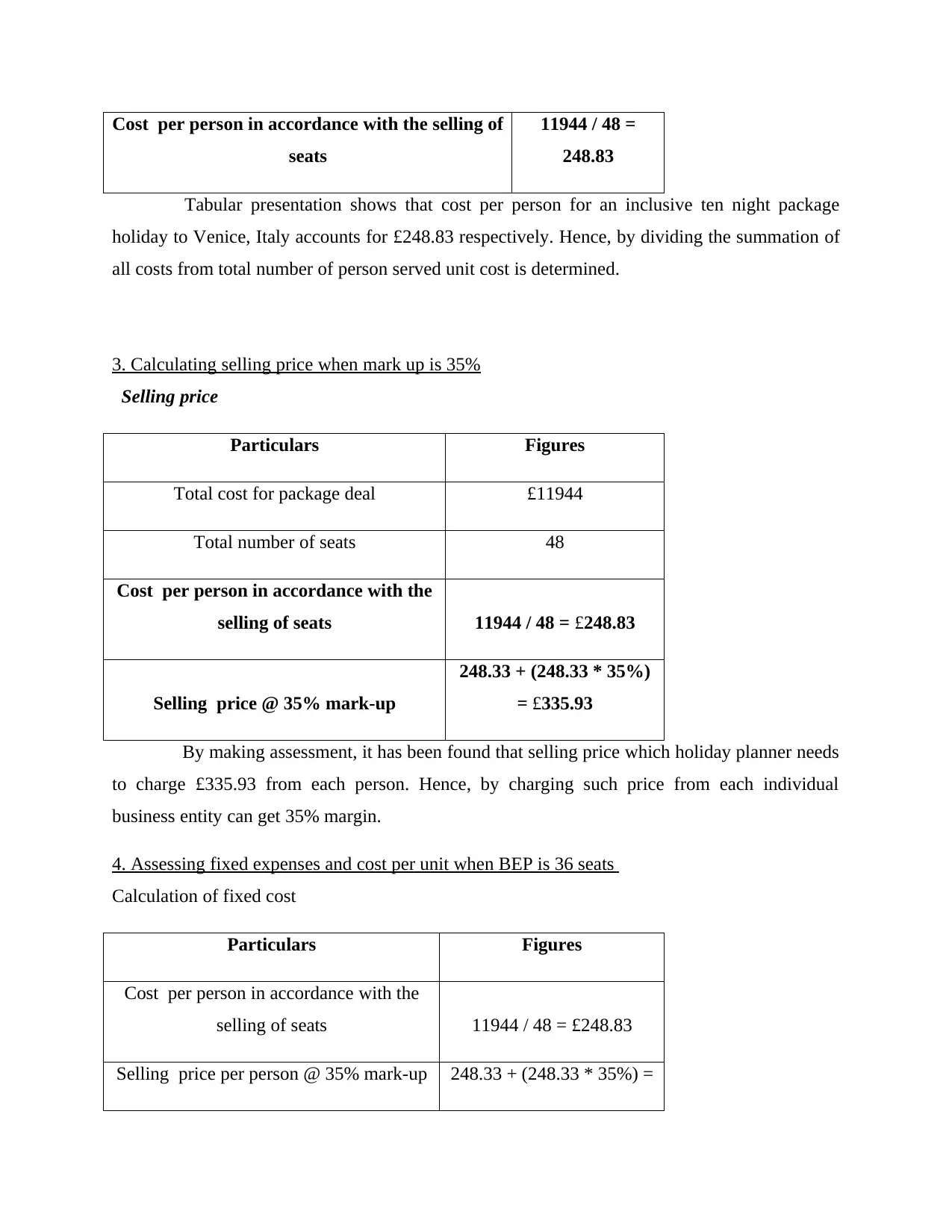

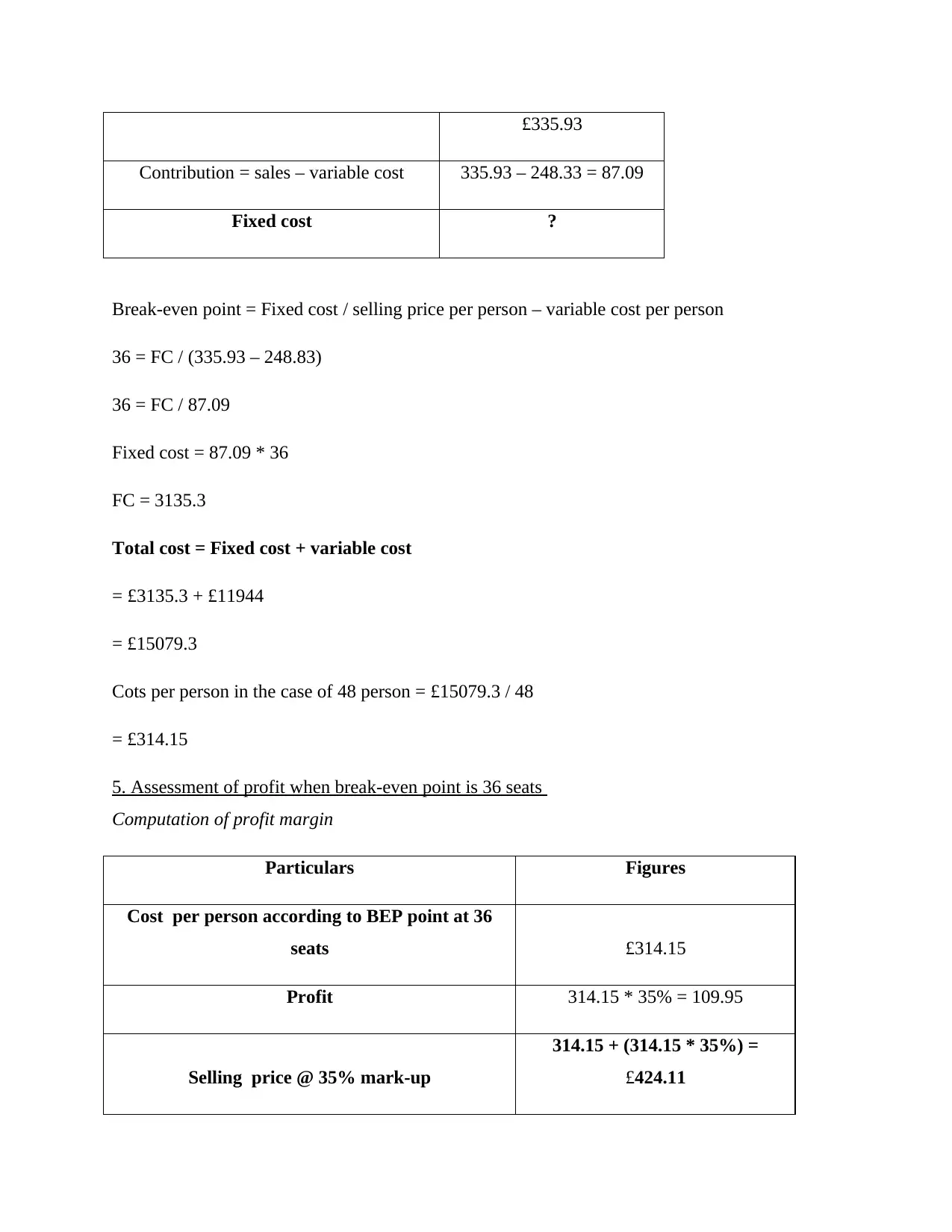

This report provides a comprehensive financial analysis within the hospitality sector. It begins by detailing the calculation of recipe costs, including ingredients and portioning, and progresses to calculating selling prices to achieve desired profit margins, specifically focusing on an 85% margin. The report then shifts to a case study involving a package deal, assessing total costs, cost per person, and calculating selling prices with a 35% markup. Furthermore, it delves into break-even point (BEP) analysis, determining fixed expenses, cost per unit, and assessing profit levels at the BEP. The report concludes by highlighting the importance of financial tools and techniques for effective decision-making within the hospitality industry, emphasizing cost management, pricing strategies, and BEP analysis for maximizing profitability and achieving business objectives. The report includes detailed calculations and tables to support its findings.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.