University Finance Assignment: Solutions to Questions 1, 2 and 3

VerifiedAdded on 2023/01/19

|13

|2257

|82

Homework Assignment

AI Summary

This document presents a comprehensive solution to a finance assignment, addressing three key questions. Question 1 delves into financial mathematics, calculating monthly deposits for a future holiday, and evaluating a mining business investment using net present value analysis. Question 2 explores the concepts of real interest rates and negative gearing in taxation. Question 3 focuses on risk and return in investments, including the Australian dividend imputation credit system, and analyzing stock performance, calculating annualized returns for both Australian and non-Australian shareholders. The analysis includes calculations of market and BHP stock returns, beta, and expected returns, incorporating graphical representations and portfolio analysis.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND FINANCE

Table of Contents

Answer to question 1:.................................................................................................................2

Sub part (a):............................................................................................................................2

Sub part (b)-i:.........................................................................................................................2

Sub part (b)-ii:........................................................................................................................2

Sub part (c)-i:.........................................................................................................................3

Sub part (c)-ii:........................................................................................................................3

Answer to question 2:.................................................................................................................4

Sub part (i):............................................................................................................................4

Sub part (ii):...........................................................................................................................4

Answer to question 3:.................................................................................................................5

Sub part (i):............................................................................................................................5

Sub part (ii):...........................................................................................................................5

Sub part (iii) and (iv):.............................................................................................................6

Sub part (v):............................................................................................................................6

Sub part (vi):..........................................................................................................................7

Sub part (vii), (viii) & (ix):....................................................................................................7

Sub part (x):............................................................................................................................8

Sub part (xi):..........................................................................................................................8

Sub part (xii):.........................................................................................................................9

Sub part (xiii):........................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Sub part (a):............................................................................................................................2

Sub part (b)-i:.........................................................................................................................2

Sub part (b)-ii:........................................................................................................................2

Sub part (c)-i:.........................................................................................................................3

Sub part (c)-ii:........................................................................................................................3

Answer to question 2:.................................................................................................................4

Sub part (i):............................................................................................................................4

Sub part (ii):...........................................................................................................................4

Answer to question 3:.................................................................................................................5

Sub part (i):............................................................................................................................5

Sub part (ii):...........................................................................................................................5

Sub part (iii) and (iv):.............................................................................................................6

Sub part (v):............................................................................................................................6

Sub part (vi):..........................................................................................................................7

Sub part (vii), (viii) & (ix):....................................................................................................7

Sub part (x):............................................................................................................................8

Sub part (xi):..........................................................................................................................8

Sub part (xii):.........................................................................................................................9

Sub part (xiii):........................................................................................................................9

2ACCOUNTING AND FINANCE

Sub part (xiv):........................................................................................................................9

Sub part (xv):........................................................................................................................10

Sub part (xvi):......................................................................................................................10

References and bibliography:...................................................................................................11

Sub part (xiv):........................................................................................................................9

Sub part (xv):........................................................................................................................10

Sub part (xvi):......................................................................................................................10

References and bibliography:...................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND FINANCE

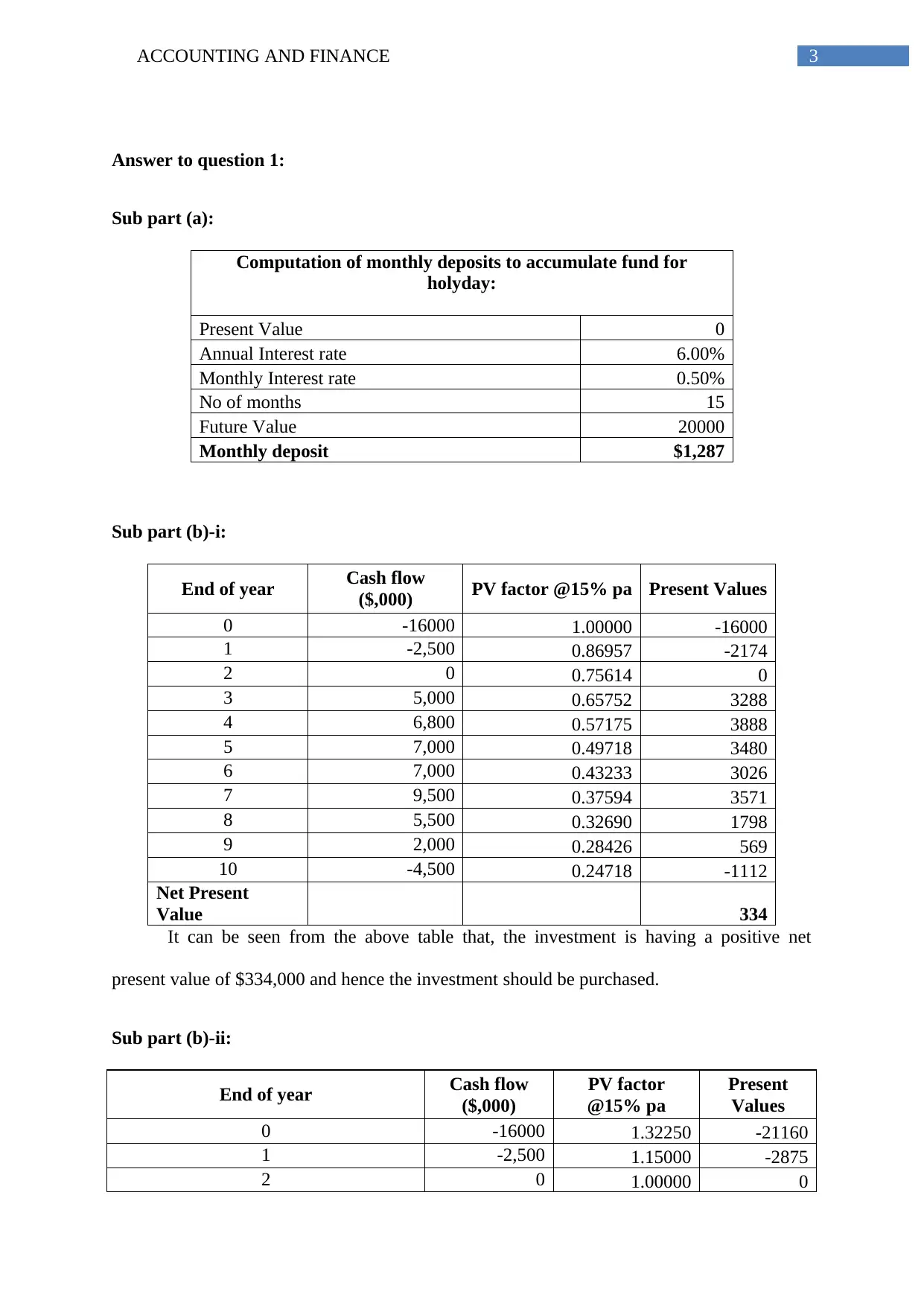

Answer to question 1:

Sub part (a):

Computation of monthly deposits to accumulate fund for

holyday:

Present Value 0

Annual Interest rate 6.00%

Monthly Interest rate 0.50%

No of months 15

Future Value 20000

Monthly deposit $1,287

Sub part (b)-i:

End of year Cash flow

($,000) PV factor @15% pa Present Values

0 -16000 1.00000 -16000

1 -2,500 0.86957 -2174

2 0 0.75614 0

3 5,000 0.65752 3288

4 6,800 0.57175 3888

5 7,000 0.49718 3480

6 7,000 0.43233 3026

7 9,500 0.37594 3571

8 5,500 0.32690 1798

9 2,000 0.28426 569

10 -4,500 0.24718 -1112

Net Present

Value 334

It can be seen from the above table that, the investment is having a positive net

present value of $334,000 and hence the investment should be purchased.

Sub part (b)-ii:

End of year Cash flow

($,000)

PV factor

@15% pa

Present

Values

0 -16000 1.32250 -21160

1 -2,500 1.15000 -2875

2 0 1.00000 0

Answer to question 1:

Sub part (a):

Computation of monthly deposits to accumulate fund for

holyday:

Present Value 0

Annual Interest rate 6.00%

Monthly Interest rate 0.50%

No of months 15

Future Value 20000

Monthly deposit $1,287

Sub part (b)-i:

End of year Cash flow

($,000) PV factor @15% pa Present Values

0 -16000 1.00000 -16000

1 -2,500 0.86957 -2174

2 0 0.75614 0

3 5,000 0.65752 3288

4 6,800 0.57175 3888

5 7,000 0.49718 3480

6 7,000 0.43233 3026

7 9,500 0.37594 3571

8 5,500 0.32690 1798

9 2,000 0.28426 569

10 -4,500 0.24718 -1112

Net Present

Value 334

It can be seen from the above table that, the investment is having a positive net

present value of $334,000 and hence the investment should be purchased.

Sub part (b)-ii:

End of year Cash flow

($,000)

PV factor

@15% pa

Present

Values

0 -16000 1.32250 -21160

1 -2,500 1.15000 -2875

2 0 1.00000 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND FINANCE

3 5,000 0.86957 4348

4 6,800 0.75614 5142

5 7,000 0.65752 4603

6 7,000 0.57175 4002

7 9,500 0.49718 4723

8 5,500 0.43233 2378

9 2,000 0.37594 752

10 -4,500 0.32690 -1471

Net Present Value at the end of year

2 441

Sub part (c)-i:

Computation of value of financial assets at the age of 60 years:

Current Age 45 years

Age to retirement 60 years

Number of years in between 15 years

Pension till the age of 90 years

Total Pension period 30 years

Interest rate on investment in pension period 3%

Present Value of portfolio $ 1,25,000

Interest rate on the portfolio 6%

Balance in superannuation account $ 7,50,000

Contribution per month $ 1,000

Interest rate on the superannuation fund 8%

Future value of superannuation at the age 60 $ 28,26,229

Future value of the portfolio at the age 60 $ 3,06,762

Total value of financial assets at the age of

60 $ 31,32,991

Sub part (c)-ii:

Computation of Monthly pension amount:

Current Age 45 years

Age to retirement 60 years

Number of years in between 15 years

Pension till the age of 90 years

Total Pension period 30 years

Interest rate on investment in pension period 3%

Present Value of portfolio $

3 5,000 0.86957 4348

4 6,800 0.75614 5142

5 7,000 0.65752 4603

6 7,000 0.57175 4002

7 9,500 0.49718 4723

8 5,500 0.43233 2378

9 2,000 0.37594 752

10 -4,500 0.32690 -1471

Net Present Value at the end of year

2 441

Sub part (c)-i:

Computation of value of financial assets at the age of 60 years:

Current Age 45 years

Age to retirement 60 years

Number of years in between 15 years

Pension till the age of 90 years

Total Pension period 30 years

Interest rate on investment in pension period 3%

Present Value of portfolio $ 1,25,000

Interest rate on the portfolio 6%

Balance in superannuation account $ 7,50,000

Contribution per month $ 1,000

Interest rate on the superannuation fund 8%

Future value of superannuation at the age 60 $ 28,26,229

Future value of the portfolio at the age 60 $ 3,06,762

Total value of financial assets at the age of

60 $ 31,32,991

Sub part (c)-ii:

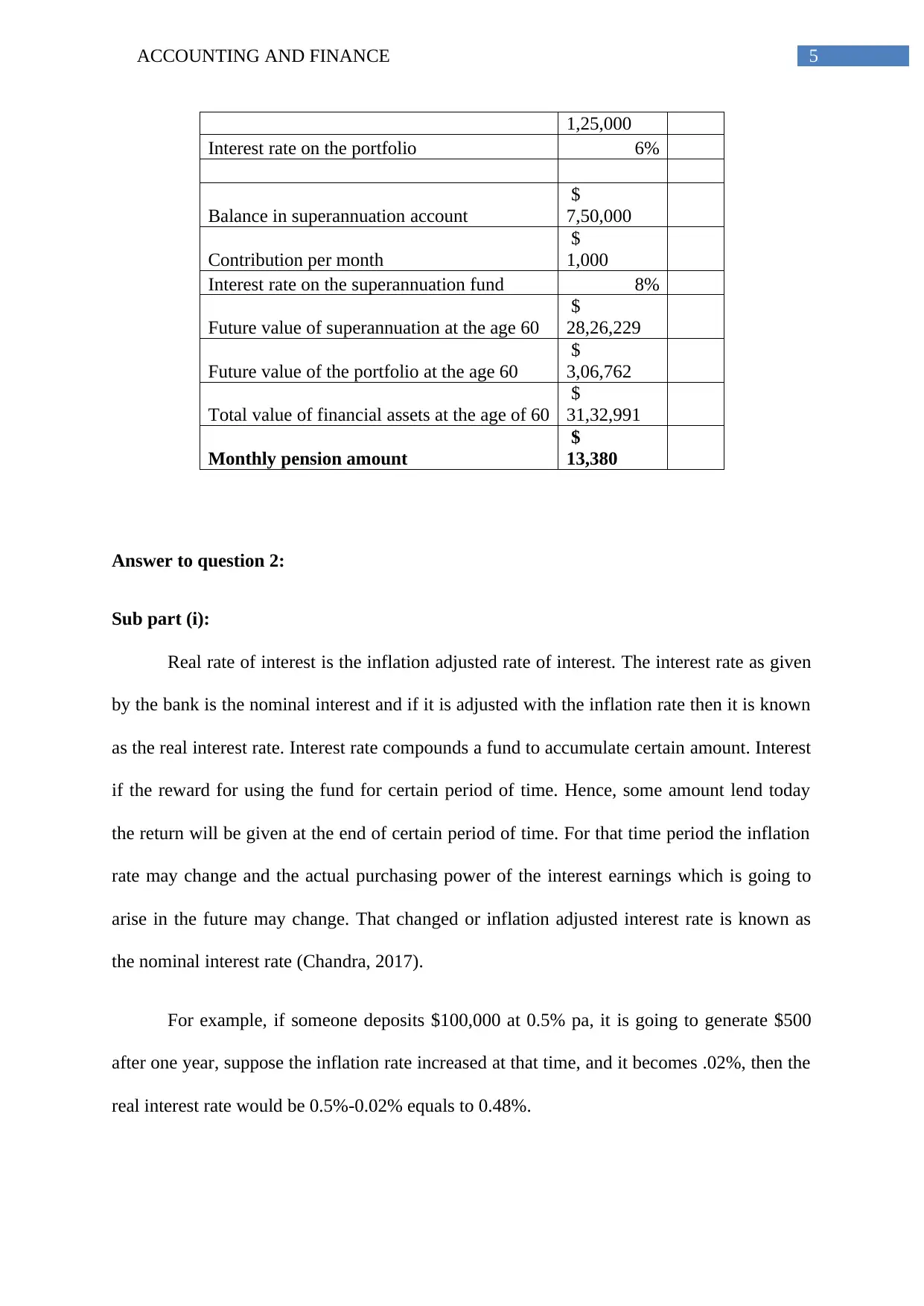

Computation of Monthly pension amount:

Current Age 45 years

Age to retirement 60 years

Number of years in between 15 years

Pension till the age of 90 years

Total Pension period 30 years

Interest rate on investment in pension period 3%

Present Value of portfolio $

5ACCOUNTING AND FINANCE

1,25,000

Interest rate on the portfolio 6%

Balance in superannuation account

$

7,50,000

Contribution per month

$

1,000

Interest rate on the superannuation fund 8%

Future value of superannuation at the age 60

$

28,26,229

Future value of the portfolio at the age 60

$

3,06,762

Total value of financial assets at the age of 60

$

31,32,991

Monthly pension amount

$

13,380

Answer to question 2:

Sub part (i):

Real rate of interest is the inflation adjusted rate of interest. The interest rate as given

by the bank is the nominal interest and if it is adjusted with the inflation rate then it is known

as the real interest rate. Interest rate compounds a fund to accumulate certain amount. Interest

if the reward for using the fund for certain period of time. Hence, some amount lend today

the return will be given at the end of certain period of time. For that time period the inflation

rate may change and the actual purchasing power of the interest earnings which is going to

arise in the future may change. That changed or inflation adjusted interest rate is known as

the nominal interest rate (Chandra, 2017).

For example, if someone deposits $100,000 at 0.5% pa, it is going to generate $500

after one year, suppose the inflation rate increased at that time, and it becomes .02%, then the

real interest rate would be 0.5%-0.02% equals to 0.48%.

1,25,000

Interest rate on the portfolio 6%

Balance in superannuation account

$

7,50,000

Contribution per month

$

1,000

Interest rate on the superannuation fund 8%

Future value of superannuation at the age 60

$

28,26,229

Future value of the portfolio at the age 60

$

3,06,762

Total value of financial assets at the age of 60

$

31,32,991

Monthly pension amount

$

13,380

Answer to question 2:

Sub part (i):

Real rate of interest is the inflation adjusted rate of interest. The interest rate as given

by the bank is the nominal interest and if it is adjusted with the inflation rate then it is known

as the real interest rate. Interest rate compounds a fund to accumulate certain amount. Interest

if the reward for using the fund for certain period of time. Hence, some amount lend today

the return will be given at the end of certain period of time. For that time period the inflation

rate may change and the actual purchasing power of the interest earnings which is going to

arise in the future may change. That changed or inflation adjusted interest rate is known as

the nominal interest rate (Chandra, 2017).

For example, if someone deposits $100,000 at 0.5% pa, it is going to generate $500

after one year, suppose the inflation rate increased at that time, and it becomes .02%, then the

real interest rate would be 0.5%-0.02% equals to 0.48%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND FINANCE

Sub part (ii):

Negative gearing in the taxation perspective means taking advantage of some undue

and inflated expenditure to get the tax burden reduced. It happen in the property dealings

mainly. Wealthy persons buys house and gives it in rent, and inflates the price and

expenditure of the house to get tax relief. They block their fund in the property and shows

high expenses on that property and a minimal rental income from the property thereby

showing a net loss. It in turn reduces the tax burden.

Practice of allowing a negative gearing will not be good for the Australian economy

as it affects the revenue generation of the Australian government and thereby reducing the

economical and social welfare of the economy as a whole.

Answer to question 3:

Sub part (i):

Risk means the uncertainty of getting anything. In terms of investment risk means the

uncertainty of getting adequate amount of return in time. It is the market fluctuation or the

slope which determines the future return from any investment. Risk can again be classified

into systematic and unsystematic risks. Risk in any investment can be eliminated to some

extent through diversification. There is a straight line relationship between risk and return, as

much as risk is assumed the return will be as higher. Hence, risk is not always bad, but

assuming high degree of risk can give higher return but on the other hand it may lose the

whole capital fund (Chandra, 2017).

Sub part (ii):

Australian Dividend imputation credit system is the process of relieving the double

taxation burden on dividend income to the shareholders. As the dividends are taxed at the

Sub part (ii):

Negative gearing in the taxation perspective means taking advantage of some undue

and inflated expenditure to get the tax burden reduced. It happen in the property dealings

mainly. Wealthy persons buys house and gives it in rent, and inflates the price and

expenditure of the house to get tax relief. They block their fund in the property and shows

high expenses on that property and a minimal rental income from the property thereby

showing a net loss. It in turn reduces the tax burden.

Practice of allowing a negative gearing will not be good for the Australian economy

as it affects the revenue generation of the Australian government and thereby reducing the

economical and social welfare of the economy as a whole.

Answer to question 3:

Sub part (i):

Risk means the uncertainty of getting anything. In terms of investment risk means the

uncertainty of getting adequate amount of return in time. It is the market fluctuation or the

slope which determines the future return from any investment. Risk can again be classified

into systematic and unsystematic risks. Risk in any investment can be eliminated to some

extent through diversification. There is a straight line relationship between risk and return, as

much as risk is assumed the return will be as higher. Hence, risk is not always bad, but

assuming high degree of risk can give higher return but on the other hand it may lose the

whole capital fund (Chandra, 2017).

Sub part (ii):

Australian Dividend imputation credit system is the process of relieving the double

taxation burden on dividend income to the shareholders. As the dividends are taxed at the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND FINANCE

corporate level when the profit is earned or the dividend is distributed, it should not be taxed

again in the hands of the share holders. To make it happen the Australian government

implemented a system to give the tax credit to the receiver of the dividend while they are

filing income tax return annually. This system is known as the franking, it may be 100%

franking or it may be partial franking. If there is a double taxation avoidance agreement with

the other country with Australia, then the same credit is given to the person who is a foreigner

and earning dividend from Australian company.

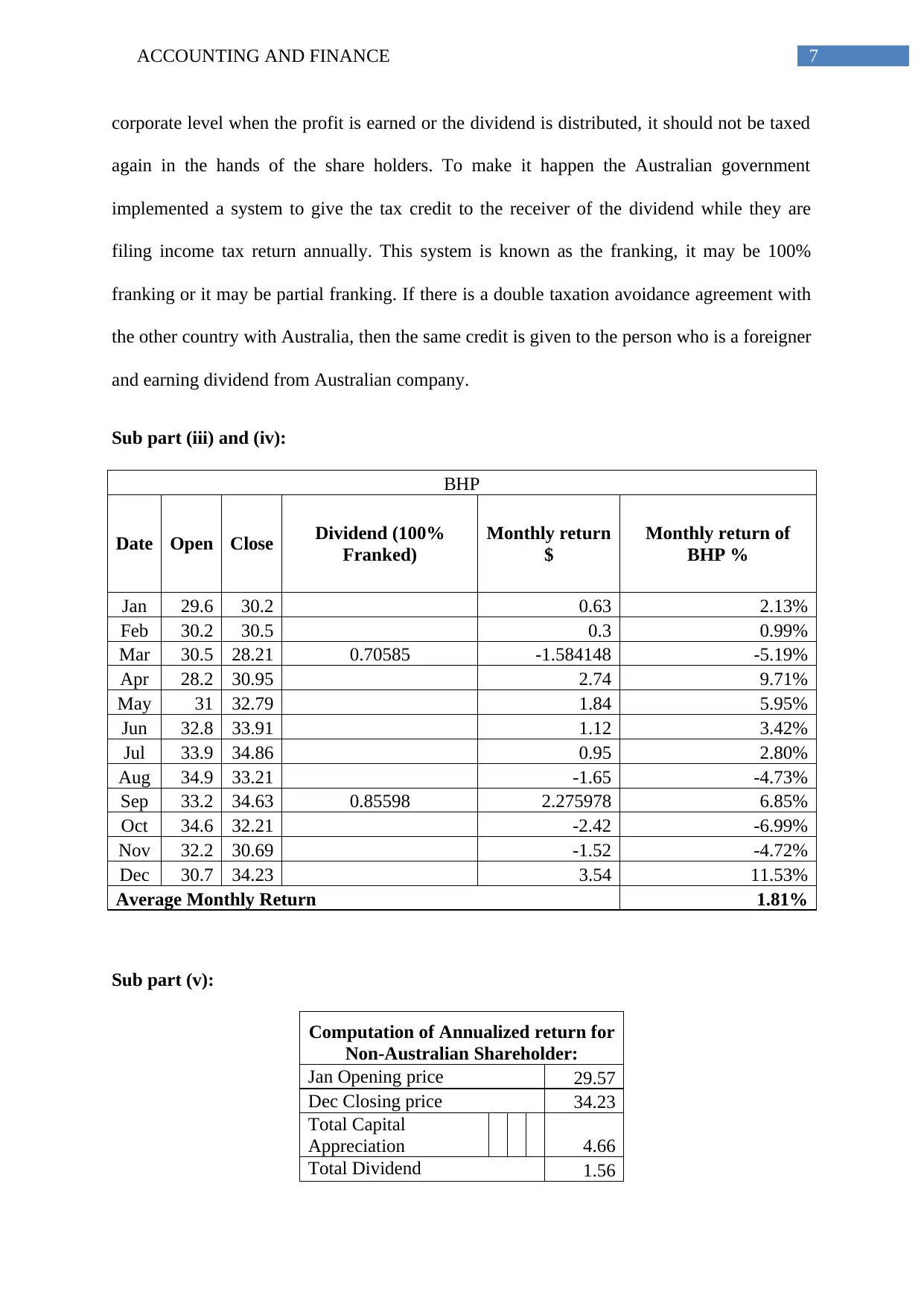

Sub part (iii) and (iv):

BHP

Date Open Close Dividend (100%

Franked)

Monthly return

$

Monthly return of

BHP %

Jan 29.6 30.2 0.63 2.13%

Feb 30.2 30.5 0.3 0.99%

Mar 30.5 28.21 0.70585 -1.584148 -5.19%

Apr 28.2 30.95 2.74 9.71%

May 31 32.79 1.84 5.95%

Jun 32.8 33.91 1.12 3.42%

Jul 33.9 34.86 0.95 2.80%

Aug 34.9 33.21 -1.65 -4.73%

Sep 33.2 34.63 0.85598 2.275978 6.85%

Oct 34.6 32.21 -2.42 -6.99%

Nov 32.2 30.69 -1.52 -4.72%

Dec 30.7 34.23 3.54 11.53%

Average Monthly Return 1.81%

Sub part (v):

Computation of Annualized return for

Non-Australian Shareholder:

Jan Opening price 29.57

Dec Closing price 34.23

Total Capital

Appreciation 4.66

Total Dividend 1.56

corporate level when the profit is earned or the dividend is distributed, it should not be taxed

again in the hands of the share holders. To make it happen the Australian government

implemented a system to give the tax credit to the receiver of the dividend while they are

filing income tax return annually. This system is known as the franking, it may be 100%

franking or it may be partial franking. If there is a double taxation avoidance agreement with

the other country with Australia, then the same credit is given to the person who is a foreigner

and earning dividend from Australian company.

Sub part (iii) and (iv):

BHP

Date Open Close Dividend (100%

Franked)

Monthly return

$

Monthly return of

BHP %

Jan 29.6 30.2 0.63 2.13%

Feb 30.2 30.5 0.3 0.99%

Mar 30.5 28.21 0.70585 -1.584148 -5.19%

Apr 28.2 30.95 2.74 9.71%

May 31 32.79 1.84 5.95%

Jun 32.8 33.91 1.12 3.42%

Jul 33.9 34.86 0.95 2.80%

Aug 34.9 33.21 -1.65 -4.73%

Sep 33.2 34.63 0.85598 2.275978 6.85%

Oct 34.6 32.21 -2.42 -6.99%

Nov 32.2 30.69 -1.52 -4.72%

Dec 30.7 34.23 3.54 11.53%

Average Monthly Return 1.81%

Sub part (v):

Computation of Annualized return for

Non-Australian Shareholder:

Jan Opening price 29.57

Dec Closing price 34.23

Total Capital

Appreciation 4.66

Total Dividend 1.56

8ACCOUNTING AND FINANCE

Total return 6.22

Annualized After tax

return 4.36

Annualized return in

percent 14.73%

Sub part (vi):

Computation of Annualized return for

Australian Shareholder:

Jan Opening price 29.57

Dec Closing price 34.23

Total Capital

Appreciation 4.66

Total Dividend 1.56

Total Annualized return 6.22

Annualized return in percent 21.04%

Sub part (vii), (viii) & (ix):

Market

Dat

e

Ope

n

Clos

e

Monthl

y

return

$

Monthly

return

of the

market

%

Jan 6147 6117 -29.2 -0.48%

Feb 6117 5869 -248.4 -4.06%

Mar 5869 6072 202.7 3.45%

Apr 6072 6124 51.9 0.85%

Ma

y 6124 6290 166.2 2.71%

Jun 6290 6366 76.5 1.22%

Jul 6366 6428 61.6 0.97%

Aug 6428 6326 -102.3 -1.59%

Sep 6326 5913 -412.2 -6.52%

Oct 5913 5749 -164 -2.77%

Nov 5749 5709 -39.9 -0.69%

Dec 5709 5783 73.9 1.29%

Average Monthly return -0.47%

Annual holding period

return -5.91%

Total return 6.22

Annualized After tax

return 4.36

Annualized return in

percent 14.73%

Sub part (vi):

Computation of Annualized return for

Australian Shareholder:

Jan Opening price 29.57

Dec Closing price 34.23

Total Capital

Appreciation 4.66

Total Dividend 1.56

Total Annualized return 6.22

Annualized return in percent 21.04%

Sub part (vii), (viii) & (ix):

Market

Dat

e

Ope

n

Clos

e

Monthl

y

return

$

Monthly

return

of the

market

%

Jan 6147 6117 -29.2 -0.48%

Feb 6117 5869 -248.4 -4.06%

Mar 5869 6072 202.7 3.45%

Apr 6072 6124 51.9 0.85%

Ma

y 6124 6290 166.2 2.71%

Jun 6290 6366 76.5 1.22%

Jul 6366 6428 61.6 0.97%

Aug 6428 6326 -102.3 -1.59%

Sep 6326 5913 -412.2 -6.52%

Oct 5913 5749 -164 -2.77%

Nov 5749 5709 -39.9 -0.69%

Dec 5709 5783 73.9 1.29%

Average Monthly return -0.47%

Annual holding period

return -5.91%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND FINANCE

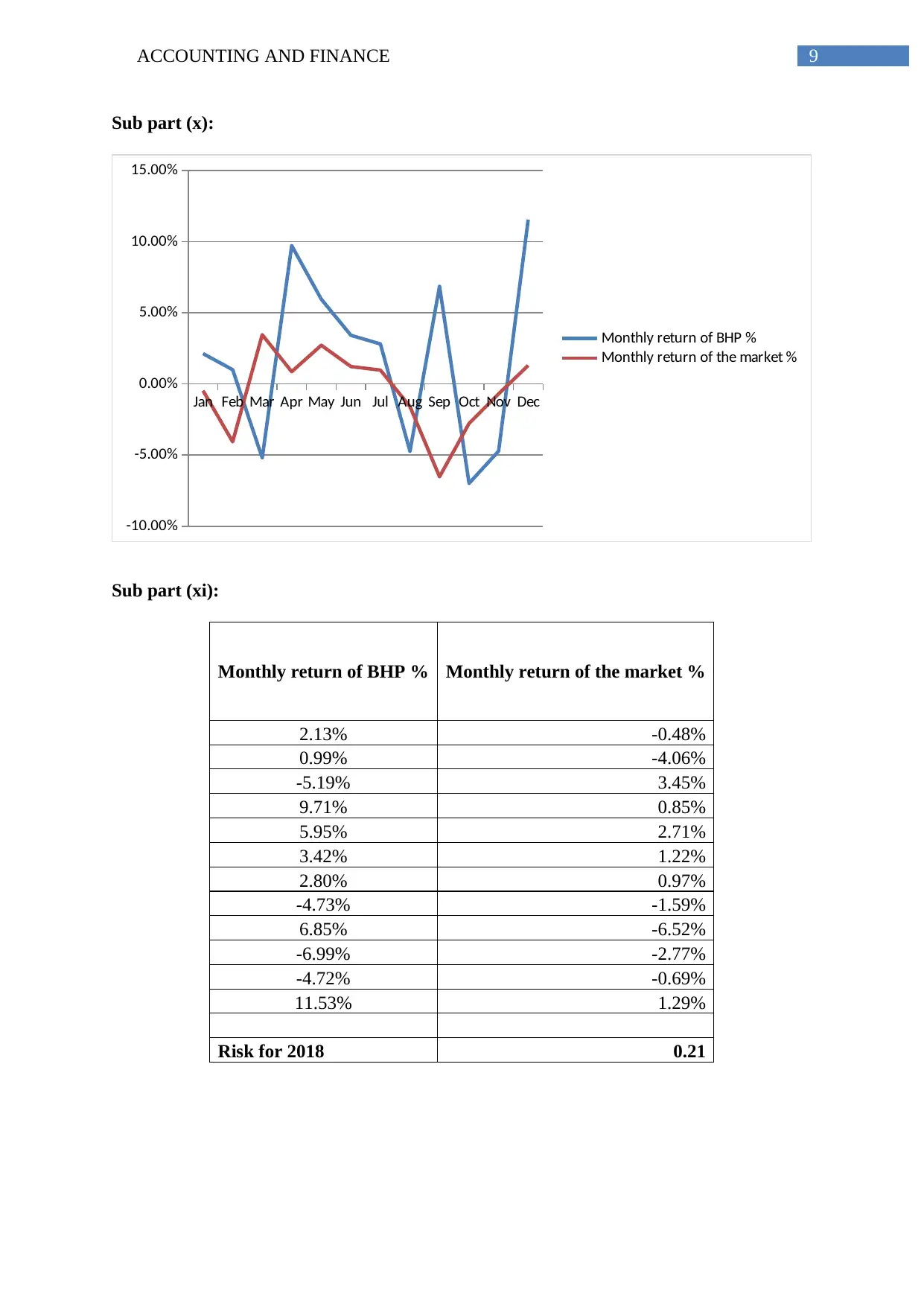

Sub part (x):

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Monthly return of BHP %

Monthly return of the market %

Sub part (xi):

Monthly return of BHP % Monthly return of the market %

2.13% -0.48%

0.99% -4.06%

-5.19% 3.45%

9.71% 0.85%

5.95% 2.71%

3.42% 1.22%

2.80% 0.97%

-4.73% -1.59%

6.85% -6.52%

-6.99% -2.77%

-4.72% -0.69%

11.53% 1.29%

Risk for 2018 0.21

Sub part (x):

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Monthly return of BHP %

Monthly return of the market %

Sub part (xi):

Monthly return of BHP % Monthly return of the market %

2.13% -0.48%

0.99% -4.06%

-5.19% 3.45%

9.71% 0.85%

5.95% 2.71%

3.42% 1.22%

2.80% 0.97%

-4.73% -1.59%

6.85% -6.52%

-6.99% -2.77%

-4.72% -0.69%

11.53% 1.29%

Risk for 2018 0.21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND FINANCE

Sub part (xii):

Bet 1.12 of BHP means the coefficient of the risk in investment in shares of BHP is

1.12. As it can be seen that the market risk coefficient in 0.21 and the risk coefficient of BHP

is 1.12 the investment in the stocks of that company is highly risky. On the other hand a high

risk can give a better future return.

Sub part (xiii):

Market rate or return 9.55%

Risk free rate 2.29%

Beta of BHP 1.12

Expected return of BHP 10.42%

Sub part (xiv):

0 2 4 6 8 10 12

0.00%

200.00%

400.00%

600.00%

800.00%

1000.00%

1200.00%

Expected Return

Linear (Expected Return)

Axis Title

Axis Title

Sub part (xii):

Bet 1.12 of BHP means the coefficient of the risk in investment in shares of BHP is

1.12. As it can be seen that the market risk coefficient in 0.21 and the risk coefficient of BHP

is 1.12 the investment in the stocks of that company is highly risky. On the other hand a high

risk can give a better future return.

Sub part (xiii):

Market rate or return 9.55%

Risk free rate 2.29%

Beta of BHP 1.12

Expected return of BHP 10.42%

Sub part (xiv):

0 2 4 6 8 10 12

0.00%

200.00%

400.00%

600.00%

800.00%

1000.00%

1200.00%

Expected Return

Linear (Expected Return)

Axis Title

Axis Title

11ACCOUNTING AND FINANCE

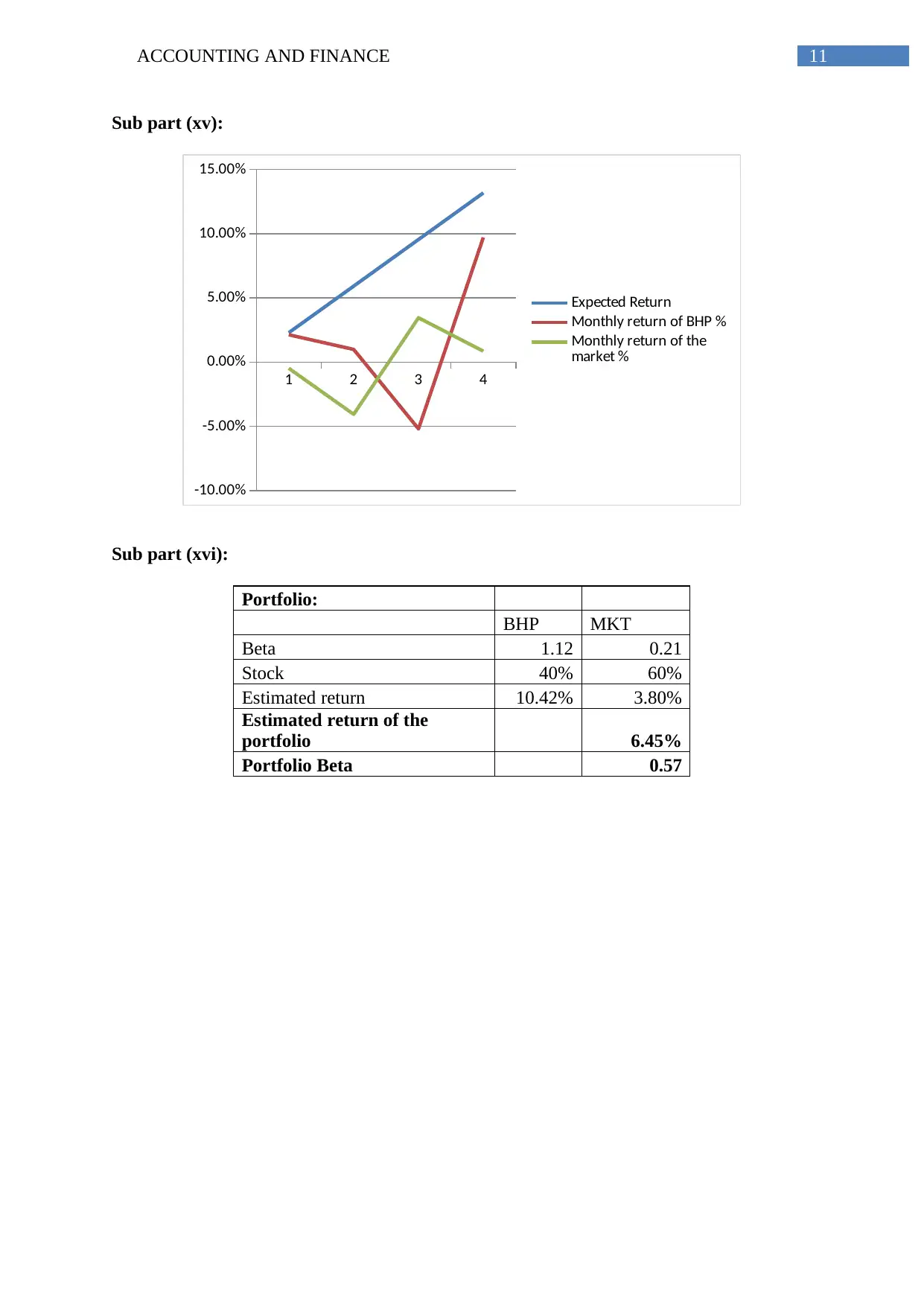

Sub part (xv):

1 2 3 4

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Expected Return

Monthly return of BHP %

Monthly return of the

market %

Sub part (xvi):

Portfolio:

BHP MKT

Beta 1.12 0.21

Stock 40% 60%

Estimated return 10.42% 3.80%

Estimated return of the

portfolio 6.45%

Portfolio Beta 0.57

Sub part (xv):

1 2 3 4

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

Expected Return

Monthly return of BHP %

Monthly return of the

market %

Sub part (xvi):

Portfolio:

BHP MKT

Beta 1.12 0.21

Stock 40% 60%

Estimated return 10.42% 3.80%

Estimated return of the

portfolio 6.45%

Portfolio Beta 0.57

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.