ACC00716 Finance Assessment 2: Business Case Studies - Session 1, 2020

VerifiedAdded on 2022/09/14

|10

|1869

|15

Homework Assignment

AI Summary

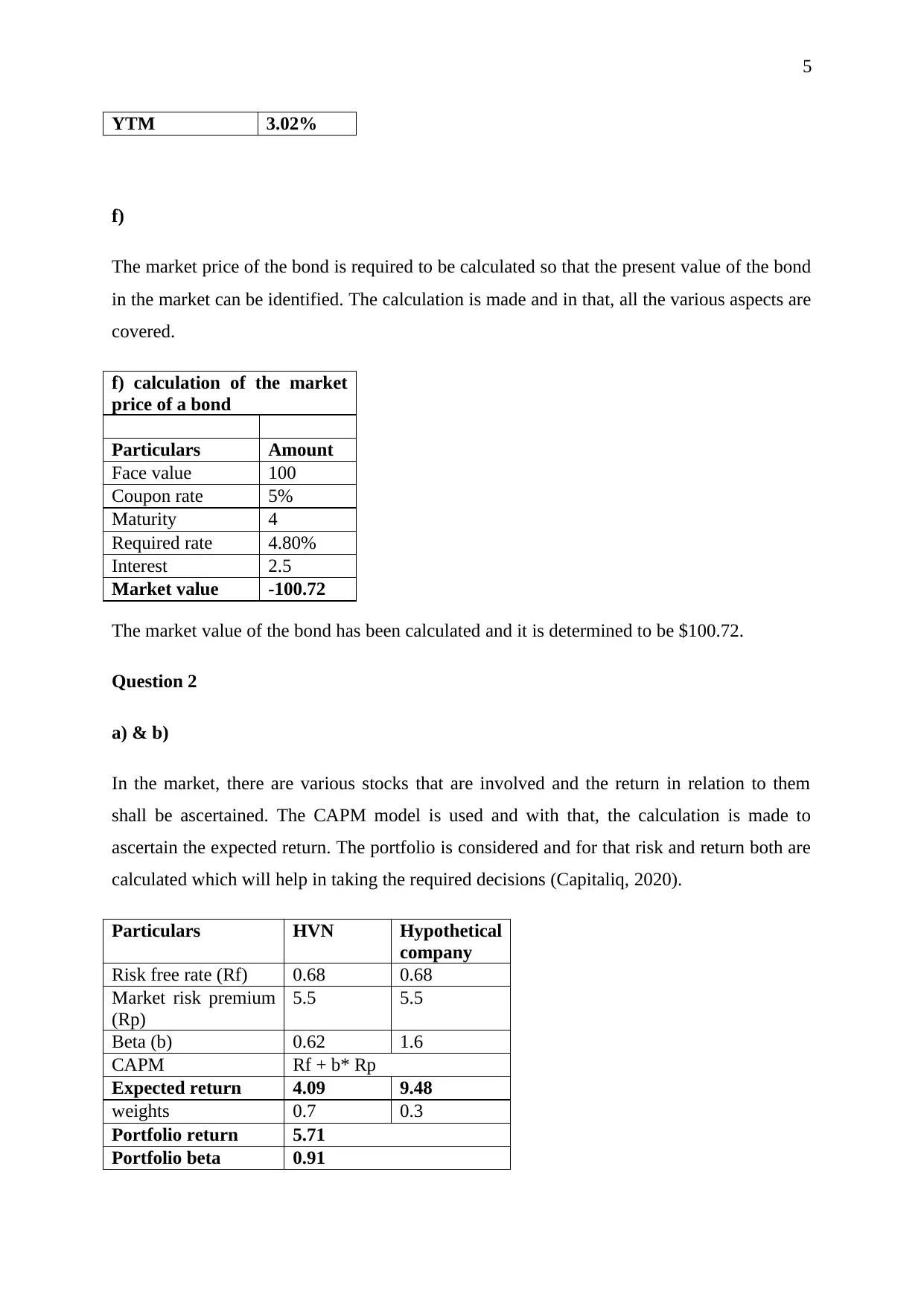

This finance assignment, completed for ACC00716, comprises a comprehensive analysis of financial concepts. The assignment is divided into three main parts: time value of money and bond valuation, and risk and return analysis. The first section involves calculations related to borrowing, annual revenue, effective annual rate, loan installments, bond yield to maturity (YTM), and market price of a bond. The second part utilizes the Capital Asset Pricing Model (CAPM) to assess the expected returns of stocks and calculate portfolio returns and beta. The third section delves into the management of stocks, considering both return and risk factors, including systematic and unsystematic risk, portfolio diversification, and the implications of beta values. The analysis includes the application of financial models to determine the expected return on stocks. The student provides calculations and interpretations based on data sourced from S&P Capital IQ, offering insights into financial decision-making and portfolio management. The assignment emphasizes the significance of risk and return in investment strategies.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.