University Finance for Managers (ACC00724) - Assessment 2 Report

VerifiedAdded on 2022/08/19

|8

|826

|13

Report

AI Summary

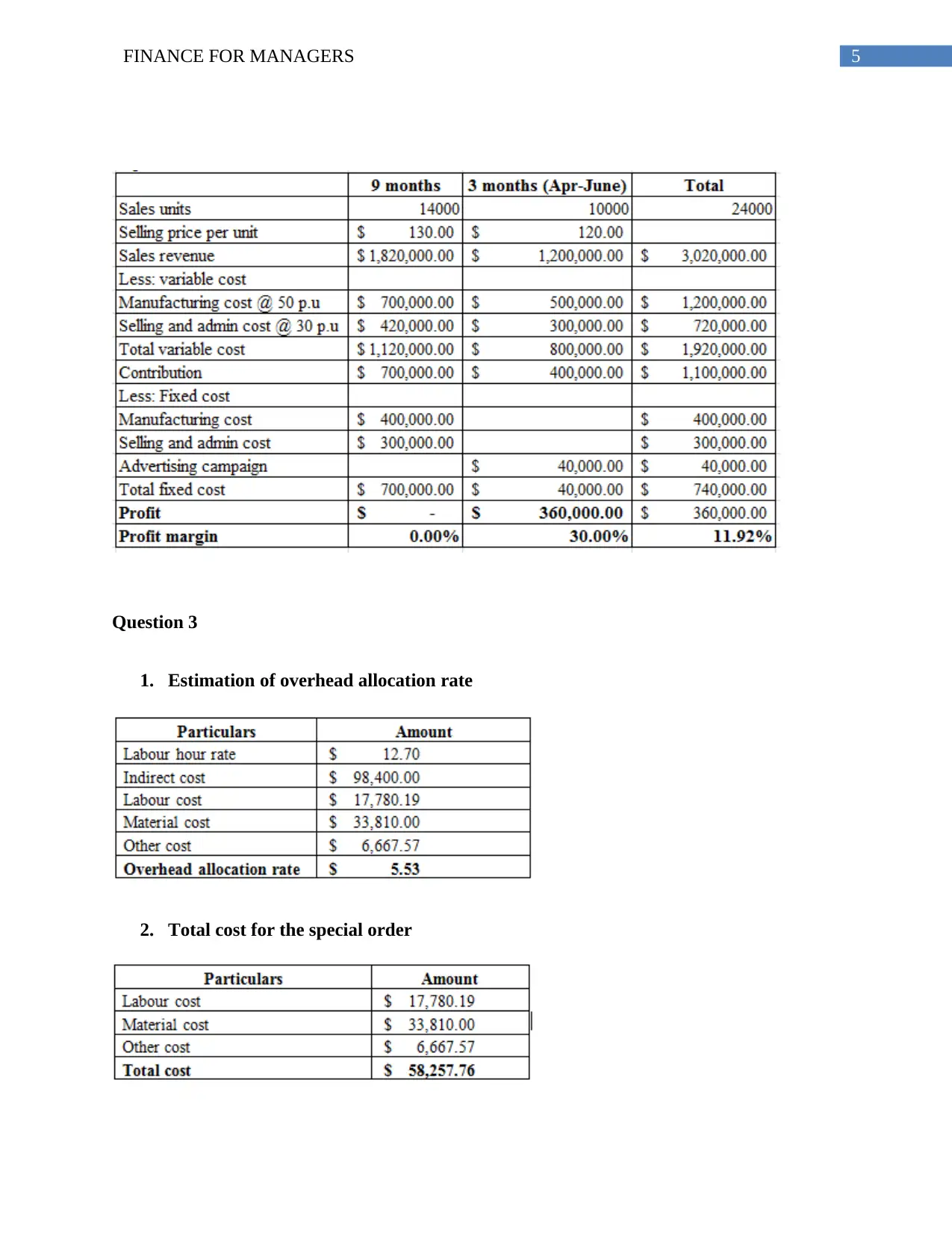

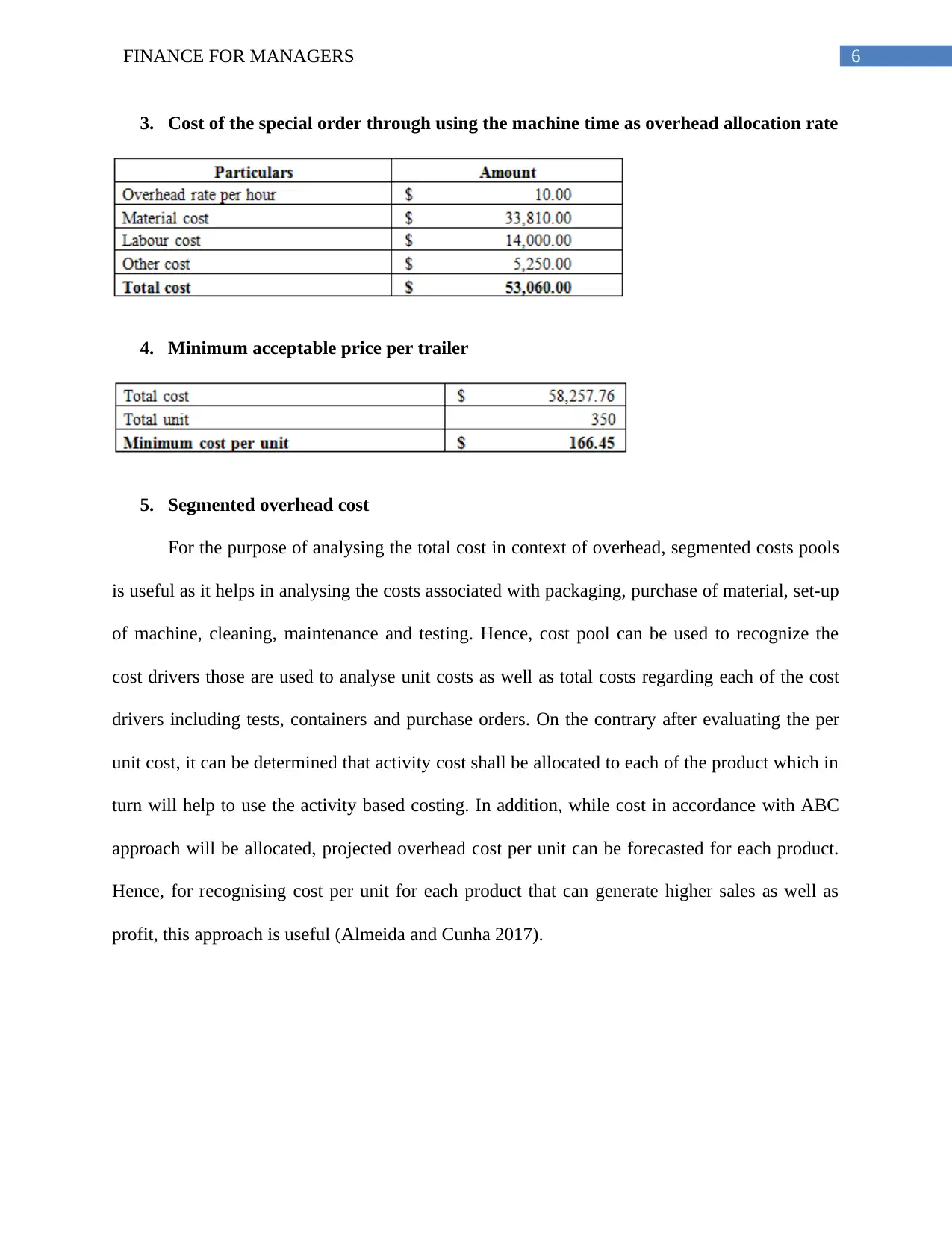

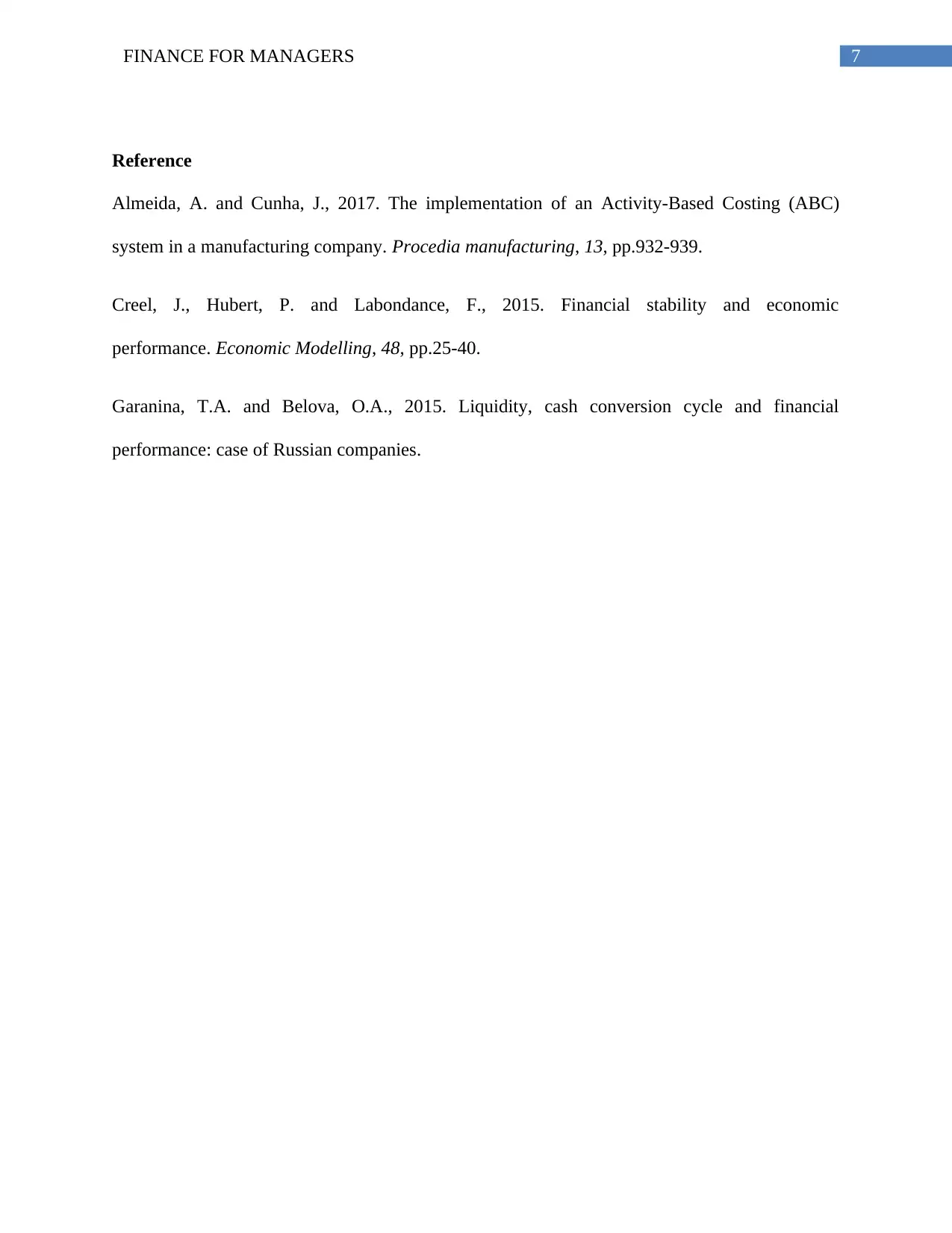

This report, prepared for a Finance for Managers course, analyzes the financial performance of Grafton Pty Ltd. It begins by calculating and interpreting liquidity and financial stability ratios for 2018 and 2019, assessing the company's position relative to industry averages. The report then evaluates three investment proposals, comparing their impact on profit, profit margin, and break-even units to recommend the most beneficial option. Finally, it delves into cost accounting, estimating overhead allocation rates and analyzing the costs associated with a special order, including segmented overhead costs and minimum acceptable pricing strategies. The report references relevant academic literature to support its analysis.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.