ACC00716 Finance Assignment 2: TVM, Risk and Return Analysis for Boral

VerifiedAdded on 2023/01/23

|15

|2509

|86

Homework Assignment

AI Summary

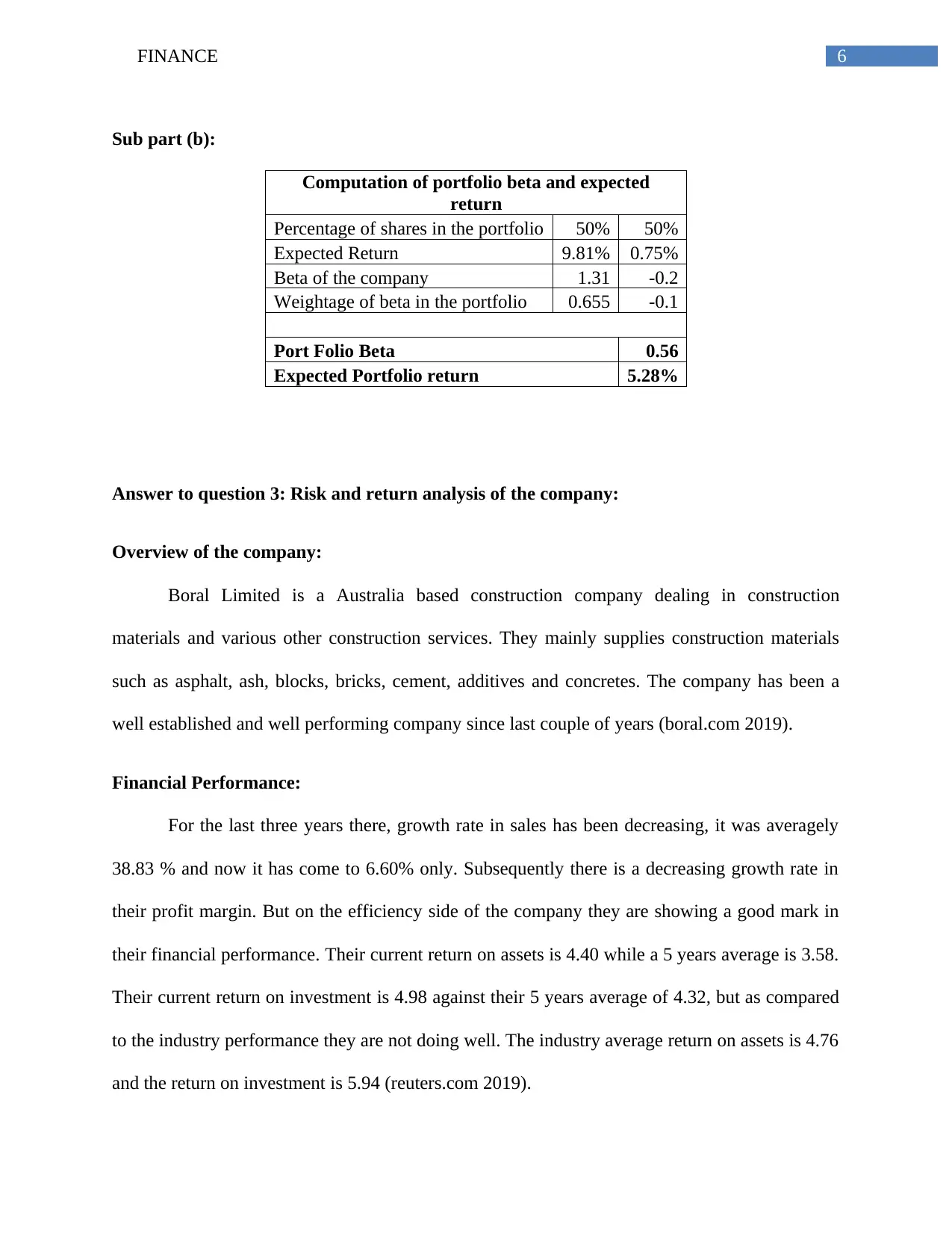

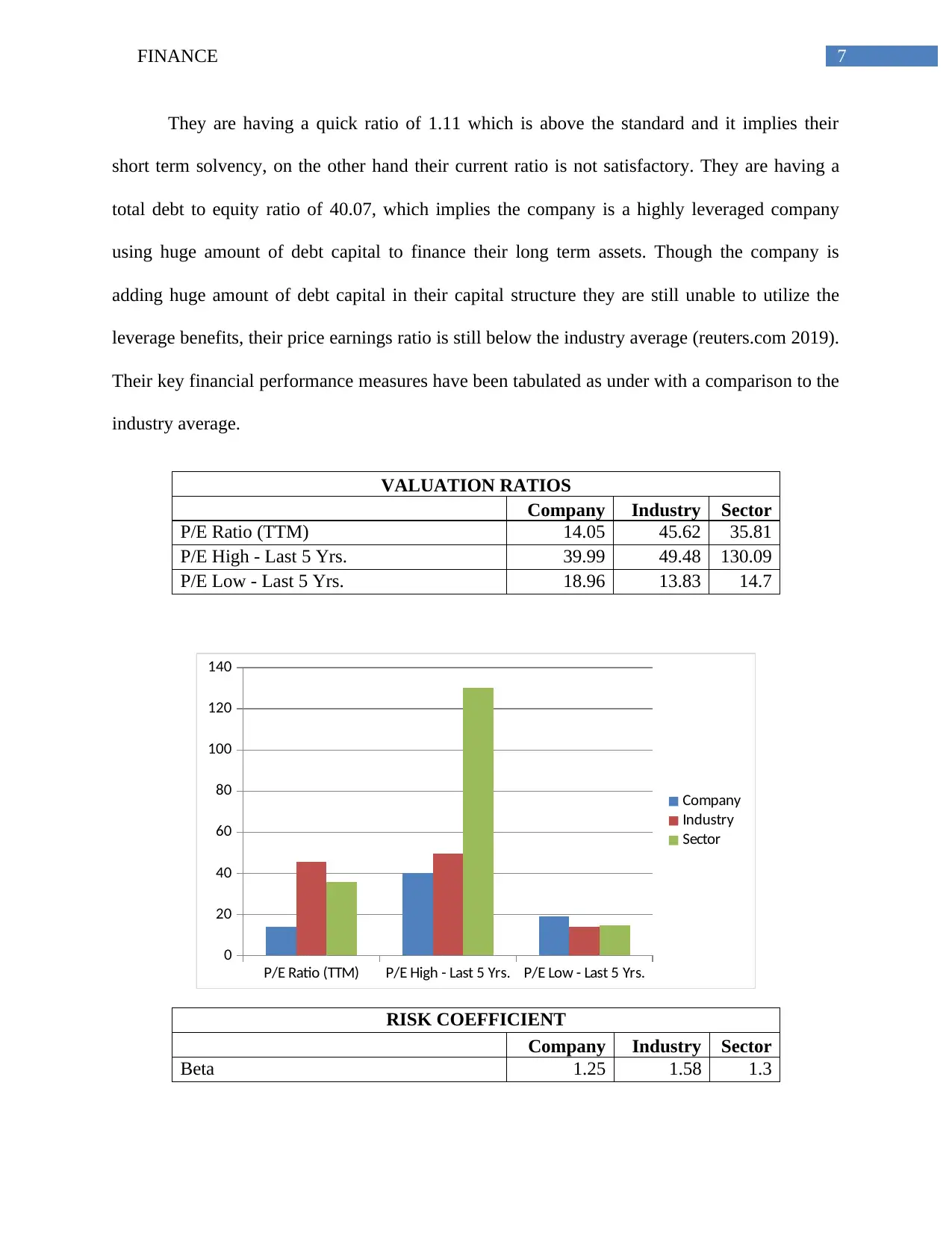

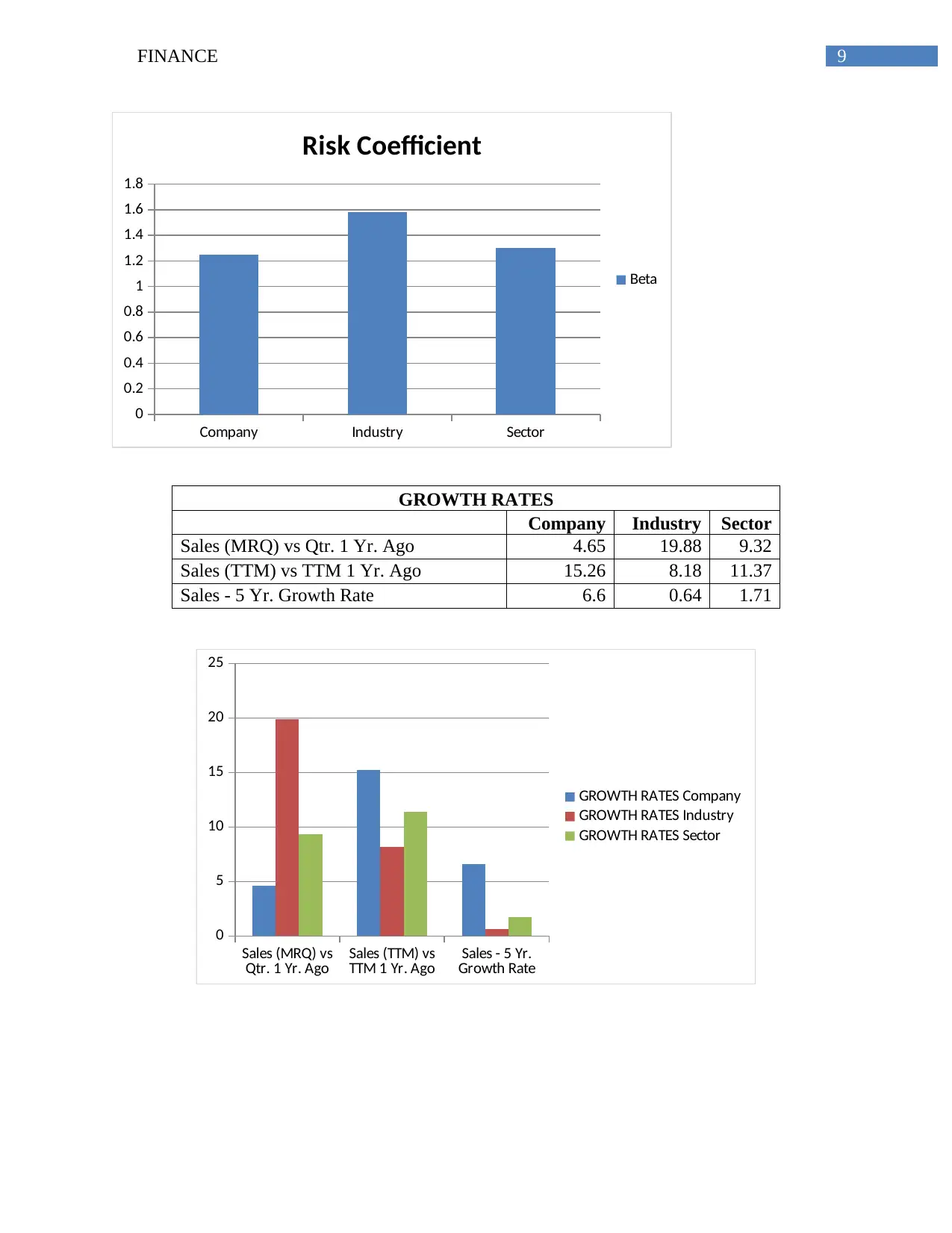

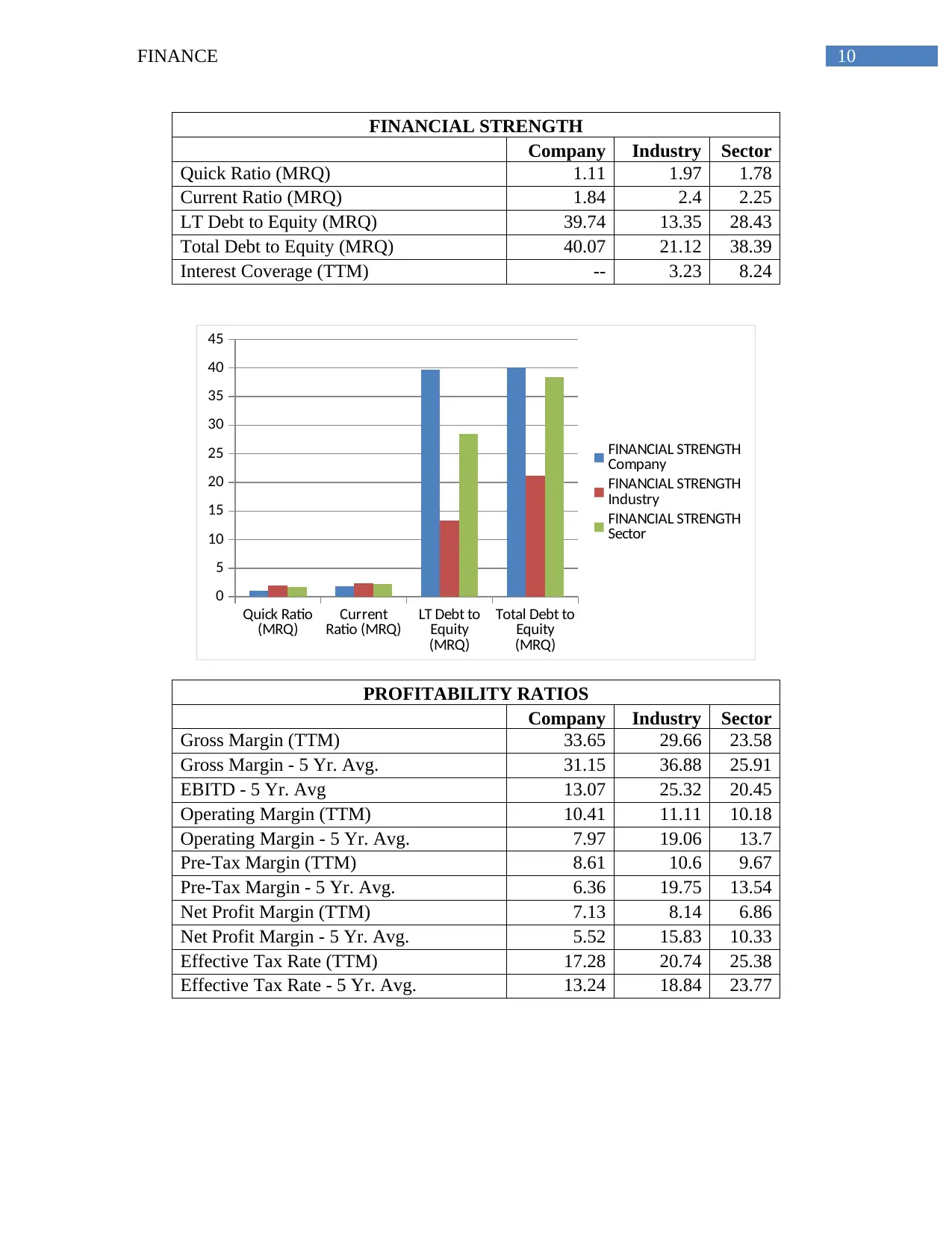

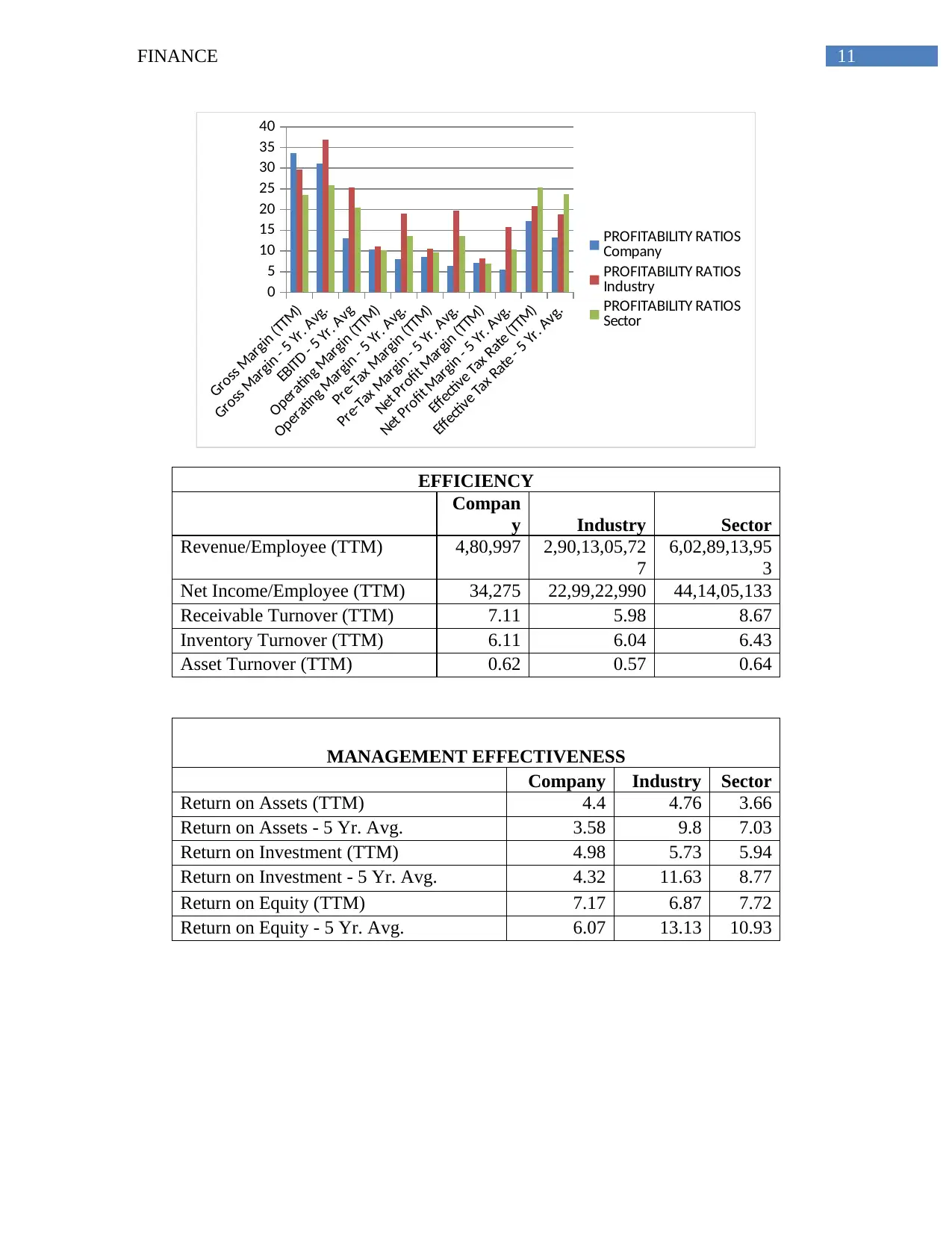

This finance assignment, completed for ACC00716, assesses the student's understanding of key financial concepts. The assignment is divided into three parts. Part 1 focuses on time value of money (TVM) and bond valuation, including calculations of discounted values, expected revenue, effective interest rates, installment amounts, and yield to maturity. Part 2 involves risk and return estimates, specifically using the Capital Asset Pricing Model (CAPM) to determine expected returns and portfolio beta. Part 3 provides a risk and return analysis of Boral Limited, an ASX-listed construction company. This section includes an overview of the company, its financial performance, and an evaluation of risk and return measures, leading to a conclusion and recommendations for the company's financial strategy. The assignment requires the use of S&P Capital IQ for data and analysis.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.