ACC00716 Finance Assignment: Time Value, Bonds, and Portfolio Analysis

VerifiedAdded on 2022/08/27

|12

|2097

|23

Homework Assignment

AI Summary

This assignment report addresses various time value of money and bond valuation questions related to a specific company, the Commonwealth Bank of Australia (CBA). The report begins with calculations of present value, revenue forecasting, effective annual rates for loan options, quarterly loan payments, and yield to maturity of bonds. It then moves on to a risk and return analysis, calculating the expected return of CBA stock and a hypothetical company using the Capital Asset Pricing Model (CAPM). A portfolio comprising the stocks of both companies is constructed, and its return and beta are calculated. The report also includes a risk assessment comparing the volatility of the CBA stock to the market index, highlighting the portfolio's diversification benefits in mitigating risk and maximizing returns. The assignment uses data sourced from S&P Capital IQ and includes a discussion of the concepts of beta and its significance in risk assessment.

Running head: CBA

CBA

Name of the Student:

Name of the University:

Author Note:

CBA

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CBA

Table of Contents

Introduction:...............................................................................................................................2

Answer to part 1:........................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................3

Part c:.....................................................................................................................................3

Part d:.....................................................................................................................................4

Part e:.....................................................................................................................................4

Part f:......................................................................................................................................5

Answer to part 2:........................................................................................................................5

Part a:.....................................................................................................................................5

Part i:..................................................................................................................................5

Part ii:.................................................................................................................................6

Part b:.....................................................................................................................................7

Answer to part 3:........................................................................................................................7

Bibliographies:.........................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Answer to part 1:........................................................................................................................2

Part a:.....................................................................................................................................2

Part b:.....................................................................................................................................3

Part c:.....................................................................................................................................3

Part d:.....................................................................................................................................4

Part e:.....................................................................................................................................4

Part f:......................................................................................................................................5

Answer to part 2:........................................................................................................................5

Part a:.....................................................................................................................................5

Part i:..................................................................................................................................5

Part ii:.................................................................................................................................6

Part b:.....................................................................................................................................7

Answer to part 3:........................................................................................................................7

Bibliographies:.........................................................................................................................10

2CBA

Introduction:

In the following report various Time value of money and bond valuation questions are

answered which had been provided in the assignment. The questions were related to the

Commonwealth Bank of Australia and the first six questions have been answered along with

the screenshot of the solved solution. In question 2, the expected return of the stock is

calculated using the capital assets pricing model and also the expected return of the

hypothetical company is calculated. A portfolio comprising of the stock of these two

companies is constructed and a risk return analysis of the stock and portfolio is conducted in

Question 3.

Answer to part 1:

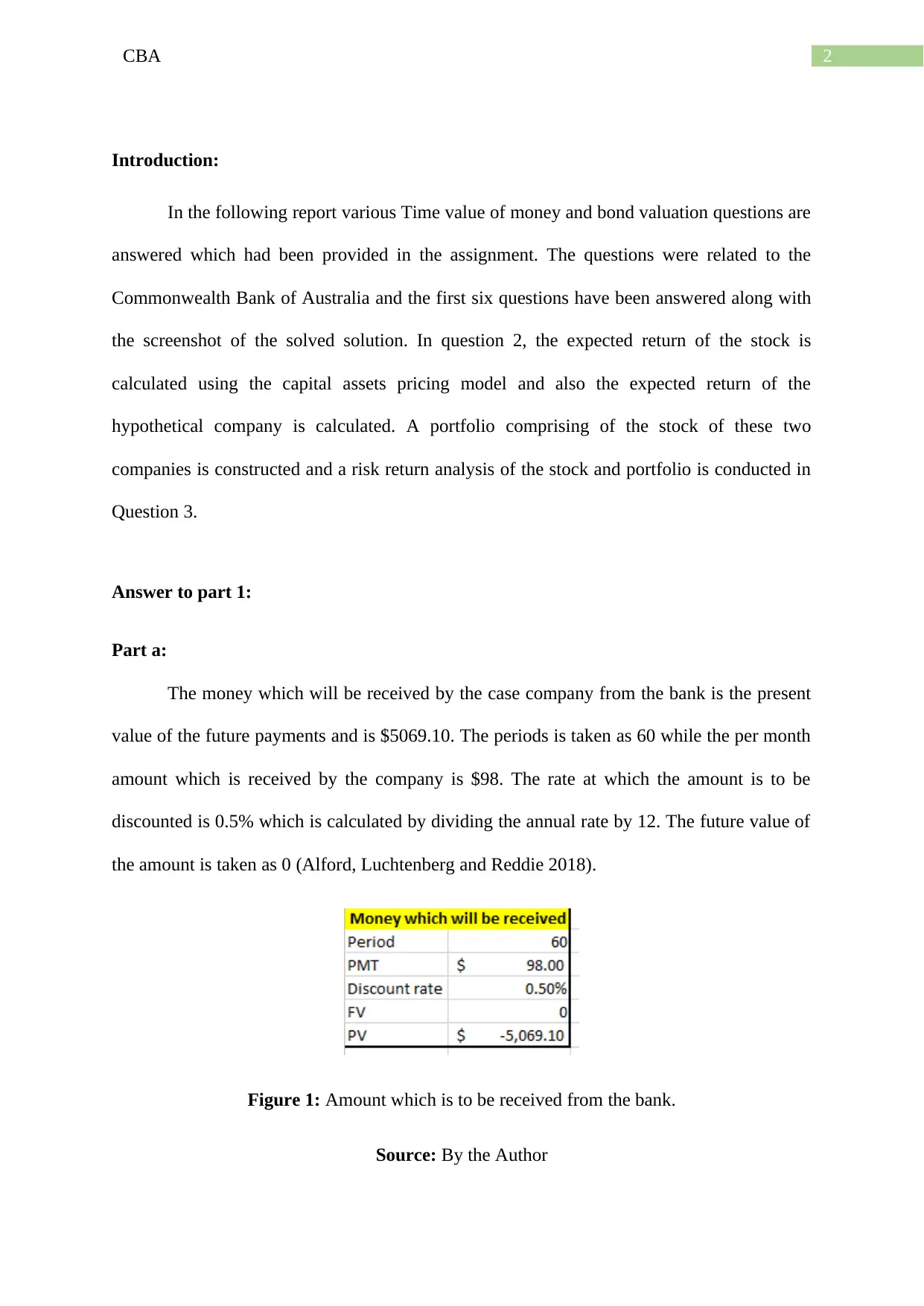

Part a:

The money which will be received by the case company from the bank is the present

value of the future payments and is $5069.10. The periods is taken as 60 while the per month

amount which is received by the company is $98. The rate at which the amount is to be

discounted is 0.5% which is calculated by dividing the annual rate by 12. The future value of

the amount is taken as 0 (Alford, Luchtenberg and Reddie 2018).

Figure 1: Amount which is to be received from the bank.

Source: By the Author

Introduction:

In the following report various Time value of money and bond valuation questions are

answered which had been provided in the assignment. The questions were related to the

Commonwealth Bank of Australia and the first six questions have been answered along with

the screenshot of the solved solution. In question 2, the expected return of the stock is

calculated using the capital assets pricing model and also the expected return of the

hypothetical company is calculated. A portfolio comprising of the stock of these two

companies is constructed and a risk return analysis of the stock and portfolio is conducted in

Question 3.

Answer to part 1:

Part a:

The money which will be received by the case company from the bank is the present

value of the future payments and is $5069.10. The periods is taken as 60 while the per month

amount which is received by the company is $98. The rate at which the amount is to be

discounted is 0.5% which is calculated by dividing the annual rate by 12. The future value of

the amount is taken as 0 (Alford, Luchtenberg and Reddie 2018).

Figure 1: Amount which is to be received from the bank.

Source: By the Author

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CBA

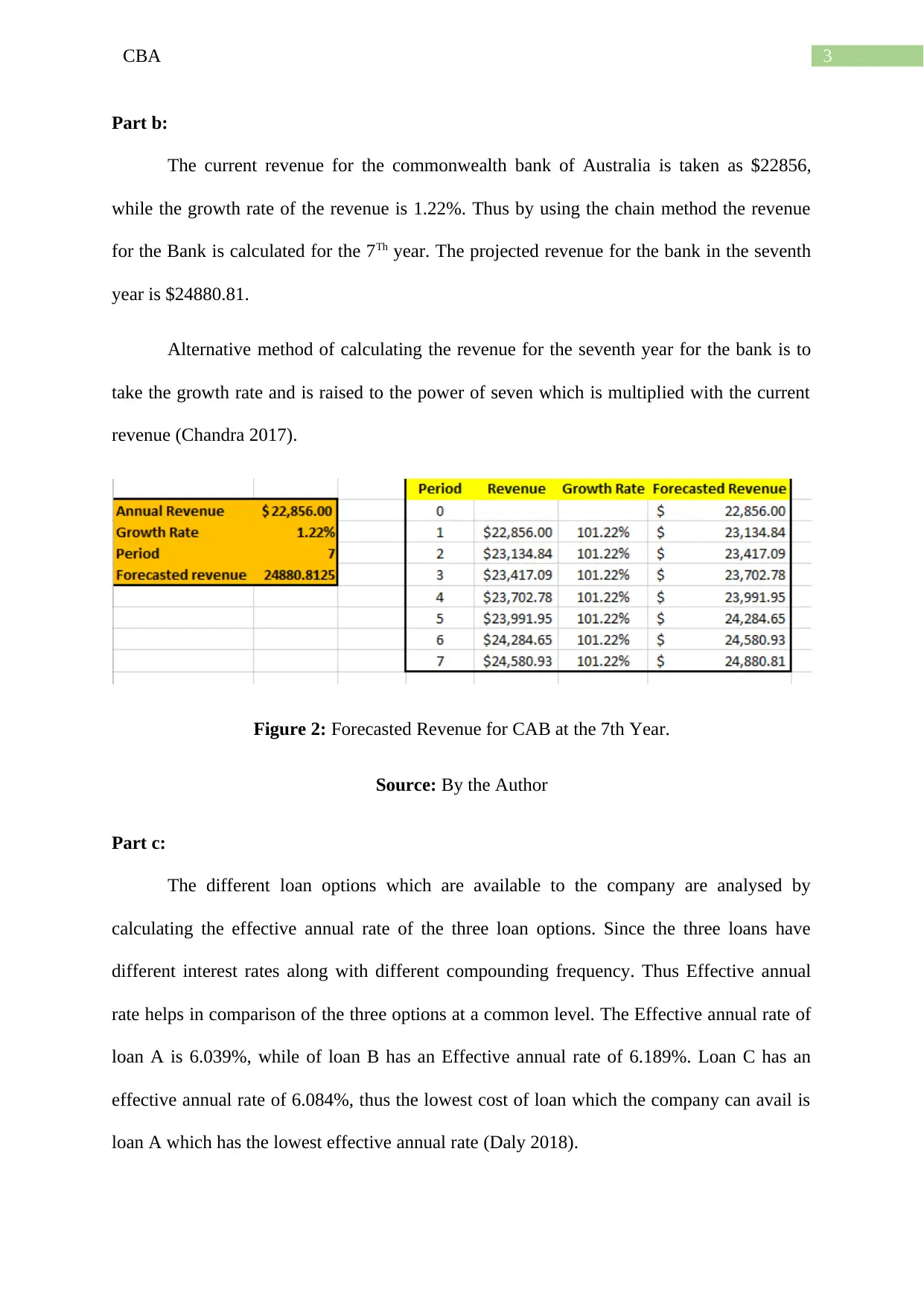

Part b:

The current revenue for the commonwealth bank of Australia is taken as $22856,

while the growth rate of the revenue is 1.22%. Thus by using the chain method the revenue

for the Bank is calculated for the 7Th year. The projected revenue for the bank in the seventh

year is $24880.81.

Alternative method of calculating the revenue for the seventh year for the bank is to

take the growth rate and is raised to the power of seven which is multiplied with the current

revenue (Chandra 2017).

Figure 2: Forecasted Revenue for CAB at the 7th Year.

Source: By the Author

Part c:

The different loan options which are available to the company are analysed by

calculating the effective annual rate of the three loan options. Since the three loans have

different interest rates along with different compounding frequency. Thus Effective annual

rate helps in comparison of the three options at a common level. The Effective annual rate of

loan A is 6.039%, while of loan B has an Effective annual rate of 6.189%. Loan C has an

effective annual rate of 6.084%, thus the lowest cost of loan which the company can avail is

loan A which has the lowest effective annual rate (Daly 2018).

Part b:

The current revenue for the commonwealth bank of Australia is taken as $22856,

while the growth rate of the revenue is 1.22%. Thus by using the chain method the revenue

for the Bank is calculated for the 7Th year. The projected revenue for the bank in the seventh

year is $24880.81.

Alternative method of calculating the revenue for the seventh year for the bank is to

take the growth rate and is raised to the power of seven which is multiplied with the current

revenue (Chandra 2017).

Figure 2: Forecasted Revenue for CAB at the 7th Year.

Source: By the Author

Part c:

The different loan options which are available to the company are analysed by

calculating the effective annual rate of the three loan options. Since the three loans have

different interest rates along with different compounding frequency. Thus Effective annual

rate helps in comparison of the three options at a common level. The Effective annual rate of

loan A is 6.039%, while of loan B has an Effective annual rate of 6.189%. Loan C has an

effective annual rate of 6.084%, thus the lowest cost of loan which the company can avail is

loan A which has the lowest effective annual rate (Daly 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CBA

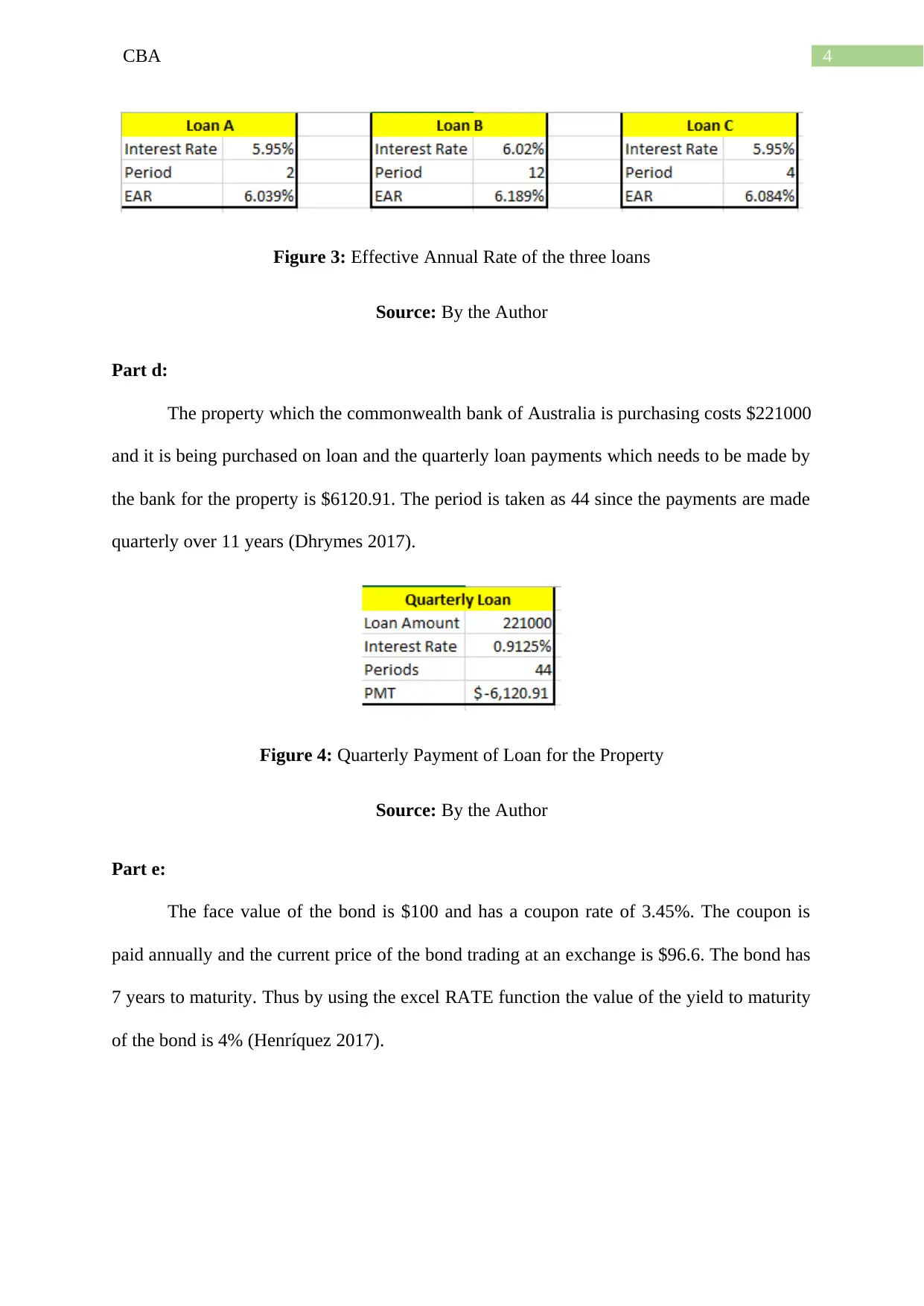

Figure 3: Effective Annual Rate of the three loans

Source: By the Author

Part d:

The property which the commonwealth bank of Australia is purchasing costs $221000

and it is being purchased on loan and the quarterly loan payments which needs to be made by

the bank for the property is $6120.91. The period is taken as 44 since the payments are made

quarterly over 11 years (Dhrymes 2017).

Figure 4: Quarterly Payment of Loan for the Property

Source: By the Author

Part e:

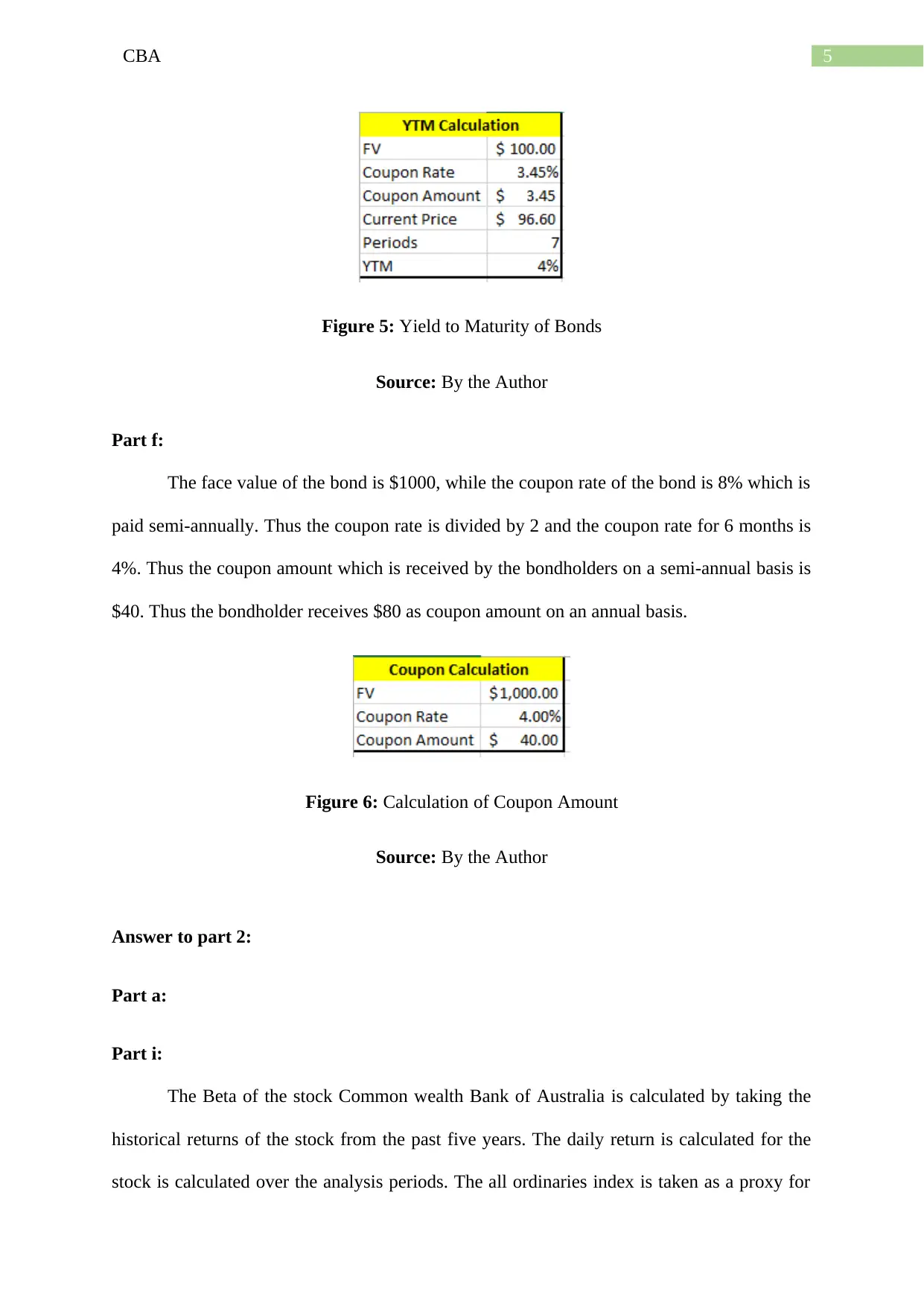

The face value of the bond is $100 and has a coupon rate of 3.45%. The coupon is

paid annually and the current price of the bond trading at an exchange is $96.6. The bond has

7 years to maturity. Thus by using the excel RATE function the value of the yield to maturity

of the bond is 4% (Henríquez 2017).

Figure 3: Effective Annual Rate of the three loans

Source: By the Author

Part d:

The property which the commonwealth bank of Australia is purchasing costs $221000

and it is being purchased on loan and the quarterly loan payments which needs to be made by

the bank for the property is $6120.91. The period is taken as 44 since the payments are made

quarterly over 11 years (Dhrymes 2017).

Figure 4: Quarterly Payment of Loan for the Property

Source: By the Author

Part e:

The face value of the bond is $100 and has a coupon rate of 3.45%. The coupon is

paid annually and the current price of the bond trading at an exchange is $96.6. The bond has

7 years to maturity. Thus by using the excel RATE function the value of the yield to maturity

of the bond is 4% (Henríquez 2017).

5CBA

Figure 5: Yield to Maturity of Bonds

Source: By the Author

Part f:

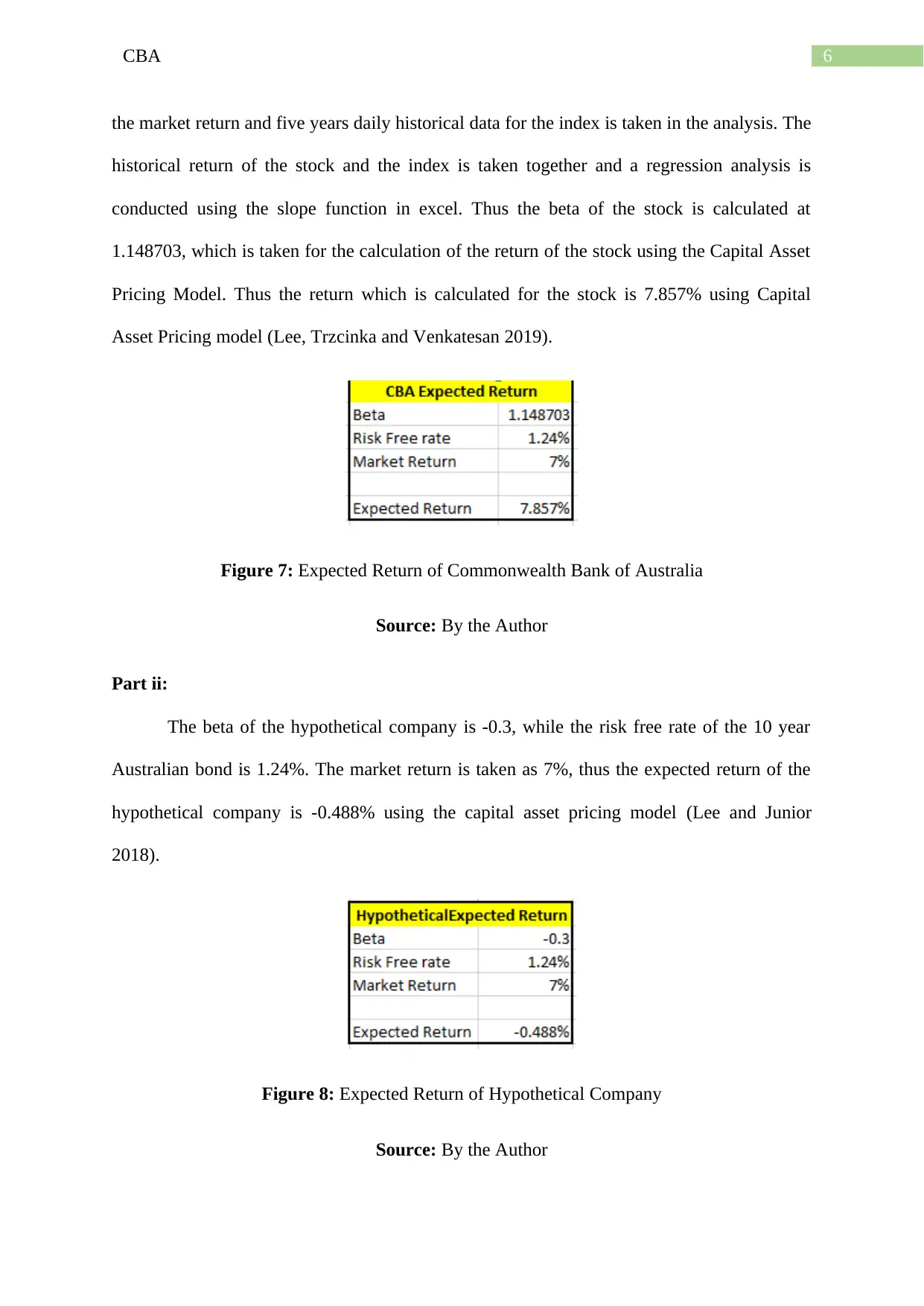

The face value of the bond is $1000, while the coupon rate of the bond is 8% which is

paid semi-annually. Thus the coupon rate is divided by 2 and the coupon rate for 6 months is

4%. Thus the coupon amount which is received by the bondholders on a semi-annual basis is

$40. Thus the bondholder receives $80 as coupon amount on an annual basis.

Figure 6: Calculation of Coupon Amount

Source: By the Author

Answer to part 2:

Part a:

Part i:

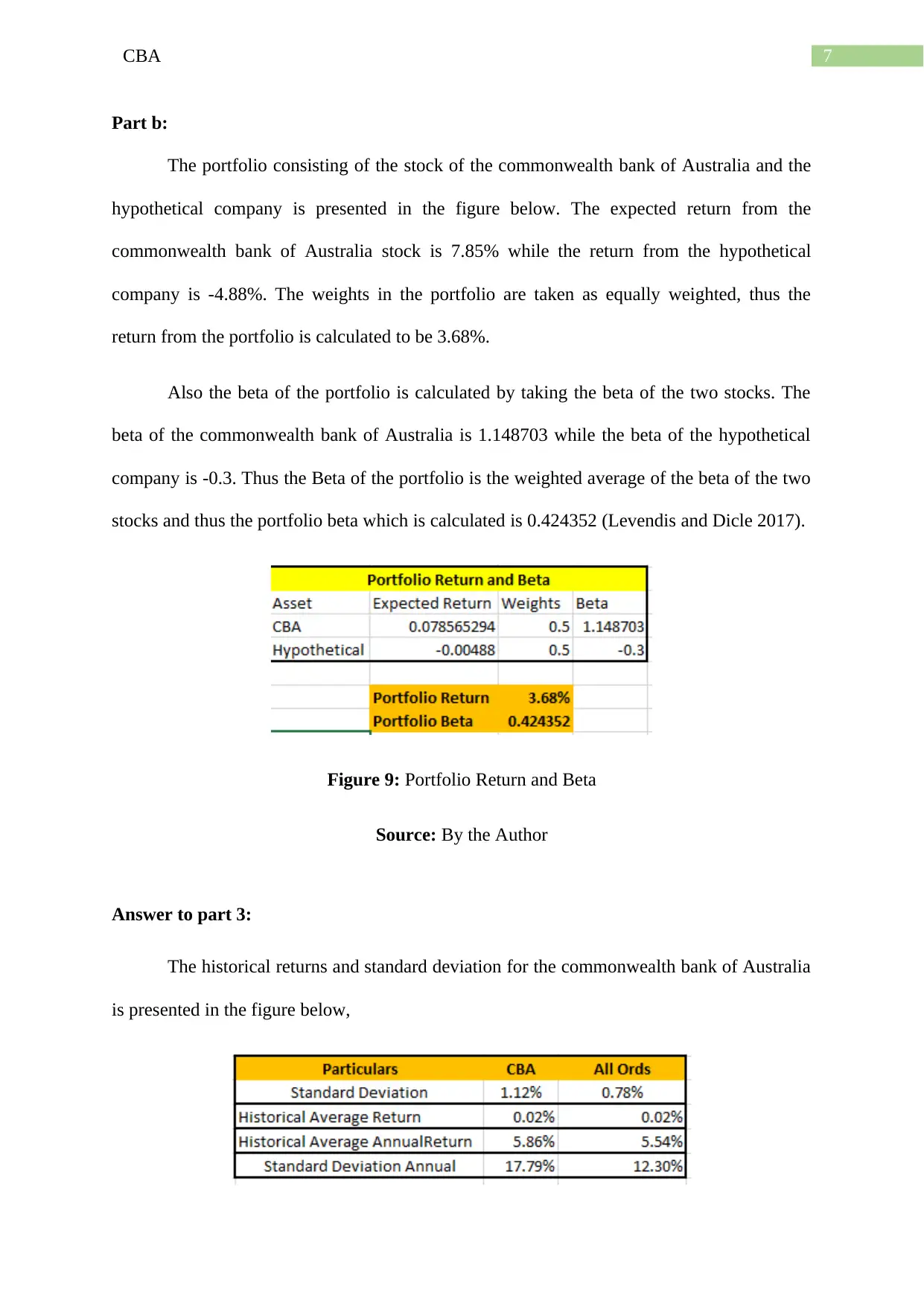

The Beta of the stock Common wealth Bank of Australia is calculated by taking the

historical returns of the stock from the past five years. The daily return is calculated for the

stock is calculated over the analysis periods. The all ordinaries index is taken as a proxy for

Figure 5: Yield to Maturity of Bonds

Source: By the Author

Part f:

The face value of the bond is $1000, while the coupon rate of the bond is 8% which is

paid semi-annually. Thus the coupon rate is divided by 2 and the coupon rate for 6 months is

4%. Thus the coupon amount which is received by the bondholders on a semi-annual basis is

$40. Thus the bondholder receives $80 as coupon amount on an annual basis.

Figure 6: Calculation of Coupon Amount

Source: By the Author

Answer to part 2:

Part a:

Part i:

The Beta of the stock Common wealth Bank of Australia is calculated by taking the

historical returns of the stock from the past five years. The daily return is calculated for the

stock is calculated over the analysis periods. The all ordinaries index is taken as a proxy for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CBA

the market return and five years daily historical data for the index is taken in the analysis. The

historical return of the stock and the index is taken together and a regression analysis is

conducted using the slope function in excel. Thus the beta of the stock is calculated at

1.148703, which is taken for the calculation of the return of the stock using the Capital Asset

Pricing Model. Thus the return which is calculated for the stock is 7.857% using Capital

Asset Pricing model (Lee, Trzcinka and Venkatesan 2019).

Figure 7: Expected Return of Commonwealth Bank of Australia

Source: By the Author

Part ii:

The beta of the hypothetical company is -0.3, while the risk free rate of the 10 year

Australian bond is 1.24%. The market return is taken as 7%, thus the expected return of the

hypothetical company is -0.488% using the capital asset pricing model (Lee and Junior

2018).

Figure 8: Expected Return of Hypothetical Company

Source: By the Author

the market return and five years daily historical data for the index is taken in the analysis. The

historical return of the stock and the index is taken together and a regression analysis is

conducted using the slope function in excel. Thus the beta of the stock is calculated at

1.148703, which is taken for the calculation of the return of the stock using the Capital Asset

Pricing Model. Thus the return which is calculated for the stock is 7.857% using Capital

Asset Pricing model (Lee, Trzcinka and Venkatesan 2019).

Figure 7: Expected Return of Commonwealth Bank of Australia

Source: By the Author

Part ii:

The beta of the hypothetical company is -0.3, while the risk free rate of the 10 year

Australian bond is 1.24%. The market return is taken as 7%, thus the expected return of the

hypothetical company is -0.488% using the capital asset pricing model (Lee and Junior

2018).

Figure 8: Expected Return of Hypothetical Company

Source: By the Author

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CBA

Part b:

The portfolio consisting of the stock of the commonwealth bank of Australia and the

hypothetical company is presented in the figure below. The expected return from the

commonwealth bank of Australia stock is 7.85% while the return from the hypothetical

company is -4.88%. The weights in the portfolio are taken as equally weighted, thus the

return from the portfolio is calculated to be 3.68%.

Also the beta of the portfolio is calculated by taking the beta of the two stocks. The

beta of the commonwealth bank of Australia is 1.148703 while the beta of the hypothetical

company is -0.3. Thus the Beta of the portfolio is the weighted average of the beta of the two

stocks and thus the portfolio beta which is calculated is 0.424352 (Levendis and Dicle 2017).

Figure 9: Portfolio Return and Beta

Source: By the Author

Answer to part 3:

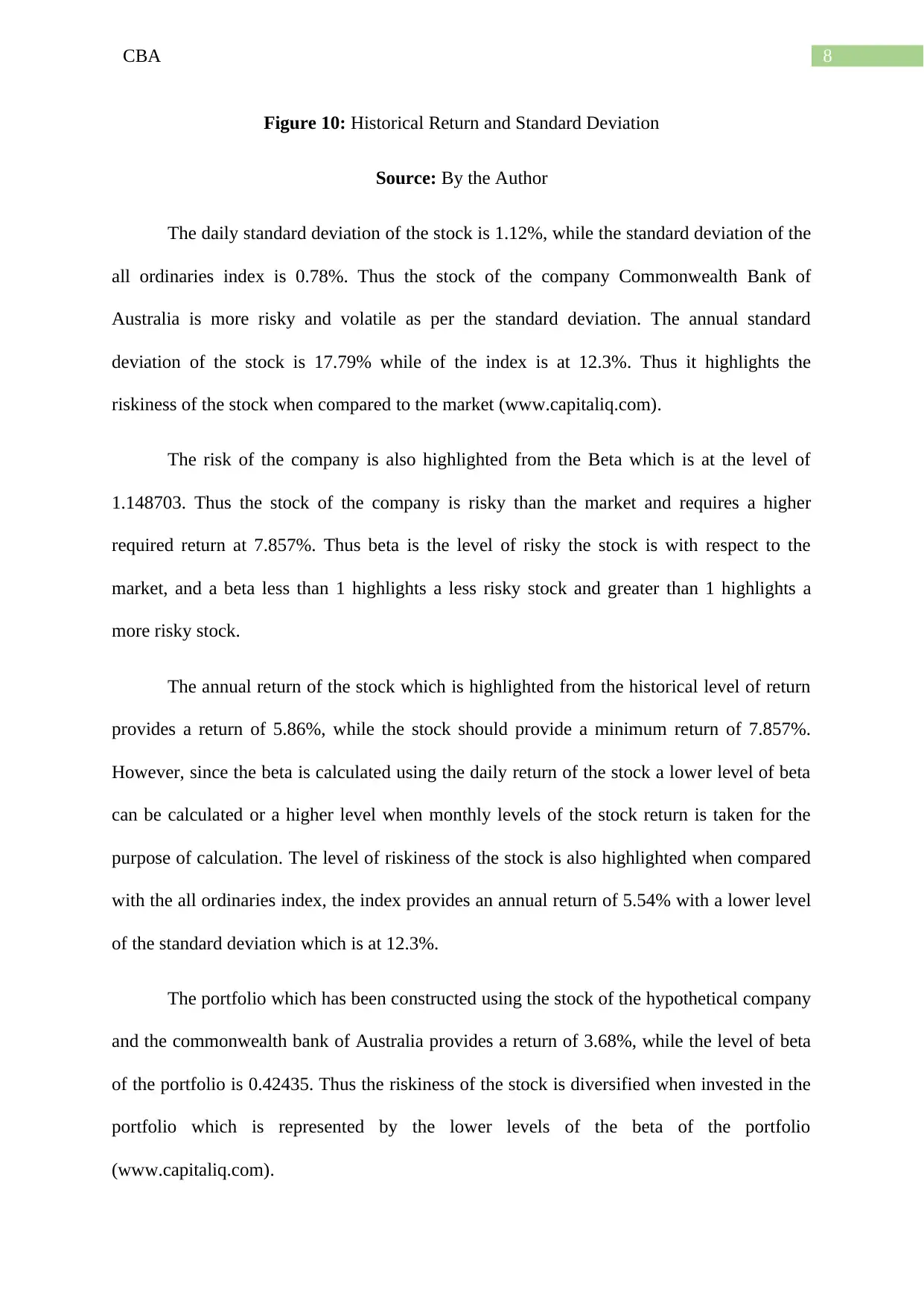

The historical returns and standard deviation for the commonwealth bank of Australia

is presented in the figure below,

Part b:

The portfolio consisting of the stock of the commonwealth bank of Australia and the

hypothetical company is presented in the figure below. The expected return from the

commonwealth bank of Australia stock is 7.85% while the return from the hypothetical

company is -4.88%. The weights in the portfolio are taken as equally weighted, thus the

return from the portfolio is calculated to be 3.68%.

Also the beta of the portfolio is calculated by taking the beta of the two stocks. The

beta of the commonwealth bank of Australia is 1.148703 while the beta of the hypothetical

company is -0.3. Thus the Beta of the portfolio is the weighted average of the beta of the two

stocks and thus the portfolio beta which is calculated is 0.424352 (Levendis and Dicle 2017).

Figure 9: Portfolio Return and Beta

Source: By the Author

Answer to part 3:

The historical returns and standard deviation for the commonwealth bank of Australia

is presented in the figure below,

8CBA

Figure 10: Historical Return and Standard Deviation

Source: By the Author

The daily standard deviation of the stock is 1.12%, while the standard deviation of the

all ordinaries index is 0.78%. Thus the stock of the company Commonwealth Bank of

Australia is more risky and volatile as per the standard deviation. The annual standard

deviation of the stock is 17.79% while of the index is at 12.3%. Thus it highlights the

riskiness of the stock when compared to the market (www.capitaliq.com).

The risk of the company is also highlighted from the Beta which is at the level of

1.148703. Thus the stock of the company is risky than the market and requires a higher

required return at 7.857%. Thus beta is the level of risky the stock is with respect to the

market, and a beta less than 1 highlights a less risky stock and greater than 1 highlights a

more risky stock.

The annual return of the stock which is highlighted from the historical level of return

provides a return of 5.86%, while the stock should provide a minimum return of 7.857%.

However, since the beta is calculated using the daily return of the stock a lower level of beta

can be calculated or a higher level when monthly levels of the stock return is taken for the

purpose of calculation. The level of riskiness of the stock is also highlighted when compared

with the all ordinaries index, the index provides an annual return of 5.54% with a lower level

of the standard deviation which is at 12.3%.

The portfolio which has been constructed using the stock of the hypothetical company

and the commonwealth bank of Australia provides a return of 3.68%, while the level of beta

of the portfolio is 0.42435. Thus the riskiness of the stock is diversified when invested in the

portfolio which is represented by the lower levels of the beta of the portfolio

(www.capitaliq.com).

Figure 10: Historical Return and Standard Deviation

Source: By the Author

The daily standard deviation of the stock is 1.12%, while the standard deviation of the

all ordinaries index is 0.78%. Thus the stock of the company Commonwealth Bank of

Australia is more risky and volatile as per the standard deviation. The annual standard

deviation of the stock is 17.79% while of the index is at 12.3%. Thus it highlights the

riskiness of the stock when compared to the market (www.capitaliq.com).

The risk of the company is also highlighted from the Beta which is at the level of

1.148703. Thus the stock of the company is risky than the market and requires a higher

required return at 7.857%. Thus beta is the level of risky the stock is with respect to the

market, and a beta less than 1 highlights a less risky stock and greater than 1 highlights a

more risky stock.

The annual return of the stock which is highlighted from the historical level of return

provides a return of 5.86%, while the stock should provide a minimum return of 7.857%.

However, since the beta is calculated using the daily return of the stock a lower level of beta

can be calculated or a higher level when monthly levels of the stock return is taken for the

purpose of calculation. The level of riskiness of the stock is also highlighted when compared

with the all ordinaries index, the index provides an annual return of 5.54% with a lower level

of the standard deviation which is at 12.3%.

The portfolio which has been constructed using the stock of the hypothetical company

and the commonwealth bank of Australia provides a return of 3.68%, while the level of beta

of the portfolio is 0.42435. Thus the riskiness of the stock is diversified when invested in the

portfolio which is represented by the lower levels of the beta of the portfolio

(www.capitaliq.com).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CBA

Thus as per the benefits of diversification of a portfolio, a portfolio tends to reduce

risk while maximising the return to the investor. Thus if an investor would have invested all

his funds in the commonwealth bank of Australia stock, it would had generated a higher

return but at a high level of risk, which is seen by the high beta. Also if an investor would

have invested all their funds in the hypothetical company the return would had been negative

even when the risk which is denoted by beta is negative. Thus when the investor had invested

their funds in a portfolio comprising of these two assets, it led to reduction in risk, which is

seen by the portfolio beta. Thus the return which is generated by the portfolio is the

maximized return at the lowest level of risk (Shrivastav 2017).

Thus as per the benefits of diversification of a portfolio, a portfolio tends to reduce

risk while maximising the return to the investor. Thus if an investor would have invested all

his funds in the commonwealth bank of Australia stock, it would had generated a higher

return but at a high level of risk, which is seen by the high beta. Also if an investor would

have invested all their funds in the hypothetical company the return would had been negative

even when the risk which is denoted by beta is negative. Thus when the investor had invested

their funds in a portfolio comprising of these two assets, it led to reduction in risk, which is

seen by the portfolio beta. Thus the return which is generated by the portfolio is the

maximized return at the lowest level of risk (Shrivastav 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CBA

References:

Alford, R.M., Luchtenberg, K.F. and Reddie, W.D., 2018. Portfolio Management and

Earnings Management: Evidence from Property and Casualty Insurers. Journal of Accounting

& Finance (2158-3625), 18(4).

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Daly, M., 2018. Feasible portfolios under tracking error, β, α and utility

constraints. Investment Management & Financial Innovations, 15(1), p.141.

Dhrymes, P.J., 2017. Portfolio theory: origins, Markowitz and CAPM based selection.

In Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Henríquez, R., Wenzel, G., Olivares, D.E. and Negrete-Pincetic, M., 2017. Participation of

demand response aggregators in electricity markets: Optimal portfolio management. IEEE

Transactions on Smart Grid, 9(5), pp.4861-4871.

Lee, J.H., Trzcinka, C. and Venkatesan, S., 2019. Do Portfolio Manager Contracts Contract

Portfolio Management?. The Journal of Finance.

Lee, S.C. and Eid Junior, W., 2018. Portfolio construction and risk management: theory

versus practice. RAUSP Management Journal, 53(3), pp.345-365.

Levendis, J. and Dicle, M.F., 2017. Calculating a Portfolio's Beta. Journal of Economics and

Finance Education, Forthcoming.

Log In | S&P Capital IQ (2020). Available at:

https://www.capitaliq.com/CIQDotNet/MacroEconomics/InterestRate.aspx?

companyId=50027527 (Accessed: 9 January 2020).

References:

Alford, R.M., Luchtenberg, K.F. and Reddie, W.D., 2018. Portfolio Management and

Earnings Management: Evidence from Property and Casualty Insurers. Journal of Accounting

& Finance (2158-3625), 18(4).

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Daly, M., 2018. Feasible portfolios under tracking error, β, α and utility

constraints. Investment Management & Financial Innovations, 15(1), p.141.

Dhrymes, P.J., 2017. Portfolio theory: origins, Markowitz and CAPM based selection.

In Portfolio Construction, Measurement, and Efficiency (pp. 39-48). Springer, Cham.

Henríquez, R., Wenzel, G., Olivares, D.E. and Negrete-Pincetic, M., 2017. Participation of

demand response aggregators in electricity markets: Optimal portfolio management. IEEE

Transactions on Smart Grid, 9(5), pp.4861-4871.

Lee, J.H., Trzcinka, C. and Venkatesan, S., 2019. Do Portfolio Manager Contracts Contract

Portfolio Management?. The Journal of Finance.

Lee, S.C. and Eid Junior, W., 2018. Portfolio construction and risk management: theory

versus practice. RAUSP Management Journal, 53(3), pp.345-365.

Levendis, J. and Dicle, M.F., 2017. Calculating a Portfolio's Beta. Journal of Economics and

Finance Education, Forthcoming.

Log In | S&P Capital IQ (2020). Available at:

https://www.capitaliq.com/CIQDotNet/MacroEconomics/InterestRate.aspx?

companyId=50027527 (Accessed: 9 January 2020).

11CBA

Log In | S&P Capital IQ (2020). Available at:

https://www.capitaliq.com/CIQDotNet/MacroEconomics/InterestRate.aspx?

companyId=50027527 (Accessed: 9 January 2020).

Shrivastav, S.M., 2017. CAPM: EMPIRICAL EVIDENCE FROM INDIA. International

Journal Of Core Engineering & Management, 3(10).

Log In | S&P Capital IQ (2020). Available at:

https://www.capitaliq.com/CIQDotNet/MacroEconomics/InterestRate.aspx?

companyId=50027527 (Accessed: 9 January 2020).

Shrivastav, S.M., 2017. CAPM: EMPIRICAL EVIDENCE FROM INDIA. International

Journal Of Core Engineering & Management, 3(10).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.