Financial Performance, Funding, and Pricing in Travel and Tourism

VerifiedAdded on 2019/12/28

|13

|4626

|201

Report

AI Summary

This report delves into the financial aspects of the travel and tourism industry, focusing on cost-volume-profit (CVP) analysis, pricing strategies, and financial performance evaluation. It examines how Merlin Entertainment Plc (MEP) can utilize CVP analysis, including break-even analysis, contribution margin, profit margin, and profit volume ratio, to make informed decisions. The report also explores various pricing methods, such as cost-oriented, competition-based, and demand-based pricing, to optimize revenue generation. Furthermore, it analyzes the impact of factors like selling price, cost of goods, sales volume, and market fluctuations on profitability. The report also includes financial statement analysis, utilizing ratio analysis to assess the performance of The Restaurant Group (TRG) and identifies different funding sources available to companies in the sector.

Finance and Funding in Travel and Tourism

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1....................................................................................................................................................3

1.2....................................................................................................................................................4

1.3....................................................................................................................................................6

TASK 2.................................................................................................................................................7

TASK 3.................................................................................................................................................7

3.1....................................................................................................................................................7

TASK 4.................................................................................................................................................9

4.1....................................................................................................................................................9

CONCLUSION..................................................................................................................................10

REFERENCES...................................................................................................................................11

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1....................................................................................................................................................3

1.2....................................................................................................................................................4

1.3....................................................................................................................................................6

TASK 2.................................................................................................................................................7

TASK 3.................................................................................................................................................7

3.1....................................................................................................................................................7

TASK 4.................................................................................................................................................9

4.1....................................................................................................................................................9

CONCLUSION..................................................................................................................................10

REFERENCES...................................................................................................................................11

2

INTRODUCTION

Travel and tourism sector is service-oriented enterprises operates in hospitality industry which

objective is to deliver wide range of services like lodging, travelling, entertainment and many

others. All the establishments that operate in the sector require procuring adequate quantity of funds

and managing it adequately so as to generate maximum return and fulfil financial objectives.

Moreover, with the changing market conditions and customer preferences, it becomes essential for

the entities to make sure proper funds availability, so that, they can respond quickly market

challenges and manage risk as well. The aim of the present project report is to acquire knowledge

and skills that will assist management to make best quality of decisions for the smooth functioning.

Moreover, the significance of cost, volume and profit analysis will be demonstrated, through which,

travel and tourism companies can manage their operations successfully. Along with this, the report

will also explain various pricing methods by which Merlin Entertainment Plc can decide their

product prices for revenue collection. At the end, assignment will interpret annual statement of The

Restaurant Group (TRG) to examine and evaluate the operational performance and financial

strength. Along with this, report will also explain different type of funding sources whereby

companies can raise money to meet their capital requirement.

TASK 1

1.1

According to the given scenario, Merlin Entertainment Plc (MEP) is a United Kingdom based

entertainment company which is operation around 115 attractions in 23 countries across four

continents. It is running its operations through three segments that are Midway Attraction,

LEGOLAND Parks and Resort Theme Parks. Out of these, first segment conduct limited number of

operations as it is located in city centers and resorts, while, LEGOLAND Park comprises LEGO

themed accommodation, rides and shows as well. Similarly, Resort Themes Parks encompasses

rides, accommodation and shows.

With the volatility in consumer demand, tough competition, high pricing pressure, MEP’s

managers are responsible to manage their business cost and maximize their return. Cost-Volume-

profit (CVP) analysis is an effective technique which companies can use to measure the impact of

volatility in cost and volume on their operational expenditures and net yield (Altinay and et.al.,

2015). CVP technique works as an important managerial way that will assist MEP’s managers to

examine the relationship between business cost and their overall return. With the help of this, they

can identify that how changes in cost of goods production and distribution will bring changes in net

3

Travel and tourism sector is service-oriented enterprises operates in hospitality industry which

objective is to deliver wide range of services like lodging, travelling, entertainment and many

others. All the establishments that operate in the sector require procuring adequate quantity of funds

and managing it adequately so as to generate maximum return and fulfil financial objectives.

Moreover, with the changing market conditions and customer preferences, it becomes essential for

the entities to make sure proper funds availability, so that, they can respond quickly market

challenges and manage risk as well. The aim of the present project report is to acquire knowledge

and skills that will assist management to make best quality of decisions for the smooth functioning.

Moreover, the significance of cost, volume and profit analysis will be demonstrated, through which,

travel and tourism companies can manage their operations successfully. Along with this, the report

will also explain various pricing methods by which Merlin Entertainment Plc can decide their

product prices for revenue collection. At the end, assignment will interpret annual statement of The

Restaurant Group (TRG) to examine and evaluate the operational performance and financial

strength. Along with this, report will also explain different type of funding sources whereby

companies can raise money to meet their capital requirement.

TASK 1

1.1

According to the given scenario, Merlin Entertainment Plc (MEP) is a United Kingdom based

entertainment company which is operation around 115 attractions in 23 countries across four

continents. It is running its operations through three segments that are Midway Attraction,

LEGOLAND Parks and Resort Theme Parks. Out of these, first segment conduct limited number of

operations as it is located in city centers and resorts, while, LEGOLAND Park comprises LEGO

themed accommodation, rides and shows as well. Similarly, Resort Themes Parks encompasses

rides, accommodation and shows.

With the volatility in consumer demand, tough competition, high pricing pressure, MEP’s

managers are responsible to manage their business cost and maximize their return. Cost-Volume-

profit (CVP) analysis is an effective technique which companies can use to measure the impact of

volatility in cost and volume on their operational expenditures and net yield (Altinay and et.al.,

2015). CVP technique works as an important managerial way that will assist MEP’s managers to

examine the relationship between business cost and their overall return. With the help of this, they

can identify that how changes in cost of goods production and distribution will bring changes in net

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profitability. Cutting-down of both fixed and variable cost and larger sales volume are the basic

ways to improve net earnings. CVP analysis is of great importance because through applying this

model in business practice, MEP can determine the most profitable combination so as to generate

greater yield (Quattrone, 2016). This mechanism assists companies in making effective short-term

decisions and reach targets easily. The significance of CVP tool for MEP is outlined below:

Break-even analysis: The most important benefit of CVP analysis is that it will assist MEP to

determine their break-even point (BEP). It represents the situation at where cost becomes similar to

the total revenue that is a sign of maximum and optimal utilization of available business resources.

It is necessary for the company to know their BEP because through this, they can identify that how

much units they are essential require to sale to cover their total cost and thereby eliminate the

possibility of loss. Every additional unit after this level contributes towards more profitability while

if MEP made less sales than it will bear loss.

Contribution: According to marginal costing practices in cost accounting, contribution

represents the different between total turnover and variable cost. Thus, it does not take into account

fixed cost because MEP will have to bear such expenditures even at the time of nil production. In

such regards, variable expenditures are those which will be increase simultaneously with the

increase in sales volume (WisCombe and et.al., 2016). However, fixed expenditure remains constant

and does not tend to vary according to the change in output. With regards to MEP, its variable cost

comprises meal cost, cost of entertainment services, accommodation facilities etc. Through

employing CVP analysis, it can determine their contribution margin by subtracting total variable

cost from the total sales. Thus, by controlling of variable expenditures and larger turnover, MEP

will be able to maximize their contribution to a great extent.

Profit margin: Contribution less of total fixed cost represents net yield or profit. Referring

MEP, insurance, depreciation, rent of premises etc. are the fixed cost which business needs to bear

even when it does not produce a single unit of product or service (Camilleri, 2015). CVP analysis

enables entrepreneur to determine their net yield by deducting their total of fixed and variable cost

from total turnover.

Profit volume ratio: PVR measure the contribution percentage over the total sales revenues.

Higher the contribution % is a good sign of business return because it indicates that MEP has

maintained an effective control over variable cost so as to enlarge their contribution.

1.2

Not only the determination of cost is sufficient, but also, it is essential for MEP to set correct

selling price for their goods and services offered to the consumers. It is because; very high product

4

ways to improve net earnings. CVP analysis is of great importance because through applying this

model in business practice, MEP can determine the most profitable combination so as to generate

greater yield (Quattrone, 2016). This mechanism assists companies in making effective short-term

decisions and reach targets easily. The significance of CVP tool for MEP is outlined below:

Break-even analysis: The most important benefit of CVP analysis is that it will assist MEP to

determine their break-even point (BEP). It represents the situation at where cost becomes similar to

the total revenue that is a sign of maximum and optimal utilization of available business resources.

It is necessary for the company to know their BEP because through this, they can identify that how

much units they are essential require to sale to cover their total cost and thereby eliminate the

possibility of loss. Every additional unit after this level contributes towards more profitability while

if MEP made less sales than it will bear loss.

Contribution: According to marginal costing practices in cost accounting, contribution

represents the different between total turnover and variable cost. Thus, it does not take into account

fixed cost because MEP will have to bear such expenditures even at the time of nil production. In

such regards, variable expenditures are those which will be increase simultaneously with the

increase in sales volume (WisCombe and et.al., 2016). However, fixed expenditure remains constant

and does not tend to vary according to the change in output. With regards to MEP, its variable cost

comprises meal cost, cost of entertainment services, accommodation facilities etc. Through

employing CVP analysis, it can determine their contribution margin by subtracting total variable

cost from the total sales. Thus, by controlling of variable expenditures and larger turnover, MEP

will be able to maximize their contribution to a great extent.

Profit margin: Contribution less of total fixed cost represents net yield or profit. Referring

MEP, insurance, depreciation, rent of premises etc. are the fixed cost which business needs to bear

even when it does not produce a single unit of product or service (Camilleri, 2015). CVP analysis

enables entrepreneur to determine their net yield by deducting their total of fixed and variable cost

from total turnover.

Profit volume ratio: PVR measure the contribution percentage over the total sales revenues.

Higher the contribution % is a good sign of business return because it indicates that MEP has

maintained an effective control over variable cost so as to enlarge their contribution.

1.2

Not only the determination of cost is sufficient, but also, it is essential for MEP to set correct

selling price for their goods and services offered to the consumers. It is because; very high product

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

price will result in loss of customers whereas very little charges will negatively impact total sales

revenue and profitability as well. Thus, prices must be decided to an acceptable or affordable level

at which consumers will be willing to buy services and at the same time, company also can gather

sufficient return at such prices (Chang, 2013). There are wide ranges of pricing techniques and

methods available to the MEP to determine their prices at which they will offer services to the

audiences, presented here as under:

Cost-oriented or cost-centric method: This pricing technique pays focus to the cost of the

product, comprising both direct as well as indirect spending and fixed as well as variable cost

(Santana-Talavera, 2016). As per the method, MEP can set appropriate selling prices for their

services by taking into account desired mark-up percentage and service cost as well, can be

represented as follows:

Selling price = Cost + Desired or target mark-up % on cost

Cost = Average fixed cost (AFC) + Average variable cost (AVC)

In this, desired mark-up % is regarded as profit % that an entity is expecting to receive

through the selling of their services. Thus, higher the mark-up % by MEP helps to procure larger

yield on total sales or vice-versa (Chand, 2012). The most important advantage of this way of

pricing determination is it helps to cover total cost of production and distribution and assure return

in the business.

Competition-based pricing: Large number of tourists from overall world visit UK every

year to enjoy their life. Due to rapid increase in number of visitors with having differences in

demand and preferences, the level of competition in the sector becomes very tough. Therefore,

while making pricing decisions, it becomes necessary for the MEP to take into consideration that

what competitors are charging for their products and services and set their own prices accordingly

(Kaplan and Atkinson, 2015). It does not necessarily means that MEP has to decide perfectly

equivalent selling prices to that of competitors. They can decide prices to some extent by delivering

more better and unique services to deliver best value to the audiences for their money invested. It is

considered effective technique to compete effectively in the market place. In UK travel and tourism

industry, aviation segment use this pricing method to set fair charges for airline services

(Papatheodorou, 2016).

Demand-based pricing: Under this method, MEP first has to anticipate or forecast their

market demand and prices will be finalized according to the demand level. Referring MEP, in case

of having the possibility of larger customer demand, manager can set high prices whilst if the

demand is comparatively less than low price should be charged to attract more audiences (Platzer,

2014). The success of this method is highly dependent upon the ability of manager to correctly

5

revenue and profitability as well. Thus, prices must be decided to an acceptable or affordable level

at which consumers will be willing to buy services and at the same time, company also can gather

sufficient return at such prices (Chang, 2013). There are wide ranges of pricing techniques and

methods available to the MEP to determine their prices at which they will offer services to the

audiences, presented here as under:

Cost-oriented or cost-centric method: This pricing technique pays focus to the cost of the

product, comprising both direct as well as indirect spending and fixed as well as variable cost

(Santana-Talavera, 2016). As per the method, MEP can set appropriate selling prices for their

services by taking into account desired mark-up percentage and service cost as well, can be

represented as follows:

Selling price = Cost + Desired or target mark-up % on cost

Cost = Average fixed cost (AFC) + Average variable cost (AVC)

In this, desired mark-up % is regarded as profit % that an entity is expecting to receive

through the selling of their services. Thus, higher the mark-up % by MEP helps to procure larger

yield on total sales or vice-versa (Chand, 2012). The most important advantage of this way of

pricing determination is it helps to cover total cost of production and distribution and assure return

in the business.

Competition-based pricing: Large number of tourists from overall world visit UK every

year to enjoy their life. Due to rapid increase in number of visitors with having differences in

demand and preferences, the level of competition in the sector becomes very tough. Therefore,

while making pricing decisions, it becomes necessary for the MEP to take into consideration that

what competitors are charging for their products and services and set their own prices accordingly

(Kaplan and Atkinson, 2015). It does not necessarily means that MEP has to decide perfectly

equivalent selling prices to that of competitors. They can decide prices to some extent by delivering

more better and unique services to deliver best value to the audiences for their money invested. It is

considered effective technique to compete effectively in the market place. In UK travel and tourism

industry, aviation segment use this pricing method to set fair charges for airline services

(Papatheodorou, 2016).

Demand-based pricing: Under this method, MEP first has to anticipate or forecast their

market demand and prices will be finalized according to the demand level. Referring MEP, in case

of having the possibility of larger customer demand, manager can set high prices whilst if the

demand is comparatively less than low price should be charged to attract more audiences (Platzer,

2014). The success of this method is highly dependent upon the ability of manager to correctly

5

estimate the demand in forthcoming years. In UK hospitality industry, many of travel and tourism

companies use this method to decide their product prices. It is considered as best technique for MEP

which enable establishment to maximize their net return if customers are willing to pay high

charges for their products and services.

1.3

There are numerous factors which impact either positively or negatively the corporate yield.

Some of the most important components along with their affects on business return are described

underneath:

Selling price: MEP will generate revenues through delivering accommodation, hotel, meal

and other entertainment like rides, shows to the consumers. Thus, selling price is the most essential

component that affects its profitability as high selling prices contributes towards grown revenues or

vice-versa (Zhou-Grundy and Turner, 2014). At the same time, it must be focused that very high

prices can influence profit negatively especially in the case, when MEP’s rivalries are rendering

services at cheaper rates. Thus, it can be said that keeping other factors constant, high prices lead to

incline total sales or vice-versa.

Cost of goods and services: Profit is determined by subtracting total cost from the business

turnover. Thus, cost is another important element that affect MEP’s return, larger the product cost

decrease net earnings whereas if company is able to control their expenditures than it can maximize

their net yield (McNaughton, McLeod and Boxill, 2016). Thus, it can be advised to MEP to

minimize their operational spending through regular monitoring via budget and thereby improve

their return position to a large extent. In such respect, larger output helps to decrease cost per unit

(CPU) due to economies of scale, which in turn, results in larger earnings.

Volume of sales: Higher the number of sales units, keeping other factors unchanged will

definitely assist MEP to maximize their net earnings. The reason behind this is if MEP became able

to attract more and more visitors and deliver services in large quantity then it will be able to

generate greater revenue at same level of cost, thus, profit can be raised.

Market fluctuations: The success of hospitality industry is greatly based upon the level of

consumer satisfaction. While, in the market, wide range of fluctuations can be seen in relation to

customer taste, preferences and attitude (Shariff, Kayat and Abidin, 2014). Thus, MEP’s

profitability also will be affected by seasonal variations and changes in social preferences.

Moreover, change in political rules and regulations and economic conditions also impact business

profitability to a great extent.

After taking into account all the components, it can be suggested to MEP’s manager to

6

companies use this method to decide their product prices. It is considered as best technique for MEP

which enable establishment to maximize their net return if customers are willing to pay high

charges for their products and services.

1.3

There are numerous factors which impact either positively or negatively the corporate yield.

Some of the most important components along with their affects on business return are described

underneath:

Selling price: MEP will generate revenues through delivering accommodation, hotel, meal

and other entertainment like rides, shows to the consumers. Thus, selling price is the most essential

component that affects its profitability as high selling prices contributes towards grown revenues or

vice-versa (Zhou-Grundy and Turner, 2014). At the same time, it must be focused that very high

prices can influence profit negatively especially in the case, when MEP’s rivalries are rendering

services at cheaper rates. Thus, it can be said that keeping other factors constant, high prices lead to

incline total sales or vice-versa.

Cost of goods and services: Profit is determined by subtracting total cost from the business

turnover. Thus, cost is another important element that affect MEP’s return, larger the product cost

decrease net earnings whereas if company is able to control their expenditures than it can maximize

their net yield (McNaughton, McLeod and Boxill, 2016). Thus, it can be advised to MEP to

minimize their operational spending through regular monitoring via budget and thereby improve

their return position to a large extent. In such respect, larger output helps to decrease cost per unit

(CPU) due to economies of scale, which in turn, results in larger earnings.

Volume of sales: Higher the number of sales units, keeping other factors unchanged will

definitely assist MEP to maximize their net earnings. The reason behind this is if MEP became able

to attract more and more visitors and deliver services in large quantity then it will be able to

generate greater revenue at same level of cost, thus, profit can be raised.

Market fluctuations: The success of hospitality industry is greatly based upon the level of

consumer satisfaction. While, in the market, wide range of fluctuations can be seen in relation to

customer taste, preferences and attitude (Shariff, Kayat and Abidin, 2014). Thus, MEP’s

profitability also will be affected by seasonal variations and changes in social preferences.

Moreover, change in political rules and regulations and economic conditions also impact business

profitability to a great extent.

After taking into account all the components, it can be suggested to MEP’s manager to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

maximize their sales volume and selling prices (up to an acceptable level) and control their routine

expenditures to minimize their cost and enhance their yield.

TASK 2

Attached in PPT.

TASK 3

3.1

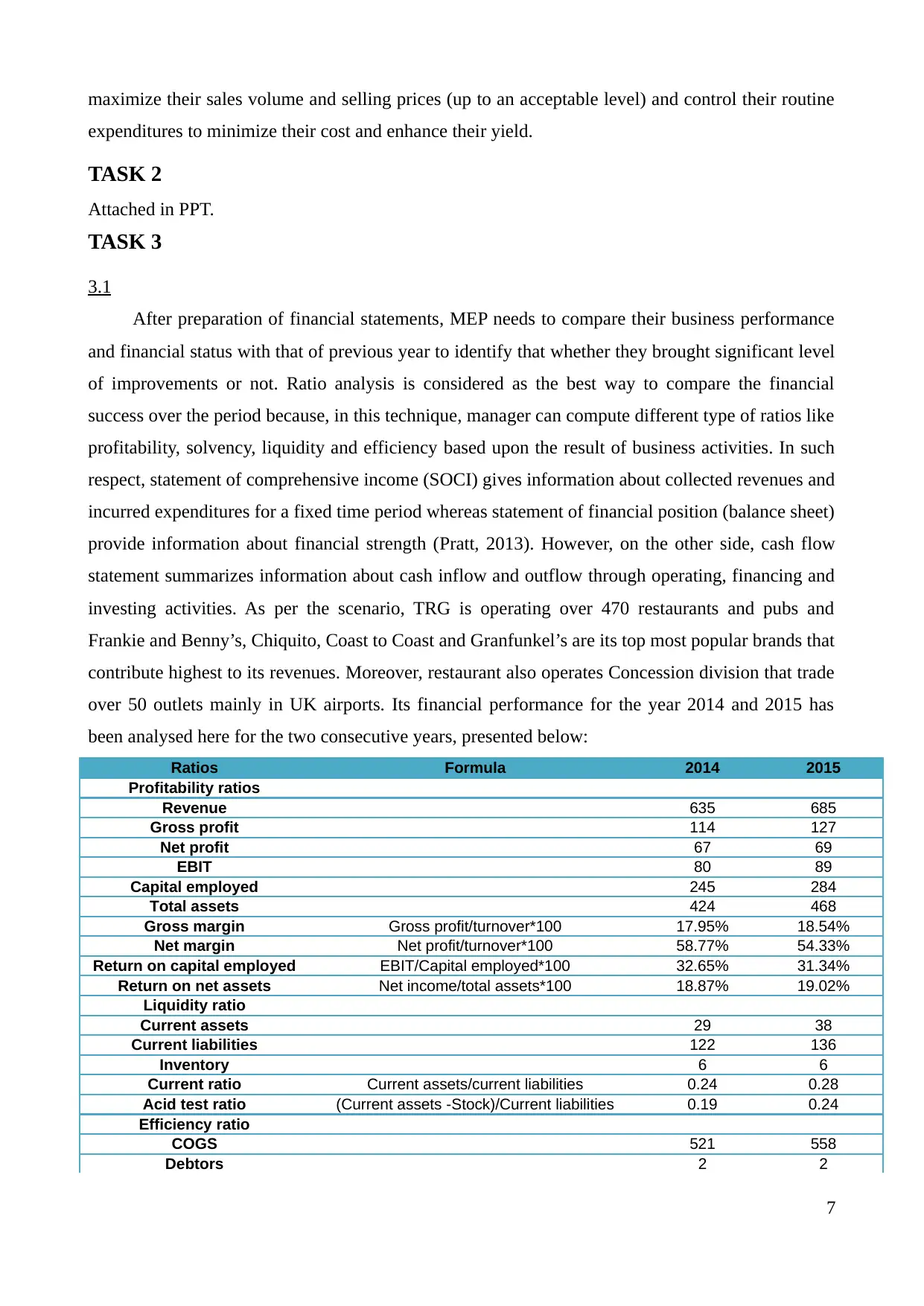

After preparation of financial statements, MEP needs to compare their business performance

and financial status with that of previous year to identify that whether they brought significant level

of improvements or not. Ratio analysis is considered as the best way to compare the financial

success over the period because, in this technique, manager can compute different type of ratios like

profitability, solvency, liquidity and efficiency based upon the result of business activities. In such

respect, statement of comprehensive income (SOCI) gives information about collected revenues and

incurred expenditures for a fixed time period whereas statement of financial position (balance sheet)

provide information about financial strength (Pratt, 2013). However, on the other side, cash flow

statement summarizes information about cash inflow and outflow through operating, financing and

investing activities. As per the scenario, TRG is operating over 470 restaurants and pubs and

Frankie and Benny’s, Chiquito, Coast to Coast and Granfunkel’s are its top most popular brands that

contribute highest to its revenues. Moreover, restaurant also operates Concession division that trade

over 50 outlets mainly in UK airports. Its financial performance for the year 2014 and 2015 has

been analysed here for the two consecutive years, presented below:

Ratios Formula 2014 2015

Profitability ratios

Revenue 635 685

Gross profit 114 127

Net profit 67 69

EBIT 80 89

Capital employed 245 284

Total assets 424 468

Gross margin Gross profit/turnover*100 17.95% 18.54%

Net margin Net profit/turnover*100 58.77% 54.33%

Return on capital employed EBIT/Capital employed*100 32.65% 31.34%

Return on net assets Net income/total assets*100 18.87% 19.02%

Liquidity ratio

Current assets 29 38

Current liabilities 122 136

Inventory 6 6

Current ratio Current assets/current liabilities 0.24 0.28

Acid test ratio (Current assets -Stock)/Current liabilities 0.19 0.24

Efficiency ratio

COGS 521 558

Debtors 2 2

7

expenditures to minimize their cost and enhance their yield.

TASK 2

Attached in PPT.

TASK 3

3.1

After preparation of financial statements, MEP needs to compare their business performance

and financial status with that of previous year to identify that whether they brought significant level

of improvements or not. Ratio analysis is considered as the best way to compare the financial

success over the period because, in this technique, manager can compute different type of ratios like

profitability, solvency, liquidity and efficiency based upon the result of business activities. In such

respect, statement of comprehensive income (SOCI) gives information about collected revenues and

incurred expenditures for a fixed time period whereas statement of financial position (balance sheet)

provide information about financial strength (Pratt, 2013). However, on the other side, cash flow

statement summarizes information about cash inflow and outflow through operating, financing and

investing activities. As per the scenario, TRG is operating over 470 restaurants and pubs and

Frankie and Benny’s, Chiquito, Coast to Coast and Granfunkel’s are its top most popular brands that

contribute highest to its revenues. Moreover, restaurant also operates Concession division that trade

over 50 outlets mainly in UK airports. Its financial performance for the year 2014 and 2015 has

been analysed here for the two consecutive years, presented below:

Ratios Formula 2014 2015

Profitability ratios

Revenue 635 685

Gross profit 114 127

Net profit 67 69

EBIT 80 89

Capital employed 245 284

Total assets 424 468

Gross margin Gross profit/turnover*100 17.95% 18.54%

Net margin Net profit/turnover*100 58.77% 54.33%

Return on capital employed EBIT/Capital employed*100 32.65% 31.34%

Return on net assets Net income/total assets*100 18.87% 19.02%

Liquidity ratio

Current assets 29 38

Current liabilities 122 136

Inventory 6 6

Current ratio Current assets/current liabilities 0.24 0.28

Acid test ratio (Current assets -Stock)/Current liabilities 0.19 0.24

Efficiency ratio

COGS 521 558

Debtors 2 2

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Creditors 51 56

Stock turnover ratio Cost of goods sold/Inventory 86.83 93

Debtors receivable period Trade debtors/Revenues*365 1.15 1.07

Creditors payment period Trade payables/Cost of sales*365 35.73 36.63

Solvency ratio

Debt 39 31

Equity 245 284

Capital gearing (Long-term liabilities/Equity capital employed 0.16 0.11

Profitability narratives:

This ratio helps to examine that whether TRG has improved their operational performance

or not (Karande and Chakraborty, 2012). Gross margin (GM) got increased from 17.95% to 18.54%

due to high proportionate increase in sales by 7.87% and effective control over direct cost are the

reason behind this. While, on the other hand, its net margin (NM) shows a little bit decrease from

10.55% to 10.07% due to high indirect expenditures demonstrates that in 2015, TRG generated less

return through operations. However, ROCE got decreased from 32.65% to 31.34% and return on

total assets improved from 18.87% to 19.02% which reflects that in 2015, TRG group collected less

profit on total capital employed and high on total assets.

Liquidity narratives:

This ratio enables TRG to determine that whether they are able or not to meet out their

short-term liabilities like creditors (Drake, 2016). Current ratio (CR) has been improved from 0.24

to 0.28 whilst acid test ratio goes increased from 0.19 to 0.24 reflects that in 2015, TRG has

improved its ability to pay suppliers on right time. But still, both the ratios are far away from the

idle ratio of 2:1 and 1:1. Henceforth, it is considered better to advice restaurant’s managers to

enhance their current assets i.e. inventory, receivable and cash position and pay off their few of the

current liabilities.

Efficiency narratives:

This ratio measures that how much managers are able to utilize optimally business assets so

as to generate greater turnover (Kumbirai and Webb, 2013). TRG’s stock turnover ratio got

improved from 86.83 to 93 which isa sign of high managerial efficiency to effectively use business

inventory. While, on the other side, debtors receivable period got decreased from 1.15 to 1.07 days

demonstrating that TRG is generating quicker cash from their receivables. Moreover, high creditors’

payment period from 35.73 to 36.73 days reveal that restaurant managers are paying suppliers

delayed for the better availability of cash in the business.

Solvency narratives:

Managers need to manage their financial risk through constructing the best mix of both debt

and equity in their capital structure (Pratt, 2013). Declined capital gearing (debt-to-equity ratio)

8

Stock turnover ratio Cost of goods sold/Inventory 86.83 93

Debtors receivable period Trade debtors/Revenues*365 1.15 1.07

Creditors payment period Trade payables/Cost of sales*365 35.73 36.63

Solvency ratio

Debt 39 31

Equity 245 284

Capital gearing (Long-term liabilities/Equity capital employed 0.16 0.11

Profitability narratives:

This ratio helps to examine that whether TRG has improved their operational performance

or not (Karande and Chakraborty, 2012). Gross margin (GM) got increased from 17.95% to 18.54%

due to high proportionate increase in sales by 7.87% and effective control over direct cost are the

reason behind this. While, on the other hand, its net margin (NM) shows a little bit decrease from

10.55% to 10.07% due to high indirect expenditures demonstrates that in 2015, TRG generated less

return through operations. However, ROCE got decreased from 32.65% to 31.34% and return on

total assets improved from 18.87% to 19.02% which reflects that in 2015, TRG group collected less

profit on total capital employed and high on total assets.

Liquidity narratives:

This ratio enables TRG to determine that whether they are able or not to meet out their

short-term liabilities like creditors (Drake, 2016). Current ratio (CR) has been improved from 0.24

to 0.28 whilst acid test ratio goes increased from 0.19 to 0.24 reflects that in 2015, TRG has

improved its ability to pay suppliers on right time. But still, both the ratios are far away from the

idle ratio of 2:1 and 1:1. Henceforth, it is considered better to advice restaurant’s managers to

enhance their current assets i.e. inventory, receivable and cash position and pay off their few of the

current liabilities.

Efficiency narratives:

This ratio measures that how much managers are able to utilize optimally business assets so

as to generate greater turnover (Kumbirai and Webb, 2013). TRG’s stock turnover ratio got

improved from 86.83 to 93 which isa sign of high managerial efficiency to effectively use business

inventory. While, on the other side, debtors receivable period got decreased from 1.15 to 1.07 days

demonstrating that TRG is generating quicker cash from their receivables. Moreover, high creditors’

payment period from 35.73 to 36.73 days reveal that restaurant managers are paying suppliers

delayed for the better availability of cash in the business.

Solvency narratives:

Managers need to manage their financial risk through constructing the best mix of both debt

and equity in their capital structure (Pratt, 2013). Declined capital gearing (debt-to-equity ratio)

8

from 0.16:1 to 0.11:1 is a sign of less financial risk because of repayment of debt and more

collection of equity capital amounted to 8 and 39. But still, 0.5:1 is considered as idle ratio that

reflects that TRG must use 50% debt resources in their capital structure to manage their financial

risk. Henceforth, it is considered advisable that TRG must collect more debt to meet their capital

requirement and thereby maintain solvency position.

TASK 4

4.1

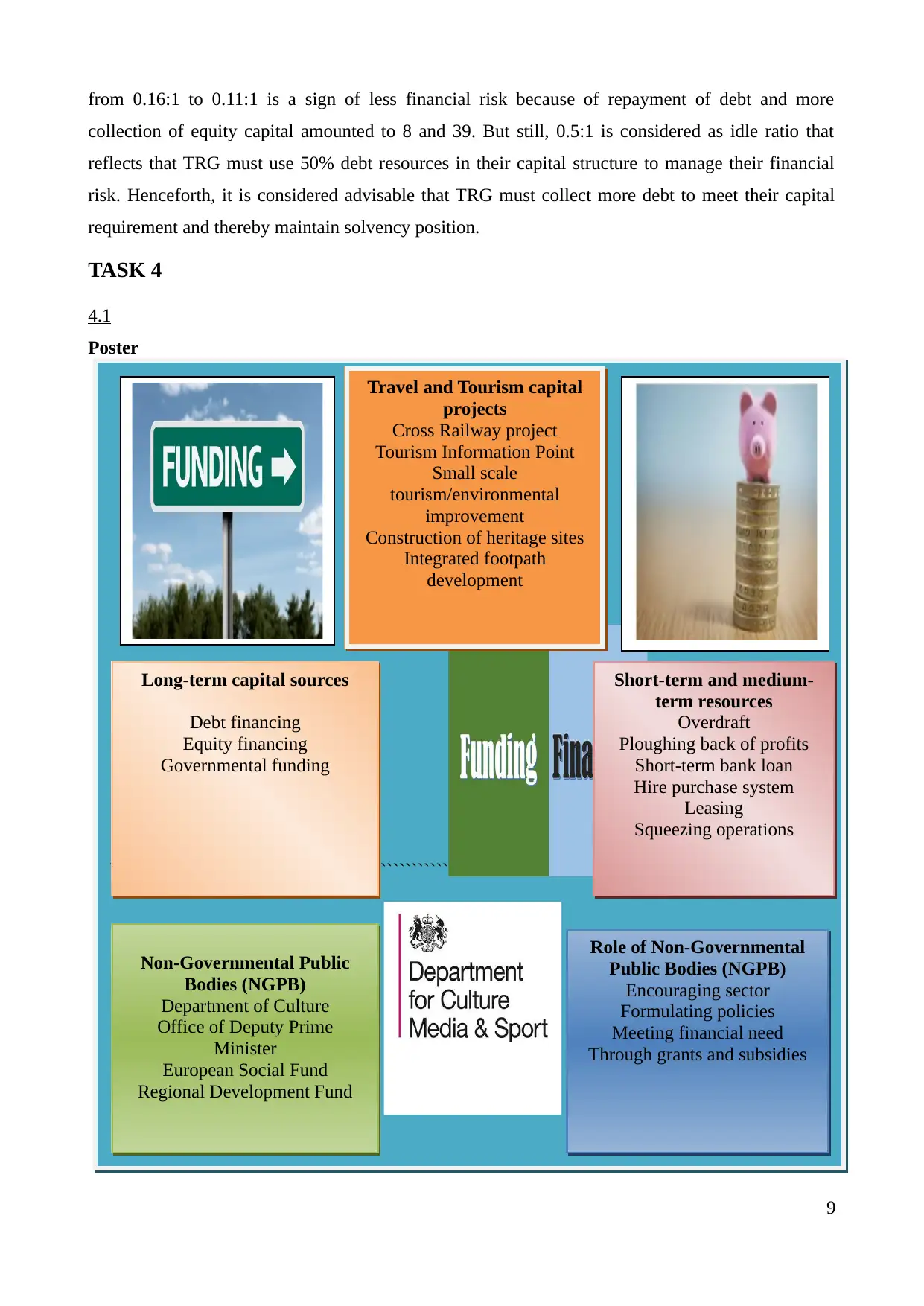

Poster

As already stated earlier, that the level of competition in UK hospitality sector is very high,

9

````````` `````````````````````````````````````

Travel and Tourism capital

projects

Cross Railway project

Tourism Information Point

Small scale

tourism/environmental

improvement

Construction of heritage sites

Integrated footpath

development

Long-term capital sources

Debt financing

Equity financing

Governmental funding

Short-term and medium-

term resources

Overdraft

Ploughing back of profits

Short-term bank loan

Hire purchase system

Leasing

Squeezing operations

Non-Governmental Public

Bodies (NGPB)

Department of Culture

Office of Deputy Prime

Minister

European Social Fund

Regional Development Fund

Role of Non-Governmental

Public Bodies (NGPB)

Encouraging sector

Formulating policies

Meeting financial need

Through grants and subsidies

collection of equity capital amounted to 8 and 39. But still, 0.5:1 is considered as idle ratio that

reflects that TRG must use 50% debt resources in their capital structure to manage their financial

risk. Henceforth, it is considered advisable that TRG must collect more debt to meet their capital

requirement and thereby maintain solvency position.

TASK 4

4.1

Poster

As already stated earlier, that the level of competition in UK hospitality sector is very high,

9

````````` `````````````````````````````````````

Travel and Tourism capital

projects

Cross Railway project

Tourism Information Point

Small scale

tourism/environmental

improvement

Construction of heritage sites

Integrated footpath

development

Long-term capital sources

Debt financing

Equity financing

Governmental funding

Short-term and medium-

term resources

Overdraft

Ploughing back of profits

Short-term bank loan

Hire purchase system

Leasing

Squeezing operations

Non-Governmental Public

Bodies (NGPB)

Department of Culture

Office of Deputy Prime

Minister

European Social Fund

Regional Development Fund

Role of Non-Governmental

Public Bodies (NGPB)

Encouraging sector

Formulating policies

Meeting financial need

Through grants and subsidies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

thus, it becomes essential for the organizations to gather sufficient capital from different sources to

meet their capital requirement effectively (Bebbington and Thomson, 2013). In order to funding

various capital projects like Cross Railway project, Tourism Information Point, small scale

tourism/environmental improvement, construction of heritage sites, integrated footpath

development, it seems necessary for the firms to gather adequate funds from the most suitable

finance source, There are wide range of finance sources available to travel and tourism companies

to meet their financial requirement, describing underneath:

Debt funding: In UK, commercial banks and financial institutions provide short-term,

medium-term and long-term funding services to the entrepreneurs at an interest rate. In order to

fulfil financial need for capital projects, travel and tourism organizations can apply for long-term

loans and raise their money by providing them collateral security or mortgage assets (Jackson,

Keune and Salzsieder, 2013). On the amount of loans, company will be liable to pay interest

periodically, otherwise, bank have authority to seize the assets so as to get back their funds. While,

it is considered as cheaper source of finance because taxation authority deduct interest amount when

determine corporate tax obligations. Moreover, it also provide convinces to the entities regarding

the repayment of debt in equal periodical instalments.

Equity funding: Entrepreneurs can also gather money through offering both the preference

and equity shares to the public. On the preference share capital, organizations will be liable to pay

fixed rate of dividend to the shareholders, however, on equity share capital; the rate of dividend is

not fixed (Vernimmen and et.al., 2014). Moreover, at the time of loss, company may decide to not

distribute dividend to the ordinary shareholders. Higher the public subscription enables businesses

to meet their financial requirement to a great extent. But still, it has one negative impact that is

shareholders have right to take part in business decisions, through which, they can interfere in

managerial decisions and minimize their freedom.

Government funding: In UK, regulatory bodies like Department of Culture, Media and

Sport, Office of Deputy Prime Minister, European Social Fund and Regional Development Fund

play an important role. The main objective of all the Non-Governmental Public Bodies (NGPB) is

to encourage and promote the growth of the sector (Vernimmen and et.al., 2014). In order to meet

this objective, they also provide financial assistance to the corporations by providing them grant and

subsidies i.e. tax subsidy. Thus, companies can meet their capital need by receiving governmental

grants to financing their capital projects. It must be noticed that the amount of grant must be used

for the specific purpose and within prescribed time limit; otherwise, it will be lapse.

Apart from this, overdraft, squeezing operations, hire purchase, leasing, ploughing back of

profits are the other financial sources available, through which, entities can meet their short-term

10

meet their capital requirement effectively (Bebbington and Thomson, 2013). In order to funding

various capital projects like Cross Railway project, Tourism Information Point, small scale

tourism/environmental improvement, construction of heritage sites, integrated footpath

development, it seems necessary for the firms to gather adequate funds from the most suitable

finance source, There are wide range of finance sources available to travel and tourism companies

to meet their financial requirement, describing underneath:

Debt funding: In UK, commercial banks and financial institutions provide short-term,

medium-term and long-term funding services to the entrepreneurs at an interest rate. In order to

fulfil financial need for capital projects, travel and tourism organizations can apply for long-term

loans and raise their money by providing them collateral security or mortgage assets (Jackson,

Keune and Salzsieder, 2013). On the amount of loans, company will be liable to pay interest

periodically, otherwise, bank have authority to seize the assets so as to get back their funds. While,

it is considered as cheaper source of finance because taxation authority deduct interest amount when

determine corporate tax obligations. Moreover, it also provide convinces to the entities regarding

the repayment of debt in equal periodical instalments.

Equity funding: Entrepreneurs can also gather money through offering both the preference

and equity shares to the public. On the preference share capital, organizations will be liable to pay

fixed rate of dividend to the shareholders, however, on equity share capital; the rate of dividend is

not fixed (Vernimmen and et.al., 2014). Moreover, at the time of loss, company may decide to not

distribute dividend to the ordinary shareholders. Higher the public subscription enables businesses

to meet their financial requirement to a great extent. But still, it has one negative impact that is

shareholders have right to take part in business decisions, through which, they can interfere in

managerial decisions and minimize their freedom.

Government funding: In UK, regulatory bodies like Department of Culture, Media and

Sport, Office of Deputy Prime Minister, European Social Fund and Regional Development Fund

play an important role. The main objective of all the Non-Governmental Public Bodies (NGPB) is

to encourage and promote the growth of the sector (Vernimmen and et.al., 2014). In order to meet

this objective, they also provide financial assistance to the corporations by providing them grant and

subsidies i.e. tax subsidy. Thus, companies can meet their capital need by receiving governmental

grants to financing their capital projects. It must be noticed that the amount of grant must be used

for the specific purpose and within prescribed time limit; otherwise, it will be lapse.

Apart from this, overdraft, squeezing operations, hire purchase, leasing, ploughing back of

profits are the other financial sources available, through which, entities can meet their short-term

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and medium-term capital need.

CONCLUSION

Report concluded the fact that CVP analysis works as an effective technique that assist Merlin

Entertainment Plc to identify the impact of different cost on their total return. Through employing

this technique, manager can make qualitative short-term decisions by making more and more sales

beyond BEP level. Moreover, its managers can evaluate and examine financial statements and can

use standard costing to meet targets via formulating better policies and decisions as well. Along

with this, application of ratio analysis technique inferred that The Restaurant Group’s profitability,

solvency and liquidity position is not effectively managed, therefore, financial manager has to make

better decisions for the performing much well in forthcoming years. At the end, report concluded

that debt, equity and governmental funding are the sources of finance available to travel and tourism

companies to raise availability of money for the capital projects. Out of these, the cost of debt is

considered cheaper than equity because government consider interest payments on loans as

deductible expenses, which in turn, minimizes tax obligations. While, equity capital does not

impose fixed financial burden as dividend rate is not fixed. Henceforth, it can be suggested that

companies has to decide an optimum mix of both the debt and equity in their capital structure to

accomplish their financial requirement.

11

CONCLUSION

Report concluded the fact that CVP analysis works as an effective technique that assist Merlin

Entertainment Plc to identify the impact of different cost on their total return. Through employing

this technique, manager can make qualitative short-term decisions by making more and more sales

beyond BEP level. Moreover, its managers can evaluate and examine financial statements and can

use standard costing to meet targets via formulating better policies and decisions as well. Along

with this, application of ratio analysis technique inferred that The Restaurant Group’s profitability,

solvency and liquidity position is not effectively managed, therefore, financial manager has to make

better decisions for the performing much well in forthcoming years. At the end, report concluded

that debt, equity and governmental funding are the sources of finance available to travel and tourism

companies to raise availability of money for the capital projects. Out of these, the cost of debt is

considered cheaper than equity because government consider interest payments on loans as

deductible expenses, which in turn, minimizes tax obligations. While, equity capital does not

impose fixed financial burden as dividend rate is not fixed. Henceforth, it can be suggested that

companies has to decide an optimum mix of both the debt and equity in their capital structure to

accomplish their financial requirement.

11

REFERENCES

Books and Journals

Altinay, L. and et.al., 2015. Social entrepreneurship in tourism. In The 5th Advances in Hospitality

& Tourism Marketing and Management (AHTMM) Conference, Beppu, Japan, 18-21 June

2015.). Washington State University. 16(3). pp. 453-461.

Bebbington, J. and Thomson, I., 2013. Sustainable development, management and accounting:

Boundary crossing. Management Accounting Research. 4(24). pp. 277-283.

Camilleri, M. A., 2015. Nurturing travel and tourism enterprises for economic growth and

competitiveness. Tourism and Hospitality Research. 13(3). p.1467358415621947.

Chang, H. C., 2013. Environmental management accounting in the Taiwanese higher education

sector: issues and opportunities. International Journal of Sustainability in Higher

Education. 14(2). pp. 133-145.

Jackson, S. B., Keune, T. M. and Salzsieder, L., 2013. Debt, equity, and capital investment. Journal

of Accounting and Economics. 56(2). pp. 291-310.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37(3). pp.317-

324.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1). pp. 30-53.

McNaughton, M., McLeod, M. T. and Boxill, I., 2016. An Actor Network Perspective of Tourism

Open Data. In Tourism and Hospitality Management. Emerald Group Publishing Limited.

12(3). pp. 47-60.

Papatheodorou, A., 2016. Aviation and Tourism: Implications for Leisure Travel. Routledge.

Platzer, M. D., 2014. US Travel and Tourism: Industry Trends and Policy Issues for Congress.

Pratt, J., 2013. Financial accounting in an economic context. Wiley Global Education.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31(5). pp. 118-122.

Santana-Talavera, A., 2016. Julio Aramberri: a sociological review of tourism studies. Anatolia.

16(6).pp. 1-7.

Shariff, N. M., Kayat, K. and Abidin, A. Z., 2014. Tourism and hospitality graduates competencies:

Industry perceptions and expectations in the Malaysian perspectives. World Applied

Sciences Journal. 31(11). pp. 1992-2000.

12

Books and Journals

Altinay, L. and et.al., 2015. Social entrepreneurship in tourism. In The 5th Advances in Hospitality

& Tourism Marketing and Management (AHTMM) Conference, Beppu, Japan, 18-21 June

2015.). Washington State University. 16(3). pp. 453-461.

Bebbington, J. and Thomson, I., 2013. Sustainable development, management and accounting:

Boundary crossing. Management Accounting Research. 4(24). pp. 277-283.

Camilleri, M. A., 2015. Nurturing travel and tourism enterprises for economic growth and

competitiveness. Tourism and Hospitality Research. 13(3). p.1467358415621947.

Chang, H. C., 2013. Environmental management accounting in the Taiwanese higher education

sector: issues and opportunities. International Journal of Sustainability in Higher

Education. 14(2). pp. 133-145.

Jackson, S. B., Keune, T. M. and Salzsieder, L., 2013. Debt, equity, and capital investment. Journal

of Accounting and Economics. 56(2). pp. 291-310.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Karande, P. and Chakraborty, S., 2012. Application of multi-objective optimization on the basis of

ratio analysis (MOORA) method for materials selection. Materials & Design. 37(3). pp.317-

324.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank performance in

South Africa. African Review of Economics and Finance. 2(1). pp. 30-53.

McNaughton, M., McLeod, M. T. and Boxill, I., 2016. An Actor Network Perspective of Tourism

Open Data. In Tourism and Hospitality Management. Emerald Group Publishing Limited.

12(3). pp. 47-60.

Papatheodorou, A., 2016. Aviation and Tourism: Implications for Leisure Travel. Routledge.

Platzer, M. D., 2014. US Travel and Tourism: Industry Trends and Policy Issues for Congress.

Pratt, J., 2013. Financial accounting in an economic context. Wiley Global Education.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31(5). pp. 118-122.

Santana-Talavera, A., 2016. Julio Aramberri: a sociological review of tourism studies. Anatolia.

16(6).pp. 1-7.

Shariff, N. M., Kayat, K. and Abidin, A. Z., 2014. Tourism and hospitality graduates competencies:

Industry perceptions and expectations in the Malaysian perspectives. World Applied

Sciences Journal. 31(11). pp. 1992-2000.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.