Finance Assessment: Accounting Principles, Budgeting, and Analysis

VerifiedAdded on 2023/01/13

|14

|2403

|38

Report

AI Summary

This comprehensive finance assessment report covers a wide range of topics within the field of finance. It begins by explaining core accounting principles such as revenue, expense, matching, cost, and objectivity. The report then explores current legislations related to sales, purchase/expense, and income tax records, as well as payments to employees and GST. The assessment further delves into audit trails, cost classifications (direct, indirect, fixed, variable, and semi-variable), and budget analysis, including sales and fees budgets. A P&L statement and balance sheet are analyzed, along with GST calculations and cash flow statements. The report concludes with an analysis of accounts receivable, cash flow plans, and organizational protocols for managing financial losses and ensuring effective financial management within a team, emphasizing the importance of budgeting and variance analysis.

ASSESEMENT

(Finance)

1

(Finance)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MAIN BODY...................................................................................................................................3

Task 1. ........................................................................................................................................3

Task 2..........................................................................................................................................3

Task 3..........................................................................................................................................4

Task 4..........................................................................................................................................4

Task 5..........................................................................................................................................5

Task 6..........................................................................................................................................5

Task 7..........................................................................................................................................6

Task 8..........................................................................................................................................6

Task 9..........................................................................................................................................6

Task 10........................................................................................................................................8

Task 11........................................................................................................................................9

Task 12........................................................................................................................................9

Task 13......................................................................................................................................10

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

2

MAIN BODY...................................................................................................................................3

Task 1. ........................................................................................................................................3

Task 2..........................................................................................................................................3

Task 3..........................................................................................................................................4

Task 4..........................................................................................................................................4

Task 5..........................................................................................................................................5

Task 6..........................................................................................................................................5

Task 7..........................................................................................................................................6

Task 8..........................................................................................................................................6

Task 9..........................................................................................................................................6

Task 10........................................................................................................................................8

Task 11........................................................................................................................................9

Task 12........................................................................................................................................9

Task 13......................................................................................................................................10

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

2

MAIN BODY

Task 1.

Revenue principle- This is an accounting principle in which income is recorded when it is

earned and regardless of when cash is received by business (Zeff, 2016). For example, if

a company sells goods to a customers and receive payment through credit card in

January. Due to some issues company does not receive cash till February. In this case that

credit card purchase is considered as cash because of this principle.

Expense principle- It is an accounting principle that states that expenditures must be

identified in similar time frame as revenues to which they link. For example, income tax

is paid in current month by companies whether expenses are higher or low.

Matching principle- The term matching principle can be defined as a type of principle

which states that revenues and expenses must be recognised together in similar time

period (Needles, Powers and Crosson, 2013). For example, a company buys a machine of

$50000 pounds with 5 years’ life and as per this principle machine cost must be matched

with revenues it creates.

Cost principle- This accounting principle is an element of generally accepted accounting

principle (GAAP). As per this principle, the assets must be recorded on their cost in the

case if asset is new. For instance, when a retailer buys stock from vendor it records the

purchase on cash price which was actually paid.

Objectivity principle- This principle is based on a concept that financial statements of

companies should be based on a solid evidence (Rutherford, 2016). For example, if

companies want to take loan from any bank then they will show prepared financial

statement as these are based on particular evidence.

Task 2.

The current legislations related to below mentioned items as per the official website of

Australian Tax office.

Sales records- An electronic sales suppression tool is used in order to enable tax

avoidance by managing business transaction record and under reported revenues. As well

as for wholesales sale 29% rate of WET is applicable.

3

Task 1.

Revenue principle- This is an accounting principle in which income is recorded when it is

earned and regardless of when cash is received by business (Zeff, 2016). For example, if

a company sells goods to a customers and receive payment through credit card in

January. Due to some issues company does not receive cash till February. In this case that

credit card purchase is considered as cash because of this principle.

Expense principle- It is an accounting principle that states that expenditures must be

identified in similar time frame as revenues to which they link. For example, income tax

is paid in current month by companies whether expenses are higher or low.

Matching principle- The term matching principle can be defined as a type of principle

which states that revenues and expenses must be recognised together in similar time

period (Needles, Powers and Crosson, 2013). For example, a company buys a machine of

$50000 pounds with 5 years’ life and as per this principle machine cost must be matched

with revenues it creates.

Cost principle- This accounting principle is an element of generally accepted accounting

principle (GAAP). As per this principle, the assets must be recorded on their cost in the

case if asset is new. For instance, when a retailer buys stock from vendor it records the

purchase on cash price which was actually paid.

Objectivity principle- This principle is based on a concept that financial statements of

companies should be based on a solid evidence (Rutherford, 2016). For example, if

companies want to take loan from any bank then they will show prepared financial

statement as these are based on particular evidence.

Task 2.

The current legislations related to below mentioned items as per the official website of

Australian Tax office.

Sales records- An electronic sales suppression tool is used in order to enable tax

avoidance by managing business transaction record and under reported revenues. As well

as for wholesales sale 29% rate of WET is applicable.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchase/expense records- Australian GST generally implies to sales of imported

products and services to consumers of Australia. The goods and service tax does not

implement on business purchases of imported services and digital items if company is

registered for GST in Australia.

Year ended income tax records- The Australian tax office information for businesses

about the records companies need to explain all transactions regarding to information.

Payments made to employees- If companies need to withhold amount from payment to

employees, consisting those who are overseas or foreign residents then they need to

complete a tax file number declaration (About records relevant to current legislations,

2019). On the other hand, in some situations company may need to complete withholding

declaration. These declarations may help them to work out how much amount of tax to

withholding by finding whether there are other factors which are needed to consider.

PAYG withholding records relating to business payments- This is an obligation or

responsibility of an employer to gather PAYG withholding amount from payment made

to workers and entities so that they can meet their end year tax liabilities.

Goods service tax (GST) – Australian goods and service tax can be apply to company for

retail sale of lower valued goods, services and digital commodities to Australia.

Task 3.

How often companies need to perform an audit trail?

The audit trail offers a vital component for detecting fraud. Rigid adherence to the

development of an audit trail provides evidence of the validity of trades. All commercial

payments must include a promoting report such as purchase orders and authorised receipts.

Basically, companies need the audit trail during different quarter of a financial year which may

be of two times.

Task 4.

Example of following costs:

Direct cost- The examples of this cost are direct labour, material, commissions,

production supply etc.

Indirect cost- Some example of indirect cost is rent, telephone charges, security expenses,

office expense etc.

4

products and services to consumers of Australia. The goods and service tax does not

implement on business purchases of imported services and digital items if company is

registered for GST in Australia.

Year ended income tax records- The Australian tax office information for businesses

about the records companies need to explain all transactions regarding to information.

Payments made to employees- If companies need to withhold amount from payment to

employees, consisting those who are overseas or foreign residents then they need to

complete a tax file number declaration (About records relevant to current legislations,

2019). On the other hand, in some situations company may need to complete withholding

declaration. These declarations may help them to work out how much amount of tax to

withholding by finding whether there are other factors which are needed to consider.

PAYG withholding records relating to business payments- This is an obligation or

responsibility of an employer to gather PAYG withholding amount from payment made

to workers and entities so that they can meet their end year tax liabilities.

Goods service tax (GST) – Australian goods and service tax can be apply to company for

retail sale of lower valued goods, services and digital commodities to Australia.

Task 3.

How often companies need to perform an audit trail?

The audit trail offers a vital component for detecting fraud. Rigid adherence to the

development of an audit trail provides evidence of the validity of trades. All commercial

payments must include a promoting report such as purchase orders and authorised receipts.

Basically, companies need the audit trail during different quarter of a financial year which may

be of two times.

Task 4.

Example of following costs:

Direct cost- The examples of this cost are direct labour, material, commissions,

production supply etc.

Indirect cost- Some example of indirect cost is rent, telephone charges, security expenses,

office expense etc.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed cost- The example of fixed cost is rent, payment of loan, premium of insurance and

many more.

Variable cost- The examples of this cost are commission on sale, raw material cost of

manufacturing, direct labour expenses etc.

Semi-variable cost- It includes repairing cost, fuel & power expenses, monthly base

telephone charges, indirect labour cost etc.

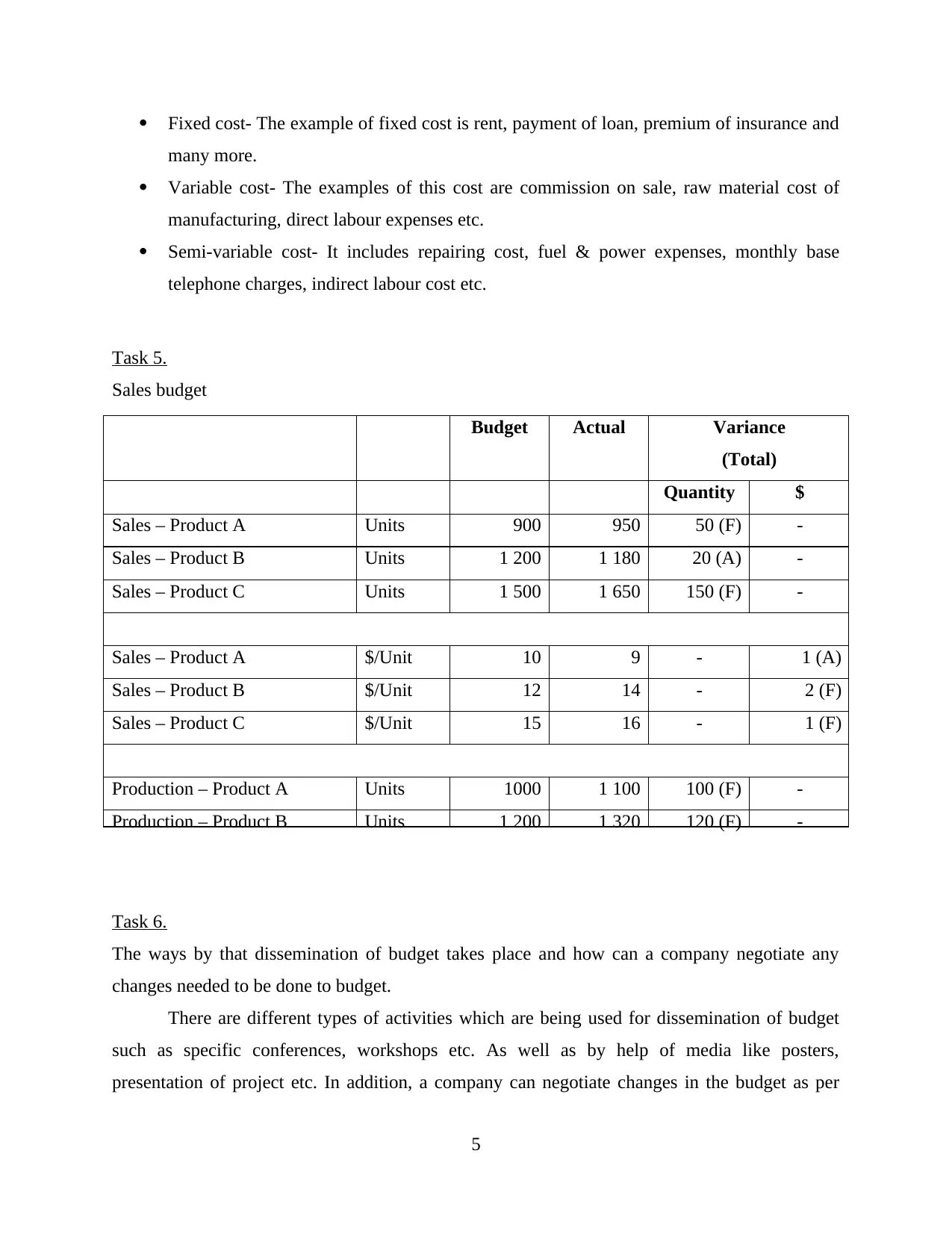

Task 5.

Sales budget

Task 6.

The ways by that dissemination of budget takes place and how can a company negotiate any

changes needed to be done to budget.

There are different types of activities which are being used for dissemination of budget

such as specific conferences, workshops etc. As well as by help of media like posters,

presentation of project etc. In addition, a company can negotiate changes in the budget as per

5

Budget Actual Variance

(Total)

Quantity $

Sales – Product A Units 900 950 50 (F) -

Sales – Product B Units 1 200 1 180 20 (A) -

Sales – Product C Units 1 500 1 650 150 (F) -

Sales – Product A $/Unit 10 9 - 1 (A)

Sales – Product B $/Unit 12 14 - 2 (F)

Sales – Product C $/Unit 15 16 - 1 (F)

Production – Product A Units 1000 1 100 100 (F) -

Production – Product B Units 1 200 1 320 120 (F) -

many more.

Variable cost- The examples of this cost are commission on sale, raw material cost of

manufacturing, direct labour expenses etc.

Semi-variable cost- It includes repairing cost, fuel & power expenses, monthly base

telephone charges, indirect labour cost etc.

Task 5.

Sales budget

Task 6.

The ways by that dissemination of budget takes place and how can a company negotiate any

changes needed to be done to budget.

There are different types of activities which are being used for dissemination of budget

such as specific conferences, workshops etc. As well as by help of media like posters,

presentation of project etc. In addition, a company can negotiate changes in the budget as per

5

Budget Actual Variance

(Total)

Quantity $

Sales – Product A Units 900 950 50 (F) -

Sales – Product B Units 1 200 1 180 20 (A) -

Sales – Product C Units 1 500 1 650 150 (F) -

Sales – Product A $/Unit 10 9 - 1 (A)

Sales – Product B $/Unit 12 14 - 2 (F)

Sales – Product C $/Unit 15 16 - 1 (F)

Production – Product A Units 1000 1 100 100 (F) -

Production – Product B Units 1 200 1 320 120 (F) -

their need. Like if company makes projection of sales revenue of $1500 but in actual they earn

revenue of $1200. In this case, company can make correction in their budget.

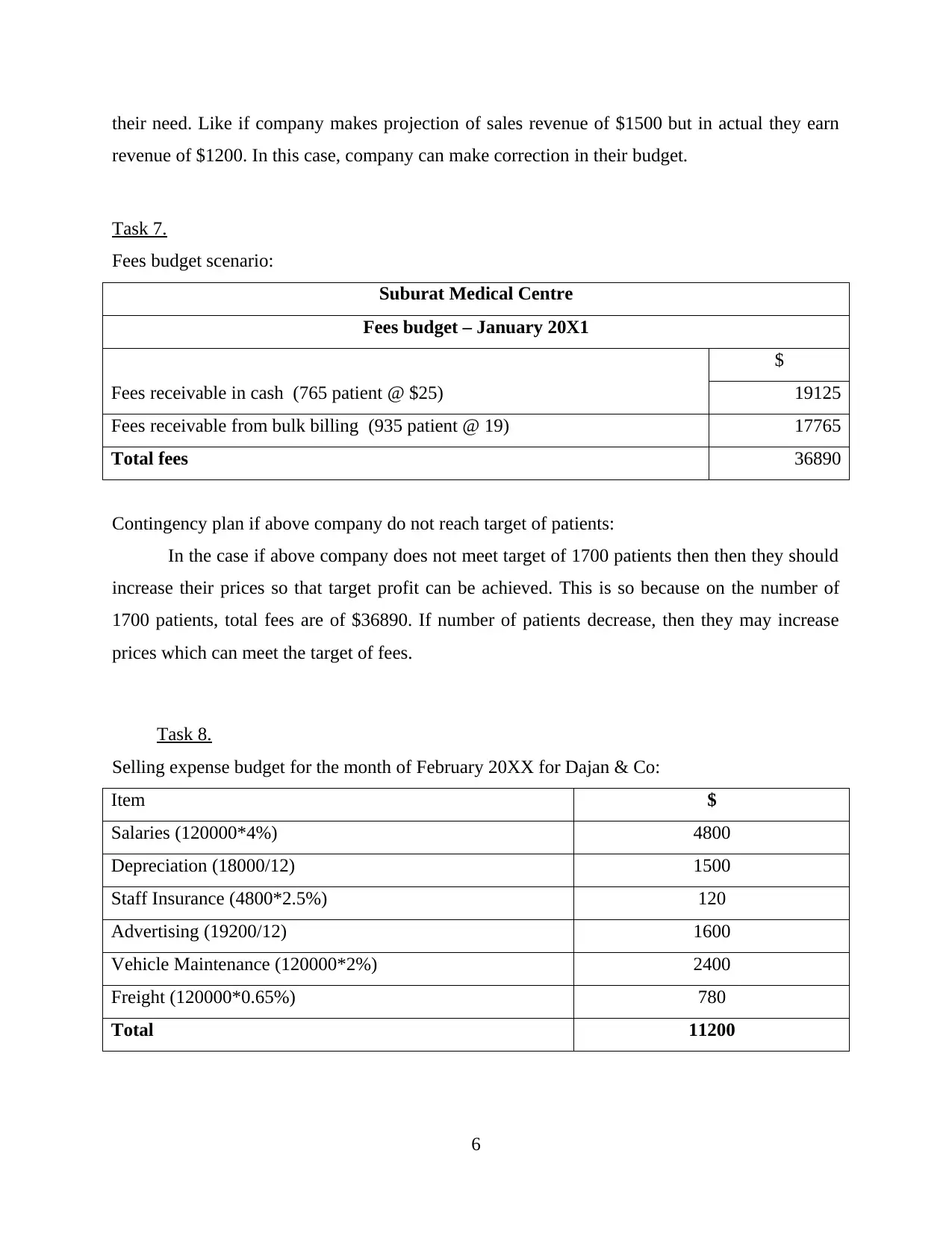

Task 7.

Fees budget scenario:

Suburat Medical Centre

Fees budget – January 20X1

$

Fees receivable in cash (765 patient @ $25) 19125

Fees receivable from bulk billing (935 patient @ 19) 17765

Total fees 36890

Contingency plan if above company do not reach target of patients:

In the case if above company does not meet target of 1700 patients then then they should

increase their prices so that target profit can be achieved. This is so because on the number of

1700 patients, total fees are of $36890. If number of patients decrease, then they may increase

prices which can meet the target of fees.

Task 8.

Selling expense budget for the month of February 20XX for Dajan & Co:

Item $

Salaries (120000*4%) 4800

Depreciation (18000/12) 1500

Staff Insurance (4800*2.5%) 120

Advertising (19200/12) 1600

Vehicle Maintenance (120000*2%) 2400

Freight (120000*0.65%) 780

Total 11200

6

revenue of $1200. In this case, company can make correction in their budget.

Task 7.

Fees budget scenario:

Suburat Medical Centre

Fees budget – January 20X1

$

Fees receivable in cash (765 patient @ $25) 19125

Fees receivable from bulk billing (935 patient @ 19) 17765

Total fees 36890

Contingency plan if above company do not reach target of patients:

In the case if above company does not meet target of 1700 patients then then they should

increase their prices so that target profit can be achieved. This is so because on the number of

1700 patients, total fees are of $36890. If number of patients decrease, then they may increase

prices which can meet the target of fees.

Task 8.

Selling expense budget for the month of February 20XX for Dajan & Co:

Item $

Salaries (120000*4%) 4800

Depreciation (18000/12) 1500

Staff Insurance (4800*2.5%) 120

Advertising (19200/12) 1600

Vehicle Maintenance (120000*2%) 2400

Freight (120000*0.65%) 780

Total 11200

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

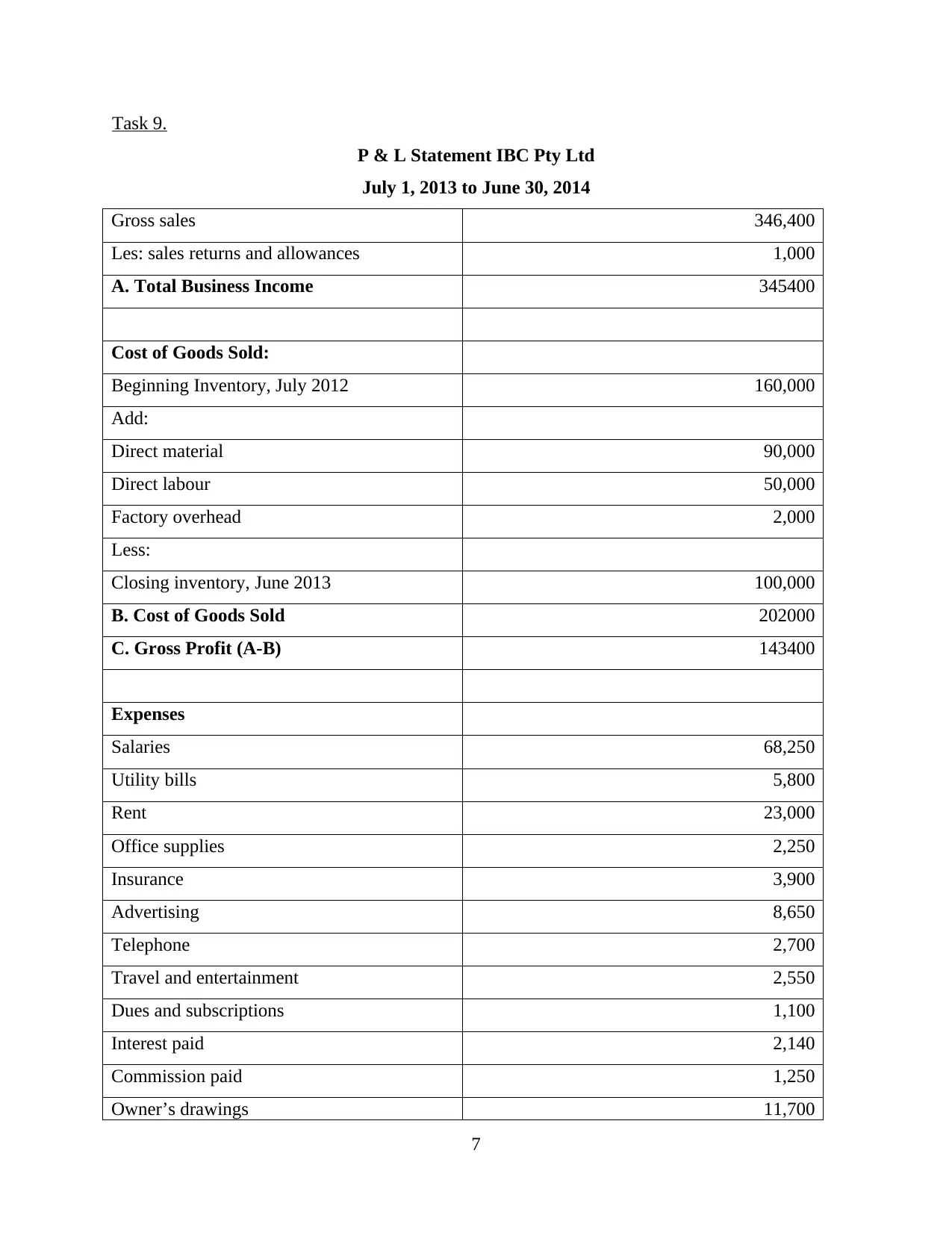

Task 9.

P & L Statement IBC Pty Ltd

July 1, 2013 to June 30, 2014

Gross sales 346,400

Les: sales returns and allowances 1,000

A. Total Business Income 345400

Cost of Goods Sold:

Beginning Inventory, July 2012 160,000

Add:

Direct material 90,000

Direct labour 50,000

Factory overhead 2,000

Less:

Closing inventory, June 2013 100,000

B. Cost of Goods Sold 202000

C. Gross Profit (A-B) 143400

Expenses

Salaries 68,250

Utility bills 5,800

Rent 23,000

Office supplies 2,250

Insurance 3,900

Advertising 8,650

Telephone 2,700

Travel and entertainment 2,550

Dues and subscriptions 1,100

Interest paid 2,140

Commission paid 1,250

Owner’s drawings 11,700

7

P & L Statement IBC Pty Ltd

July 1, 2013 to June 30, 2014

Gross sales 346,400

Les: sales returns and allowances 1,000

A. Total Business Income 345400

Cost of Goods Sold:

Beginning Inventory, July 2012 160,000

Add:

Direct material 90,000

Direct labour 50,000

Factory overhead 2,000

Less:

Closing inventory, June 2013 100,000

B. Cost of Goods Sold 202000

C. Gross Profit (A-B) 143400

Expenses

Salaries 68,250

Utility bills 5,800

Rent 23,000

Office supplies 2,250

Insurance 3,900

Advertising 8,650

Telephone 2,700

Travel and entertainment 2,550

Dues and subscriptions 1,100

Interest paid 2,140

Commission paid 1,250

Owner’s drawings 11,700

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

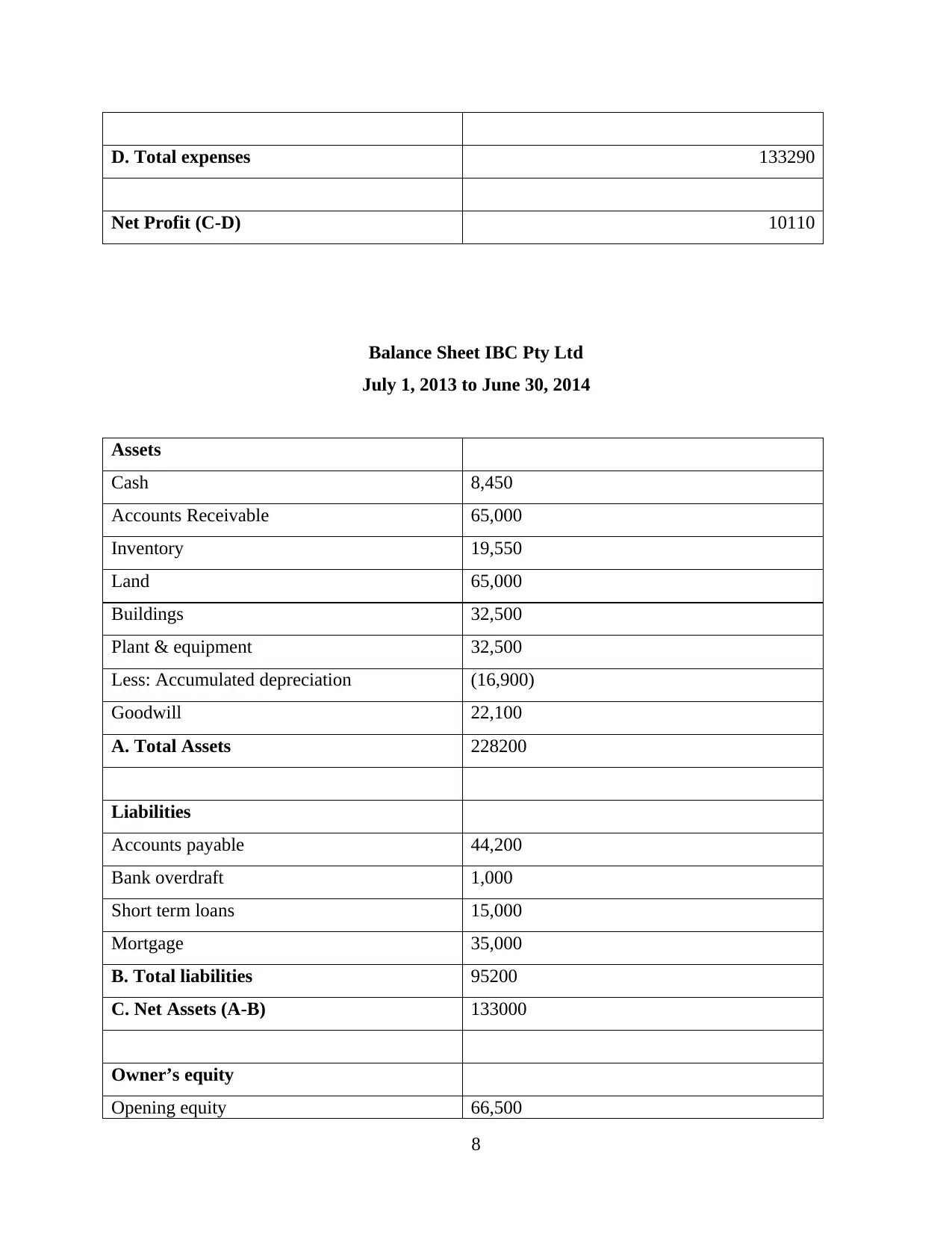

D. Total expenses 133290

Net Profit (C-D) 10110

Balance Sheet IBC Pty Ltd

July 1, 2013 to June 30, 2014

Assets

Cash 8,450

Accounts Receivable 65,000

Inventory 19,550

Land 65,000

Buildings 32,500

Plant & equipment 32,500

Less: Accumulated depreciation (16,900)

Goodwill 22,100

A. Total Assets 228200

Liabilities

Accounts payable 44,200

Bank overdraft 1,000

Short term loans 15,000

Mortgage 35,000

B. Total liabilities 95200

C. Net Assets (A-B) 133000

Owner’s equity

Opening equity 66,500

8

Net Profit (C-D) 10110

Balance Sheet IBC Pty Ltd

July 1, 2013 to June 30, 2014

Assets

Cash 8,450

Accounts Receivable 65,000

Inventory 19,550

Land 65,000

Buildings 32,500

Plant & equipment 32,500

Less: Accumulated depreciation (16,900)

Goodwill 22,100

A. Total Assets 228200

Liabilities

Accounts payable 44,200

Bank overdraft 1,000

Short term loans 15,000

Mortgage 35,000

B. Total liabilities 95200

C. Net Assets (A-B) 133000

Owner’s equity

Opening equity 66,500

8

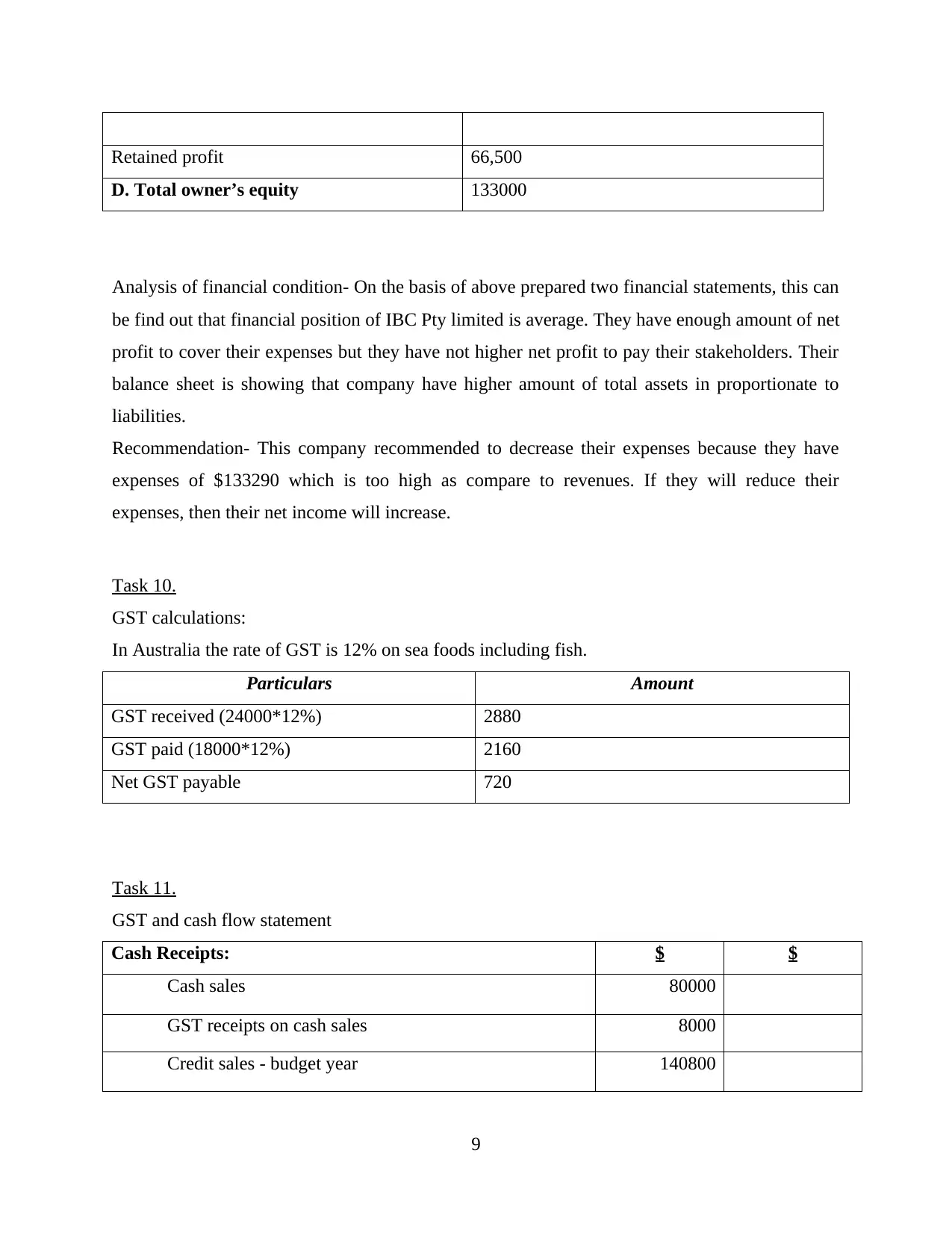

Retained profit 66,500

D. Total owner’s equity 133000

Analysis of financial condition- On the basis of above prepared two financial statements, this can

be find out that financial position of IBC Pty limited is average. They have enough amount of net

profit to cover their expenses but they have not higher net profit to pay their stakeholders. Their

balance sheet is showing that company have higher amount of total assets in proportionate to

liabilities.

Recommendation- This company recommended to decrease their expenses because they have

expenses of $133290 which is too high as compare to revenues. If they will reduce their

expenses, then their net income will increase.

Task 10.

GST calculations:

In Australia the rate of GST is 12% on sea foods including fish.

Particulars Amount

GST received (24000*12%) 2880

GST paid (18000*12%) 2160

Net GST payable 720

Task 11.

GST and cash flow statement

Cash Receipts: $ $

Cash sales 80000

GST receipts on cash sales 8000

Credit sales - budget year 140800

9

D. Total owner’s equity 133000

Analysis of financial condition- On the basis of above prepared two financial statements, this can

be find out that financial position of IBC Pty limited is average. They have enough amount of net

profit to cover their expenses but they have not higher net profit to pay their stakeholders. Their

balance sheet is showing that company have higher amount of total assets in proportionate to

liabilities.

Recommendation- This company recommended to decrease their expenses because they have

expenses of $133290 which is too high as compare to revenues. If they will reduce their

expenses, then their net income will increase.

Task 10.

GST calculations:

In Australia the rate of GST is 12% on sea foods including fish.

Particulars Amount

GST received (24000*12%) 2880

GST paid (18000*12%) 2160

Net GST payable 720

Task 11.

GST and cash flow statement

Cash Receipts: $ $

Cash sales 80000

GST receipts on cash sales 8000

Credit sales - budget year 140800

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

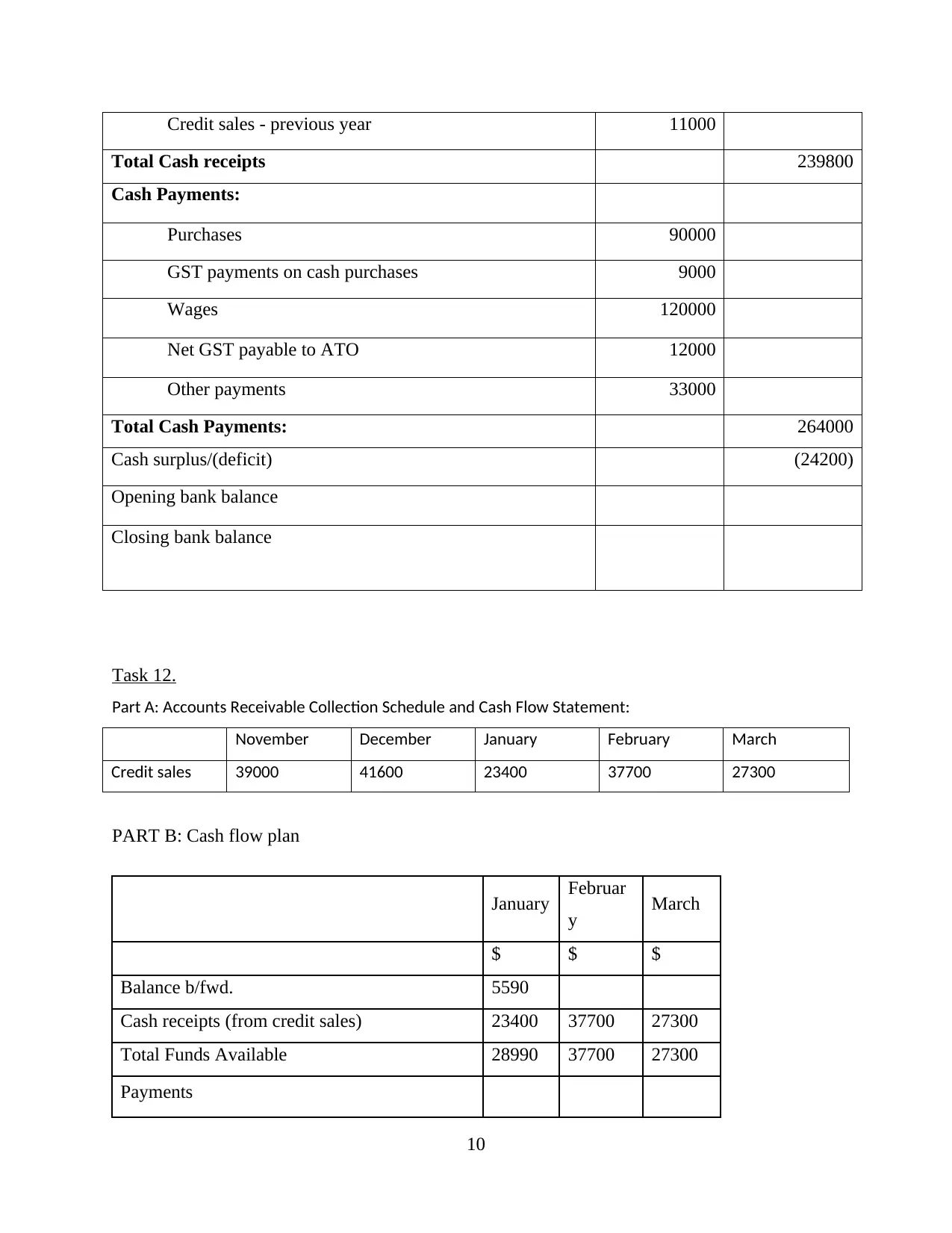

Credit sales - previous year 11000

Total Cash receipts 239800

Cash Payments:

Purchases 90000

GST payments on cash purchases 9000

Wages 120000

Net GST payable to ATO 12000

Other payments 33000

Total Cash Payments: 264000

Cash surplus/(deficit) (24200)

Opening bank balance

Closing bank balance

Task 12.

Part A: Accounts Receivable Collection Schedule and Cash Flow Statement:

November December January February March

Credit sales 39000 41600 23400 37700 27300

PART B: Cash flow plan

January Februar

y March

$ $ $

Balance b/fwd. 5590

Cash receipts (from credit sales) 23400 37700 27300

Total Funds Available 28990 37700 27300

Payments

10

Total Cash receipts 239800

Cash Payments:

Purchases 90000

GST payments on cash purchases 9000

Wages 120000

Net GST payable to ATO 12000

Other payments 33000

Total Cash Payments: 264000

Cash surplus/(deficit) (24200)

Opening bank balance

Closing bank balance

Task 12.

Part A: Accounts Receivable Collection Schedule and Cash Flow Statement:

November December January February March

Credit sales 39000 41600 23400 37700 27300

PART B: Cash flow plan

January Februar

y March

$ $ $

Balance b/fwd. 5590

Cash receipts (from credit sales) 23400 37700 27300

Total Funds Available 28990 37700 27300

Payments

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

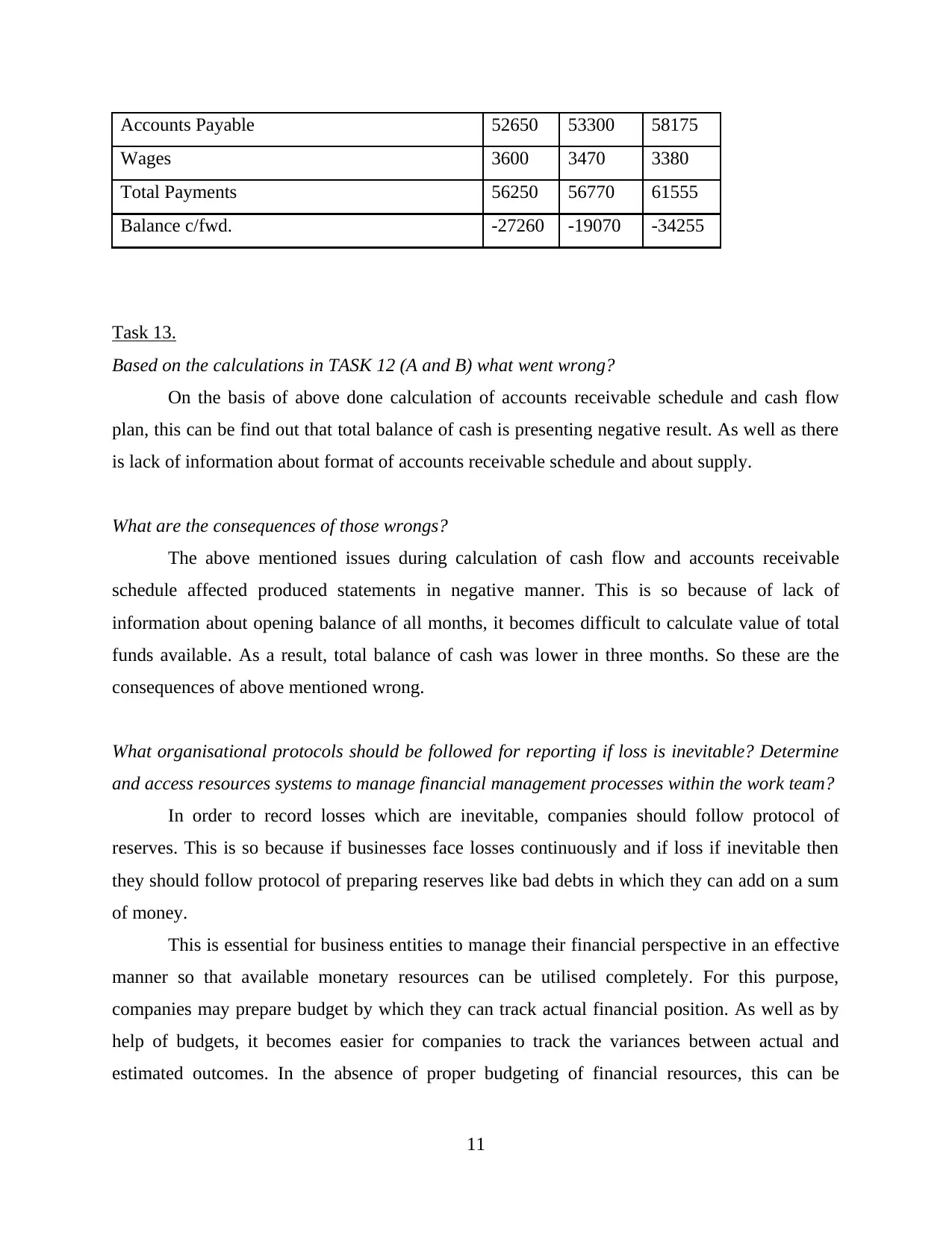

Accounts Payable 52650 53300 58175

Wages 3600 3470 3380

Total Payments 56250 56770 61555

Balance c/fwd. -27260 -19070 -34255

Task 13.

Based on the calculations in TASK 12 (A and B) what went wrong?

On the basis of above done calculation of accounts receivable schedule and cash flow

plan, this can be find out that total balance of cash is presenting negative result. As well as there

is lack of information about format of accounts receivable schedule and about supply.

What are the consequences of those wrongs?

The above mentioned issues during calculation of cash flow and accounts receivable

schedule affected produced statements in negative manner. This is so because of lack of

information about opening balance of all months, it becomes difficult to calculate value of total

funds available. As a result, total balance of cash was lower in three months. So these are the

consequences of above mentioned wrong.

What organisational protocols should be followed for reporting if loss is inevitable? Determine

and access resources systems to manage financial management processes within the work team?

In order to record losses which are inevitable, companies should follow protocol of

reserves. This is so because if businesses face losses continuously and if loss if inevitable then

they should follow protocol of preparing reserves like bad debts in which they can add on a sum

of money.

This is essential for business entities to manage their financial perspective in an effective

manner so that available monetary resources can be utilised completely. For this purpose,

companies may prepare budget by which they can track actual financial position. As well as by

help of budgets, it becomes easier for companies to track the variances between actual and

estimated outcomes. In the absence of proper budgeting of financial resources, this can be

11

Wages 3600 3470 3380

Total Payments 56250 56770 61555

Balance c/fwd. -27260 -19070 -34255

Task 13.

Based on the calculations in TASK 12 (A and B) what went wrong?

On the basis of above done calculation of accounts receivable schedule and cash flow

plan, this can be find out that total balance of cash is presenting negative result. As well as there

is lack of information about format of accounts receivable schedule and about supply.

What are the consequences of those wrongs?

The above mentioned issues during calculation of cash flow and accounts receivable

schedule affected produced statements in negative manner. This is so because of lack of

information about opening balance of all months, it becomes difficult to calculate value of total

funds available. As a result, total balance of cash was lower in three months. So these are the

consequences of above mentioned wrong.

What organisational protocols should be followed for reporting if loss is inevitable? Determine

and access resources systems to manage financial management processes within the work team?

In order to record losses which are inevitable, companies should follow protocol of

reserves. This is so because if businesses face losses continuously and if loss if inevitable then

they should follow protocol of preparing reserves like bad debts in which they can add on a sum

of money.

This is essential for business entities to manage their financial perspective in an effective

manner so that available monetary resources can be utilised completely. For this purpose,

companies may prepare budget by which they can track actual financial position. As well as by

help of budgets, it becomes easier for companies to track the variances between actual and

estimated outcomes. In the absence of proper budgeting of financial resources, this can be

11

difficult to measure actual level of performance as well as to know about adverse variances.

Thus, budgeting is a way that can be helpful in order to manage financial management process.

What support can be provided to the team members to ensure that proper management of

finances is in action? How can the organisation to ensure that documented outcomes are

achievable, accurate and comprehensible in the near future?

In order to ensure that proper management of finance is in action, team member are

needed to be provide data of variance of budget. This is so because it can be helpful to them to

know about those aspects in which performance of company is weaker. As well as they can

ensure that there is effective management of finance is in action.

An organisation can assure that produced outcomes are achievable and accurate in the

future by evaluating their efficiency. This can be done by making comparative analysis of set

financial goals with availability of resources.

12

Thus, budgeting is a way that can be helpful in order to manage financial management process.

What support can be provided to the team members to ensure that proper management of

finances is in action? How can the organisation to ensure that documented outcomes are

achievable, accurate and comprehensible in the near future?

In order to ensure that proper management of finance is in action, team member are

needed to be provide data of variance of budget. This is so because it can be helpful to them to

know about those aspects in which performance of company is weaker. As well as they can

ensure that there is effective management of finance is in action.

An organisation can assure that produced outcomes are achievable and accurate in the

future by evaluating their efficiency. This can be done by making comparative analysis of set

financial goals with availability of resources.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.