Finance Report: Financial Analysis of Business Operations (2nd Sem)

VerifiedAdded on 2020/06/06

|17

|4173

|89

Report

AI Summary

This finance report provides an in-depth analysis of key financial concepts. It begins with an introduction to finance and its importance in business, followed by an examination of stakeholders and their contributions to external accounting. The report then explores different types of medium and long-term financing, including buyer credits, supplier credits, and equity financing. It delves into the calculation of WACC and NPV, comparing two investment projects and analyzing the strengths and weaknesses of investment appraisal techniques like ARR, payback period, IRR, and NPV. The report further distinguishes between variable and fixed costs, analyzes an income statement with break-even points and marginal costing, and evaluates operating and cash conversion cycles. The report concludes with a comprehensive overview of financial tools and techniques, providing valuable insights for financial decision-making and organizational stability. The report emphasizes the importance of financial management in achieving both short-term and long-term business objectives.

Introduction of finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION:1..................................................................................................................................1

A): Stakeholders of business and there contribution to reporting external accounting..............1

b): Types of medium and long-term finance ..............................................................................3

QUESTION: 2.................................................................................................................................4

a): WACC of Redrock plc...........................................................................................................4

b): NPV computation..................................................................................................................5

c): Analysis of two projects.........................................................................................................5

d): Strength and weaknesses of investment appraisal techniques...............................................5

QUESTION 3...................................................................................................................................7

(a) Examples subject to distinguish between variable and fixed cost.........................................7

(b) Income statement, analysation of break even[points and contribution per unit....................8

(c) Assessment of advantages and disadvantages of marginal costing.......................................8

QUESTION 4...................................................................................................................................9

(a) Difference between organisation's operating cycle and its cash conversions cycle..............9

(b) Practical evaluation of operating and cash conversion cycle..............................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

QUESTION:1..................................................................................................................................1

A): Stakeholders of business and there contribution to reporting external accounting..............1

b): Types of medium and long-term finance ..............................................................................3

QUESTION: 2.................................................................................................................................4

a): WACC of Redrock plc...........................................................................................................4

b): NPV computation..................................................................................................................5

c): Analysis of two projects.........................................................................................................5

d): Strength and weaknesses of investment appraisal techniques...............................................5

QUESTION 3...................................................................................................................................7

(a) Examples subject to distinguish between variable and fixed cost.........................................7

(b) Income statement, analysation of break even[points and contribution per unit....................8

(c) Assessment of advantages and disadvantages of marginal costing.......................................8

QUESTION 4...................................................................................................................................9

(a) Difference between organisation's operating cycle and its cash conversions cycle..............9

(b) Practical evaluation of operating and cash conversion cycle..............................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is an essential aspects for every business organisation without which they cannot

able to operate there business activities. The present business environment is more turbulent so it

has been seen that corporate houses can find it very hard to manage their financial statements.

The objective of business is to make proper allocation of finance so that short term and long term

goals can be attain in more quick time (Föllmer and Schied, 2011). In this particular situation,

financial managers play crucial role for the company's in organise finance from various sources.

Under the following study several financial tools and appraisal techniques are explain which are

helpful in future stability of an organisation. Those tools are effective enough to analyse

financial performance which are help in decision making for betterment of an organisation.

QUESTION:1

A): Stakeholders of business and there contribution to reporting external accounting

An individual or a group of people those are having some kind of interest and value in an

organisation. They can affect or are affected by attainment of a firms aims and objectives. In

order word, stakeholder are those person or organisation who can be directly or indirectly

impacted by decisions of the company. A stakeholder is any person, organisation, social group or

community at wide level that has certain stake into the business activities. Hence, stakeholders

can either be internal or external to the administration (Brandimarte, 2013). They are one of the

crucial element to the successful transfer of any project or event that are organise by the

organisation. Some useful examples of key stakeholder are directors, creditors, government

bodies, owners, unions and community from which the commercial enterprise can draws there

resources. It is necessary to manage stakeholder as they are most valuable parties that are

working for the motive to generate maximum profit from the company. Often the procedure of

managing stakeholder is identified by project manager in order to determine any risk associate

with the management. After making every demand of stakeholder and fulfilling there expectation

will help the company to reduce all those risk those are creating negative impacts on the

profitability of a concern.

Stakeholder model: There are various methods by which undoubtedly has huge impacts

to business in present time. It would be argue that there are collective experience of stakeholder

actions those are seen in an organisation. The knowledge of managing various change and

1

Finance is an essential aspects for every business organisation without which they cannot

able to operate there business activities. The present business environment is more turbulent so it

has been seen that corporate houses can find it very hard to manage their financial statements.

The objective of business is to make proper allocation of finance so that short term and long term

goals can be attain in more quick time (Föllmer and Schied, 2011). In this particular situation,

financial managers play crucial role for the company's in organise finance from various sources.

Under the following study several financial tools and appraisal techniques are explain which are

helpful in future stability of an organisation. Those tools are effective enough to analyse

financial performance which are help in decision making for betterment of an organisation.

QUESTION:1

A): Stakeholders of business and there contribution to reporting external accounting

An individual or a group of people those are having some kind of interest and value in an

organisation. They can affect or are affected by attainment of a firms aims and objectives. In

order word, stakeholder are those person or organisation who can be directly or indirectly

impacted by decisions of the company. A stakeholder is any person, organisation, social group or

community at wide level that has certain stake into the business activities. Hence, stakeholders

can either be internal or external to the administration (Brandimarte, 2013). They are one of the

crucial element to the successful transfer of any project or event that are organise by the

organisation. Some useful examples of key stakeholder are directors, creditors, government

bodies, owners, unions and community from which the commercial enterprise can draws there

resources. It is necessary to manage stakeholder as they are most valuable parties that are

working for the motive to generate maximum profit from the company. Often the procedure of

managing stakeholder is identified by project manager in order to determine any risk associate

with the management. After making every demand of stakeholder and fulfilling there expectation

will help the company to reduce all those risk those are creating negative impacts on the

profitability of a concern.

Stakeholder model: There are various methods by which undoubtedly has huge impacts

to business in present time. It would be argue that there are collective experience of stakeholder

actions those are seen in an organisation. The knowledge of managing various change and

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

delivering projects and keep record in more effective manner. There are basically, three

stakeholder models that enable company's to clearly articulate that they are more effective part of

the society (Peirson and et. al., 2014). Those are discuss underneath:

Illustration 1: Models of Stakeholders

(Source: Bucholtz and Carroll, 2017)

Descriptive value: Under this process, relationship among various factors are determine

those are affecting the performances of an organisation. It attempts in order to ascertain

whether company can actually do consider stakeholder interest.

Normative stakeholder model: It is associated with the presumption that are based on

stakeholder inherent value. There legitimate stakes in corporate activity is totally relies

on there interest in the business organisation (Hale and Held, 2011). It is an important

aspect that is noted while stakeholder require an acceptance that they are more valuable

2

stakeholder models that enable company's to clearly articulate that they are more effective part of

the society (Peirson and et. al., 2014). Those are discuss underneath:

Illustration 1: Models of Stakeholders

(Source: Bucholtz and Carroll, 2017)

Descriptive value: Under this process, relationship among various factors are determine

those are affecting the performances of an organisation. It attempts in order to ascertain

whether company can actually do consider stakeholder interest.

Normative stakeholder model: It is associated with the presumption that are based on

stakeholder inherent value. There legitimate stakes in corporate activity is totally relies

on there interest in the business organisation (Hale and Held, 2011). It is an important

aspect that is noted while stakeholder require an acceptance that they are more valuable

2

part of an organisation. It attempts to provide a perfect reason about why company should

take consider interest of stakeholder.

Instrumental stakeholder model: under this, managing stakeholder in efficient manner

to attain business objectives in the form of profit, growth and future sustainability. It also

allows to test link among business goals and stakeholder interest. It attempts to provide

solution to plenty of critical questions those are related with stakeholder value.

Corporations are not commonly manage in the stake of there stakeholders alone, but that

there are wide range of stakeholders. It determine various models the groups those are related

with stakeholder of a corporation and they require certain techniques to satisfy needs and

demand. In order to make crucial decision regarding proper reporting of financial statement so

that better decisions can be made on that basis.

b): Types of medium and long-term finance

Medium term financing are arrange as systematic structure for repayment for the

maximum period of five year. While, the repayment of long term can varies from 5 to 15 years.

Banks and other institution those are offering such kind of finance plan or service in support of

large projects. At the time of offering such kind of facilities they assume risk of non-payment

those are arises from the failure of the buyer or from political instability. Some of the most

common financing are:

Buyer credits: These are used to finance an export over the period of medium or long

time. By the help of this method, finances are lent instantly to the international buyers.

These are outspread on a non-recurring basis to the exporter as they enters into a direct

contract with the lending banks.

Supplier credit: In this particular case, banks can purchase from the outside parties a

international buyers for goods and services (Esty, 2014). Arranging such kind of finance

can be more easier and affordable than arranging a buyer credit. Under this situation, not

any parties has to directly deal or negotiate with foreign clients.

Counter trade: It is an arrangement in which a sale to an importer is conditional on a

correlative purchasing done by the merchandise. Such kind of finance is related with

counter purchase and offset arrangements.

Export leasing: It is mostly associated with private companies that are specialise in this

particular financing for the purpose of particular sector. Such as motor vehicle, aircraft

3

take consider interest of stakeholder.

Instrumental stakeholder model: under this, managing stakeholder in efficient manner

to attain business objectives in the form of profit, growth and future sustainability. It also

allows to test link among business goals and stakeholder interest. It attempts to provide

solution to plenty of critical questions those are related with stakeholder value.

Corporations are not commonly manage in the stake of there stakeholders alone, but that

there are wide range of stakeholders. It determine various models the groups those are related

with stakeholder of a corporation and they require certain techniques to satisfy needs and

demand. In order to make crucial decision regarding proper reporting of financial statement so

that better decisions can be made on that basis.

b): Types of medium and long-term finance

Medium term financing are arrange as systematic structure for repayment for the

maximum period of five year. While, the repayment of long term can varies from 5 to 15 years.

Banks and other institution those are offering such kind of finance plan or service in support of

large projects. At the time of offering such kind of facilities they assume risk of non-payment

those are arises from the failure of the buyer or from political instability. Some of the most

common financing are:

Buyer credits: These are used to finance an export over the period of medium or long

time. By the help of this method, finances are lent instantly to the international buyers.

These are outspread on a non-recurring basis to the exporter as they enters into a direct

contract with the lending banks.

Supplier credit: In this particular case, banks can purchase from the outside parties a

international buyers for goods and services (Esty, 2014). Arranging such kind of finance

can be more easier and affordable than arranging a buyer credit. Under this situation, not

any parties has to directly deal or negotiate with foreign clients.

Counter trade: It is an arrangement in which a sale to an importer is conditional on a

correlative purchasing done by the merchandise. Such kind of finance is related with

counter purchase and offset arrangements.

Export leasing: It is mostly associated with private companies that are specialise in this

particular financing for the purpose of particular sector. Such as motor vehicle, aircraft

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and other equipments. For this purpose banks can deliver export leasing facilities through

subsidiaries units.

Equity financing: It means that dealing a part of ownership of business for the purpose

of increasing goodwill of the company. It involves a constant investment in a company

which is not repaid by an organisation at a later date.

Venture capital: It is associated with that financing that comes from individuals in

business of investing in privately held company's. They use to invest in companies that

have equity investments from the owner.

Comparison

Newly establish Private Company Public Limited company

It is has been seen that for newly establish

company they need to raise funds from own

resources.

In case of public company which is already

operating in the market have plenty of sources

where they can collect finance.

Personal saving and bank loans are the best

option for these types of the company.

Equity financing and IPO are the right option

for the company to raise capital.

The risk associated with the company is more

as they don't have any supporting parties to

deal with.

The entire operation are manage and control

through government rules and legal aspects.

QUESTION: 2

a): WACC of Redrock plc

It is the calculation of a firm's cost of capital under which every category of assets is

proportionally weighted. Every sources of capital consists of common stock, bonds and other

long term debt.

WACC = ((E/V) * Re) + [(D/V) * Rd)*(1-T)]

E: Market value of equity

D: Market value of debt

v: Total market value of the company

Re = Cost of Equity

Rd = Cost of Debt

4

subsidiaries units.

Equity financing: It means that dealing a part of ownership of business for the purpose

of increasing goodwill of the company. It involves a constant investment in a company

which is not repaid by an organisation at a later date.

Venture capital: It is associated with that financing that comes from individuals in

business of investing in privately held company's. They use to invest in companies that

have equity investments from the owner.

Comparison

Newly establish Private Company Public Limited company

It is has been seen that for newly establish

company they need to raise funds from own

resources.

In case of public company which is already

operating in the market have plenty of sources

where they can collect finance.

Personal saving and bank loans are the best

option for these types of the company.

Equity financing and IPO are the right option

for the company to raise capital.

The risk associated with the company is more

as they don't have any supporting parties to

deal with.

The entire operation are manage and control

through government rules and legal aspects.

QUESTION: 2

a): WACC of Redrock plc

It is the calculation of a firm's cost of capital under which every category of assets is

proportionally weighted. Every sources of capital consists of common stock, bonds and other

long term debt.

WACC = ((E/V) * Re) + [(D/V) * Rd)*(1-T)]

E: Market value of equity

D: Market value of debt

v: Total market value of the company

Re = Cost of Equity

Rd = Cost of Debt

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

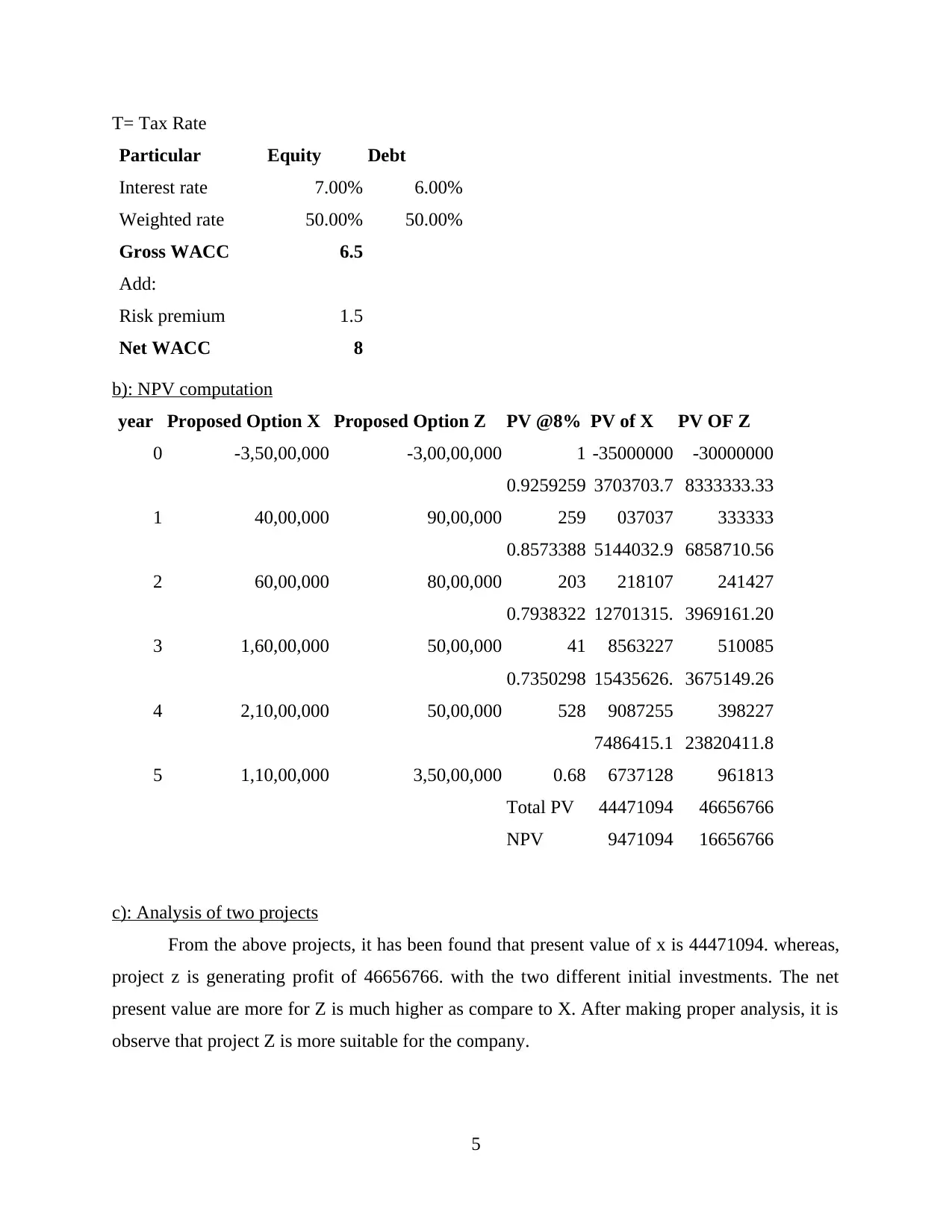

T= Tax Rate

Particular Equity Debt

Interest rate 7.00% 6.00%

Weighted rate 50.00% 50.00%

Gross WACC 6.5

Add:

Risk premium 1.5

Net WACC 8

b): NPV computation

year Proposed Option X Proposed Option Z PV @8% PV of X PV OF Z

0 -3,50,00,000 -3,00,00,000 1 -35000000 -30000000

1 40,00,000 90,00,000

0.9259259

259

3703703.7

037037

8333333.33

333333

2 60,00,000 80,00,000

0.8573388

203

5144032.9

218107

6858710.56

241427

3 1,60,00,000 50,00,000

0.7938322

41

12701315.

8563227

3969161.20

510085

4 2,10,00,000 50,00,000

0.7350298

528

15435626.

9087255

3675149.26

398227

5 1,10,00,000 3,50,00,000 0.68

7486415.1

6737128

23820411.8

961813

Total PV 44471094 46656766

NPV 9471094 16656766

c): Analysis of two projects

From the above projects, it has been found that present value of x is 44471094. whereas,

project z is generating profit of 46656766. with the two different initial investments. The net

present value are more for Z is much higher as compare to X. After making proper analysis, it is

observe that project Z is more suitable for the company.

5

Particular Equity Debt

Interest rate 7.00% 6.00%

Weighted rate 50.00% 50.00%

Gross WACC 6.5

Add:

Risk premium 1.5

Net WACC 8

b): NPV computation

year Proposed Option X Proposed Option Z PV @8% PV of X PV OF Z

0 -3,50,00,000 -3,00,00,000 1 -35000000 -30000000

1 40,00,000 90,00,000

0.9259259

259

3703703.7

037037

8333333.33

333333

2 60,00,000 80,00,000

0.8573388

203

5144032.9

218107

6858710.56

241427

3 1,60,00,000 50,00,000

0.7938322

41

12701315.

8563227

3969161.20

510085

4 2,10,00,000 50,00,000

0.7350298

528

15435626.

9087255

3675149.26

398227

5 1,10,00,000 3,50,00,000 0.68

7486415.1

6737128

23820411.8

961813

Total PV 44471094 46656766

NPV 9471094 16656766

c): Analysis of two projects

From the above projects, it has been found that present value of x is 44471094. whereas,

project z is generating profit of 46656766. with the two different initial investments. The net

present value are more for Z is much higher as compare to X. After making proper analysis, it is

observe that project Z is more suitable for the company.

5

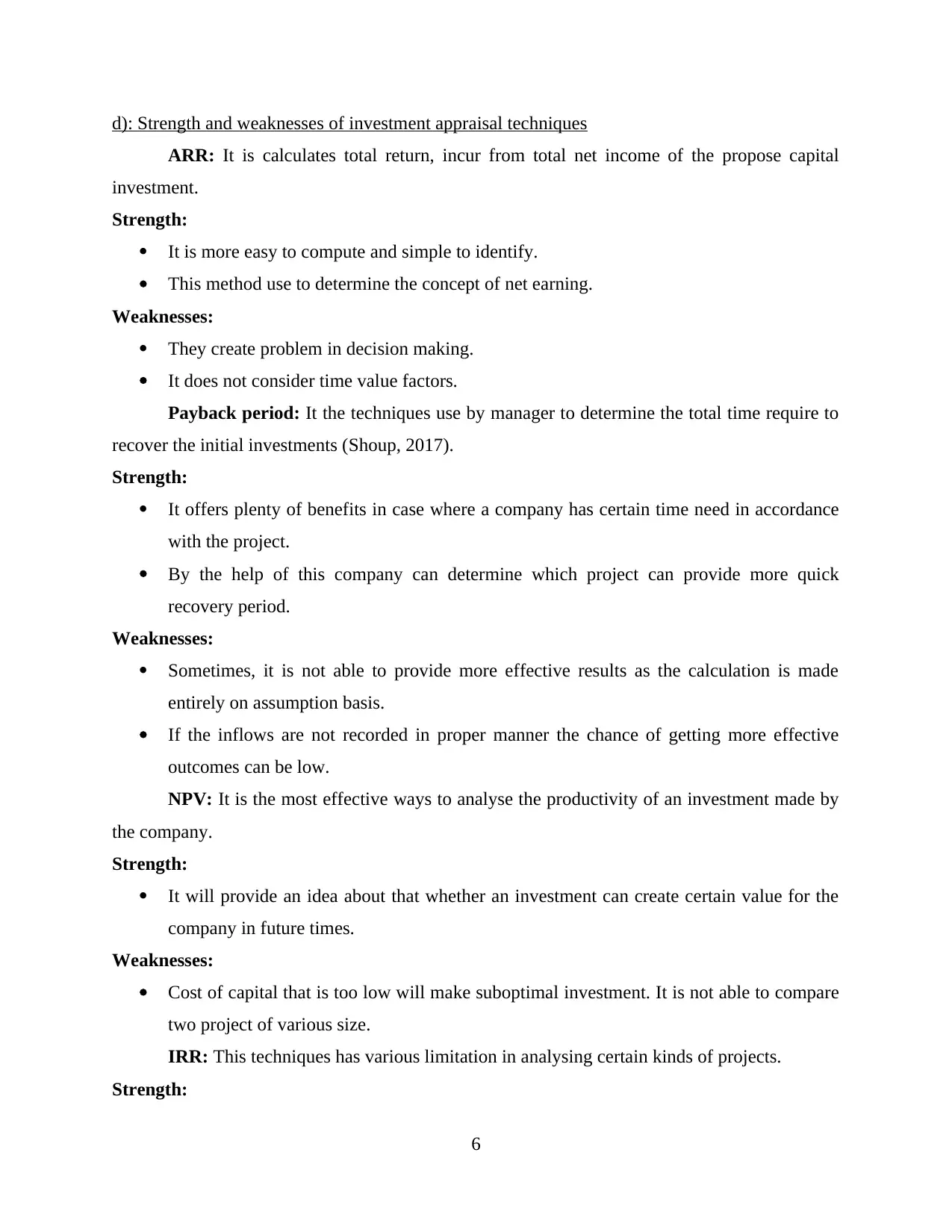

d): Strength and weaknesses of investment appraisal techniques

ARR: It is calculates total return, incur from total net income of the propose capital

investment.

Strength:

It is more easy to compute and simple to identify.

This method use to determine the concept of net earning.

Weaknesses:

They create problem in decision making.

It does not consider time value factors.

Payback period: It the techniques use by manager to determine the total time require to

recover the initial investments (Shoup, 2017).

Strength:

It offers plenty of benefits in case where a company has certain time need in accordance

with the project.

By the help of this company can determine which project can provide more quick

recovery period.

Weaknesses:

Sometimes, it is not able to provide more effective results as the calculation is made

entirely on assumption basis.

If the inflows are not recorded in proper manner the chance of getting more effective

outcomes can be low.

NPV: It is the most effective ways to analyse the productivity of an investment made by

the company.

Strength:

It will provide an idea about that whether an investment can create certain value for the

company in future times.

Weaknesses:

Cost of capital that is too low will make suboptimal investment. It is not able to compare

two project of various size.

IRR: This techniques has various limitation in analysing certain kinds of projects.

Strength:

6

ARR: It is calculates total return, incur from total net income of the propose capital

investment.

Strength:

It is more easy to compute and simple to identify.

This method use to determine the concept of net earning.

Weaknesses:

They create problem in decision making.

It does not consider time value factors.

Payback period: It the techniques use by manager to determine the total time require to

recover the initial investments (Shoup, 2017).

Strength:

It offers plenty of benefits in case where a company has certain time need in accordance

with the project.

By the help of this company can determine which project can provide more quick

recovery period.

Weaknesses:

Sometimes, it is not able to provide more effective results as the calculation is made

entirely on assumption basis.

If the inflows are not recorded in proper manner the chance of getting more effective

outcomes can be low.

NPV: It is the most effective ways to analyse the productivity of an investment made by

the company.

Strength:

It will provide an idea about that whether an investment can create certain value for the

company in future times.

Weaknesses:

Cost of capital that is too low will make suboptimal investment. It is not able to compare

two project of various size.

IRR: This techniques has various limitation in analysing certain kinds of projects.

Strength:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is more attractive method which is use to interpret after making computation of IRR.

It estimate rough idea about the manager in order to take necessary decision.

Weaknesses:

Economies of scale is ignored in order to get better results.

It is entirely depend upon dependent or contingent project.

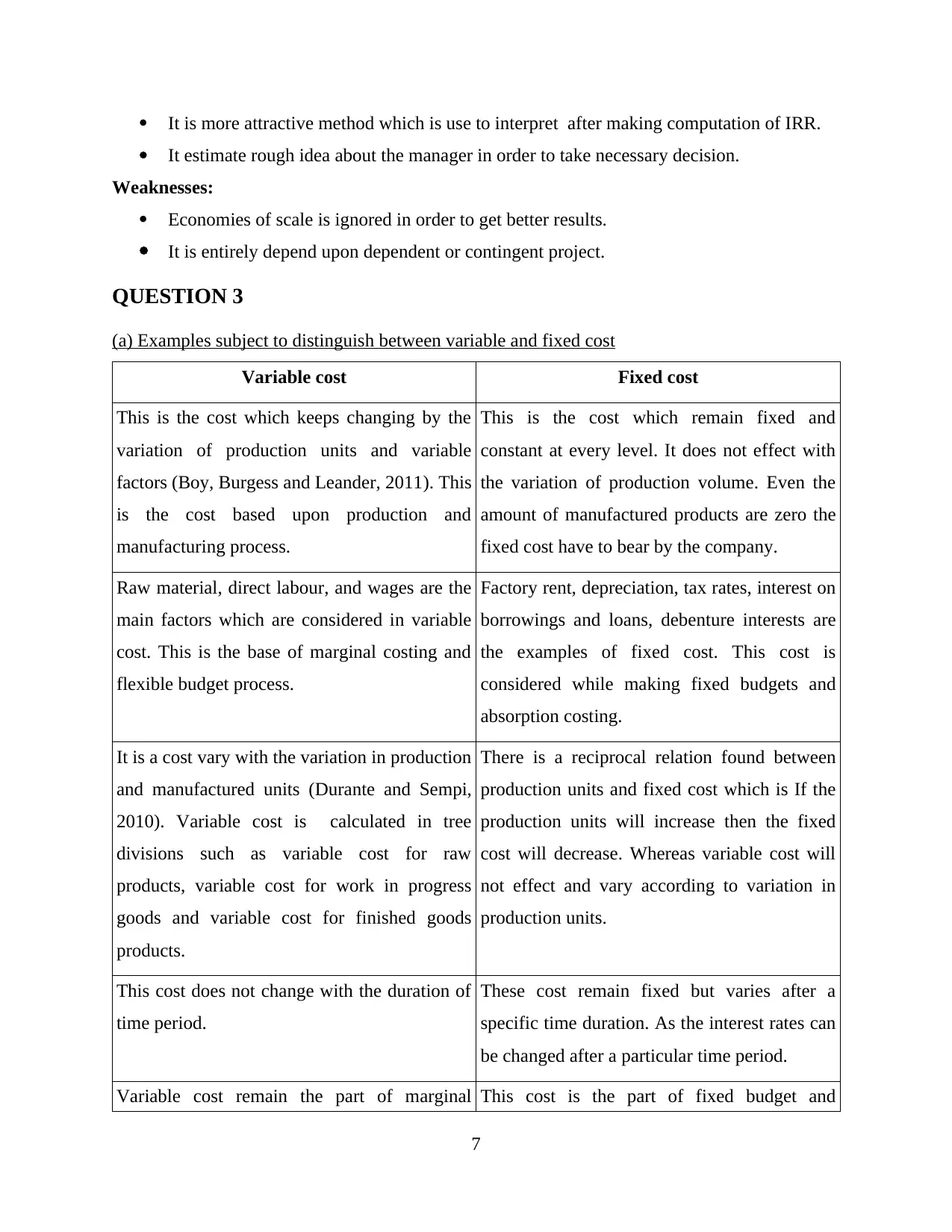

QUESTION 3

(a) Examples subject to distinguish between variable and fixed cost

Variable cost Fixed cost

This is the cost which keeps changing by the

variation of production units and variable

factors (Boy, Burgess and Leander, 2011). This

is the cost based upon production and

manufacturing process.

This is the cost which remain fixed and

constant at every level. It does not effect with

the variation of production volume. Even the

amount of manufactured products are zero the

fixed cost have to bear by the company.

Raw material, direct labour, and wages are the

main factors which are considered in variable

cost. This is the base of marginal costing and

flexible budget process.

Factory rent, depreciation, tax rates, interest on

borrowings and loans, debenture interests are

the examples of fixed cost. This cost is

considered while making fixed budgets and

absorption costing.

It is a cost vary with the variation in production

and manufactured units (Durante and Sempi,

2010). Variable cost is calculated in tree

divisions such as variable cost for raw

products, variable cost for work in progress

goods and variable cost for finished goods

products.

There is a reciprocal relation found between

production units and fixed cost which is If the

production units will increase then the fixed

cost will decrease. Whereas variable cost will

not effect and vary according to variation in

production units.

This cost does not change with the duration of

time period.

These cost remain fixed but varies after a

specific time duration. As the interest rates can

be changed after a particular time period.

Variable cost remain the part of marginal This cost is the part of fixed budget and

7

It estimate rough idea about the manager in order to take necessary decision.

Weaknesses:

Economies of scale is ignored in order to get better results.

It is entirely depend upon dependent or contingent project.

QUESTION 3

(a) Examples subject to distinguish between variable and fixed cost

Variable cost Fixed cost

This is the cost which keeps changing by the

variation of production units and variable

factors (Boy, Burgess and Leander, 2011). This

is the cost based upon production and

manufacturing process.

This is the cost which remain fixed and

constant at every level. It does not effect with

the variation of production volume. Even the

amount of manufactured products are zero the

fixed cost have to bear by the company.

Raw material, direct labour, and wages are the

main factors which are considered in variable

cost. This is the base of marginal costing and

flexible budget process.

Factory rent, depreciation, tax rates, interest on

borrowings and loans, debenture interests are

the examples of fixed cost. This cost is

considered while making fixed budgets and

absorption costing.

It is a cost vary with the variation in production

and manufactured units (Durante and Sempi,

2010). Variable cost is calculated in tree

divisions such as variable cost for raw

products, variable cost for work in progress

goods and variable cost for finished goods

products.

There is a reciprocal relation found between

production units and fixed cost which is If the

production units will increase then the fixed

cost will decrease. Whereas variable cost will

not effect and vary according to variation in

production units.

This cost does not change with the duration of

time period.

These cost remain fixed but varies after a

specific time duration. As the interest rates can

be changed after a particular time period.

Variable cost remain the part of marginal This cost is the part of fixed budget and

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

costing while evaluating the cost per unit and

calculating contribution per unit (Ghosh,

2010).

analysation of desired profit.

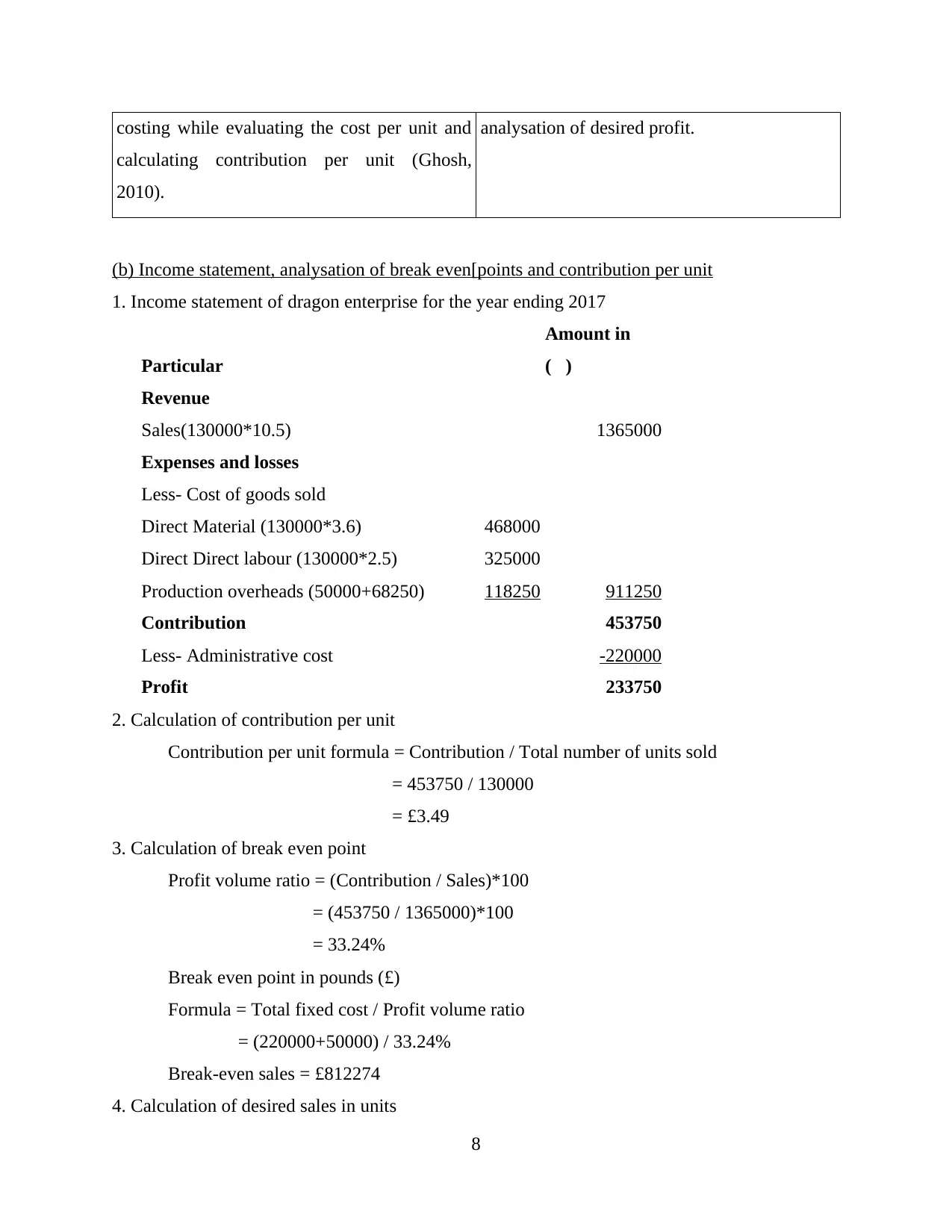

(b) Income statement, analysation of break even[points and contribution per unit

1. Income statement of dragon enterprise for the year ending 2017

Particular

Amount in

(£)

Revenue

Sales(130000*10.5) 1365000

Expenses and losses

Less- Cost of goods sold

Direct Material (130000*3.6) 468000

Direct Direct labour (130000*2.5) 325000

Production overheads (50000+68250) 118250 911250

Contribution 453750

Less- Administrative cost -220000

Profit 233750

2. Calculation of contribution per unit

Contribution per unit formula = Contribution / Total number of units sold

= 453750 / 130000

= £3.49

3. Calculation of break even point

Profit volume ratio = (Contribution / Sales)*100

= (453750 / 1365000)*100

= 33.24%

Break even point in pounds (£)

Formula = Total fixed cost / Profit volume ratio

= (220000+50000) / 33.24%

Break-even sales = £812274

4. Calculation of desired sales in units

8

calculating contribution per unit (Ghosh,

2010).

analysation of desired profit.

(b) Income statement, analysation of break even[points and contribution per unit

1. Income statement of dragon enterprise for the year ending 2017

Particular

Amount in

(£)

Revenue

Sales(130000*10.5) 1365000

Expenses and losses

Less- Cost of goods sold

Direct Material (130000*3.6) 468000

Direct Direct labour (130000*2.5) 325000

Production overheads (50000+68250) 118250 911250

Contribution 453750

Less- Administrative cost -220000

Profit 233750

2. Calculation of contribution per unit

Contribution per unit formula = Contribution / Total number of units sold

= 453750 / 130000

= £3.49

3. Calculation of break even point

Profit volume ratio = (Contribution / Sales)*100

= (453750 / 1365000)*100

= 33.24%

Break even point in pounds (£)

Formula = Total fixed cost / Profit volume ratio

= (220000+50000) / 33.24%

Break-even sales = £812274

4. Calculation of desired sales in units

8

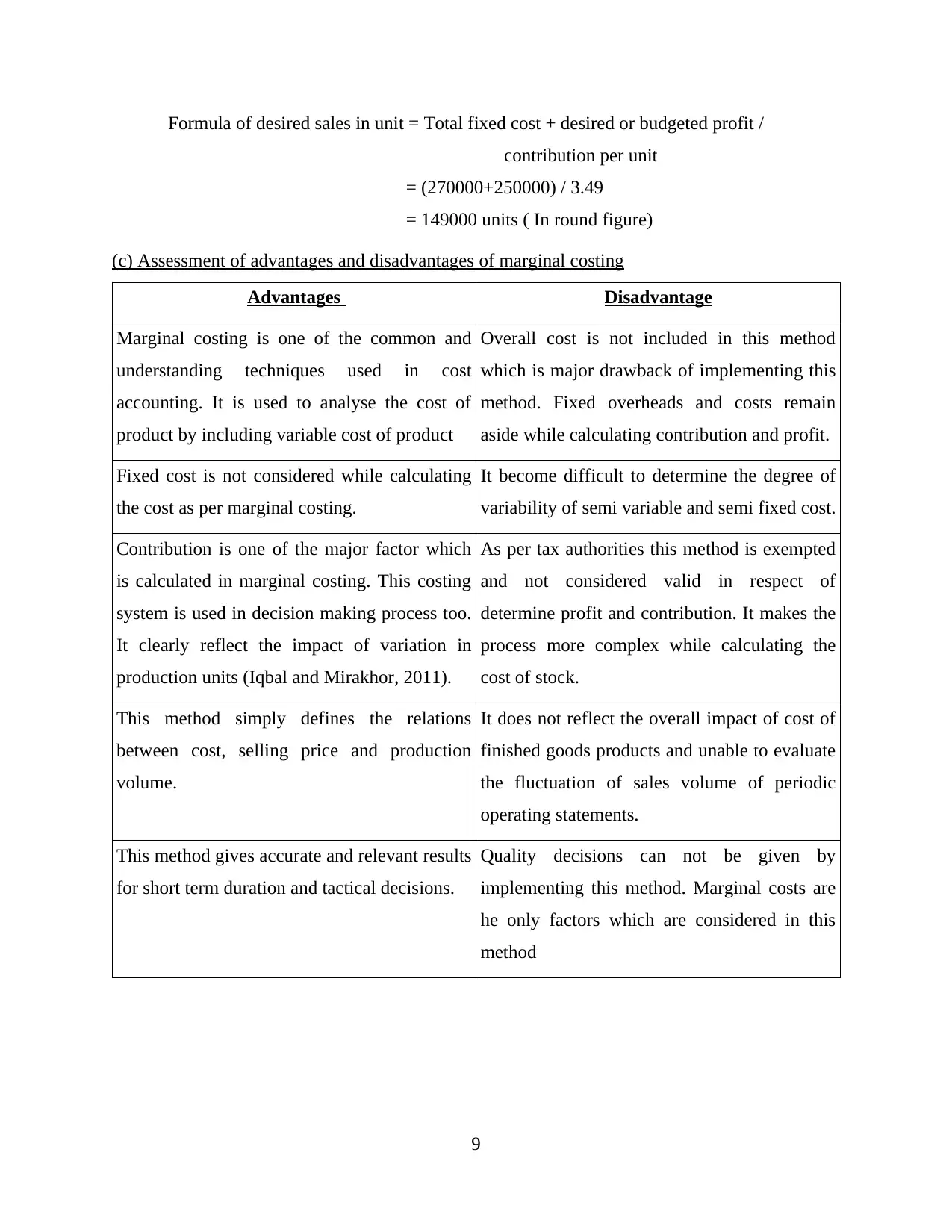

Formula of desired sales in unit = Total fixed cost + desired or budgeted profit /

contribution per unit

= (270000+250000) / 3.49

= 149000 units ( In round figure)

(c) Assessment of advantages and disadvantages of marginal costing

Advantages Disadvantage

Marginal costing is one of the common and

understanding techniques used in cost

accounting. It is used to analyse the cost of

product by including variable cost of product

Overall cost is not included in this method

which is major drawback of implementing this

method. Fixed overheads and costs remain

aside while calculating contribution and profit.

Fixed cost is not considered while calculating

the cost as per marginal costing.

It become difficult to determine the degree of

variability of semi variable and semi fixed cost.

Contribution is one of the major factor which

is calculated in marginal costing. This costing

system is used in decision making process too.

It clearly reflect the impact of variation in

production units (Iqbal and Mirakhor, 2011).

As per tax authorities this method is exempted

and not considered valid in respect of

determine profit and contribution. It makes the

process more complex while calculating the

cost of stock.

This method simply defines the relations

between cost, selling price and production

volume.

It does not reflect the overall impact of cost of

finished goods products and unable to evaluate

the fluctuation of sales volume of periodic

operating statements.

This method gives accurate and relevant results

for short term duration and tactical decisions.

Quality decisions can not be given by

implementing this method. Marginal costs are

he only factors which are considered in this

method

9

contribution per unit

= (270000+250000) / 3.49

= 149000 units ( In round figure)

(c) Assessment of advantages and disadvantages of marginal costing

Advantages Disadvantage

Marginal costing is one of the common and

understanding techniques used in cost

accounting. It is used to analyse the cost of

product by including variable cost of product

Overall cost is not included in this method

which is major drawback of implementing this

method. Fixed overheads and costs remain

aside while calculating contribution and profit.

Fixed cost is not considered while calculating

the cost as per marginal costing.

It become difficult to determine the degree of

variability of semi variable and semi fixed cost.

Contribution is one of the major factor which

is calculated in marginal costing. This costing

system is used in decision making process too.

It clearly reflect the impact of variation in

production units (Iqbal and Mirakhor, 2011).

As per tax authorities this method is exempted

and not considered valid in respect of

determine profit and contribution. It makes the

process more complex while calculating the

cost of stock.

This method simply defines the relations

between cost, selling price and production

volume.

It does not reflect the overall impact of cost of

finished goods products and unable to evaluate

the fluctuation of sales volume of periodic

operating statements.

This method gives accurate and relevant results

for short term duration and tactical decisions.

Quality decisions can not be given by

implementing this method. Marginal costs are

he only factors which are considered in this

method

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.