Farm Organic Ltd: Budgeting, Variance Analysis, Costing Solutions

VerifiedAdded on 2022/10/14

|12

|2916

|471

Homework Assignment

AI Summary

This document provides a comprehensive solution to a finance assignment for Farm Organic Ltd. The assignment covers several key areas of financial management, including preparing a cash budget with detailed calculations for budgeted receipts and payments, including purchase and cash collection schedules. It also delves into variance analysis, calculating material price and usage variances, as well as labor rate and efficiency variances. Furthermore, the assignment explores activity-based costing (ABC) through a memorandum, comparing traditional costing methods with ABC and recommending its use. Additionally, the document addresses non-routine decisions, such as make-or-buy analysis, and discusses qualitative factors that influence these decisions. Finally, the assignment includes a discussion on zero-based budgeting (ZBB) explaining its advantages, disadvantages and behavioral implications.

Answer 1

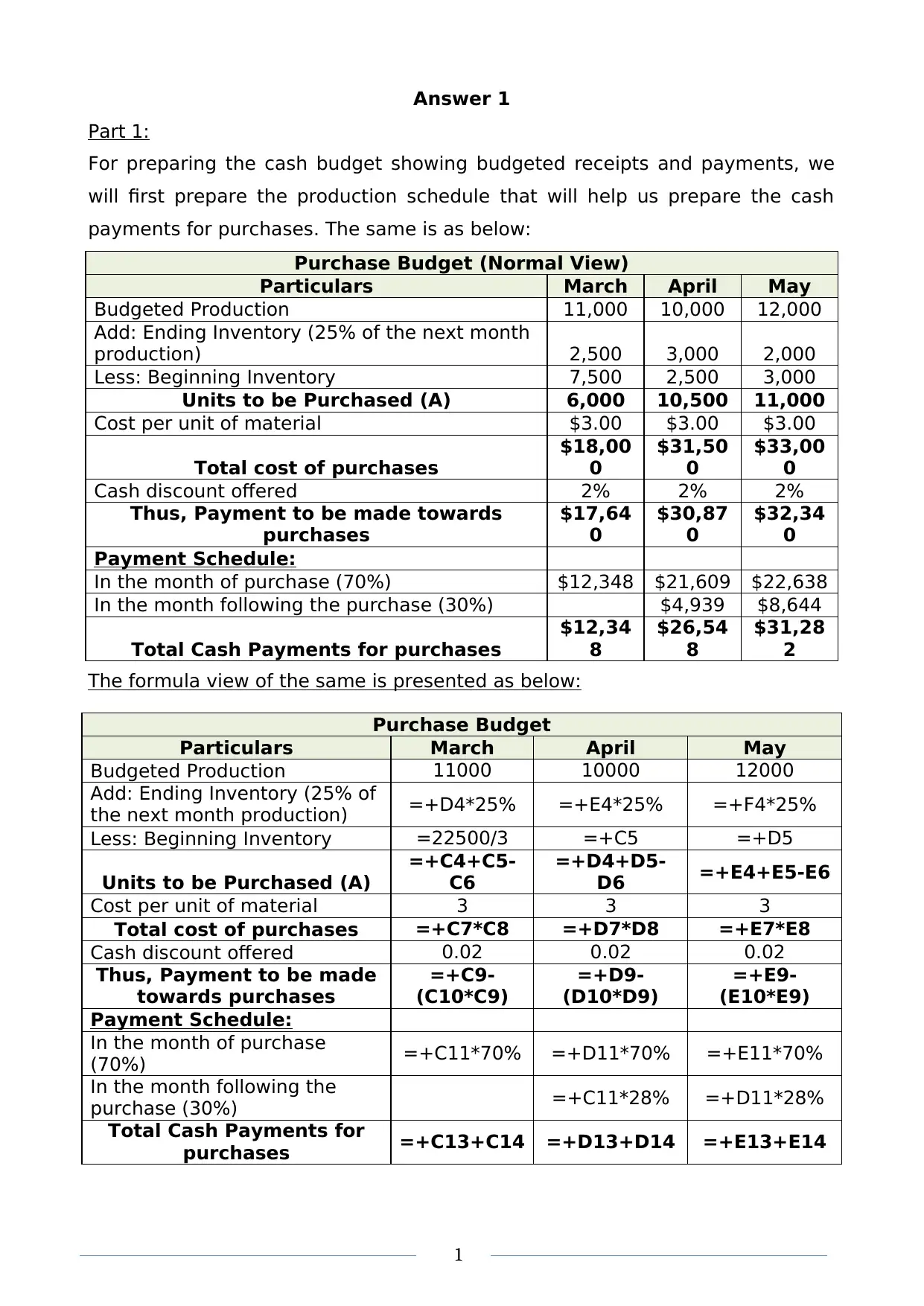

Part 1:

For preparing the cash budget showing budgeted receipts and payments, we

will first prepare the production schedule that will help us prepare the cash

payments for purchases. The same is as below:

Purchase Budget (Normal View)

Particulars March April May

Budgeted Production 11,000 10,000 12,000

Add: Ending Inventory (25% of the next month

production) 2,500 3,000 2,000

Less: Beginning Inventory 7,500 2,500 3,000

Units to be Purchased (A) 6,000 10,500 11,000

Cost per unit of material $3.00 $3.00 $3.00

Total cost of purchases

$18,00

0

$31,50

0

$33,00

0

Cash discount offered 2% 2% 2%

Thus, Payment to be made towards

purchases

$17,64

0

$30,87

0

$32,34

0

Payment Schedule:

In the month of purchase (70%) $12,348 $21,609 $22,638

In the month following the purchase (30%) $4,939 $8,644

Total Cash Payments for purchases

$12,34

8

$26,54

8

$31,28

2

The formula view of the same is presented as below:

Purchase Budget

Particulars March April May

Budgeted Production 11000 10000 12000

Add: Ending Inventory (25% of

the next month production) =+D4*25% =+E4*25% =+F4*25%

Less: Beginning Inventory =22500/3 =+C5 =+D5

Units to be Purchased (A)

=+C4+C5-

C6

=+D4+D5-

D6 =+E4+E5-E6

Cost per unit of material 3 3 3

Total cost of purchases =+C7*C8 =+D7*D8 =+E7*E8

Cash discount offered 0.02 0.02 0.02

Thus, Payment to be made

towards purchases

=+C9-

(C10*C9)

=+D9-

(D10*D9)

=+E9-

(E10*E9)

Payment Schedule:

In the month of purchase

(70%) =+C11*70% =+D11*70% =+E11*70%

In the month following the

purchase (30%) =+C11*28% =+D11*28%

Total Cash Payments for

purchases =+C13+C14 =+D13+D14 =+E13+E14

1

Part 1:

For preparing the cash budget showing budgeted receipts and payments, we

will first prepare the production schedule that will help us prepare the cash

payments for purchases. The same is as below:

Purchase Budget (Normal View)

Particulars March April May

Budgeted Production 11,000 10,000 12,000

Add: Ending Inventory (25% of the next month

production) 2,500 3,000 2,000

Less: Beginning Inventory 7,500 2,500 3,000

Units to be Purchased (A) 6,000 10,500 11,000

Cost per unit of material $3.00 $3.00 $3.00

Total cost of purchases

$18,00

0

$31,50

0

$33,00

0

Cash discount offered 2% 2% 2%

Thus, Payment to be made towards

purchases

$17,64

0

$30,87

0

$32,34

0

Payment Schedule:

In the month of purchase (70%) $12,348 $21,609 $22,638

In the month following the purchase (30%) $4,939 $8,644

Total Cash Payments for purchases

$12,34

8

$26,54

8

$31,28

2

The formula view of the same is presented as below:

Purchase Budget

Particulars March April May

Budgeted Production 11000 10000 12000

Add: Ending Inventory (25% of

the next month production) =+D4*25% =+E4*25% =+F4*25%

Less: Beginning Inventory =22500/3 =+C5 =+D5

Units to be Purchased (A)

=+C4+C5-

C6

=+D4+D5-

D6 =+E4+E5-E6

Cost per unit of material 3 3 3

Total cost of purchases =+C7*C8 =+D7*D8 =+E7*E8

Cash discount offered 0.02 0.02 0.02

Thus, Payment to be made

towards purchases

=+C9-

(C10*C9)

=+D9-

(D10*D9)

=+E9-

(E10*E9)

Payment Schedule:

In the month of purchase

(70%) =+C11*70% =+D11*70% =+E11*70%

In the month following the

purchase (30%) =+C11*28% =+D11*28%

Total Cash Payments for

purchases =+C13+C14 =+D13+D14 =+E13+E14

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

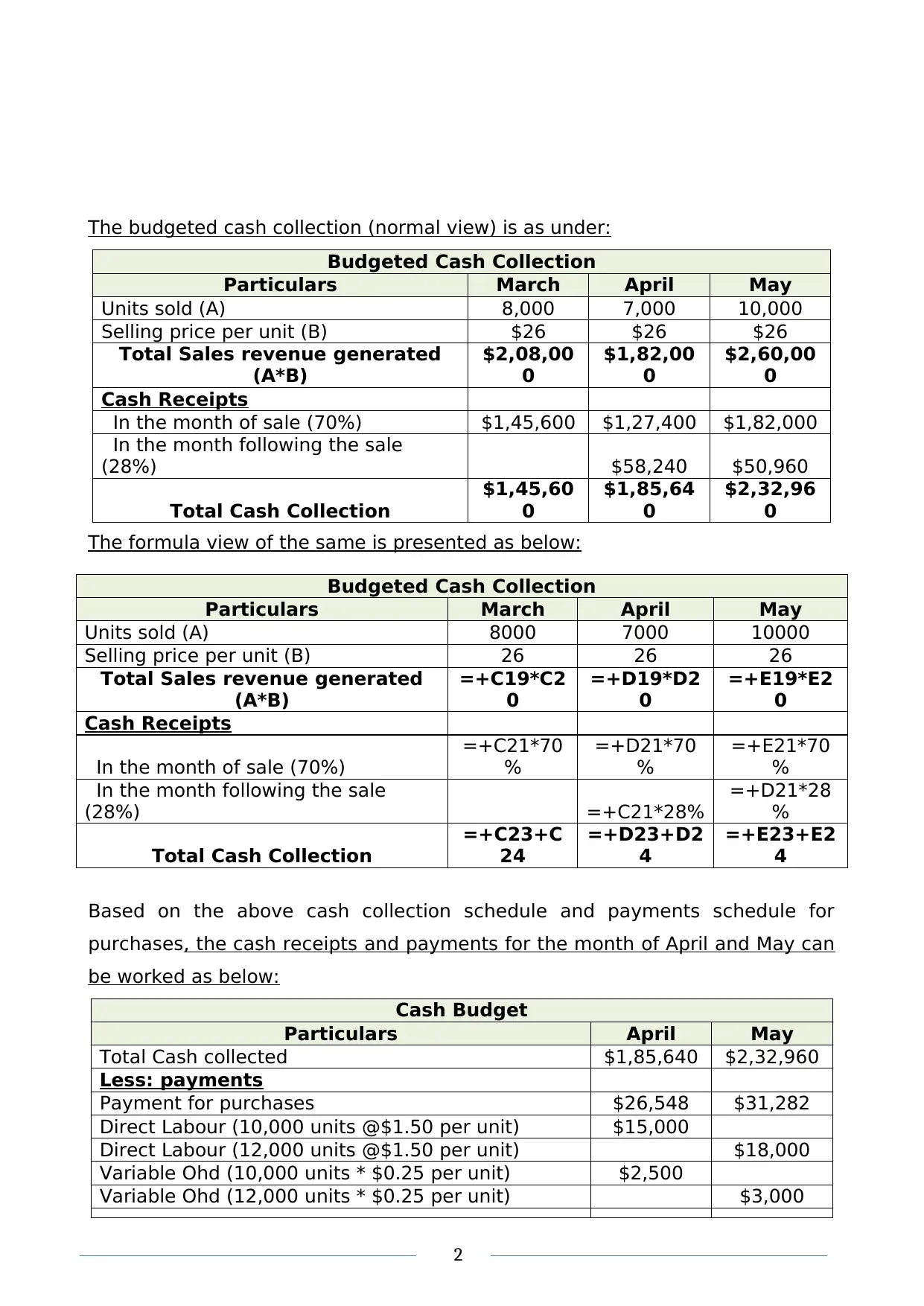

The budgeted cash collection (normal view) is as under:

Budgeted Cash Collection

Particulars March April May

Units sold (A) 8,000 7,000 10,000

Selling price per unit (B) $26 $26 $26

Total Sales revenue generated

(A*B)

$2,08,00

0

$1,82,00

0

$2,60,00

0

Cash Receipts

In the month of sale (70%) $1,45,600 $1,27,400 $1,82,000

In the month following the sale

(28%) $58,240 $50,960

Total Cash Collection

$1,45,60

0

$1,85,64

0

$2,32,96

0

The formula view of the same is presented as below:

Budgeted Cash Collection

Particulars March April May

Units sold (A) 8000 7000 10000

Selling price per unit (B) 26 26 26

Total Sales revenue generated

(A*B)

=+C19*C2

0

=+D19*D2

0

=+E19*E2

0

Cash Receipts

In the month of sale (70%)

=+C21*70

%

=+D21*70

%

=+E21*70

%

In the month following the sale

(28%) =+C21*28%

=+D21*28

%

Total Cash Collection

=+C23+C

24

=+D23+D2

4

=+E23+E2

4

Based on the above cash collection schedule and payments schedule for

purchases, the cash receipts and payments for the month of April and May can

be worked as below:

Cash Budget

Particulars April May

Total Cash collected $1,85,640 $2,32,960

Less: payments

Payment for purchases $26,548 $31,282

Direct Labour (10,000 units @$1.50 per unit) $15,000

Direct Labour (12,000 units @$1.50 per unit) $18,000

Variable Ohd (10,000 units * $0.25 per unit) $2,500

Variable Ohd (12,000 units * $0.25 per unit) $3,000

2

Budgeted Cash Collection

Particulars March April May

Units sold (A) 8,000 7,000 10,000

Selling price per unit (B) $26 $26 $26

Total Sales revenue generated

(A*B)

$2,08,00

0

$1,82,00

0

$2,60,00

0

Cash Receipts

In the month of sale (70%) $1,45,600 $1,27,400 $1,82,000

In the month following the sale

(28%) $58,240 $50,960

Total Cash Collection

$1,45,60

0

$1,85,64

0

$2,32,96

0

The formula view of the same is presented as below:

Budgeted Cash Collection

Particulars March April May

Units sold (A) 8000 7000 10000

Selling price per unit (B) 26 26 26

Total Sales revenue generated

(A*B)

=+C19*C2

0

=+D19*D2

0

=+E19*E2

0

Cash Receipts

In the month of sale (70%)

=+C21*70

%

=+D21*70

%

=+E21*70

%

In the month following the sale

(28%) =+C21*28%

=+D21*28

%

Total Cash Collection

=+C23+C

24

=+D23+D2

4

=+E23+E2

4

Based on the above cash collection schedule and payments schedule for

purchases, the cash receipts and payments for the month of April and May can

be worked as below:

Cash Budget

Particulars April May

Total Cash collected $1,85,640 $2,32,960

Less: payments

Payment for purchases $26,548 $31,282

Direct Labour (10,000 units @$1.50 per unit) $15,000

Direct Labour (12,000 units @$1.50 per unit) $18,000

Variable Ohd (10,000 units * $0.25 per unit) $2,500

Variable Ohd (12,000 units * $0.25 per unit) $3,000

2

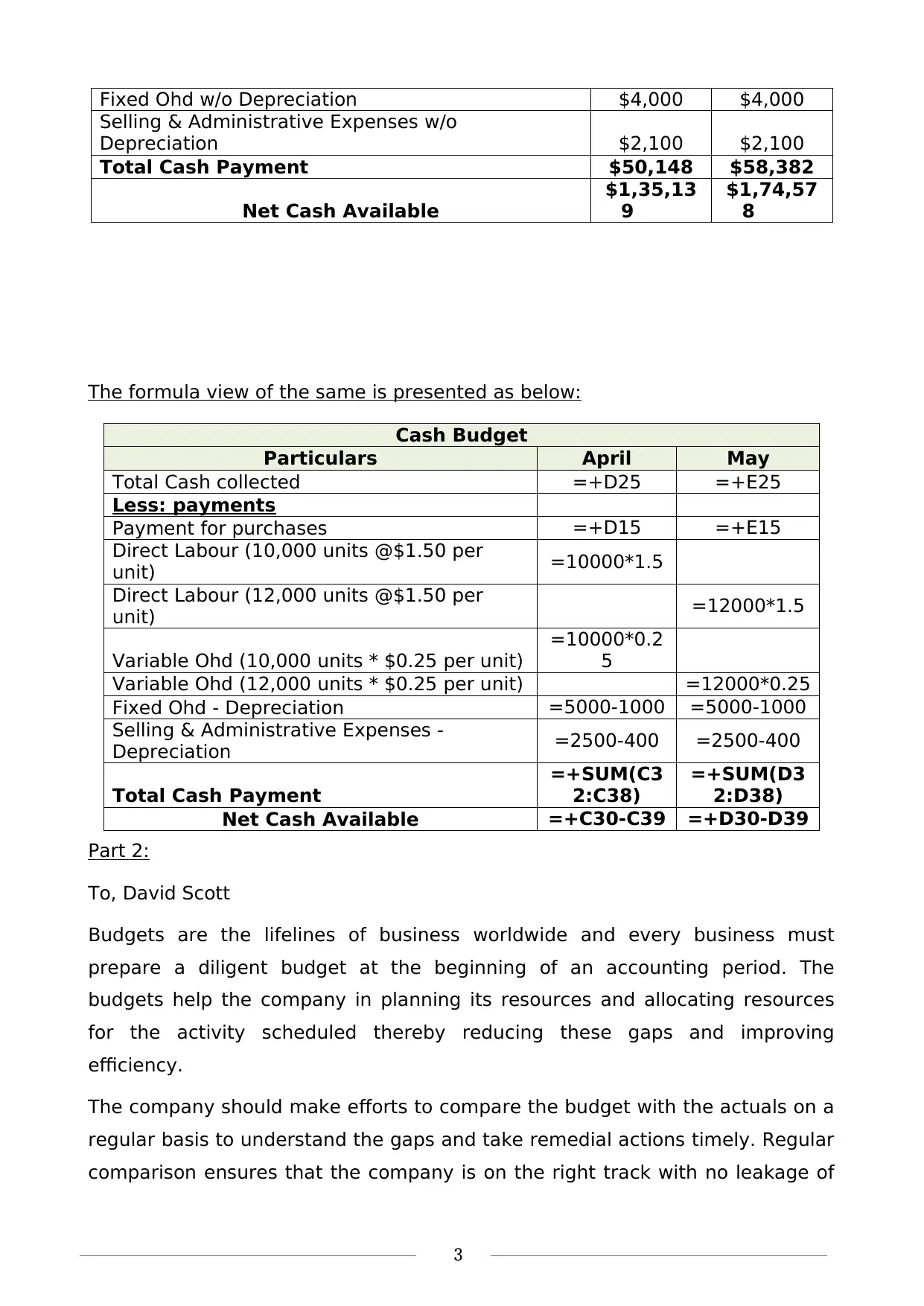

Fixed Ohd w/o Depreciation $4,000 $4,000

Selling & Administrative Expenses w/o

Depreciation $2,100 $2,100

Total Cash Payment $50,148 $58,382

Net Cash Available

$1,35,13

9

$1,74,57

8

The formula view of the same is presented as below:

Cash Budget

Particulars April May

Total Cash collected =+D25 =+E25

Less: payments

Payment for purchases =+D15 =+E15

Direct Labour (10,000 units @$1.50 per

unit) =10000*1.5

Direct Labour (12,000 units @$1.50 per

unit) =12000*1.5

Variable Ohd (10,000 units * $0.25 per unit)

=10000*0.2

5

Variable Ohd (12,000 units * $0.25 per unit) =12000*0.25

Fixed Ohd - Depreciation =5000-1000 =5000-1000

Selling & Administrative Expenses -

Depreciation =2500-400 =2500-400

Total Cash Payment

=+SUM(C3

2:C38)

=+SUM(D3

2:D38)

Net Cash Available =+C30-C39 =+D30-D39

Part 2:

To, David Scott

Budgets are the lifelines of business worldwide and every business must

prepare a diligent budget at the beginning of an accounting period. The

budgets help the company in planning its resources and allocating resources

for the activity scheduled thereby reducing these gaps and improving

efficiency.

The company should make efforts to compare the budget with the actuals on a

regular basis to understand the gaps and take remedial actions timely. Regular

comparison ensures that the company is on the right track with no leakage of

3

Selling & Administrative Expenses w/o

Depreciation $2,100 $2,100

Total Cash Payment $50,148 $58,382

Net Cash Available

$1,35,13

9

$1,74,57

8

The formula view of the same is presented as below:

Cash Budget

Particulars April May

Total Cash collected =+D25 =+E25

Less: payments

Payment for purchases =+D15 =+E15

Direct Labour (10,000 units @$1.50 per

unit) =10000*1.5

Direct Labour (12,000 units @$1.50 per

unit) =12000*1.5

Variable Ohd (10,000 units * $0.25 per unit)

=10000*0.2

5

Variable Ohd (12,000 units * $0.25 per unit) =12000*0.25

Fixed Ohd - Depreciation =5000-1000 =5000-1000

Selling & Administrative Expenses -

Depreciation =2500-400 =2500-400

Total Cash Payment

=+SUM(C3

2:C38)

=+SUM(D3

2:D38)

Net Cash Available =+C30-C39 =+D30-D39

Part 2:

To, David Scott

Budgets are the lifelines of business worldwide and every business must

prepare a diligent budget at the beginning of an accounting period. The

budgets help the company in planning its resources and allocating resources

for the activity scheduled thereby reducing these gaps and improving

efficiency.

The company should make efforts to compare the budget with the actuals on a

regular basis to understand the gaps and take remedial actions timely. Regular

comparison ensures that the company is on the right track with no leakage of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

resources. The comparison with the actual reflects the variances, which should

be analyzed and minimized.

Budgets help the company identify the variances timely thereby enabling the

company to take corrective actions in time and improve the profitability and

performance of the company.

Budget is a shield, which helps the company in overcoming the challenges in

time, and thus run the business smoothly.

Regards.

Answer 2

To, David Scott

Sub: Zero-Based Budgeting (ZBB)

Zero based budgeting as the name suggests starts with zero base indicating all

the expenses to be incurred by the company must be justified for each period

(Kagan, 2019). This is different from the traditional budgeting approach where

the previous year budget becomes the base for the current year. Here, all the

expenses and costs must be analyzed from scratch and justified before they

are approved.

The benefits of Zero-Based Budgeting are:

Decision Making: Analyzing each item of costs from scratch ensures

that all costs are explained and justified, thus improving the decision

making based on reliable costs (“Zero Based Budgeting | Meaning, Steps,

Advantage, Disadvantage”, 2019).

Optimal Allocation of Funds: The reliable estimation ensures that the

funds are allocated optimally between the activities of the firm.

ZBB returns proper justification of all expenses and costs.

The redundant activities and processes of the company are eliminated as

the ZBB focuses on the most important activities and allocated costs for

it.

4

be analyzed and minimized.

Budgets help the company identify the variances timely thereby enabling the

company to take corrective actions in time and improve the profitability and

performance of the company.

Budget is a shield, which helps the company in overcoming the challenges in

time, and thus run the business smoothly.

Regards.

Answer 2

To, David Scott

Sub: Zero-Based Budgeting (ZBB)

Zero based budgeting as the name suggests starts with zero base indicating all

the expenses to be incurred by the company must be justified for each period

(Kagan, 2019). This is different from the traditional budgeting approach where

the previous year budget becomes the base for the current year. Here, all the

expenses and costs must be analyzed from scratch and justified before they

are approved.

The benefits of Zero-Based Budgeting are:

Decision Making: Analyzing each item of costs from scratch ensures

that all costs are explained and justified, thus improving the decision

making based on reliable costs (“Zero Based Budgeting | Meaning, Steps,

Advantage, Disadvantage”, 2019).

Optimal Allocation of Funds: The reliable estimation ensures that the

funds are allocated optimally between the activities of the firm.

ZBB returns proper justification of all expenses and costs.

The redundant activities and processes of the company are eliminated as

the ZBB focuses on the most important activities and allocated costs for

it.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

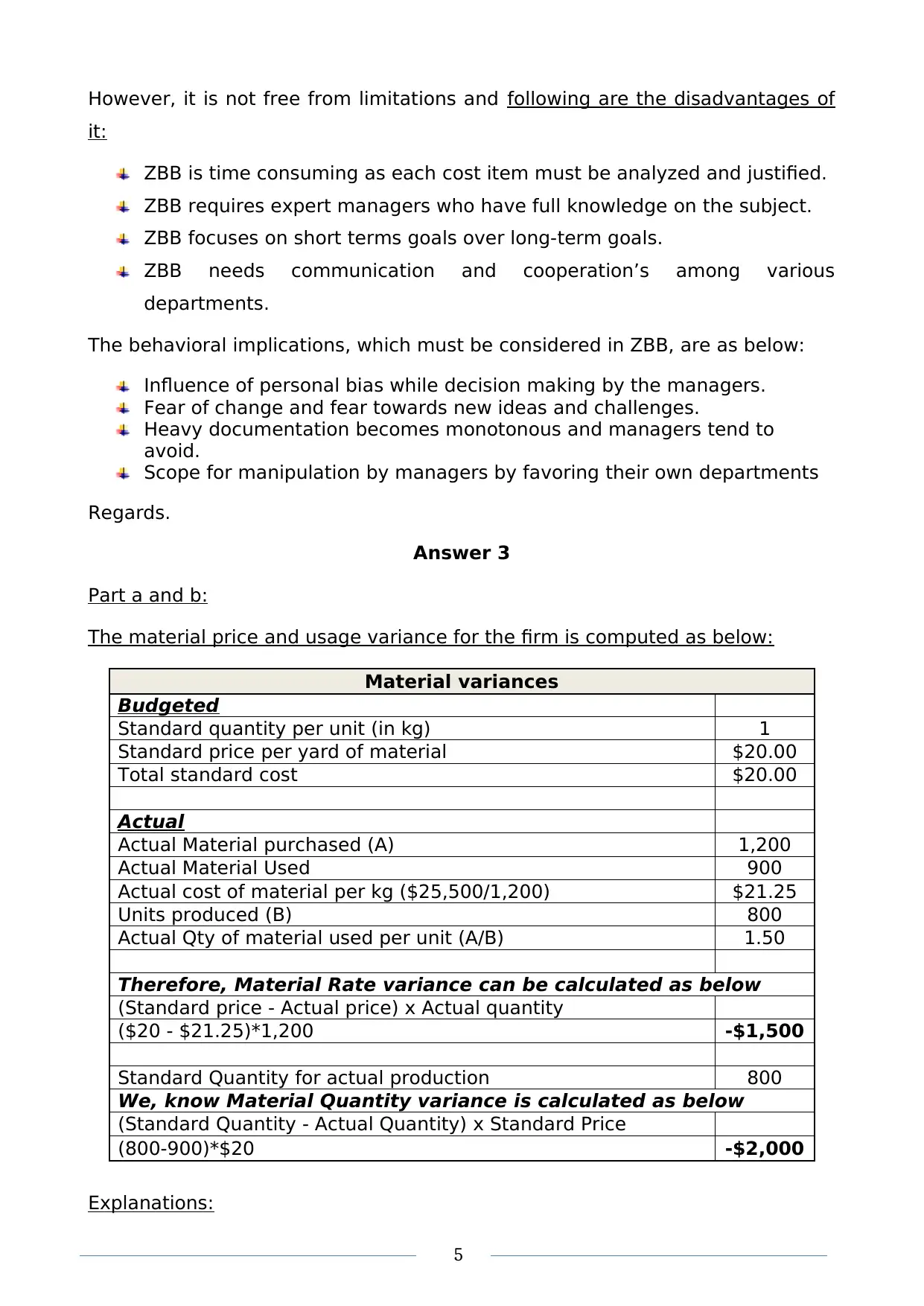

However, it is not free from limitations and following are the disadvantages of

it:

ZBB is time consuming as each cost item must be analyzed and justified.

ZBB requires expert managers who have full knowledge on the subject.

ZBB focuses on short terms goals over long-term goals.

ZBB needs communication and cooperation’s among various

departments.

The behavioral implications, which must be considered in ZBB, are as below:

Influence of personal bias while decision making by the managers.

Fear of change and fear towards new ideas and challenges.

Heavy documentation becomes monotonous and managers tend to

avoid.

Scope for manipulation by managers by favoring their own departments

Regards.

Answer 3

Part a and b:

The material price and usage variance for the firm is computed as below:

Material variances

Budgeted

Standard quantity per unit (in kg) 1

Standard price per yard of material $20.00

Total standard cost $20.00

Actual

Actual Material purchased (A) 1,200

Actual Material Used 900

Actual cost of material per kg ($25,500/1,200) $21.25

Units produced (B) 800

Actual Qty of material used per unit (A/B) 1.50

Therefore, Material Rate variance can be calculated as below

(Standard price - Actual price) x Actual quantity

($20 - $21.25)*1,200 -$1,500

Standard Quantity for actual production 800

We, know Material Quantity variance is calculated as below

(Standard Quantity - Actual Quantity) x Standard Price

(800-900)*$20 -$2,000

Explanations:

5

it:

ZBB is time consuming as each cost item must be analyzed and justified.

ZBB requires expert managers who have full knowledge on the subject.

ZBB focuses on short terms goals over long-term goals.

ZBB needs communication and cooperation’s among various

departments.

The behavioral implications, which must be considered in ZBB, are as below:

Influence of personal bias while decision making by the managers.

Fear of change and fear towards new ideas and challenges.

Heavy documentation becomes monotonous and managers tend to

avoid.

Scope for manipulation by managers by favoring their own departments

Regards.

Answer 3

Part a and b:

The material price and usage variance for the firm is computed as below:

Material variances

Budgeted

Standard quantity per unit (in kg) 1

Standard price per yard of material $20.00

Total standard cost $20.00

Actual

Actual Material purchased (A) 1,200

Actual Material Used 900

Actual cost of material per kg ($25,500/1,200) $21.25

Units produced (B) 800

Actual Qty of material used per unit (A/B) 1.50

Therefore, Material Rate variance can be calculated as below

(Standard price - Actual price) x Actual quantity

($20 - $21.25)*1,200 -$1,500

Standard Quantity for actual production 800

We, know Material Quantity variance is calculated as below

(Standard Quantity - Actual Quantity) x Standard Price

(800-900)*$20 -$2,000

Explanations:

5

Since, the actual material rate per kg is higher than the standard rate per

kg, the variance is unfavorable

Since, the actual quantity used is more than the standard quantity for

actual production, the variance is unfavorable

Answers:

The material price variance is $1,500 unfavorable

The material usage variance is $2,000 unfavorable.

Part c and d:

The direct labour rate and efficiency variance for the firm is computed as

below:

Labour Variances

Budgeted

Standard Labour Hours per unit 0.25

Standard Labour Rate per Hour ($15/0.25) $60.00

Actual

Direct labour hours worked 280

Production (in units) 800

Actual Direct Labour Rate per hour $60.00

From above information, we can calculate the

following:

Actual Labour Rate cost (Labour rate * labor hours) 16,800

Labour Rate variance can be calculated as below

(Standard rate - Actual rate) x Actual hours worked $0

Labour Efficiency variance can be calculated as below

Std hrs for actual production $200

(Standard hours - Actual hours) x Standard rate -$4,800

Explanations:

Since, the actual labour rate per hour is equal to the standard rate per

hour, the variance is NIL

6

kg, the variance is unfavorable

Since, the actual quantity used is more than the standard quantity for

actual production, the variance is unfavorable

Answers:

The material price variance is $1,500 unfavorable

The material usage variance is $2,000 unfavorable.

Part c and d:

The direct labour rate and efficiency variance for the firm is computed as

below:

Labour Variances

Budgeted

Standard Labour Hours per unit 0.25

Standard Labour Rate per Hour ($15/0.25) $60.00

Actual

Direct labour hours worked 280

Production (in units) 800

Actual Direct Labour Rate per hour $60.00

From above information, we can calculate the

following:

Actual Labour Rate cost (Labour rate * labor hours) 16,800

Labour Rate variance can be calculated as below

(Standard rate - Actual rate) x Actual hours worked $0

Labour Efficiency variance can be calculated as below

Std hrs for actual production $200

(Standard hours - Actual hours) x Standard rate -$4,800

Explanations:

Since, the actual labour rate per hour is equal to the standard rate per

hour, the variance is NIL

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Since, the actual hour is more than the standard hour for actual

production, the variance is unfavorable

Answers:

The direct labour rate variance is 0

The direct labour efficiency variance is $4,800 unfavorable.

Part e:

The total overhead variance for the company will be Actual Overhead less the

standard overhead applied.

Actual Overhead cost = $4,500

Standard overhead applied = 200 units * $3 per unit = $600

Thus, overhead variance = $600 - $4,500 = $3,900 unfavorable.

The journal entries for the cost flow will be as under:

Particulars Debit Credit

Raw Material Inventory $22,500

To Accounts Payable $22,500

(Being raw material purchased on credit)

Work In process Inventory $16,800

To Wages Payable $16,800

(Being wages payable @60 per hour for 280

hours)

Work In process Inventory $4,500

To Manufacturing Overhead $4,500

(Being mfg. ohd. incurred)

7

production, the variance is unfavorable

Answers:

The direct labour rate variance is 0

The direct labour efficiency variance is $4,800 unfavorable.

Part e:

The total overhead variance for the company will be Actual Overhead less the

standard overhead applied.

Actual Overhead cost = $4,500

Standard overhead applied = 200 units * $3 per unit = $600

Thus, overhead variance = $600 - $4,500 = $3,900 unfavorable.

The journal entries for the cost flow will be as under:

Particulars Debit Credit

Raw Material Inventory $22,500

To Accounts Payable $22,500

(Being raw material purchased on credit)

Work In process Inventory $16,800

To Wages Payable $16,800

(Being wages payable @60 per hour for 280

hours)

Work In process Inventory $4,500

To Manufacturing Overhead $4,500

(Being mfg. ohd. incurred)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer 4

Memorandum on Usage of Activity Based Costing

To, David Scott,

Overhead costs are an important part of the product cost and their appropriate

allocation is quintessential for the company.

1. The company is currently using the traditional method of allocating the

indirect product costs using the direct labour costs of the company. The

total overhead costs of the company is a percentage of the total direct

labour cost incurred by the company and allocated evenly to all the

products of the company.

2. ABC or the Activity Based Costing System is a modern approach to

costing where all the major activities of the company are identified along

with their total costs. These total costs are then allocated to the

company’s products based on their usage of the resources under the

activity (AccountingCoach.com, 2019). Thus, under ABC system, we have

3 activities with their total costs and total activity level for the year,

based on which we can compute the cost per usage of activity as below:

8

Memorandum on Usage of Activity Based Costing

To, David Scott,

Overhead costs are an important part of the product cost and their appropriate

allocation is quintessential for the company.

1. The company is currently using the traditional method of allocating the

indirect product costs using the direct labour costs of the company. The

total overhead costs of the company is a percentage of the total direct

labour cost incurred by the company and allocated evenly to all the

products of the company.

2. ABC or the Activity Based Costing System is a modern approach to

costing where all the major activities of the company are identified along

with their total costs. These total costs are then allocated to the

company’s products based on their usage of the resources under the

activity (AccountingCoach.com, 2019). Thus, under ABC system, we have

3 activities with their total costs and total activity level for the year,

based on which we can compute the cost per usage of activity as below:

8

Activity Predicte

d cost $

Predicted

Activity

level

Cost/Activity

Inward materials handling $1,500.00 5 $300.00

Research/Quality control $5,000.00 900 $5.56

Outwards materials handling $2,500.00 90 $27.78

5. The costs under traditional and ABC system are different as the base

for allocating the indirect costs are different this leading to different

cost estimation.

6. I would recommend using ABC system of costing, as it is more logical,

modern and robust system of accounting. The use of Activity Based

coting eliminates the problem of even allocation of overheads to all

products of the company by identifying the various activities, and

their usage by each product thereby facilitating appropriate allocation

and better pricing.

Answer 5

Part 1:

The schedule showing the comparison between making and buying of the

component is as below:

Particulars

Make Buy

Total Per

unit Total Per

unit

No. of units 2,00,000 2,00,000

Direct Material $12,00,000 $6.00 $13,20,000 $6.60

Direct Labor $1,90,000 $0.95 $1,90,000 $0.95

Variable Factory Ohd $25,000 $0.13 $25,000 $0.13

Fixed Factory Ohd $3,00,000 $1.50 $1,05,000 $0.53

Total Costs

$17,15,00

0 $8.58

$16,40,00

0 $8.20

Less: Sales value of Surplus

material $1,35,000 $0.68

Net total Costs

$15,80,00

0 $7.90

$16,40,00

0 $8.20

Thus, the difference between making and buying decision is $0.30 per unit

where making the unit @$7.90 is cheaper than buying them at $8.20 per unit.

Part 2:

9

d cost $

Predicted

Activity

level

Cost/Activity

Inward materials handling $1,500.00 5 $300.00

Research/Quality control $5,000.00 900 $5.56

Outwards materials handling $2,500.00 90 $27.78

5. The costs under traditional and ABC system are different as the base

for allocating the indirect costs are different this leading to different

cost estimation.

6. I would recommend using ABC system of costing, as it is more logical,

modern and robust system of accounting. The use of Activity Based

coting eliminates the problem of even allocation of overheads to all

products of the company by identifying the various activities, and

their usage by each product thereby facilitating appropriate allocation

and better pricing.

Answer 5

Part 1:

The schedule showing the comparison between making and buying of the

component is as below:

Particulars

Make Buy

Total Per

unit Total Per

unit

No. of units 2,00,000 2,00,000

Direct Material $12,00,000 $6.00 $13,20,000 $6.60

Direct Labor $1,90,000 $0.95 $1,90,000 $0.95

Variable Factory Ohd $25,000 $0.13 $25,000 $0.13

Fixed Factory Ohd $3,00,000 $1.50 $1,05,000 $0.53

Total Costs

$17,15,00

0 $8.58

$16,40,00

0 $8.20

Less: Sales value of Surplus

material $1,35,000 $0.68

Net total Costs

$15,80,00

0 $7.90

$16,40,00

0 $8.20

Thus, the difference between making and buying decision is $0.30 per unit

where making the unit @$7.90 is cheaper than buying them at $8.20 per unit.

Part 2:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To, David Scott

Sub: Qualitative Factors for non-routine decisions

Dear Sir,

A company in order to run smoothly must make effective and efficient non-

routing decision apart from its core operating decisions that affects the

financial performance of the company. The non-routine decisions may not

directly affect the core operations of the company but affects its financial

performance and thus taking an effective non-regular decision is imperative for

the success of the organization.

These non-routine decisions are non-repetitive, tactical decision that the firm

must make (Bragg, 2019). They fall outside the ambit of the regular operating

decisions, which the firm makes for the smooth operations of its business.

These decisions thus are directed towards the manager for resolution and do

not follow the traditional or usual decision making hierarchy of the

organization. Some examples of such decisions are:

Offering or extending a credit to customers who are experiencing weak

financial position.

Fulfill a rush order by altering the production schedule

Make or buy decisions for a raw material required in the production.

Acceptance or rejection of special order by a customer that is different

from the standard product offering of the company and thus require

changes in the production line.

These non-routine decisions can never be standardized, as they are never the

same. Decisions concerning such non-routine decisions are made tactically

keeping into the incremental income and incremental costs for the firm. The

cost-benefit analysis is undertaken each time for such non-routine decisions

and based on the additional profit margins that the opportunity generates the

decision is made either on acceptance or rejection of the proposal.

10

Sub: Qualitative Factors for non-routine decisions

Dear Sir,

A company in order to run smoothly must make effective and efficient non-

routing decision apart from its core operating decisions that affects the

financial performance of the company. The non-routine decisions may not

directly affect the core operations of the company but affects its financial

performance and thus taking an effective non-regular decision is imperative for

the success of the organization.

These non-routine decisions are non-repetitive, tactical decision that the firm

must make (Bragg, 2019). They fall outside the ambit of the regular operating

decisions, which the firm makes for the smooth operations of its business.

These decisions thus are directed towards the manager for resolution and do

not follow the traditional or usual decision making hierarchy of the

organization. Some examples of such decisions are:

Offering or extending a credit to customers who are experiencing weak

financial position.

Fulfill a rush order by altering the production schedule

Make or buy decisions for a raw material required in the production.

Acceptance or rejection of special order by a customer that is different

from the standard product offering of the company and thus require

changes in the production line.

These non-routine decisions can never be standardized, as they are never the

same. Decisions concerning such non-routine decisions are made tactically

keeping into the incremental income and incremental costs for the firm. The

cost-benefit analysis is undertaken each time for such non-routine decisions

and based on the additional profit margins that the opportunity generates the

decision is made either on acceptance or rejection of the proposal.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The qualitative factors that must be considered while making any non-routine

decisions or specifically for make and buy decisions as in the given case for the

firm are:

Quality: By quality we mean the quality of the end product or end

component that we intend to outsource to external supplier, i.e. Factor X

in the given case. The quality of the factor X should not be compromised

even if bought from the external supplier as quality issue here will affect

the quality of the end product for the company.

Credit Terms extended by the external supplier: The external supplier

should offer favorable terms for the company for us to manage the

working capital requirements.

Credibility and goodwill of the external supplier: The buy decision solely

depends on the goodwill of the supplier. Factor X is a critical part for the

end product and they must be supplied in required quantity at the right

time to enable smooth production. The supplier should have reputation

for timely delivery of materials.

Effect on employee morale owing to reduction in earnings as when the

products are outsourced the earnings of the company are affected.

Thus, non-routine decisions are crucial and must be taken with utmost care to

maximize the performance of the company.

Regards,

11

decisions or specifically for make and buy decisions as in the given case for the

firm are:

Quality: By quality we mean the quality of the end product or end

component that we intend to outsource to external supplier, i.e. Factor X

in the given case. The quality of the factor X should not be compromised

even if bought from the external supplier as quality issue here will affect

the quality of the end product for the company.

Credit Terms extended by the external supplier: The external supplier

should offer favorable terms for the company for us to manage the

working capital requirements.

Credibility and goodwill of the external supplier: The buy decision solely

depends on the goodwill of the supplier. Factor X is a critical part for the

end product and they must be supplied in required quantity at the right

time to enable smooth production. The supplier should have reputation

for timely delivery of materials.

Effect on employee morale owing to reduction in earnings as when the

products are outsourced the earnings of the company are affected.

Thus, non-routine decisions are crucial and must be taken with utmost care to

maximize the performance of the company.

Regards,

11

References

AccountingCoach.com. (2019). Activity Based Costing | Explanation |

AccountingCoach. Retrieved from

https://www.accountingcoach.com/activity-based-costing/explanation on 23

Sep. 2019

Bragg, S. (2019). Nonroutine decision — AccountingTools. Retrieved 23

September 2019, from

https://www.accountingtools.com/articles/2017/5/12/nonroutine-decision

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C., Datar, S., Rajan, M., Maguire, W. and Tan, R. (n.d.). Cost

accounting.

Kagan, J. (2019). Zero-Based Budgeting (ZBB). Retrieved 23 September 2019,

from https://www.investopedia.com/terms/z/zbb.asp

Zero Based Budgeting | Meaning, Steps, Advantage, Disadvantage. (2019).

Retrieved 23 September 2019, from

https://efinancemanagement.com/budgeting/zero-based

12

AccountingCoach.com. (2019). Activity Based Costing | Explanation |

AccountingCoach. Retrieved from

https://www.accountingcoach.com/activity-based-costing/explanation on 23

Sep. 2019

Bragg, S. (2019). Nonroutine decision — AccountingTools. Retrieved 23

September 2019, from

https://www.accountingtools.com/articles/2017/5/12/nonroutine-decision

Garrison, R., Noreen, E. and Brewer, P. (n.d.). Managerial accounting.

Horngren, C., Datar, S., Rajan, M., Maguire, W. and Tan, R. (n.d.). Cost

accounting.

Kagan, J. (2019). Zero-Based Budgeting (ZBB). Retrieved 23 September 2019,

from https://www.investopedia.com/terms/z/zbb.asp

Zero Based Budgeting | Meaning, Steps, Advantage, Disadvantage. (2019).

Retrieved 23 September 2019, from

https://efinancemanagement.com/budgeting/zero-based

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.